“If you're first out the door, that's not called panicking.” - John Tuld

“I’ve spent since 1983 working with people that sold companies, and we see a lot of wealth…I have to say that a lot of these people - I know they’re not happy, and they’re not happy for different reasons, really. Some of them really are not happy with their spouse, a number of them are not happy by the way - they feel a tremendous guilt about the way they raised their children, because they were working all the time. They never saw their children, and now they’re paying the price for that, because the children are really sort of away from them. I see that quite a bit…

Now the ones I see that really do it correctly, they have done it right, they have tremendous family lives, number one, and number two - they’re fulfilled in life.”

Reminded of these two quotes:

“I’ve always told young people, in terms of parenting, forget ‘quality time’ - it’s quantity time. All time with your children is quality time…” - Stan Druckenmiller

And this, from John Bogle:

At a party given by a billionaire on Shelter Island, the late Kurt Vonnegut informs his pal, the author Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch 22 over its whole history.

Heller responds, “Yes, but I have something he will never have . . . Enough.”

Good thing the Fed has now cooled inflation!

"We've made a lot of really bad choices, and it takes a long time to see the consequences of those choices, and we've only just begun."

"It's OK to miss out." - Melody Wright

A lot of wisdom in that line.

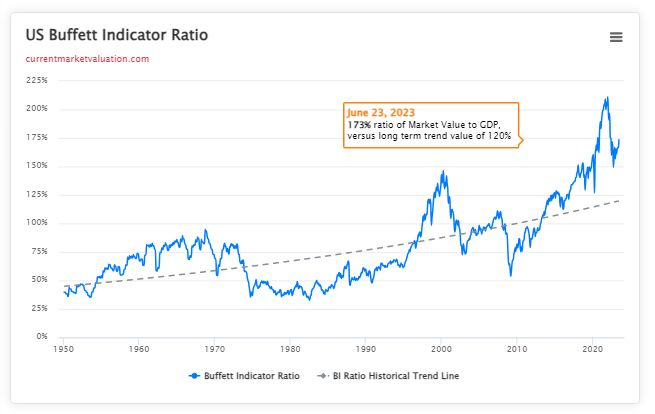

We remain in a crazy bubble.

Via Grant’s:

A minuscule handbag measuring less than 0.03 inches wide − or 657 by 222 by 700 microns − sold for more than $63,000 at an online auction this week. Aptly dubbed the “Microscopic Handbag" by creator MSCHF, the fluorescent yellow-green tote appears to be based on a popular Louis Vuitton design and is "smaller than a grain of salt."

This was from August 2020:

The Balance Sheet is back to where it was before the regional banks blew up. That QT is really coming along.

This will end well.

The government should encourage greater co-investment with private sector pension funds if it wants to unlock more retirement cash for the economy, the trade body for Britain’s trillion-pounds savings industry has said.

The Association of British Insurers (ABI) — which represents the biggest pension providers — said state backing for riskier, illiquid investments would help make the UK a “more attractive” destination for its members.

“By developing further initiatives that use co-investment as an incentive, the government could create opportunities for pension funds to put more money behind assets that align with its wider policy objectives,” it said.

UK Apparatchiks diverting money to their favorite pet projects.

“The statesman who should attempt to direct private people in what manner they ought to employ their capitals would not only load himself with a most unnecessary attention, but assume an authority which could safely be trusted, not only to no single person, but to no council or senate whatever, and which would nowhere be so dangerous as in the hands of a man who had folly and presumption enough to fancy himself fit to exercise it.”

- Adam Smith, The Wealth of Nations

The A.I. Bull Market

SPX/SPX Equal Weight

I’ve never watched Yellowstone, but Taylor Sheridan wrote Sicario (and its sequel), Hell or High Water, and Wind River, four movies I really liked.

Nice anecdote here: Taylor Sheridan Does Whatever He Wants: “I Will Tell My Stories My Way”

“We go to lunch in some snazzy place in West L.A.,” Sheridan says. “And [Yellowstone co-creator] John Linson finally asks: ‘Why don’t you want to make it?’ And the vp goes: ‘Look, it just feels so Middle America. We’re HBO, we’re avant-garde, we’re trendsetters. This feels like a step backward. And frankly, I’ve got to be honest, I don’t think anyone should be living out there [in rural Montana]. It should be a park or something.’ “

OK, so there’s a lot more below. Try a paid subscription if you’re interested. I do a lot of reading (and a little thought) to put these together - I think Bill Fleckenstein said of his writings years ago that if it’s worth his time, it’s worth paying (a nominal sum) for.

The most common reason people give for unsubscribing from paid is 50/50 price and time. Price is 27 cents a day. Time, I can understand. I used to get the WSJ newspaper every day, and they’d stack up because I almost never got to them (I do look ‘em on online from time to time now). There’s often a lot of eclectic stuff in my non-single topic posts - don’t view it as a giant meal to eat, but as a buffet - delve into what’s interesting to you, and skip the rest. Unfortunately, just about everything interests me.

And if you can’t pay, that’s fine. I still do a lot of free stuff, no hard feelings. I do appreciate the people who have paid subscriptions. It’s encouraging.

Regardless, my 81 million free & paid subscribers seem to get something out of it.

Lately I’ve been focusing mostly on real estate, because that’s where I think the big changes may be occurring. Clearly in some parts of the country/world things are correcting, but other areas seem more bubbly than ever. Location, Location, Location. I suspect that the “this isn’t 2008” crowd maybe be right in theory, just not in practice. We shall see. It took 5 years last bubble from top to bottom (using Case-Shiller for the sake of argument.) These battleships turn slowly (although CRE seems more like a Destroyer.)

As I’ve said before, I think CNBC or the New York Times or Forbes are not the places to look for the nation’s pulse. During the bubble before this bubble, it was the little bloggers that nailed the housing bubble, not the LA Times or Fox Business. It’s not that Reddit - which I use frequently nowadays for anecdotes and ideas - isn’t full of misinformation and liars - it is, just like CNBC - but it’s also full of regular people, you know, non-billionaires. This is also why I like people like Melody Wright, who is actually doing boots-on-the-ground research, and who also has a memory of what happened before March 9, 2009, which almost no one else today seems to have.

We all know Barry Sternlicht’s take - he wants/needs ZIRP, QE and high inflation, STAT! That view doesn’t play as well in your local supermarket though.

“Predicting an event is one thing, and benefiting from it is another thing. See, I’m a very bad predictor - I’m wrong most of the time - but it doesn’t cost me much to be wrong. That’s what matters, it’s the payoff, not the frequency of being correct.”

This is also true in poker. - rh

“Homes Are Expensive. Building More Won’t Solve the Problem.”

While housing construction lagged behind population growth over the last decade, there was a surplus of housing in the run-up to the GFC.

Overall, the US has a surplus of housing.

26 metros have shortages of housing, but their aggregate population size adds up to only 1%

In 681 other metros totaling 72% of US population, including New York, actually have surplus of housing (!)

The problem is a mismatch in the price-point of housing supply and income of local populations. Prosperous metros have a larger perceived problem because they have the worst price-income mismatch in their excess housing supply.”

Sorry, kids!

Shortly before home prices began to surge in 2021, Amazon.com Inc. Founder Jeff Bezos made a bet on a Seattle-based startup that had a mission to make real estate investments more accessible to retail investors. That year, Arrived Homes became the first company to legally sell shares of individual rental properties to nonaccredited investors. Investors on the real estate platform have now funded over 275 single-family homes with a total value of more than $102 million.

Then again…

4M baby boomer homes should hit market each year until 2032

More than 4 million existing homes from the aging and mortality of older homeowners will come on to the market each year through 2032. [Yay!]

But sustained homebuyer demand from population growth and younger-generation households should lead to minimal excess housing supply, the study found. [Boo!]

Wow.

BLUF: My wife and I live north of Austin and own two houses. We are currently living in the first, renting the 2nd. Cashflow in the 1st year on the 2nd is only $120/mo. We have extensive savings and are trying to strategize on what’s next for us.

Tenants in house 2 are fantastic and have already indicated they will be looking to renew lease while they build savings to buy their own house in the future. I believe I can increase rent by $100-150 without effort for next year, increasing cash flow of the rental.

House 1’s PITI make it unrealistic to cashflow with the rental rates I’m seeing in the area. I believe it would be short of market rents by about $300-400 in a perfect world. Wife and I aren’t comfortable house hacking - we have a baby on the way (before everyone hones in on this detail, we have separate savings set aside for baby and very good health insurance).

Here’s the fun part: properties I believe could easily rent around us are priced about 340-420k. With interest rates and central Texas taxes involved, PITI is significantly affected. We have roughly 90k in investments that I am willing to sell to pick up property 3. My question is if it’s worth it. A BRRRR is going to require time we don’t currently have, and I don’t have the capital yet for MFH. Should I purchase now, and probably only generate $200-300 cashflow, or continue building my savings and waiting for a better option / MFH-level money?

BLUF = bottom line up front

PITI = Principal, Interest, Taxes, and Insurance

BRRRR = buy, rehab, rent, refinance, repeat

MFH = multi-family housing

House hacking = finding ways to generate income from your home

The (unedited) comments were amusing:

This is exactly why raising interest rates works. The deals that barely penciled at super low rates don’t now

You can make almost $400/mo risk free on that 90k, why are you wanting to leverage yourself further for half the income and lots of risk?

Cash flowing a couple hundred a month on a rental is nothing to write home about. You’re one small repair from wiping out years of gains.

interest rates need to be higher

(A different thread) Dude your like one furnace/plumbing/etc. issue away from being severely under on house 2. Why buy another?

The people who get hurt in real estate are the ones who think it is a get rich quick scheme where they can leverage to the hilt and flip properties. Once the music stops and markets correct, they end up losing out.

Owning rental property used to be an investment that paid off in 20 years. It's only been a gold rush for the last 5 or 6, so this is more like things reverting back to norm.

My friend's parents are millionaires now. While we were growing up they ended up with about 12 rental properties and were basically scrimping money and DIYing them the entire time. Like they had no lives outside of their rentals and dealing with maintenance and tenant bullshit. Made me decide then and there that I would never be a landlord. But man they hit their 50s and were basically rolling in money once all those properties were paid off.

If youre planning on appreciation as the mechanism that is going to make you money, do you think that maybe you should take a look at some metrics?In my state, 75% of the residents have been pushed out of the housing market. The median income here (household) is about 70k per year. The median home price is about 550. If youre going to buy rentals, believing the appreciation is where you will make money (and yes, this is where you should be focusing), does your area have median house prices that will work for the median earner? The reality is that in order to make money from appreciation, you have to know with a fair amount of certainty that the appreciation youre expecting is supported by your local wages…Before you buy a rental, do some basic economic analysis of whether or not its even a possibility that you can make what youre expecting. The whole "own it for 20 years and youll have tons of money" is such a shit piece of advice. I know many, many investors who have lost their asses because they take these shotgun investing approaches and dont know jack shit about what really drives real estate investing. The answer to that question is very simple. Wages.

Certainly a lot of "I believes" for a rental shack in Austin, of all places. That place is cratering due to unaffordability just like many other places, and will continue to crater for years, once the employment picture reverses.

It'll take years though, just like during the GFC, when it took another 4 years after the Fed had actually started cutting interest rates.

If appreciation is only 3%, and you put 20% down, that's really a return of 15%. It goes the other way too if values decrease, but that's not much of a factor when planning on long term. [i.e., Homes everywhere always go up - rh]

Some color on “post bank-failure regulatory exams” from Randy Woodward:

Developer Leverages Unique California Housing Laws To Get Plans Approved

Oxford Capital Group, the Chicago-based firm looking to overhaul the Creekside Inn hotel at 3400 El Camino Real in the San Francisco suburb of Palo Alto, plans to invoke California's "builder's remedy" provision. It's doing so after failing to win over city planning officials and residents with its initial plan to reposition the property into a mix of housing, updated hotel rooms and amenity space…

In an effort to tackle the state's intertwined housing shortage and affordability problem, California’s unique housing laws — initially intended to promote development and cut through any unnecessary red tape — have evolved to pit state officials against those from local municipalities.

The so-called builder's remedy, which gives homebuilders leverage over California cities and their zoning codes, is possible only when cities and local municipalities don't have an approved plan to meet their housing development goals.

"With builder's remedy, builders can come in with development on pretty much any property and we don't have a lot of leeway to say no," San Jose City Councilmember Dev Davis said in a statement on the provision, which has been invoked for a growing handful of projects across the Silicon Valley area. What's more, Davis said there isn't much the city can do to push back because it's a California regulation, so more builders could adopt the same process.

"The state and our state representatives have basically sided with developers and said developers get carte blanche and the average resident gets no say," she said.

OK, so I’ll take the old man “get off my lawn” side on this. In California, in theory, this “builders remedy” is wonderful for the builders and the city pension funds, but reality is not so good.

California’s lawmakers side with the builders (who donate more than the average homeowner) in the name of “affordable housing,” even though it’s never “affordable,” whether condos or rentals. The builders then come into residential neighborhoods and put up six-story apartment buildings next to 1920 bungalow, with no curb setbacks and ridiculously low parking requirements. I saw this happening decades ago even before they came up with the “builder’s remedy”, and it’s far worse now.

I guess they think you’ll pay $3k a month for your studio apartment, walk to work at California Pizza Kitchen, and then take nonexistent public transportation to your second job. The builders take the money and run, and leave the residents with increased traffic, crime etc. It can ruin neighborhoods, but that’s ok.

Rather than address “the unnecessary red tape” - passed by the same CA lawmakers who make Mike Bloomberg look like a raging Libertarian - they say, “We don’t care what the people want. We know best.” and thank the builders for their campaign contributions.

You think Gavin Newsom is going to have an apartment complex built next to his home? Of course not.

"The evil of aristocracy is not that it necessarily leads to the infliction of bad things or the suffering of sad ones; the evil of aristocracy is that it places everything in the hands of a class of people who can always inflict what they can never suffer."

Your vote does not matter - unless you vote these lawmakers out, but in California, a one-party state, the pendulum has swung so far to the left Jerry Brown now looks like a John Bircher.

This song applies even more today than in 1979:

According to Freddie Mac, the average 30-year mortgage rate since April 1971 has been 7.74%, and the median has been 7.42%.

The problem is the home price, not the interest rate. I realize this is hate speech.

This post below was quickly deleted by the Reddit hall-monitors:

Coming from a place where sub-40 temps were unusual, I moved once to a place where it freezes in the winter, and I remember the local news one night reminding everyone to let their faucets drip and open their cabinets so the heat could get in. It had never before occurred to me that you might need to do stuff like this.

I’m reminded a bit of this poster from the bubble before this bubble:

Main point is people are buying homes at 10-20% over listing price while only putting down 5% of total value at 6-7% interest rates. Add taxes, PMI, Insurance, and people are paying big amount of monthly payments, while possibly having low reserves. You know what happens to people who don’t prepare for rainy days when economy goes south [Connecticut]

Pending Home Sales

Nobody Wants to Buy a Fixer-Upper Right Now

Rent Going Up? One Company’s Algorithm Could Be Why.

On a summer day last year, a group of real estate tech executives gathered at a conference hall in Nashville to boast about one of their company’s signature products: software that uses a mysterious algorithm to help landlords push the highest possible rents on tenants.

“Never before have we seen these numbers,” said Jay Parsons, a vice president of RealPage, as conventiongoers wandered by. Apartment rents had recently shot up by as much as 14.5%, he said in a video touting the company’s services. Turning to his colleague, Parsons asked: What role had the software played?

“I think it’s driving it, quite honestly,” answered Andrew Bowen, another RealPage executive. “As a property manager, very few of us would be willing to actually raise rents double digits within a single month by doing it manually.”

RealPage Impact on Housing in Denver I found this thread to be very interesting.

My SO and I rent a 700sq ft 1bd1ba in Denver, who uses RealPage to set their prices. They tried increasing our rent YoY by 46% from $1161/mo to $1693/mo for a 12 mo lease. Appalled, we tried negotiating saying we were hoping not to pay more than $1300/mo and would need to decline the offer. We ended up getting a new offer from them a few weeks later for $1500/mo, which we accepted.

Neighbors in two apartments next to us moved out a few weeks ago and the apartments do not appear to have been listed or leased.

Does RealPage's "Revenue Management" artificially reduce supply to charge higher prices at the specific community and/or throughout the city?

If apartment rental prices are artificially inflated, does that cause increased demand for purchasing condos, aptmts, THs and SFHs?

According to their website, RealPage services over 24 million units operating in North America, Europe, and Asia, so not isolated to Denver. Could their Revenue Management service be a factor in lower US housing supply due to renters looking for alternatives?

Various comments on the above:

Same things banks did after 08. So Many homes were held off the books until the prices returned to range they wanted.

I mean, this is sales/marketing strategy 101 and one of the things we start training new reps on immediately at hire. A lot of inexperienced reps love to discount fast and loose to quickly close sales. They want to win everything and get into that habit of discounting immediately to do it. But a rep/company will be much more successful holding a firm line on higher pricing. Will they lose a couple more deals? Sure. But that will be more than made up for by the increase in price realized on everything else they didn't discount.

The institutional players control the price, not the property management company. They are told what to do when it’s all said and done. Unfortunately, that’s the only goal in CRE; increase the NOI…

Bro, where the hell are you finding those f*g prices in Denver? I'm paying $2k/month lmao.

I've worked in property management for 15 years now and implemented Yieldstar (before it was bought by Realpage I believe) at one of the companies I worked for 10 years ago…Yieldstar would just recommend a price, and you accepted it or not. It would be more aggressive in areas that were growing fast, and would even cut prices in areas that were spiraling. Before Yieldstar, property managers would just call around and ask each other what they were charging and their occupancy. So it has probably lead to prices increasing quicker, but it's nothing compared to what the eviction moratorium and rent relief did.

RealPage antitrust lawsuits over rent prices consolidated in Tennessee

More than 20 lawsuits accusing technology company RealPage Inc of conspiring with multifamily residential property managers to keep rental prices artificially high will be consolidated in Nashville federal court, according to a Monday order from the U.S. Judicial Panel on Multidistrict Litigation.

Almost 23,000 Denver metro area apartments are vacant as eviction filings climb Median rent is $1,774.

First-quarter apartment vacancy rates in 2023 are at 5.6% in the seven-county metro Denver area…About 22,673 apartments of 404,880 units in the area are empty…“Buildings constructed since 2020 had the highest vacancy at 6.8%,” according to the report. “Those constructed prior to 1970 had the lowest vacancy at 4.9%…Apartments built in the past three years cost nearly $850 more a month than apartments built before 1970…

There are currently 43,000 new apartments under construction, according to the report. Of those, 25% will be available to tenants this year.

Maybe Denver rents are about to drop. Wouldn’t that be awful. The Fed needs to act.

The Next “Wave” of Foreclosures and Markets With the Deepest Discounts w/Auction.com’s Daren Blom Promotional, but might be interesting to those looking into multifamily real estate

We are just starting to see distressed opportunities coming to the market to sell, not from the small syndicators, but from the large syndicators. I wouldn’t say they were household names but you’ve seen them on LinkedIn or Facebook, all over the place…we received some inside information that a few large properties are coming to the market shortly, and that’s gonna be a tell that these properties were bought at a high sales price about 30 months ago, with high leverage, now have much higher interest rates, with higher operating expenses, like property taxes that have gone up tremendously, insurance premiums that have almost doubled here in Texas - these syndications could be selling for whatever the loan amount that’s held against it, or a greatly reduced limited-partner equity position, so a lot of these syndications are out of money, and they want to get out before the rush comes in.

Alexandria sells Newton offices for half the $235M purchase price

A MassMutual subsidiary and Boston-based developer Greatland Realty Partners have acquired a three-building Newton office complex from Alexandria Real Estate Equities Inc. for $117.5 million, exactly half the price that Alexandria paid for the site three years ago.

This next story is sponsored by Blacksone:

The working-from-home illusion fades “It is not more productive than being in an office, after all”

I’m a dinosaur, and can’t imagine doing what I used to do for years from home. Then again, I know young people who do it (techies) and it seems to work fine. I could say I’m working from home now but it’s more a labor of love.

Credit Spreads

This is remarkable, from Grant’s: “Perhaps most strikingly, the iShares iBoxx U.S. Dollar High Yield Corporate Bond ETF now sports a 5.64% indicated yield, compared to the 5.41% on offer for one-year T-bills.”

“For a while, everyone was convinced that rates were just going to go right back down . . . so, a lot of issuers were waiting for the Fed to pivot before coming back to market,” David Rosenberg, co-portfolio manager for U.S. and global high yield at Oaktree Capital Management, told Axios. “Now, I think people are starting to realize that maybe the Fed does exactly what they’ve been telling everyone they’re going to do for the past six months, and not lower rates so quickly. And if that’s the case, maybe waiting is not so smart.”

Indeed, historical analogues arguably suggest that more tightening is called for. Following 10 rate hikes over the past 15 months, the effective Fed Funds rate sits at just over 5%, while the core personal consumption expenditures index registered at 4.6% year-over-year in May. That near 50 basis point real rate sits just below the average 55-basis point spread going back to 1990. “We are probably not going to end the 40-year spike in inflation with an average real rate,” strategists at Bank of America conclude. “It has to go higher.”

…Economists Ander Perez-Orive and Yannick Timmer found last week that 37% of U.S. nonfinancial firms tracked by data firm Compustat are already in distress, up from just over 20% during the pandemic and the representing the highest share since the financial crisis.

Average Weekly Hours

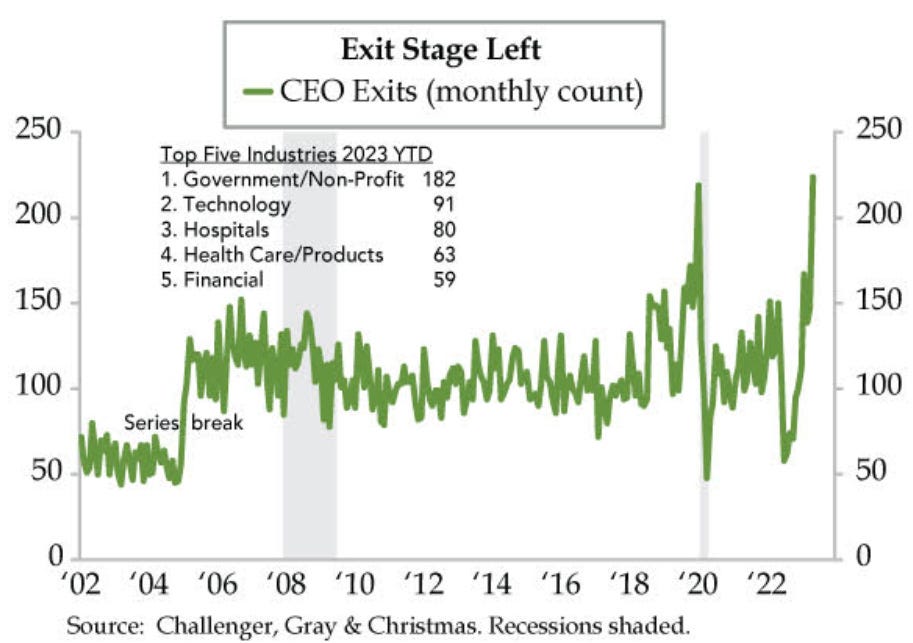

They probably all need money to paint their house(s):

"Successful investing is about having people agree with you ... later." - Jim Grant

This was amusing:

“The only thing that really matters in asset allocation is sidestepping some of the pain when the rare, great bubbles break.”

Amazing post. So rich - Blackstone Defaults - priceless. So much going on but been thinking a lot about RealPages. and that ProPublica article. These rent movements or lack thereof make no sense. Nashville in particular is very bizarre. Something has to break...And thank you so much for the support.

That photo with those 3 clown criminals. "I'll take who are operators of the greatest Ponzi scheme ever seen for $2000, Alex"