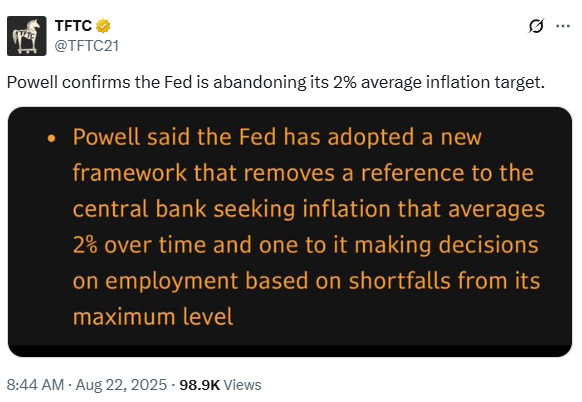

A Profoundly Dovish Shift

A fascination with criminals, embezzlers, gamblers, manipulators, thieves & crooks of all kinds.

So Nvidia - which I don’t believe I own, even indirectly - earnings came out tonight, and I think they were good (not that I believe numbers), but the stock was somehow down 3% in after-hours gambling trading.

I figured I should post what I have now, since the markets may not even open tomorrow unless the Fed does a 75 basis-point emergency cut (h/t Jeremy Siegel!)

I’d suggest filling your bathtubs up with water tonight, and making sure you have enough food, and ammo. Godspeed. Hopefully we will get through this.

“Comedy is the last refuge of the nonconformist mind.”

Gilbert Seldes, The New Republic, 20 Dec. 1954

Thomas Jefferson “believed that the sole function of government was to protect citizens in the enjoyment of their lawfully acquired rights and goods, and that when it had gone so far it should shut down. But today its field of operation has been immensely widened, and its principal aim, in nearly all the great countries of the world, is to maintain itself in power by transferring rights and goods from those who oppose it to those who support it. The object vended is always somebody else’s property. The consideration is votes.”

H.L. Mencken, On Politics: A Carnival of Buncombe

Powell Always Chickens Out

“Inflation has been above our target for more than four years and remains a prominent concern for households and businesses…Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance….The past five years have been a painful reminder of the hardship that high inflation imposes, especially on those least able to meet the higher costs of necessities.”

Quite a remarkable statement from Jay Powell at Jackson Hole.

To summarize:

Yes, we know we've abysmally failed our inflation mandate, and you're very worried about the cost of living.

We don't care.

To repeat, we are aware that inflation hurts almost all of you...but we still don't care.

“We’ve reverted to 2% inflation as a long-term aspirational goal rather than a definitive target to be achieved in this cycle. This is a *profoundly* dovish shift by Powell, and if you don’t understand that you will continue to get ripped by this market.”

“The Fed is actually a political entity”

“I have written repeatedly that the Fed is actually a political entity. They claimed to be politically independent, but the reason they did it [cut in 2024] was because it was seven weeks before the presidential elections, and we all knew that there was no love lost between Powell and Trump at the end of the Trump first term. So clearly he was not going to be re-nominated if Trump got reelected last November, but his chances were significantly better if Kamala Harris came to office. So I think it was a move which was done close to the elections. There was no indication that the economy urgently needed a 50 basis point cut, but he did it. I think there was a significant amount of political motivation, in addition to a wrong calculation about inflation. They were all related factors. I don't think the economy needs any cut at all at this time. And the reason for that is that inflation is edging up.”

As Joseph Wang pointed out last year: “Basically, every single person who donates who works at the Fed donates to Democratic Party."

And - love or loathe Trump - never forget Goldman’s Bill Dudley in 2019:

“There’s even an argument that the election itself falls within the Fed’s purview. After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020.”

“Monetary policy is too restrictive.” Discuss.

Even using the nonsense CPI model, we've been well above the Fed's made-up "2% target" YOY for 52 months in a row.

That would suggest that we should already be worried about inflation.

Most people already are, just not those invited on Bloomberg or CNBC

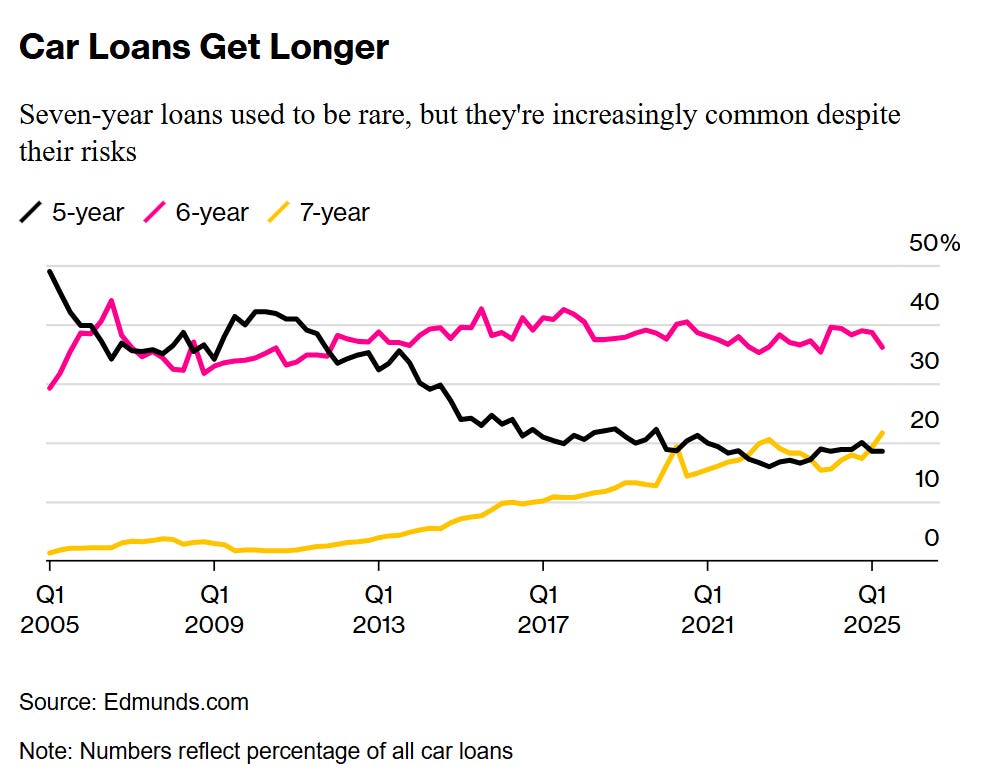

Cars Are So Expensive That Buyers Need Seven-Year Loans

“Once rare, seven-year car loans are fast becoming the norm. They’re often the only way buyers can afford new rides, with average sale prices surging 28% in five years to approach $50,000. Compared to a five-year loan, they can make the difference between a $1,000 monthly payment and a $780 one. In the second quarter of 2025, seven-year loans represented 21.6% of all new-vehicle financing, according to Edmunds.com. Six-year loans, at one time considered the upper end of the range, are now the most common, accounting for 36.1% of loans in the second quarter…

The average interest paid on an 84-month loan is $15,460, said Ivan Drury, director of insights at Edmunds.com. That’s $4,600 more than the average on a five-year loan, which used to be standard.”

"I now realized there was an entire industry, called consumer finance, that basically existed to rip people off.”

- Steve Eisman in The Big Short

Tractor Supply must be one of those A.I. companies.

Mike Green

Loved this question from the host:

“Are you forecasting an actual Armageddon type of event? Or is there not the idea that, well, because everyone's doing it, effectively S&P US equity markets have become too big to fail.

This is basically baby boomer retirement accounts. Uh, the government can't let this fail. They're surely they would bail out any situation that that goes in an Armageddon type scenario. And so at worst you're looking at like very poor returns. You're not looking at actual collapse to, you know ,great depression types of events are you?”

Such faith in the government’s ability to always (nominally) save the day! Yellen has suggested that the Fed buy stocks, and Michael Howell claims the New York Fed was buying futures during the 1987 crash, so nothing would surprise me.

I do wonder how many of those in a huff over Trump’s 10% Intel stake would stand against the government or the Fed buying trillions of stocks in the next 50% downturn?

And by the way, lower stock prices are great for young people.

Mike:

“More than anything else, what I'm trying to do is raise awareness ahead of what I think is a likely event that will precipitate the actions that you're describing so that we can build a better system on the other side of it, instead of doing what we have largely done since 2000, which is throw our hands up at every event saying who could possibly have predicted this, right? And therefore we just try to kick the can down the road.”

Host:

“So you're basically you're effectively saying that this massive dominance of passive investing is going to end badly?”

So I saw Tom Lee (again) on Tuesday talking about how early it is to invest in A.I., and it reminded me a bit of the DotCom era, which reminded me of Global Crossing, which went bankrupt in 2002.

I’d saved this from SiliconInvestor back in the day:

TEN Reasons to Buy GBLX Now: (revised 10/16/99)

Hope this brightens your weekend. Still as valid as when I first published it a month ago, when GBLX was at $23. Updated for your enjoyment......

1. Frontier merger. This acquisition is immediately additive to earnings. It serves to link Global Crossing's undersea cables with Frontier's extensive network of terrestrial cabling across the United States. Also, Frontier brings services to the Global table. Global Crossing is not satisfied with operating the toll booth on the information super highway; they want to repair the road and service vehicles moving along on it. Frontier enables Global to do all that.

2. Microsoft and Softbank backing. These two giants (in market cap alone) will ensure success for Global Crossing. If you look at the structuring of their arrangement, you realize they are forced to pony up more and more money as the market cap of Global grows. The effect will be a logarithmic increase in GBLX share price for the next three years.

3. "Lock" on insider sales for six months past merger. Both Frontier and Global executives have pledged to keep 100 % of their shares for at least six months after the merger closes. In the recent Switzerland Conference, Winnick said "I'm not going anywhere and neither is my money. You ought to have great confidence that every thing I do is tied to investor return."

4. Insider ownership. Winnick (AKA - "The Rainmaker") owns 25% of Global Crossing. What is good for him as a shareholder is good for you. Enough said.

5. Fidelity Asset Management (FMR) ownership. FMR recently announced they have established a 5% stake in GBLX. They bought GBLX stock from $22-$28 a share. Did you?

6. $500 million stock buy back. Global has pledged to buy back at least half a billion...that's with a "B", folks...of it's own stock after the merger. What better way to emphasize the bright future the board of directors sees for this company.

7. "First There" advantage. By being the first company to be a true global telecommunications enabler, Global Crossing has a distinct advantage shared by many extremely successful companies. Everyone else has to catch up and (take it from me) that's a harder and harder thing to do in an industry where barriers to entry are a mile high and getting higher every day that interest rates go up.

8. Visionary leadership. Look at who is at the top of the Global pyramid. If you don't know them, you better learn who they are. They are the future faces of telecommunications in the world. Winnick recently said "They will be writing books about what we have done in this industry."

9. Lowest cost structure, most efficient business model, and technology only makes it cheaper. Global Crossing, when the network is complete, will have the lowest cost structure in the industry. It is THE most efficient business model I have ever seen. No longer do customers have to pay tolls for bandwidth as they transition across carrier networks...it's like Club Med for bandwidth (you pay only once for everything). As WDM technology gets better, Global's cost of providing bandwidth shrink exponentially, and they make money at an exponential rate.

10. Cause you want to have $1,000,000! This company will make at least $1.00 in earnings next year and $3.00 in 2001. What will the P/E be then? Still over 100 and you will be in Nassau or Hawaii, happily cashing your monthly money market dividends and wondering what color the sunset will be as you toast your good fortune.

Buy now or kick yourself for the rest of your life.

Nvidia

via Grant’s:

More than 20 funds are tied to Nvidia alone, including ones seeking to generate two times the daily move in either direction, as well as those selling covered call options and employing other income-generating strategies. “There’s only one Nvidia,” Will Rhind, founder and CEO at GraniteShares, which offers a quartet of funds focused on the chipmaker, told Morningstar last fall. “It’s the highest-conviction trade in the world.”

In late 1999, in under 6 months, the Nasdaq composite went up over 80%.

Schrödinger’s Durable Goods Orders

“Durable goods orders excluding defense in the United States fell by 2.5% month-over-month in July 2025, following a revised 9.5% plunge in June and compared to market estimates of a 3.6% decline.”

“Durable Goods Orders Ex Transportation in the United States increased to 1.10 percent in July from 0.20 percent in June of 2025.”

Do I want to invest in Germany, who closed all their nuke plants, or the UK, where they’re arresting people for saying “We like bacon”? No.

But then again, I’m generally aberrant, and the ratio below is a little out of whack:

“I think we are at the cusp of first slowly and then a sudden rebalancing of financial markets and capital allocation away in particular from the US, which is heavily overrated, but more generally from developed economies towards emerging economies where most growth potential, most human capital, most productively enhancing investments lie.”

“As long as China controls rare earths, China de facto controls what the U.S. can make in its industrial and military-industrial supply chains. It may sound odd, but it's true. So until then, there's going to have to be some kind of quid pro quo, and that is China suffers a high tariff, but not an absolute nosebleed tariff. It's enough to disincentivize trade with China, but not completely kill it.”

I'm gonna suggest that it's the red area here that was the real problem, but I have no econ PhD so I don't know what the wrong answer is.

Michael Kao on a “Reverse Marshall Plan”

“You've got a structural dynamic from China where they are exporting what is essentially hostile industrial policy that will hollow out any competitor that's that's pursuing a free market path. Because it's cheaper to just buy Chinese goods. Let's forget about manufacturing anything here. Let's just buy everything from China. Well, the problem is that China is our biggest geopolitical adversary. So that's how we got into this mess. Now we have to unwind it, and it it's a fraught path, but so far I like what I see.”

“I think it was Macron who was saying, "Well, you know, we obviously need to turn to China more." And I put out a lot of tweets back in April and May saying that would exactly be akin to inviting the fox right into the hen house.”

“For the EU to say that the solution is to align more closely with China, well, be my guest, because then you you will see your entire industrial sector get hollowed out.”

“It never made sense to me why we would necessarily have tariffs on what I call t-shirts and tchotchkes, because look, we don't care. We want to be able to have cheap Chinese goods in areas that are not vital to national security, but in critical path industries like chips, ship building, pharmaceuticals, defense, energy, right? These areas I think need to be targeted.”

Via Grant’s: Comedy is tragedy plus time.

“CME Group, the country’s largest futures exchange, announced a “groundbreaking alliance” with sports betting firm FanDuel designed to “expand access to financial markets for millions of FanDuel customers in the United States.” Along with analog assets such as the S&P 500 and gold, users will be able to wager on cryptocurrencies as well as economic indicators such as GDP and CPI beginning later this year, with additional product offerings to be introduced in coming months.

“Individual investors are increasingly sophisticated and [are] continually pursuing new financial opportunities,” commented CME chairman and CEO Terry Duffy. “To meet this demand, we have created this innovative partnership, which will operate a non-clearing futures commission merchant. Together, our event-based products will appeal to the growing public interest in markets, and we will provide education to attract a new generation of potential traders not active in derivatives today.”

I’m reminded of this passage, from Richard Evans in The Coming of the Third Reich:

"It was not least as a consequence of the inflation that Weimar culture developed its fascination with criminals, embezzlers, gamblers, manipulators, thieves & crooks of all kinds. Life seemed to be a game of chance, survival a matter of the arbitrary impact of incomprehensible economic forces.”

Sorry kids!

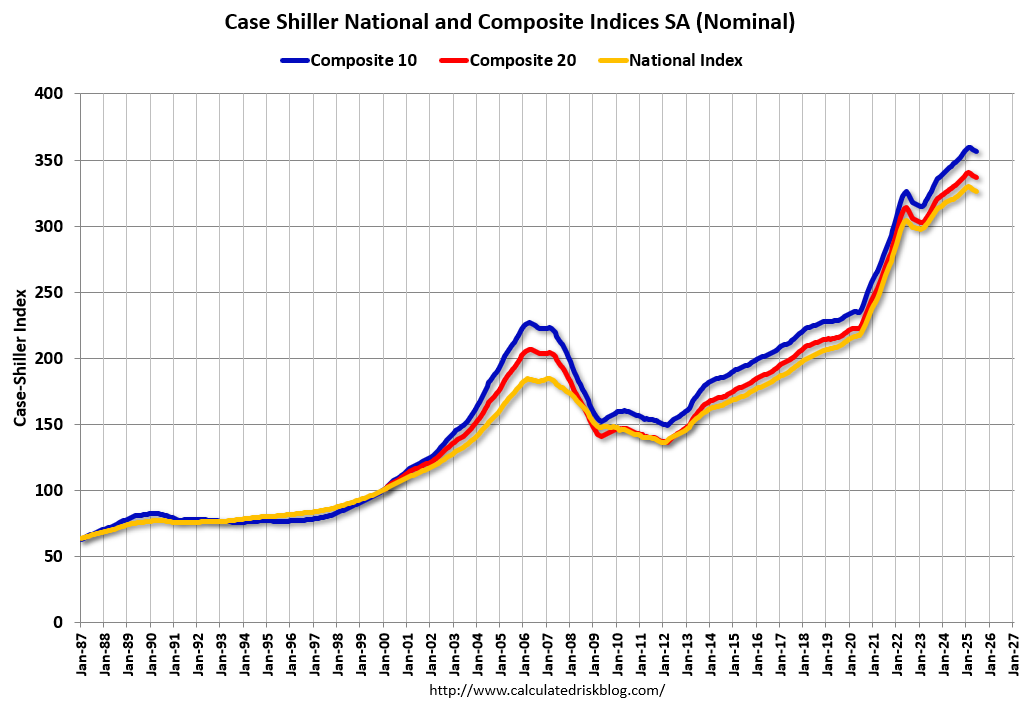

"Despite the recent downturn, home prices are still up 2.6% compared to a year ago."

Sorry Kids!

Case-Shiller: National House Price Index Up 1.9% year-over-year in June

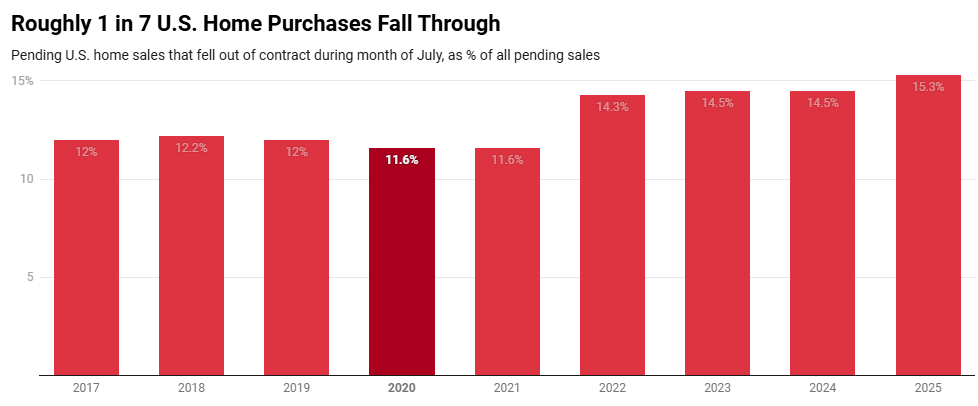

Roughly 1 in 7 U.S. Home Purchases Fall Through

“Roughly 58,000 U.S. home-purchase agreements were canceled in July, equal to 15.3% of homes that went under contract last month. That’s up from 14.5% a year earlier and marks the highest July rate in records dating back to 2017.”

Less data than I’d like to see for something like housing, but interesting.

Ivy Zelman

“Assuming they're going to buy the median priced home, and it's the median income for a single household,, that person would have to spend 60% of their income today for a non-supervisory employee to not only make a mortgage payment, which includes their interest payment, but also homeowners insurance and property taxes. And back since the early 70s and really the only time we saw it higher than 60% was back in 1982, when we had mortgage rates north of 16%.”

It’s the prices this time, more than the rates, that are insane.

Also interesting: “70% of the student loans that are delinquent are from people that have not finished their higher education.”

Melody Wright

Home Prices Will Be Heading Lower For Years

“What's so kind of upsetting about this inventory shortage narrative is I have driven all over this country and I can tell you there are vacant homes everywhere.”

In my own area I see the same thing.

Adam: “Ivy basically said she thinks more or less the worst is in for the housing market. She said we're going to be kind of grinding along the bottom here for a while and yes, she expects prices to be down nationally in 2025, but she does expect things to be healing and and really things to get better as 2026 goes along. I get the sense from you that you feel like no, we are still in the early stage of a multi-year housing correction, and looking at at least through the end of 2026, you just think it's just basically going to get worse. Correct?”

Melody: “Absolutely.”

"You may have heard the phrase ‘the plural of anecdote is not data.’ It turns out that this is a misquote. The original aphorism, by the political scientist Ray Wolfinger, was just the opposite: The plural of anecdote is data."

Tales from the Reddit

“Chase closed my account due to their “flags””

“Woke up today to find out Chase is closing all my accounts with them. I went to the branch, and they told me there’s nothing that can be done—it’s final.”

In the replies, I found this information interesting:

…I work in anti-money laundering compliance, including at JPMorgan some years ago. There are a lot of factors that go into making a risk closure decision, but at some point the bank decided that the risk of keeping you on as a customer was greater than the value of having your money banked with them.

I should also note, that as a general rule, banks don’t close relationships flippantly. You have to remember, you being a customer is revenue, they like revenue.

For example, I once saw a customer who had not one, not two, but 8 separate suspicious activity reports filed for transactional activity not commensurate with the known profile of the customer. This spanned over 3 years of the same activity.

As a general rule, analysts are instructed to escalate for relationship closure at 3.

The bank decided to keep them on each time because the risk profile hadn’t reached a point where the risk outweighed the profit.

So I have to ask—what did you do?

Do you transact heavily in cash? Do you often send wires to international counterparties with no known affiliation? Do you have a wildly disproportionate amount of P2P (Zelle, Venmo, etc) activity with no transaction memos entering and exiting your accounts? Do you own a business? What industry is it in?

Something happened in your accounts, often enough, to trigger several levels of automated heuristics, before it got escalated to analysts to investigate manually and then escalated again before being reported to FinCEN multiple times before finally being sent for a relationship closure recommendation (of which maybe 1/5 get approved).

This stuff doesn’t happen over night or frivolously.

Edit: So it sounds like OP updated for more context. He has repeat wire activity back to his home country of Nigeria, which is on a list of what is known as “High Risk Jurisdictions”. This list is designated and maintained not by Chase, but by an international body known as FATF, typically in tandem with OFAC here in the United States. Countries make it onto this list for a number of reasons, but the most common one being lax banking regulations.

The amounts that you sent, were likely too high for what your stated employment or income profile at Chase could reasonably support. Are you a US citizen? Do you have Nigerian citizenship? If so, they would have no way to know you have any ties back to Nigeria unless you had provided that information to them during onboarding. You can update your client information at a banking center for this reason. It’s critically important to keep your financial institution appraised of things like, change in jobs and income brackets, because the decisions they make are based entirely on what YOU tell them, or in this case don’t tell them.

Sorry this happened to you.

“Parents in over 100k debt. I’m scared”

“23F Recently discovered how bad my parents situation is and it’s weighing on me. They have borrowed over 100k in the past 2 years (Sofi, 401k, cash out refinancing on the house, Rocket mortgage). They have a monthly income of about 8k with 2.2k mortgage and 2.6k personal loan repayments, spend about 4k month on other bills (credit card minimums, utilities, groceries, etc.). They do not have a car payment or monthly subscriptions. They are 53 and 52. My dad was 400k in his 401k im not sure about my mom. Any advice is appreciated. Are they going bankrupt?

…Updated edits: 9k cash out refinance on house (July 2025), 20k of moms 401k (Jan 2025), 90k Sofi loans (2023), 17k personal loan (2022), took 50k of cash out refinance on the house in 2022 (to pay off 50k private Sallie Mae student loan. I have to pay the remaining 50k left, yes I know a priv loan is dumb! but I didn’t know at the age of 18 what I was getting into and obviously my parents don’t either). The only thing used for my schooling was the 50k cash out refinance to pay off some of the Sallie. I believe that has added a few hundred to our mortgage every month. Do you think this was the reason we started getting personal loans (on top of the credit cards too), was it was just all too much? I feel guilty yet grateful it’s so complex. I stress for them and know it’s not my responsibility. They are in a debt cycle. I have worked my ass off in college and I have a full ride for my masters program that I am currently in and pay for my own rent, groceries, etc. I will be graduating in May 2026 and tacking my 50k of Sallie Mae which was used for housing, tuition and basic needs for in state undergrad. I don’t necessary want to give them money (as it will take me at least 1 or 2 years to pay off my Sallie Mae) but I just want to be secure enough to take care of them when they hit retirement and need housing/food/care etc.”

Clearly this family is still better off than many, but it’s a bit tragic, and I wonder how many others are in similar situations, or worse. And I don’t mean Barry Sternlicht.

“Car Debt. Haven’t paid my car in 4 years.”

“I haven’t paid my car loan in over 4 years. Covid happened, I lost my best friend. I lost my job, was down bad, got addicted to drugs. Paying that bill was the last thing on my mind. Fast forward, I am sober, trying to rebuild my life. Got a steady job. Car is parked. I uber to work. They never repoed it. It is written as a charge-off on my credit report. Statute of Limitations is 3 years. I don’t drive it as it is not registered or insured. What can I do?”

From the comments:

“Lenders cannot report as stolen unless it was obtained fraudulently. Retired fraud investigator for a car finance company.

Charge off does not stop the car finance company from having on a repo list. Here are your choices:

Contact finance company & pay. They might be willing to set up a schedule.

Contact finance company & voluntary repo. They will sell at auction & you will be responsible for deficiency balance. They will setup payments for this.

Take your chances that it doesn’t get repo’d. However, if you register it, they will be notified.”

“Bleeding $1,700/month on Two Rental Properties. Did I Mess This Up?”

I bought two houses in Texas . one about 2.5 years ago, and the second one about a year ago. For the past year or so, I’ve been losing around $1,700/month combined on these properties.

The first house is older and needed a lot of work. The second one is brand new, in what I thought was a promising, up-and-coming area. My “strategy” (if you can even call it that) has mostly been betting on future appreciation. I figured with all the growth in Texas, it would eventually pay off.

I initially tried Airbnb, but the hassle was unbearable — too much management, too many headaches. So I switched to long-term tenants, thinking it would be more stable, but it still feels like a weight on my chest. I dread getting texts from tenants. Like, even a simple maintenance request just ruins my day. I know that might sound dramatic, but real estate just hasn’t been a good emotional fit for me.

The problem is I want to be location-independent. I want to travel. I don’t want to be responsible for $4,000 in mortgage payments if someone moves out unexpectedly. I’m realizing now that I probably didn’t take a very calculated risk with these properties. I wanted to build wealth, but I think I underestimated how much stress this would bring me.

So now I’m thinking… should I just sell both houses? Maybe take the hit, get whatever money I can, and treat this as a very expensive lesson in what not to do with real estate?

Am I being delusional thinking these properties will appreciate enough to make this all worth it? I’d genuinely appreciate any honest thoughts or advice. Thanks.

"The thing I have noticed is when the anecdotes and the data disagree, the anecdotes are usually right. There's something wrong with the way you are measuring it."

Grant Williams and Vic Sperandeo

“The debt to GDP ratio keeps rising, but they don’t care. There’s no constituency to make a change. So let me just say this. The endgame, 100% convinced, is hyperinflation.” - VS

“I think if the average person in the street understood the way the monetary system really works, there’d be mass crowds of people storming the Marriner Eccles building tomorrow.”

“The thing that I struggle to understand, how it manages to continue as the fear rises, is that this idea that we get where we’re going, but we can still make money in the meantime, and we can still make money by selling vol, and we can still make money by owning stocks, because we’ll get the chance to get out and the Fed will step in. This belief that what has worked so well in the past will always continue to work - it just blows my mind, because we’ve got a lot of sophisticated investors here who seem to have thrown the towel in and said, “You know what? To hell with it. I know this is a dumb thing to do, and I know at some point I’m going to get caught with my pants down here, but if I’m not playing like everybody else is playing, if I’m not buying the mag seven, if I’m not selling vol, I’m basically leaving money on the table.”

Grant Williams

Jean-Claude Juncker:

"We all know what to do, but we don’t know how to get re-elected once we have done it."

“When it becomes serious, you have to lie.”

“Same guy, those two quotes, that’s all you need to know. That’s all you need to know.” - Grant Williams

Speaking of Juncker, here’s another gem from Juncker on the introduction of the Euro:

"We decide on something, leave it lying around and wait and see what happens. If no one kicks up a fuss, because most people don't understand what has been decided, we continue step by step until there is no turning back."

Google Searches for “Sell Blood”

Billionaire philanthropists’ bankrolling the news (2020)

“Last August, NPR profiled a Harvard-led experiment to help low-income families find housing in wealthier neighborhoods, giving their children access to better schools and an opportunity to “break the cycle of poverty.” According to researchers cited in the article, these children could see $183,000 greater earnings over their lifetimes—a striking forecast for a housing program still in its experimental stage.

If you squint as you read the story, you’ll notice that every quoted expert is connected to the Bill & Melinda Gates Foundation, which helps fund the project. And if you’re really paying attention, you’ll also see the editor’s note at the end of the story, which reveals that NPR itself receives funding from Gates.

NPR’s funding from Gates “was not a factor in why or how we did the story,” reporter Pam Fessler says, adding that her reporting went beyond the voices quoted in her article. The story, nevertheless, is one of hundreds NPR has reported about the Gates Foundation or the work it funds, including myriad favorable pieces written from the perspective of Gates or its grantees.”

"If you're gonna get involved in questionable activities, make sure you're a philanthropist, because a lot of people will forgive you."

Columbus reporter Robert Fitrakis

“A joke's a very serious thing.”

“It is so important to understand that one of the primary means of immobilizing the American people politically today is to hold them in a state of confusion in which anything can be believed but nothing can be known, nothing of significance that is.

And the American people are more than willing to be held in this state because to know the truth - as opposed to only believe the truth - is to face an awful terror and to be no longer able to evade responsibility. It is precisely in moving from belief to knowledge that the citizen moves from irresponsibility to responsibility, from helplessness and hopelessness to action, with the ultimate aim of being empowered and confident in one's rational powers.”

Unpublished letter, E. Martin Schatz to Vincent J. Salandria, May 14, 1992

Thank you as always. All folks have to do is take a little look around to see what is really happening in housing but so many just don't have the time.

Fantastic work as always! That private equity meme had me rolling on the floor. That whole industry is such a farce. A compensation scheme masquerading as an asset class.