A Strange Asymmetry

More thinking, less talking

“I'm bad for business because I cause people to think.”

Very common nowadays to hear that inflation is “good for stocks.”

Stephanie Link even blocked me the other day because I dared challenge her on this.

Oh well, her loss.

Anyway, a reminder from this 1979 article, “The Death of Equities”:

“The one rule whose demise did the stock market in could be summed up thus: By buying stocks, investors could beat inflation. Stocks were a reasonable hedge when inflation was low. But they proved helpless against the awesome inflation of the past decade. “People no longer think of stocks as an inflation hedge, and based on experience, that’s a reasonable conclusion for them to have reached,” says Richard Cohn, an associate professor of finance at the University of Illinois. Indeed, since 1968, according to a study by Salomon of Salomon Bros., stocks have appreciated by a disappointing compound annual rate of 3.1%, while the consumer price index has surged by 6.5%. By contrast, gold grew by an incredible 19.4%, diamonds by 11.8%, and single-family housing by 9.6%…

There are at least four good reasons why inflation is killing equities:

• Stock prices reflect anticipated corporate profits. During periods of rapid inflation, however, profits fall because most businesses cannot raise prices quickly enough to keep up with costs.

• Even gains in profits are largely illusory because inflation makes them look rosier than they actually are. And because plant and equipment are depreciated at historic cost rather than replacement price, money that should go into capital investing and inventory purchasing instead goes to the government in taxes.

• Experience has taught investors that inflation will lead to an economic downturn that will wreck corporate profitability and stock prices. This happened in 1974, when the worst recession since the Depression followed the last burst of double-digit inflation.

• Investors jump from stocks to bonds to nail down high rates. Inflation also prompts corporations to sell debt because it is tax-deductible and can be paid off in cheaper dollars—thereby reducing the flow of new stocks to market.”

“I think about gold much differently than most people. I think there's a lot of people who own gold as a way to get rich. I own gold for insurance. I honestly don't even really care whether it goes up or down, I'm going to own it regardless of whether it does or not.”

Congressman: “We’re compromised.”

Nick Bryant: “We want to know why the government has covered up this child trafficking, and we want the perpetrators to be prosecuted, and you wrote this letter and I really resonated with it. Why do you think nothing has been done by the government with regards to that?

Rep. Tim Burchett: “Because we're compromised, pure and simple. You've got some of these dirtbags and and elected officials that have taken part in some of this awful behavior, and it's the honeypot, you know? They get them, and then you always wonder why good conservatives vote for horrible legislation occasionally, or or good liberals vote for something conservative. I think it's because they've been caught in some situation like that, and somebody's whispered in their ear - you know, man, we don't need this stuff out, you need to help - if you can help us on this bill, I can make that go away, but it never goes away. It's a temporary fix, because they're just going to keep hanging over them for the rest of their lives. They've done business with the devil, and now they're gonna face the consequences.”

“You want it to be one way, but it’s the other way.”

Jim Grant: "Apropos of demographics, what happened to the American population between 1880 and 1900?"

Evan Lorenz: "It went up about 50%"

Jim Grant: "Over the same period, what happened to consumer prices?"

Evan Lorenz: "They went down about 14%."

Tell me again how restrictive Fed policy is.

This is on ongoing pet peeve and serious problem - our financial media - particularly the small group allowed to question FOMC members - is full of shills, cheerleaders and publicists!

“After lunch, at Michelle’s request, I took calls from reporters. If we were going to hold our own in the court of public opinion, we needed to get our side of the story out. Generally, I spent the most time with the beat reporters who wrote regularly about the Fed, including Jon Hilsenrath of the Wall Street Journal, Greg Ip of the Economist, Krishna Guha of the Financial Times, Neil Irwin of the Washington Post, John Berry of Bloomberg, Steve Liesman of CNBC, and Ed Andrews of the New York Times. I knew that these more specialized reporters were best equipped to understand and then explain what we were doing and why. Other media would pick up on their reporting.”

- Ben Bernanke, The Courage To Act In My Own Best Interest

The gaslighting is offensive. This was today:

"They’ll be covering what Powell and the other influential Central Bankers basically tell them to cover, so the story is told by the storytellers, and the storytellers are the central bankers, and that's the problem. It's all basically propaganda."

Here’s Jeanna Smialek’s latest book:

"...telling the stories of the women and men who kept pushing the limits of what economic policy could accomplish." - from a Jason Furman blurb

Good grief - like all of them, she’s a publicist, not a reporter!

Below the fold: Thomas Hoenig, Kevin Warsh, Murray Stahl, Greg Weldon, Neely Tamminga, Melody Wright, High Yield, CRE, Private Credit, 25-Sigma Events, O.J., the Inflation, Mike Green, Insiders, Mike Meixler, The Wire, Wargames, Led Zeppelin, and much more!

“When you monetize debt, directly or indirectly, it eventually affects something in the economy in an inflationary manner, and I think we've seen the effects of that. It's redistributed wealth in this country. It's created social unrest in this country, and I think those are a high price to pay for what I call excessive accommodation beyond the immediate crisis need.”

Kevin Warsh

“It is the Fed that wandered into politics on a permanent basis.”

“When they [the Federal Reserve] kept interest rates near zero for a decade, and did quantitative easing, where the Central Bank is buying the bonds of the Treasury Department in crises, and they decided to make that more or less a permanent feature - it is the Fed that wandered into politics on a permanent basis. In a period of free money, what was the clear sign to Congress? You can spend all the money you want, and so they did1. You don't have to do much to get a bunch of members of the Congress to want to spend money, and they said come at it, because it's free, and it'll be free forever.

Remember ‘secular stagnation’ and zero rates and zero lower bound? They encouraged this spending boom over the course of the last few years Congress at a time of relatively full employment added $5 trillion doll in deficits cumulatively, and have put the country in a much more dangerous place. This level of debt is dangerous for our economy, and it's a terrible sign to the world, because we're all talking about economics. Bad economic policy provokes our adversaries to take us on, so that makes the country less prosperous and less peaceful.”

“…while economic experts generally consider the U.S. Fed as politically independent, consumers do not necessarily share this view.”

Warsh continues:

“What I would do first is stop talking so much. We have 19 people around that table, and they're all coming on to your show and others and they're giving you their forecast for rates, and their dots, and all the rest, and they're all herding around the same numbers. More thinking, less talking.”

“If Washington writ large were trying to design a set of policies that were good for asset holders, made the stock market go up every day, we're bad for folks that are living on their W2 income that don't own assets, that just have income. You're taking risks with their paychecks every day. So what this Administration has done over the course of the last several years, especially the last year, is to goose the stock market. That's what this mix of big, irresponsible fiscal policy does…if the focus from the Central Bank were on the real economy, the financial markets will take care of itself.”

“The power of the Federal Reserve comes from its credibility. Its credibility comes from making the right calls, making the right decisions. The central bank's done a lot more harm to itself over the last several years making the wrong calls, leading to inflation, which is deeply harmful for 52% of our fellow Americans who don't own any assets. That is more important to the Fed's credibility than whether these politicians are screaming at you.”

“If you ensure stable prices - something that hasn't been accomplished for a long time - the central bank will do much of its job, and then we can have strong employment, we can have strong, robust economic growth. When you don't have stable prices, you're not going to to hit any of these objectives.”

“I would grade the economy as having been goosed by17 trillion dollars of stock market wealth that came about starting last December, when the central bank said we've got lots of cuts coming, so with all of that massive liquidity, it is hard to judge how strong or weak the economy is because liquidity is everywhere.”

“The Federal Reserve very recently cut interest rates by 50 basis points. The strange thing is when inflation was at 7%, 8% and 9%, and they wanted to start to quash inflation, what did they do then? They waited nine more months and they raised rates by a quarter, so there's a strange asymmetry in how they act.”

Murray Stahl

“In my opinion it’s just starting, okay? The inflationary trend…it can last decades.”

“The trouble is, the data-center requirement is now, and it takes too long to build nuclear power, if it's even permissible. Then we have the intermittent sources - solar and wind, but data centers are constant. We can't rely on solar and wind, so the vehicle of choice is of course natural gas. That's going to happen. You need reliability, you need the supply predictability, and it's inexpensive as well. Wind and solar is basically the opposite of what I just said.”

“I recently read an article in the Wall Street Journal which described in a survey the extent that the large majority of people still cherish the American dream: a home, a job, a family, and a decent retirement, and what the article also pointed out is more of them feel that that is beyond their grasp today, and the data unfortunately tends to support that.”

While Hoenig is about as heterodox a Fed insider as there is (even as he says, quote, "I love the Fed"), he admits "the effect [of QE] in a sense was to redistribute wealth even further than it was."

But he still “loves” the Fed. Thanks, Tom. Cognitive dissonance.

Interesting graphic from friend of the show The Chart Store (I added the smaller wording, from Grok).

Note how the monetary base and CPI diverge in the 1980's when the BLS began to really monkey with it. Once "hedonic-quality adjustments" fully introduced, fuggedaboutit.

I know, correlation is not causation, but it’s also not necessarily not correlation.

Greg Weldon

One of the more entertaining and skeptical macro guys around.

“the consumer balance sheet is not healthy, the consumer is not strong. It's

bull. It's absolute bull.”

“you've been at a record high in the total number of people working multiple jobs”

“Retail sales just came out. Everyone was all excited - retail sales stronger than

expected for the month, right? Strong is not the word. 1.7% year-over-year increase, even the CPI - the lowest of the inflation rates at 2.4% - you're still negative on a real basis! All of the increase in dollar terms is because of price increases.”

“the retail sales have been negative - deflation in retail sales, on a real basis, 26 of the last 29 months, and every single month in 2024”

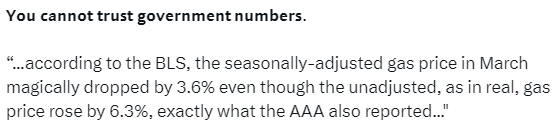

“they fudge these numbers with the seasonal adjustments”

“central banks will choose to reflate every single time”

“average hourly wages are up 4% but weekly hours worked fell, so you're making more per hour but you're working less hours The average weekly earnings growth fell. It fell.” [This is rarely mentioned]

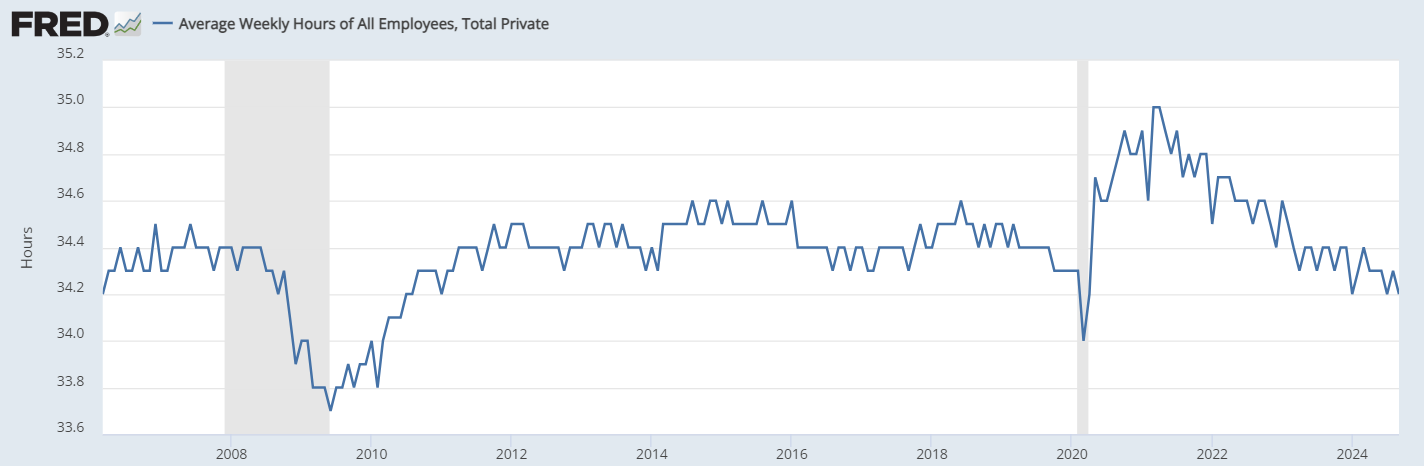

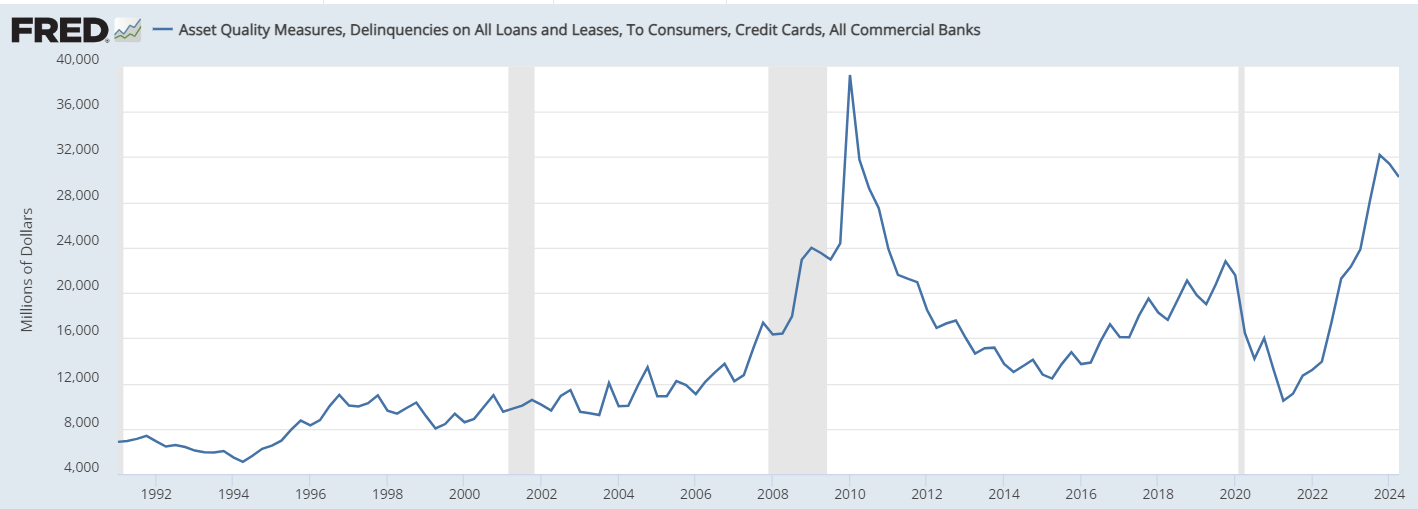

It took many decades to reach $2.5 trillion in Total Consumer Credit. Only took 16 years to double that.

Good grief.

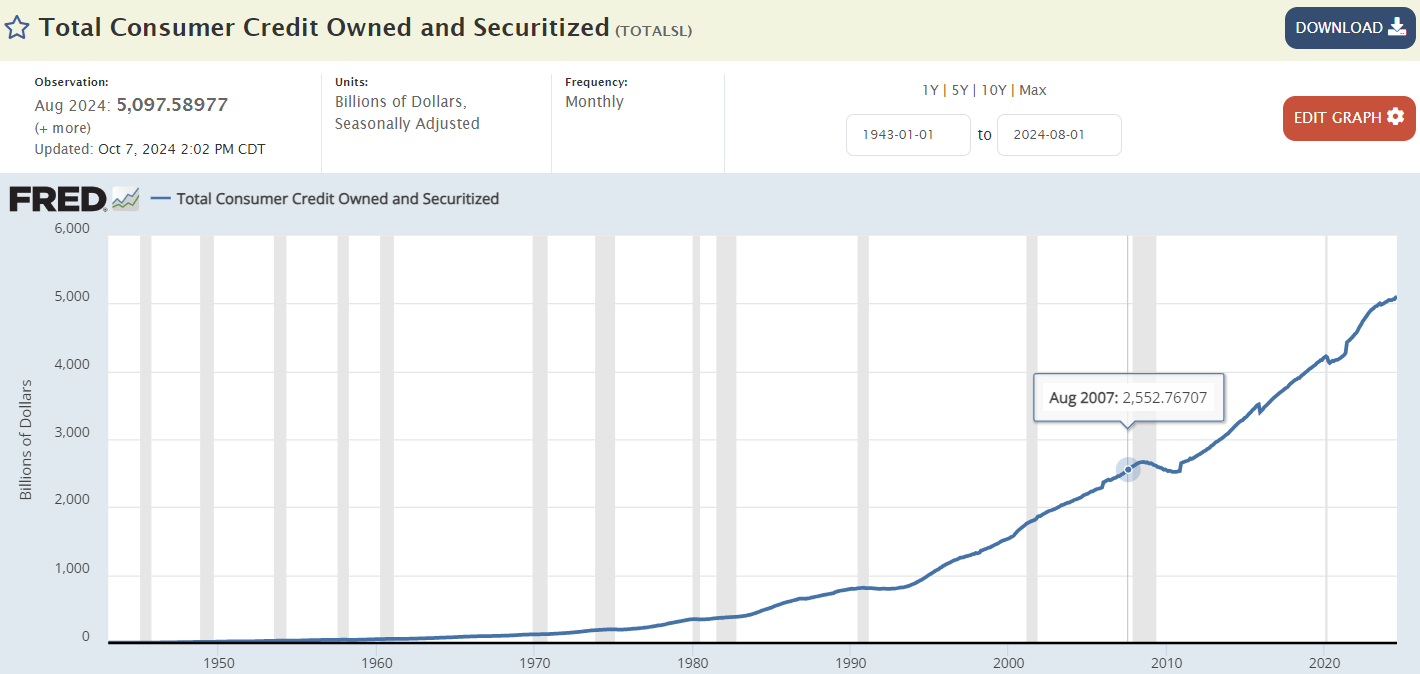

Credit card rates:

Orange Juice

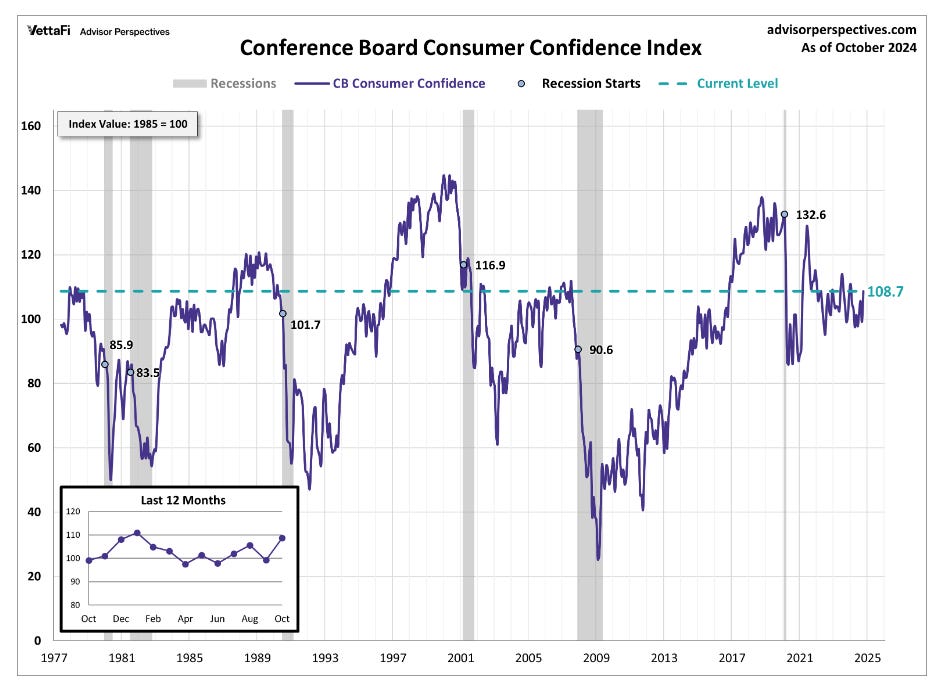

Consumers are a little more confident lately:

“The proportion of consumers anticipating a recession over the next 12 months dropped to its lowest level since the question was first asked in July 2022, as did the percentage of consumers believing the economy was already in recession. Consumers’ assessments of their Family’s Current Financial Situation were unchanged, but optimism for the next six months reached a series high.

Consumers became more upbeat about the stock market: 51.4% of consumers expected stock prices to increase over the year ahead, the highest reading since the question was first asked in 1987. Only 23.6% expected stock prices to decline.”

Neely Tamminga

“We still have not returned to repaying student loans with penalty. It's officially happening this month, but it's the first month in what 56, 57 months or something like that, consecutive. We haven't actually had that since March of 2020 where you had to repay your student loans and if you didn't, there was a consequence. This is the first month, October 2024, so when we blame this generation for being entitled, maybe we kind of did it a little bit by removing what it is to have consequence for decisions and loans and contracts, and I know that's a harsh statement, but there's a there is a price. There's always a price, and it’s a tradeoff whenever we make these decisions.”

“The second thing, and it's related I think again to the workplace entitlement sort of perception, is this is the generation that did remote school. Remote for one or two years in many cases, not our school, but a lot of schools were remote, and they're graduating into a place where they're like, I don't even understand the value of going into the office. Why do I have to go into the office? So could there also be some lingering effects of policymaking that have influenced and affected this generation?”

“History does not suggest you get to graduate from college and immediately have your own palatial penthouse estate. You cohabitate, whether it's with roommates, or someone you're married to, or your parents, right? I mean, the idea that you live by yourself is new, and it I think it's because of social media.”

“Mortgage rates follow the 10-year Treasury, and the 10-year has its own dynamics outside of what the Fed does and does not do. A closed sale can take 45-60 days, and 60 days ago 30-year mortgage rates averaged around 6.36%. As of this writing, they are 6.85%.”

Since the Fed cut 50bp, the 10-year yield is up about 0.6%.

Jim Bianco pointed out this week that the above behavior is not normal in past rate cut cycles.

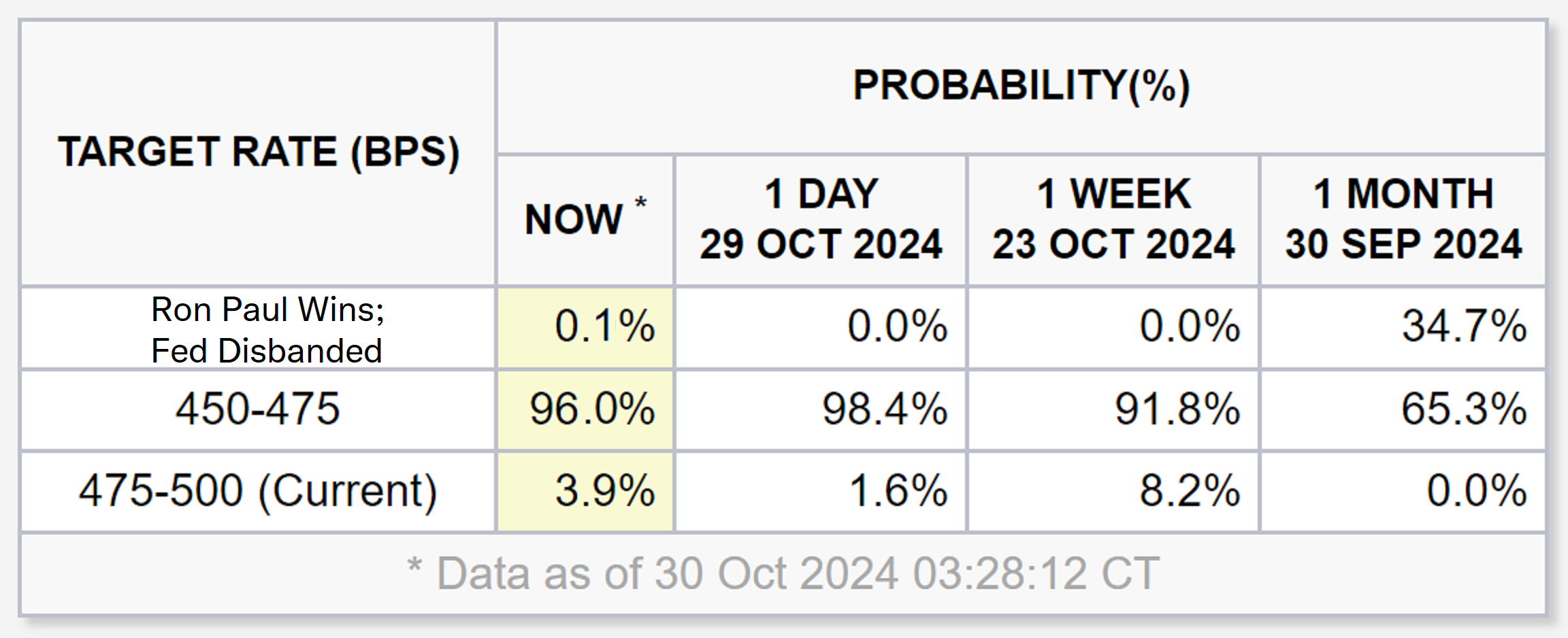

Target Rate Probabilities for Next Rate Decision (November 6)

Meanwhile, FHFA House Prices:

The Fed believes “that financial market conditions are somehow restrictive, that policy is somehow restrictive. I'm looking around to find that restrictiveness, and I can't find it. They've loosened policy so that it is less restrictive, but what happened to the bond market since they [cut]? Ten-year yields are up 60 basis points.”

I posted this the other day:

So then I get this serious (possibly-classified) outtake from a post by friend of the show Bearded Miguel:

“There’s something puerile about nuclear power gaining acceptance due to the power required for artificial intelligence. I often think back to Chris Dixon’s 14-year old quote that the next big thing always starts out looking like a toy, and there have been many of those since. Few people take AI anything but seriously, even though much of the regular consumer use looks an awful lot like a toy. Meanwhile given the leaders in GPU spending it looks as if the killer app for the foreseeable future will be selling bauble to the masses more efficiently. I’m annoyed by all of this because I think having cheap abundant energy for normies is a worthy pursuit, regardless of whether that helps Bezos build another rocket, or Zuckerberg get one step closer to real life Ready Player One. Amory Lovins is a renewables crusader who slanders nuclear energy with purported statistics that would make Michael “hockey stick” Mann blush. But before adopting that tactic he agreed with famous Malthusian Death Cult member Paul Ehrlich (of Population Bomb infamy) that abundance was the problem with nuclear energy.

Ehrlich stated flatly “giving society cheap abundant energy at this point would be the equivalent of giving an idiot child a machine gun.” Lovins said cheap abundant energy would be “disastrous” “because of what we would do with it. We ought to be looking for energy sources that are adequate for our needs, but that won’t give us the excesses of concentrated energy with which we could do mischief to the earth or to each other.” This is the Death Cult’s crude answer to the Jevons paradox, which observes increased efficiency can lead to increased consumption. That means if actual efficiency was the goal of climate activists, it could just lead to more emissions. Gains in US energy efficiency have been stunning, but since 1950 energy consumption still increased to 2.8x 1950 levels; real GDP grew more than 9x during that period. There is no “adequate” amount of energy for a capitalist economy where the basic impulse is growth.

One of the common lines of attacks from critics is that building new nuclear plants is too expensive and takes too long, but that charge depends on circular logic. It’s activism itself that has extended project timelines in the US and increased compliance costs. The Nuclear Regulatory Commission (NRC) “has a 32-step construction licensing process” many of which require the involvement of other regulatory agencies. Of course, stringent regulation of something like nuclear power seems quite reasonable on its face, but American plants “used to be built at a similar pace” as other nations. Japanese plants take between three to four years to build from groundbreaking to grid connection, while French plants take five to eight years. According to Doomberg, “the federal agency charged with overseeing the US civilian nuclear power fleet has, since its inception nearly five decades ago, worked tirelessly to stunt the industry’s growth, oppose nuclear innovation at every opportunity, and rob the American people of the benefits of clean and reliable nuclear power.””

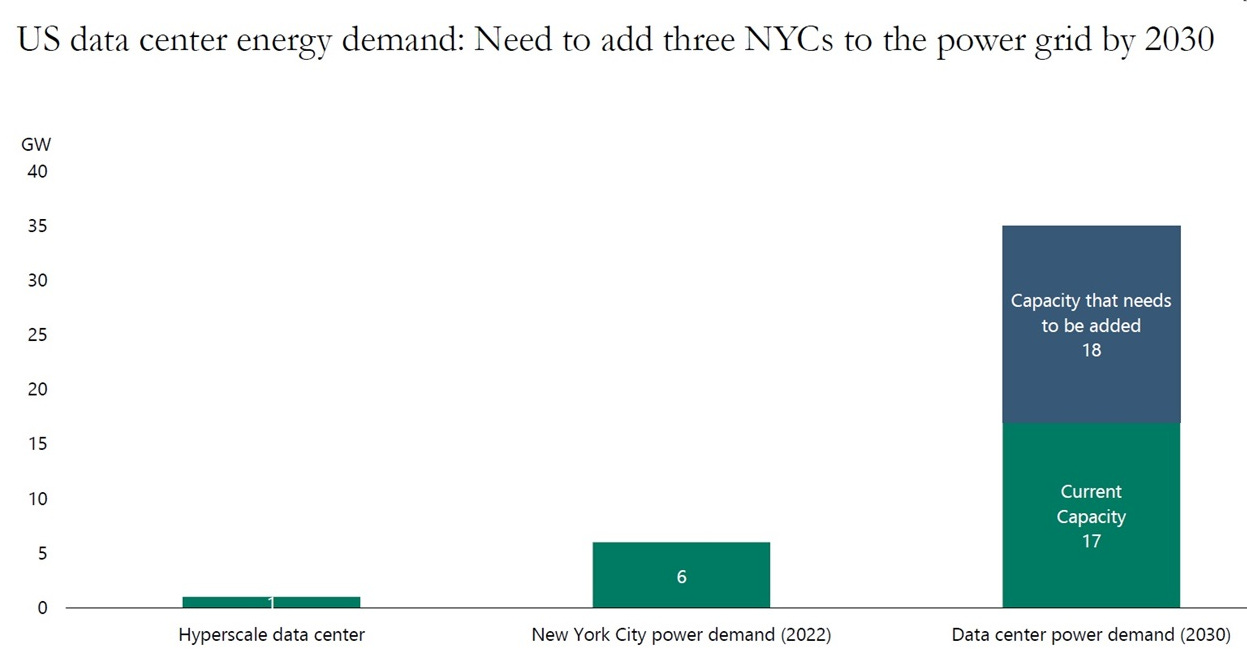

Need to Add Three NYCs to the US Power Grid by 2030

This is from Apollo, so take it with a grain of salt.

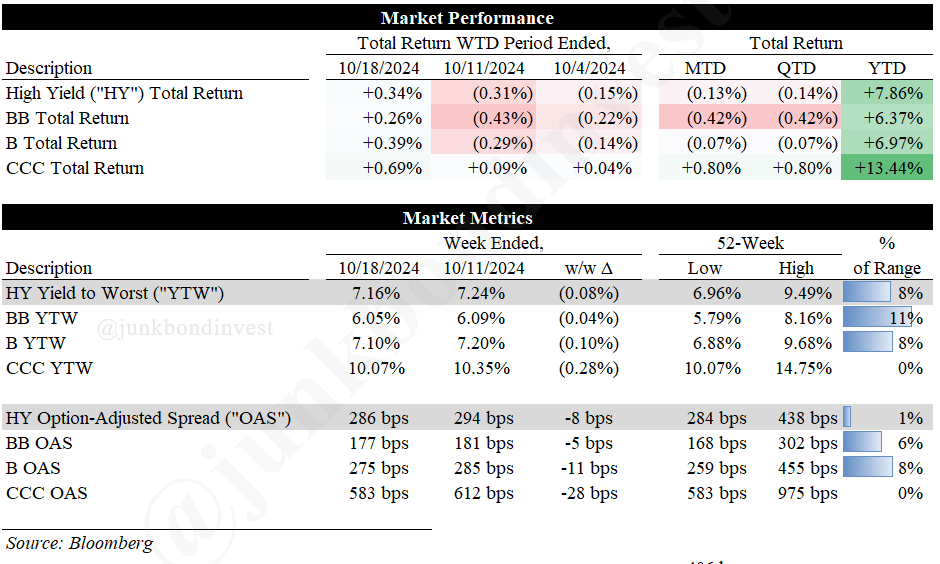

“Just when you thought the high yield market couldn’t get any hotter, it’s gone and surprised everyone again. Last week, spreads tightened to near post-GFC tights”

NY Fed says banks obscuring commercial real estate risks by extending loan terms “Banks have been tweaking the terms of commercial real estate mortgages to obscure losses, and in delaying the day of reckoning, are increasing risks to the broader financial system, a paper released Wednesday by the Federal Reserve Bank of New York said.”

How dare banks "obscure losses, delaying the day of reckoning, and increasing risks to the broader financial system" - isn't that the Federal Reserve's job?!

Just a reminder, from Jeff Gundlach back in May 2024.

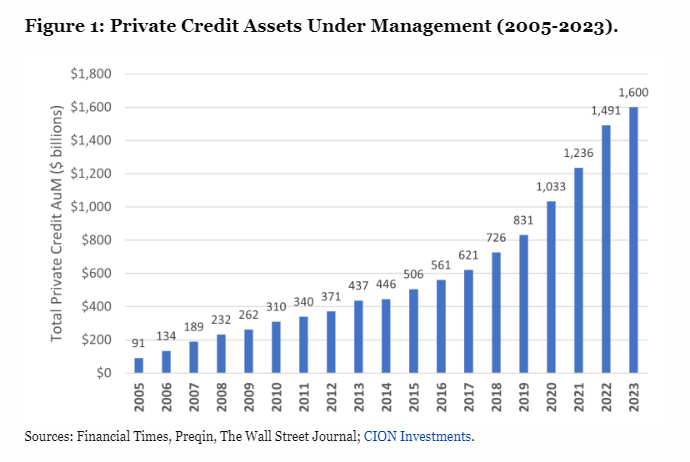

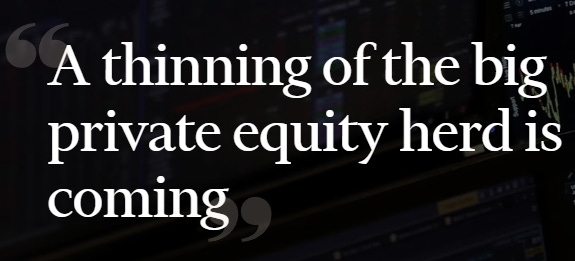

Private Credit

“In 2024, trustees of institutional investment plans are surrounded by consultants who have a deep-seated incentive to recommend alternative investments for little reason other than because their business models depend on clients believing that these recommendations add value. They are not required to prove their skill. They only need clients to believe unsubstantiated claims that they have it. More than any other reason, this is why investment consultants pepper trustees with recommendations to allocate to alternative assets like private credit…The reality is that private credit entered the flood phase several years ago. It is not a pristine, undiscovered watering hole. It is a treacherous swamp full of opportunists.”

From the FT, a Wall Street blog:

Let’s hope the entire herd goes off a cliff!

“1407 Broadway was, as far as the financiers of Wall Street could tell, as rock-solid an asset as could possibly exist. Located in the heart of Manhattan’s storied Garment District, its entrance cut from white marble flecked with a soft bronze terrazzo motif, the 43-floor tower was a money-minting machine with a never-ending roster of well-heeled corporate tenants.

So when the owners floated a $350 million bond backed by the building’s rental income in 2019, the bulk of the debt was stamped with a AAA credit rating, the highest grade awarded by ratings firms. Not even US Treasury bonds, the North Star for global financial markets, are deemed that safe. But 1407 Broadway, the thinking went, was so impervious to the vagaries of economic cycles that a default was unfathomable — nothing more than a once-in-5,000 years kind of freak event.

On June 17 — four years and 212 days after the bond was issued — investors in the AAA rated chunk of debt were informed they wouldn’t be getting the full $1 million interest payment they were owed that month. They’re now foreclosing on the building to salvage whatever they can of their investment.”

Reminded me of this:

“We were seeing things that were 25-standard deviation moves, several days in a row.”

- David Viniar, 2007

Maybe the models are wrong. And there’s this, from the same paper:

"...the probability of a 25 sigma event is comparable to the probability of winning the lottery 21 or 22 times in a row."

“they're not even close to bringing inflation back to target.”

“More than half of all the components within CPI are running at above 3% year-over-year, so there's a lot of celebration that the Fed has tamed inflation, brought it back down to target, but even if you look beneath the headline measures of inflation, these the measures - the Atlanta Fed sticky price CPI and all these types of things that kind of measure these the inflation persistence - suggest they're not even close to bringing inflation back to target. I think on the inflation side of things, it's very difficult to make the case that mission accomplished, inflation is back down to the to 2% in a sustainable way.” - Jesse Felder

“Inflation is still simmering. We’ve certainly had a comedown in the pace of inflation, but it’s just not subsiding as quickly as I think many had hoped.” - Lakshman Achuthan

Mike Green

“The structure that we've actually built involves people who are buying indices - whether those are total market, or the S&P 500, and we label those investors passive. We're doing ourselves a disservice - they're not passive. They are algorithmically simple investors that are choosing a very common strategy which is to buy stocks in proportion to their float-adjusted market cap weight.”

“…a situation in which the attempt to withdraw from those same passive investors overwhelms the available liquidity in the market and the market ultimately collapses.”

“When I started doing this work, I looked around at different markets to try to find ones that had the highest fraction of passive or systematic investors who had a defined strategy and a known response to flows into price behavior, that's where I stumbled across the XIV, which was a trade that kind of launched me into the public sphere. This is no different, right? What we're actually seeing is we're seeing a pattern of the traditional discretionary investor - a professional investor who attempts to do a discounted cash-flow type analysis to figure out what something is worth - being replaced by investors who presume that everybody else has done that work, and therefore they're not having any impact. But that's simply untrue.”

“Part of the reason why I'm speaking out is not because I actually think that I can change anything now, but when the event actually occurs, I want people to hold Vanguard's feet to the fire and say, ‘wait - we're not doing this again’”

Inside Out

“If there's one indicator - macro indicator - that I could have, and get rid of all the rest, if I could only have one, it would be the aggregate activity of insiders in their own shares. So what are the leaders of corporate America doing with their own money in the stock market? That, right now - in aggregate, insiders are more bearish than they've ever been in at least a decade” - Felder

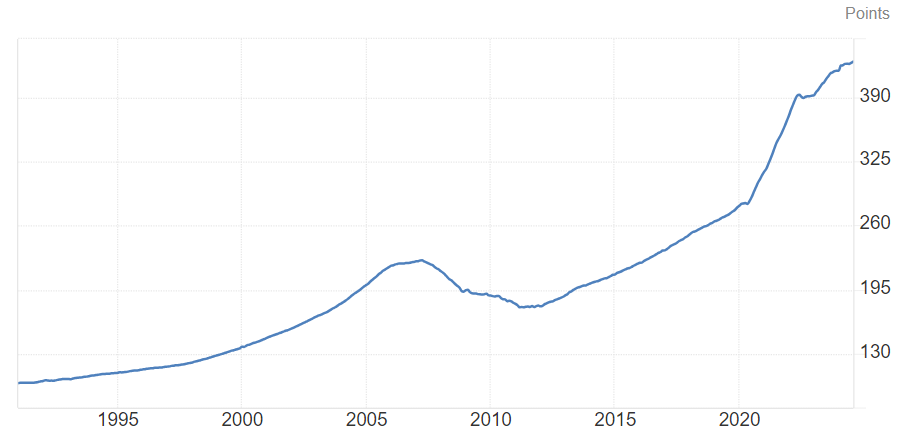

Interesting chart from here. Existing home sales and mortgage rates appear quite similar to the bubble before this bubble.

“It’s almost like we lost World War II. When you lose a war, your industry is destroyed, and then the winner gets to sell stuff. Like after World War II, everyone's industry was destroyed, and the US was intact. I think we've voluntarily given our industrial base to overseas. The CEO of Raytheon said in a speech a year ago there was 7002 components in the military industrial supply chain that they had no supplier other than China, so it's like borrowing money from China to make stuff made in China that you need to protect yourself from China. It's just not a good business plan.”

“In the stock market we get that 100-year flood every seven to ten years.”

The U.S. Military Rigged a War Game. It Still Lost.

“Millennium Challenge 2002 was the U.S. military’s most elaborate and expensive war game ever, designed to showcase the “military of the next century” on full display. Three years in the planning, budgeted at $250 million, it involved 13,500 participants waging mock war in nine training sites across the United States as well as 17 “virtual” locations in the powerful computers of the Joint Forces Command in Norfolk, Virginia. The scenario, on Iran, posited a “Blue” U.S. force pitted against a “Red” enemy bearing a strong resemblance to Iran.

The U.S. lost.

Unwisely, the planners had recruited a retired Marine Lieutenant General, Paul Van Riper, to lead the Red forces. In a series of brilliantly imaginative initiatives and maneuvers, Van Riper made quick work of the Blue force, sinking most of the attacking fleet in short order while circumventing his opponent’s attempts to cut off communications with his forces. Afterwards, he wrote a scathing report outlining ways in which the game had been rigged to ensure a Blue victory. Unsurprisingly, the report was immediately classified. Now, twenty years later, it has finally been released, albeit with many redactions.

It makes for instructive reading. The organizers forbade Van Riper to attack at night, for example, because “there were insufficient Blue service cell personnel..to support 24-hour operations.” Other restrictions included a ban on “adaptive thinking” on his part, an all-too realistic possibility in a real war. It was assumed that Blue force weapons would all perform perfectly. Critical press were thrown out of Blue force briefings. He was forbidden to use chemical weapons. It was assumed that he, the enemy commander, would be assassinated at a certain point by a Special Operations team - even though they had no idea where he was.

Reviewing the report today, it is striking how much the thinking underlying the strategy and tactics deployed by the losing U.S. force still dominates today’s Pentagon…”

“When the Federal Reserve began quantitative easing, the national debt was around 11 to 12 trillion. Today it exceeds $35 trillion, and what really bothers me is we talk about trillions as if they were peanuts. People - they're not shocked, and we all should be shocked.“ - Thomas Hoenig

I had several people tell me this number is far too low.

As regards the our national debt, I think the amount is so large it’s beyond human comprehension so its risk - and our national vulnerability - fails to impact IMO. Possibly too the average person with their own issues takes a ‘not my problem’ attitude - afterall what can we do about it? Warmongers need money afterall.

I think it was Chris Martinson of Peak Prosperity who equated the debt to time - if I recall, at one dollar = 1 second, 35 trillion equals 3.1 million years. Personally, I found that measure more relatable.

Thank you again for lightening my reading load with your summaries.

The gaslighting is going into overdrive with just a few days until the election. Jeanna Smialek is not alone. Greg Ip's article today has the following title and subtitle: "The Next President Inherits a Remarkable Economy. The high quality of recent economic growth should put a wind at the back of the White House’s next occupant".

No one asks: What if inflation is understated? If so, some (or even all) of the "real" growth these people are crowing about is not actually real.

I guess the people who don't believe the Democratic Party/MSM nonsense narratives are "garbage" people, just like the "basket of deplorables" from 2016. If the economy was really so great, Kamala would be running on the Biden economic record rather than running away from it and Trump would be down 10-15 points in the polls rather than tied (and probably up considerably given the polling bias we saw in 2016 and 2020).