Almost irresponsible.

Sunday desk clearing...

Actually I have a lot more stories to go through, but one of the main reasons people unsubscribe is listed as “time.” That said, you don’t have to read every story - I’m a bit eclectic as you know - but scroll through and maybe something intrigues you.

“Ivar decided to introduce a new type of security, which he called a “B Share.” Ivar began with Swedish Match. He divided its common shares into two classes. Each class would have the same claim to dividends and profits, but the B Share would carry only 1/1000 of a vote, compared to one vote for each A Share. It was a simple, but profound, insight. B Shares could be sold to investors without affecting control. Ivar could double the size of his capital, while diluting his control by just a fraction of a percent.”

Frank Partnoy, The Match King

The Nifty 10

“The top 10 holdings in the S&P 500 now make up 30.5% of the index, the highest concentration we've seen with data going back to 1980.”

In he late 1960s and early 1970s, major institutional portfolio managers became so enamored with the idea of growth in general, and with the so-called “Nifty-Fifty” growth stocks in particular, that they were willing to pay any price at all for the privilege of owning shares in companies like Xerox, Coca-Cola, IBM, and Polaroid. These investment managers defined the risk in the Nifty-Fifty, not as the risk of overpaying, but as the risk of not owning them: the growth prospects seemed so certain that the future level of earnings and dividends would, in God’s good time, always justify whatever price they paid. They considered the risk of paying too much to be minuscule compared with the risk of buying shares, even at a low price, in companies like Union Carbide or General Motors, whose fortunes were uncertain because of their exposure to business cycles and competition.

Peter Bernstein, Against the Gods

This thought process was identical during the DotCom bubble as well (and seemingly today). A great example is the classic February 2000 Jim Cramer tome, “The Winners of the New World”:

How did this stock market get like this, to where the only people who can make a dime in it are the people who are interested in the most arcane subject, the moving of data from one space to another, via strange new machines and software? How did it get to the point where nothing else matters, most particularly the 90% of the stock market I have studied for the last 20 years? How did all of that knowledge become totally irrelevant and the only stocks that work are the stocks of companies that didn't exist five years ago and came public in the last two or three years?

If you bought the ten stocks he recommended there you got destroyed.

United States FHFA (Federal Housing Finance Agency) House Price Index

The Value of Residential Real Estate Broke a New Record $52 Trillion

OK, just some aberrant thoughts here on “value.” Say you have a neighborhood of ten identical homes. In 2019, they all sold for $100k, so the “value” of the neighborhood was $1 million.

Now in 2023, the last one sold for $500k, so the “value” of the neighborhood is considered $5 million. If one house in the next year sells for $600k, then everyone will consider the value of their house to be $600k, and the neighborhood would be worth $6 million. But is it right?

In many ways this type of “valuation” is similar to the way crypto coins, baseball cards, stocks etc. are “valued” in aggregate (although I do concede that with stocks and houses, there is some there there.)

When Dogecoin briefly hit 60 cents, could you value all outstanding Dogecoins at that value? Of course not, but people did. Any real selling drove the price down dramatically. No way all holders could get out at 60 cents, 50 cents or 40 cents. Same is true of Nvidia.

Valuing housing markets is somewhat similar. If five homeowners in the above neighborhood were to suddenly decide to sell, would they all get $500k? Maybe, but doubtful. Say one seller was desperate, and sold at $400k. Would the value of the neighborhood suddenly fall by $1 million? Just as on the way up, I think it might, in the minds of realistic sellers, and certainly savvy buyers. The next eager seller might list at $375k, and buyers might offer $350k. I saw this sort of thing during the last housing bubble. Homes would list at last year’s price, and slowly chase the market lower, finally selling at a massively discounted price (from the initial offer).

Asking Rents Down 1.2% Year-over-year

Rainier Valley homeowner lives in van while delinquent tenant lists rental on Airbnb

Jason’s deadbeat renter is listing the downstairs living space on Airbnb for $434 a night. Jason believes he is generating at least $2k a month, and possibly closer to $3k or possibly even $4k, depending on the month.

The city gave the delinquent renter a short-term rental license. A spokesperson for the city said, “…the license this individual has is not valid because it was obtained using inaccurate information about ownership of the property.”

“OK. So, not only is he not paying me, but he’s generating an income through the basement Airbnb unit, and meanwhile, I’m having to pay the utilities for that unit,” said Jason.

He’s tried to work with the renter and even came up with a payment plan, the renter signed it, paid a thousand bucks - and that’s it. Jason also tried dispute resolution, with no results. Now, he has to wait until late October for an eviction hearing. The current process for an eviction in King County is about 12 months. That’s another 12 months that Jason has to pay the mortgage on his house, that he can’t access. Before all is said and done, he is looking at $50k in losses.

Attorney Ryan Weatherstone said that King County courts are only hearing six cases per day. Half of those hearings get automatically continued for another three and a half months. So, the court is only really hearing three hearings per day and they’re only hearing it for four days a week for the biggest county in Washington.

Brutal.

Real Core Durable Goods New Orders Per Capita peaked 23 years ago.

“The Consumer Confidence Index is more influenced by employment and labor market conditions, while the Michigan Sentiment Index is more focused on household finances and the impact of inflation.”

“And finally, let's take a look at the correlation between consumer confidence and small business sentiment, the latter by way of the NFIB Small Business Optimism Index. The consumer measure is the more volatile of the two, so it is plotted on a separate axis to give a better comparison of the two series from the common baseline of 100. As the chart illustrates, the two have tracked one another fairly closely since the onset of the financial crisis. The two have diverged at brief periods and been highly correlated at others.”

Meanwhile, in Texas…

I guess other countries have stock markets too.

Bloomberg noted yesterday that the Sherman Ratio, (named after the inventor, DoubleLine’s deputy chief investment officer Jeffrey Sherman) which measures the amount of yield on offer for each unit of duration, reached a record low of 0.1968 on Dec. 31, down nearly half from the 0.3468 seen at the start of 2020. In other words, as Bloomberg’s Brian Chappatta put it yesterday, “investors were more susceptible to losses from a move higher in interest rates than at any time in history.”

Almost Daily Grant’s, January 15, 2021

Interesting overview of the RV market from an insider (from July 2023)

Podcasts

Trepp: Nowhere to Hide: CRE & CMBS Delinquencies, Jingle Mail, Dwindling Consumer Confidence Manus Clancy calls Jamie Dimon’s potential 7% Fed Funds rate call, “almost irresponsible.”

Neal Bawa on Multifamily The bull case.

Old Capital Real Estate Investing Podcast with Michael Becker & Paul Peebles A more realistic case perhaps for multifamily. “Before, as a broker, the longer a deal sat on the market, the price kept going up and up and up and up. Right now, as a broker, you want zero time on the market. You want it to go under contract right now. I think people are going to start realizing that - if there’s a good offer, they need to just take it, as a seller, and get it under contract and start the process.”

Bankruptcy Attorney: Busiest I’ve EVER BEEN "What's remarkable for us is we're seeing a lot of...lower-middle, middle-class people - that are well above the median income of California - who are just bombarded with these loans - it's something I've never seen before. We're also seeing a lot more businesses coming to us..."

Dr. Harald Malmgren and Nicholas Glinsman: The U.S. Treasury Market Is The ‘Ultimate Wrecking Ball’ "The selloff in the Treasury market, these higher rates - people say, 'oh, you know, how much more is there gonna be?' The market is massively long Treasuries, from the short-end to mid-curve to the long end! They're massively long." - Glinsman

Frank Giustra “I don’t think the West is listening. The gold enthusiasts are in the East. That’s where we see all the physical gold is going”

Demetri Kofinas with Nick Halaris Two good guys.

How America Hides the Human Toll of its Forever Wars, with Norman Solomon

GameStop, Citadel, And The Fleecing Of Small Investors | Spencer Jakab

I have not read the book, but I listened to the entire hour and a half podcast, which I suggest you do as well. A couple comments/questions I made to Mr. Jakab:

Regulation failed long before the Gamestop situation, if Robinhood was allowed to let new clients trade before they had collateral in their accounts. Clearinghouse regulators only seemed to care once some rich guys started getting squeezed. I never had a position but do have a memory.

Re: rehypothecation of shares How is it possible in 2023 that the brokerage where a buyer of shares "doesn't know" they're borrowed shorts them again (and again, and again, theoretically), leading to more shares short than the float? Regulators see no issue here?

What set me off - other than a quick comment that “he didn’t want to get into who was to blame for 2008” - was Mr. Jakab’s utter dismissal of anyone who even questioned the possibility that there may have been collusion between hedge funds and regulators as “conspiracy theorists.” He even causally compared suspicious minds to “flat earthers” and “grass knoll” types (even though he himself admitted to using anonymous hedge funds as sources for his book).

When I challenged him on these things, I got this in reply:

Ha ha.

Recently I mentioned that Mike Taylor recommended “avoiding companies tied to "under 40 mega-discretionary consumption." I believe one of his top examples of this was Doordash. Meanwhile (via Grant’s):

Delivery “platforms” in the Big Apple must fork over a $17.96 hourly wage to their couriers, the New York State Supreme Court ruled yesterday. Justice Nicolas Moyne thwarted efforts by app-based outfits Uber, Grubhub and DoorDash to scuttle the new law, which was initially set to be implemented in July before the companies, who have the option to appeal Moyne’s decision, successfully lobbied for a restraining order. Delivery staff earn roughly $11 per hour under the current regulatory regime, the city estimates.

“This is a deeply disappointing outcome for delivery workers, merchants and customers who look to our platform,” a DoorDash spokesperson said. “The city’s insistence on forging ahead with such an extreme pay rate will reduce opportunity and increase costs for all New Yorkers.” Indeed, the company (ticker: DASH) warned of “an adverse effect on our operations” from the pending law in the risk factors section of its most recent form 10-Q, noting that mandated wage hikes could lead to higher consumer prices and correspondingly weaker demand and that “we expect other such measures may be enacted in the future.”

Shares currently change hands at 59 times consensus adjusted earnings per share guesstimates for 2025.

Alongside that arguably fancy valuation comes slow but steady dilution. The outstanding count of class A common shares reached 365.8 million as of July 31, up 19% from the same period in 2021. Stock-based compensation – which is excluded from DASH’s adjusted Ebitda calculation – footed to $541 million over the first six months of the year, equivalent to 12% of revenue over that stretch and up 50% from the same period in 2022.

No position here other than the sidelines.

Alan Blinder and Ricardo Reis, 2005

No one has yet credited Alan Greenspan with the fall of the Soviet Union or the rise of the Boston Red Sox, although both may come in time as the legend grows. But within the domain of monetary policy, Greenspan has been central to just about everything that has transpired in the practical world since 1987 and to some of the major developments in the academic world as well. This paper seeks to summarize and, more important, to evaluate the significance of Greenspan’s impressive reign as Fed chairman—a period that can rightly be called the Greenspan era. It is a period that started in earnest with a frightening one-day crash of the stock market in October 1987, and included wars in Iraq in both 1990 and 2003, a rolling worldwide financial crisis in 1997-1998, the biggest financial bubble in history, an amazing turnaround in productivity growth after 1995, and a deflation scare in 2003. It is now culminating with Greenspan’s fourth attempt at a soft landing.

We do not offer a comprehensive monetary history of the period here, although we must indulge in a bit of that. Rather, our aim is to highlight what we see as the most notable contributions of the Greenspan Fed to both the theory and practice of monetary policy— and to speculate on what Alan Greenspan’s legacy might therefore be. There is no doubt that Greenspan has been an amazingly successful chairman of the Federal Reserve System. So this paper will appropriately include a great deal of praise for his decisions—and even some criticism. But our focus is not on grading Greenspan’s performance. It is, rather, on the lessons that both central bankers and academics can and should take away from the Greenspan era. How is central banking circa 2005 different from what it was circa 1987 because of what Alan Greenspan did at the Fed?

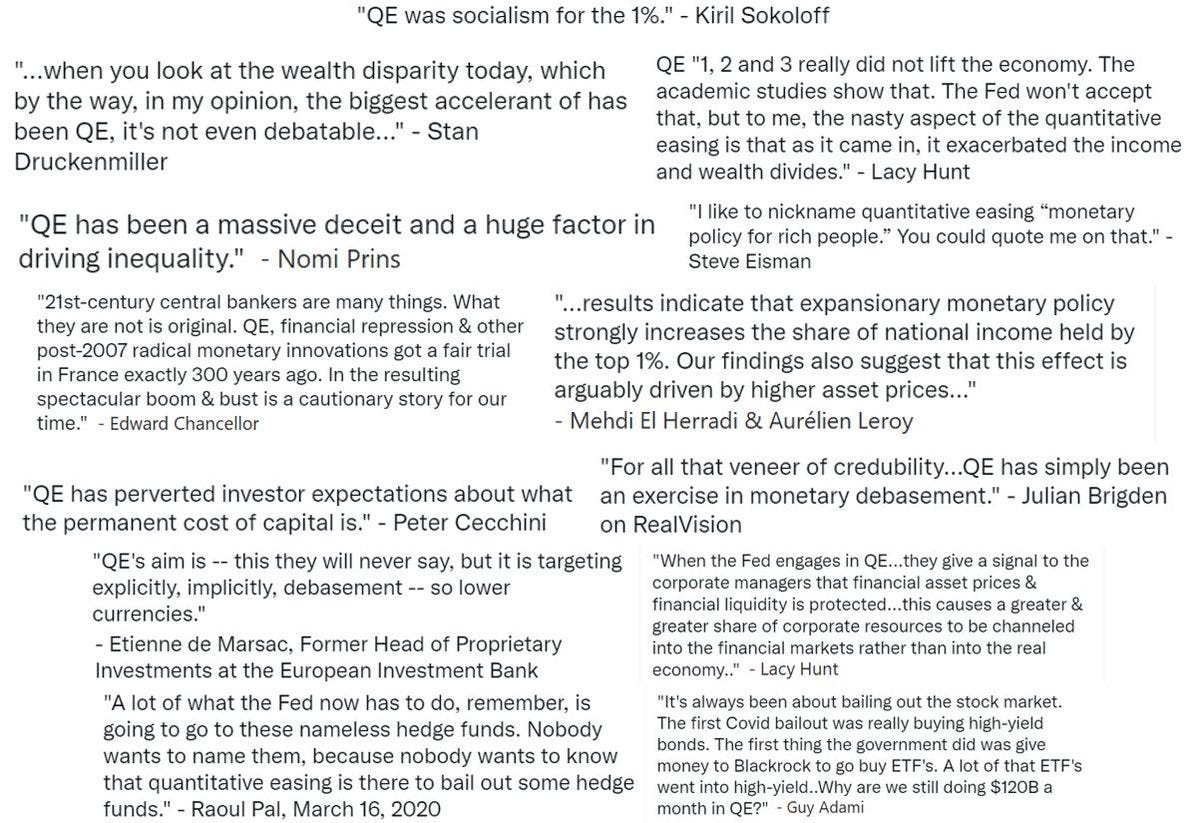

Thomas Hoenig reminiscing with David Beckworth about the ridiculous hyperbole above, among other things. Not a terrible podcast considering it’s between two economists, although Hoenig is far, far better than the clowns we currently have on the FOMC.

For example, Chris Leonard in The Lords of Easy Money, notes how Hoenig was a lone voice warning about QE:

The things that bothered Hoenig about quantitative easing were just as important to the American people as the things that bothered Williams Jennings Bryan. The FOMC debates were technical and complicated, but at their core they were about choosing winners and losers in the economic system. Hoenig was fighting against quantitative easing because he knew that it would create historically huge amounts of money, and this money would be delivered first to the big banks on Wall Street. He believed that this money would widen the gap between the very rich and everybody else. It would benefit a very small group of people who owned assets, and it would punish the very large group of people who lived on paychecks and tried to save money. Just as important, this tidal wave of money would encourage every entity on Wall Street to adopt riskier and riskier behavior in a world of cheap debt and heavy lending, potentially creating exactly the kind of ruinous financial bubble that had caused the Global Financial Crisis in the first place. This is what Hoenig had been arguing inside the secret FOMC meetings for months, his arguments growing sharper and more direct, punctuated by his dissenting votes.

As it turned out, Hoenig was almost entirely correct in his concerns and his predictions. Perhaps no single government policy did more to reshape American economic life than the policy the Fed began to execute on that November day, and no single policy did more to widen the divide between the rich and the poor. Understanding what the Fed did in November 2010 is the key to understanding the very strange economic decade that followed, when asset prices soared, the stock market boomed, and the American middle class fell further behind.

See also this December 2021 article by Leonard: The Fed’s Doomsday Prophet Has a Dire Warning About Where We’re Headed

One interesting anecdote Beckworth and Hoenig discuss - which I remember - related to a Jackson Hole meeting in 2005:

Beckworth: Then here comes Raghuram Rajan with a little dour, pessimistic, at least “let's be careful” paper. His paper was titled, *Has Financial Development Made the World Riskier?* He goes through all of the things that we now know have happened. Let me read one excerpt from his paper, and it says, "Taken together, these trends suggest that even though there are far more participants today able to absorb risk, the financial risks that are being created by the system are indeed greater. Even though there should be, theoretically, a diversity of opinions and actions by participants and a greater capacity to absorb risk, competition and compensation may induce more correlation in behavior than desirable.”

“While it is hard to be categorical about anything as complex as the modern financial system, it is possible that these developments may create more financial sector-induced procyclicality than in the past. They also may create albeit a still small probability of a catastrophic meltdown."

Boom. He called it. Now, again, this is in the context of a conference that's generally upbeat, and everything's going well, and let's praise Alan Greenspan. As you noted during these conferences, they gave a presentation. I believe Donald Kohn gave the comments, and he was reasonable. The comments from the audience were much more fierce and biting, and really strong pushback. I'm going to read the comments from two people in the audience. Here's what Larry Summers says. "I speak as a repentant, brief Tobin tax advocate and someone who has learned a great deal about this subject like Don Kohn from Alan Greenspan, and someone who finds the basic, slightly Luddite premise of this paper to be largely misguided." He comes out swinging. Then later Alan Blinder comes and says some nice things. But there was a lot of pushback against this paper. Tell us about that moment.

Hoenig: I remember the moment well. It was in some ways stunning, because it was a very caustic comment on the part of Larry. People were surprised by it. It usually didn't happen at that symposium. Now, Larry was in the administration, I believe. He was not only defending, I guess, Alan at the time, but others in the administration as well. It really was not well-received, I think, by many in the audience. In fact, I think it was the next year or maybe it was even two years later after everything had blown up that one of the participants at this particular conference got up and reminded Larry and others that Raghu Rajan had made these comments and they chastised him for it. It seemed that maybe Raghu was right and some others were wrong. Some of the comments were that Larry is often wrong but never in doubt. I think it came back, as it should have, on Larry, because what Raghu said was thoughtful. It wasn't caustic. It wasn't overly critical. It was merely saying, "I wonder if--," and I would say not unlike a comment that Greenspan made years before in terms of irrational exuberance. It was appropriate to say it and [it was] part of what we wanted in the conference, and that is opposing views. It was a moment of, shall we say, interesting outcomes.

Beckworth: For sure. It will definitely will go down in history as one of the great moments of the Jackson Hole Symposium.

Charles Ferguson describes it a bit more floridly in his excellent 2010 article, Larry Summers and the Subversion of Economics:

Summers remained close to Rubin and to Alan Greenspan, a former chairman of the Federal Reserve. When other economists began warning of abuses and systemic risk in the financial system deriving from the environment that Summers, Greenspan, and Rubin had created, Summers mocked and dismissed those warnings. In 2005, at the annual Jackson Hole, Wyo., conference of the world’s leading central bankers, the chief economist of the International Monetary Fund, Raghuram Rajan, presented a brilliant paper that constituted the first prominent warning of the coming crisis. Rajan pointed out that the structure of financial-sector compensation, in combination with complex financial products, gave bankers huge cash incentives to take risks with other people’s money, while imposing no penalties for any subsequent losses. Rajan warned that this bonus culture rewarded bankers for actions that could destroy their own institutions, or even the entire system, and that this could generate a “full-blown financial crisis” and a “catastrophic meltdown.”

When Rajan finished speaking, Summers rose up from the audience and attacked him, calling him a “Luddite,” dismissing his concerns, and warning that increased regulation would reduce the productivity of the financial sector. (Ben Bernanke, Tim Geithner, and Alan Greenspan were also in the audience.)

Soon after that, Summers lost his job as president of Harvard after suggesting that women might be innately inferior to men at scientific work.

Sorry to hear that “time” is an oft given reason for unsubscribing. The world is an eclectic place. There are no shortcuts but many distractions.

"Grass knoll" types turn out to be right about the JFK assassination. The details about the four shooter teams are in my friend Alan Kent's book. Coup in Dallas with HP Albarelli and others.