“The inconceivable is absolutely conceivable

when the survivability of the state is threatened.”

Russell Napier

The latest numbers are out from the Fed: "Corporate equities and mutual fund shares by wealth percentile group"

Since pre-Covid - all the trillions we spent to prop up the stock market - I mean save the economy - and the top 1% just got a bigger share of it all.

I am working on a, well, not sure yet, but a manifesto that I will hopefully put out for paid subscribers, someday. The problem is I want to be comprehensive with something like that (I have so much in my files), and, to some, comprehensive is synonymous with overwhelming. Also I don’t want to write a book because I’d just get distracted by something shiny. TL;DR

So here’s another eclectic selection of things you may find interesting, or not.

I’ve noticed that almost half of my subscribers are not in the United States (or at least their VPN isn’t), with decent numbers from the UK, Canada, India and Australia. I’ve been to two of those countries, so cheerio, take off ‘eh, namaste and g'day, mates. Glad to have y’all here.

From Almost Daily Grant’s:

The Bank of England today increased its benchmark bank rate by 50 basis points to 5%, marking a 15-year high and defying economist’s expectation of a 25-basis point rise. Wednesday’s inflation report, which showed an 8.7% annual increase for May, helped set the stage for that move, with BoE governor Andrew Bailey commenting that “the economy is doing better than expected but inflation is still too high and we’ve got to deal with it. . . If we don’t raise rates now, it could be worse later.” Economists at Bloomberg now project a 5.75% rate by the fall from a previous 5% guesstimate, “a level we already thought would be enough to tip the economy into recession.”

Same Andrew Bailey:

All the Central Banks went insane, but few went as insane as the Bank of England.

On March 17, 2022, the Federal Reserve began its interest rate hiking cycle, which has, thus far, evolved into 10 consecutive rate hikes, making it the fastest rate increases in 40 years. The Fed’s actions to tame inflation included four consecutive interest rate hikes of an aggressive 75 basis point hike (three quarters of one percent) on June 16, July 28, September 22, and November 3 of last year.

At that point, every trading veteran on Wall Street was scratching their head and asking themselves the same question:

Why aren’t we hearing about interest rate derivatives blowing up and taking down either a U.S. mega bank or its counterparty on the wrong side of the trade?

That’s a great question.

As of December 31, 2021 – prior to the March 17, 2022 launch of the fastest Fed rate hikes in 40 years, those same four banks were holding a combined $18 trillion notional in interest rate derivative contracts which had a maturity of more than five years. Exactly how does one get out of these contracts, or find a counterparty to hedge them with, once the Fed starts tightening and shows no signs of stopping? Did all four banks have a magical crystal ball and make bets in those 5+year contracts that interest rates would be skyrocketing?

Here are the numbers for Q1 2023. There are now $21 trillion in notional interest rate derivative contract maturing in over five years. $21 trillion used to be a lot of money.

Yet as of March 31, nobody seems to have taken any meaningful charge-offs.

Adding to our curiosity as to how everybody landed on the correct side of the interest rate derivative trades during the fastest rate hikes in 40 years, is a chart in the most recent OCC derivatives report for the first quarter of this year. It shows how much commercial banks have charged off quarterly for derivative losses since 2000. Following the financial crisis of 2008, the charge-offs spiked to as high as $1.6 billion in 2011 but have been absolutely tame in the past two years. How is this possible?

Well, 2011 was three years after 2008, so maybe there’ll be huge charge-offs in 2025?

WSOP is the best:

Earlier this week, we emailed the very nice and responsive folks in the press office of the OCC with two questions on the current OCC report on derivatives for the quarter ending March 31, 2023. The first question inquired about the following:

“Regarding Table 16 in the current report, where does the OCC get the data for the column titled ‘Bilaterally netted current credit exposure’? That is, does the OCC calculate it or does the OCC rely on the respective bank to calculate it and provide it to the OCC?”

An OCC spokesperson responded as follows:

“Bilaterally netted current credit exposures shown in Table 16 are calculated and reported by each respective bank. This information is reported on Call Report Schedule RC-R Part II, Risk-Weighted Assets, Memorandum Item #1 ‘Current credit exposure across all derivative contracts covered by the regulatory capital rules.’ ”

In other words, banks that have rigged everything from foreign exchange to Libor interest rates, to precious metals, to U.S. treasury securities have the full confidence of the OCC to accurately report their derivative exposures.

Bilateral netting is defined by the OCC as follows:

“A legally enforceable arrangement between a bank and a counterparty that creates a single legal obligation covering all included individual contracts. This arrangement means that a bank’s receivables or payables, in the event of the default or insolvency of one of the parties, would be the net sum of all positive and negative fair values of contracts included in the bilateral netting arrangement.”

According to Table 16 in the current OCC report, through the use of bilateral netting, those four mega banks mentioned above have reduced their total derivative contracts (interest rate, credit, equities, precious metals, foreign exchange, etc.) for the purpose of calculating total credit exposure to capital, as follows: JPMorgan Chase Bank’s total derivatives went from $59.8 trillion to $317.4 billion. Goldman Sachs Bank USA’s total derivatives went from $56.5 trillion to $76.34 billion – making JPMorgan Chase look like an amateur at bilateral netting. Citibank’s total derivatives went from $55 trillion to $181 billion; and Bank of America’s total derivatives dived from $22 trillion to a very tame $100 billion. (See chart below derived from Table 16 data on page 20 of the current OCC report.)

Our second question to the OCC was this:

“How does the OCC explain the fact that despite the fastest Fed rate increases in 40 years, the public has heard no reports about massive losses on interest rate derivatives — despite the fact that this is a highly concentrated market? To express it another way, how could everybody have been on the correct side of these trades?”

The OCC spokesperson responded as follows:

“Banks are required to have sound risk management and control practices for managing and monitoring interest rate risk and trading activities. The vast majority of OCC supervised banks’ derivative activities are for the purpose of hedging exposures. Thus, most interest rate derivative positions entered into by banks are to neutralize interest rate risk exposure resulting from on balance sheet and customer-driven positions.”

The ability of the mega banks on Wall Street to have “sound risk management and control practices” would have far more credibility were it not for the fact that century old mega banks on Wall Street either blew up in 2008 or were on the verge of blowing up when the Fed decided to secretly inject them with cumulative loans totaling $16.1 trillion over two and a half years

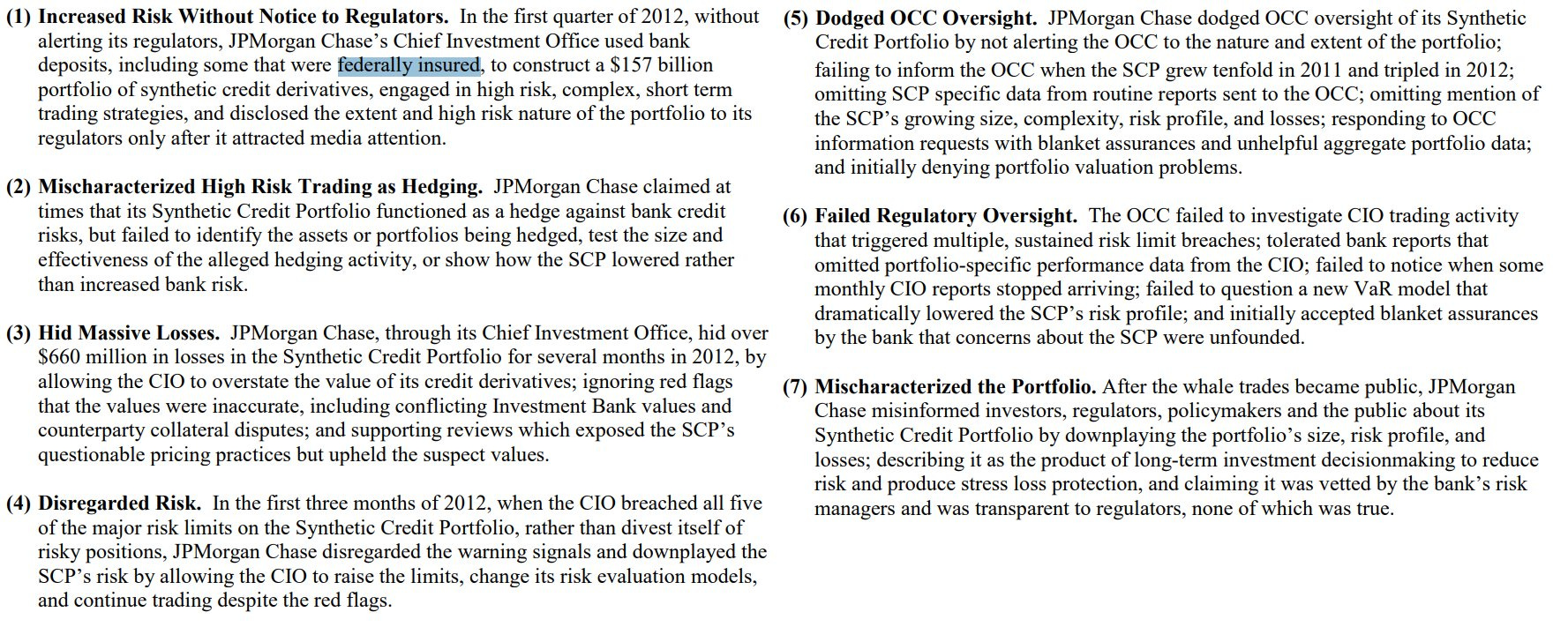

Then there is also the pesky detail that the largest holder of derivatives in the United States is JPMorgan Chase, the bank that used depositors’ money to gamble in derivatives in London in 2012 and lose $6.2 billion of depositors’ money. The recklessness of this action on the part of the largest bank in the United States was so egregious that the U.S. Senate’s Permanent Subcommittee on Investigations conducted an intense investigation into the matter and released a damning 300-page report in 2013.

Here’s the repot: JPMORGAN CHASE WHALE TRADES: A CASE HISTORY OF DERIVATIVES RISKS AND ABUSES

The late Senator Carl Levin, chair of the Subcommittee at the time, told the American people that JPMorgan Chase “piled on risk, hid losses, disregarded risk limits, manipulated risk models, dodged oversight, and misinformed the public.”

Q: What sent you down this path?

John Titus: The bailouts of 2008-2009, when I realized that the rule of law in the country was out the window.

"Our system is run by criminals."

John Titus is great. Check out his Youtube channel before he gets banned.

Home Flipping is now our national pastime.

ATTOM, a leading curator of land, property, and real estate data, today released its first-quarter 2023 U.S. Home Flipping Report showing that 72,960 single-family homes and condominiums in the United States were flipped in the first quarter. Those transactions represented 9 percent of all sales.

The latest portion was down from 9.4 percent of all home sales in the nation during the first quarter of 2022. But it was still up from 8 percent in the fourth quarter of last year, hitting the second-highest level this century.

There was a great show, the U.S. version of "Property Ladder" with Kirsten Kemp from 2005-2007. First time flippers with zero experience rushing to complete their "remodel" before the first payment was due. Comedy.

Rental landlords may have to brace for impact.

The pressure will come during the second half of this year and into the next as more rental supply hits the market, reaching the highest level since the 1980s, according to RealPage.

“We're going to deliver more supply than what we can realistically absorb,” Carl Whitaker, director of research and analysis at RealPage told Yahoo Finance.

Rent prices have fallen the most in three years in May as the number of rentals grows, tipping the rental market scale in favor of tenants. The median asking rent dropped to $1,995 in May, down 0.6% from a year ago, Redfin reported, the steepest annual decrease since March 2020.

Redfin noted the amount of completed units available grew 24.2% in April from a year ago. Separately, RealPage found that more than 500,000 are scheduled to be finished in the next two years. Most of those new buildings are mainly Class A apartments, Whitaker said.

A 0.6% drop! Better get back to ZIRP and massive QE so we can get those rents back up.

Hawaii: “This is a very strange market. No inventory, with sluggish sales and lots of price reductions. Yet some properties still sell for full price or even occasionally over-asking.”

Seeing a lot of comments like this:

UK: “Landlords are warning that their finances are on the brink of crisis as surging buy-to-let mortgage rates wipe out profits and force growing numbers to sell at discounts of up to 25 per cent…

The average two-year fixed rate mortgage is now 6.1 per cent, up from 5.56 per cent at the beginning of last month and 2.96 per cent two years ago, according to rates scrutineer Moneyfacts. Landlords owe around £533,000 in buy-to-let borrowing on average, typically in interest-only mortgages.

Rising costs mean that profits are quickly evaporating – and some landlords are now plunging into the red.

The average buy-to-let property in England and Wales currently generates around £12,000 a year in rental income, according to analysis from estate agent Hamptons. The latest hike in mortgage rates will see average profits fall overnight from £4,490 to £1,780 for a basic-rate taxpayer.

Sorry about all the ads.

"0% inflation feels like deflation for people who have made commitments that depend on gradual currency devaluation."

Denver Airbnb host talks rental income

Various market signals — stock prices, credit spreads, volatility — seem to be shrugging off the inversion. More surprisingly still, parts of the economy itself seem to be mocking the curve with shows of strength. This week’s big surge in housing starts is just the latest example. One has to ask whether this eminently sensible and super-reliable indicator could be wrong this time around.

OK, first off - was there a “big surge in housing starts” Mike Shedlock?

Another Heavily Revised Housing Starts Joke of a Report for May 2023

Last month I stated “History suggests the April rise will be revised away in May.” Sure enough. The Commerce Department revised housing starts in April from 1,401,000 to 1,340,000. That’s a negative revision of 4.4 percent. The big jump in April is now a reported decline. So take the huge jump this month with with a heavy dose of skepticism.

This theory intrigues me:

The second way to call the yield curve a liar is to suggest that long rates have become hopelessly distorted — are too low, essentially — and therefore the curve no longer sends a reliable signal. It is common to blame the Fed’s bond-buying programs for the distortions. All you really need, though, is an argument that 10-year bonds are badly mispriced and that their yields should be higher (meaning the “real” yield curve is shallower than the apparent one).

Hmmm…

71%!

The average American faces spending 71% more on groceries than they did last year

I'm sorry - the math geeks at the BLS say food only went up 5.8%, and it was better food, so the price actually dropped, seasonally adjusted, if you stopped buying hamburger and ate sawdust instead.

“Maybe you own 10 houses, you sell one, and you buy some treasuries, diversify. Take some chips off the table. Don’t sell everything. If you’re in Florida, you might want to sell more there than if you’re in Ohio.”

After she leaves:

Jamil: I mean, look, there’s aspects of what she’s saying that are really right. There’s risk involved. If you’re buying a property right now and your cap rate or cash on cash is 5%, I mean, why?

Dave: Yeah.

Zelman isn’t falling for the “housing shortage” thing, and I agree. There is no housing shortage nationally - there is an affordable housing shortage.

I personally think big investors - while a small % of investors - hold a huge number of housing units. Also a lot of ma and pas got into 1 to 100 units in a desperate reach for yield because the couldn’t just get a 5% CD anymore.

This includes the 2 million + AirBnb’s in the U.S. alone that would otherwise be long-term rentals or owned by people who’d actually live there and hopefully contribute to the community, instead of just being a residential neighborhood motel.

I think homes for sale will rise over time, regardless of rates. Death, Divorce, Default…

This chart above looks terrifying to some, but then again:

The Scariest Thing CRE Investors Might Hear: Recourse Loans Only

Want to scare an investor, developer, buyer, or owner in CRE looking for a new loan or refinance? Try the words “recourse only.” If everything beyond the value of the property is on the line, to what degree will the asset class be considered more trouble than it’s worth?

…“Through May, CMBS issuance declined 75% from the same period last year, while the number of deals dropped 66%, per Trepp”

Hey, maybe then you guys wouldn’t be so leveraged up!

A return to a vehicle environment closer to the pre-pandemic norm has allowed for inventories to replenish and for vehicle values to stabilize. A newly released TransUnion and J.D. Power study contends that this normalization of the market has put many recent borrowers in a far less advantageous equity position, posing some payment risks.

The study, “Impact of Unsettled Vehicle Values on Lenders and Consumers,” found that as a result of well-established supply and inventory challenges early in and throughout much of the pandemic, vehicle values increased dramatically, in particular in the used vehicle market. As a result, many consumers secured loans with relatively high monthly payments.

As vehicle values have declined in recent quarters, used car loan-to-value ratios (LTVs) at origination have trended in the wrong direction for consumers. Originating LTVs in Q1 2023 averaged 125 up from 110 in Q1 2022 and 104 two years prior. LTVs measure the difference between the loan amount and the market value of the auto. A lower LTV generally means a borrower has more equity in their auto loan. This means that while the majority of consumers will find themselves with positive equity, there are some in more challenging spots.

“To a large extent, used vehicle values were elevated as a result of the scarcity brought on by pandemic-related supply chain and inventory issues,” said Satyan Merchant, senior vice president and auto business lead at TransUnion. “As those issues have abated, and inventories have begun to return to more of a normal state, the value of those used vehicles have begun to decline.”

From Almost Daily Grant’s

Cumulative unrealized losses at the Vision Fund and Vision Fund 2, (SoftBank’s combined $140 billion, in-house v.c. arms) reached $6.7 billion in the fiscal year ending in March, after the firm booked $66.4 billion in mark-to-market gains during the peak of the pandemic mania.

“There are no bids.”

Meanwhile, Son’s venture capital peers still wrestle with the fallout of the recent private capital bacchanal. PitchBook relayed last week that v.c. behemoth Tiger Global has redoubled efforts to offload a portion of its portfolio of late-stage startups after receiving a cool reception from would-be bidders. The fund dove headlong into the asset class during the Covid-era crucible, investing in 315 companies in 355 transactions during 2021 alone.

That was then. In hopes of burnishing its cash position, Tiger recently offered to sell a chunk of its positions in roughly 30 startups in bulk via a so-called strip sale, receiving no takers. As a result, the firm has reportedly opened bidding for any of its individual portfolio companies, a move that “suggests that it faces more pressure for liquidity compared to other venture firms.”

Then again, Tiger has company in its struggles to offload assets, this year’s near 40% stampede in the tech-heavy Nasdaq 100 aside. Ken Sawyer, managing director at Saints Capital, told PitchBook that at least five such strip portfolios of at least $200 million in net asset value have recently been shopped around. “Many of these are brand name funds and brand name family offices,” Sawyer concluded. “There are no bids.”

On Housing:

Supply is broadly on the wane, as analysts at Barclays found last month that listings top their spring 2019 levels in only a single market within the nation’s top 50 (Austin, Tex.), with most other regions stuck far below levels seen four years ago. As a result, newly completed dwellings account for 32% of nationwide inventory for sale – double the average ratio seen in the last 40 years – leaving homebuilders in an enviable position.

To be more succinct, the next bear market will occur in indexed portfolios. Anyone who defines risk as the tracking error of a portfolio versus an index is going to be massacred, as occurred when Japan made up more than 50% of the global index, with Japanese banks alone having a 25% weighting.

The [WSJ] article claims that inflation in the U.S. and Europe is still around 5% which is only correct if you believe official inflation numbers - the same numbers that purported to state that inflation was below 2% for years while financial asset inflation skyrocketed. In truth, the price of everything that matters increased at double digit while central banks lowered benchmark rates to (or below) zero. The fact that governments rely on wildly inadequate official inflation numbers should surprise nobody - if they used real world numbers they would go bust overnight as those numbers are used to determine increases in entitlement payments that comprise the vast majority of their obligations. But investors should have no illusions about the true rate at which prices are rising.

Interesting slideshow from the 2023 Ben Graham Value Investing Conference, titled, “Investing Like A Forensic Accountant.”

Updated Bitcorn Ratio chart, which I’ve been doing since 2017:

Food prices have skyrocketed at regular grocery stores over the past year. The only way to contain the damage is to play the weekly sale/reward club game. My grocery bill has been somewhat contained over the past year only because I started shopping at Costco, an option unavailable to poor people, especially in urban areas, and even if they could get to a Costco they don’t have the “working capital” to buy quantities more than their current week’s paycheck can cover, which isn’t enough to buy in bulk. But as you often say, the Fed doesn’t much care about what happens to the poor and middle class.

Off topic (which topic?)….yesterday I was distracted by a shiny object ….EB Sledge’s book With the Old Breed (documenting the WW2 marine battle for Peleliu and Okinawa).

Reading along, something jumps off the page at me….he mentions that a Marine grunt in the thick of the horror show was being paid $60 a month.

That was approximately 30 years after the advent of the Fed, and it just struck me how nothing has ever changed. They were borrowing/printing like hell to build (buy) planes and tanks, but nothing for the fodder.

Fast forward to the latest war (Covid) and look what happened.