"I learned that my assets were ephemeral, while my debts were money-good." - Rick Rule

"Nothing’s more socio-politically destabilizing than inflation.

And we’ve had a lot of inflation. We just haven’t measured it."

Dave Dredge, October 2021

There is one thing they teach you in mortgage default land….the cross from 30 to 60 days is the death-cross, and May’s increase was significant. Black Knight’s data should be out next week, so I will use it to confirm how systemic this might be and then share the %s because they were just that large….and I’m still of a bit of a perfectionist :).

Why is the cross from 30 to 60 so bad - it’s just 30 days, you say? It’s the decision that’s made by the borrower to let it happen…in the U.S. we are obsessed with credit scores. When you let that payment slide to Day 31, you are giving up on your credit score as most know that your delinquency gets reported after day 30.

Now I’m not saying we are about to have a million foreclosures tomorrow. I recommend you check out my deep dive on loss mitigation to understand it could be a year before we see serious foreclosures and longer in some states. But what I’m seeing is SEVERE consumer stress. How do I know it’s severe? Part of my methodology is to sample the comments from borrowers that come through the call centers, and folks are reeling from tax season….reeling.

As I talked about in previous posts delinquency was starting to get severe in December, but then most people were able to catch up in bonus and tax season as is typically the case (not for autos though). I guess when we realize the new debt-to-income reality of these borrowers we should not be surprised, but during the boom time many forgot that it isn’t just the credit score that matters - it’s important to dive under the score. My plan is to spend a good deal more time talking about this when the Black Knight report gets published likely next week, so stay tuned.

“Adam Rozencwajg of Goehring & Rozencwajg shares his thoughts on where gold is at in the current cycle and what could be next.”

MacroVoices #381 Leigh Goehring: Global Food Crisis Update (I have a position in Adam and Leigh’s GRHAX mutual fund. They do good research. Caveat emptor.)

2021 was an environment where we saw, instead of late-cycle, closer to early-cycle behavior, where, because interest rates were so low, and that was creating a boom in the stock market, we had really very lax lending standards, record new issuance - that’s typically when mistakes happen, that’s typically when there is little variation in the pricing of risk, and that’s the period where you build up risk and you pay for it later. That can be in valuation, but it’s also in structure, it’s in the types of companies that get financed. Now you fast forward to today, weaker companies don’t have access to capital, so the market is very discerning concerning credit. Mistakes that were made in 2020-2021 you’re starting to see the outcomes of those here in 2023…

The Big Names That Got Backstop for Billions in Uninsured SVB Deposits

The decision to guarantee all accounts above the $250,000 federal deposit insurance limit also helped bigger companies that were in no real danger. Sequoia Capital, the world’s most prominent venture-capital firm, got covered the $1 billion it had with the lender. Kanzhun Ltd., a Beijing-based tech company that runs mobile recruiting app Boss Zhipin, received a backstop for more than $900 million.

"The bailout really did protect billionaires from taking a modest haircut"

Been hearing a lot about Debt Service Coverage Ratio (DSCR) loans. These loans look “at the cash flow generated from an investment property to qualify for a mortgage instead of personal income.”

I found an interesting discussion with a poster who seemed to know what they were talking about. Caveat emptor.

“DSCR Loans” are a specific product designed for 1-4 unit Resi assets, but can go up to 10-units. General characteristics are asset cash flow based underwriting with no tax returns or “global” cash flow run on the sponsor.

11+ unit deals follow standard CRE lending suite, typically small balance commercial, local banks, or (depending on size) DU lenders. All those products will look at asset DSCR as a component of underwriting, but also consider booked tax figures for both the asset (if refinance) and personal taxes for a “global underwrite” to make sure the sponsor ability repay expands a bit beyond just the asset itself. DSCR of the asset does, generally, carry most weight but net worth and liquidity are far more important for a CRE loan than a “DSCR” loan. DSCR loans are where only a few months of PITIA and decent credit are required on the sponsorship side...

Q: So large cre is expected to be covered by personal net worth?

“CRE loans are underwritten holistically. I underwrote for an Austin based small balance commercial lender ($500k - $20mm loan sizes) and, on a $1mm loan for example, the core “bases to cover” are:

1.20x asset DSCR

1.00x+ global DSCR on sponsor

net worth of 2x loan amount (down to 1x loan amount if the asset is great or cash flows exceptionally well)

verified liquidity for down payment + 6-12 month PITI [Principal, Interest, Taxes, and Insurance]

There are many more pieces to underwrite like verified rent receipts, estoppels, etc. on the tenant side but loosely speaking those are four larger hurdles.”

…We’ll look at booked tax forms Schedule E (or a P&L if taxes not yet filed) for those assets, back out interest or depreciation and make sure they’re positively cash flowing globally. If a sponsor has a “loser” on their books negatively cash flowing, it will not necessarily kill a deal since other assets positive income (and personal income from W-2) can offset globally.

Again to be clear none of this exercise is done for a “DSCR Loan”, the non-QM [Qualified Mortgage] Resi product. This type of UW applies to CRE deals on Resi, office, industrial, mixed use, mobile home parks, retail, etc.

Google:

“There have been 46 applications for bank branch closures in Massachusetts since the start of the year—and 33 are from Santander Bank.”

The Spanish bank entered the retail and commercial banking business in the United States in 2010 with the acquisition of Sovereign Bank. In October 2013, Sovereign's name was changed to Santander.

Miami-Dade’s housing market sets price record, bucks national trend of deflating prices

Compared to the rest of the country, South Florida also saw a much higher percentage in May of home purchases that closed with cash. Nearly 41% of home transactions last month were cash deals in Miami-Dade and Broward counties, considerably higher than the national average of 25%.

Manhattan Multifamily Loan Hits Special Servicing

A $195.8 million commercial mortgage-backed securities (CMBS) loan on A&R Kalimian Realty’s The Aire luxury apartment tower on Manhattan’s Upper West Side has transferred to special servicing despite a large occupancy recovery following a big dip during the height of the COVID-19 pandemic.

…The outstanding debt, which is split between the JPMCC 2013-C16 and JPMCC 2013-C17 conduit deals, is facing “imminent” default ahead of its November 2023 maturity date…

The Aire saw occupancy drop to 70 percent from 97 percent in 2020 before rebounding recently back to 97 percent, according to Trepp. The property’s debt service coverage ratio net cash flow has remained under 1.0x since 2017 after bottoming out at 0.36x in 2017, according to Trepp. It was 0.84x in 2022.

“The property was certainly impacted by the pandemic, but cash flow issues were evident pre-pandemic”…

The property was valued at $365 million at the time of the CMBS issuance in 2013, according to CRED iQ.

From everything I’ve read, doing this is almost prohibitively expensive - i.e., these won’t be “affordable” units without massive public subsidies - and there are a variety of other issues…

"The subsidized rent they're talking about doesn't cover those truly in need of housing, and this is a bad location for lower-income housing due to lack of green space and parking. Grant Park isn't that close, and there are no other 'pocket parks' nearby. There are no supermarkets within walking distance or easy transit access. They're all south or west. And there's a lack of consumer retail."

Even if the units were marketed to higher-income tenants, the resident still sees a problem. "Who's their target market? There's plenty of competition and better offerings for residential space relatively close by in the West Loop, South Loop, River North, and River East for those paying the market rates. The mid and higher earners who work in nearby businesses and industries that are still in the CBD can afford the competitors and get much better space for their money."

The Myth that Drives Private Equity

The narrative is not that alternatives always perform well, or indeed better than traditional asset classes. Nor is it that alternatives investment benefits only ordinary workers. Yet it is the latter that Blackstone and its peers invariably highlight. When, for example, skeptics question why the trustees of pension schemes persevere with high allocations of retirement savings to alternatives funds such as those managed by Blackstone, they are told that reducing such allocations will hurt ordinary workers most. And so the status quo persists.

This narrative is profoundly misleading, however. To say this is not to suggest that ordinary workers do not benefit when the funds in which their retirement savings are invested perform well. It is to argue rather that the benefits accruing to such workers are minor, both in relative terms (most benefits are captured elsewhere) and absolute terms. Thus, to center and highlight specifically ordinary workers among the cast of beneficiaries is to grossly distort reality.

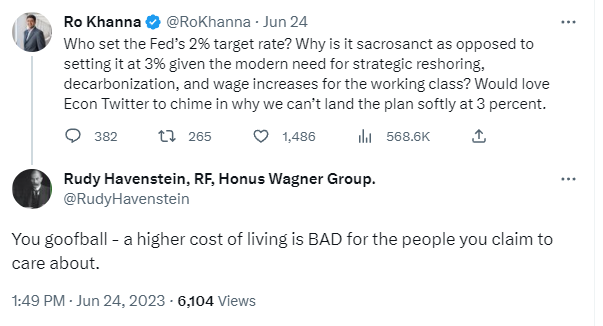

They mention Ro Khanna in the article. I noticed him again the other day:

An amazing number of otherwise smart people seem to think inflation is good for poor people, or something. They usually only say this around rich people though.

Another one I had an exchange with, Dean Baker talking about the BLS CPI math model:

Your income is never hedonically-adjusted. I can’t help Dean.

Digital currencies can be programmable by being assigned functions to operate only under certain conditions. This could eventually lead to an economy controlled by the government at an individual level. The government would be able to monitor its citizens, determine how money can be limited and used, identify political dissidents and take action against them.

The Canadian government has already proved it is willing to use financial tools against protestors.

Moreover, centralized digital infrastructures are inherently vulnerable to software updates that could override initial safeguards. Issuing a central bank digital currency may be a point of no return.

Fed Governor Michelle Bowman, talking about the recent Fed report on bank failures by Michael Barr:

In my view, a necessary next step is to engage an independent third party to analyze the surrounding events of the recent bank failures to fully understand the factors and circumstances that contributed to the recent bank failures and to the ensuing stress in the banking system….much of this work was prepared internally, by Federal Reserve supervision staff, relying on a limited number of unattributed source interviews, and completed on an expedited timeframe with a limited scope. [Foxes reporting on mysterious chicken deaths? - RH]

Although the report was published as a report of the Board of Governors, it was the product of one Board Member, and was not reviewed by the other members of the Board prior to its publication. Troublingly, other Board members were afforded no ability to contribute to the report's content. There is a genuine question whether these efforts provide a sufficient accounting of what occurred. A supplemental, independent review would help overcome the limitations of scope and timing of these initial efforts, and address concerns about the impartiality and independence of the reviews.

More on Michael Barr, Fed Vice Chair for Supervision:

During Dodd-Frank, Barr wrote the initial Treasury blueprint for financial reform and served as a key liaison between the White House and Congress. Reformers argue that Barr backed up his boss Timothy Geithner at every turn, persistently seeking to weaken the bill. He publicly opposed tougher derivatives regulations, like forcing banks to spin off their trading desks. And former FDIC Chairwoman Sheila Bair writes in her book Bull By the Horns about Barr trying to water down provisions like the Volcker rule, and add loopholes that would allow for future bailouts of financial institutions.

Greg Weldon was talking a bit about Turkey recently. They just raised their minimum wage to 11,402 Lira per month, a 34% jump. Their minimum wage is up 100% in the past year. to about $483 dollars per month.

Not quite a currency collapse, but getting there. Turkey, a very strategic country, ranks about 18th in world population, ahead of Germany, the UK and France.

"Historians write about inflation in a very different way than economists.

Historians view inflation as a destabilizing force, whatever the cause."

This is for future historians:

I’m used to hearing this.

I remember 2015, when gold was around $1100…

And this was a gem: "Who Needs Gold When We Have Greenspan?" May 4, 1999, Gold price: $287/oz.

"There would be a universal money whose value was based not on gold in the vaults, but on the wisdom of Mr. Greenspan and his successors at the Federal Reserve."

- Floyd Norris

If I cherry-pick Jan. 1, 2000 as the starting date, gold has actually slightly outperformed the S&P 500. I bet you very few CNBC guests would know that.

In late 1999, in under 6 months, the Nasdaq composite went up over 80%.

“You goofball” hahaha.

Ro loves the fun coupons + inside info so he and his wife can get rich playing the stock market.