Number Goes Up

"Extend and pretend kicks into high gear."

"The statistics aren't designed to inform, they're designed to hide the truth."

Number Go Up

Price levels matter. And the CPI is just a model of some math PhD’s reality.

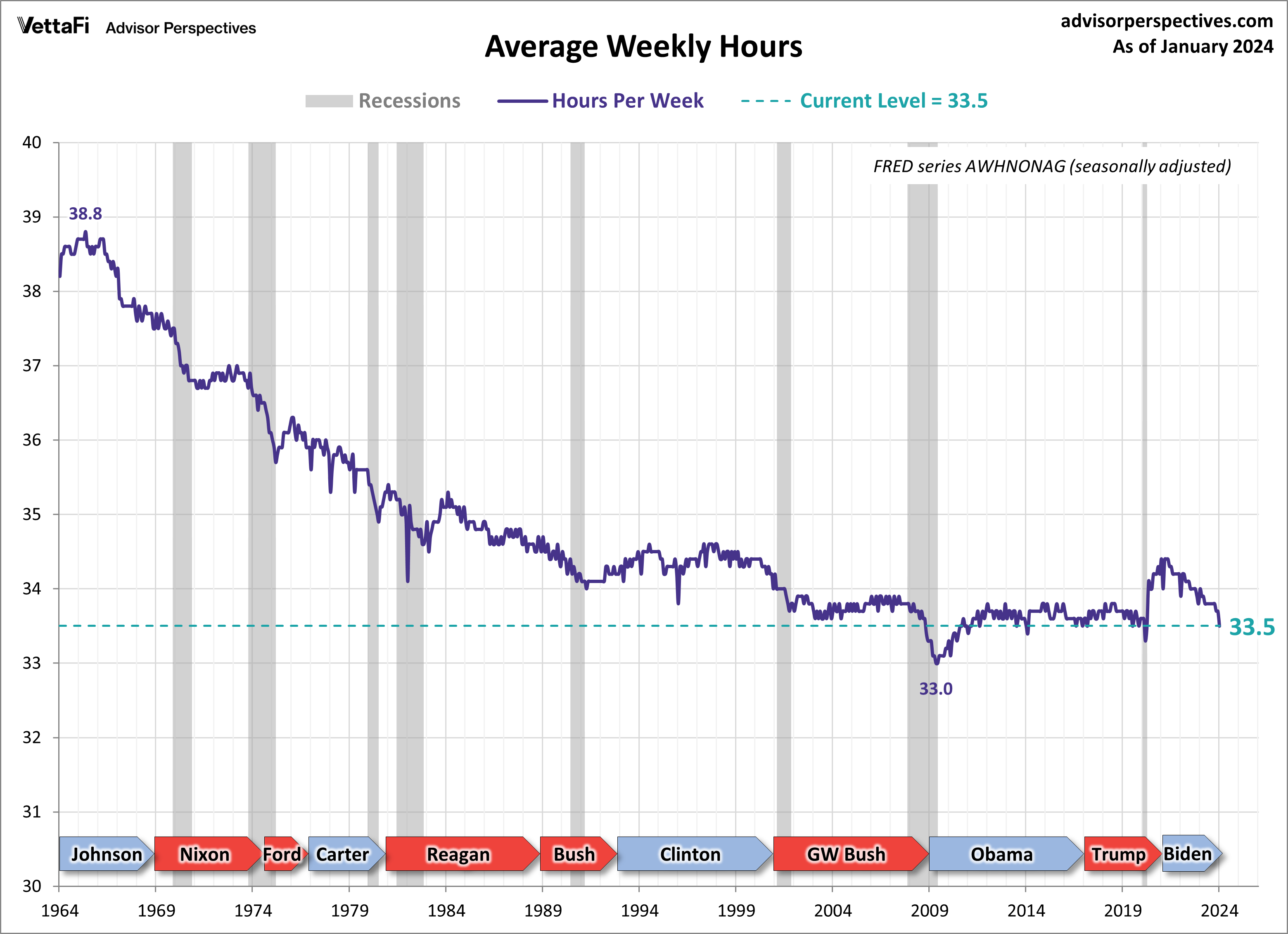

Real wages are deflating.

“What I'm telling you is, because there were less hours worked - people work less hours, their average weekly earnings fell for the month. Fell. Deflation outright for the month, because there were so much less hours worked.

So, who cares if you're making them more per hour now…the average weekly take-home pay, which fell below three percent year-over year, 2.966%, so they round it to three, they say it's three, but it's below 3% which means again real wages are deflating. Your paycheck's worth less the second you cash it.”

The median wage per the SSA is about $40k. So you get a 5% raise - that’s like one car repair bill. And what happens when your rent goes up $200 a month?

"The FTC's Bureau of Economics said it's a ridiculous premise - no one is ever going to use search engines on their phone...You know I I have contempt for economists, and this is kind of why."

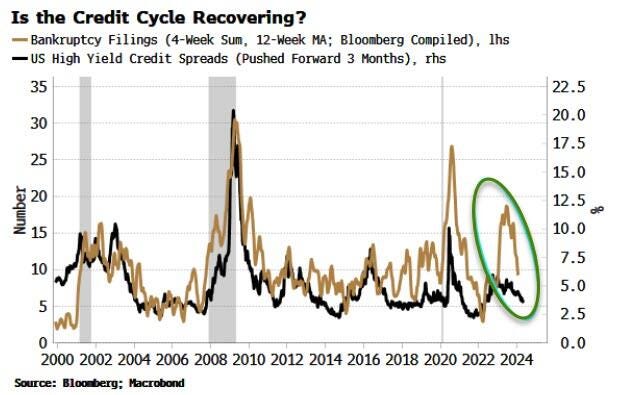

A drop in bankruptcies…

Simon White: “A drop in bankruptcy filings suggests that credit conditions are improving, despite a downturn that was looking almost inevitable last year. As long as growth remains in a cyclical upswing, the path of least resistance for credit spreads is likely to be further tightening.”

“Retail sales tumbled 0.8% in January, much more than expected”

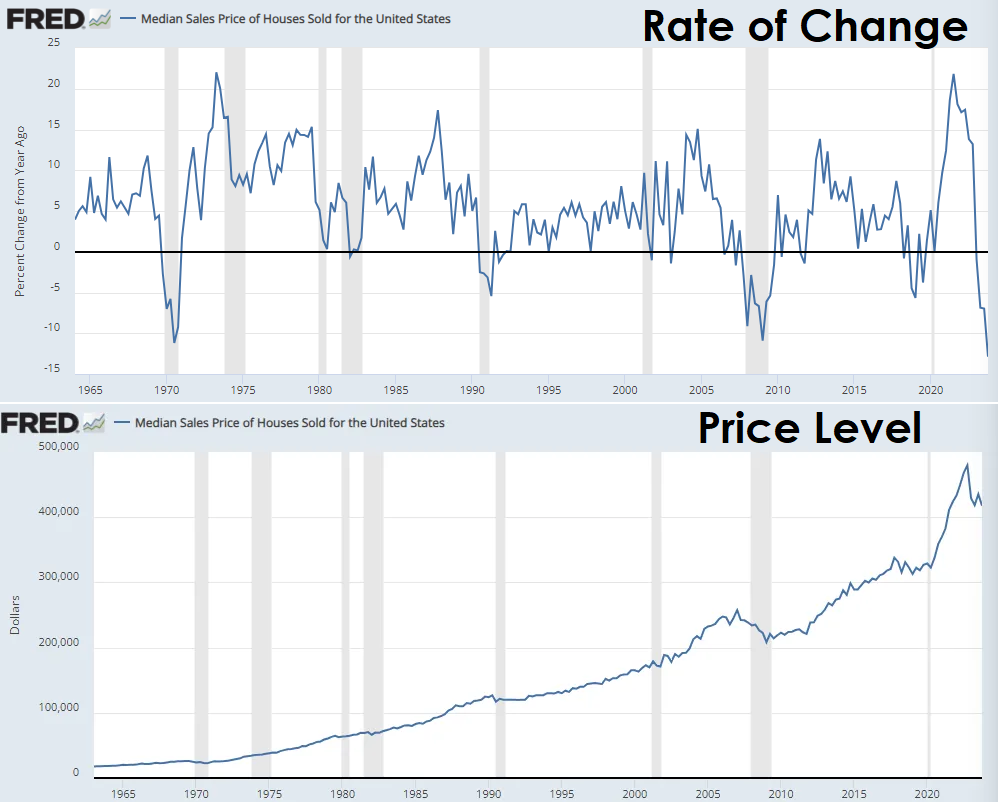

And this doesn’t take inflation into account…

Median Sales Price of Houses Sold for the U.S.

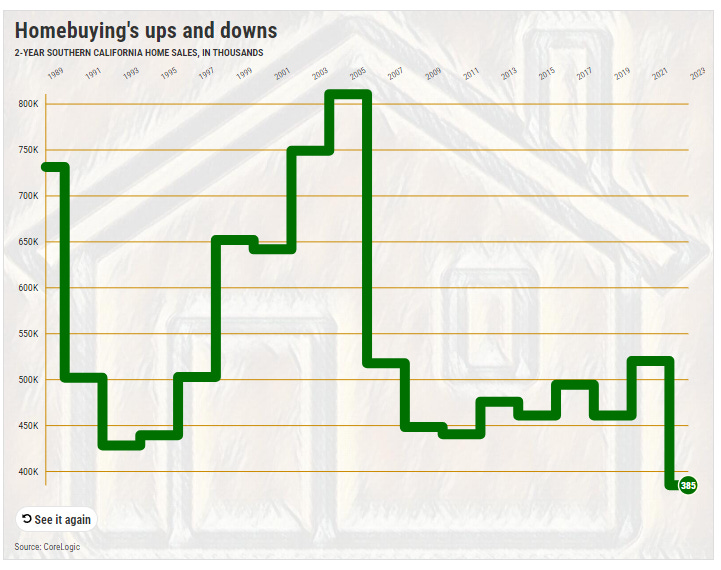

Two-year Southern California Home Sales, in Thousands

Huge sales declines were found across all counties:

Ventura: 51% two-year dip – biggest on record, topping 2007.

Orange: 45% two-year dip – No. 2 behind 2007.

San Diego: 44% two-year dip – biggest on record, topping 2007.

Los Angeles: 43% two-year dip – No. 2 behind 2007.

San Bernardino: 40% two-year dip – No. 3 behind 2007 and 2008.

Riverside: 38% two-year dip – No. 3 behind 2007 and 2008.

Stable Prices! If the Fed can’t do it, CA housing can!

San Bernardino: $481,500 median in December after a 1% two-year gain vs. a 34% jump in 2020-21.

Los Angeles: $820,000 after a 2% gain vs. 27% in 2020-21.

Riverside: $550,000 after a 3% gain vs. 34% in 2020-21.

Ventura: $786,000 after a 3% gain vs. 34% in 2020-21.

San Diego: $800,000 after an 8% gain vs. 28% in 2020-21.

Orange: $1.1 million after a 17% gain vs. 28% in 2020-21.

“Sadly, local homebuying has become a game largely for folks with fat paychecks, investment windfalls – or generous relatives.”

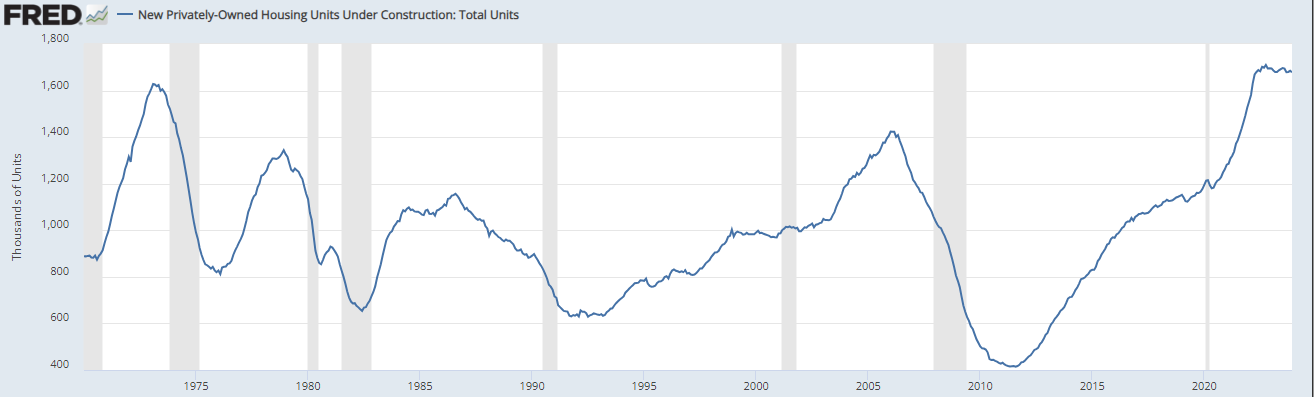

New Privately-Owned Housing Units Under Construction

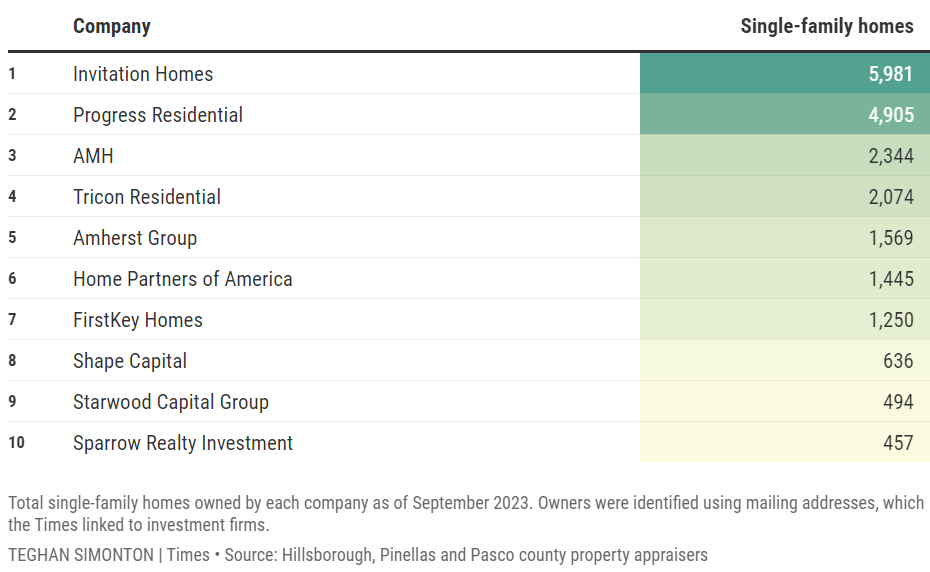

‘How corporate investors are taking over Tampa Bay’s neighborhoods’

Corporate investors own 27,000 homes across Tampa Bay.

“Major investment firms are Tampa Bay's largest landlords.”

“It’s not uncommon to see entire blocks bought up by corporate owners…Once a corporate landlord buys a home, it’s pretty much off the market for good.”

Maybe that will change.

…Maybe not.

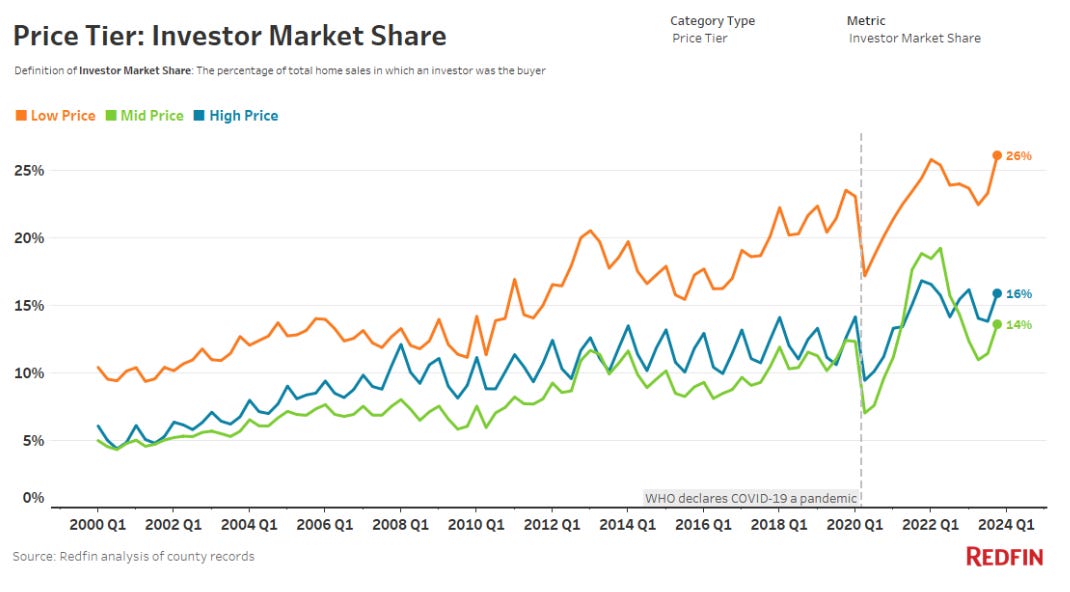

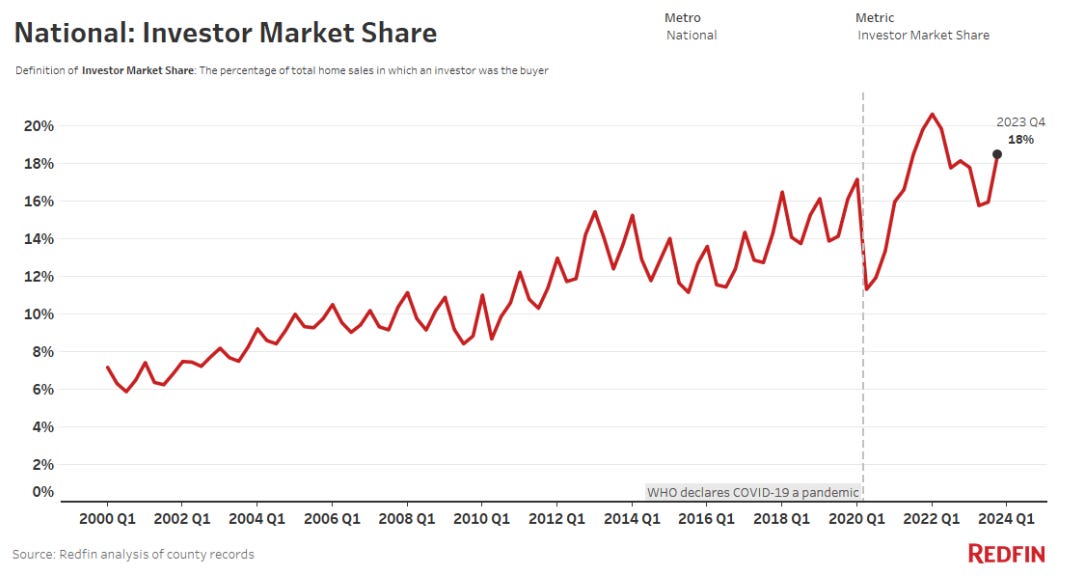

“Investors Bought 26% of the Country’s Most Affordable Homes in the Fourth Quarter—the Highest Share on Record”

Biggest increases: Riverside, CA (+25%), Chicago (+20.9%), San Jose, CA (+18%)

Biggest decreases: Cincinnati (-28.8%), Providence, RI (-27.7%), Orlando, FL (-26.5%)

Highest share: In Miami, investors bought 31.5% of homes that sold. Next came Jacksonville, FL (25.6%) and Anaheim, CA (25.5%)

Lowest share: Providence (9.9%), Warren, MI (10.1%), Montgomery County, PA (10.2%)

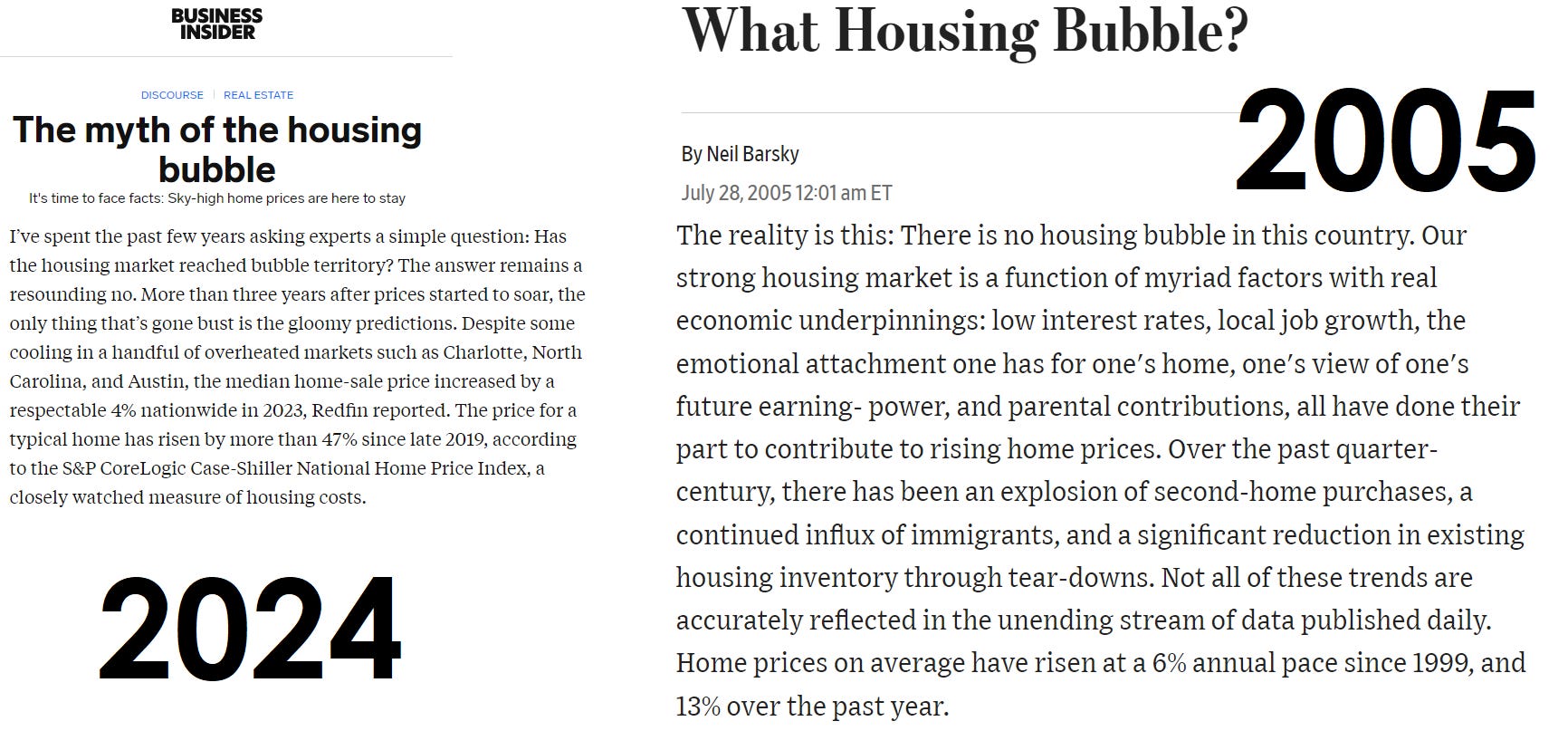

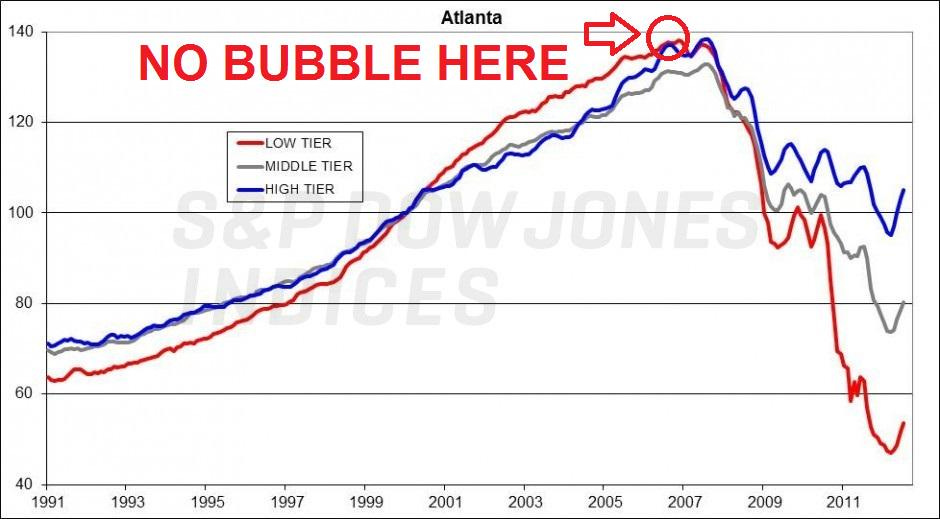

August 2006: “5 Reasons there is No Housing Bubble in Metro Atlanta”

“Hate to Burst Your (Housing) Bubble But there isn't one” (July 2006)

A particularly hubristic take.

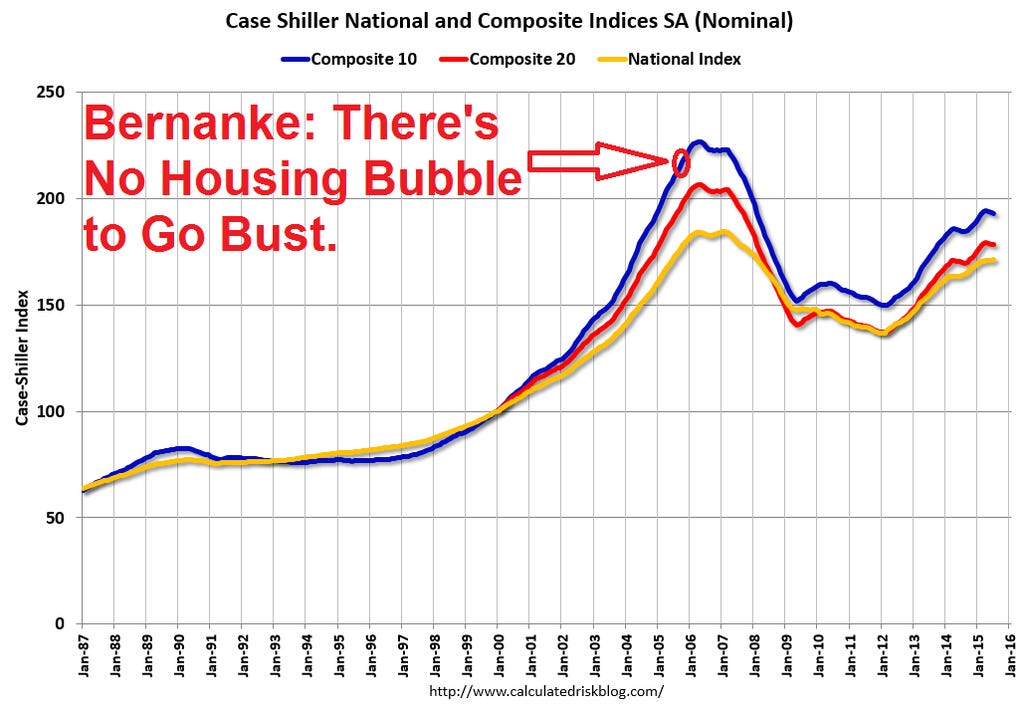

Bernanke: There's No Housing Bubble to Go Bust (2005)

“Life sciences giant Alexandria Real Estate Equities has sold another property at a loss as it sells underperforming assets and focuses on its bigger campuses. Alexandria sold a three-story office building at 138 River Road in Andover for $3.9M to Lawrence-based Energy North Group, according to public records. The sale price represents just more than a quarter of the $14.3M the life sciences REIT bought it for two years ago…”

“New York Community Bank - there were some headlines that came out today that said they’re trying to offload their mortgage risk, planning to sell RV loans - little did we know they were having overexposure to some RV loans - but what’s interesting, the takeaway from here is that they were trying to create a synthetic risk transfer, backed by a portfolio of about $5 billion of home loans that were originated when interest rates were lower, so, for everything that we just go through saying, when I hear people talking about deleveraging their risk using synthetic instruments, it doesn’t exude a ton of confidence, right? I think that’s the reality. These synthetic securitizations effectively allow them to offload their exposure by transferring the risk to the assets to the buyer. It’s an interesting concept. Maybe they’ll be successful at this.”

Industrial CRE

Lonnie Hendry then went on to discuss The SorrentoView Business Park, “a multi-tenant Class-A business park located in Sorrento Mesa, San Diego, has been sold for a price of $45,000,000. The park consists of seven buildings and spans approximately 139,340 square feet, resulting in a price per square foot of $323.”

Stephen Buschbom: “So Lonnie - as you were going through those stories, I’m gonna show my age here, but when you’re reading off the dollar-per-square-foot here, I’m thinking, gosh, when I was underwriting this stuff it was $40, $60 a square foot price, and if we hit $80, or heaven forbid $100 a square foot, you got some raised eyebrows who thought this stuff was rich, so it continues to amaze me how far we’ve come with industrial valuations, and the strength this market shows, with few signs of slowing.”

Hendry: “…We’ll see how long this can last. The first story we talked about, that had a 14 to 16-foot clear height, to your point, that’s like a $45 a square foot building in my brain, sold for 322 bucks.”

“We drank a lot of cheap debt for a long time and the reckoning is painful.”

Matthew Cypher, director of the Steers Center for Global Real Estate at Georgetown University’s McDonough School of Business

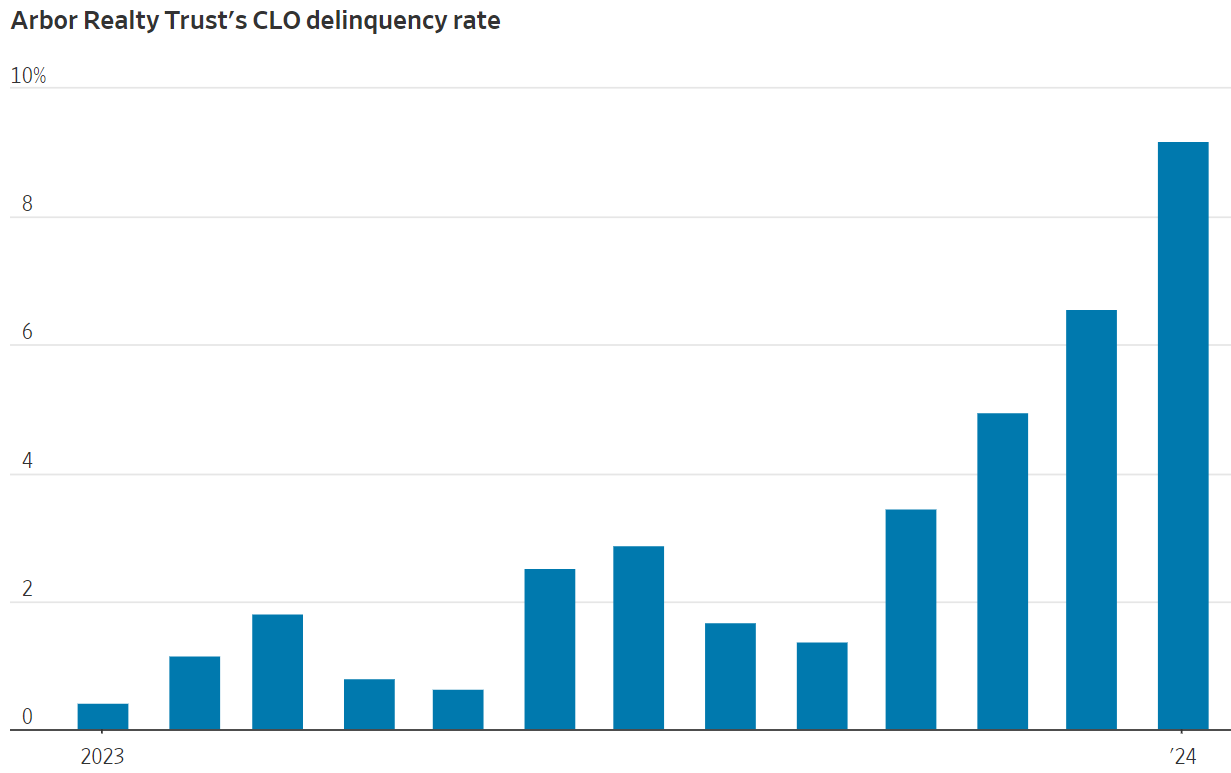

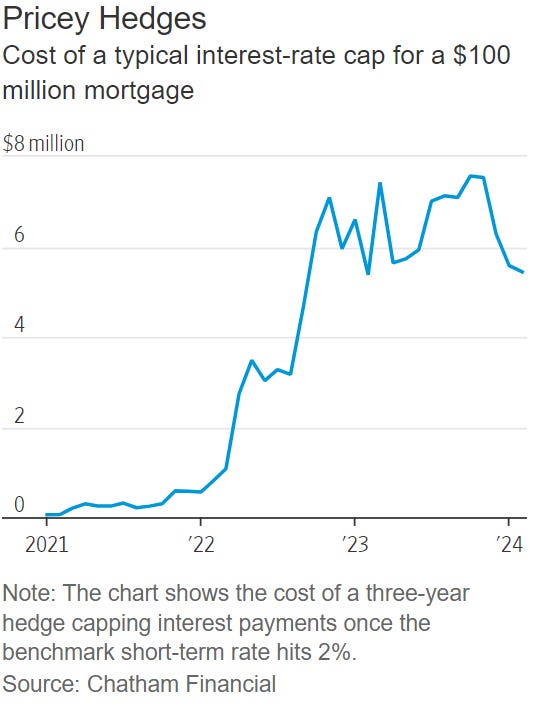

“Arbor Realty loans funded a Sunbelt apartment boom. Many of its borrowers are now struggling with higher interest rates.”

“Most borrowers who were late on January payments eventually paid, an Arbor spokesman said, and he said 5.8% of Arbor’s securitized debt payments are still not current on January payments…The company sits at the center of what a growing number of analysts say is one of commercial real estate’s biggest trouble spots: floating-rate apartment loans. “Multifamily could be the next shoe to drop,” said Jade Rahmani, a real-estate stock analyst at KBW…

The vast majority of late payments on CLO loans haven’t led to foreclosure. Still, the large number of late payments shows the strain on borrowers and the growing risk of losses for lenders.”

Related: Unpacking The CRE CLO with Stewart McQueen of Dechert

Aleksey Chernobelskiy: Capital calls: when, why, and how limited partners can respond His substack: Limited Partner Investing Lessons

CRE Loans Coming Due in 2024 Balloon to $929 Billion, as Loans that Matured in 2023 Weren’t Paid Off but Extended

On February 6, 2024, a $975 million loan on a 1.58 million square-foot One Market Plaza office tower in San Francisco matured. In January, credit-rating agency KBRA warned that the loan faced “imminent maturity default.” The tower, owned by a joint-venture of Blackstone and Paramount Group, was built in the 1970s and renovated in 2016. It was refinanced in 2017 with an interest-only mortgage of $975 million, which was then securitized into a single-asset CMBS (OMPT 2017-1 MKT) and sold to investors, including a variety of bond funds…

So the Blackstone-Paramount joint-venture and the special servicer representing the CMBS holders sat down and made a deal in January, ahead of the loan expiration, and last week, they announced the details of their deal: the mortgage was modified and extended.

The joint venture agreed to pay down by $125 million the existing $975 million loan and bring it to $850 million.

This modified loan has been extended for three years to February 2027, with an option to extend it for another year.

The existing loan’s fixed interest rate of 4.03% was raised to 4.08% for the modified loan.

So the landlord got a huge deal in terms of the interest rate (4.08%, fixed for three years), which is below the three-year Treasury yield (currently 4.26%), and far below current CRE mortgage rates. And they got a huge deal by not having to get a new loan, which would have been nearly impossible, and much more expensive. The CMBS holders got a deal because the loan was paid down by $125 million, thus reducing their exposure and potential loss, and because they didn’t end up with an older office tower that they would have to sell in the worst office market in the US, and take massive losses.

Now both parties pray that in three years office CRE is a changed world with full offices, low availability rates, higher rents, and much lower interest rates. And if that’s not the case, it’ll start all over again. But until then, extend and pretend averted massive losses for both parties. That’s how the better office properties will be dealt with: Extend and pretend in the hope for better times. Weaker office properties – where extend and pretend cannot be worked out – will go back to the lenders, and they get to sort out the fate of those properties at massive loss ratios.

Evergrande

“Investors probably did not fully appreciate the risk of state intervention,” said David Knutson, chair of The Credit Roundtable, an organization of investors that works to respond to corporate actions averse to bondholders. “Apportioning losses between domestic creditors and foreign creditors will be political.”

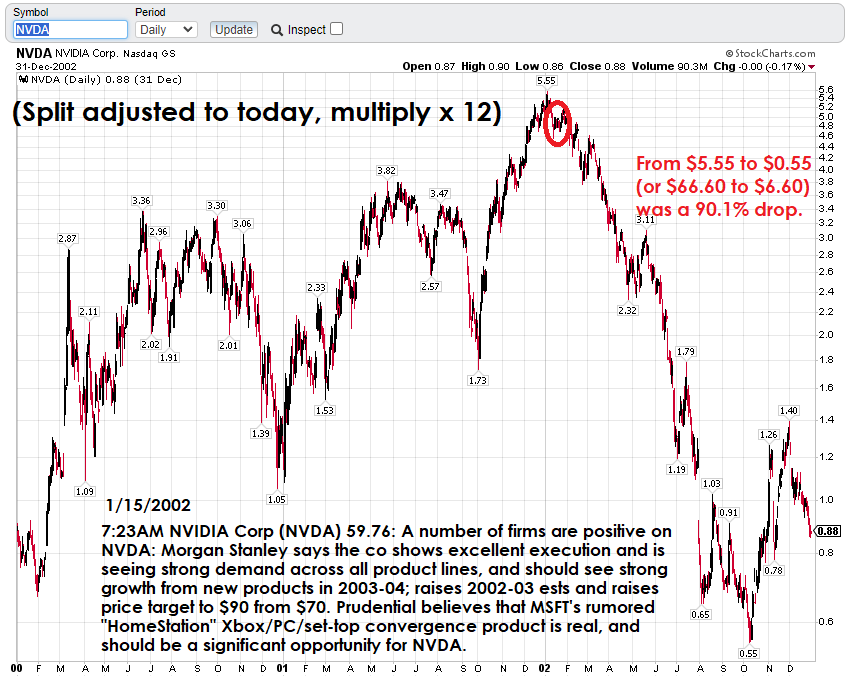

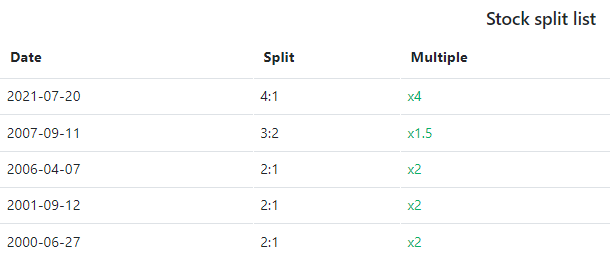

Nvidia 2002

Not many people can hold through a 90% decline, as Nvidia holders did in 2002 (there was also about an 85% top-to-bottom drop in 2007-2008).

January 2002

THE ONE THAT GOT AWAY. I OWNED THIS ONE AND SOLD TOO SOON.

It's hard to believe, but Wall Street's big winner of 2001 was a technology stock.

Nvidia Corp., which makes graphics chips for Xbox , Microsoft Corp.'s popular game system, saw its shares more than quadruple, making it the year's best performer in the Standard & Poor's 500 index.

Nvidia opened the year at $16.50, and then quadrupled to close 2001 at $66.90 -- even as shares of dot-coms, chip makers and telecommunications companies melted -- fueled by a strong video game market and its recent addition to the prestigious S&P 500.

The Santa Clara, California-based company, however, hopes to avoid the fate of earlier winners.

Nvidia inherits the award from Enron Corp., the once-darling energy giant now shattered by its murky finances. Opening the year at $83.13, Enron shares now trade at 60 cents, a drop of 99 percent.

In 1999, the winner was wireless communications company Qualcomm Inc., which rocketed 2,600 percent amid an inferno of optimism that eventually burned out virtually the entire sector. The stock now trades nearly 75 percent below its 1999 high, adjusted for a stock split, of $185.03.

Qualcomm achieved a bit of infamy after failing to achieve one of the most bullish predictions of the dot-com era. A PaineWebber analyst said the stock would hit $250 a share, which, before a four-to-one split, was equivalent to $1,000.

Widely respected among video game fanatics, Nvidia makes chips that churn data into realistic-looking video in game systems and computers. Its stock has succeeded even as the S&P 500 index dropped 12 percent.

Nvidia has outperformed its customers, growing earnings in the third quarter by 60 percent despite the worst-ever slump for the semiconductor industry, which was ailing from overcapacity and sluggish demand.

In the summer, however, Nvidia was hit by heavy speculation that its stock would fall because of impending competition from other graphics chip companies. Some investors predicted the stock would dip to $15 a share, a forecast the company has thus far shown to be false.

Marc Klee, co-portfolio manager of the $900 million John Hancock Technology Fund, said Nvidia will face competitive challenges in 2002 that could threaten its stock performance. But, he said, the company is not likely to repeat the troubled history of past top performers.

``Unlike Qualcomm and Enron, where there was a very strong consensus, you don't have that with Nvidia,'' he said, referring to the boundless optimism about the first two companies.

Fun podcast. Bob's disclaimer is epic.

Best line: "If you're not a conspiracy theorist that just means you haven't read enough." - Jim Iuorio

"I still know people who are in Cisco. They have prices above 65, and they've been holding it since 2000 hoping to break even." - Mike Arnold

“Shadow Vacancy”

Jeff Snider and Ken McElroy on CRE

“I was talking to a guy this weekend. He had an office building in San Francisco, and one in Phoenix, and his rent was a million dollars a year, and he wasn't even going there because his employees now all work from home. So he's just waiting for those leases to burn off, and you're starting to see these leases burn off. There's a lot of folks that have changed the way they do business, and they're not going to go back into these office buildings.” - McElroy

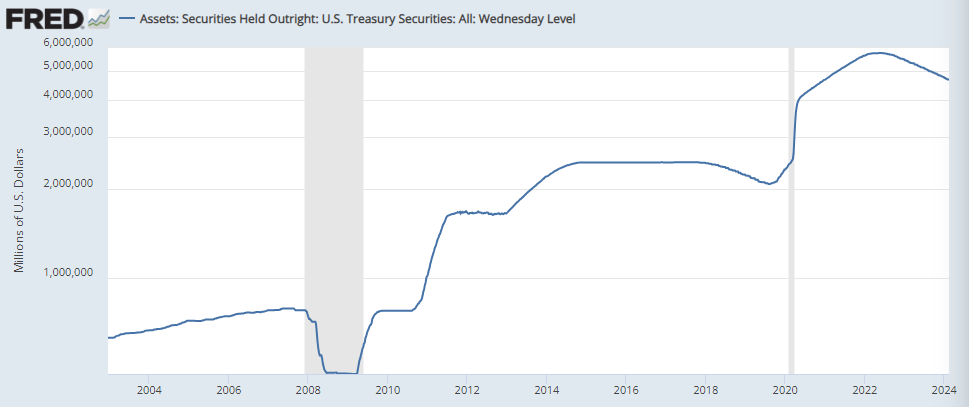

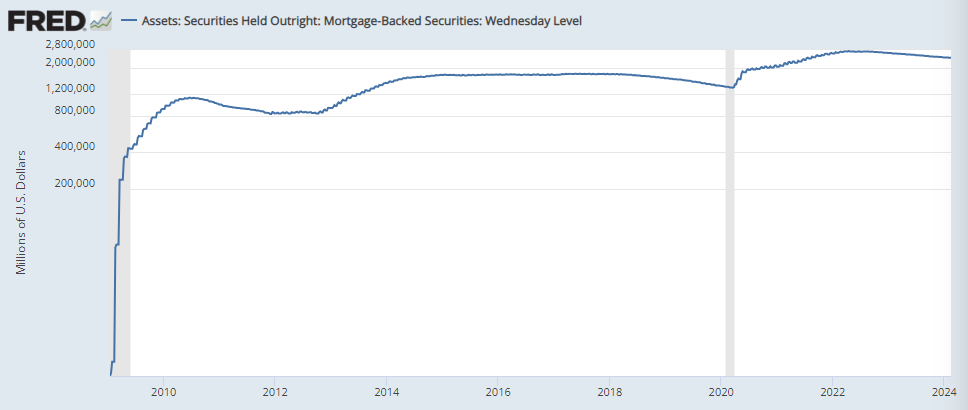

Quantitative Loosening

“They've certainly said that they [the Fed] could continue to shrink the balance sheet, maybe at a tempered pace compared to where they are now, and certainly if they're lowering interest rates, and that was to show up in people paying their residential mortgages off at a faster pace, then the Fed could could allow the mortgage-backed securities to come off of the Fed's balance sheet while they pull back on quantitative tightening on the treasury side.” - Danielle DiMartino Booth

“It's very likely by March of 2024 the Fed will have to seriously rethink its QT proposals and likely slim these down significantly.” - Michael Howell

And this is the one I think is particularly outrageous and unforgivable - the Fed massively distorting the U.S. mortgage market:

The Fed still holds $2.417 TRillion of MBS, as opposed to ZERO in 2008.

Michael Howell

“If the private sector defaults, that has a deflationary effect on an economy. If public debt defaults, well in fact the reality is it doesn't default, it tends to be inflated away [which is just a more dishonest type of default - rh], and what you can really say as a very broad summary is that private debt crises are deflationary, but public debt crises are inflationary because the government doesn't default, what it does is it prints money to pay back its debts. It monetizes the debt. Now that is what is going on in several countries and the heads up is it is happening in the US as well.”

Nasdaq 100 vs Russell 2000

“Two years ago the United States came out and said, U.S. treasuries are only risk-free if you forever more agree politically with everything the United States says. And increasingly, the United States, geopolitically, economically, socially, and culturally has been losing its mind…”

“What nobody ever talks about is - the biggest macro development for me of the past 15 years or so was the Permian revolution - the fact that all of a sudden the US added eight and a half, nine million barrels a day, or eight million barrels a day, to to its production. Massive increase in natural gas, collapse in the price of natural gas - all this gave the US a tremendous tremendous comparative advantage. Well, what you're describing is a world where the US will suddenly lose this comparative advantage.”

"The U.S. is a hedge fund dreading a margin call."

Why We Shouldn’t Trust BlackRock with Whitney Webb & Mark Goodwin

Tom Gara: “NY Mag's personal finance columnist was convinced by a cold caller claiming to be a CIA agent in Langley that she needed to empty her bank account, put the money in a shoebox and give it to a guy coming to meet her on the street.”

Larry Summers strikes again: Federal regulators are probing whether Cash App leaves door open to money launderers, terrorists

Excellent post and love the "no housing bubble" quotes.

I'm assuming the Bloomberg Bankruptcy chart was for companies? I think I shared that in my client books, bankruptcies increased 200% month-over-month.

That Redfin headline really annoys me as I think it is political....below the headline it also says "Overall, investor home purchases dropped 11% from a year earlier, though that’s the smallest decline since they began falling in 2022." It may be the smallest, but it is still declining. But, if stock market sentiment keeps on going I am sure they will start putting their foot on the gas. Just wish headlines could be less....

I clicked the cnbc link for January retail figures and got a pop-up giving me the opportunity to claim the offer for “CNBC Club - Cramer’s Executive Offer $149.99 for 6 months”

I don’t know what CNBC Club is, but using Cramer to try to sell it is perfection.