Everybody's Lying

The Hunger Games

Here’s your weekend beach reading.

Lots of wisdom below (not from me).

“Goethe wisely said, ‘in the general throng, many a fool receives decorations and titles.’”

- Stefan Zweig, The World of Yesterday

Good Riddance, Alan Greenspan

“a story from a finance professional prominent enough to be regularly invited to Economics Club of New York talks:”

One time, when I was on the last shuttle flight from Washington DC to New York, Greenspan was on the same plane. I debated whether I would be willing to die in a crash if it killed Greenspan too. I quickly concluded “yes”.

“As we explained long form in ECONNED, the 2008 crisis was not a housing crisis but a derivatives crisis of instruments that referenced particularly risky subprime exposures. The entire subprime market was not big enough to produce more than at worst something a big nastier than the saving & loan crisis, nor a near failure of the global financial system. But credit default swaps and CDO composed heavily of CDS referencing BBB-subprime tranches created exposures of 4 to 6 times the real economy value and concentrated them at systemically important, overleveraged financial institutions.

And Greenspan’s pathological neglect and the systemic effects greatly predate the famed row of Greenspan and Treasury Secretary Bob Rubin against CFTC chair Brooksley Born over regulation of credit default swaps, with Born lost. Greenspan ushered in the widespread use of derivatives which are used almost entirely for speculation, thus diverting resources and “talent” into socially destructive activity. And as we will soon explain, the explosive growth of over-the-counter derivatives markets was a major driver of demand for securitized products.”

From The Big Short:

“Steve Eisman finally understood the madness of the machine. He and Vinny and Danny had been making these side bets with Goldman Sachs and Deutsche Bank on the fate of the triple-B tranche of subprime mortgage-backed bonds without fully understanding why those firms were so eager to accept them. Now he was face-to-face with the actual human being on the other side of his credit default swaps. Now he got it: The credit default swaps, filtered through the CDOs, were being used to replicate bonds backed by actual home loans.

There weren’t enough Americans with shitty credit taking out loans to satisfy investors’ appetite for the end product. Wall Street needed his bets in order to synthesize more of them. “They weren’t satisfied getting lots of unqualified borrowers to borrow money to buy a house they couldn’t afford,” said Eisman. “They were creating them out of whole cloth. One hundred times over! That’s why the losses in the financial system are so much greater than just the subprime loans. That’s when I realized they needed us to keep the machine running. I was like, This is allowed?””

Something to think about

Right now, there are nine companies in the S&P 500 with market capitalizations over one trillion dollars: NVDA, AAPL, GOOGL, MSFT, AMZN, AVGO, TSLA, META, and MU. (SpaceX has not been added to the index.) These nine trade for 32 times earnings and throw off a 1.5 percent free-cash-flow yield on enterprise value. (All free-cash-flow figures here are net of stock-based compensation.)

We were wondering whether you could hide from this overvaluation elsewhere in the S&P index. The first, obvious thought would be to skip the top nine and own the other 491. They trade for 27 times earnings and throw off 2.6 percent on the same basis. Cheaper, but still expensive.

So we looked at various ways of slicing up SPY. We screened out every company with meaningful stock-based compensation, on the theory that the companies paying employees in stock also have the most overvalued shares. (This line of thought actually gave us a good Apple entry point in April 2024.) The low-SBC survivors yielded 2.1 percent, worse than the index, because the screen mostly caught the bid-up defensive complex: utilities, staples, telecom, the names people own for safety. We tried another screen, keeping only the companies that have shrunk their share count over the past five years. That group was the best of the lot at 3.2 percent, but it is not a number worth writing home about.

Put the four cuts together and the ladder of free-cash-flow yields runs from 1.5 to 3.2 percent of enterprise value. None of them are “cheap.” Unfortunately, the 491 are not a bargain hiding behind the nine. They are slightly lower-quality businesses, on average, at a quality-adjusted price that is roughly the same. There is no secret cheap slice in the index, because the index as a whole is pretty expensive on the cash that actually reaches an owner.

One option would be to sit in cash and bonds and wait. If the correction doesn’t come in a year, you’ll be rooting for the world to end. Also, the U.S. federal debt to GDP and the deficit are both high enough that the government will be sorely tempted to inflate its way out, and a government that wants inflation usually gets it. In that world, cash and bonds hand you a negative real return after tax.That is the box. Stocks are expensive, but bonds are expensive too. We need a “third way.”

There are two ways for a good business to slip through the cracks and be excluded from the passive, indexation bid. One is structure: a master limited partnership or other pass-through cannot go into the index, because the funds that track it cannot hold those companies without tax problems. The other is size: a company too small to move the index gets no meaningful flows. Either way the price is set by people doing valuation arithmetic rather than by a machine that has to buy. These have been called “orphaned securities.”

"Debt doesn't dilute shareholders." - CNBC spokesmodel

No, but it can supplant them.

“The single act of freezing some $600 billion in Russian sovereign reserves sent a message to every central bank in the world: dollar reserves aren’t sovereign. They’re hostages, and you hold them at the pleasure of an increasingly capricious Washington.”

Grant Williams, 2022

“Iran doesn’t need a nuclear weapon any more. They have a weapon. It’s called the Persian Gulf Strait Authority.”

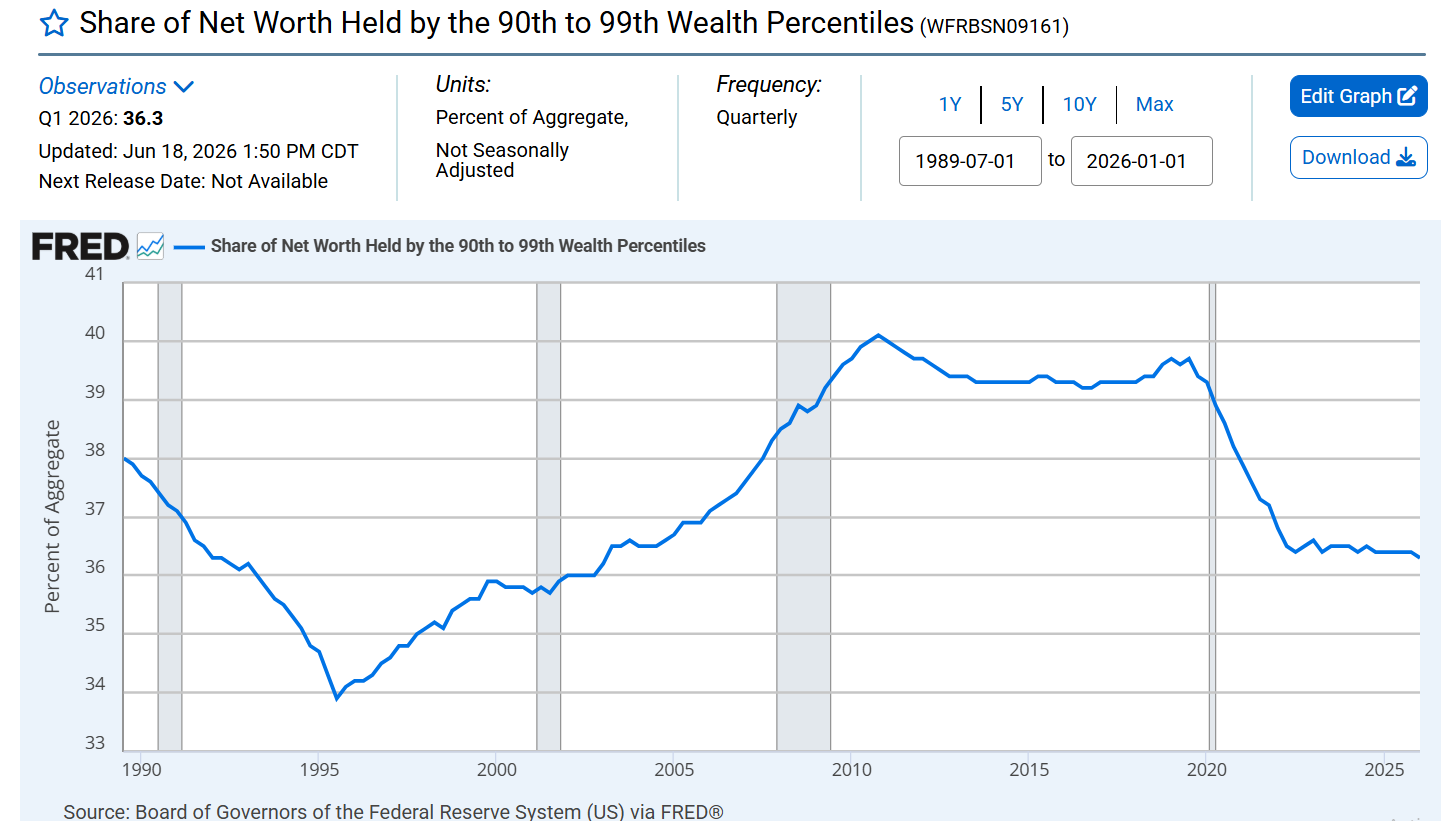

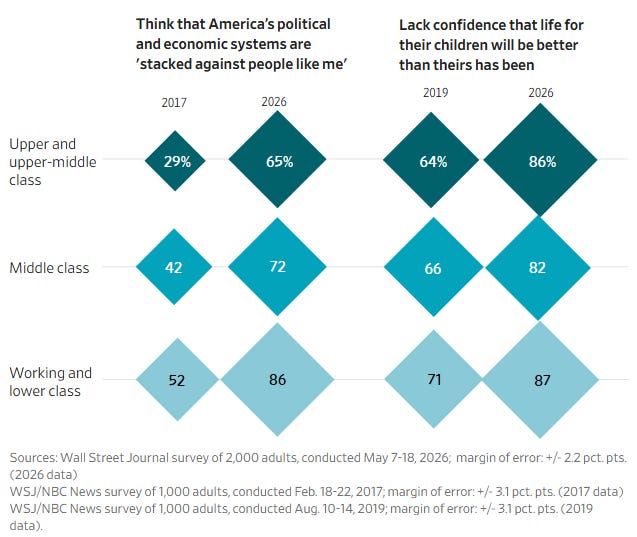

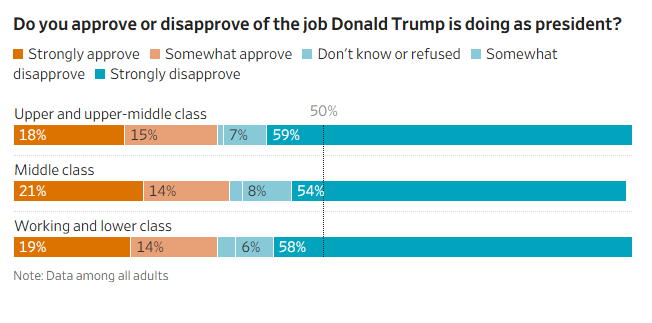

America’s Economic Anxiety Is Rising Up the Income Ladder

…More than 40% of Americans who call themselves upper class or upper-middle class say they haven’t saved enough money to retire comfortably. Only about 40% say their financial security is where they thought it would be at this point in their lives. Nearly three in five say they are strained by high gasoline prices.

Those in the wealthiest classes have lost faith that an economy that has benefited them can lift future generations. Some 86% of people who call themselves upper class or upper-middle class say they lack confidence that life for their children will be better than theirs has been. That’s up from 64% in a 2019 survey and shows a level of pessimism that matches the views of less-fortunate groups.

And 65% in the most affluent classes say America’s political and economic systems are “stacked against people like me.” That’s a remarkable statement by the nation’s most privileged groups and a substantial rise from 29% who saw a rigged system in 2017. Many surveys have found that economic optimism, long considered a core American trait, has given way to a pervasive unease…

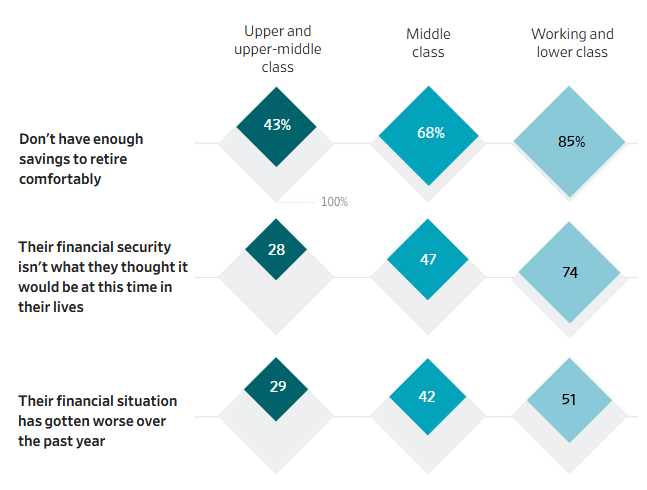

Among middle-class respondents, only about one in four said they made enough money to save for anything beyond emergency expenses, had enough to retire comfortably and had achieved the level of financial security they expected at this point in their lives. Roughly the same share said they have credit-card debt they cannot pay off each month.

“…Pessimism about the economy in recent years has puzzled many economists…”

“The Wall Street Journal poll surveyed 2,000 adults from May 7-18. The margin of error for the full sample is plus or minus 2.2 percentage points.”

Via Grant’s:

…Average new vehicle transaction prices registered at $48,402 last year, a Wednesday report from Edmunds revealed, up 30% since 2019…The market share of vehicles priced at $60,000 and above topped 20% last year, triple its 2019 levels. In turn, only 4.7% of inventory changed hands at or below $25,000 in 2025 versus 21% within that range six years prior.

“Not long ago, walking into a dealership with $25,000 in hand meant you had real options in the new-car market,” the Edmunds team related. “Today, it means you’re largely out of luck.”

More than five million open U.S. auto loans and leases sported monthly payments of at least $1,000 during the first quarter, Experian Automotive found late last month, equivalent to 19% of the total. That compares to 17.4% four-figure payments in the first quarter of 2025 and just 5.4% five years ago.

“The assumption is that it’s all luxury, it’s high-line, and that is not the case,” Melinda Zabritski, Experian’s head of automotive financial insights, told CNBC. Indeed, workaday models such as the Ford F-150, Chevy Silverado 1500 and Ram 1500 pickup trucks account for 74% of the $1,000-per-month cohort.

“You could divide restaurant spending into three buckets, each by income cohort. Under $50,000, $50,000 to $100,000, $100,000 up. And those are equal thirds, which is pretty remarkable. A lot of people are taken aback by that because they think that seems rather low income to be honest with you.”

Restaurant Analyst David Palmer

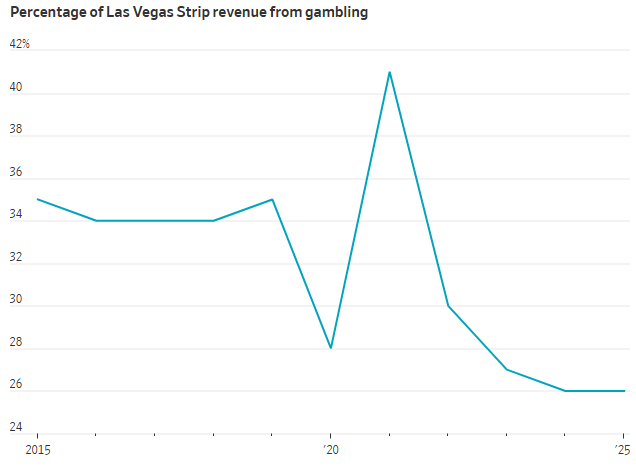

Vegas Was Once America’s Bargain Vacation. Now It’s a Luxury Destination

A trip to this desert city once meant dirt-cheap hotel rooms and buffets, all subsidized by gambling revenue. Now visitors organize their trips around big-ticket events—and pay top dollar for everything else while they are in town.

Postpandemic Las Vegas is built to cater to the well-off. Hotel rates have risen faster than in any other major market in the U.S. New venues are drawing visitors to town for pro football, concerts and Formula One racing. A $26 bottle of water went viral last year.

Not long ago, lower- and middle-income families and young partyers on tight budgets made up most of the visitors to Las Vegas. In 2019, 28% of visitors lived in households earning six figures, according to the city’s visitors authority. Last year, 75% were in that income bracket.

Starting in the 1990s, Ed Schaplow, who lives in Chelan, Wash., visited Vegas twice a year, once for work and once for fun. He runs three small businesses, including a fruit farm. He and his wife could put together a five-night trip, including flights, meals and multiple shows, for under $1,000.

Their last visit was in 2023, when they stayed at the budget hotel Circus Circus. Even then, Vegas was starting to become out of reach. Schaplow was surprised by the hotel’s resort fee (now $45 per night plus tax) and the high cost of everyday items across the city. They could afford only one performance, a little-known act at a casino.

The couple looked into visiting last fall but were deterred by the prices for airfare and hotel. “We just wrote it off as it’s not worth it,” Schaplow said.

Las Vegas usually reflects the American economy—and then some. Few places were hit harder by the 2008-09 financial crisis or the early Covid lockdowns. The city rebounded thanks to the YOLO travel-and-spending boom that followed.

Now Las Vegas, like the economy more broadly, is increasingly dependent on spending by a smaller group of well-off people who are often invested in the booming stock market.

I’d been going to Vegas since I was 18 with a fake ID. It was a far better place when the mob ran it. Soulless greedy corporations destroyed it, except for the Epstein class and the wannabes.

David Dredge

“The risk is actually the leverage…the risk is hidden in the leverage, it is hidden in the flawed accounting methodology.”

“The whole banking system and their zero risk-weighted assets, and hold to maturity, no mark to market, no impairment of capital so they could pay themselves bonuses on an annual basis, destroying value. I mean, the unrealized losses in the banking system on sovereign debt are just astronomically large. The insurance industry the same way, where Solvency II forced them to own more and more duration, right? A super long-dated government bond required less risk capital than holding cash. It was less risky than holding cash by the concept there, and again this accounting treatment of liability driven investments and risk-parity type strategies where leveraging bonds inside pension funds were risk reducing. And that all went on while interest rates were forced to zero and below. That was the peak. $17 trillion dollars of negative yielding debt at the peak? Madness.

And so these people who were buying all these bonds are what I call rational accounting man. They’re not rational economic man as exists in the mythical world of Sharpe world economic models. They’re rational accounting man. They’re not making decisions about investing their own wealth and capital for their retirement. They’re following regulatory rules and very short-term compensation incentive structures and zero-risk weighted assets and no mark-to-market accounting and FX reserve mandates and monetary policy mandates and all that, until virtually the entirety of the volume in government bond markets was rational accounting man. It was all passive non-price sensitive because otherwise who would own them at zero and negative yields? No individual would. And then that created this massive distortion in bond markets that…we’re in this sixth year of trying to figure out how to clean up. And that’s literally what’s going on day in and day out in the markets right now. It’s still this problem of this overhang of all this dead capital tied up in box.”

“There virtually is no capital behind the bond market, right? The central banks are all insolvent on the unrealized losses. The banks all have massive unrealized losses. Silicon Valley Bank most famously went out of business owning zero-risk weighted assets, you know, just, you know, fully regulated, fully compliant with all their capital rules and 100% insolvent, right? So that’s prolific throughout the whole financial industry.

And so this is why - and you go all the way back to March 2020, all of the big interventions in recent years - well really go back to 2018, go back to 2019 - all of the big interventions have come because of the fragility of the bond markets. So when the Fed stepped in in the third week of March 2020, was it because the equity markets had been melting down for four weeks at that point? No, because the bond market started melting down. And likewise, when Trump taco’d after the tariffs last year, it wasn’t because the equity markets were going down. It was because the bond market started to melt down. And when Trump ceasefired this time around, wasn’t because the equity markets were melting down. It was because the bond market started melting down. And so, in a sense, the fragility of the bond market has been the best friend of the equity markets.”“In the financial industry, we measure risk as the frequency of fires. We say the longer we’ve gone without a fire, the less risk there is, which is the exact opposite.”

“QE, as we’ve learned, if it doesn’t work, you have to do more. And if it does work, you have to do more.”

“In Germany and in Northern Europe, the bulk of pensions were in bonds and levered in bonds through risk parity and liability-driven investment structures. The retirement for those people’s savings since 2022 has just been destroyed. Meanwhile, inflation price level keeps going higher and higher and higher.”

From The Big Short:

Vinny: It’s zero-sum. Who’s on the other side? Who’s the idiot?

Lippmann: Dusseldorf. Stupid Germans. They take rating agencies seriously. They believe in the rules.

Vinny: Why does Deutsche Bank allow you to trash a market that they sit at the center of?

Lippman: I don’t have any particular allegiance to Deutsche Bank...I just work there.

Vinny: Bullshit. They pay you. How do we know the people running your CDO machine aren’t just using your enthusiasm for shorting your own market to exploit us?

Lippman: Have you met the people running our CDO machine?

“Economies don’t drive markets. Markets drive economies. Markets don’t crash because we had a recession. We have a recession because markets crash, and the market crash destroys the purchasing power of the wealthy who own all the assets, and that causes a recession. And so everything’s now downstream of the market.”

“Because the bond market’s dying, they’re going to play the same game that Janet Yellen played back in 2023, and stop issuing duration bonds, because the banks were screaming we’re full, and they just issue bills. And of course Scott Bessent criticizes Janet Yellen for doing that, until he takes her job and he does the exact same thing.”

Germany is “an aggressive issuer of bonds. The EU is an aggressive issuer of bonds. So the EU that was never going to issue bonds, just kind of referee everyone else’s bond issuance, is now issuing bonds. They’re now competitors with France and Japan.”

“The best answer is that they find a market-clearing price where actual capital owners are willing to buy the bonds. I have a bad feeling that to get to that

price, all the current bond holders who own them with leverage and no capital go out of business.”

“The 1995 to 1999 era, and my memories of that being such a unique period where in particular US equity markets went up up so the S&P 500 was up five years in a row. 28.6% CAGR for five years 28.6 over five years, and the whole world blew up, right?”

“The capital controls I think are coming. We’re already seeing hints of them in these comments from Reserve Bank of India, and Rachel Reeves announced

that she’s going to subsidize British tourists’ local amusement park costs this summer, but cover the cost of that by raising taxes on airplane tickets. So think about that. She’s literally now intentionally disincentivizing holiday abroad, and incentivizing holiday domestically, right? That’s in a sense a form of a capital control.”

“The last time it was, in my mind, attractive to own bonds was sort of December 1999, January 2000. The 30-year bond was getting close to 7% yield. And then people said, you know what, at these valuations of equities, you worked

out the equity risk premium relative to that yield, I’d rather own bonds now. And then you went through a very long period, 85% decline of the NASDAQ. And owning those long-dated treasuries at six and a half, 7%, you know, through the GFC was probably not a such a bad idea. So maybe we have to get there again. We have to find a level of interest rates that people say, “I’d rather own that asset than these assets.”

“I don’t really care what starts the next fire…but if you push me for an opinion, I’d say it’ll probably be Japan. Japan’s the likely next trigger, because it is the last sort of provider into the global hunger games1. It’s the last guy still buying everyone’s else’s bonds.”

“Are we comfortable lending to Amazon for 3 years, for 5 years at about one half of 1% above Canadian government bonds? Yes, but longer term, we’re we’re not so sure.”

Brian Carney, Mawer Investment Management (Mark’s brother)

I just looked this up for posterity…

“Approximately 124 publicly traded companies listed on U.S. exchanges (including ADRs) with market capitalizations over $10 billion have a price-to-sales (P/S) ratio over 102.

For companies with market capitalization of $100 billion or higher, the top 5 highest P/S ratios (sorted descending, from the same screener data) are approximately:

ARM Holdings (ARM) — P/S ≈ 71.7 (market cap ≈ $353B)

Palantir Technologies (PLTR) — P/S ≈ 52.1 (market cap ≈ $272B)

CrowdStrike Holdings (CRWD) — P/S ≈ 34.6 (market cap ≈ $176B)

Marvell Technology (MRVL) — P/S ≈ 26.8 (market cap ≈ $233B)

AppLovin (APP) — P/S ≈ 26.1 (market cap ≈ $161B)”

“The market needs to believe that they have the political will to actually put these folks into some kind of a [temporary government-run company to run the bank’s operations until it’s sold or liquidated], wipe out the shareholders, impose losses on unsecured creditors, as you would in a bankruptcy proceeding, and if you just did that once, you would probably end bailouts.”

Jeff Gundlach

“I’ve been talking about the entitlement programs’ dire finances for a long time, and it’s one of these things where it used to be our grandchildren’s problem, and then it looked like it was going to be our our children’s problem, and suddenly it’s on the doorstep. I mean the social security administration just last week acknowledged - when I started this business, they said they were they they were good until 2060, and then 10 years later it was good until 2050, and then few years later it was 2040, and then it was 2038, and now they say they’re out of money in 2032. Now 2032 is close enough, but since the the date of of running out of money keeps rolling forward, because the assumptions are too optimistic, it means that it’s before 2032. And I’ve been targeting somewhere like 2029, maybe even 2028, that this has to be really front and center. But here it is, we’re getting to the second half of 2026. So we’re talking a couple of years on this thing, and it’s going to have to be addressed one way or another. So it’ll be interesting to see. What Social Security Administration said last week was they’re they’re trying to get people’s attention by saying we’re going to have to cut benefits by 20%. It’s a round number. They had a more specific number, but it was close to 25%, and probably start cutting some people out of the program, and that sort of a thing. And that’s that’s another one of these systems that that used to work that doesn’t work anymore.”

On Private Equity and Private Credit

“It’s amazing that you’ve got a creditor that’s not paying and so you say, “Okay, you don’t have to pay me cash.” We’ll just put it the back of the loan, and they keep the loan marked at par. And there’s one case that was actually reported last month where the private equity interest underneath the payment in kind was wiped out. It was marked down 98% from about a hundred million to $800,000 overnight. And they still marked the PIK bonds at par. I don’t know where’s the DOJ on this one. [laughter] But that kind of stuff’s going on.”

“I’m getting that feeling that I had in 2005, 2006, where I feel like everybody’s lying about everything.”

Howard “Marks wrote 6,000 words about the fragility of everyone else’s direct lending book while his own publicly traded BDC is on negative watch by Moody’s.”

“People don’t understand how well prepared Kevin Warsh is for this job. He was tutored by some of the smartest people in finance over the past 30 years, and I think this is really great. I think it’s going to be a good inflection point for the central bank. They’re going to get back to focusing on their job and leave behind a lot of the progressive nonsense we heard during both Powell and Janet Yellen.”

“If you’re Kevin Warsh and you want to minimize rate hikes so you don’t tank the economy, well, the only way to do that is to change the definition [of inflation]. And the Fed’s done this before. You’ve watched this process for a while. Whenever they run into an obstacle like higher prices, we redefine what inflation is. And I suspect that that narrow version of inflation that Chairman Warsh has referred to in his public comments is probably going to be what we end up with.”

At the Fed, Tom Hoenig was courageous. Kevin Warsh went along.

This is from Ben Bernanke’s fantasy novel, “The Courage to Act in My Own Best Interest”:

Hoenig’s comments had irked me, but, despite hearing from a few FOMC colleagues who were piqued at Warsh’s op-ed, I was comfortable with it. I never questioned Kevin’s loyalty or sincerity. He had always participated candidly and constructively, as a team player, in our deliberations. And I was grateful that he had voted for the second round of asset purchases despite his unease. I saw his public comments more as an indictment of policymakers outside the Fed than as an attack on Fed policies. Kevin would leave the Board three months later, but not because of any policy disagreement. We had agreed when he was appointed in 2006 that he would stay for about five years. We remain close to this day.

“Warsh was the worst possible choice for Trump, so the argument is either Warsh’s last 15 years of rantings were all lies, or Trump was told, ‘you’re going to take Warsh.’”

Edward Chancellor: Galbraith’s bezzle lurks beneath the AI frenzy

In his book “The Great Crash 1929”, John Kenneth Galbraith coined the term “bezzle”. The economist defined the term as “an inventory of undiscovered embezzlement in – or more precisely not in – the country’s businesses and banks.” According to Galbraith, the bezzle grows “in good times [when] people are relaxed, trusting, and money is plentiful”. We are living through such times, once again. Enthusiasm for anything related to AI has made investors too relaxed and trusting about the financial activities of the leading companies involved in the technology revolution…

The vendor financing trend of the dot-com bubble has been superseded by vendor-investing. Microsoft committed to large investments in OpenAI, which in turn agreed to use the software giant’s cloud services. Nvidia owns more than 10% of the neocloud firm, CoreWeave , which is a large customer for the $5 trillion chip giant’s graphics processing units (GPUs). When OpenAI secured commitments for $110 billion of new funding in February, $50 billion came from Amazon.com and $30 billion from Nvidia. Naturally, the ChatGPT-maker committed to using Amazon Web Services and Nvidia’s GPUs.

“We’ve all been forced into a giant casino”

“I’ve never wanted to participate in the so-called AI bubble,” Tim continued. “Basically my entire retirement is in the S&P 500. Not out of choice, but if you don’t have investments in the stock market, you’re losing ground compared to everybody who does. That’s the pernicious thing about it. There’s really no way for the average person to diversify.”

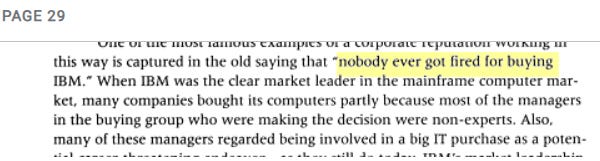

Forced is a bit much (this is from The Guardian), but I know every corporate investment committee member is thinking ‘nobody ever got fired for putting people into an S&P 500 index fund.’

Here’s a snippet I found from “California Management Review,” 1958:

Jeremy Grantham on career risk in 2012:

The central truth of the investment business is that investment behavior is driven by career risk. In the professional investment business we are all agents, managing other peoples’ money. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority “go with the flow,” either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest.

“We are a cyclical world, a world of market people. It’s as sure as can be that a great enthusiasm for private credit is going to result in a bear market in all credit. You can see it in the quality - deterioration - of underwriting. You can see it in the deterioration in the quality of the fine print that used to present a degree of protection against lenders. You can see it in the proclivity of these private equity partnerships to overpay for business during the fine old high-cotton3 days of early 2020s…I would be astounded if there were not a down cycle to our credit operations, having been so long in a bubble environment.”

A slightly less pessimistic interview on private equity owning reinsurance companies: “I’m a life insurance company, and I’m going to I reinsure my book to my own captive reinsurer? How is that allowed? Just how is that allowed that I can reinsure my book to myself? Why wouldn’t a regulator say you want to reinsure your book? Go reinsure with a third party. That’s legit. Like how how is that allowed?” - Eisman

Nick Nemeth: The Smart Money Is the Subprime This Time

Read the whole thing. I love Nick’s writing style.

For the better part of fifteen years it was the easiest money anyone ever made, and not just in the lending — in the buyouts most of all. Rates sat on the floor and the price of everything went up, so you bought a company with a little of your own cash and a great deal of borrowed money, and a few years later you sold it to the next firm at a higher multiple than you paid, or you refinanced the loan cheaper and paid yourself a dividend while you waited. The borrowed money was the whole engine, and the leverage was easy to defend, because you were always going to be able to sell…

The buyout firm and the credit firm stopped being separate companies. The credit lends the money that buys the business; the equity owns the business the credit is lending against; more and more it is the same firm in both chairs, and behind both chairs now sits an insurance company it went out and bought so it would never have to ask anyone for the money again. We still say private equity. Private equity is the old room at the back. Apollo is Athene. Blackstone is a lender that happens to own some office towers, and when one of them goes on television to defend private equity, what he is defending is the credit, because the credit is the business now.

Then 2022 came and the floor moved. Rates went up, the prices stopped rising, the buyers went home, and the one assumption the whole machine was poured on top of — that you could always sell, that you could always refinance — stopped being true without anyone announcing it. The leverage that was so easy to justify while the exit was a sure thing is still sitting on every one of those companies. The exit is not…

At Apollo, at Blackstone, at all of them, once you reach a certain level you are not allowed to just run the fund. You have to be in it — two percent of every dollar you put to work, your own money alongside the investors’. Eat your own cooking, they call it, and for a long time it cost nothing, because the funds were small and the money came back. The funds are not small now. Two percent of what these people deploy is half a million, a million dollars a year, after a tax bill that New York and Connecticut have already cut in half. They do not have it lying around. So they borrow it — a margin loan against the portfolio, a second mortgage on the house in Greenwich — to make the capital calls into the funds they are themselves out on the road raising. It is a wonderful arrangement for exactly as long as the money comes back. The money is not coming back. There are funds in their sixth year that have not returned a single dollar, and the men who run them are still calling capital, still wiring their own borrowed money in, into companies a number of which they already know, privately, are zeroes…

You will know it has finished breaking when the men who built it turn up on Bloomberg and CNBC to explain, gravely, that unless somebody does something we are looking at ten, twelve, fourteen percent unemployment. When you hear it, remember they mortgaged their own homes on the certainty that someone would always be there to catch them.

I am not sure anyone will be, and that is what makes this feel less like 2008 than like 1929.

The ordinary person should care, and not because anyone is asking him to feel sorry for Greenwich. He never got the upside — fifteen years of it went over his head — and he is going to get the bill anyway: the layoffs that come after the credit goes, the cost of propping up an insurance company he was told was the safe choice, the pension he does not manage and was never asked about, the one that has been quietly packed with these same funds. He paid in, and he gets the loss anyway. That is most of the last fifteen years right there.

But the shape of the loss is different this time. In 2008 it started at the bottom, with a family and a foreclosure sign, and the rescue traveled up from there to the banks that had it coming, and there was a face on the misery you could be made to feel something for. There is no such face this time. This time it starts at the top. It is the kid taken out of the private school over the summer because seventy-five thousand a year suddenly does not make sense. It is the margin call arriving for people who were certain margin calls happened to other, smaller men. 1929 wiped out the people at the top who had borrowed to get there and took the country down with them. 2008 wiped out the borrower and saved the lender. This one looks like 1929.

Which is why the rescue may not come. There is no family on the lawn this time. There is Greenwich, and I am not certain the country still has it in itself to bail out the richest and most pleased-with-themselves people in it when there is nobody sympathetic standing in front of them to justify it. They are counting on the save anyway, the way they always have, because in fifteen years not one of them has ever had to sit with the possibility that this time the reason is them.

And if it does come, the number will be one nobody is ready to say out loud, because this was never just the buyouts and the leveraged loans. The same cheap money and the same faith that you can always refinance went into the asset-based lending, the commercial mortgages, the houses people live in, the credit cards the whole country has been running its life on. There is no program large enough for all of that. You can only print it, and you cannot print a number that size without breaking the dollar it is printed in.

By the time the number is that big, it will be plain why it came and who it came for — three-quarters of a trillion a year, going to a few hundred thousand people — and a country does not stay one country once that is the thing everyone knows. The outcomes from here are wide and varied, and not one of them is good. For fifteen years these men have been certain the fault was always somebody else’s. This time it is theirs, and the people who never saw a dollar of the upside will pay for it anyway.

The music is still playing, but it will stop.

A recent podcast with Nick…Here’s a clip he shared: “It’s not just private credit”:

“It’s very clear that the boomers have outsized-power [compared to] any generation in the history of humanity, and that is because of the Federal Reserve. It might not have been the reason why they did it, but it is a direct result.”

Mark Moss: “What real estate allows me to do is not pay tax.”

Nick Nemeth: “Yeah. Well, that’s that’s another problem.”

Moss: “Why is that a problem?”Nemeth: “…I don’t think that you should be able to use leverage which already has perverse incentives and creates bubbles in order to not pay taxes.”

Bain Capital CLO Tranche Defaults in Post-2008 First for Europe

Part of a European collateralized loan obligation managed by Bain Capital has failed to repay investors in full, the first such default since an overhaul of the asset-backed securities more than a decade ago.

Rating agency Fitch said it downgraded the most junior tranche of the private investment firm’s Euro CLO 2018-1 DAC bond to default on Thursday, after the note returned €7.4 million ($8.5 million) to its holders compared with a par value of €11.2 million. The total value of the vehicle was €361 million.

PE Owners Tap a Hot Loan Market to Pay Themselves

“Blackstone Inc. and Warburg Pincus just piled more debt onto their portfolio company IntraFi to fund a payout to themselves. For the seventh time in three years.”

Apollo curbs withdrawals after exit requests hit 17%

Apollo is capping withdrawals from its Apollo Debt Solutions private credit vehicle at 5% after redemption requests soared in the second quarter to almost 17%, or $2.4 billion…

It highlighted a “notable regional split” in second-quarter withdrawal requests, with U.S. onshore clients looking to pull out about 4.3%, while redemptions from offshore investors jumped to 12.5%.

You know, when Old Yeller got rabies, they didn't try to keep coming up with ways to extend his life.

"The finding and fighting of positive evil is the beginning of all fun—and even of all farce."

G.K. Chesterton, "The Flying Inn"

“I am wondering what will happen to the world when we go off the gold standard in ideas, dress, morals, etc.”

Henry Miller, Tropic of Cancer

Grant Williams

In 1914, as Germany left the Gold Standard to help finance the Great War, an ounce of gold cost a fixed 475 goldmarks. By 1920, an ounce cost 1,400 Papiermarks— the new fiat currency that had replaced it. Just three years later, at the peak of the hyperinflation in late 1923, that same ounce of gold cost 20 trillion Papiermarks.

We all think we know the lessons of hyperinflation. But there’s one aspect that’s less understood. Through that entire debauchment of the currency, the price of gold swung wildly. The idea of gold being “in a bear market” because it fell some arbitrary 20% is laughable. Gold would regularly soar over 100% in Papiermark terms in a single month — then “crash” 20–30% the next.

There was never a bull market in gold. There was only a bear market in paper promises. And today, just like its chemical properties, gold’s function hasn’t changed.

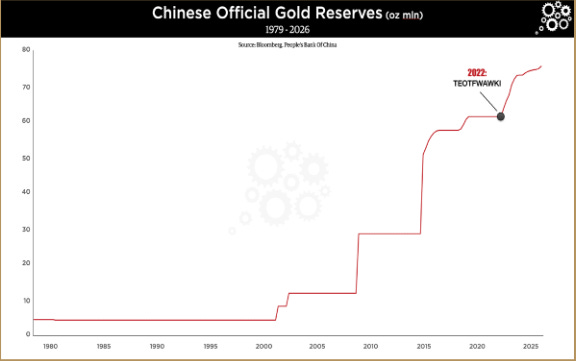

Gold tells you what your currency is worth. Not the other way around. The bond market has broken, the dollar’s safe-haven status has cracked, US debt service costs now exceed defence spending, and the BRICS alternative architecture is under construction. Central banks are buying gold at sixty-year highs, and perhaps most importantly, Liberation Day demonstrated, in real time, that the reflex of the last fifty years—sell everything at the first sign of trouble and buy dollars and Treasuries—is no longer automatic

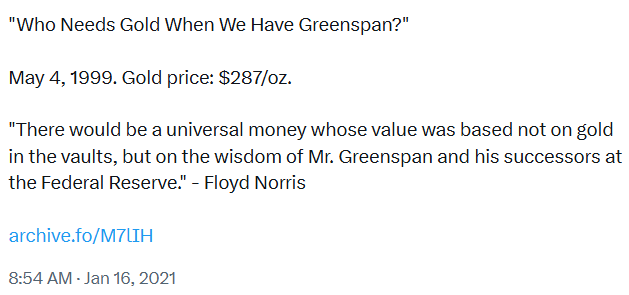

Gold and Economic Freedom by Alan Greenspan

The Objectivist, July 1966.

An almost hysterical antagonism toward the gold standard is one issue which unites statists of all persuasions. They seem to sense—perhap more clearly and subtly than many consistent defenders of laissez-faire—that gold and economic freedom are inseparable, that the gold standard is an instrument of laissez-faire and that each implies and requires the other.

In order to understand the source of their antagonism, it is necessary first to understand the specific role of gold in a free society.

Money is the common denominator of all economic transactions. It is that commodity which serves as a medium of exchange, is universally acceptable to all participants in an exchange economy as payment for their goods or services, and can, therefore, be used as a standard of market value and as a store of value, i.e., as a means of saving.

The existence of such a commodity is a precondition of a division of labor economy. If men did not have some commodity of objective value which was generally acceptable as money, they would have to resort to primitive barter or be forced to live on self-sufficient farms and forgo the inestimable advantages of specialization. If men had no means to store value, i.e., to save, neither long-range planning nor exchange would be possible.

What medium of exchange will be acceptable to all participants in an economy is not determined arbitrarily. First, the medium of exchange should be durable. In a primitive society of meager wealth, wheat might be sufficiently durable to serve as a medium, since all exchanges would occur only during and immediately after the harvest, leaving no value-surplus to store. But where store-of-value considerations are important, as they are in richer, more civilized societies, the medium of exchange must be a durable commodity, usually a metal. A metal is generally chosen because it is homogeneous and divisible: every unit is the same as every other and it can be blended or formed in any quantity. Precious jewels, for example, are neither homogeneous nor divisible.

More important, the commodity chosen as a medium must be a luxury. Human desires for luxuries are unlimited and, therefore, luxury goods are always in demand and will always be acceptable. Wheat is a luxury in underfed civilizations, but not in a prosperous society. Cigarettes ordinarily would not serve as money, but they did in post-World War II Europe where they were considered a luxury. The term “luxury good” implies scarcity and high unit value. Having a high unit value, such a good is easily portable; for instance, an ounce of gold is worth a half-ton of pig iron.

In the early stages of a developing money economy, several media of exchange might be used, since a wide variety of commodities would fulfill the foregoing conditions. However, one of the commodities will gradually displace all others, by being more widely acceptable. Preferences on what to hold as a store of value will shift to the most widely acceptable commodity, which, in turn, will make it still more acceptable. The shift is progressive until that commodity becomes the sole medium of exchange. The use of a single medium is highly advantageous for the same reasons that a money economy is superior to a barter economy: it makes exchanges possible on an incalculably wider scale.

Whether the single medium is gold, silver, seashells, cattle, or tobacco is optional, depending on the context and development of a given economy. In fact, all have been employed, at various times, as media of exchange. Even in the present century, two major commodities, gold and silver, have been used as international media of exchange, with gold becoming the predominant one. Gold, having both artistic and functional uses and being relatively scarce, has always been considered a luxury good. It is durable, portable, homogeneous, divisible, and, therefore, has significant advantages over all other media of exchange. Since the beginning of World War I, it has been virtually the sole international standard of exchange.

If all goods and services were to be paid for in gold, large payments would be difficult to execute, and this would tend to limit the extent of a society’s division of labor and specialization. Thus a logical extension of the creation of a medium of exchange is the development of a banking system and credit instruments (bank notes and deposits) which act as a substitute for, but are convertible into, gold. A free banking system based on gold is able to extend credit and thus to create bank notes (currency) and deposits, according to the production requirements of the economy. Individual owners of gold are induced, by payments of interest, to deposit their gold in a bank (against which they can draw checks). But since it is rarely the case that all depositors want to withdraw all their gold at the same time, the banker need keep only a fraction of his total deposits in gold as reserves. This enables the banker to loan out more than the amount of his gold deposits (which means that he holds claims to gold rather than gold as security for his deposits). But the amount of loans which he can afford to make is not arbitrary: he has to gauge it in relation to his reserves and to the status of his investments.

When banks loan money to finance productive and profitable endeavors, the loans are paid off rapidly and bank credit continues to be generally available. But when the business ventures financed by bank credit are less profitable and slow to pay off, bankers soon find that their loans outstanding are excessive relative to their gold reserves, and they begin to curtail new lending, usually by charging higher interest rates. This tends to restrict the financing of new ventures and requires the existing borrowers to improve their profitability before they can obtain credit for further expansion. Thus, under the gold standard, a free banking system stands as the protector of an economy’s stability and balanced growth.

When gold is accepted as the medium of exchange by most or all nations, an unhampered free international gold standard serves to foster a world-wide division of labor and the broadest international trade. Even though the units of exchange (the dollar, the pound, the franc, etc.) differ from country to country, when all are defined in terms of gold the economies of the different countries act as one—so long as there are no restraints on trade or on the movement of capital. Credit, interest rates, and prices tend to follow similar patterns in all countries. For example, if banks in one country extend credit too liberally, interest rates in that country will tend to fall, inducing depositors to shift their gold to higher-interest paying banks in other countries. This will immediately cause a shortage of bank reserves in the “easy money” country, inducing tighter credit standards and a return to competitively higher interest rates again.

A fully free banking system and fully consistent gold standard have not as yet been achieved. But prior to World War I, the banking system in the United States (and in most of the world) was based on gold, and even though governments intervened occasionally, banking was more free than controlled. Periodically, as a result of overly rapid credit expansion, banks became loaned up to the limit of their gold reserves, interest rates rose sharply, new credit was cut off, and the economy went into a sharp, but short-lived recession. (Compared with the depressions of 1920 and 1932, the pre-World War I business declines were mild indeed.) It was limited gold reserves that stopped the unbalanced expansions of business activity, before they could develop into the post- World War I type of disaster. The readjustment periods were short and the economies quickly re-established a sound basis to resume expansion.

But the process of cure was misdiagnosed as the disease: if shortage of bank reserves was causing a business decline—argued economic interventionists—why not find a way of supplying increased reserves to the banks so they never need be short! If banks can continue to loan money indefinitely—it was claimed—there need never be any slumps in business. And so the Federal Reserve System was organized in 1913. It consisted of twelve regional Federal Reserve banks nominally owned by private bankers, but in fact government sponsored, controlled, and supported. Credit extended by these banks is in practice (though not legally) backed by the taxing power of the federal government. Technically, we remained on the gold standard; individuals were still free to own gold, and gold continued to be used as bank reserves. But now, in addition to gold, credit extended by the Federal Reserve banks (“paper” reserves) could serve as legal tender to pay depositors.

When business in the United States underwent a mild contraction in 1927, the Federal Reserve created more paper reserves in the hope of forestalling any possible bank reserve shortage. More disastrous, however, was the Federal Reserve’s attempt to assist Great Britain who had been losing gold to us because the Bank of England refused to allow interest rates to rise when market forces dictated (it was politically unpalatable). The reasoning of the authorities involved was as follows: if the Federal Reserve pumped excessive paper reserves into American banks, interest rates in the United States would fall to a level comparable with those in Great Britain; this would act to stop Britain’s gold loss and avoid the political embarrassment of having to raise interest rates.

The “Fed” succeeded: it stopped the gold loss, but it nearly destroyed the economies of the world, in the process. The excess credit which the Fed pumped into the economy spilled over into the stock market—triggering a fantastic speculative boom. Belatedly, Federal Reserve officials attempted to sop up the excess reserves and finally succeeded in braking the boom. But it was too late: by 1929 the speculative imbalances had become so overwhelming that the attempt precipitated a sharp retrenching and a consequent demoralizing of business confidence. As a result, the American economy collapsed. Great Britain fared even worse, and rather than absorb the full consequences of her previous folly, she abandoned the gold standard completely in 1931, tearing asunder what remained of the fabric of confidence and inducing a world-wide series of bank failures. The world economies plunged into the Great Depression of the 1930’s.

With a logic reminiscent of a generation earlier, statists argued that the gold standard was largely to blame for the credit debacle which led to the Great Depression. If the gold standard had not existed, they argued, Britain’s abandonment of gold payments in 1931 would not have caused the failure of banks all over the world. (The irony was that since 1913, we had been, not on a gold standard, but on what may be termed “a mixed gold standard”; yet it is gold that took the blame.)

But the opposition to the gold standard in any form—from a growing number of welfare-state advocates—was prompted by a much subtler insight: the realization that the gold standard is incompatible with chronic deficit spending (the hallmark of the welfare state). Stripped of its academic jargon, the welfare state is nothing more than a mechanism by which governments confiscate the wealth of the productive members of a society to support a wide variety of welfare schemes. A substantial part of the confiscation is effected by taxation. But the welfare statists were quick to recognize that if they wished to retain political power, the amount of taxation had to be limited and they had to resort to programs of massive deficit spending, i.e., they had to borrow money, by issuing government bonds, to finance welfare expenditures on a large scale.

Under a gold standard, the amount of credit that an economy can support is determined by the economy’s tangible assets, since every credit instrument is ultimately a claim on some tangible asset. But government bonds are not backed by tangible wealth, only by the government’s promise to pay out of future tax revenues, and cannot easily be absorbed by the financial markets. A large volume of new market—triggering a fantastic speculative boom. Belatedly, Federal Reserve officials attempted to sop up the excess reserves and finally succeeded in braking the boom. But it was too late: by 1929 the speculative imbalances had become so overwhelming that the attempt precipitated a sharp retrenching and a consequent demoralizing of business confidence. As a result, the American economy collapsed. Great Britain fared even worse, and rather than absorb the full consequences of her previous folly, she abandoned the gold standard completely in 1931, tearing asunder what remained of the fabric of confidence and inducing a world-wide series of bank failures. The world economies plunged into the Great Depression of the 1930’s.

With a logic reminiscent of a generation earlier, statists argued that the gold standard was largely to blame for the credit debacle which led to the Great Depression. If the gold standard had not existed, they argued, Britain’s abandonment of gold payments in 1931 would not have caused the failure of banks all over the world. (The irony was that since 1913, we had been, not on a gold standard, but on what may be termed “a mixed gold standard”; yet it is gold that took the blame.)

But the opposition to the gold standard in any form—from a growing number of welfare-state advocates—was prompted by a much subtler insight: the realization that the gold standard is incompatible with chronic deficit spending (the hallmark of the welfare state). Stripped of its academic jargon, the welfare state is nothing more than a mechanism by which governments confiscate the wealth of the productive members of a society to support a wide variety of welfare schemes. A substantial part of the confiscation is effected by taxation. But the welfare statists were quick to recognize that if they wished to retain political power, the amount of taxation had to be limited and they had to resort to programs of massive deficit spending, i.e., they had to borrow money, by issuing government bonds, to finance welfare expenditures on a large scale.

Under a gold standard, the amount of credit that an economy can support is determined by the economy’s tangible assets, since every credit instrument is ultimately a claim on some tangible asset. But government bonds are not backed by tangible wealth, only by the government’s promise to pay out of future tax revenues, and cannot easily be absorbed by the financial markets. A large volume of new government bonds can be sold to the public only at progressively higher interest rates. Thus, government deficit spending under a gold standard is severely limited.

The abandonment of the gold standard made it possible for the welfare statists to use the banking system as a means to an unlimited expansion of credit. They have created paper reserves in the form of government bonds which—through a complex series of steps—the banks accept in place of tangible assets and treat as if they were an actual deposit, i.e., as the equivalent of what was formerly a deposit of gold. The holder of a government bond or of a bank deposit created by paper reserves believes that he has a valid claim on a real asset. But the fact is that there are now more claims outstanding than real assets.

The law of supply and demand is not to be conned. As the supply of money (of claims) increases relative to the supply of tangible assets in the economy, prices must eventually rise. Thus the earnings saved by the productive members of the society lose value in terms of goods. When the economy’s books are finally balanced, one finds that this loss in value represents the goods purchased by the government for welfare or other purposes with the money proceeds of the government bonds financed by bank credit expansion.

In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value. If there were, the government would have to make its holding illegal, as was done in the case of gold. If everyone decided, for example, to convert all his bank deposits to silver or copper or any other good, and thereafter declined to accept checks as payment for goods, bank deposits would lose their purchasing power and government-created bank credit would be worthless as a claim on goods. The financial policy of the welfare state requires that there be no way for the owners of wealth to protect themselves.

This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the “hidden” confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.

Who needs gold when we have Warsh?

Every tragedy could really start with the words:

“Nothing would have happened had it not been that...”

- Ludwig Wittgenstein, 𝘊𝘶𝘭𝘵𝘶𝘳𝘦 𝘢𝘯𝘥 𝘝𝘢𝘭𝘶𝘦

Cover your hair and your eyes

I don’t think A.I. is the biggest threat to humans.

I think economics professors are the biggest threat to humans.

“...with log utility it is optimal to take a 1 in 3 chance of ending human existence in exchange for a 2/3 chance of dramatically raising living standards”

Dredge “uses the phrase “Hunger Games” as a metaphor for intense, zero-sum or winner-take-most competition among governments and large borrowers for a shrinking pool of global savings, liquidity, and capital to fund exploding public debts.”

Scott McNealy, March 2002: “Two years ago we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don't need any transparency. You don't need any footnotes. What were you thinking?”

“The term "high cotton" or "tall cotton" originates from the rural farming community in the antebellum (pre-Civil War) South when "high cotton" meant that the crops were good and the prices were, too.”

https://ritholtz.com/2010/07/greenspan-chair-at-nyu/

The Fed Chair is dead. Long live the Fed Chair.