Ordinary People

1995 or 1999?

Apropos of nothing…

Many people, once they have tied their entire identity to some thing, can't tolerate any questioning of that thing, whether it's gold, bitcoin, Nvidia, a political candidate or ideology, an NFL team - whatever. Their insecurity is painful to see.

Sentiment Check:

Not many short-sellers left…

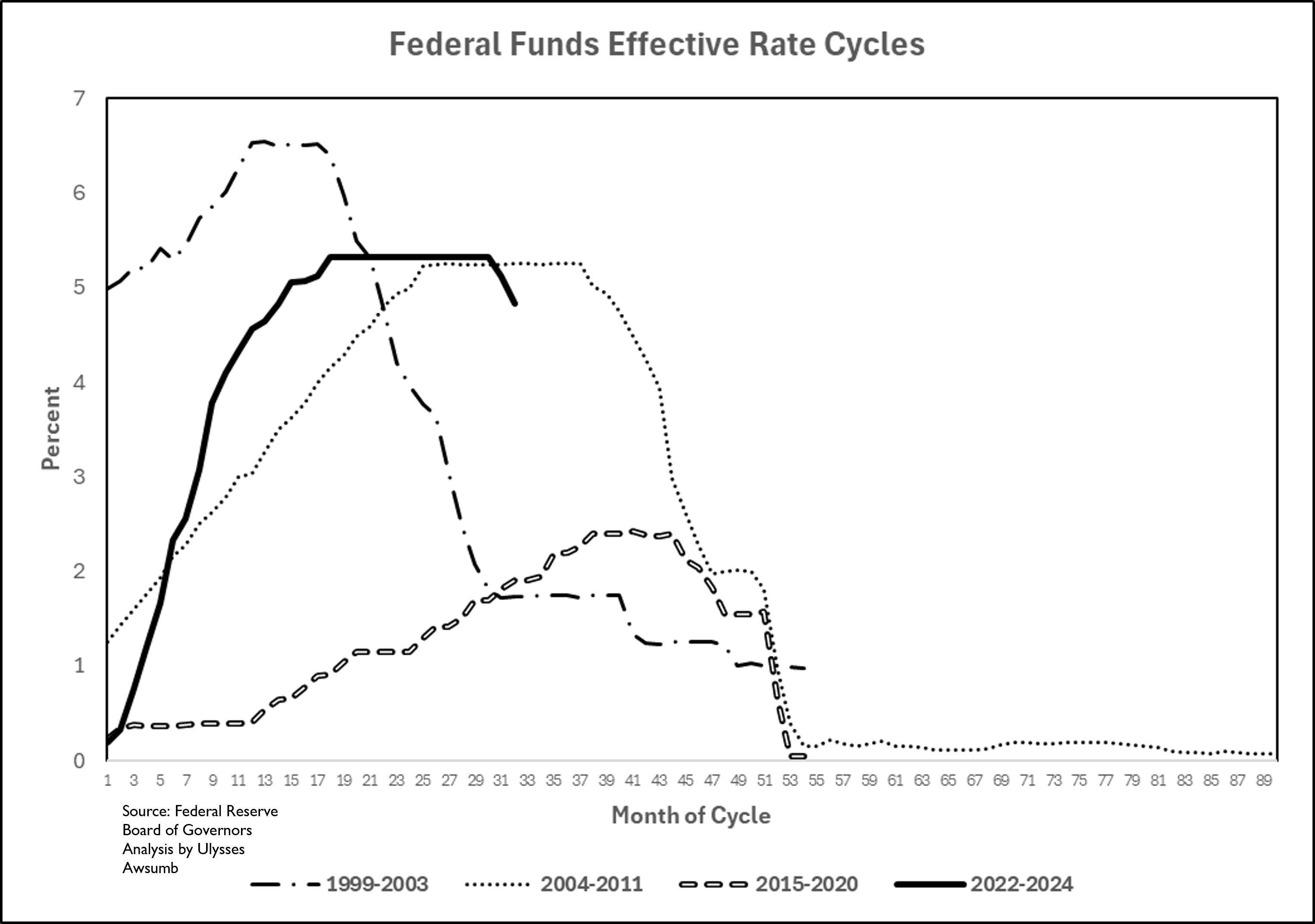

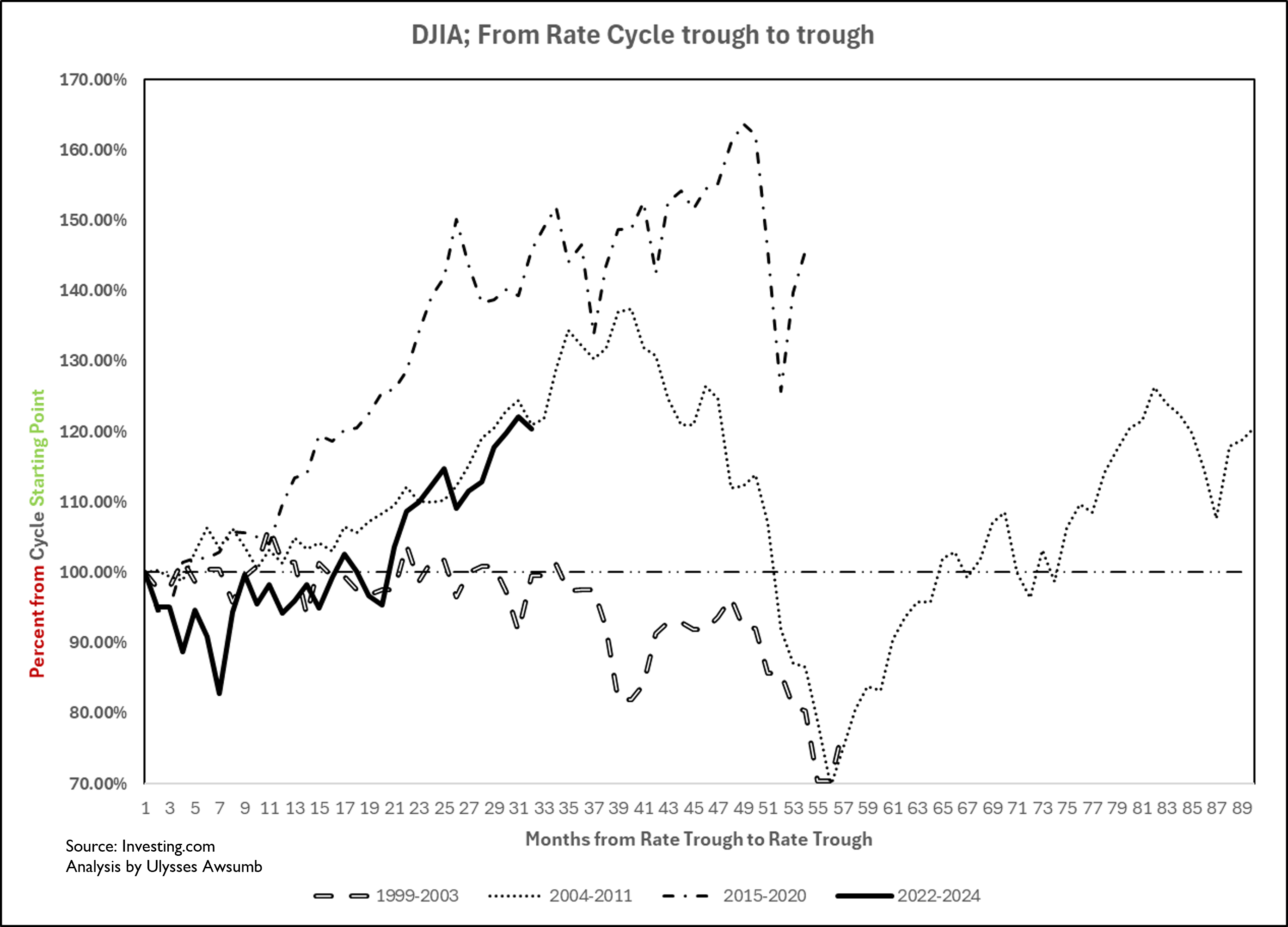

Some interesting charts and commentary from The Fourth Rate Turning, by friend of the show Mr. Awsumb.

From friend of the show Jim Walker:

“We must look at the scale on the respective y-axes to understand the enormity of the problem. Federal government spending prior to Covid never reached the heights seen since on a quarterly basis.”

The above figures are post-Covid, a period Biden, Yellen and the media described as “the best economy ever.”

Walker:

“No matter how hard we look at it, Mr. Trump looks boxed in and his key policy, the imposition of tariffs, looks set to deliver his worst outcome – higher inflation and reduced US growth at a point when interest rates are being forced higher and the dollar is rising. Full-blown recession could be staring him in the face within six months. If that were to come to pass, all the dollar’s recent strength would evaporate.”

“It was always the Fed's job to make the Treasury look solvent. That was their job, but now you can't do it.”

Scrooge McDuck Explains (1967)

Insurers’ Rule Change Puts ALL California Homeowners on the Hook for L.A. Fire

“A little-noticed rule change last year by California’s insurance regulator will likely shift a large chunk of the cost of the Los Angeles wildfires to homeowners across the state.

Pushed by insurers, the change puts California homeowners on the hook to pay directly toward the cost of rebuilding from very large disasters through even fatter insurance bills—whether they were exposed to the L.A. fire or not.

“That would be a huge wake up call for Californians because they have no idea that the rules have changed,” said Dave Jones, a former California insurance commissioner.

The new policy affects the backstop for California’s Fair Plan, the state’s insurer of last resort, which sells fire-damage policies to homeowners who can’t get coverage elsewhere.

The worry is that the Fair Plan lacks the resources to pay for the quickly escalating cost of the fires, which have destroyed tens of thousands of structures.

The rules change means insurance companies can bill their customers if they are forced to bail out the plan, which has an estimated $200 million in cash and $2.5 billion in reinsurance, according to data it reported last year.

That is likely not enough to cover the Fair Plan’s share of the losses from the fires, forecast at up to $6 billion by analysts at Evercore ISI.

The Fair Plan’s business ballooned after private insurers pulled back from the state, gearing up for a disaster by not renewing policies as their risk models warned of likely conflagrations.

“Most people thought the time would come, but no man prepar'd for it, no man consider'd it would come like a Thief in the night, exactly as it happens in the case of our death. Methinks God has punish'd the Avaritious as he often punishes sinners, in their own way, in the very sin itself: the thirst of gain was their crime, that thirst continued, became their punishment and ruin.”

Alexander Pope, on the South Sea Bubble

“Ordinary people are struggling, but ordinary people are never interviewed on CNBC, or on your program, or on Fox News. They have no voice, so the elite can tell the public, ‘Oh, the economy is doing well.’”

Below the Fold: David Dredge, housing, Greg Weldon, Brent Johnson, Dan Rasmussen, high-yield spreads, Michael Howell, Rick Rule, Simon Mikhailovich, Chuck E. Cheese, random music and more.

Welcome to the (new) paid subscribers. I appreciate it. Give it a spin, and if it’s not for you, that’s fine. Thanks to all those who have stuck around. I imagine there’ll be no shortage of material in the coming years.

Unpopular Thought: A tremendous amount of energy is expended talking about the dollar, when it seems to a simpleton like me that it really hasn’t done much over time.

Then again, here’s David Dredge…

“I’ve talked again about just nostalgia that I feel at the moment for the 1995-1999 period when US equity markets just ripped straight higher, and the dollar ripped straight higher and tore apart all the rest of the world and everybody who had tied themselves to the dollar. And you see some sort of, I don’t know, similarities around that with the dollar strength since the Trump election, since the Fed rate cuts, the equity market strength, the higher longer end bond yields, which again we saw after the ‘95 to ‘96 Fed rate cuts and in the ‘98 rate cuts. In both cases 10-year yields went higher, which is kind of unique.

Obviously, people have been talking a lot. I think I heard you and Cem talking about it last week about what happens after S&P is up over 20% two years in a row. Usually it goes down. The exception to that rule is 1995 to 1999 where it went up over 20% five years in a row compounded over that five year period, I think total return with dividends at 28%, 29% for five years with every year up over 20%.”

In late 1999. in under 6 months, the Nasdaq composite went up over 80%.

Wall Street Thinks U.S. Homes Are Overpriced

“House hunters don’t need to be told that property is too expensive right now. But Wall Street has an idea by just how much.”

Reminds me a bit of when it is said that it’s cheaper to buy oil in the stock market than in the ground.

“The stock market is pricing portfolios of American homes at a hefty discount to what houses are changing hands for in the open market. Shares of single-family landlords Invitation Homes and American Homes 4 Rent are trading at 35% and 20% discounts to their net asset values, respectively, according to real-estate analytics firm Green Street. Invitation Homes’ stock has traded at a particularly large discount to NAV since interest rates began to rise in early 2022, but the gap has widened by 10 percentage points in the past year.

Put another way, while the average house in the metro areas where Invitation Homes owns its properties sells for $415,000 based on Green Street’s analysis of prevailing market values, the company’s share price implies that investors think $310,000 is more appropriate…

“Share prices are signaling that single-family-home prices are too high and are not sustainable,” says John Pawlowski, a managing director at Green Street. However, he points out that home values can remain disconnected in public and private markets for longer than for commercial real estate because prices are set by owner-occupiers rather than investors.

Wall Street landlords are notably quiet at the moment. In the third quarter of 2024, large institutional investors that already own more than 1,000 properties were behind just 0.3% of all U.S. home purchases…

Notably, landlords can’t make the math work, even though their cost of debt is slightly lower than a regular buyer.”

Counterpoints:

I’d love to see a 35% drop in house prices near me (an exceedingly unpopular view on Fintwit by the way). It’d be bad for me on paper, but great for young families (assuming Blackstone didn’t come in and buy everything).

Then again…

“Home prices are on the hop across the United States, freshly released data from Redfin show, as each of the top 50 metro areas logged a year-over-year increase in December to mark the first such comprehensive updraft since May 2022. That clean sweep is particularly impressive considering the fact that 30-year mortgage rates now average upwards of 7% per Freddie Mac compared to about 3% in 2021…

“Places that have been long known as affordable. . . like Cleveland and Milwaukee, are now seeing double digit price increases – and that’s after home prices skyrocketed during the pandemic,” commented Redfin senior economist Elijah de la Campa. “Affordable housing havens have become harder and harder to come by; even places that saw some price relief last year, like Texas and Florida, are now seeing prices tick back up.”

…lumber futures now change hands at $585 per thousand board feet, up 31% from the late-June nadir and 10% north of their average price over the past two years. Thanks to Covid-induced supply hiccups and feverish demand in response to generous fiscal and monetary stimulus, lumber prices spiked to nearly $1,700 in May 2021 after averaging $356 over the five years through 2019.”

I think these cities all have one thing in common/

Hedge Funds: A compensation scheme masquerading as an asset class.

"A hedge fund is a “compensation scheme masquerading as an asset class”...Investors in hedge funds have paid out almost half of their profits in fees since the early days of the industry more than half a century ago, the data shows.

Managers generated $3.7tn of total gains before fees, but fees charged to investors were $1.8tn, or about 49 per cent of gross gains, according to LCH.

The figures, which date back to 1969, show how the scale of the fees raked in by managers has soared as the industry has matured.

“Up to the year 2000, the hedge fund fee take had been running at around a third of overall gains, but since then it has increased to a half”…The increase in the overall fee take from 30 per cent to about 50 per cent of gross gains is largely the result of higher management fees…

Whereas management fees used to eat up less than 10 per cent of gross gains in the late 1960s and 1970s, they had taken almost 30 per cent in the past two decades, LCH said."

Just noticed this…

“The 40-year downtrend in inflation and interest rates is over. It's toast.”

- Greg Weldon

Weldon:

“They've been cutting rates even though inflation is nowhere near the target rate”

“We have seen declines in revolving credit for 3 months within a period of 18 months only twice: the pandemic, the 2008-2009 crisis, and now.”

“The only other time when you had multiple months in a row with real retail sales and eating and drink establishments negative was 2009 and 2010. That's it.”

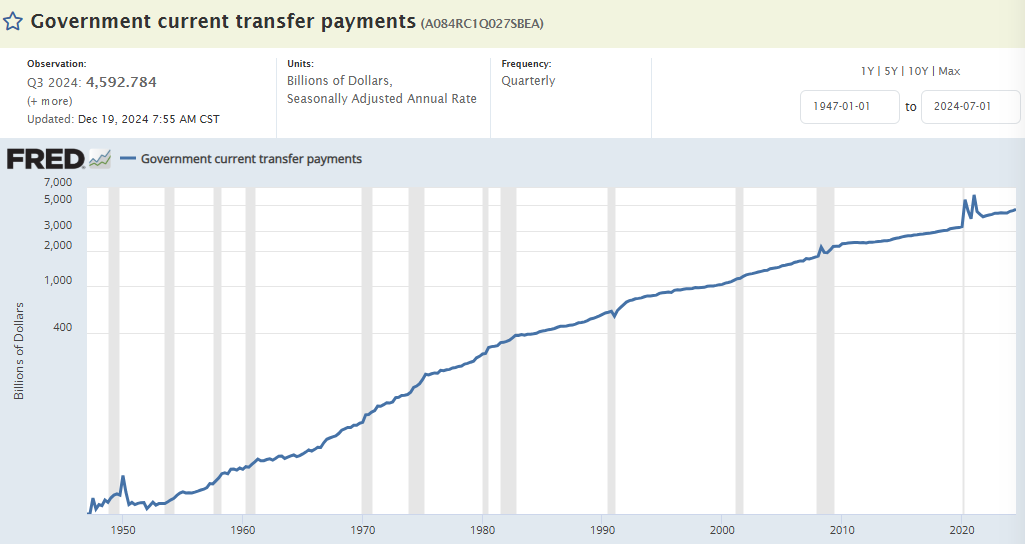

“Transfer payments from the government - you know, social care, entitlements, all this kind of stuff - is right now $4.6 trillion, 12 months running total. It's the fourth highest ever outside the pandemic, and including the pandemic this the eighth highest ever.”

Brent Johnson

“If you analyze the United States in isolation, and you look at its policies and its fiscal position, and the amount of debt that it's borrowed, and these crazy programs that the politicians have put in place - there's really no conclusion you can come to other than that this is a situation that's going to end in a disaster. The problem is is we don't live in a vacuum. It's a big world, and currencies trade relative to each other. So when you do the same level of analysis on the other countries you quickly realize that they have almost all the same problems that the United States has, but they don't have nearly the advantages that the United States does.

For all of the problems that the United States has, we still have an incredible amount of resources, economic weapons, military weapons, rule of law - and I know a lot of people will say those have all degraded over the last 20, 30 years - and I guess I'm kind of sympathetic to that argument, but again it's a relative basis. Where is it better? And if you can't find someplace that is better, then that thing that you're looking at is probably going to outperform, and that's kind of the the conclusion that I have come to. I certainly think we have a number of issues. I think they're sort of in the process of being addressed. How? Well, they're addressed in the timeline it takes to address them. That's a bit of a wild card, but when I look around at other countries around the world, they're in the same position, and if I had to bet on one place, I'm happy to bet on America.”

Dan Rasmussen: Smart Investors Are Too Early

“I read a bunch of investor letters from the great investors, Ray Dalio, Peter Lynch, Howard Marks, Seth Klarman - you know, what were they saying in the 90s? It was really interesting, because all these great investors knew it was a bubble. They all wrote about it. Ray Dalio said we're approaching a blowoff phase of the US stock market. Peter Lynch said not enough investors are worried. The only problem is that those two quotes are from 1995. Smart, data-driven people can pick up on these things, valuations are too high - the problem is that smart investors tend to be way too early. The bubble didn't burst for five years, and each subsequent year it doesn't burst, you look stupid, and the people that supported the bubble look right. I think that that's the type of situation we're in now.”

Spreads

“I like to look at the high yield spread - high yield relative to treasuries, duration matched, which is - there's actually been research showing the longer that the longer spread stays abnormally low, the greater the risk of a financial crisis…” - Dan Rasmussen

ICE BofA US High Yield Index Option-Adjusted Spread

Currently 2.73%. Since 1997, the average is 5.29%, the median is 4.63%, the lowest was 2.43% in June 2007(!), and the highest was 21.09% in December 2008.

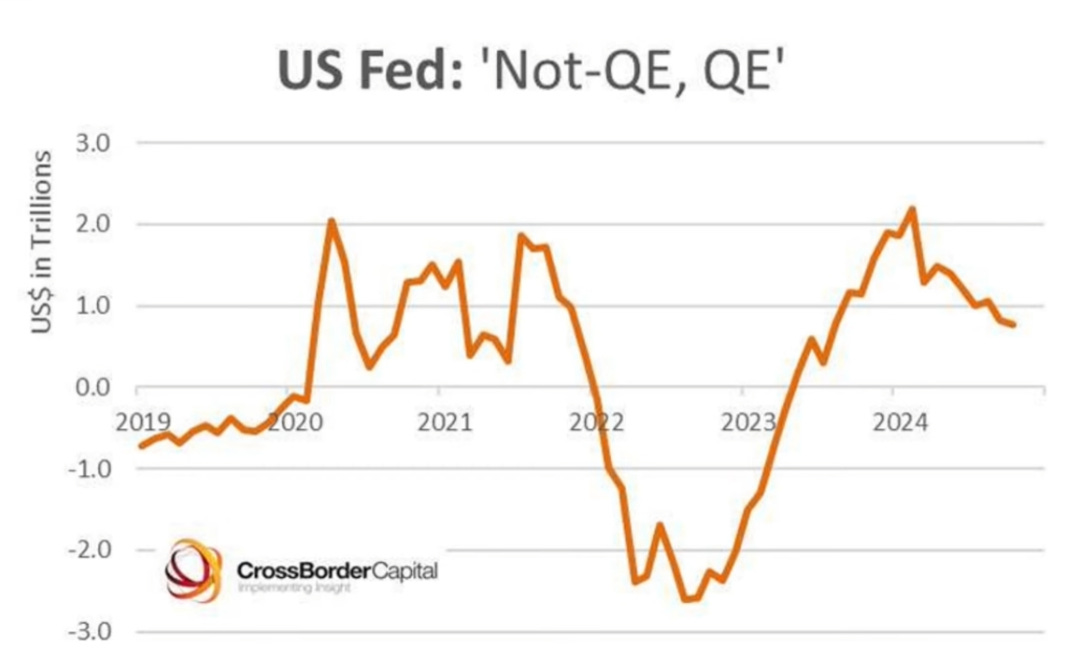

Michael Howell

“They're purportedly doing QT, Quantitative Tightening, but actually they're injecting liquidity. Now, how can they do that? How can we square that circle? That is because they define their QT in terms of the overall balance sheet size - so the overall balance sheet of the Federal Reserve is definitely shrinking, that's not a question but not all items on the balance sheet actually create liquidity. So even though the overall balance sheet is shrinking, the non- liquidity-creating parts are falling much faster and the liquidity creating parts are actually expanding, and specifically, things like the reverse repo facilities being wound down quite dramatically - you've got fluctuations which are occurring in the Treasury general account, which is an account that the Treasury holds at the Fed - it's like a cash deposit account. They can run that down or build that up. That's been a source of liquidity at different times. You've got the bank term funding program which was a support program put in place during the Silicon Valley Bank turmoil. That's now run off, but it was adding liquidity through the year, and you've also got the operating losses that the Federal Reserve is suffering because it's paying out more interest to coupon holders than it is taking in, or it's basically paying out more on the the reverse repo facility than it's that it's taking in, and that basically is a source of loss, but it's actually an injectional liquidity for markets. So all these factors add up, and you can see on slide 15 we calibrate that in what we call not-QE QE.”

“It was a very painful spring. You couldn’t be half the index weight in the biggest sector that was going up the fastest and expect to keep up with the indexes, much less the pack. Some of my clients became upset as their portfolios lagged, and I was subjected to considerable abuse. Some of it was well-meaning advice. A Japanese friend told me of an old and famous Japanese proverb about manias. It goes, “Only fools are dancing, but the bigger fools are watching.” Someone else unkindly quoted Nietzsche: “And those who were seen dancing were thought to be insane by those who could not hear the music.” Those pithy sayings made me feel like an idiot for not participating at the Great Tech Ball. The young, swaggering tech types at the office rolled their eyes.”

Barton Biggs, Hedgehogging

Rick Rule

“If you use the CPI number, the arithmetic around the US 10-year Treasury isn't bad. You're getting paid four and a half percent a year in a currency where your purchasing power is declining by 2.6%, which means you're getting almost 2% real yield. If, by contrast, you use the seven and a half percent number - that is, you're getting paid four and a half percent in a currency that's depreciating by seven and a half percent, you're losing 3% a year. The concept of investing in a riskless asset - a US 10-year Treasury - where your purchasing power declines by 3% a year compounded over 10 years is not very attractive.”

“JP Morgan Chase suggests that the market share of precious metals and precious metals-related securities is less than one half of one percent of total savings and investment assets in the United States. In other words, an infinitesimal market share. The four-decade mean market share is estimated by JP Morgan Chase to be 2%, so gold doesn't have to win the war against the US dollar, gold doesn't have to demolish the treasury markets like some gold bugs suggest. All it needs to do is return to mean. If it returns to mean, demand for this asset class increases fourfold. One can only guess what a four-fold increase in demand would do to a commodity where increases in supply are extremely limited, and that's precisely what I think is going to happen.”

“I don't own gold uh because I think it might go from $2,700 to $3,000. I own gold because I'm afraid it's going to go to nine or ten-thousand.”

“What'll happen is that if you're supposed to get $4,000, you'll continue to get $4,000, but the $4,000 will buy you $1,000 worth of stuff. In other words, they will not index your tax to inflation, and they'll inflate away the value of your benefit. That's precisely what they did in the decade of the 1970s.That's one of the reasons why the CPI understates the rate of inflation…it is in their interest to

understate inflation.”

“So you're cruising along, making $100,000 a year thinking you're doing very well, and when you're budgeting for yourself in 2035 think about the fact that that $100,000 will buy you $25,000 worth of goods and services, so plan your savings and your retirement accordingly”

“I'm delighted that being anti-establishment has become popular. I'm delighted by the protest vote. As to Mr. Trump personally, I read his book, The Art of the Deal, and he believes fundamentally differently than I do. I believe in a transaction where both sides do well, and he believes in a one-sided, or - pardon me - in a winner-take-all transaction, a win- lose transaction. I don't believe in that.”

“I don't believe that Mr. Trump is serious about cutting spending I think he's serious about rewarding people who give him power. By the way - I don't think he's worse than who he preceded. I don't think he's as good as the people who purport to be his acolytes believe him to be. As to the department of government efficiency1, I think that's the strangest form of fiction I've read in many years. The first instance, to appoint the person who heads it, to appoint to that position somebody who has enjoyed literally billions of dollars of subsidies and transfer payments - I mean, you know, Tesla wouldn't exist without subsidies, nor would SpaceX, so to appoint admittedly a very efficient hog who was wallowed up to the trough to be the person to remove the feed from the trough seems suspect to me.”

“I would probably change the defense budget to reflect the dictionary definition of “defense,” which is to say the protection of the domestic interest within our

borders. I wouldn't have troops in 110 countries. A Rule Presidency would be truly ugly, a fact-based presidency, one that isn't narrative-based. I think it would be extremely unpopular with Americans, so at this point, all roads lead to

inflation.”

“The US dollar is the worst currency in the world, with the sole exception of all the others. When I do the arithmetic around most countries, including our neighbor to the north - who I'm very fond of - their math is even worse than

ours. Their expectations are lower, and they have not had the ability for 40 years to externalize their inflation by maintaining the world's currency.”

Simon Mikhailovich

“For the past 20 years, or 30 years or 40 years, the main priority of financial authorities and the government has been maintaining this wealth effect, maintaining the stability of the financial markets and suppressing volatility. The priority that is emerging, which is why Trump is talking, what he’s talking about, is geopolitical risk. And if you have to choose between dealing with one and the other, I think it’s clear that the US government and any government would ultimately favor national security matters. They don’t want to make that choice.”

“Inflation that’s manipulated down to present there’s real growth going on, where I don’t think in aggregate the economy has been growing, which that’s why we see people in the lower distribution of income suffering more and more. What’s been growing are financial markets, which is a derivative of the real economy, but derivative of the real economy is separated from the real economy. And so, when that kind of money is sloshing around, when you have Fartcoin, which has become the poster child of this latest episode, going from not being around in October to becoming worth a billion and a half, to whom, for what, with what money, what is this? And unlike some other cryptos, I mean, this is a joke to begin with.”

What's the over/under on when Chuck E. Cheese goes bankrupt?

Search Tips

If you want to search for something in my posts, this is the best method I have found. Using Google, enter:

keyword(s) site:rudy.substack.com

e.g.,

“harley bassman” site:rudy.substack.com

Some more color on searches from friend of the show Jim (thank you):

“A joke's a very serious thing.”

The Predictable Capitulation of Tulsi Gabbard

“…Tulsi Gabbard now says she is all for the unconstitutional law that permits the national security state to surveil Americans without obtaining legal warrants beforehand — a law Donald Trump’s nominee for director of national intelligence has previously and vigorously pledged to repeal…

You had to admire Gabbard for all the noise she made about Section 702 during her years in Congress as a Democrat from Hawaii. She voted against reauthorization on several occasions. In 2020 she co-sponsored a bill with Thomas Massie, a Republican and an ardent constitutionalist from Kentucky, to repeal not only the post–Sept. 11 FISA Amendments Act, but the whole of the egregious Patriot Act.

Gabbard quoted Ben Franklin and laid into the intelligence apparatus for “not [being] transparent or honest with the American people or even Congress about what they’ve been doing.” Among much else, the bill she co-sponsored made retaliation against whistleblowers illegal and banned the National Security Agency’s use of the “back doors” the NSA was using to gain access to computers, telephones, televisions and who knew what else.

The Protect Our Civil Liberties Act did not pass, needless to say. But it was a carefully researched, serious piece of legislation.

Then, long story short, came Trump’s tap on Gabbard’s shoulder. She seemed an obvious choice for a President-elect determined to prevent the Deep State — the Central Intelligence Agency and the rest of the national security apparatus — from subverting his second term as it had his first. It does not look now as if Gabbard will perform this service for Donald Trump even if she wins Senate confirmation when her nomination comes up for review…

The press I am reading from Washington indicates that Gabbard has little chance of winning any Democrat’s support for her nomination, so thoroughly and disgracefully has the party allied with intel since the old Russiagate days. On the Republican side, they have made it plain that Gabbard’s stance on Section 702 of the FISA laws is more or less make-or-break: insofar as she can become DNI or sent back to the wilderness.”

“We put U.S. troops inside Syria with the Kurds years ago, to kind of keep them from being annihilated, so right now you’ve got the Turks and their Islamic allies waging war on the Kurds, and our troops are right in the middle of that, so you could just wait for any day that our guys are going to start - intentionally or unintentionally - some of our guys are going to get killed, and then you're going to be, like, so let's see… A NATO ally just killed our guys. What's the plan now? What's happening is it’s a mess. It's a real mess, and I don't think anybody has a freaking plan for what we're doing about it.”

“In a democracy, the tragedy is that people like the policies that lead to inflation. They like subsidies. Musk lives from subsidies from the government. It's a joke. Now they put him in charge of cutting government expenditures. do you think he's going to cut the subsidies that the government pays to him?“ - Marc Faber

Donald Duck quacking Austrian economic theories of sound money in 1967???? I guess our ruling elite were busy watching Road Runner cartoons instead.

Thanks again for a wonderful read! A far better way to start my day than the drivel which the WSJ has become. I will be chuckling over the Jay Powell toast image all day! 😂😂😂