Heresies for Lab Rats

Wheat and Chaff

“These highs in the stock market may actually mark the lowest point for political morality and fiscal responsibility in our time.”

2015 Kansas City Fed paper on abolishing paper currency:

We're all just lab rats to these people.

“The most straightforward way to unencumber interest rate policy completely at the zero bound is to abolish paper currency.

In principle, abolishing paper currency would be effective, would not need new technology, and would not need institutional modifications. However, the public would be deprived of the widely-used bundle of services that paper currency uniquely provides—a generally accepted paper medium of exchange providing transactions services especially for low-value transactions; a readily accessible, safe liability of the central bank; a store of value; a degree of privacy in financial management; and the option to hold money outside the banking system and to withdraw deposits at par as paper currency in times of financial stress.

Hence, the public is likely to resist the abolition of paper currency at least until mobile access to bank deposits becomes cheaper and more easily available, ATM charges for access to paper currency become excessive, and/or electronic currency substitutes become widely available.”

In other news…

Can someone explain to me how the public is allowed into the New Orleans killer’s house the day after his attack? This makes no sense, and the entire thing looks staged to me.

Dad: "This is $500?"

Daughter: "It's normally $600."

Dad: "No it's not. It's abnormally $600."

OK, sports fans - the last two months have been rather boring (at least for a longer-term caveman-type speculator like me.)

My market call for 2025 is that prices will fluctuate, and I think mine will be one of the more accurate calls you’ll come across. Godspeed.

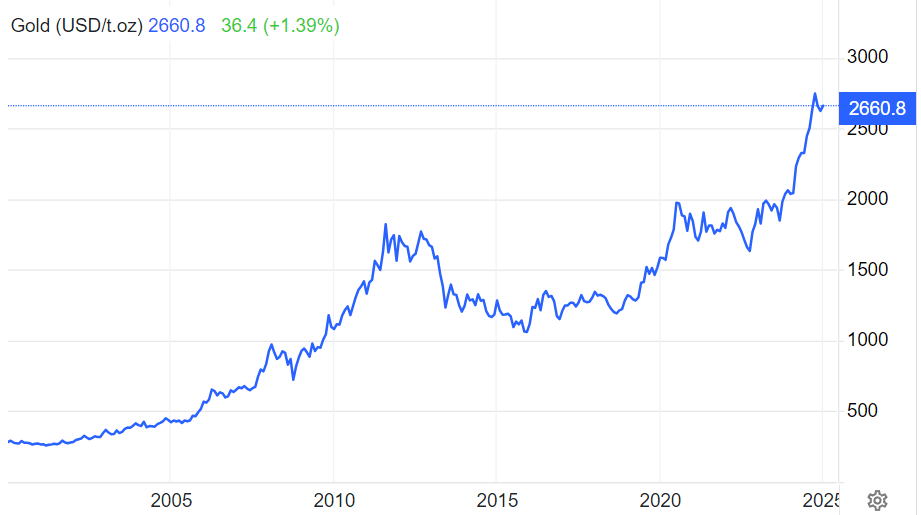

Although commodities have done ok…

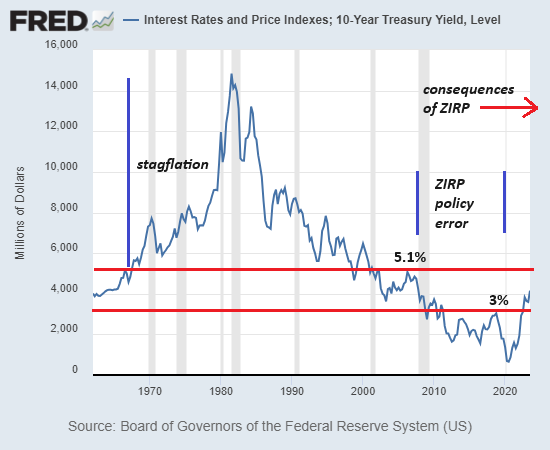

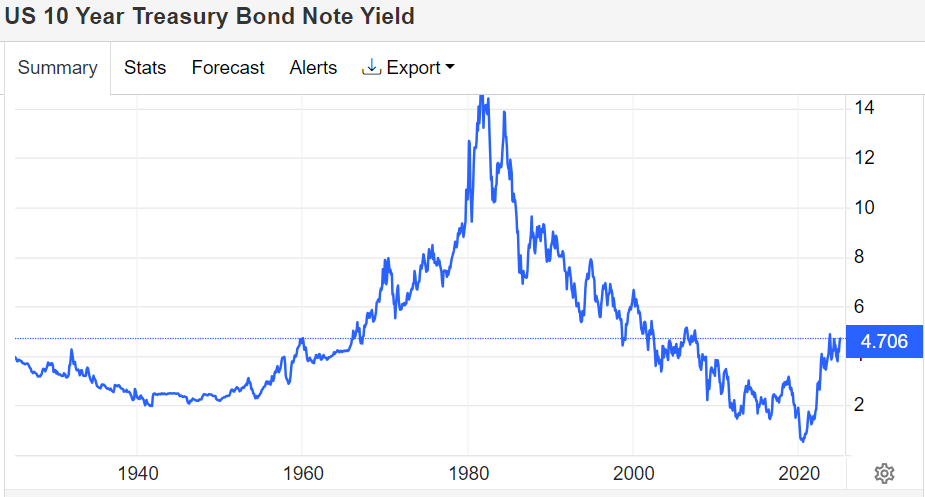

And everyone’s getting worried about (or completely dismissing) the ten-year move:

I’m just waiting for January 20 to pass so we can begin to try to separate the wheat from the chaff.

Jason Shapiro on "what's clearly driving this whole thing"

Private equity to lobby Trump for access to savers’ retirement funds

“the industry is seeking to…allow tax-deferred defined contribution plans such as 401ks to back unlisted investments such as leveraged buyouts, low-rated private loans and illiquid property deals…”

“Blackstone joins private equity deal wave in US accounting sector”

“A Blackstone-led investor group is buying a majority stake in US accounting firm Citrin Cooperman, in a deal that gives the target an enterprise value over $2bn and marks a significant step up in valuations across the sector. Blackstone has acquired the stake from smaller rival New Mountain Capital…

New Mountain was one of the first major private equity groups to invest in the US accounting sector when it purchased a controlling stake in Citrin Cooperman in late 2021, in a deal that gave the accountancy group an enterprise value of about $500mn. Its sale has been keenly awaited in the sector for a signal on valuations.

Two people familiar with the matter said Blackstone was buying Citrin Cooperman at a multiple of around 15 times earnings before interest, taxes, depreciation and amortisation, compared with New Mountain’s initial acquisition at 11 times ebitda.”

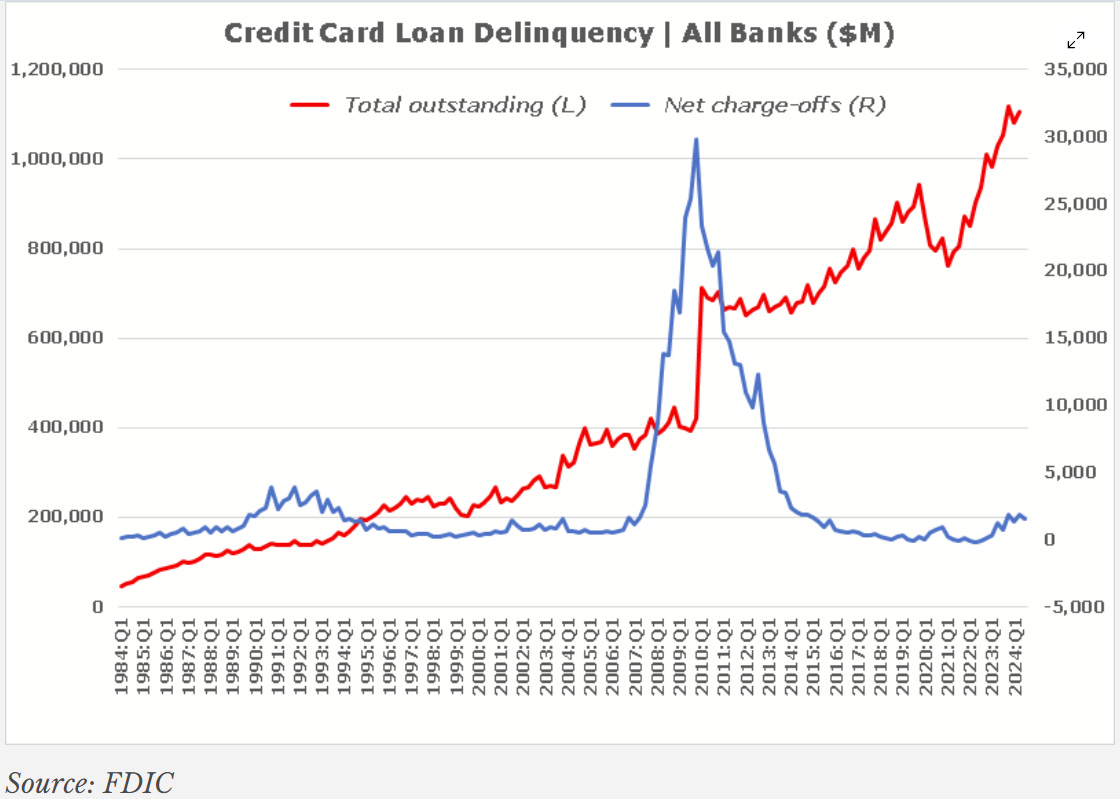

Chris Whalen on Credit Card Delinquencies

”Look at that chart [above] that shows those net losses for credit cards, going back 40 years, and what you see is that the credit card market that's issued by banks has gone up almost three-fold since 2008, yet the level of net loss - which we call charge-offs, net charge-offs - has basically been flat. So other than 2008, which was quite a horrific loss event, the numbers haven't been that bad. I have a lot of friends in the market, who I love dearly, who keep predicting the end of the world, and I look at the data and it just doesn't show that. We looked at the top six consumer lenders - they're basically flat revenues, good funding, costs have stabilized, net losses are flat. They have not shown any degree of uptick that we've been waiting for. I mean, every analyst that I know has been waiting for this hockey stick in consumer delinquency - credit cards, autos - hasn't happened yet. My suspicion is that consumers are cutting back on discretionary items, and they're trying to remain current on credit, because they don't want to lose their car. They don't want to lose their home. These are the things that they're going to defend, whereas they may stop spending money on going out the restaurants…”

Also:

“There's a lot of continuing inflation in the system. The question is, is anybody at the Fed or any of the other monetary authorities around the world willing to tighten enough to get rid of it, and the answer is no.”

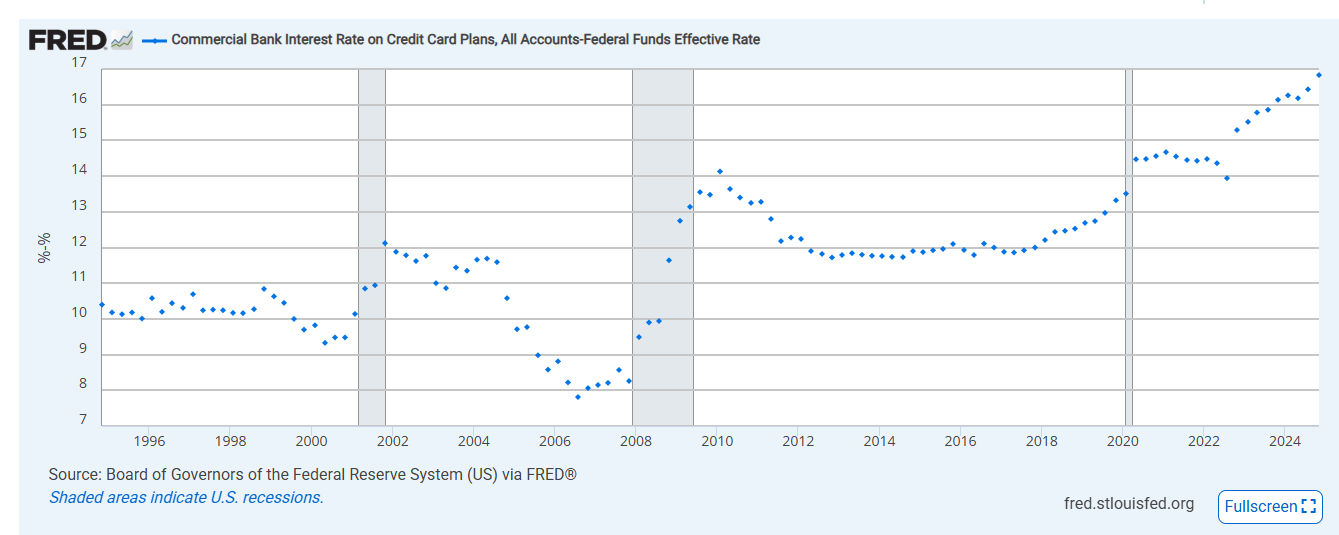

A 16.8% spread on credit card rates above the Fed Funds Rate!

I find this chart incredible (I used the ‘edit graph’ function to get this): Commercial Bank Interest Rate on Credit Card Plans, All Accounts minus the Federal Funds Effective Rate (as of November 2024, the latest Fred data.)

LendingTree tells me the average rate at this moment is 24.26%.

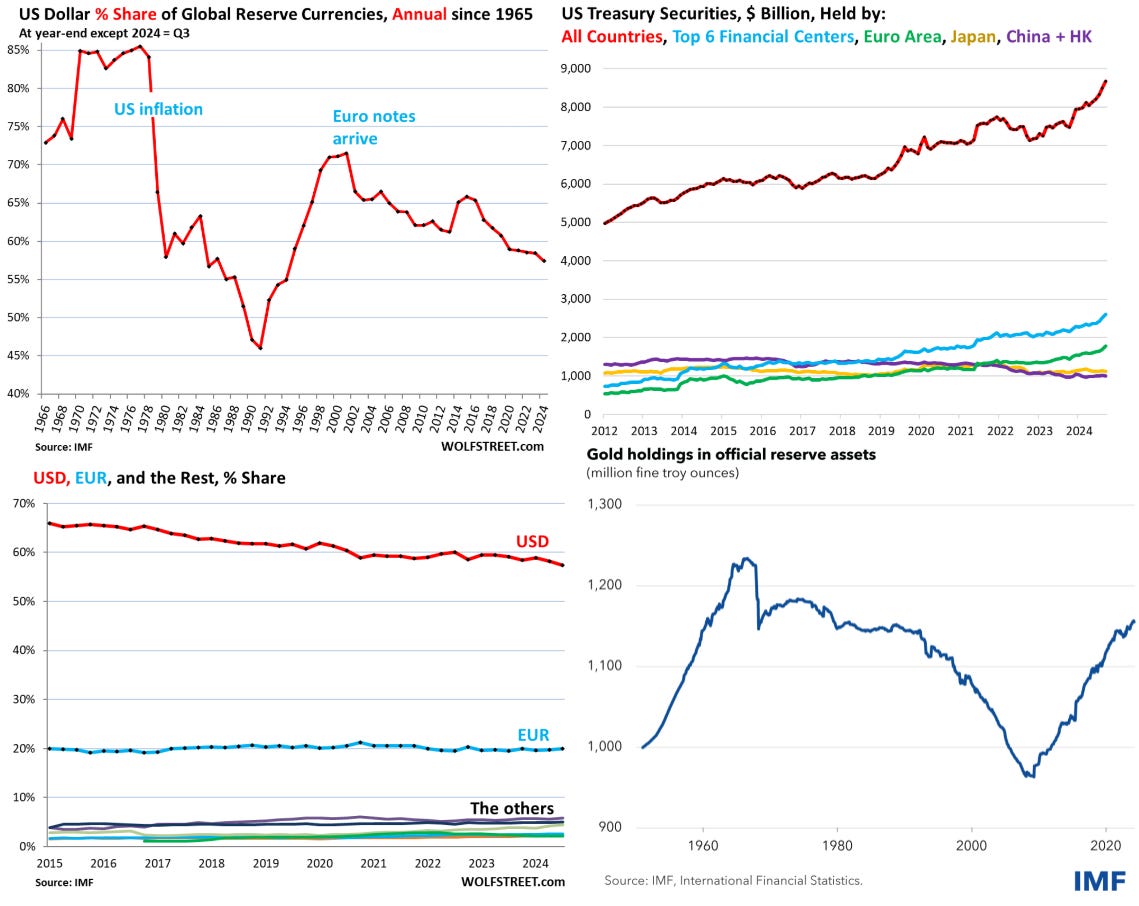

The Dollar as Reserve Currency

I still accept dollars.

1969 book, Death of the Dollar

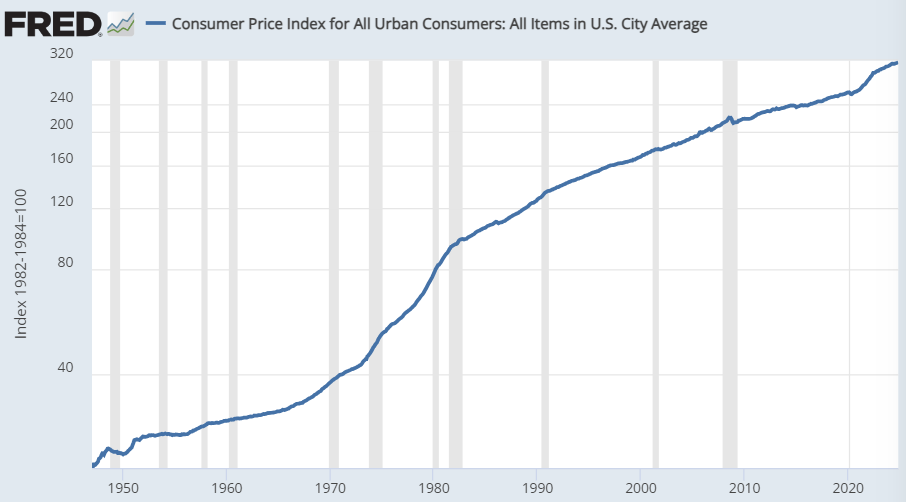

So the dollar didn’t die, but since the U.S. went off silver and then gold in the 1960’s and 1971, the purchasing power of the U.S. dollar has been massively debased (i.e., inflation). No brakes any longer.

And this chart below is assuming that the BLS’ intentionally understated model is accurate. The true picture is far worse.

Via RationalWalk, a timely passage from Aristophanes Frogs, first performed in 405 BC:

I’ll tell you what I think about the way

This city treats her soundest men today:

By a coincidence more sad than funny,

It’s very like the way we treat our money.

The noble silver drachma, which of old

We were so proud of, and the one of gold,

Coins that rang true (clean-stamped and worth their weight)

Throughout the world have ceased to circulate.

Instead the purses of Athenian shoppers

Are full of phoney silver-plated coppers.

Just so, when men are needed by the nation,

The best have been withdrawn from circulation.

Charles Hugh Smith: High Interest Rates Are Healthy, Low Rates Are Poison

“Low rates are now essential to prop up the wreckage left from previous doses of default and cascading losses.”

“The economy prospers when marginal borrowers doomed to default are excluded and risky ventures doomed to fail are tabled. Low interest rates and loose credit inject default and catastrophic losses into the system, and as these defaults and losses ripple through the tightly bound financial system, they trigger other defaults and losses, forcing financial authorities to reward the losers with bailouts: the profits skimmed from risky lending and investments are private, but the losses fall on the taxpayers and the public.

IN effect, the big players in the casino can go ahead and gamble on high-risk bets, knowing the house will cover their losses. The individuals sucked into margin debt, pyramided debt and risky gambles will be wiped out--no bailout for you--while those that enabled the casino are saved from the consequences of their risky gambles.

The Federal Reserve moved Heaven and Earth to push interest rates near zero and open the credit spigots as the means to "grow the economy." Depending on more poison to treat the previous poisoning is itself a risky gamble. As with real-world fentanyl, whether the dose of financial fentanyl is lethal or not is unknown until it's too late.

High interest rates and tight credit are healthy, low rates and loose credit are sugar-high poison. The status quo has it backwards: low rates are now essential to prop up the wreckage left from previous doses of default and cascading losses.”

Why Deflation Is Good for the Economy

“Whenever the central bank artificially inflates money into the economy this benefits various individuals engaged in activities which sprang up on the back of the expansionary monetary policy, at the expense of true wealth-generators. Through expansionary monetary policy, the central bank gives rise to a class of individuals whose ventures could not come into existence without continued inflation and which distort the structure of production.

The consumption by these recipients of the newly generated money and credit is made possible through the diversion of real savings from wealth producers. Through this process, these recipients divert production, saving, and capital investment without contributing anything in return.

The expansionary monetary policy of the central bank generates an environment where it appears that it is possible to consume without production. Not only does the easy-money policy raise the prices of existing goods, but monetary inflation also gives rise to the production of goods and assets which would otherwise not be the case. These goods are not demanded in those amounts and/or prices by consumers.

Once the central bank reverses its expansionary monetary policy, the diversion of production from wealth producers to non-wealth producers is arrested. This, in turn, undermines the demand of non-wealth-producers for various goods and services thereby exerting downward pressure on their prices.

A tighter monetary policy undermines various activities that sprang up the previous expansionary monetary policy. This partially halts the bleeding of wealth generators. The decline in prices comes in when prices realistically realign with the new production caused by previous inflation. Deflation during recession signifies the beginning of economic healing…

Contrary to the popular view, deflation is good for the economy. Thus, when prices are declining in response to the expansion of wealth, this means that individuals’ living standards are rising. Further, when prices decline because of the bursting of a financial bubble, it is also overall good for the economy, for it indicates that the impoverishment of wealth producers is being arrested.”

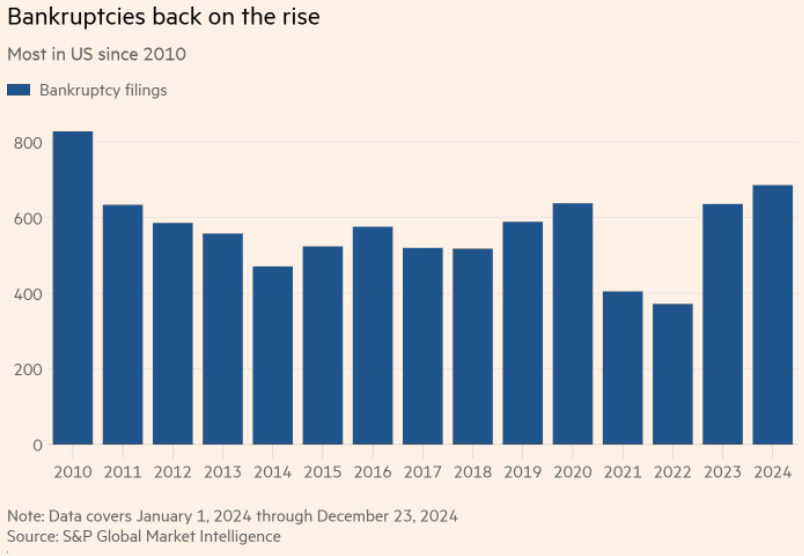

Which businesses do you see going bankrupt in the next 2-3 years and why? Some short ideas for the insane.

Bankruptcies

“The collapse of party supply retailer Party City was typical of 2024 corporate failures. In late December, it submitted its second bankruptcy filing in as many years, after emerging from Chapter 11 proceedings in October 2023.

Party City said it would shut down its 700 stores nationwide after struggling “in an immensely challenging environment driven by inflationary pressures on costs and consumer spending, among other factors”."

“Corporate borrowers are looking to get while the getting’s good, with investment-grade supply in the U.S. poised to reach $200 billion in January, if Bloomberg-compiled estimates of Wall Street dealers prove accurate, the highest on record for the opening month of the year.

“Issuers are taking advantage of calm markets, low volatility and tight spreads before January 20th,” Palinuro Capital CIO Alfonso Peccatiello told Bloomberg, referencing Donald Trump’s imminent return to the Oval Office. Option-adjusted spreads on the ICE BofA US Corporate Index settled Tuesday at 84 basis points, down from 108 basis points at this time last year to hover near their tightest of the post-Lehman Brothers era…

The post-Covid era has proven decidedly unremunerative to long-dated Treasury bulls, as the iShares 20+ Year Treasury Bond ETF has generated a minus 37% total return over the past four years. During that stretch, the lynchpin vehicle has seen net assets climb to just under $50 billion from $18 billion in January 2021.

“By now, plenty of faces have been ripped off by the most recent bond-market tantrum,” Thomas Tzitzouris, director of fixed income research at Strategas, commented to Bloomberg. “Even though we’d love to say that the worst is over, there’s no indication that shorts are exhausted or that data is supportive” of a rebound. Tzitzouris added that the combination of upward pressure on yields with the narrowest default-risk compensation for corporate creditors of the cycle leaves both speculative and default risk-free assets in the “danger zone.””

Sorry, I have to:

Speaking of Rates

Trivia

Since January 5, 1962 (where the FRED dataset began, 3,289 weeks), the average U.S. weekly 10-year yield is 5.85%, and the median is 5.555%. At this second we are at 4.69%.

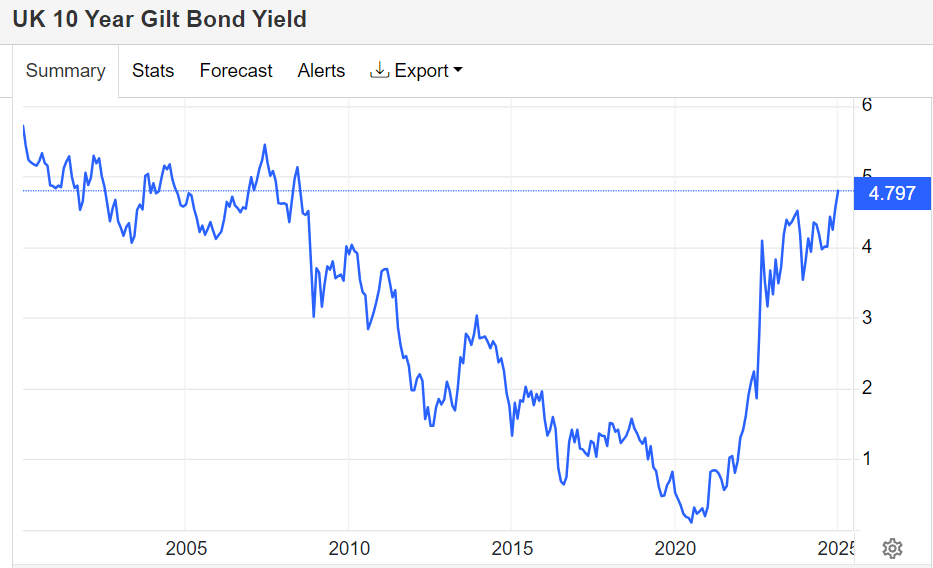

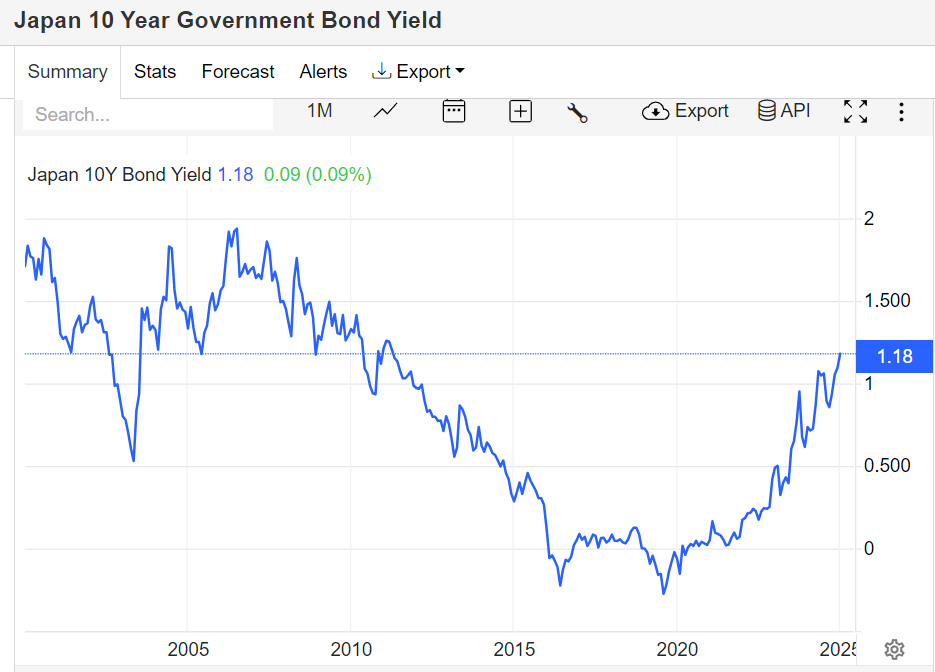

Might as well do some currencies…

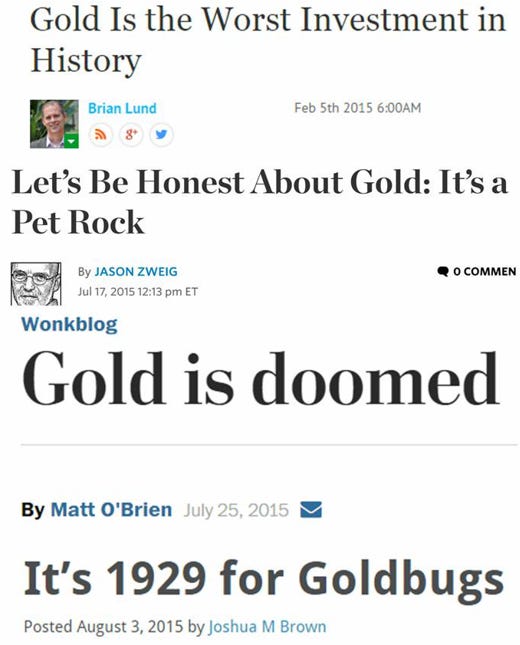

Remember these headlines? I do.

Austin

It’s just one small development, but I used to see many videos just like this one, back before the housing bubble before this housing bubble burst.

From July 2024: 'What the heck happened?' Concerns grow over unfinished South Austin development

If you go to the website listed above - which presents a slightly different situation - it appears these homes were/are listed in the $400k to $500k range.

Some more color here, from last year:

I was researching a claim in a book, and discovered that someone else had already researched the exact same claim from the same book. It’s a good overview of something I do all the time - try to find original sources.

Trust but verify.

Legalized Gambling

“When you start writing to satisfy someone's algo, you've stopped being original.”

Plus ça change, plus c'est la même chose.

Here's a 2-hour BBC Radio 1 mix from 1995, apparently done by Portishead...

Playlist in the comments…

Great piece!

The gambling chart was very informative, not unexpected, but unreported.

Great post.

Here is the video Travis and I did on the abandoned site in Austin: https://youtu.be/L9YsN6MP1_w?si=cNSbFQQ8gOohJppH

When I posted it last year one commentor said I should be ashamed of showing it as it was potentially detrimental to the business owner. I said if the business owner was concerned they would have cleaned up the site.