A.I. doesn't understand me.

What's the opposite of "restrictive"?

The FOMC is full of geniuses like Austan.

"There's not always a trade. Sometimes you gotta wait."

The Fed is So Restrictive!

"I'm pretty disappointed with reality right now."

An interesting 2019 article I just came across: Did Jeffrey Epstein Personally Set Off the Financial Crash of 2008?

“Interestingly, Jeffrey Epstein may have personally initiated the dominos falling that eventuated in the collapse of Bear Stearns by asking, on April 18, 2007, for his $57 million back from a hyper-leveraged Bear Stearns hedge fund investing in mortgage-based financial gimcrackery.”

The article references a June 2007 Dealbook article: More Bad News for Jeff Epstein?

“BusinessWeek reports that Mr. Epstein’s Virgin Islands-based money-management firm, Financial Trust Company, is listed in a filing with the Securities and Exchange Commission as a stakeholder in Bear Stearns‘s High-Grade Structured Credit Strategies Enhanced Leverage Fund, which became much easier to refer to in recent weeks as “Bear Stearns’ collapsing hedge fund.”

…Regulatory filings show that Mr. Epstein’s firm had voting power over 10 percent of the equity in the Bear Stearns fund, which, aided by loans from some of Wall Street’s biggest banks, bet heavily on the securities linked to the market for subprime mortgages, or those to homeowners with weak credit histories. As the subprime mortgage market has been rocked by a rise in defaults, many of those bets have gone bad. As of the end of April, the Bear fund was down 23 percent for the year.”

And I’ll throw this article in just for fun: "Jeffrey Epstein Chaired a $6.7 Billion Company that Documents Suggest May Have Received a Secret Federal Reserve Bailout"

Barry Strauss with Grant Williams and Michael Kao:

“First of all, I want to say that I’m bullish on America, and I think that we suffer from a surfeit of angst and worry about where we are. I think it’s partly related to social media and the fact that everybody has a microphone nowadays. Anybody can talk and it’s easy to say, “We’re in a terrible time and everything’s falling apart.” I don’t really think so. I don’t really think that’s true. That being said, there certainly are strains on our society, and there are issues that in some ways we are in the period of the third century [Rome] crisis, but I think, again, we have to take all this with a grain of salt. I think the United States remains a very strong country and a very strong and resilient society. It’s not an accident that people from all over the world want to come to the United States. Not every place in history has had that distinction.”

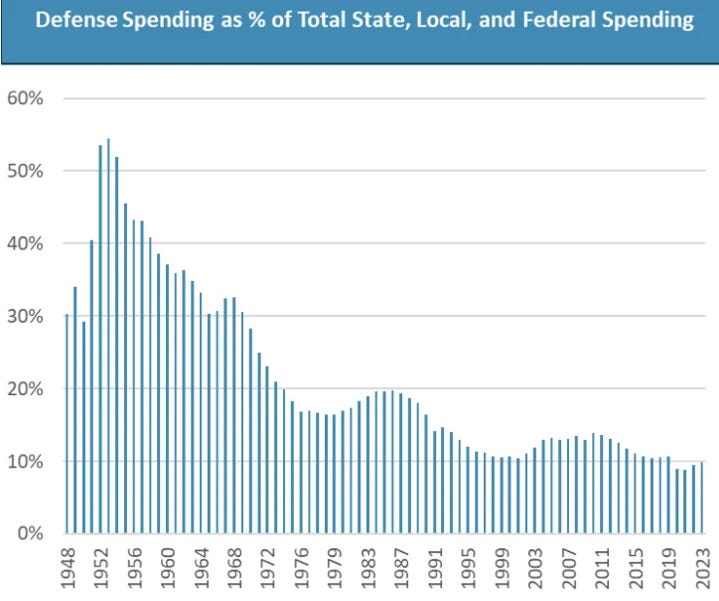

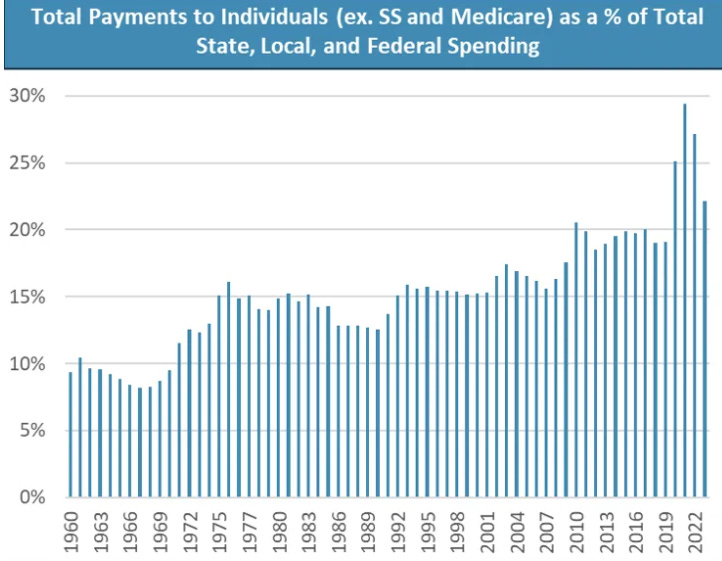

Will "Efficiency" Fix the Budget?

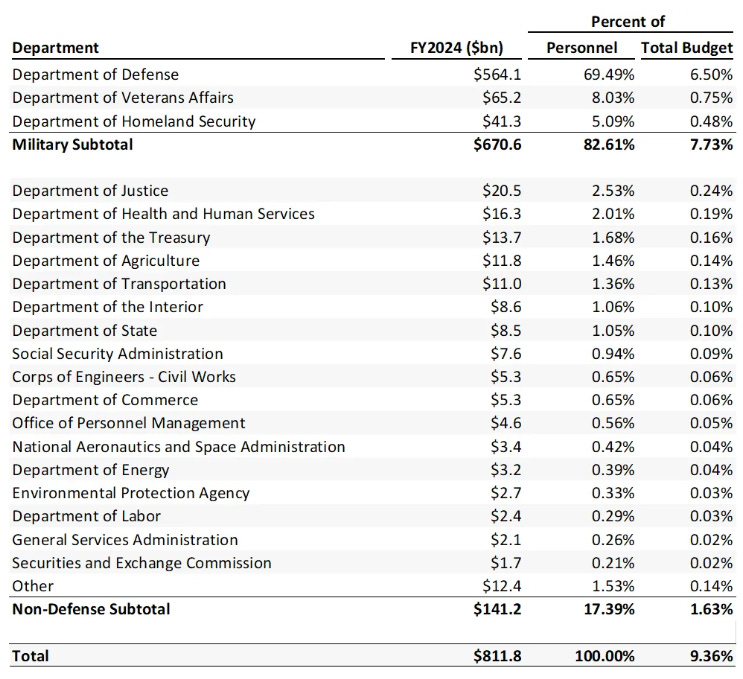

“If we assume that “draining the swamp” doesn’t mean reducing active duty military or restructuring veteran pensions, there is just $141 billion in remaining employee costs to address, just 1.6% of the budget.”

“Rebalancing Social Security through the end of the century would require either an immediate 41% hike in payroll taxes from 12.4% to 17.4%, or a 26% permanent reduction in Social Security benefits. If Trump succeeds in his campaign promise to eliminate tax on Social Security, the Trust depletion will occur even faster, and the required adjustments will be even greater.”

“Addressing the long-term structural challenges are necessary for the decades to come. If these core issues of demographics, entitlement spending, and overall revenues are to be addressed, it won’t be from executive-appointed cost cutters. Rather, it will require wholesale legislative changes, with implicit buy-in from the population.”

Dot Com 2.0

“Comedy value aside, what we have here is what I’d argue to be the fundamental flaw behind the latest advancements in generative AI, and the reason why most current predictions of what it will go on to do are utter nonsense…

Because of the way human language works, so long as your dataset is large enough and the statistical models are good enough, this can actually approximate human speech and knowledge pretty well. Indeed, much of the ‘shock’ of current AI’s capabilities has arisen from the fact that a surprising number of human tasks can essentially just be replicated by splurging a load of glorified predictive text onto a page…at no point during this process does the AI ever ‘understand’ any of what it writes…

To use an analogy based on the famous Chinese room thought experiment, imagine an English-speaking man in an enclosed room, who does not speak a word of Chinese. While in that room, he is able to find an enormous library of books written entirely in Chinese, with no English translations. He does not understand a word of it, but as he reads through, he begins to notice patterns, where in certain contexts certain characters are more likely to occur after certain other characters and symbols. He reads more and more through the books, and is eventually able to put together a rough model for the continuous patterns he finds. Now, if someone were to post a conversational message in Chinese, he would be able to ‘respond’ in a roughly accurate way (being more accurate the more books he has on the subject and the better his pattern identifying skills). However, if they were to post him an instruction (eg pass me one of your books), he would be no more capable of being able to carry it out than before he read through the pile of books, as he has no way of being able to relate the characters he sees to actual meaning.

…customer service is an area many people claim to be obsolete following AI. Certainly I can see that an AI can replicate the advice side of things (“Have you tried switching it off and on again etc”), but as soon as you arrive at a situation in which action needs to be taken (eg something’s gone wrong with a purchase), an AI will be either almost entirely useless at solving it, or be stuck with incredibly simplistic responses such as providing refunds. This may change in future, but there is nothing in the current ‘AI revolution’ that has brought us any closer to this.

…from my outside layman’s perspective, so far I had kind of been assuming that however difficult it is to construct semantic models, they would have at least managed them in incredibly basic areas like mathematical functions. However, as the images show, it cannot even do that….As it stands then, we have a large group of people hurling money at AI hoping it will change the world, without realising that it is barely even capable of interacting with it even in basic mathematical ways.. And once they do realise there is no possible way for them to get their returns back, they will also have no idea why that is the case, and won’t be able to distinguish between the valuable AI and tech stocks and the bogus ones. The likely result - dot com 2.0.”

The above reminded of this hilarious article from June 2024, and coincidentally as I write this I just noticed this Herb Greenberg post, “Proof that Gen-AI Can’t Think”

Why Buffett Is Selling(?)

Another interesting Substack post I came across: Building up a war chest to serve as lender of 2nd to last resort when Apollo Falls

“If all this is going over your head, Burry not — for all you need to know is that this is the 2008 subprime mortgage crisis all over again. The only difference this time is that it’s happening in a different sector — rather than banks, it’s now in the Insurance sector.”

The article was a bit over my head, but maybe you folks will find it interesting. There are a number of comments on the article here from the ValueInvesting subreddit.

“Come on in, the water’s warm. “Number go down” is the name of the game throughout the U.S. corporate bond pool, with the average yield-to-worst on triple-C-rated issues tracked by Bloomberg tumbling below 10% this week for the first time since spring 2022, down more than four percentage points over the past 12 months. Option-adjusted spreads on the ICE BofA U.S. High Yield Index settled Thursday at 273 basis points, easily undercutting the 302-basis points seen in late 2021 to establish a fresh 17-year nadir.

The eroding buffer in high-grade obligations likewise leaves that cohort in rarely trod territory. Bloomberg’s U.S. Corporate Investment Grade Index compressed to a 75-basis point option-adjusted spread Thursday, half its average premium over the past two decades and the narrowest pickup since May 1998. “Spreads haven’t been this low in the career of most [investment] professionals,” Andrew Hofer, head of taxable fixed income at Brown Brothers Harriman, marveled to Bloomberg.”

The average spread for US investment-grade bonds has fallen to its lowest level since 1997.

If it's such a great trade, why are you offering it to me?

BlackRock Readies $1.3 Billion Private Credit Continuation Fund

“BlackRock Inc. is setting up a private credit loan fund that will allow it to raise as much as $1.3 billion it can distribute to existing investors…BlackRock is putting portions of about 300 first-lien loan positions into the deal, slated to be among the largest ever transfers of private credit into a so-called continuation fund, the people said, who requested anonymity because the trade is private.”

This stuff is too sophisticated for me. Maybe Blackrock is just embarrassed.

Some fun comments about this article here

‘Flood of Money’ Chases US Banking’s Hottest New Trade

“At his perch just across the river from the Federal Reserve, Neal Wilson likes to evangelize about the opportunity that the regulator is helping create for investment firms like his.

A campaign by US watchdogs to strengthen banks’ balance sheets is spurring lenders to explore creative ways to reduce risks on their books. Increasingly, they’re turning to significant risk transfers — a bit of Wall Street alchemy that shifts the first losses on loans for things like cars, commercial properties and corporate operations — to investors such as Wilson. If the loans perform well, he can reap a tidy profit…

The drumbeat of SRT deals from the likes of JPMorgan Chase & Co. down to mid-size US lenders is starting to look like the industry’s next big thing. It’s a trend emanating from deposit runs on regional banks last year and cracks in commercial real estate, spurring bank leaders to realize that balance sheets can always be a bit stronger. Another nudge came as US regulators unveiled proposals for tougher capital rules, known as Basel endgame, potentially forcing large banks to beef up buffers against losses. But perhaps most importantly, the Fed simply signaled a new willingness last year to recognize SRTs when measuring capital, making the deals a relief valve for various pressures.

…Now, when some SRT specialists look around, they see “tourists” with varying amounts of expertise.”

I don’t know - it just seems that everywhere I look the idea that conditions are “restrictive” seems to be a joke (other than perhaps housing, due to high prices).

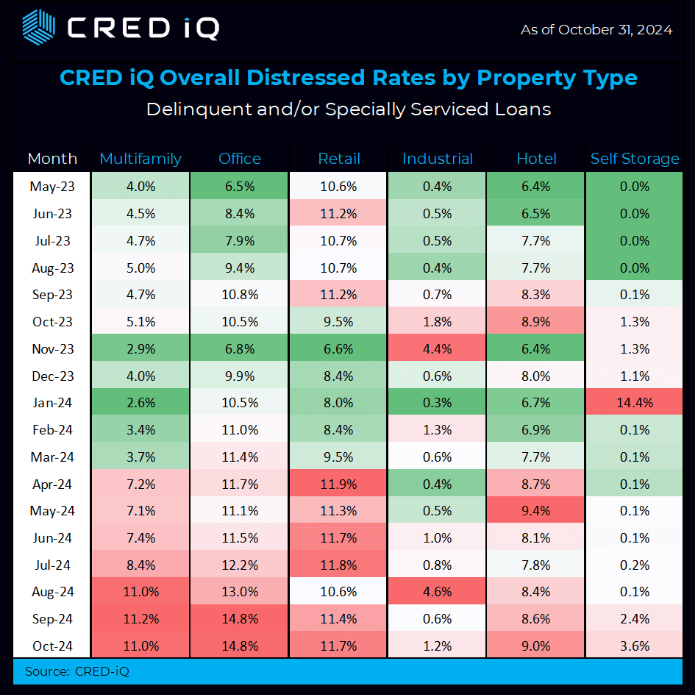

Instead of distributions, they’re getting capital calls

“The office market’s severe downturn is forcing some of the city’s multigenerational family owners to do something they managed to avoid during world wars, financial meltdowns and a global pandemic: Sell their core properties…real-estate investment banking firm Eastdil Secured says that New York real-estate families have sold about 10 office buildings over the past 24 months. In the previous decade there were fewer than five such deals. “Instead of 50 different aunts and uncles getting distributions, they’re getting capital calls””

“The Real Estate Roundtable’s Q4 Sentiment Index hit 73, marking its highest point since 2021, revealing cautious optimism among CRE execs.”

The Real Estate Roundtable’s Sentiment Index reached 73 in Q4, up 9 points from Q3, with expectations for market improvement in 2025.

The Future Index climbed to 77, its highest level since 2011, while 88% of respondents anticipate better market conditions within a year.

Asset values are expected to stabilize or go up, and the availability of equity and debt capital is improving, despite high capital costs.

Industrial, Class A office space, shopping centers, and data centers show promise, but multifamily and office deals remain challenging.

Via Grant’s:

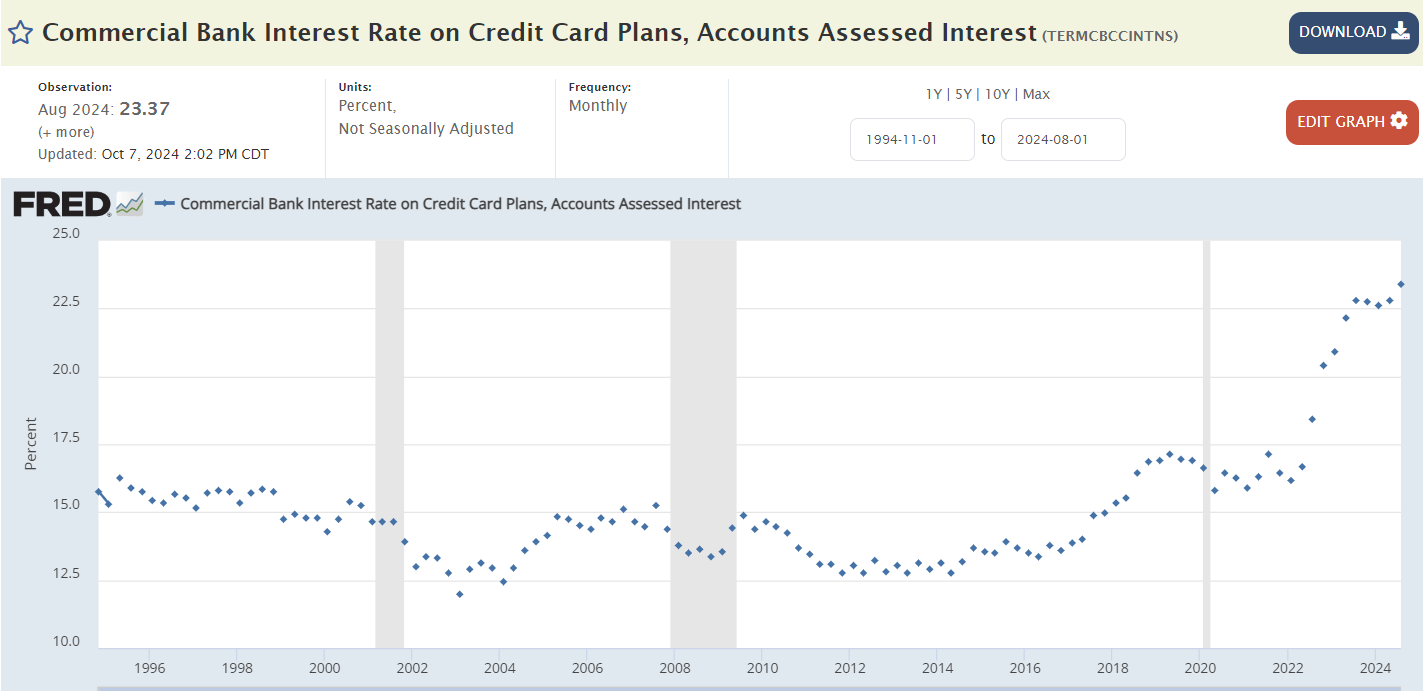

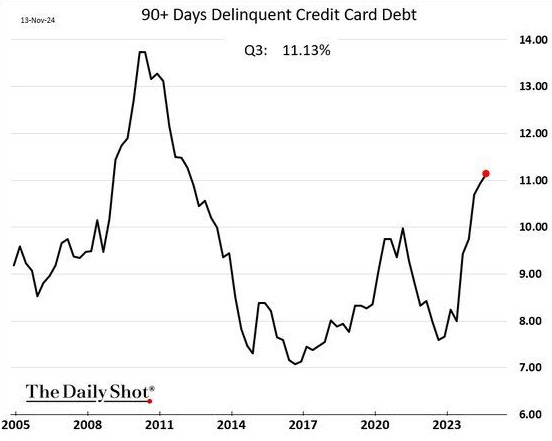

“…aggregate domestic household debt reached a record $17.94 trillion as of Sept. 30 per a Wednesday report from the Federal Reserve Bank of New York, up 4.5% over the past year to outpace the 4% uptick in nonfarm wages as measured by the Economic Policy Institute. Credit card balances reached $1.17 trillion per the New York Fed, up 8.1% from September 2023 and 26% over the past two years, while the share of serious delinquencies (meaning in arrears by at least 90 days) is nearly 12%. That’s the highest since at least 2003 outside the aftermath of the Great Recession.”

$1.17 Trillion at a (probably understated) 23.37% rate is a lot of money.

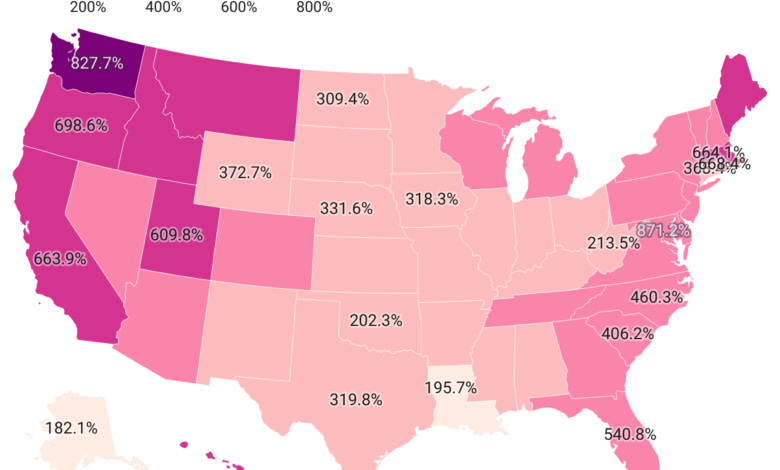

Meanwhile: U.S. State-by-State House Price Changes Since 1984

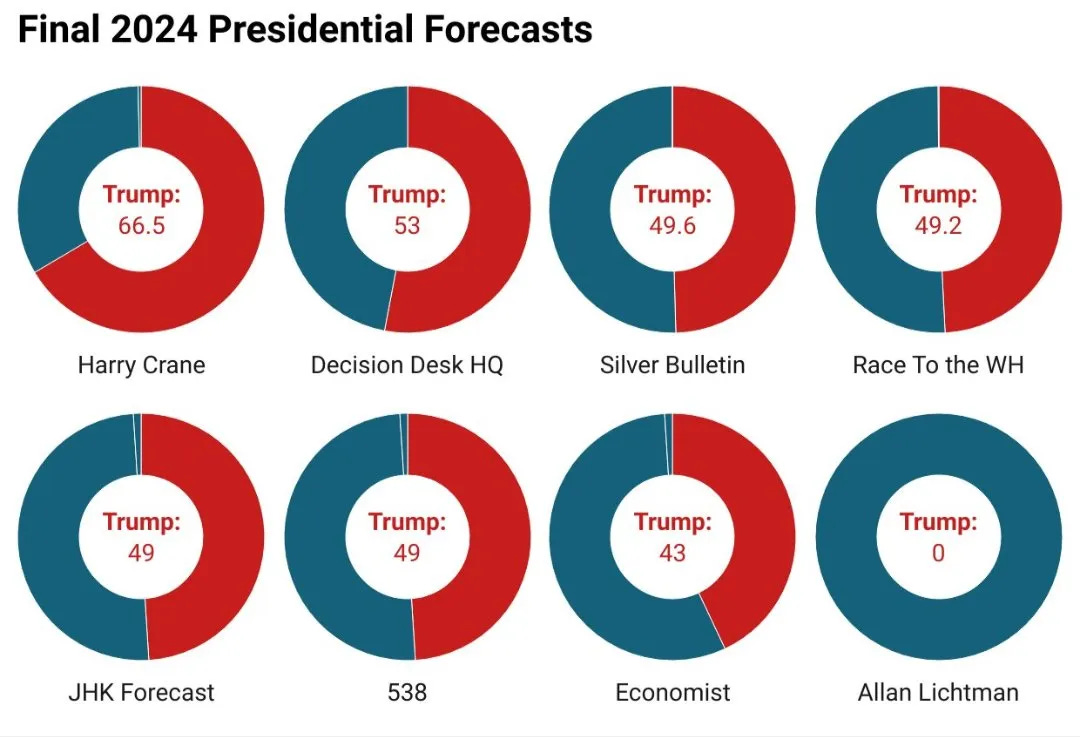

Interesting comments from pollster Harry Crane, who had Trump above 60% to win since May, and 66.5% on election day.

“It doesn't matter that I had some good calls on your [podcast], okay? I'm here to tell you that less than half of my calls are right, and that these are the kind of lessons that I'm trying to show…that's not what matters. What matters - and I didn't make this concept up, go listen to interviews with Stanley Druckenmiller… - is to minimize how much you lose when you're wrong, and maximize how much you make when you're right.”

Suing to recover billions, FTX’s receiver discloses the stunning scale of its grift — and stupidity (Generally, Michael Hiltzik is one of the worst, most insane, super-partisan guys around, but in this case I’ll make an exception)

“In the months before FTX collapsed and filed for bankruptcy court protection on Nov. 11, 2022, Bankman-Fried and his cohorts engaged in what the receivers call a “campaign of influence-buying” in which Bankman-Fried made “lavish and showy ‘investments’ ... to project financial strength and stability,” including through hundreds of millions of dollars in contributions to charities and politicians and political action committees. Bankman-Fried resigned as CEO of FTX just before its bankruptcy.

The true purpose of this spending had been “to prop up Bankman-Fried’s standing in the worlds of politics and traditional finance,” the receivers assert. Those words come from their lawsuit to recover some $67 million in investments FTX made to SkyBridge Capital, a firm headed by onetime Trump White House advisor Anthony Scaramucci.

Those investments made “no economic sense” for FTX, the receivers said. But they helped bail out Scaramucci and SkyBridge, whose cryptocurrency investments were failing. What Scaramucci offered Bankman-Fried, however, were “established financial, political, and social connections which included high-profile celebrities and wealthy investors around the world,” the receivers said…Indeed, once the investment closed, Scaramucci introduced Bankman-Fried to his contacts, including the crown prince of Saudi Arabia”

"NORTHCOM Jellyfish UAP Crosses US-Mexico Border: On USG networks, there exists FLIR footage of an irregularly shaped UAP flying across the southern border. The UAP appeared in FLIR to be ‘mottled’ irregularly with hot/cold emissions and approximated a jellyfish or floating ‘brain’ with hanging appendages in appearance. The UAP flew against the wind with no visible means of propulsion, maintained an unnatural ‘rigidity’ in its movements and flight path, and maintained a comparatively low altitude to geographic features. In appearance and behavior, footage of this UAP violating the airspace of the southern border resembled the same class of UAPs observed near DoD facilities in Iraq and Afghanistan. There exists at least one compilation video of this class of UAP, sourced from DoD force protection assets and Theater ISR, which uses this footage as a point of comparison."

Good Read on Price Level and “Inflation”

https://open.substack.com/pub/johnhcochrane/p/inflation-vs-prices?r=1z5qli&utm_medium=ios

Best read of the week Rudy, thanks.

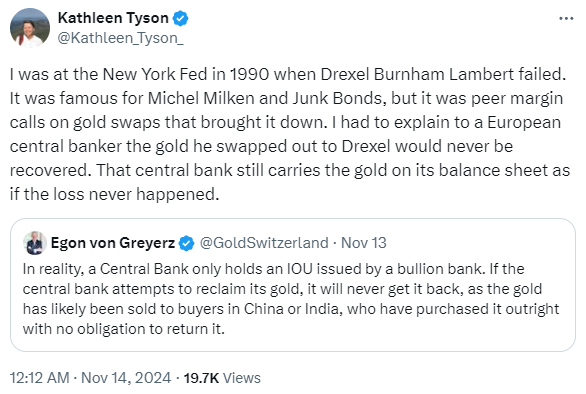

I had never heard the Gold rehypothecation story before