So “core” inflation has now been above the Fed’s make-believe 2% target for two solid years. Heckuva job, FOMC!

This is good. A concise must-read from Bill Bonner and Joel Bowman:

Between 1968 and 1971, gold was removed from the US currency. For the first time, dollars could multiply much faster than the things they could buy. Second, in the 1990s, the Fed began manipulating interest rates to boost asset prices. These two moves destroyed America’s prosperity.

Gold – or something like it – is essential to a capitalist economy. It links our ‘money’ to the real world of time, work, and resources. Before 1971, if you wanted more money, you had to earn it by producing more goods or services (GDP). Then, you had ‘capital’ that you could invest to build new shops and factories to produce even more goods and services. That was how the US became the richest nation on earth.

But the post-1971 dollar led to a new form of wealth – financial wealth. It was capitalism without real capital. Instead, it was based on credit provided by the Fed and the banks…This is what became known as the “financialization” of the economy.

Check out the entire article.

Along the same lines as the above…

You might think twice before trading lives with RFK, Jr. Both his father and his uncle were shot dead. How come? He must wonder.

Lyndon Johnson had the blood of thousands of Americans and maybe a million Vietnamese on his hands. Nobody shot him. George W. Bush’s hands are stained red too – a million corpses in the Middle East, and yet, he still breathes. And there is Joe Biden…providing billions of dollars, and the latest weapons, to keep the Russo-Ukrainian War going; where’s his Sirhan Sirhan…his Lee Harvey Oswald?

Normies care only about status, not facts, and when it comes to communications media status comes from high production values. An anti-war newspaper will have no advertisers. A pro-war newspaper will have advertisements from war profiteers. The mass media that works for Scams will always have higher production values than the honest ones, and so they are the ones that normies will believe.

Great interview on the JFK assassination. The host is so-so, but James DiEugenio, and David R. Montague, Senior Investigator for the JFK Assassination Records Review Board, are excellent.

Another winner: How we messed up Iran, the illegal and ongoing U.S. torture programs, Covid, Avril Haines, Gina Haspel, John Brennan, surviving prison, the Pentagon Papers and Vietnam, JFK, RFK etc...CIA Whistleblower John Kiriakou with RFK Jr.

Robert F. Kennedy, Jr. on who murdered his uncle. Note that RFK, Jr. has a vocal condition called spasmodic dysphonia.

Short clip of Robert F. Kennedy's son, talking about who he thinks killed his uncle (the CIA) and his father (not Sirhan Sirhan).

The very same NY Fed President John Williams:

Someone asked when was the last time we’d had a real crisis over the debt ceiling. Apparently in 1953 there was a delay, but to keep the lights on the government simply sold some of the gold they’d confiscated in 1933.

People forget that the United States defaulted three times in the 20th century: 1933, 1968, and 1971.

“Not unlike many households, the government is reliant on debt to fund its obligations,” said Mark Hamrick, a senior economic analyst at Bankrate. “And like many households, it doesn’t have sufficient income to fund its expenses.”

Hang on a second here! Geniuses have long told us that the U.S. government is NOT like a household at all, so which is it? So confusing.

Fortunately, we can just print infinite money.

Nobody saw this coming.

This entire century has been all about bringing demand forward.

Mad Money, November 15, 2021 (Affirm shares were at $148 - Mad Money indeed): CEO of buy now, pay later powerhouse Affirm says ‘treat people right,’ they’ll pay you back

Buy now, pay later (BNPL) apps such as Affirm, Klarna, and Sezzle are tightening credit standards to prioritize profitability over growth amid higher interest rates and recession concerns. Customers have reported unexpected denials or lower spending limits while attempting to make purchases. The BNPL companies, which market themselves as a transparent, accessible alternative to credit cards, have seen loans increase from $2 billion in 2019 to $24.2 billion in 2021 but have yet to make an annual profit.

Regulators and consumer advocates have warned that BNPL plans might encourage consumers to take on too much debt and lead to a pattern of overspending with sustained use. BNPL providers have had to slow down lending more than traditional lenders because they need to borrow from other lenders and investors to make loans.

The Federal Reserve's interest rate hikes have made it harder to offer consumers zero-interest installment plans. In response, companies have started cutting costs and getting pickier to avoid future loan losses. The delinquency rate of BNPL plans for borrowers aged 18-24 has been rising, reaching a high of 5.7% in 2021, while the average delinquency rate for consumer loans tracked by the Federal Reserve was below 2%.

New customers with lower credit scores and existing customers with a history of late payments are more likely to be rejected. Affirm began implementing tougher credit requirements about a year ago and has stepped up scrutiny several times since, at the expense of hitting some of its growth targets. The percentage of Affirm transactions that include interest fees rose to 67% in the most recent quarter, displacing the 0% transactions the company helped popularize.

Affirm’s delinquency rate is still surprisingly low. Let’s see where that goes.

Japan is adopting the Fed’s 2020 playbook:

BOJ Will End Yield Curve Control Once Stable Inflation Target in Sight, Ueda Says

“We would like to end yield curve control and then proceed to shrinking a balance sheet once we have an inflation outlook indicating that sustainable and stable 2% inflation will be achieved”

Gee that sounds familiar…

Now here’s a central bank that knows what it’s doing: Argentina’s!

And then there’s “average inflation targeting,” an idea so stupid that only someone with a doctorate in economics could come up with it.

Jim Bullard is a menace to society.

Watch now (2 min) | In case you never saw this, St. Louis Fed President James Bullard, who has been at the Fed since 1990, made these insane comments in January 2020. Bullard explains how the Fed was experimenting on 330 million Americans with "average inflation targeting,"

I mean, come on. Banning shorts is something only banana republics do, right? Oh, wait…

Nobody has any memory, but the $XLF fell about 70% AFTER the September 2008 SEC ban on shorting financials.

Federal Reserve Financial Stability Report, May 2023

It’s from the Fed, so take it with a grain of salt.

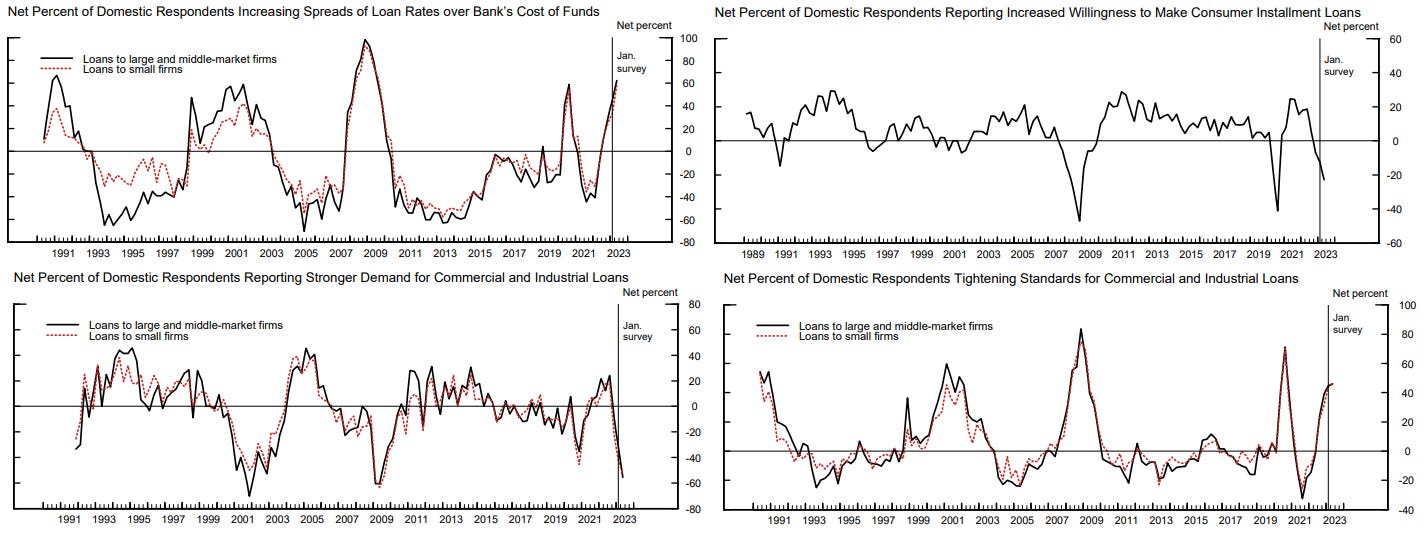

The April 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices

NFIB Small Business Optimism Index

Yesterday I mentioned a podcast with Ron Zeff, who, when asked about areas of worry, suggested construction loans.

Naturally I looked that up:

And while we’re at it, here’s some more color on bank CRE loans:

The silliest headline I saw Monday:

Bonds Backed by Apartments Are Under Stress as Housing Market Cools “The market has really changed for these people,” said Selina Parelskin, chief executive of Beacon Default Management, a company that helps lenders foreclose.

CLO’s!

This product, known as collateralized loan obligations, or CLOs, are mortgages packaged into bonds that are sold to investors. These mortgages helped fuel the rise in housing costs across Sunbelt states such as Arizona, Texas and Nevada, facilitating the purchase of buildings where property owners saw opportunities to raise rents.

Rental apartments accounted for two-thirds of the CLOs issued in 2021 and 81% of those issued in 2022, according to real-estate data firm Trepp.

The mortgages associated with CLOs appeal to property owners because they can put down less equity and take on more debt than with bank mortgages. They also have shorter terms and floating interest rates that make it easier for owners to sell or refinance their buildings after a few years.

But some of the same characteristics that made these loans attractive to property owners also made them riskier and more vulnerable to sudden changes in borrowing rates. Last year’s surge in interest rates, a softening rental market and rising expenses mean many landlords no longer earn enough money to pay back their loans.

Sounds like some wealthy apartment buyers need a bailout!

‘Frankly, the machine is shut down,’ says investor in key area of commercial real estate finance

If you’re having re-financing problems, I feel bad for you, son.

I’ve got 99 problems but your over-leverage ain’t one.

Hit me.

Are you sitting down?

US commercial real estate deal volume drops in Q1 Coming down from ridiculous multi-year Fed-spawned asset bubbles is hard!

Even for Canadians!

Brits are being offered no-deposit 100% mortgage loans for the first time since 2008

The Fed As Drug Dealer

Watch now (20 sec) | "I like to say that we injected cocaine and heroin into the system, and now we're maintaining it on Ritalin. How's that?” [LAUGHTER] former Dallas Fed President Richard "Dick" Fisher (now at Barclays), March 9, 2016

US office REITs trade at largest discount to NAV as of May 1

Maybe the NAV is wrong?

The Fed could be on the verge of repeating its 1970s mistake, Fed historian says

Yes. Every day I hear how the Fed’s big mistake has been returning rates to historically average levels, not the decade plus of ZIRP and QE. I’m sure this article reiterates this…what, what?

A premature retreat could cause the Fed to lose its handle on the situation, presenting even grimmer options down the road. That’s what happened in the 1970s, he said.

Quick rewind: The chair of the Federal Reserve at the time, Arthur Burns, hiked interest rates dramatically between 1972 and 1974. Then, as the economy contracted, he changed course and started cutting rates.

Inflation later roared back, forcing the hand of Paul Volcker, who took over at the Fed in 1979, Richardson said. Volcker brought double-digit inflation to heel — but only by raising borrowing costs high enough to trigger back-to-back recessions in the early 1980s that at one point pushed unemployment above 10%.

“If they don’t stop inflation now, the historical analogy [indicates] it’s not going to stop, and it’s going to get worse,” said Richardson, an economics professor at University of California, Irvine.

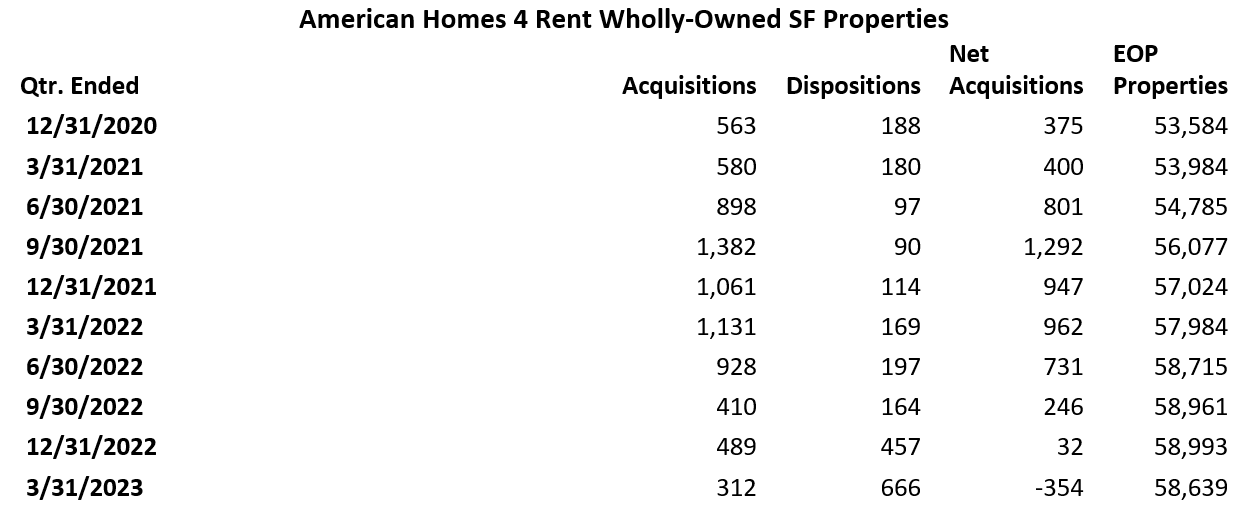

The question I have is who is American Homes selling to? Young families, or Stephen Schwarzman?

Rent increases reported by the largest single-family rental landlords:

Invitation Homes [INVH], in its earnings call for Q1 on May 2, said that rent growth in April showed “further acceleration” in newly executed leases:

April new lease rent increase: +7.5%

April renewal rent increase: +7.2%

April blended rent increase: +7.3%.

In terms of Q1, it said, “We have also seen stronger demand return following the winter leasing season, with new lease rent growth accelerating sequentially each month during the first quarter”:

Q1, new lease rent increase: +5.7%

Q1, renewal rent increase: +8.0%

Q1, blended rent increase: +7.3%.

American Homes 4 Rent [AMH], in its Q1 earnings call on May 5, said that “strong demand continues to fuel solid occupancy and rental rate growth,” in Q1 and continued in April.

April new lease rent increase: +9.4%

April renewal rent increase: +6.2%

April blended rent increase: +7.1%

Which were “well above our seasonal pre-pandemic norms,” it said.

Q1 new lease rent increase: +7.8%

Q1 renewal rent increase: +6.8%

Q1 blended rent increase: +7.1%

Here you can read people argue about the direction of the San Diego housing market.

I build 2-3 houses a year. The house I'm just finishing up had lumber cost roughly the same as the one I built of similar size in early 2018.

However, the carpenters were 30% more.

The drywall, installed, was 50% more.

The HVAC system was literally 2.5x more.

The plumber is now 30$ more per hour.

The electrician somehow stayed the same.

Ultimately, the last house cost 250k to build, this one will be 400k. (Ignoring land costs, permit fees, other things that aren't strictly Materials + Labor).

So.... lumber prices going back to where they were are not going to pull down prices. It'll help stabilize them I hope.

“Bill Wilby on the problems with U.S. Treasuries and why financials are uninvestable” Good diagnosis.

Stanley Druckenmiller | May 2023 | USC Marshall Keynote

Corbin’s Bergstrom on Credit Landscape: State of Distressed Debt “If an investment is going to be successful or not successful depending on whether SOFR or Fed Funds is at 4% or 5%, if that’s important it’s probably not a good investment for us.”

JPMorgan claims Jes Staley thwarted efforts to sever ties with Jeffrey Epstein

One Nation Under Blackmail with Whitney Webb | The Nick Bryant Podcast

Nick Bryant at the beginning of the interview asks Whitney Webb for an “overview” of her 900+ page, 2-volume book, “One Nation Under Blackmail.” I immediately thought of the opening passage to her book, a note from former CIA officer and Iran-Contra whistleblower Bruce Hemmings, circa 1990, from archived papers of the late journalist Danny Casolaro:

“Who are these people? They are the group that is popularly called the Enterprise. They are in and outside [the] CIA. They are mostly Right Wing Republicans, but you will find a mix of Democrats, mercenaries, ex officio Mafia and opportunists within the group. They are CEOs, they are bankers, they are presidents, they own airlines, they own national television networks. They own six of the seven video documentary companies of Washington, DC and they do not give a damn about the law or the Constitution or the Congress or the Oversight committees except as something to be subverted and manipulated and lied to.

They abhor sunlight and love darkness. They deal in innuendo and character assassination, and planted stories, the incomplete thought and sentence. They burn and shred files if caught, they commit perjury, and when caught they have guaranteed sinecures with large US corporations.

If you let them, they will take over not only [the] CIA but the entire government and the world, cutting off dissent, free speech, a free media, and they will cut a deal with anyone, from [the] Mafia to Saddam Hussein, if it means more power and money. They stole $600 billion from the S & L’s and then diverted our attention to the Iraqis. They are ripping off America at a rate never before seen in history. They flooded our country with drugs from Central America during the 1980s, cut deals with Haro in Mexico, Noriega in Panama, and the Medillin and Cali cartels, and Castro, and recently the Red Mafia in the KGB.

They ruin their detractors and they fear the truth. If they can, they will blackmail you. Sex, drugs, deals, whatever it takes.”

Nick Bryant wrote a brave book about the Franklin Scandal, described here: Still Evil After All These Years

This is a 1993 documentary on the Franklin scandal, "Conspiracy of Silence" Jeff Epstein was just another cog in a very big machine.

My new book is out, “How to Lose 90% of Your Money in Unpronounceable Swedish Property Companies.”

Steve Eisman was on a recent Twitter Spaces where he was asked about emerging markets, and he said something along the lines of, “There are plenty of companies I can be wrong on in the U.S. I don’t need to broaden that number.”

This is just amazing to me, and never discussed - the only groups where the labor participation rate has grown since 2000 is among the 55 and older crowd, and especially among those 65 and older.

Now I understand that America is aging, but I don’t think that 55.1% pop among the 65 and overs is entirely because they love their jobs at Carls, Jr.

Good thing inflation was non-existent until a year or two ago.

Speaking of working, here is the saddest article you will ever read.

I guess that weird issue with the low 1-month yield has been fixed…

I rate this post your best yet. It is such a dense download of central banking bullshit, mixed with evidence of outright wealth theft through financialization. I was finding it hard to control my rage near the end. David Bowie did help though.

What are you thinking posting that FRED graph? You will spark a revolution.

Thank you for the RFK Jnr links; he is always great to listen to.

I shared the Bruce Hemings quote and Franklin Scandal link with an Irish friend and she passed this on to me https://www.owleyes.org/text/modest-proposal/read/modest-proposal-by-dr-jonathan-swift#root-422325-33 with the view that ritualistic abuse of children has a long tradition, and wonders is Swift’s proposal truly satire or expose. Dublin was no stranger to dead or sold children in the 1800s