'The longer I live the more beautiful life becomes.”

Attributed to Frank Lloyd Wright

‘DOJ, FBI conclude Epstein had no "client list," died by suicide’

J.D. Vance a few years ago…

February 27, 2025. Counselor to the President Alina Habba:

Great 2021 article by Nick Bryant: The Jeffrey Epstein Cover Up

Cindy McCain, widow of one of the most powerful men in the world - who runs a foundation which supposedly fights human trafficking - at a "Scourge of Human Trafficking" conference in 2020:

"They were afraid of" Epstein.

Of Course Trump Doesn’t Want to Release the Epstein Files

I know way too much about this case. It’s massive and has gone on for decades, involving intelligence agencies and many of the wealthiest, most powerful men (and women) in the world. It’s an ongoing, largely financial crime story, along with the other stuff (and no one cares at all about the victims.)

It’s bipartisan, and I don’t think anyone in power wants the truth to come out, because it would - and should - destroy both parties and probably take down a couple governments. Very discouraging - but not surprising - to see Trump now claiming the entire thing is a “hoax.” We are ruled by utterly amoral people.

“...the simple step of a simple, courageous man is not to take part in the lie, not to support deceit. Let the lie come into the world, even dominate the world, but not through me."

Aleksandr Solzhenitsyn, Nobel Speech on Literature, 1970

Core CPI YOY has been above the Fed’s made-up "2%-target" now for FIFTY-ONE MONTHS IN A ROW.

Two new podcasts from Maggie Lake:

Tony Greer: “An asteroid to Time Square on Saturday afternoon would be bearish.” Tony is very bullish on the U.S.A. He’s sort of bearish on gold, neutral-ish on oil and the dollar. Tony, like 98% of Fintwit, totally downplays inflation.

Marko Papic: “You should take whatever allocation you have to US assets and half them…the winner is the rest of the world.” Marko has some rather non-consensus takes on the BBB and tariffs. A couple other quotes: “Iran and Israel could nuke each other…and it wouldn't impact global markets” and “Those of you who are watching this and who are American, your tax dollars are going towards securing China's energy security. Like that's literally what the Fifth Fleet of the United States of America is doing. It's not securing America's energy security. It's in Bahrain so that China can have gasoline. That's a fact.”

And do not fear!

David Hunter: “I've raised targets. So I'm at 8,000 on the S&P 500, 27,000 on the NASDAQ, 55,000 on the Dow, and 3,300 on the Russell.”

Here’s a good Jim Grant interview with Dean Curnutt of Macro Risk Advisors. I’d quote from it, but they didn’t do a transcript, and I don’t feel like transcribing.

One nice quip from Jim Grant:

“You are a ‘yes, but’ guy in a ‘gee whiz’ world.”

An interesting Florida Real Estate update from Todd Sachs and Phil Simonetta

Marc Faber: “Trump Is a Gift from God for Gold Investors”

Link I somehow have a 33 minute version, but this link is only for a 4-minute clip.

Meanwhile, in India…

"Take the younger generation. They're forced to buy houses that are overpriced, cars that are overpriced, investments that are overpriced. Interest rates are too low, not too high. The guys calling for Powell to reduce the rates...I don't give shit how leveraged you are."

We’re all very proud of the Fed QT

What Is American Exceptionalism, and Is It Coming to an End?

This Bloomberg headline is a bit reassuring as a contrary indicator.

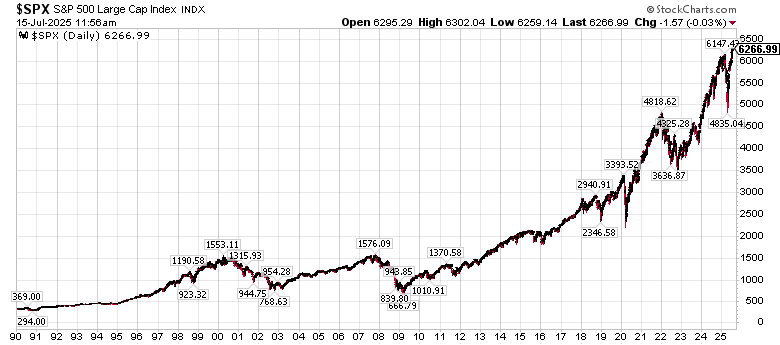

I can see that U.S. stocks are very richly priced, and comprise a huge percentage of global stocks - and I remember when Japan was going to take over the world - but I still can’t get excited about rushing to the relative safety of U.K. or German equities. I’m an American dead-ender, and there’s a reason none of this here is investment advice!

I remember posting this back in 2018, when there was similar suggestions that U.S. investors should get into ‘cheaper’ emerging-market shares.

Here’s EEM relative to the SPX since my 2018 tweet:

The roughly $65 trillion combined value of US stocks is almost half of the global total. US stocks account for almost 70% of the MSCI World Index, compared with less than 50% just after the global financial crisis of 2008.

Earnings growth in the US has far exceeded that of any other region in the past 10 years. A focus on shareholder returns turbocharged by stock buybacks has widened the performance with the rest of the world. Over the past 10 years, combined earnings per share of companies on the S&P 500 Index have doubled — twice the increase seen for the Stoxx Europe 600 benchmark.

There is this sort of thing coming though:

“The government has drafted legislation that would compel large UK pension funds to allocate money to domestic companies, as part of an effort to boost investment and drive economic growth.”

I have to admit that this stuff makes my head hurt, but it seems(?) important?

Investors pile into tokenised Treasury funds

Melody Wright

“We’ve had short-term rentals for a very long time, and I think you'll have them in pockets all over the country, but you don't need as many as there are, and I mean places that just don't make any sense. Like over almost 4,000 in Minneapolis, you know? It just doesn't make any sense. We'll always have short-term rentals in our vacation spots, but yes, Airbnb, I think, is on its way out. This trend is going to disappear, because people simply do not make enough money. And you know, according to Mashvisor, vacancy has increased almost 7% this year already. I mean, there's 15,000 of them in San Diego, for instance. Even if San Diego was fully booked for some event, you never need 15,000 of those. So we just went overboard. We went crazy.”

Jesse Felder

I would just start by pointing out that Powell only seems hawkish relative to the policy that we've become accustomed to after the great financial crisis, right? He's only hawkish relative to 0% interest rates. If you look at the Taylor rule, which is basically designed to show what a neutral interest rate policy would look like, a neutral monetary policy would look like, the Fed has - even after all the rate hikes and everything over the past 3, four years - never even got the policy rate back to where the Taylor rule would say it it should be. So policy is still remains and has always been throughout Powell’s term dovish relative to the Taylor Rule.

Now that that is still a departure from history. Even back in the 1970’s, the Fed funds rate was was raised above what the Taylor rule would recommend during the cycle. We've never seen a hawkishness that even Arthur Burns was able to implement during his term. So to say that he's hawkish I think is only relative to the past 10-15 years. Policy is probably where it should be right now.

The Battle to Keep Consumers Means Smaller Packs of Cookies and Chips

Consumer goods companies are enlarging their range of products—by making them smaller.

Diminutive snack and drink sizes are hitting store shelves as brands try to keep stretched consumers buying with lower-price options. PepsiCo now sells Lay’s potato chips in half a dozen different-sized bags, costing from around 50 cents to roughly $5. Campbell’s now markets teensy packages of Pepperidge Farm cookies and Goldfish crackers. And Mondelez International has six different Milka chocolate bar sizes with prices from under $1 to $6.

I love how what we used to call “shrinkflation” is now presented merely as companies altruistically providing their customers with more choices.

New York firm buys distressed Wacker Drive tower at massive discount

A New York real estate investor known for buying distressed malls has purchased one of Chicago's tallest skyscrapers for about 85% less than it traded for more than a decade ago, one of the biggest losses of value ever for a downtown office building.

A venture of Great Neck, N.Y.-based Kohan Retail Investment Group paid close to $45 million last week for the 65-story office tower at 311 S. Wacker Drive, according to sources familiar with the deal. The sale price for the 1.3 million-square-foot building is a staggering discount from the $302 million it traded for in 2014 to an affiliate of Chicago-based Zeller Realty Group and Chinese investor Cindat Capital Management.

Meet the players tied to the big [multifamily] mortgage mess

The companies and dealmakers connected to the country's broadening fraud scandal rocking real estate

Fannie and Freddie allowed borrowers to self-certify their rental income. Borrowers had a gaping loophole to inflate their rental income and commit fraud.

A few schemes started to emerge.

Scheme 1: Inflating financials. Property owners manipulated their financial statements, especially their trailing 12 months of financials known as the T12.

Scheme 2: The flip. Sponsors bought properties and sold them quickly to straw men as if in legitimate transactions between two unrelated parties. Only the second deal was fake and no money was exchanged, though documents showed a new, higher sale price…

Lenders then provided loans based on the higher sales price, meaning the property had been bought with no equity or negative equity. To date, no lenders or underwriters have been indicted by the Department of Justice or accused of wrongdoing by a federal agency. But, the lenders could be the missing link in the federal probe into mortgage fraud, helping answer questions like: What is the culpability of banks and non-banks to ensure that borrowers are qualified or that lenders are engaging in proper due diligence? To what extent have lenders in the quest for fees encouraged the bad actors?

…Wells Fargo, in a suit in federal civil court as trustee on a $481 million CMBS loan, alleges JPMorgan knew the mortgage it made to Chetrit for a national multifamily portfolio was based on inflated financials. But it allegedly doled out the debt anyway. Wells Fargo alleged in the suit that JPMorgan “was willing to issue such a risky loan because it never intended to hold it.”

How Goldman Sachs won big in the Fed’s annual stress test

“A critical change to the Fed’s test of particular benefit to Goldman was the exclusion of private equity investments from its market shock scenario, an area where Goldman has more direct exposure than its peers.”

BlackRock tried private credit once before. Will this time be better?

From FT commenter ‘Ai Hong’: ‘A quiet form of managerial feudalism’

In the modern economy, BlackRock, Vanguard, and State Street have ceased to be mere asset managers. They now act as the quiet sovereigns of capital allocation, with top shareholder positions across nearly every major sector, from airlines and banks to tech and retail. Their dominance is not loud or coercive. It is systemic, invisible, and routinised. They do not need to conspire. Their ownership structure alone discourages competition and fosters stability in the name of shareholder value.

This is not monopoly in the industrial sense. It is what Antonio Gramsci might call a cultural hegemony, where power is exercised not through force but through consent and common sense. These firms do not intervene aggressively. They shape the background conditions. Through passive voting, standardised risk models, and fiduciary rhetoric, they teach boards and executives what is acceptable and what is not.

The result is a form of governance without government. Quarterly earnings become sermons in discipline. Market signals are taken as truth. Policymakers, far from acting independently, increasingly mirror the frameworks devised in financial models. Regulation gives way to translation. Public interest is filtered through private metrics.

This is not capitalism as most imagine it. It is a quiet form of managerial feudalism, wrapped in the language of neutrality. We should ask whether democracy can function when economic sovereignty lies not with elected governments, but with institutions whose authority is exercised through ownership rather than law…

It’s not about conspiracy. It’s about control through passive scale. BlackRock, Vanguard, and State Street are not activist investors, they are cooperating owners. Together, they form a corporate trinity that quietly shapes board selection, CEO appointments, and governance norms across nearly every major listed company.

There is no need for overt coordination when alignment is embedded in the structure itself. Influence flows not through pressure, but through presence.

Monopoly, after all, is good for business. Keep profits high through tacit alignment among nominal competitors. Business School 101.

This is not the invisible hand. It is the indivisible hands.

These comments were off-topic, but this really is a keeper:

“There are casualties littered throughout history for those trying to boost income but on the wrong side of volatility.”

Via Grant’s:

Ample liquidity, meanwhile, burnishes credit default swaps’ appeal for portfolio managers, with $1.2 trillion of the products changing hands across North America and Europe during April’s trade-related tumult. “You can easily do $500 million of CDX high-yield today,” Martin Coucke, global credit portfolio manager at Schroders, relates to Bloomberg. “Buying $500 million of bonds today on the high-yield side is close to impossible.”

Yet alongside that virtue comes basis risk, meaning an imperfect correlation between the swaps and underlying corporate obligations. Thus, the IG CDX reached a 63% premium to its year-end 2024 levels following Liberation Day, well above the 49% jump in equivalent benchmark bond spreads. “This activity is implicitly short volatility,” cautions Bloomberg’s chief global derivatives strategist Tanvir Sandhu. “There are casualties littered throughout history for those trying to boost income but on the wrong side of volatility.”

Mike Green

“This is the best possible environment for those who are old.”

“So if you give me a dollar, I go buy some stocks, the impact on the aggregate market cap is roughly a $2 increase in the market. If you give it to a passive fund, at this point, my numbers are saying somewhere between $17 and $20 worth of multiplier.”

“The US stock market has outperformed significantly off of the April lows. It was one of the first in the world to make new all-time highs, and it was of course led by those large, inelastic stocks that we think of as kind of the MAG7, the largest components of the S&P 500. So things have been looking very good overall, but there is some weakening beneath the surface and I think that's important for people to be aware of.”

“The majority of baby boomers are now starting to hit the point at which withdrawals are no longer discretionary. They're mandatory. Right? So 72 is the age at which you have to start taking distributions.”

“Now we're in a situation in which we've got a high stock market, and we're receiving high interest rates. This is the best possible environment for those who are old. You can sell your stocks to schmucks who are willing to pay an outrageous fee for them, and you can roll it into bonds that are paying the highest real yields that we've seen in 25 years. And you know the crazy part, Adam? Nobody wants to do it.”

“What happens when you introduce a new participant that has a 100% propensity to buy or sell with no consideration for valuations?”

Chris Whalen

How detached Americans are from reality

“You know, the fact that people in Washington think all they have to do is extend the debt ceiling, and they don't worry about selling the debt, is fascinating to me. But they'll they'll figure it out soon, I'm confident.”

“We think we can legislate economic outcomes. People in Congress really believe that, so they don't worry about deficits anymore, because it's inconvenient politically.”

“You have the Chinese and the Russians and several other significant buyers basically buying gold by volume rather than price. They are just going to put

it in the vault. And so I think when you see these kinds of behaviors, what it tells you is that people have already made a decision to change the allocation that they have from primarily dollars to a much broader portfolio.”

“The inflationary aspects, especially going back to Covid, have the biggest political ramifications”

“I think the thing that head fakes a lot of people, especially economists, is that the Fed continued to manage both the reality and the narrative around monetary policy as though everything was normal during Covid, and then expanded the balance sheet dramatically. And most economists can't even talk about the balance sheet. They don't understand it. So what we saw was that the Fed went out did too much. They continued to reinvest even after they did too much. And the result was higher home prices…And the thing is, home prices may not go down. So, when you do that, you create a huge political problem.”

“We don't have a lot of credibility on fiscal issues at the present time. Until the U.S. has a President and also members of Congress who are willing to talk about reducing the deficit, we're in a defensive posture. When you see an issuer - and I learned this in Latin America in the 70s and the 80s - issuing all T-bills, what is that? That's Mexico. Mexico used to have to keep the CETES1 rate - which is what they call T-bills - at 20%. And then their yield curve went down from there. Okay? And that was a penalty rate because nobody believed it. They were all short the currency. So the government had to defend the Peso. the U.S. could come under some pretty serious selling pressure this year, because Trump has essentially passed on the fiscal issue. And everybody in Washington's with him by the way. Nobody in Washington thinks that deficits matter. If you actually say something like that in public, you get in a lot of trouble.”

“What are we going to do? Is the Fed going to buy [the debt]? If we do that, we have hyperinflation. We already saw that with the banking system during Covid, right? It directly flows through the banks. When the Fed buys a security, you create a deposit. The fact that they've tightened as long as they have I think is remarkable. We still haven't heard a definitive announcement of when they're

going to end QT, but I think they're going to have to do so pretty soon.”

They’ve already pretty much ended QT:

“Stablecoins are like prepaid gift cards.”

“So, the fact that the stablecoins are all going out to get bank charters - mostly to evade state law regulation. Let's face it, they are regulated as money transfer businesses until they get a federal banking charter. To me, there's no alpha here. You're running a utility.”

“Go ask Brian Moynihan at Bank America how he'd like to see a five and a half or 6% ten-year.”

“Isn't it amazing that the Fed ran the stress test and they ignored private equity exposures at the big bank? I mean, you know, this is crazy.”

“Multi-family is in a terrible state. It really is. And the politics of inflation are going to make it worse. Look at New York City. We got a guy who seriously thinks we can cap rents and not have these buildings fall apart around our ears.”

“Inflation is not a partisan issue. It affects everybody. So whether you're a landlord of a building, or you're a consumer, or whatever it is, doesn't matter. It affects everybody, and it is affecting our politics dramatically. This is why what Powell did wrong - and I do agree he did a lot of things wrong during his term - was to do too much. You know, he had Janet Yellen and the rest of these progressives on the board, and they said, "Oh, well, we got to keep reinvesting. We got to do this and that." And that was fatal because not only did it generate the losses at the Fed, which are going to continue, but it did horrible things to housing that were really unnecessary.”

Ray Dalio explains

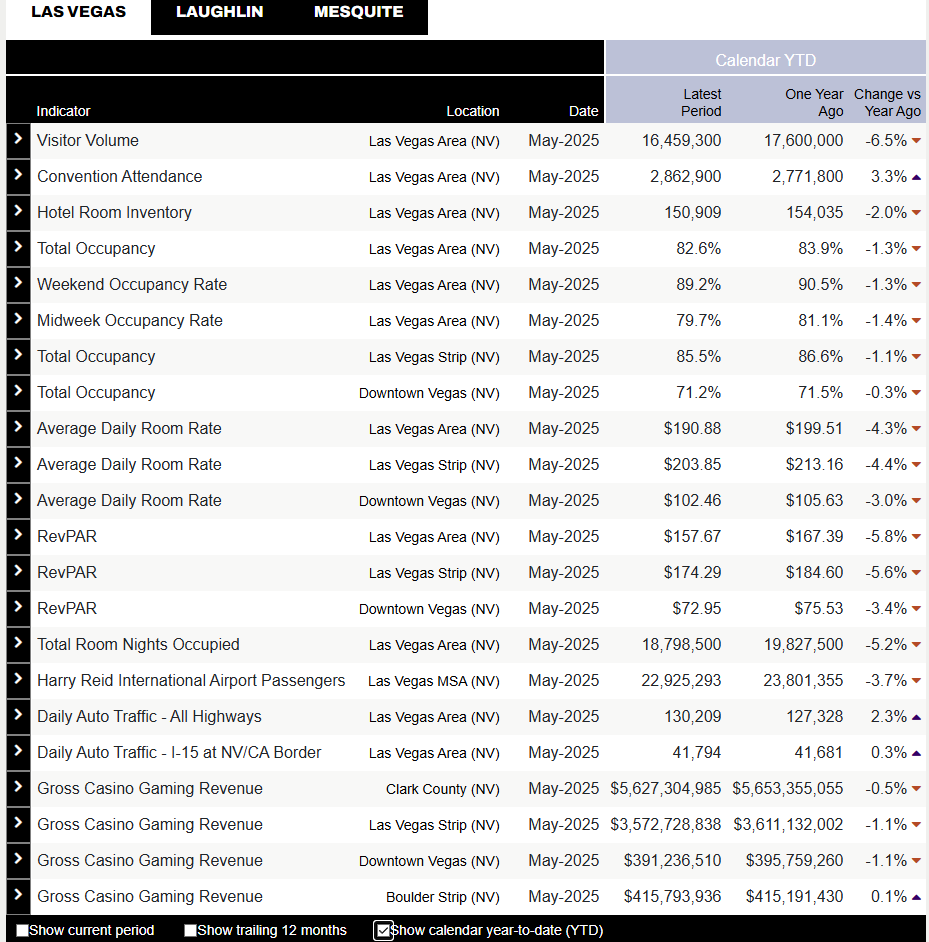

Las Vegas Traffic Year-To-Date

Jordan Ellenberg: How Not To Be Wrong

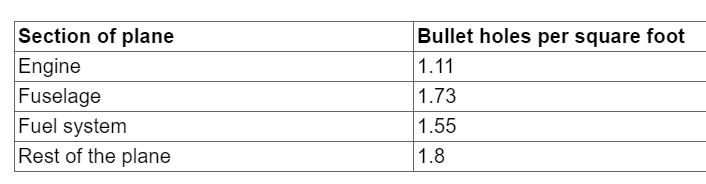

So here’s the question. You don’t want your planes to get shot down by enemy fighters, so you armor them. But armor makes the plane heavier, and heavier planes are less maneuverable and use more fuel. Armoring the planes too much is a problem; armoring the planes too little is a problem. Somewhere in between there’s an optimum. The reason you have a team of mathematicians socked away in an apartment in New York City is to figure out where that optimum is.

The military came to the SRG with some data they thought might be useful. When American planes came back from engagements over Europe, they were covered in bullet holes. But the damage wasn’t uniformly distributed across the aircraft. There were more bullet holes in the fuselage, not so many in the engines.

The officers saw an opportunity for efficiency; you can get the same protection with less armor if you concentrate the armor on the places with the greatest need, where the planes are getting hit the most. But exactly how much more armor belonged on those parts of the plane? That was the answer they came to Wald for. It wasn’t the answer they got.

The armor, said Wald, doesn’t go where the bullet holes are. It goes where the bullet holes aren’t: on the engines.

Wald’s insight was simply to ask: where are the missing holes? The ones that would have been all over the engine casing, if the damage had been spread equally all over the plane? Wald was pretty sure he knew. The missing bullet holes were on the missing planes. The reason planes were coming back with fewer hits to the engine is that planes that got hit in the engine weren’t coming back. Whereas the large number of planes returning to base with a thoroughly Swiss-cheesed fuselage is pretty strong evidence that hits to the fuselage can (and therefore should) be tolerated.

If you go the recovery room at the hospital, you’ll see a lot more people with bullet holes in their legs than people with bullet holes in their chests. But that’s not because people don’t get shot in the chest; it’s because the people who get shot in the chest don’t recover.

Here’s an old mathematician’s trick that makes the picture perfectly clear: set some variables to zero. In this case, the variable to tweak is the probability that a plane that takes a hit to the engine manages to stay in the air. Setting that probability to zero means a single shot to the engine is guaranteed to bring the plane down. What would the data look like then? You’d have planes coming back with bullet holes all over the wings, the fuselage, the nose—but none at all on the engine. The military analyst has two options for explaining this: either the German bullets just happen to hit every part of the plane but one, or the engine is a point of total vulnerability. Both stories explain the data, but the latter makes a lot more sense. The armor goes where the bullet holes aren’t.

Wald’s recommendations were quickly put into effect, and were still being used by the navy and the air force through the wars in Korea and Vietnam. I can’t tell you exactly how many American planes they saved, though the data-slinging descendants of the SRG inside today’s military no doubt have a pretty good idea. One thing the American defense establishment has traditionally understood very well is that countries don’t win wars just by being braver than the other side, or freer, or slightly preferred by God. The winners are usually the guys who get 5% fewer of their planes shot down, or use 5% less fuel, or get 5% more nutrition into their infantry at 95% of the cost. That’s not the stuff war movies are made of, but it’s the stuff wars are made of. And there’s math every step of the way.

Grady Hendrix on post-apocalyptic stories:

“It Comes at Night drives me crazy because I can’t stand movies where there’s been some disaster, and now everyone’s an asshole. It’s like ‘asshole rays’ have hit the Earth. That’s never what happens in real life. Every time there are these big disasters, people act more altruistically. It’s just a fact. And so when these movies are like, ‘Hey man, we’re all just animals. If I took away your cell phone, you’d be eating your baby in about five minutes,’ that whole Lord of the Flies thing, it is a big line of bullshit. It just reminds me of those kids who listen to Slipknot and are total edgelords in high school. … I’m just like, ‘Oh my god, yes, you’re edgy. OK, fine. Marilyn Manson rules. It drives me bananas.”

Did the ‘Deep State’ Invent the U.F.O. Craze?

…several possible mythology-forging projects inside the military-industrial complex: a combination of deliberate psychological operations aimed at covering up top secret technologies, possible bureaucratic pranks and hazing rituals that accidentally made midlevel personnel into U.F.O. believers, and top secret experiments that the government allowed its own personnel to interpret as possible close encounters.

Again, this is closest to my own take on the phenomena:

"There is a superabundance of historical documentation which plainly indicates that these objects and their elusive occupants have always been a part of the environment of earth and that they seem to know everything about us, are able to speak our languages, and are even familiar with the total lives of some—if not all—human beings.

So long as we adhere to the notion that we are dealing with random extraterrestrial visitors, none of these contactee stories makes any sense. So I ask you to place the UFOs into a terrestrial or ultraterrestrial framework. Think of them as you might think of a next-door neighbor who is hooked up to your party line. The pieces of this puzzle will begin to fall into place."

John Keel, Operation Trojan Horse

"If we were to call these things anything, they would be in the realm of the Angelic and the Demonic. That's how I feel about them personally right now."

“In Russian, the most popular proverbs are about truth. They express the not inconsiderable and bitter experience of the people, sometimes with astonishing force. One word of truth outweighs the whole world.”

Aleksandr Solzhenitsyn, Nobel Speech on Literature, 1970

Donald Sutherland’s epic monologue in the film JFK:

“I love talking about Kennedy. I was just down in Dallas, Texas. You know you can go down there to Dealey Plaza where Kennedy was assassinated. And you can actually go to the sixth floor of the School Book Depository. It’s a museum called “The Assassination Museum.” I think they named it that after the assassination. I can’t be too sure of the chronology here…

Anyway they have the window set up to look exactly like it did on that day. And it’s really accurate, you know. ’Cause Oswald’s not in it.”

"What you have to understand, John, is that sometimes there are forces and events too big, too powerful, with so much at stake for other people or institutions, that you cannot do anything about them, no matter how evil or wrong they are."

William Colby, to John DeCamp (author of 'The Franklin Cover-Up"

WHO MURDERED THE CIA CHIEF?

“I knew Colby would have been a fatalist about it. He wouldn’t have put up a fight when they came for him.”

Fascinating account. Check it out.

I like this guy John Kiriakou. Listened to him a number of times. Former CIA guy who served a couple years in prison as revenge for his opposition to the torture program.

"Who did you not at all trust even though you had to work with them?"

"The Israelis."

Good interview.

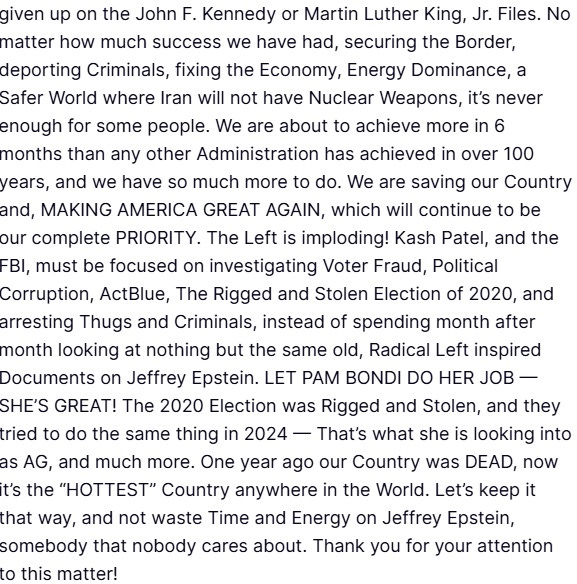

On July 9, I posted this as a joke (too many thought it was real):

Three days later Donald Trump posted this:

And then a few days later Trump sends this:

Unbelievable.

“In Mexico, Treasury Bills are called Certificados de la Tesorería de la Federación, often shortened to CETES.”

Really appreciate Rudy's take. Should Rudy accept this mission be happy to share this on another feed. Been feeling my groove again and staying in the Zone. Let's Win BABY!

Lemme know

Von Danikens Chariots of the Gods convinced me many years ago. Great to read your commentary, as always!