Leopards don't change their spots

Most models are bad models

Via Grant’s: “…fans were particularly outraged last month when tickets to see punk band Green Day went on sale and prices for shows in Sydney quickly soared above the initial price shown. Tickets were sold at more than three times their face value at A$500.” [about $333 US]

According to the BLS, $15 in 1970 is the same as $125 today!

The Fed wants high inflation. They just don't want to acknowledge that inflation is high. Hence all the models, hedonics, weightings, substitutions, seasonal adjustments, propagandists, etc.

Also via Grant’s: “The New York Fed’s freshly released September Survey of Consumer Expectations finds that the average perceived probability of missing a minimum debt payment over the next three months accelerated to 14.2% last month, up from 13.6% in August and represented the highest reading since April 2020. Notably, that sequential uptick was concentrated among middle-aged consumers sporting annual household incomes above $100,000. “

And this:

Finally, 24.2% of third quarter new vehicle trade-ins included auto loans in excess of the vehicle’s current worth accordingly to freshly released data from Edmunds, up from an 18.5% share sporting negative equity in the same period last year. Then, too, the average amount owed on those underwater loans reached a record $6,458 over the three months through September, up 11.2% year-over-year, while 22% of that negative equity cohort owe $10,000 or more with 7.5% on the hook for upwards of $15,000.

“Consumers owing a grand or two more than their car is worth isn’t the end of the world, but seeing such a notably share of individuals affected at the $10,000 or even $15,000 level is nothing short of alarming,” commented Jessica Caldwell, Edmunds’ head of insights. Peer Ivan Drury added that “it’s easy to assume that only specific customers trading in higher-ticket luxury vehicles are the ones underwater on their car loans, but the reality is that this is a problem across the board.”

I had to read this twice. Look at what Austan Goolsbee is saying here:

…the post-Covid inflationary outburst appears firmly in the monetary mandarins’ rear-view mirror, as demonstrated by last month’s supersized, 50 basis point rate cut. Recent monetary misadventures aside, Chicago Fed president Austan Goolsbee flagged the potential for insufficient price growth in a Bloomberg Television interview last week: "if you look at [consumer] expectations, there are some signs that inflation might undershoot the 2% target, and we want to be mindful of that too.”

Goolsbee is saying that he is worried inflation might go to 1%.

These guys do not think like normal people.

“So three weeks ago the 30-year Bond was under 4%, it was 3.96%, right? [Now 4.32%].

If you look at this in the context of the election, if Trump gets elected, the deficits are going to get bigger. If Kamala gets elected, the deficits are going to get incredibly bigger, you're going to have more issuance, you're going to get more inflation. The last thing I want to own is a 30-year Bond.”

I'm not an economist, so I don't know what the wrong answer is, but is it really an indisputable fact that lower rates and lower unemployment are synonymous?

Here’s Melody Wright, with everything you need to know about flood insurance…

…including something I hadn’t thought about - ‘catastrophe bonds’:

In preparation for the 2024 hurricane season, “FEMA has transferred $1.92 billion of the NFIP’s flood risk to the private sector.” Its early days, and there are currently no estimates for NFIP claim payouts for Helene and Milton that I can find. Stay tuned.

According to a report by Reuters on October 11th, “seven NFIP-issued catastrophe bonds totaling $1.3 billion fell between 13% and 59% on Friday compared with a week ago, according to the note from broker Aon seen by Reuters.” It could take “weeks or months” to determine if the cat bonds are triggered. During that time, investors will be unable to redeem their bonds while the government also figures out what their payout will be.

I’ve added some new paid subscribers lately, after a lull, so that’s encouraging. I hope you like this one - and all of them - but I’m eclectic, so it’ll be hit or miss. Some good interviews, a possible canary in the private equity coal mine, some smooth tunes, and the usual other stuff. Sláinte.

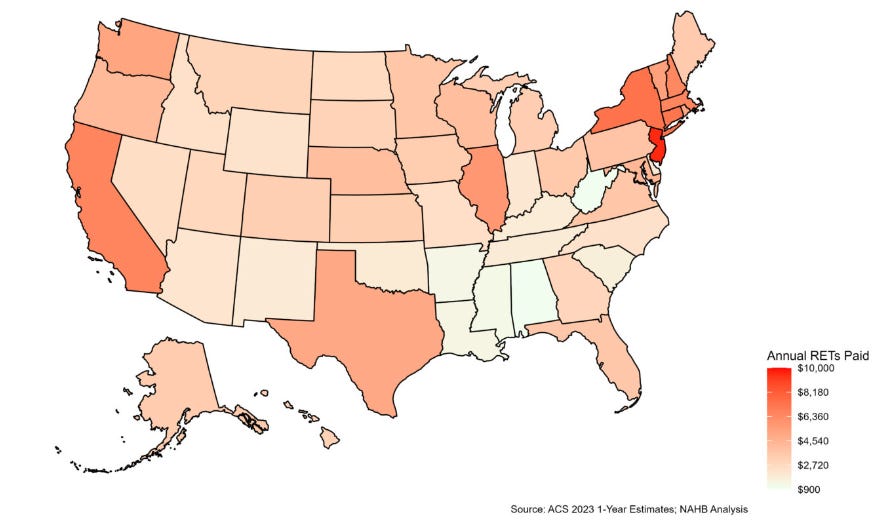

“Homeowners in New Jersey continued to pay the highest real estate taxes, paying an average of $9,572, 30.6% higher than the second highest, New York, at $7,329.”

“Illinois, a change from New Jersey in 2022 , had the highest effective property tax rate at $18.25 per $1,000 of home value. Consistent with 2022, Hawaii had the lowest effective property tax rate at $3.18 per $1,000 of home value. Additionally, Hawaii had the largest increase over the year, up 18.8% from $2.68 in 2022.”

Turnover in the U.S. housing market is the lowest it has been in more than three decades

Top 100 Most Expensive U.S. Zip Codes: Nearly 70% of Luxury Markets Rebound in 2024 “Newport Beach, Calif., claims an unprecedented three spots among the country’s 10 priciest zip codes”

Marc Cohodes

“There's so much money, and there's so much lobbying going on. You have Ken Griffin worth 50 to 60 billion, you have Steve Schwarzman worth 50 to 60 billion, you have Musk worth God knows what he's worth - these guys are all political. They all have PAC’s, they're all too big to fail, they all give people in the government an inordinate sum of money, and they play the revolving door game. They hire really sharp former government officials who are making 300 grand a year and they pay them 3 million a year, plus bonus. Who wouldn't go work for him? So when the people who I think are the bad guys hire the best and the brightest, who used to work at the government, they know how to play the system, so it's sort of a dynamic flywheel process where the rich and the scamsters keep making, and the people on the outside really aren't protected, and guys like me, you know, I can speak out. I'm an army of one, I don't have an assistant, I don't even use a computer. I mean, my computer is what I'm using right now, which is my cell phone, so I just try to lead my best life, and have fun, and expose people here and there.”

“I call CNBC ‘The Cartoon Network’ because it's cartoonish, and whenever you listen to them, you're going to lose your money”

“We've gone so long without really a cleansing process, without sort of a correction. Whenever things go down, and things do go down, everyone

wants the government to ease interest rates, or step into the market, or, you know - the ‘Quick Fix’ to get everything going”

“At least in the United States, the people who are doing well are doing exceedingly well. They're making all sorts of money. The people - the have nots, if you will - are really struggling. I mean there's a lot of people in this country who are struggling, and struggling mightily, and that's sad, and I've never seen such a big gap of of wealth in a spot, ever”

Marc on Jensen Huang of Nvidia:

Adam Butler: “Experts” and Models

"Most models are bad models. I mean the canon of empirical finance is littered with a statistical technique that doesn't actually give you any information about what to expect in the period after the experiment was conducted."

Adam Butler on "experts" who cannot predict anything

“There was virtually no correlation between what these senior analysts had forecast was going to happen, and why, and what actually happened over the subsequent months and quarters.”

"There was not a single expert who demonstrated either an accuracy or a calibration above 50%, so, you know, in aggregate we're not very good."

“I think we should all just acknowledge now that we operate within a fully managed financial system where the authorities have all of the tools necessary at their disposal to ensure that we never have a 2008-style crisis again, and even a recession, or certainly recessionary conditions, reflected in financial markets again, and so that the big risks now don't really exist in the areas of the market that most people typically look, but rather they're externalized to the political domain and to the social domain.”

I’m not so sure the Fed is as omnipotent as Adam suggests.

“So, for example, the big risk that I see is at some point in the future, there will be a political party that will be put in place in Europe or in the US, or a major economy, where the party recognize the people's frustration and anger about various issues - one of them being that more and more people are feeling left out, or feeling left behind, and perceiving that the Fed is a major instrument of that - of propagating this accelerating gap, and we'll just decide to take away power from the Fed.”

I don’t see the above as a risk. I see it as a solution.

“You've got the Fed setting up a situation of intense moral hazard” What else is new?

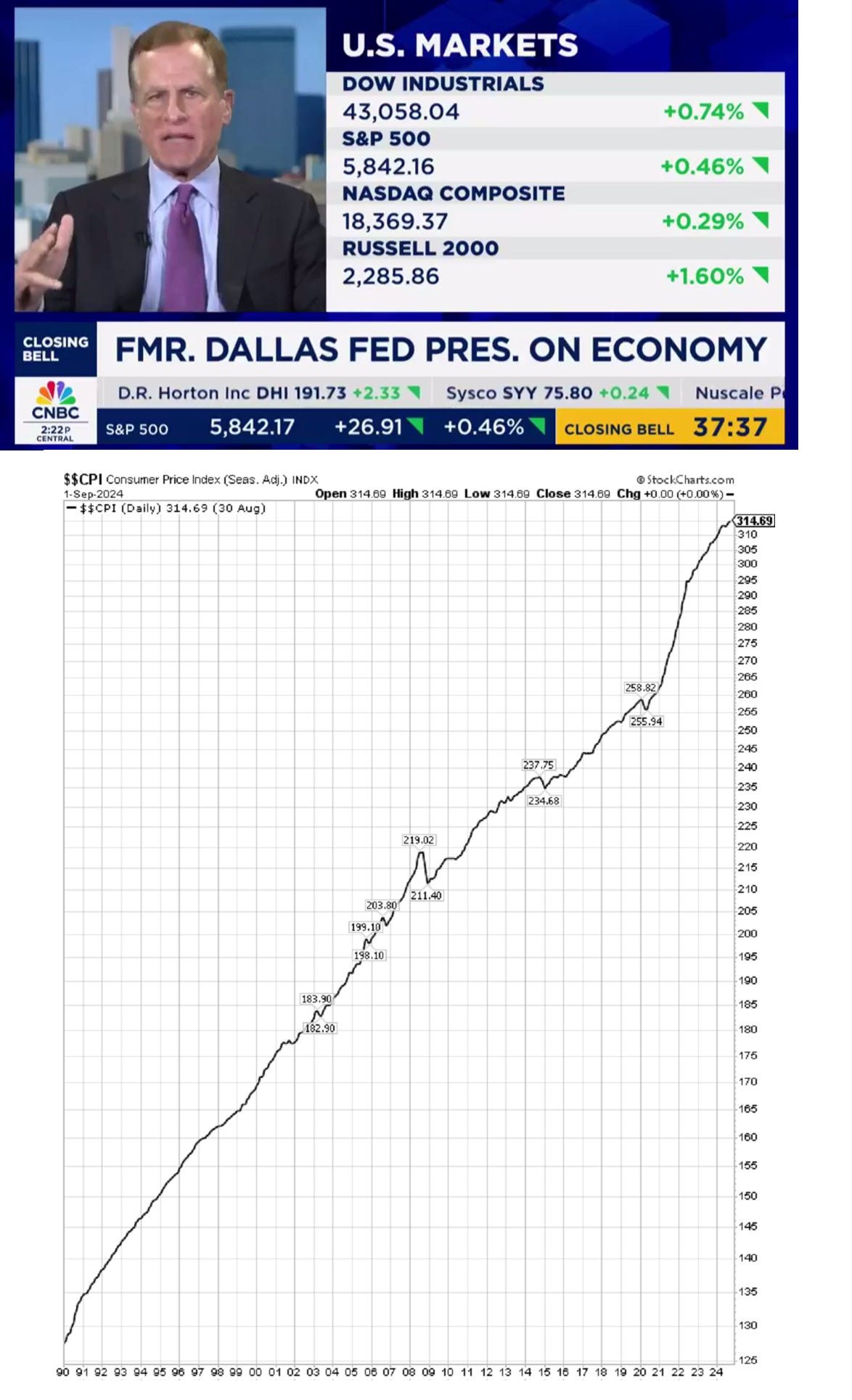

“We just don't have any real precedent for inflation over the last 30 years”

Ok, Adam (and Demetri) of course lose me here. Take a quick look at the CPI chart at the bottom of this post.

Overall a good hour though!

“The truism that when you tax something you get less of it is also applicable to commercial properties. The city of Los Angeles, for instance, had only $2.87 billion of commercial properties - industrial, office, retail and multifamily - change hands this year through the third quarter. That's down $1.9 billion, or 39.8%, from the same period a year ago…Part of the reason: the city's Measure ULA, also known as the Mansion Tax, which became law in April 2023. It imposed a 4% transfer tax on properties sold for more than $5 million and 5.5% tax on deals valued at more than $10 million. Those tariffs now affect properties sold for $5.15 million and $10.3 million, respectively.”

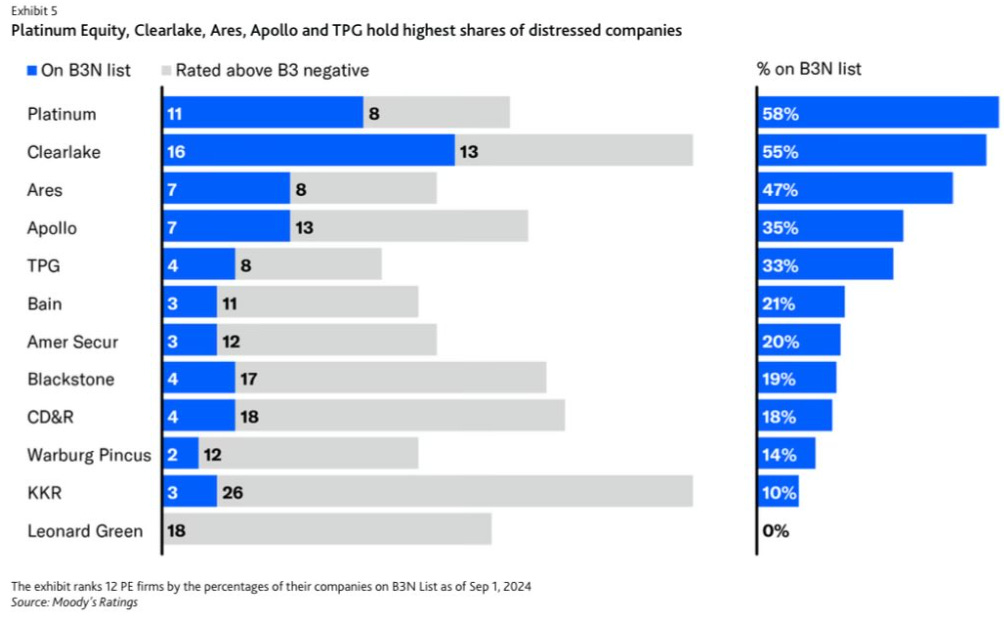

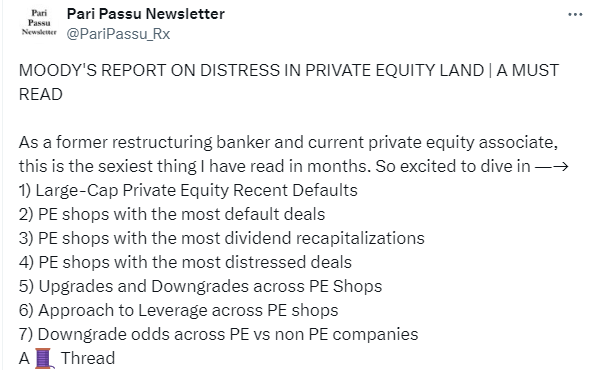

“Private Equity Pummeled by Higher Interest Rates as Portfolio Companies and Credit Funds Struggle; Use of PIK Loans Now Recalls Late 1980s LBO Crisis”

NakedCapitalism summarizes Financial Times and Moody’s reporting

The Financial Times has published two articles, each based on reports by Moody’s of more signs of distress in private equity land in the wake of central bank interest rate increases and very low odds of interest rates going back to the old abnormal of sustained super low levels. The first analysis and related article described how more private equity portfolio companies were having their debt downgraded to levels that pointed to good odds of default, which means a bankruptcy or some other cram-down of current equity holders. The second related to the not-as-well-known world of private credit funds. In the hoary old days of private equity, Chase dominated the business of making so-called leveraged loans, which Chase then would syndicate to banks and other investors like life insurers and sovereign wealth funds. Private equity firms stepped in and started making the loans via so-called credit funds, with the investor profile resembling that of private equity investors (as in public pension funds in particular are big players).

These developments are reminiscent of the end-of-cycle phase of the LBO boom of the 1980s, which ended in a crash in LBO activity, many recent deals going belly up, and lots of debt restructurings. Oddly this big development is not much part of discussions of the end of the LBO wave or the very nasty early 1990s recession, perhaps because the S&L crisis was a headline-dominating event. But it was still serious. For instance, knock-on effects included employment in M&A falling by 75% and a severe commercial real estate recession in NYC (of major developer/owners, only Steve Ross and Trump were able to keep all of the equity in their portfolios).

It’s not clear what the systemic impact might be. In general, financial crises are the result of too much private sector debt. The private equity business is also vastly larger than then. However, by virtue of the lending bagholders having substantial non-bank representation, this trend alone probably won’t threaten the financial system. But it could, as in the early 1990s, be a nasty addition to other excessive debt woes). In general, the lack of good data, as with the subprime crisis, is frustrating. They call it “private” for a reason.

However, at this juncture, the bad outcome seems more likely to be zombification, as well as increases in underfunding at public pension funds. Remember that some of these problems are being finessed with valuation chicanery, with PE players perversely providing their own marks. However, an un-fixable problem for public pension funds will be even less cash coming out of private equity/debt investments. Public pension funds reassured themselves that private equity and debt were good long term investments. But the cash flow pattern across the industry changed even in the super-low interest rate era to private equity funds distributing more cash than enthusiast investors put in, to private equity consuming more cash than it was paying out (due in large measure to ever-rising investor commitments despite steadily falling returns, particularly post ~2006). For those who piled into credit funds (we’re looking at you, CalPERS) the PIK, as in “payment in kind,” which is finance vaporware, will lead limited partners in those funds getting less cash out than they expected.

Recall that these warnings come from Moody’s. Credit agencies are very rarely out in front of adverse developments; for instance, they usually downgrade only after Mr. Market has reduced the price of bonds to reflect newly higher investor concerns. In fairness, Moody’s in one of its reports also discussed even less transparency than before due to diminished activity by some big players (more on that soon). But we also must remember their storied history.

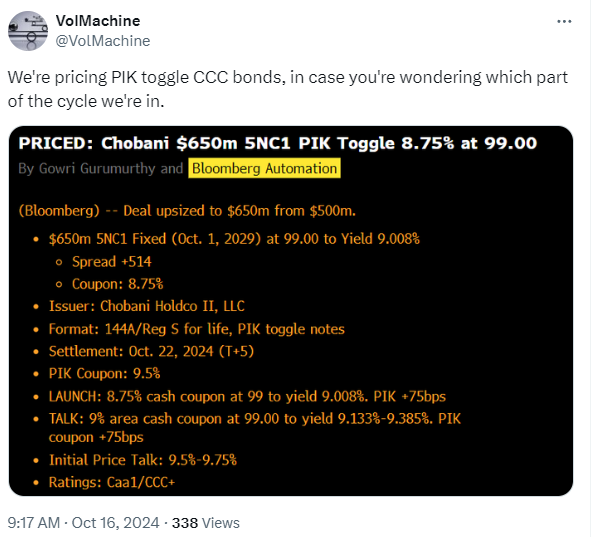

I don’t have the Moody’s report. For more color, there’s a thread here:

“A toggle note is a type of payment-in-kind (PIK) bond in which the issuer has the option to defer an interest payment by agreeing to pay an increased coupon in the future.”

The unfortunates who borrow to pay debts are described in the very ancient Greek proverb: “I cannot carry a goat; put an ox on my shoulder.”

“The prize for most obnoxious party at Davos (2011) was won on the first night, with the Davos Tasting put on by the Wine Forum. Wine tasting was historically one of the more interesting and enjoyable events that was put on at Davos, but it got nixed in 2009 when conspicuous consumption of first-growth clarets was considered inappropriate in the face of the global financial crisis…The plutocrats at Davos, of course, both western and eastern, are exactly the kind of people who spend thousands of dollars a bottle on fine wines…

The event was held at the semi-legendary Piano Bar of the Hotel Europe, which was fully booked out by the Wine Forum for two and a half extremely expensive hours. The Piano Bar is the late-night haunt of Davos Man and it comes with the permanent tang of stale cigarette smoke and a general culture of heavy drinking.

The result was basically a drunken mess. Revelers would cluster around stations loaded up with fine wine, getting large pours of increasingly-indistinguishable heavy cabernets, competing to find the Cheval Blanc and Le Pin (which were naturally considered the most desirable wines, just because they were the most expensive)…

…the event really wasn’t remotely conducive to tasting and appreciating the wines, so much as it was a way of celebrating and appreciating Anthony Scaramucci and Skybridge Capital, who underwrote the event…ultimately events like this aren’t much about taste at all: they’re about putting down markers of various kinds and confirming in the plutocrats’ minds just how exclusive they, and Davos, really are.”

Mike Taylor: “Honestly, Trump didn't think he was going to win.”

Keith McCullough: “That’s right!"

MT: Oh, by the way, when he won, he's like, what?

KM: “He didn't have - like Scaramucci. He wasn't on the B or C team, he came from - in Canada we we have this other league, Beyond Junior C…”

MT: “I think Scaramucci was a butt dial.”

“I think that lateral thinkers who are able to contemplate possibilities outside of the very tightly defined Overton window in which we’re all supposed to be thinking, that the state has got everything under control, there is no need to panic, everything is being done in the best possible worlds and that the people in charge are uniquely qualified to determine what is in our best interest and will continue to do that as they have always done. If you believe that, then when it turns out to be misplaced confidence, the shock can kill you. It’s as simple as that.”

Sir Steven Wilkinson with Grant Williams

Along similar lines we have this recently from Bill Fleckenstein:

“What happens is that people talk about it for so long, and nothing happens, so people decide nothing's going to ever happen, and then it does, and they're not prepared.”

Whitney Webb: “Any parting advice you’d like to give to people?”

John Titus: “Yeah, turn off your television, get rid of it and never turn it on again.”

“We've made a lot of progress on inflation in the last few years."

- Robert Kaplan, Goldman Sachs mole as President of the Dallas Fed for six years, and trader extraordinaire

Excellent post. Love this: proverb: “I cannot carry a goat; put an ox on my shoulder.” Gonna use that. Thank you as always. And I hear heavy drinking causes cancer….

So there actually are people who listen to Green Day?

And are willing to pay to do so?

What an amazing world.

(We haven’t had a TV since 2011).