A very strange way to think of things

The Fed will fix it

Best concise overview I’ve heard of what’s going on in markets lately, from Nick Megaw (except he’s joking):

“Economy Bad

Japan Scary

Retail Investors Dumb”

“The Fed has become more and more a facilitator of the Treasury, and of our our fiscal situation, and less and less acting as an independent guardian for the public interest [was it ever?? - rh].

Fed chairmen like Arthur Burns used to threaten to raise interest rats if Congress didn't deal with the budget deficit. You don't hear anything from Jay Powell, he's mute. I think unfortunately history is going to be very unkind to him, because both he and Yellen and even Bernanke - they kind of did the right thing initially - but then they did too much, and they didn't let up on the gas, so we ended up with an inflation problem, and we also ended up with a environment that encouraged the Congress to follow their worst instincts, and they did.

The one thing you can depend on with American democracy is that Congress will always do the wrong thing, and it doesn't matter which party you're talking about. So here we are. We have $35 trillion worth of debt, and it's mostly funded short-term, so whoever wins the White House inherits this mess. That's it's going to limit their flexibility rather considerably.”

A prescient Diego Parrilla on RealVision in 2020:

"Let's not fool ourselves, all we did with artificial low interest rates and this insane amount of desperate search for yield and lending and whatever, is create bubbles without precedents...the next decade is the transformation of bubbles that are too big to fail into inflation."

Just a heads up -

I saw that friend of the show Phil Bak posted this:

I’m unaware of any Substack email issues, but, just as Phil says, any emails from me would just be the posts you already get, and I would never send any other sort of nonsense (other than this nonsense) or requests to you for anything.

Anyway…

Brook Benton fixes this.

“If you’re convinced, for instance, that the music of your own youth is superior to whatever’s being made these days, then you can now cite a scientific paper to claim that today’s hits are just dumbed-down slop.”

I love the gaslighting.

That was some bear market we had, huh?

“The media, led by our friend Steve Liesman, is trying to stampede the Fed into a rate cut, in part because I think the equity markets have lost their way.”

How about a compromise: we cut the base rate to the 2-year yield (4% or so), and disband the Fed?

The Fed whisperers were out in force. To annoy me, they say Wharton’s Jeremy Siegel, instead of Wisdomtree’s Jeremy Siegel:

Similarly, Claudia Sahm - who is another uber-interventionist econ-cultist - was on CNBS the other day, saying she wants the Fed to cut rates, and "Get out of the way!"

Huh? I wish economists would get out of the way, permanently.

On a hunch, I checked, and of course. Paging Upton Sinclair!

It’s always amusing that the market can go up 8 million points in a year, but if stocks then fall 2% (or 8%), the asset gatherers and other degenerates come out of the woodwork screaming for the Fed to do something!!

What are you, five? Grow up.

Remember -

It’s sort of like a Texas holdem player who’s been on a hot streak suddenly watching his pocket aces get cracked by a set of twos, and then crying about “how lucky” the other guy is. Have you never played poker before??

Stock prices are the same way. They often seem unfair, perhaps more so nowadays than ever. Suck it up, or just buy T-Bills like Warren Buffett.

Hard to feel bad for shareholders when you see charts like this:

This guy, every time:

Meanwhile, rates are cutting themselves, which might not be good economic news.

“What is everybody worried about that they drive the ten-year down that fast?”

fyi A paid subscription gets you a lot more fun stuff, which I recommend, but I’m not your dad.

People spend so much time parsing the news and the data, seeking to find a leg up on markets, and I often wonder - does it do any good at all?

“How can it be that events, conditions and authorities’ actions have no impact on the stock market? The answer is: They are not causes but results.”

Invert, always invert.

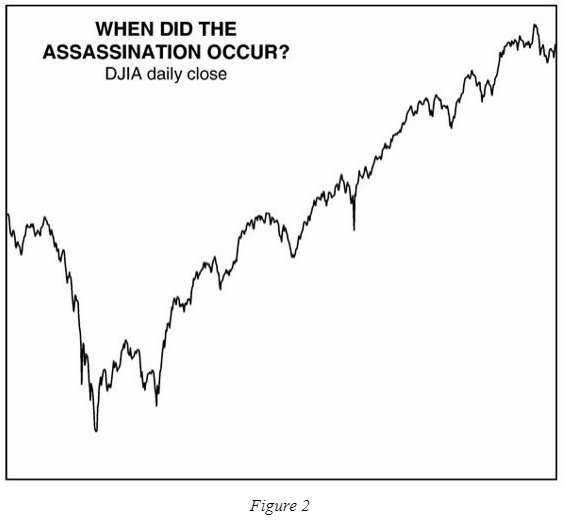

“Suppose the devil were to offer you historic news a day in advance, no strings attached. “What’s more,” he says, “you can hold a position in the stock market for as little as a single trading day after the event or as long as you like.” It sounds foolproof, so you accept.

His first offer: “The president will be assassinated tomorrow.” You can’t believe it. You are the only person in the world who knows it’s going to happen.

The devil transports you back to November 22, 1963. You quickly take a short position in the stock market in order to profit when prices fall on the bad news you know is coming. Do you make money?

Figure 2 shows the DJIA around the time when President John F. Kennedy was shot. First of all, can you tell by looking at the graph exactly when that event occurred? Maybe before that big drop on the left? Maybe at some other peak, causing a selloff?”

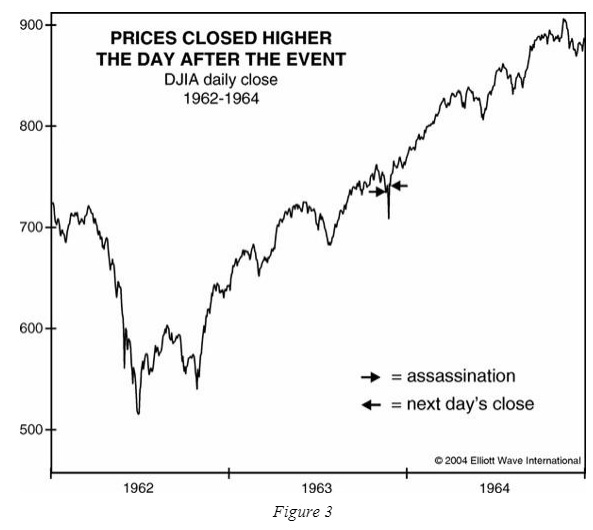

“The first arrow in Figure 3 shows the timing of the assassination. The market initially fell, but by the close of the next trading day, it was above where it was at the moment of the event, as you can see by the position of the second arrow. The devil had said that you could hold as briefly as one trading day after the event, but not less. You can’t cover your short sales until the following day’s up close. You lose money.”

“You aren’t really angry because, after all, the devil delivered on his promise. Your only error was to believe that a presidential assassination would dictate the course of stock prices. So, you vow to bet only on things that will directly affect the economy.

The devil pops up again, and you explain what you want. “I’ve got just the thing,” he says, and announces, “The biggest electrical blackout in the history of North America will occur tomorrow.” Wow. Billions of dollars of lost production. People stranded in subways and elevators. The last time a blackout occurred, there was a riot in New York City, causing extensive property damage. “Sold!” you cry. The devil transports you back to August 2003.

Figure 4 shows the DJIA around the time of the blackout. Does the history of stock prices make it evident when that event occurred? After all, if market prices change due to action and reaction, then this surprise economic loss should show up unmistakably, shouldn’t it? There are two big drops on the graph. Maybe it happened just before one of them.”

“The arrow in Figure 5 shows the timing of that event. Not only did the market fail to collapse, it gapped up the next morning. You sit all day with your short sales and cover the following day with another loss.”

Prechter goes on to give numerous other examples.

“People object, “You can’t tell me news doesn’t move the market. I see it happen every day!”

But they don’t see any such thing, and it takes careful study to reveal that they don’t.”

The VIX!

I'm a caveman, and it seemed incredible that the VIX seemingly just had its 3rd highest spike "event", second only to 2008, when Hank Paulson's buddies' billionaire status was threatened, and 2020, when a coronavirus was going to kill everyone on Earth.

Andy Constan graciously set me straight:

“There was a mispricing of one of the reference strikes used in the calculation which caused this. Notice the difference between your chart and the front month futures. The thing you are looking at is a calculation and not tradeable.”

Other than Andy responding to me, I haven’t seen this VIX explanation anywhere, certainly not in the financial MSM. This seems like misinformation!

Grant Williams

”I learned a long long time ago that having plans is not the best thing for me.”

I think I’m a few years older than Grant. I can personally relate to large parts of this interview (not the English football or pole dancing parts).

The interviewer is great too. He actually let’s Grant talk! (Grant’s the same way.)

“Growing up in the ‘70’s and early '80’s, as I did, it was a much more independent time. We we were left to fend for ourselves. We were the original latch-key kids. You got up in the morning before your mom, you went out on your bike with your pals, and whoever's house you were nearest at when you got hungry, you went there and that Mom fed you, and you came home when it got dark, and that was that. There was a resiliency, and a habit of making decisions. There wasn't anyone on a daily basis to run them by - you had to make decisions, and live and die by them.”

“I've always been happy with the decision I made [to forego college]. It's funny, the first time it became an issue ironically was when I went to moved to America in 1996, and to get my H1B Visa in America is a box-ticking - what's your college degree - and of course I didn't have a college degree, and there's a stipulation that if you don't have a college degree, they will accept - I think it was three years of real world experience counts for one year of a college degree - which I always found was probably the wrong way around. I’d done my 12 years at that point in time, and so I qualified for the exemption, but that always struck me as a very strange way to think of things.”

“I grew up in the same house from the age of three until I left home when I was 22 and bought a house myself. Imagine that, being 22 and able to afford a deposit on a house. I grew up in that same house on the same street, all my buddies were in that street. I'm still friends with my really close friends. I was at my best friend's mother's 90th birthday party two weeks ago back in the UK, I just grew up with that group of friends that were constant, and we went everywhere together, and we did everything together, and there's something magical about it.

I remember the first time I watched Stand By Me. That was my childhood, right? I had that group of buddies that you could just be merciless with , and at any given point in time three of you would have been ganging up on one guy, and then it would all switch around. It was something about that movie that really connected with me, because that's exactly what my childhood was like.”

Matt Zeigler: “You had kids - you started early enough that, especially working in finance, you've had more than one crisis through their younger and their developing years. How much does, I mean, the Asian currency thing, Long-term Capital Management, the tech bubble, then the financial crisis - you're a father with kids through all these periods. That's different than a slight downturn at the office or in the manufacturing plant. How'd that impact your family?”

Grant: “You know, I don't know the right way to put this - I never took it too seriously.”

“I got used to watching people who were more experienced than me not get too crazy when they had a big win, and not let big losses get them down.”

“I was around calm people early on in my career, and all the way through, I've been around calm people, and that's helped me for many years not get too high or too low, and not to let things shake me out of what I need to do.”

Grant on writing, content and community

“If you if you decide that the size of your audience is the most important thing, then no matter who you are or what you do, you have to alter your content”

“If you make the integrity of the content the key, and you allow that audience to grow organically over time, it may not grow to the size you want it and it may not grow as quickly as you want, but as it grows, it becomes organically bigger, and it becomes sticky, because those people have come to you not because you've gone out and sold them the idea of the content - they've gravitated towards it because it resonates with them.”

Thanks to the paid subscribers here!

“You can already see the mass bands of the Royal Guards standing behind Kamala trying to put wall to wall positive coverage about her in the media. I mean, it’s fascinating to me to watch really if you have the ability to step back far enough. And me being English, I don’t have a dog in the hunt, so that’s probably much easier for me than any average American. But the thing that surprised me is how obvious it all is. What’s going on with the favoritism and the desperation to do anything to keep Trump out of office?”

- Grant Williams on his recent podcast with Steph Pomboy

Mike Green, and Mike Taylor

New Jack Farley podcast with Mike Green, on the problem with passive. If you’re interested in the topic, check it out. Too much to just pick out a few quotes.

Mike Green: I think a lot of the excitement that there'll be an emergency cut, even though I feel it's the right thing to do from a purely economic standpoint, I don't see the Fed willing to trade away its credibility this quickly.

[Long Pause]

Mike Taylor: Oh, its credibility. Ok.

[Laughter]

“A major buyer out there [of CRE] was all of these private wealth products…Blackrock, JP Morgan - all of them…They’re all sellers now, and they’re all sellers because they have redemptions, and those redemptions go into a queue, and it’s very long. They’re now at the point where they’re selling just blocks of real estate, and there’s no buyers, except for strategic, smaller guys on the other side, that have independently raised capital…They’re getting stuff at 40% off, because that’s sort of the going rate now, and these big players are these forced sellers, and this is just the beginning of them selling. So they’re look at these great deals - at least they think they’re great deals, this is before a recession by the way…”

Looks like WaFd unloaded some of their exposure to rock-solid Bank of America back in May.

“While WaFd has decided to reduce its CRE exposure, still huge exposure to commercial loans makes us apprehensive. Significant exposure in only one category of the loan portfolio is likely to hurt the company’s financials if the economic situation deteriorates.”

Top 20 U.S. Banks by Assets: Commercial Property Exposure

The Austin Housing Bubble

“Austin, Texas, epitomizes the post-COVID real estate market, with home prices soaring by 101% from June 2016 to June 2022”

“When looking at current debt-to-income levels (DTI), the majority of borrowers are well over the 28% mark which used to be the industry standard. According to a document found on the FDIC website guiding on how much one can afford to borrower, “lenders usually require the PITI (principle, interest, taxes, and insurance), or your housing expenses, to be less than or equal to 25% to 28% of monthly gross income.” Using Black Knight data, 66% of all mortgages are over 30% DTI and 34% are over 40% DTI.”

“Office is a bigger problem than people realize.”

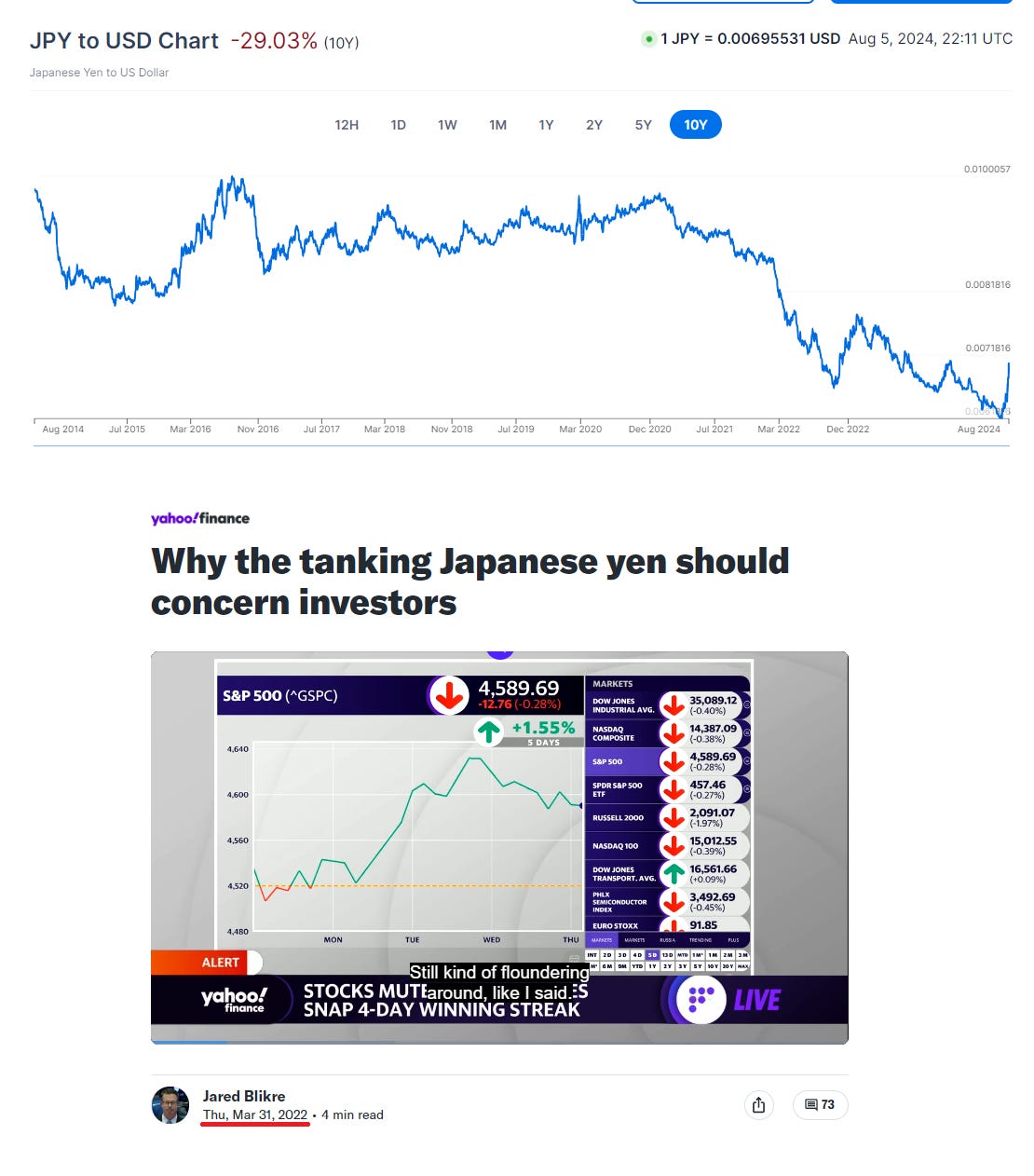

Japan

So confusing…

The Yen moving in any direction is apparently bad.

Wayfair

“Q2 was a dynamic quarter that resulted in another period of share gain, amid continued macro headwinds that are pressuring the ways customers are shopping the category. Customers remain cautious in their spending on the home, and our credit card data suggests that the category correction now mirrors the magnitude of the peak to trough decline the home furnishing space experienced during the great financial crisis," said Niraj Shah, CEO, co-founder and co-chairman, Wayfair.

More Americans Are Tapping Home Equity Credit Lines, NY Fed Says

Amusing final sentence in this article:

"Meanwhile more than 10% of the youngest credit card borrowers had not made a payment in at least 90 days as of the end of June, double the rate at the end of 2021."

Sorry you lost your house because you used your HELOC to buy groceries.

GOLD: A CONSTRUCTIVELY INHIBITING INSTITUTION

“I understand the imperative of creative destruction, but where has prudence gone?

It was nowhere to be seen in 2008, when a half dozen great American banks became wards of the state, triple-A-rated General Electric required a government bailout, and the edifice of subprime mortgages collapsed. “The greatest failure of ratings and risk management ever”—that’s what Doug Lucas, an executive director at the Swiss bank UBS, called this shameful episode when it was happening. And it was true.

Financial upheaval is as old as finance. Fractional reserve banking is inherently risky. But the so-called Great Recession stands alone for the pedigree of the victims it claimed—or would have claimed except for the saving, smothering, costly federal intercession.

On Wall Street, the fear of loss is the best regulator. It inhibits the human tendency, especially marked in boom times, to overdo it. Zero percent interest rates and reams of paper money work in the opposite direction. They are the great disinhibitors…

In the monetary vein, I think of the chaotic scenes at Cleveland’s Municipal Stadium, home of the old American League Indians, on the night of June 4, 1974. To draw fans into the cavernous ballpark, Indians’ management staged a ten-cent beer promotion. Before many innings had passed, spectators were wandering out on the field to introduce themselves to the players. The full moon didn’t help, but the underlying problem—the remote cause of the seven emergency-room visits and nine arrests—was the mispricing of a substance nearly as intoxicating as artificially cheap credit…

The “exact opposite” of the gold standard is really the system in place today in the United States. One might call it the PhD standard. It’s the system of discretionary manipulation of interest rates by doctors of economics to achieve a little inflation—not too much, mind you—and maximum employment.”

“Kings are maintained and secured by their friends but it is characteristic of tyrants to distrust them above all others, for whereas everyone wants [to overthrow tyrants], it is their friends who have most power to achieve this. The methods applied in extreme democracies are thus all to be found in tyrannies. They both encourage feminine influence in the family, in the hope that wives will tell tales of their husbands; and for a similar reason they are both indulgent to slaves. Slaves and women are not likely to plot against tyrants: indeed, as they prosper under them, they are bound to look with favour on tyrannies and democracies alike—of course the people likes to act as absolute ruler. This is the reason why, under both these forms of government, honour is paid to flatterers, in democracies to demagogues, who are flatterers of the people, and, in the case of tyrants, to those who associate with them on obsequious terms—which is the function of the flatterer.

Tyranny is thus a system dear to the wicked. Tyrants love to be flattered, and nobody with the soul of a freeman can ever stoop to that; a good man may be a friend, but at any rate he will not be a flatterer. Bad men are useful for achieving bad objects; ‘nail knocks out nail’, as the proverb says. It is a habit of tyrants never to like anyone who has a spirit of dignity and independence. The tyrant claims a monopoly of such qualities for himself; he feels that anybody who asserts a rival dignity, or acts with independence, is threatening his own superiority and the despotic power of his tyranny; he hates him accordingly as a subverter of his own authority. It is also a habit of tyrants to prefer the company of aliens to that of citizens at table and in society; citizens, they feel, are enemies, but aliens will offer no opposition.”

“The same vein of policy also makes tyrants warmongers, with the object of keeping their subjects constantly occupied and continually in need of a leader.”

“This is how capitalism works - we shift the problem to somebody else and we run.”

Don’t know if I ever posted this here, but it is summertime…

Jim Grant's story about the ten-cent beer promotion had me rolling on the floor

“It is also a habit of tyrants to prefer the company of aliens to that of citizens at table and in society; citizens, they feel, are enemies, but aliens will offer no opposition.”

This was interesting. One of the more tinfoil hat theory I’ve heard about the reason for allowing the invasion of the country is dilution. The theory used the alleged Covid jab numbers as the base. 75% got it. They were captured once and most will likely get captured again. But 25% said no. And they are the resistance and the real enemies of the state, maybe 60-70 million strong. Too big a number and too big a percentage. So what’s the easiest way to reduce their influence and strength. Dilute it. Import 30 million who owe their allegiance to the importers. And the % of resisters goes down significantly as against the whole, making them easier to control. . And the % of loyalists goes up. I blew it off when I first read the theory. But the more I think about it, the more sense it makes.

I guess we’ll know for sure when they start giving them weapons along with the free housing, food, debit cards and phones.