If it's such a great trade, why are you offering it to me?

None of this is true.

“In 1925, Britain was the richest, most powerful country in the world. Fifty years later they were bankrupt. That's not a typo. In 1976 the IMF had to bail out Britain, because they went bankrupt. They literally couldn't pay their bills.”

Thomas Massie

Justin Amash

“The usual suspects in the “conservative” influencer griftosphere are shouting, “What’s the practical alternative? Trump’s hands are tied by Congress!”

The idea that Trump is somehow hamstrung by a GOP Congress that treats him like a deity is beyond ludicrous.

Trump has been demanding passage of precisely this bill, the one he nicknamed the Big, Beautiful Bill. He has threatened to primary anyone who opposes it.

The practical alternative is for a Republican president to use his position of considerable influence to actually get spending under control. Just once, maybe, he could demand real spending cuts.

Trump had every political advantage this term—a Republican Congress, Elon Musk and DOGE, and post-election momentum. Yet he chose the most impractical route of all: insisting that Congress continue its massive overspending, pushing the United States further down the path of a debt crisis.”

Get in the Bunker.

The co-founder of ChatGPT maker OpenAI proposed building a doomsday bunker that would house the company’s top researchers in case of a “rapture” triggered by the release of a new form of artificial intelligence that could surpass the cognitive abilities of humans, according to a new book.

Ilya Sutskever, the man credited with being the brains behind ChatGPT, convened a meeting with key scientists at OpenAI in the summer of 2023 during which he said: “Once we all get into the bunker…”

A confused researcher interrupted him. “I’m sorry,” the researcher asked, “the bunker?”

“We’re definitely going to build a bunker before we release AGI,” Sutskever replied, according to an attendee.

The plan, he explained, would be to protect OpenAI’s core scientists from what he anticipated could be geopolitical chaos or violent competition between world powers once AGI — an artificial intelligence that exceeds human capabilities — is released.

“Of course,” he added, “it’s going to be optional whether you want to get into the bunker.”

For all intents and purposes, the Fed has stopped tapering their Treasury Holdings.

Live stream of the Fed's balance sheet unwind

“The United States federal government intends on borrowing another $86 trillion over the next 10 years, which is an absolute impossibility, quite frankly.”

“The bottom line is my cohort and others around us just wanted to spend a lot of money, and didn't want to pay for it.”

Maya MacGuineas, President of the Committee for a Responsible Federal Budget

How many U.S. Treasuries do China and Japan combined own? Maybe $2 trillion at most?

Since 2008 the Fed's monetized about $3.7 trillion of Treasuries, using fun coupons, or asset swaps, or something. They own $4.21T at this moment.

I'm not counting the $2.1T of MBS they still have (they had $0 in 2008.)

“Who's the Fed’s current person in charge of fighting inflation, who now sounds hawkish? It’s the same guy who was buying $50 billion of mortgage-backed securities in 2021, when we had 9% inflation, and home prices were up by 25% YOY. I mean, how can you seriously say that you are committed to fighting inflation when you let that happen?”

Heck, the Fed bought almost a HALF A TRILLION DOLLARS of MBS in just three months in early 2020, using air money, or something.

They owned $0 until 2009.

The 4th Branch of Government

"If there must be madness, something may be said for having it on a heroic scale."

From Pickleball Paradise to Investor Nightmare: Inside the 'Bell Bank Park' Fraud Scandal

“…defrauding investors out of more than $280 million by using forged documents, inflated revenue projections, and fictitious commitments from sports organizations—including some from the pickleball world—to sell municipal bonds funding the project.”

“The point of Economics is to create a language for discussing politics that excludes ordinary people.”

Matthew Stoller

I’ll get this one out a bit early, because I hope to get out of town for Memorial Day, and will try not to pay attention to any nonsense, at least until the middle of next week.

For my 81 million paid subscribers, I have a blistering William White Fed critique, a number of charts - mostly housing related - with updates on Denver, Austin, Florida, Galveston etc.

Check out the Apollo housing report (and more on Apollo), another great Melody Wright interview, Todd Sachs, reaching for yield, FHA subprime, CRE madness, private credit and private equity are coming for your money - privatize profits and socialize losses! Also Jamie Dimon, debt(!), and more.

William White

“I want to raise is the possibility that there's something wrong with the fundamental assumptions on which the inflation targeting framework is based. We actually live in a world of complexity, as opposed to the kind of simple world that most Central Bank models seem to to assume that we live in.”

“The first point I guess I would make is that if you've got a positive inflation target, it ensures that price levels drift upwards. So if you've got a framework that basically says we can't tolerate prices going down - even though they ought to go down, because of increases in productivity, or other positive supply-side shocks - the prices are never allowed to go down. They're only ever allowed to go up. You get this constant upward drift in the level of prices that people find really quite disquieting.” [Gee, where did the weird populism come from? - rh]

“The second point - again, looking back over the last 20, 30 years - successive bouts of monetary easing have become ineffective, so that if you look at successive cycles, what you see is that each cycle - the degree of monetary easing, the Vigor with which the easing takes place - has become larger and larger. The reason why that is so is because the way monetary policy works is it induces people to take out debts to receive the money that they can then use for spending. Over periods of time that buildup of debt gets higher and higher and higher, especially if safety nets don't really allow the debt to be reduced.”

“The third point - and I think this might even be a worse outcome - again, a longer run implication of of the way in which policy is conducted is that you eventually get debt levels, both public and private, that become so high that the system becomes incapable of of dealing with higher for longer, or, above that, incapable of dealing with even higher interest rates. I call it financial and fiscal dominance. Financial dominance is when private debts are so high the central bank is afraid to raise interest rates higher, because it will threaten the stability of the financial system. Fiscal dominance refers to the situation in which debt levels are already so high that if you were to raise interest rates higher, you would generate fears of increasing inflation, not decreasing inflation, as the government has to turn to the central bank to print more money to finance itself . So we have a problem here if the debt levels are high enough you can't raise interest rates because of fear of setting off these problems.”

“Another point - again looking back over the last 20 or 30 years - inequality has increased, and in part I think it's because when you lower interest rates, you raise asset prices, and the assets belong to rich people, so the gap in terms of wealth becomes greater and greater, and at the same time, looking back over the last 20 or 30 years, what we do see is that in all the advanced market economies, potential growth is decreased. I think that's something to do with what Hayek called malinvestment, that when you have very easy monetary conditions, people invest their money in in rather stupid ways, and potential growth suffers in consequence.”

“My conclusion from all of this is that the underlying analytical framework

needs re-thinking. The fundamental error is that all of the models have been set up - the analytical frameworks - basically assume that the economy is a machine, that it's simple, it's understandable, and it's controllable, and the problem is that none of these things are true. In the course of simplification, so much stuff has to be stripped away in most of the models that are being used - there's no financial system, basically; the supply side is is very, very oversimplified; and then in order to make these models what they call tractable, you have to make a

number of other sort of simplifications. All the functions are linear. We know the probability distributions of all these functions. Nothing changes over time. The economy has a natural tendency to to go back to equilibrium, at full employment, to the inflation target that the central bank has laid out. The problem is none of this stuff is true.”

What is true is that the economy is is not a machine, it's a forest. That is to say that it is a system made up of millions of interacting agents, all observing what

others are doing, and learning from them, changing their decision processes over time. These kinds of systems have been well studied in many many other disciplines, and these systems referred to here as complex adaptive systems have properties which are totally different from the properties that I've just described as underlying the current inflation targeting frameworks. These complex adaptive systems have nonlinear properties - that is to say that they have tipping points. Things can start to go wrong, and go wrong very badly. They are models in which uncertainty prevails, not risk, and once once you define a function as having well understood probability functions, you're basically saying you know what the risks are. That's a very different thing from uncertainty as Frank Knight and Keynes originally made that distinction. Uncertainty is a world in which you have no idea what the probability function is, and in these complex adaptive systems like a forest, there's there's no equilibrium either. You don't have this delightful property where the system itself goes back to doing things that you want it to do. Put otherwise, in the framework that we have that underlies inflation targeting, really bad things can't happen, whereas the assumption of complex adaptive systems these are systems with nonlinear properties, in which really bad things can happen, and once you make that distinction between the properties of the system that we currently assume, as opposed to the properties that are held by complex adaptive systems, then you have not only different models… but you need radically new approaches to policy.”

William White sounds very Austrian in the above, which must terrify and anger many of his former colleagues. I’ve quoted him a number of times before - he’s an insider who’s also quite an erudite maverick.

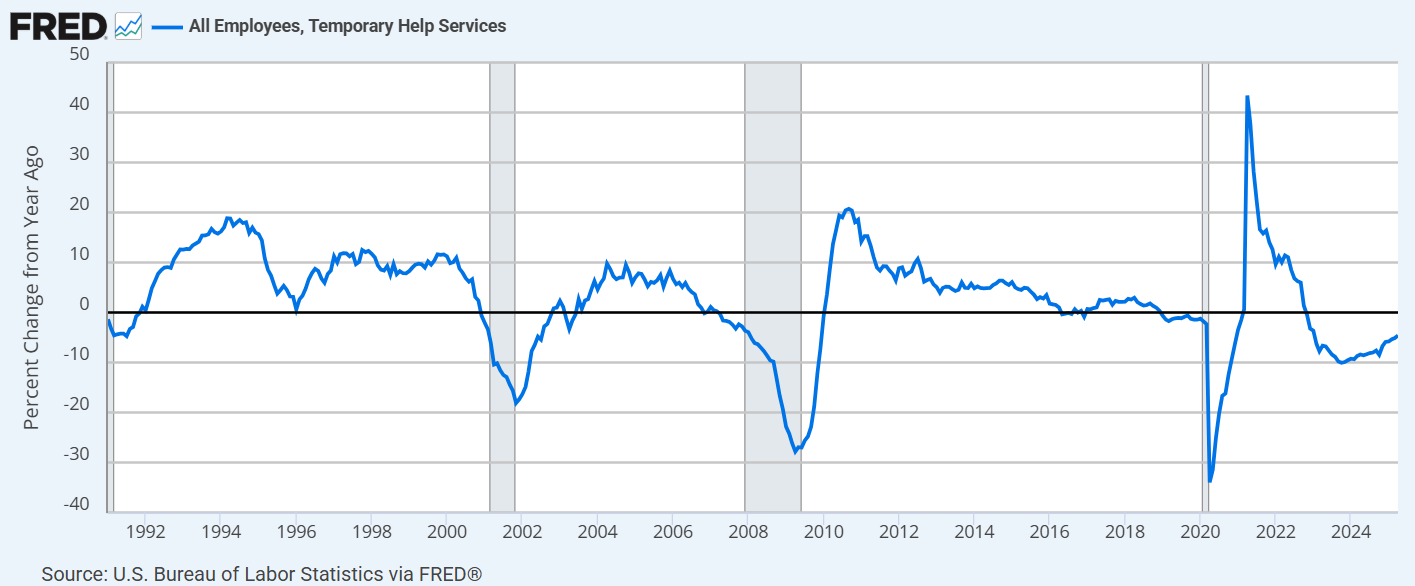

Temporary Help Services, % Change YOY

Haven’t checked this in a while. No gray recession bar, yet…

“We wrote about an apartment property in Tampa, Florida yesterday, where gross revenues had increased by 50% over the past 5 years or so, but expenses had increased by substantially more. Rent growth is nice, but if your expenses are growing at the same rate you're not winning.”

Orest Mandzy, Managing Editor of CRE Direct

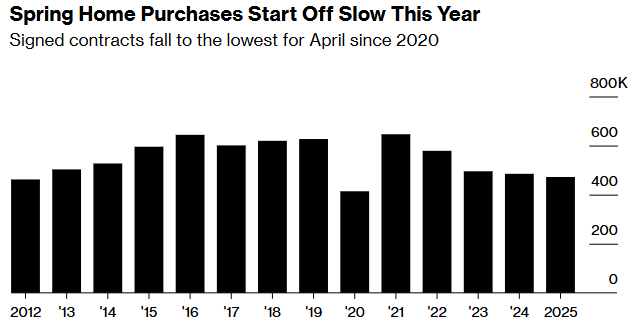

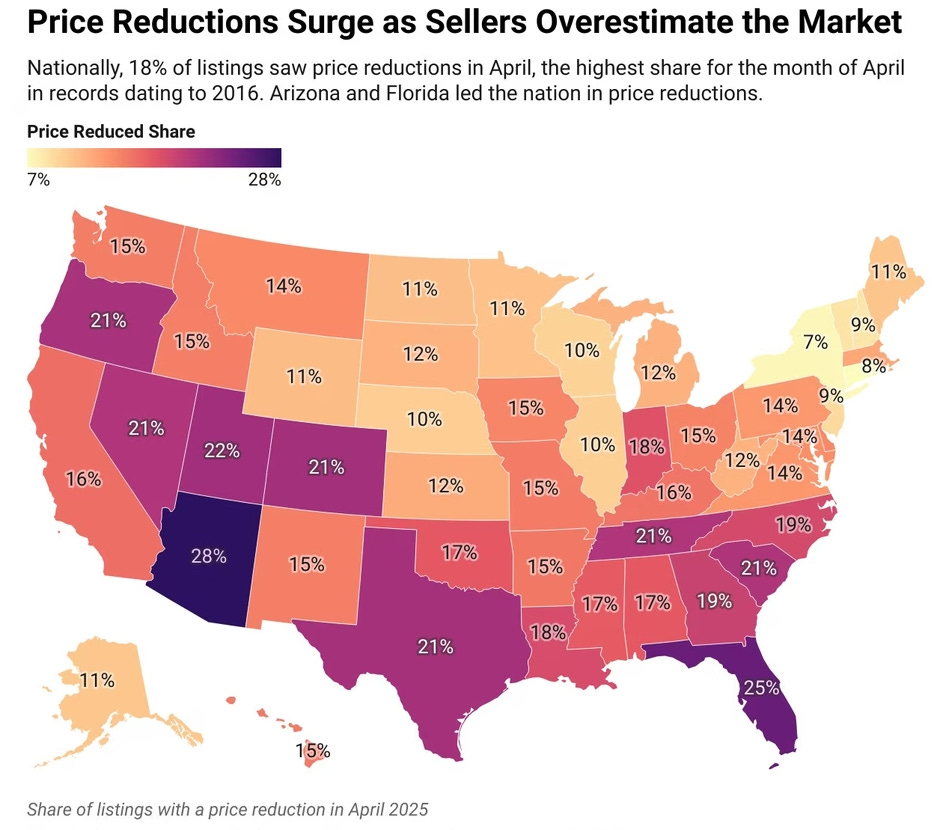

US Spring Homebuying Season Has Its Weakest Start in Five Years

"The rising share of price reductions suggests that a lot of sellers are anchored to prices that aren't realistic in today's housing market," says Realtor.com Chief Economist Danielle Hale. “Today's sellers would be wise to listen to feedback they are getting from the market.”

Apollo U.S. Housing Outlook

Median age of all homebuyers is now 56 years old, compared to 31 years old in 1981.

Tragic.

Median age of first time home buyers now sit at 38 years old vs 30 years old in 2008

Wow, this seems high. Wonder if this includes HELOC’s.

Real Estate Broker Todd Sachs on how the housing market got so screwed up:

“The Federal Reserve manipulated rates.”

The rest of this podcast is mostly about Florida.

I sometimes hear real estate agents say, “I’ve never seen this before!”

Florida

Citrus County homebuyers left with unfinished homes as builder files bankruptcy

2006 vibes…

“It was a dream, but a Citrus Springs home is now Frank Sherrill’s nightmare. “I need flooring. I need all the baseboards put in. All the framing for the doors,” he said of the unfinished home on Vespero Street.

He hired Van Der Valk Construction, a Citrus County-based homebuilder, in September 2022, but almost three years later, the work still isn’t done. Months ago, the work seemingly stopped.

Then, on April 30, Van Der Valk Construction filed for Chapter 11 bankruptcy. Now, Sherrill’s dream home is officially an unfinished money pit, filled with most of his retirement savings…

Van Der Valk is also building many homes in Inverness Village 4, a Citrus County neighborhood that has attracted constant criticism for years, because it was built without paved streets or a drainage system….

Inverness Village 4, the recent bankruptcy has also left dozens of home buyers in limbo, including Dyandria Darel. “I’m devastated,” she said.

Darel was planning to move from New York City to Inverness Village 4, which should have been her Florida retirement home. “It’s not only a retirement home, it was virtually my entire life savings,” she said. “I put the money down on this house in 2022. It’s now 2025.”

More than two years after she made her first payment, the home is unfinished and is now shrouded by a forest of weeds. The house still isn’t enclosed, and Darel has no indication she will ever live in it.”

Evacuations ordered at Clearwater high-rise after structural crack discovered

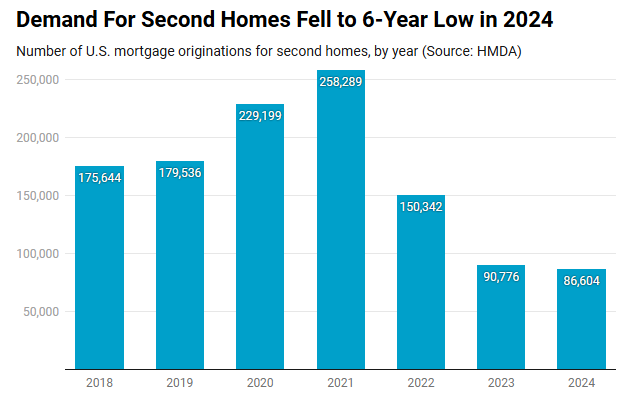

Demand for Second Homes fell to 6-year low

$373,200 income required to buy Orange County home, up 129% in five years

“The annual income required to purchase a typical California house has nearly doubled over the past five years.”

It’s ok though because everyone’s income went up 129% too!

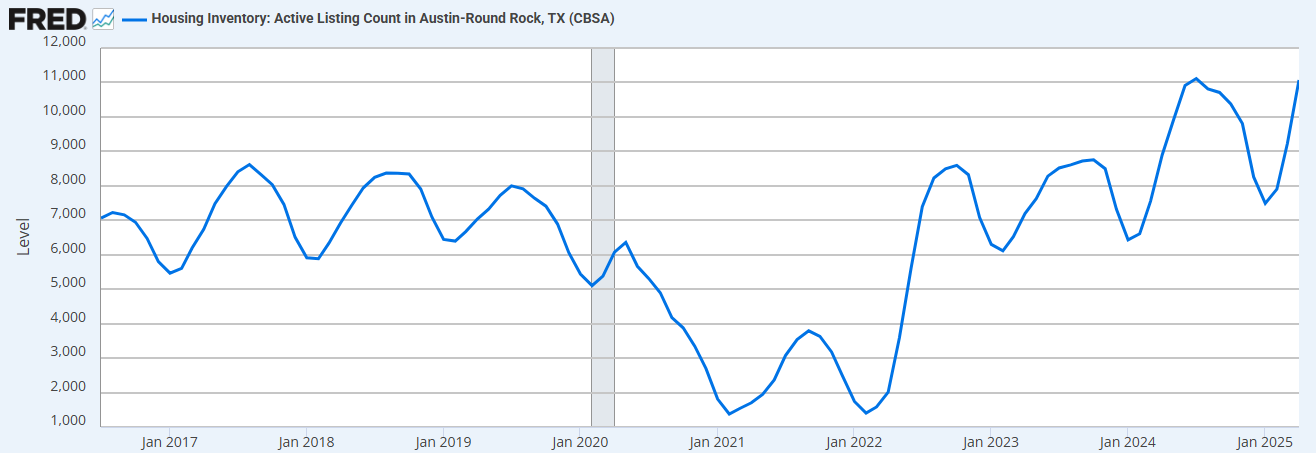

Denver

We cannot allow this deflation or the system will implode!

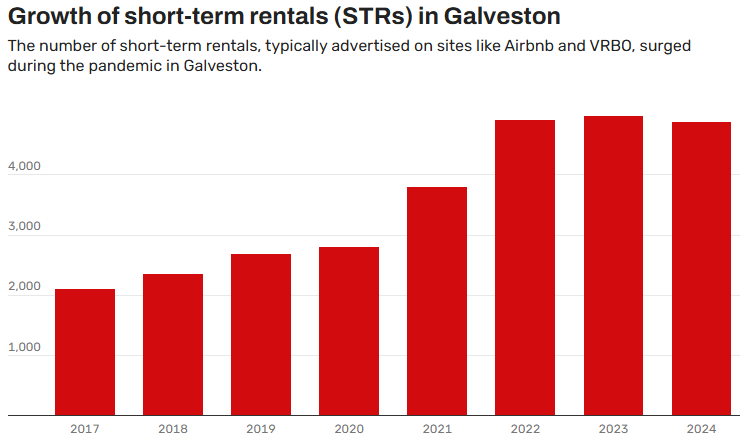

Galveston may be the Houston region’s biggest buyer’s market as a wave of Airbnbs floods listings

“We didn’t expect this,” said Linda Stickline, who has bought and sold multiple homes in the Houston area and Galveston over the years, always managing to sell quickly. Even after successful open houses, the Sticklines still haven’t received an offer. “This isn’t how it usually goes for us, so I think it’s a tough one.”

Although the $1.05 million asking price puts the home in the luxury range, the Sticklines’ broker, Tom Schwenk, said, “I don't think that the price is what's really stopping anyone anyway.”

“Nobody’s really even looking,” Linda Stickline added.

Sellers like the Sticklines are competing with a wave of vacation rentals hitting the market thanks to a surge in short-term rental owners looking to offload their properties. For some, the demands and costs of operating short-term rentals can outweigh the rewards.

“Galveston is a lovely place…but we're not the Hamptons”

How a “We Buy Ugly Houses” Franchise Left a Trail of Financial Wreckage Across Texas

Ronald Carver was skeptical when his investment adviser first tried to sell him on an “ugly houses” investment opportunity eight years ago. But once the Texas retiree heard the details, it seemed like a no-lose situation. Carver would lend money to Charles Carrier, owner of Dallas-based C&C Residential Properties, a high-producing franchise in the HomeVestors of America house-flipping chain known for its ubiquitous “We Buy Ugly Houses” advertisements. The business would then use the dollars to purchase properties in which Carver would receive an ownership stake securing his investment and an annual return of 9%, paid in monthly installments. “Worst case, I would end up with a property worth more than what the loan was,” Carver said of the pitch.

Carver started with a $115,000 loan in 2017. And sure enough, the interest payments arrived each month. He had worked three decades at a nuclear power plant, and retired without a pension and before he could collect Social Security. He and his wife lived off the investment income.

The deal seemed so good, Carver talked his elderly father into investing, starting with $50,000. As the monthly checks arrived as promised, both men increased their investments. By 2024, Carver estimates they had about $700,000 invested with Carrier.

Then, last fall, the checks stopped. The money Carver and his father had invested was gone.

Carrier is accused of orchestrating a years long Ponzi scheme, bilking tens of millions of dollars from scores of investors, according to multiple lawsuits and interviews with people who said they lost money. The financial wreckage is strewn across Texas, having swept up both wealthy investors and older people with modest incomes who dug into retirement savings on the advice of the same investment advisor used by Carver.

‘More money has been lost reaching for yield than at the point of a gun.’ - Ray DeVoe

Oftentimes what an investor thinks the “worst case” is, isn’t what the worst case is.

John Comiskey: The looming impact of student loan repayment on the FHA portfolio?

“…the student loan default data thus far has largely been irrelevant towards the FHA portfolio. But with 2.5m borrowers facing an average $625 a month payment shock sometime in the next 9-10 months, that reckoning is coming.”

Melody Wright

Another informative interview, where you hear things you rarely hear anywhere else about real estate, from someone in the trenches.

“We have over 15 million vacant properties in this country, and an additional three million seasonal properties, So I encourage everybody on your drives, just look around. There's so much vacancy.”

“The Fed has no idea what's actually going on.”

“Guess what's going to be in Q2's credit panel - and this is not even my bombshell yet? Affirm is now reporting to credit, and that's buy now pay later. They started that May 1st, and and on FinTwit and Reddit you're hearing all these stories about credit being shut down, they're actually now being denied, whereas by Affirm they weren't before, so I can't wait to see the Q2 credit panel, because it's going to look kind of crazy.”

“…The SubTo friends who are out there, an army looking for any sign of default to go in and swoop in, and I think I've got several in my client books right now, because I just had a sale stopped in California, and I think it was one of these guys talking to the borrower, because she she would not know how to do this - put it that way. So this army - because Pace Morby has 10,000 followers - if not more, I don't even know - they're out there looking for any signs of distress, and picking it up, right:? At least they were when they could turn these over very quickly. I I think that is starting to change, because the appetite has started to change. I think we are starting to get an inkling of true delinquency, but if those servicers don't report to Experian - and they don't have to. They can report to TransUnion, they can not report at all - then the Fed has no idea what's

actually going on.”

“We're kind of entering a very precarious time, where all these shadow markets, all this private credit - I read a great study from a guy who tracks just bank balance sheets. So guess what lending has increased? It's not to mom and pop, it's not to Joe and Jane - it’s to private credit. It's to these companies like Affirm. It's to these so called non-depository financial institutions, or NDFIs. So you can look at the banks, and what they're doing is they're funding all these operations like Affirm, which is a house of cards. I'm sorry it just is. This is very concerning. We've got so much speculation out there in these companies that, again, are not reporting to the government.”

Government Subprime (FHA)

“A lot of this was fraud. This was investors taking out these FHA loans…certain originators were showing a 50% early payment default rate…this is a program that’s supposed to be for first-time homebuyers - we had the lowest number of first time homebuyers ever last year. This program has been used by speculators.”

Gee, do you think AirBnb might be a big reason it seems like we have a “housing shortage”?

CRE

“Private markets generally are now starting to tap into the retail investor a lot more than 10, 15, 20 years ago…At some level, some issuers almost looked down upon the retail investor, and now there's no shortage of top-tier firms and sponsors that are you know really trying to specifically address the retail investment market”

Jim Dowd of North Capital

“Anyone noticing more off-market multifamily deals getting circulated lately?”

“In the past few weeks, I’ve been seeing a ton more off-market opportunities—especially 5–50 unit buildings where owners are “testing the waters” but don’t want to list publicly. Most of them seem tied to ballooning loan maturities or softening NOI. Some are clean value-add plays, others feel like quiet distress. Wondering if others are seeing the same across different markets? Are brokers bringing you more deals? Or are sellers still holding out? (I’m part of a lending team at Everest Capital CRE so we’ve been hearing a lot of this in our convos—but genuinely curious what folks are seeing on the acquisition side.)”

“A BPO, or broker price opinion, also known as a BOV, or broker opinion of value, is an estimate provided by a real estate broker to help a potential investor get a better idea of how much they should bid for a property.”

A Fire Sale of Portland’s Largest Office Tower Shows How Far the City Has Fallen

After Digital Trends moved out of the U.S. Bancorp Tower in Portland, Ore., the technology publisher didn’t hold back about why it left.

The property, once a premier address in the city, was afflicted with “vagrants sleeping in hallways of vacant office floors.” They were “starting fires in stairwells, smoking fentanyl and defecating in common areas,” according to papers the company filed in a lease-termination lawsuit.

Two years later, the city’s biggest office tower stands more than half empty. U.S. Bank, the largest tenant whose parent company’s name is on the building, pulled most of its employees out last year after more than a century in the city.

The 42-story tower was recently put up for sale. The building affectionately known as Big Pink because of its pink-hued Spanish granite and pink glazed glass has an asking price of about $70 million, according to brokers. That is more than 80% below what the owners paid for it a decade ago.

Even investors like Jordan Menashe who seek out distressed properties are steering clear of this one. He says any turnaround looks years away.

“I don’t see a way to get it into the green in the next five to seven years,” Menashe said.

This a complete failure of city governance.

From Trepp:

Portland “has suffered 11 straight quarters of negative absorption, where previously occupied space becomes vacant. The five largest buildings in the city have a total of 1.11 million sf of availability. The central business district's availability rate is an astronomical 40.6%. It's a relatively small market, with 16.7 million sf—the overall Portland market has just more than 52 million sf. Still, that means 5.46 million sf of that is vacant and available directly from landlords. Another 438,074 sf is available for sublease.”

‘It’s Like a War Zone’: What Happened When Portland Decriminalized Fentanyl

During decriminalization, overdoses became so common that the city asked Burke to install a naloxone dispenser in the lobby (she refused), and drive-by shootings between rival drug gangs punctured the night. Although the violence has tapered off, the hotel’s front doors remain locked. Sidewalks outside are lined with tents and addicts nodding off next to pipes and burnt tinfoil. Some are missing limbs. When I visited last May, a half-naked man streaked by in a fit of psychosis. The week before, another man high on meth armed with a machete threatened to chop the head off an employee’s three-year-old daughter. “You have to be tough as nails to work here,” says Burke. “Most days it’s like you’re entering a war zone, and you don’t realize it until you leave.”

“Are you ready to dip your toe into private markets?”

Unprecedented amounts of capital are being raised by large private asset fund managers, and they are now setting their sights on your pension and savings as a fresh source of capital. In the US, the industry is urging the Trump administration to allow retail investors access to funds that were once only available to institutions.

Donald Trump considers order to open US retirement plans to private equity

Donald Trump’s administration is debating an executive order that could open the nearly $9tn US retirement market to private capital groups focused on corporate takeovers, property and other high-octane deals.

The order would instruct agencies such as the departments of labour and Treasury and the Securities and Exchange Commission to study the feasibility of opening 401k plans, a primary vehicle for US retirement savings, to the private funds, according to four sources familiar with the talks.

Trump opened the door for private capital access to American retirement savings in his first term, but few firms have moved ahead with the offering out of concern for liability risk. The order, if issued, would give retirement fund managers more cover to expand access to private investments — while opening a source of funding long coveted by the world’s largest private capital groups, including Blackstone, Apollo and KKR.

Top industry executives predict that offering their funds to 401k retirement plans could attract hundreds of billions of dollars in new industry assets.

And just think of the fees!

401(k) Giant to Allow Private Markets Investments in Its Retirement Portfolios

The 401(k) giant Empower will start allowing private credit, equity and real estate in some of the accounts it administers later this year. The firm is expected to announce Wednesday that it has joined with seven firms to offer these investments, including Apollo Global Management and Partners Group.

Wall Street firms have been pushing to get private investments into the hands of individual investors, and they see the $12.4 trillion market for 401(k)-type retirement plans as crucial to this growth. Empower, which oversees $1.8 trillion in 401(k)-type plans for 19 million people, is the biggest plan provider yet to offer these investments in 401(k)s.

“A lot of private asset managers see tremendous opportunity there,” said Ed Murphy, chief executive of Empower. “And we believe there are tremendous opportunities for retirement investors in private investing.”"

“Tremendous Opportunities”!

The deal that has spurred Apollo’s plan to remake Wall Street

Atlas SP has become the cornerstone of Apollo’s ambitious plan to remake Wall Street, through the market for private credit. “When you look back at really, really strategic transactions for this firm, that’s got to be up there,” Apollo president Jim Zelter told me in December, “because it really was a first massive foray of an origination business of that scale, owned by a non-bank.” He said he jokes with Marc Rowan, Apollo’s chief executive, that five years ago they didn’t even know how to spell Atlas.

Now, it’s central to the firm’s core strategy of increasing the amount of private credit that Apollo originates to generate the income-producing assets it needs to cover the liabilities generated by Athene, Apollo’s wholly owned annuity business. It captures the spread between the two as profit.

Of Apollo’s $785bn of assets under management, some $641bn is private credit, with the balance being private equity.

I will note that Apollo’s history includes ties to Jeffrey Epstein - not that anyone cares.

Private Credit Strains Are Keeping Advisors Busy $1.6 Trillion

Private credit funds are increasingly turning to restructuring advisers to sort out their problem loans, suggesting that while the hot asset class is still raking in capital, there are risks simmering under the surface. “The amount of work we’ve been doing with private credit has doubled in the last three to four years and we weren’t doing any ten years ago,” said David Morris, head of UK restructuring and chief operating officer of EMEA corporate finance at FTI Consulting…

The default rate in Fitch Ratings’ privately monitored ratings portfolio, which is made up of mid-sized US companies, jumped to 8.1% last year, from just 3.6% in 2023…The opaque nature of private credit means that some distress can stay hidden.

Moody's downgrades Maryland's AAA bond rating

And that’s Baltimore!

And yet…

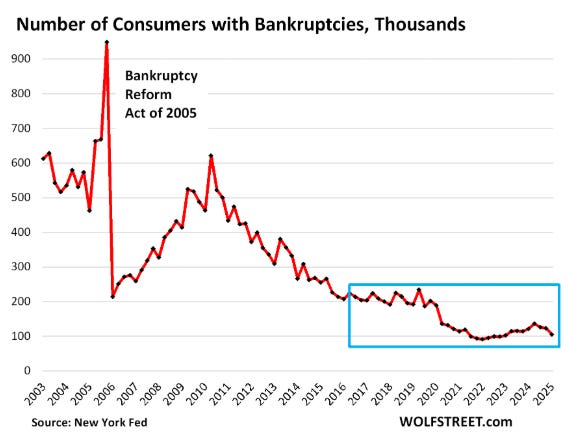

The 2005 Bankruptcy Bill (supported by Joe Biden) made it so student loans were almost never dischargeable in bankruptcy.

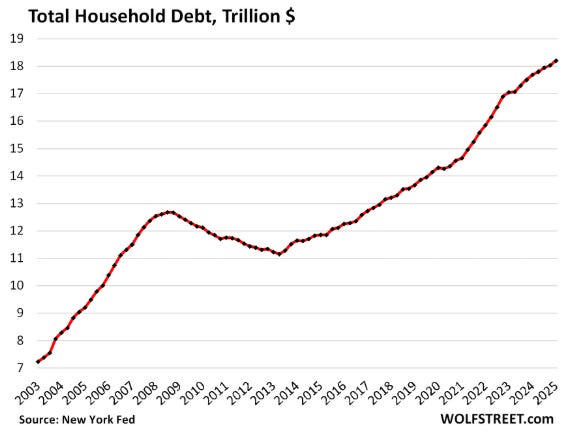

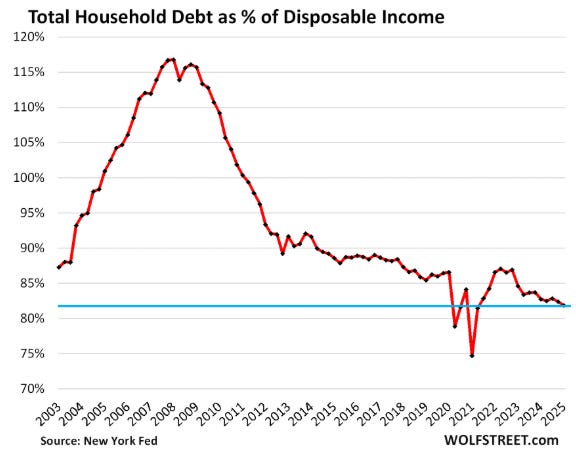

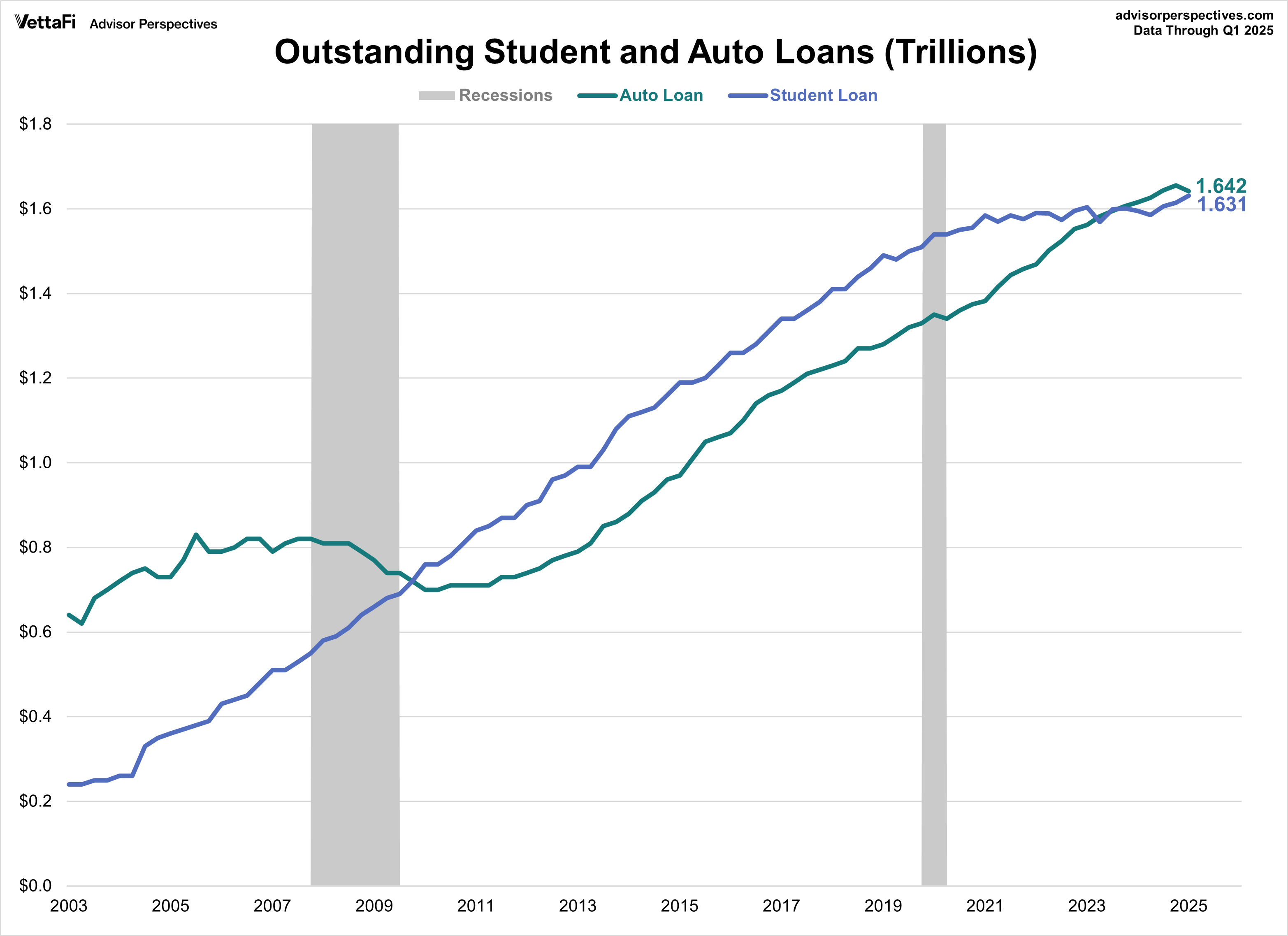

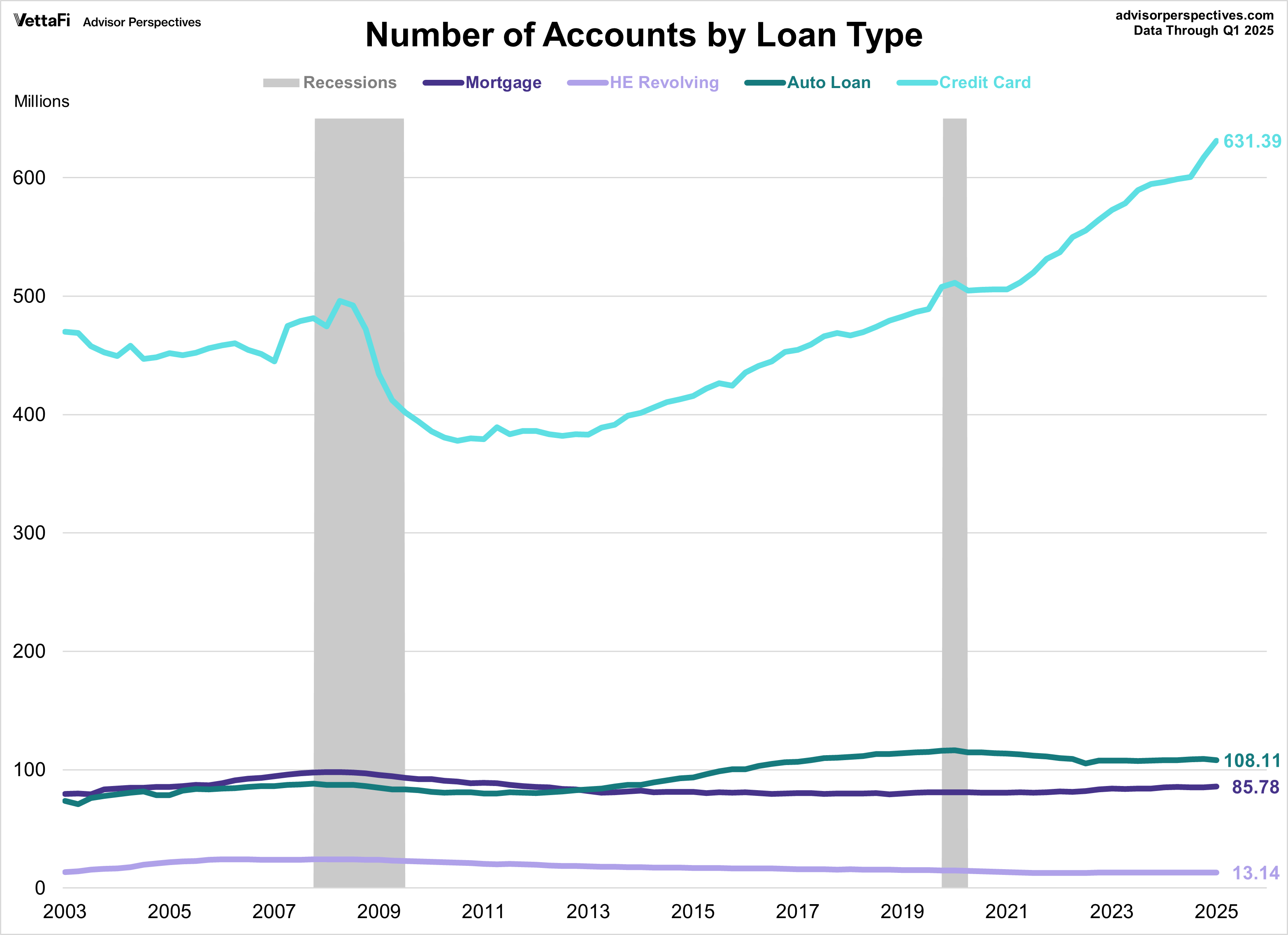

Household Debt Rises to $18.20 Trillion in Q1

This is an interesting chart:

Jamie Dimon: “I am not a buyer of credit today. I think credit today is a bad risk.”

Klarna’s losses widen after more consumers fail to repay loans

Klarna’s net loss more than doubled in the first quarter as more consumers failed to repay loans from the Swedish “buy now, pay later” lender as concerns rose about the financial health of US consumers.

The fintech, which offers interest-free consumer loans to allow customers to make retail purchases, on Monday reported a net loss of $99mn for the three months to March, up from $47mn a year earlier.

The company, which makes money by charging fees to merchants and to consumers who fail to repay on time, said its customer credit losses had risen to $136mn, a 17 per cent year-on-year increase.

From the comments:

“Relying on people too poor to pay for £100 of clothes one transaction always struck me as an insane business model, unless you’re charging payday loan levels of interest straight off the bat.”

New interview with Whitney Webb, the bravest investigative reporter out there:

“How You Are Being Played By Silicon Valley Oligarchs.”

I took a few notes1, but I’ll leave it to you to listen, if you’re interested - and if you’re not interested, that’s ok. You don’t need to tell me.

Flotsam and Jetsam

Berkshire Hathaway’s Latest 13F About 25% of the total is in Apple, and the smallest position is in Pool Corp.

“United Adds Caviar Service and Luxe Jammies in Race for Superpremium Travelers”

Chicago Sun-Times Prints AI-Generated Summer Reading List With Books That Don't Exist

2-tier

Heralded

Decoupled from reality

Narrative management

Embracer

Eager to embrace

Stablecoins USDT

Digital signature

Programmable...Orwellian

Dialectics play

Public private partnership

No one cares...privatized

Grudge

Vacuum

Great Gatsby...money launder...JPM

Focus on one

Learned hopelessness

Incredible post with lots of punches. Heard from a colleague who was at an Atlanta Fed conference this week that everyone is suddenly concerned with private credit. It's getting real out there. And, I still cannot get over what I saw in Skid Row. Have seen plenty of homeless and even someone OD as Travis and I drove by in San Antonio, but nothing prepared me for Skid Row. On that uplifting note, have a wonderful Memorial Day!

Sending my campaign contribution to Rep. Thomas Massie today! It must be absolutely miserable to be an intelligent voice of reason in a slimy swamp of crooks, grifters and utter morons. I really don’t know how he does it. Thanks for another excellent read!