Salting the Lots

Bitcoin: the painting in the attic

This is a fantastic idea:

Which one’s fake?

“The U.S. is starting to behave more and more like a third-world emerging market economy than an advanced economy, with budget deficits this large. It’s a huge issue, and it’s something that the bond market is going to have to grapple with.”

The DXY

Janet’s phony photo-op

You can see the anger on her face after her insensitive comments led the Biden Admin to order a photo-op with the serfs, forcing Yellen to leave her nice pleasant gated community and physically walk into a DISGUSTING grocery store filled with mask-less dirt-people!

"The key is to learn to translate elite-speak to English. "Disinformation" is code for dissent. If there's enough dissent, then it makes it more difficult for them to do their job, which is to rule the world. Dissenters are getting in their way.”

BennyOcean

“An era called Neoconservatism”

“It really was started in the last year of the Bush Sr. White House in 1992. And it was really started, you can pinpoint it, by the Secretary of Defense Richard Cheney, who of course, went on to become vice president under George W. Bush Jr. and his deputy, Paul Wolfowitz, and they already in 1992 said, We're it, we're the only superpower in the world. Our grand strategy as a nation is to remain completely unchallenged, what came to be called Full Spectrum dominance in every part of the world. So we have to be militarily the dominant, economically the dominant, financially the dominant, technologically the dominant, we need to dominate. And that is the foreign policy that we've had since 1992. So it's 32 years running.”

“Bitcoin is the painting in the attic.”

Very succinct. The reason I’m not a billionaire today is because I thought the government would crush it. So far, they have not (I have my own crackpot theories on that.)

Consider a paid subscription to continue reading further. I hope that people find the posts useful, interesting, and entertaining.

I don’t spend a lot of time trying to give some sort of stock market analysis or deep dive into some jobs report or unemployment data - other people do that far better, and I think a lot of “the data” is severely and often intentionally distorted.

I just like to present things I find interesting that may also provide some amusement or perhaps insight into our unknown future.

“We always have to remember one thing about Europe: We are in a state of constant crisis, all the time, and yet nothing ever changes.”

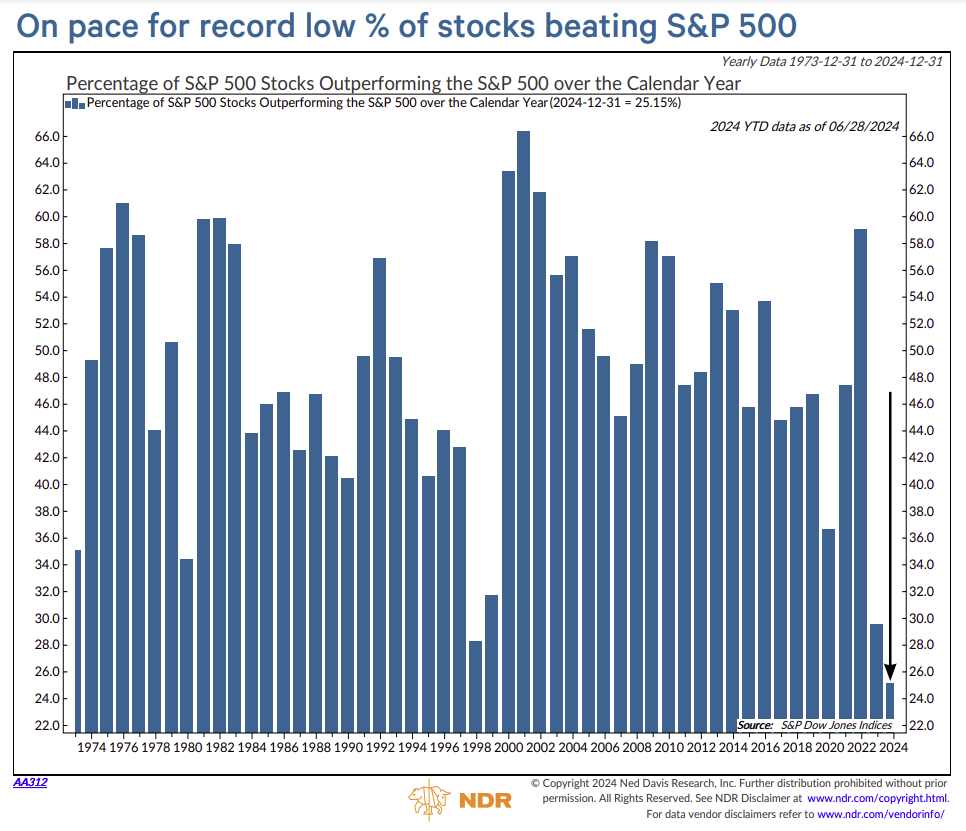

Looks like markets are slightly extended. From the Vampire Squid:

Late 1990’s is the comparison here:

Meanwhile, every day seems to look like this:

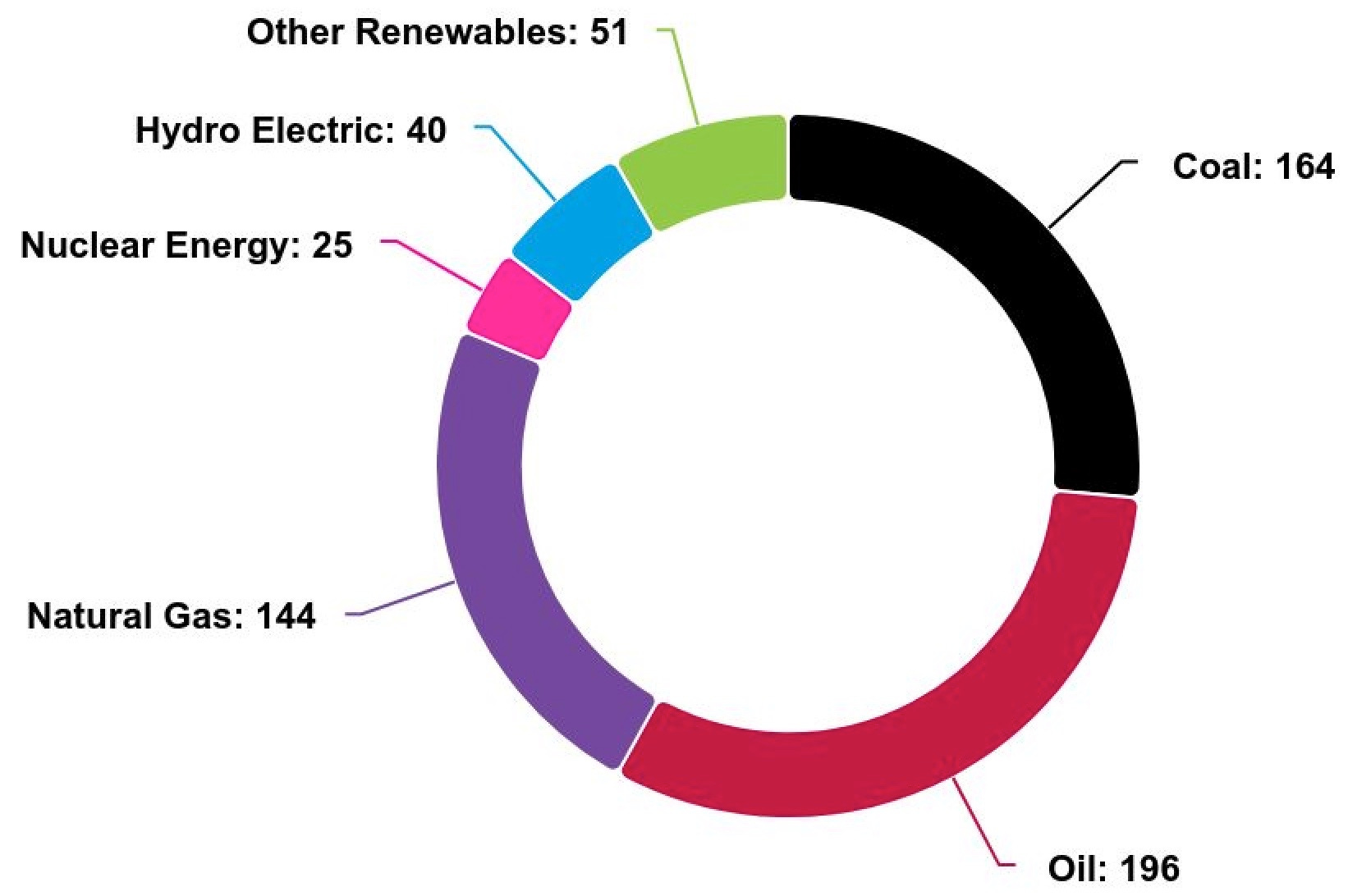

Robert Bryce on Energy

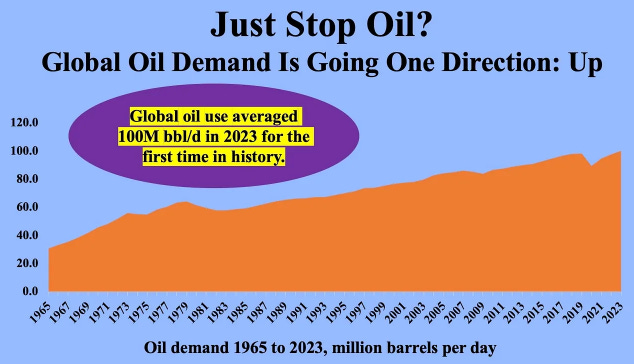

“Global hydrocarbon use and CO2 emissions hit record highs in 2023, with hydrocarbon consumption up 1.5% to 504 exajoules (EJ). That increase was “driven by coal, up 1.6%, [and] oil up 2% to above 100 million barrels [per day] for the first time.” Global natural gas demand was flat, mainly due to stunning declines in Europe.”

”The U.S. again led the world in emissions reductions in 2023, but as shown in the previous two slides, those reductions are being swamped by the growth in India and China.”

Coal

A brief aside…

“Anybody who can go down 3,000 feet in a mine can sure as hell learn to program as well…Anybody who can throw coal into a furnace can learn how to program, for God’s sake!” - Joe Biden to coal miners, 2019

“The Inflation Reduction Act provides tens of billions of dollars in subsidies for wind and solar in the U.S. However, as seen below, gas-fired generation is still growing faster than those two sources combined. Note that in 2023, wind generation fell despite the addition of 6 gigawatts of capacity. Why? The wind didn’t blow.”

46% of U.S. Electric Vehicle drivers “likely to switch back to ICE” (Internal Combustion Engines)

CRE

Office vacancies set a new all-time high, ‘breaking the 20% barrier for the first time in history’

In the second quarter of this year, “the office sector set a record vacancy rate at 20.1%, breaking the 20% barrier for the first time in history,” a Moody’s analysis published today read. “The slow bleed occurring in the office sector has led to a steady rise in the vacancy rate as permanent shifts in working behavior have outlasted the initial wave of the pandemic four years ago.”

In the prior quarter, as Fortune previously reported, the office vacancy rate had already reached 19.8%, which was 50 basis points above recessionary peaks recorded in 1986 and 1991, according to Moody’s.

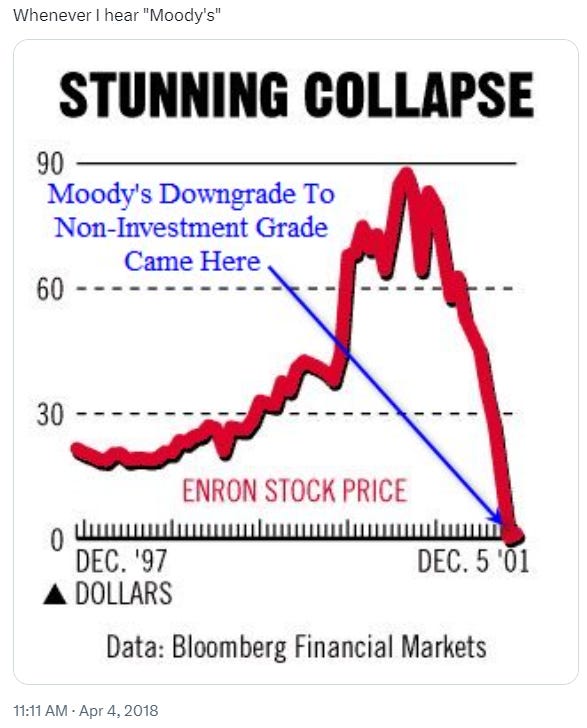

As an aside, Moody’s always cracks me up…

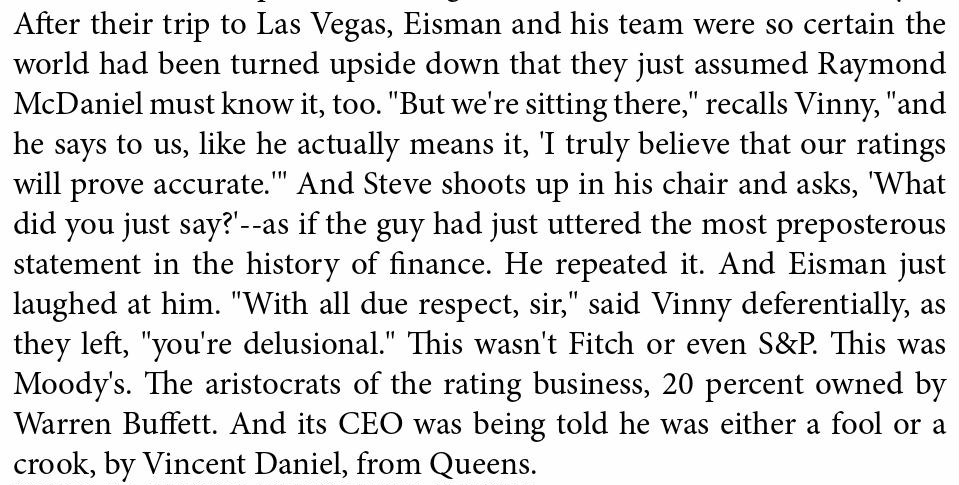

And this, from The Big Short:

Raymond W. McDaniel Jr. is still CEO of Moody’s.

Apartments

“What's happening in the apartment sector today…is due to the increased amount of supply, a lot of folks, when they were underwriting these assets, they thought they would see three, four, five percent annual rent growth. Well, because of new supply, rents are actually going down in a lot of these Sunbelt markets, so they overpaid for the assets because debt was pretty cheap. Now they have rents declining, and then they also have inflation in their operating expenses, so insurance is going up, property taxes are increasing…”

Shash Aryal, Peak Vortex Capital

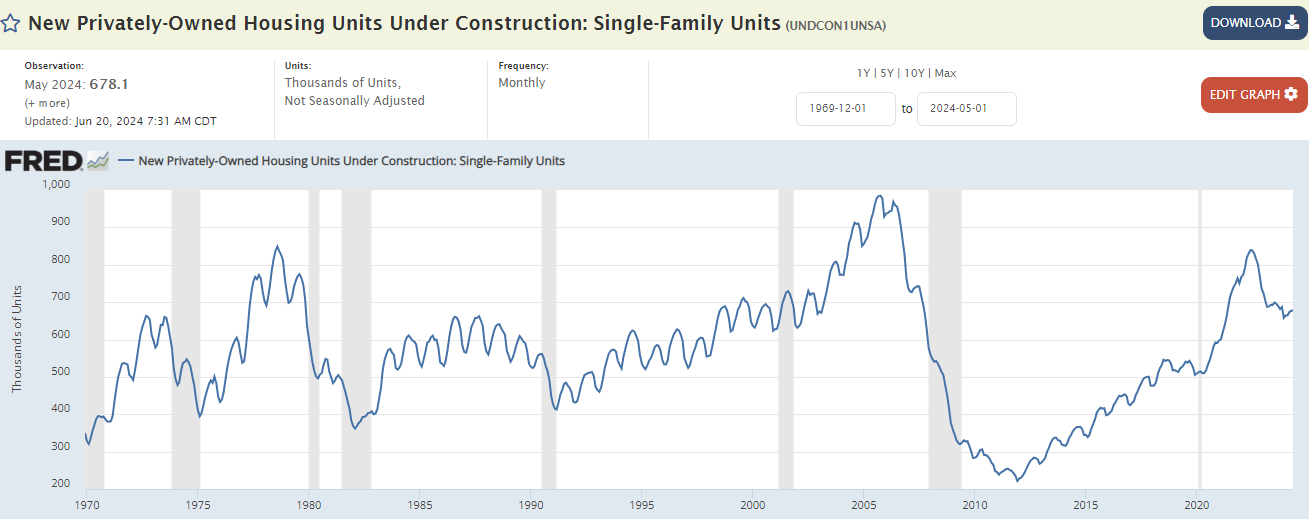

The consensus lately is that in a few years - due to a drop off in multifamily construction now - rents will rise again, but if you look at this FRED chart, we’ve had an epic amount of apartment construction going on.

Also, nobody seems to be building duplexes or triplexes any more, although there’s been a flurry of “ADU” type discussions…

Here’s single-family construction:

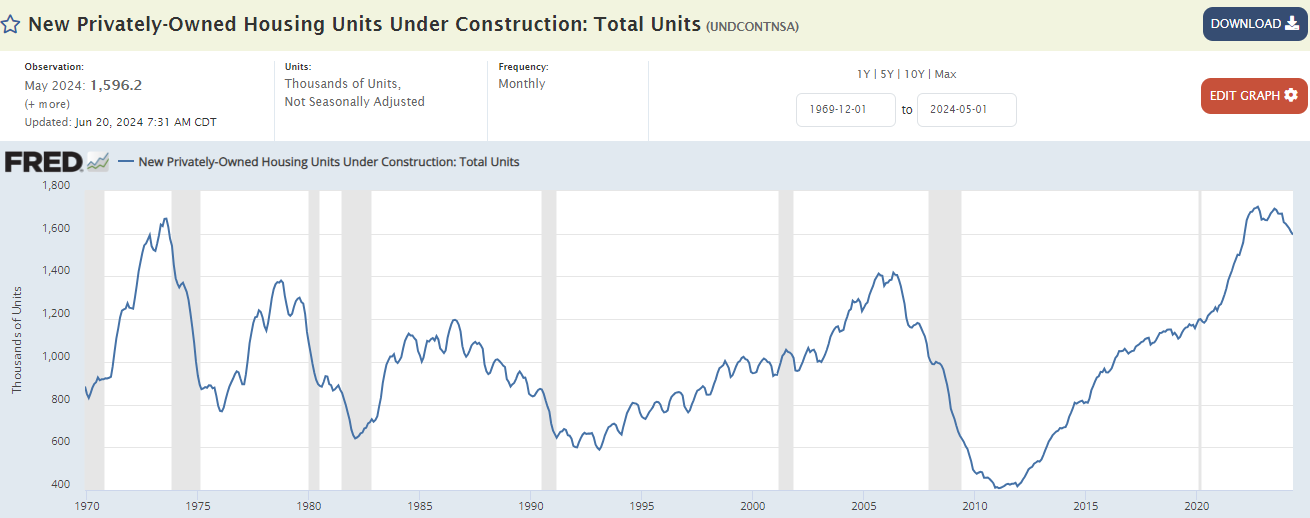

Here’s TOTAL housing units under construction:

Housing shortage? I think it’s more like affordable housing shortage.

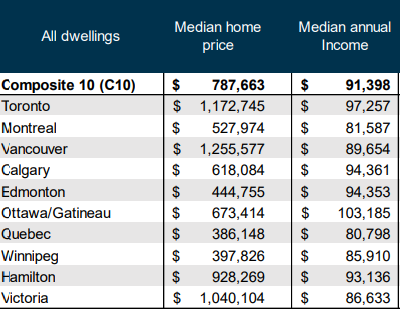

Here’s some dated (2022) data on Median Sales Price/Median Household Income:

Prices are too high relative to incomes in most places. (Gee, how did that happen?)

“Lennar, one of the largest homebuilders in the US, filed its 10-Q for its second quarter with the SEC last Friday. And it disclosed what these incentives cost:

In the first half of 2024, the average incentive costs, including the costs of mortgage-rate buydowns, rose to $47,100 per house sold, or to 10.1% of the average sales price, up from 9.2% a year ago.

The costs of those incentives vary by market. In Texas, they reached 16.9% or $51,600 per house. In “Other” regions, which include Florida, they amounted to 13.4%, or $81,700 per house.”

Important:

“These costs are not reflected in contract prices.

“The Census Bureau, when it reports on new residential sales, relies on contract prices — the amount in the purchase agreement with the buyer — to come up with its median prices, and those contract prices don’t reflect the costs of mortgage-rate buydowns and incentives.”

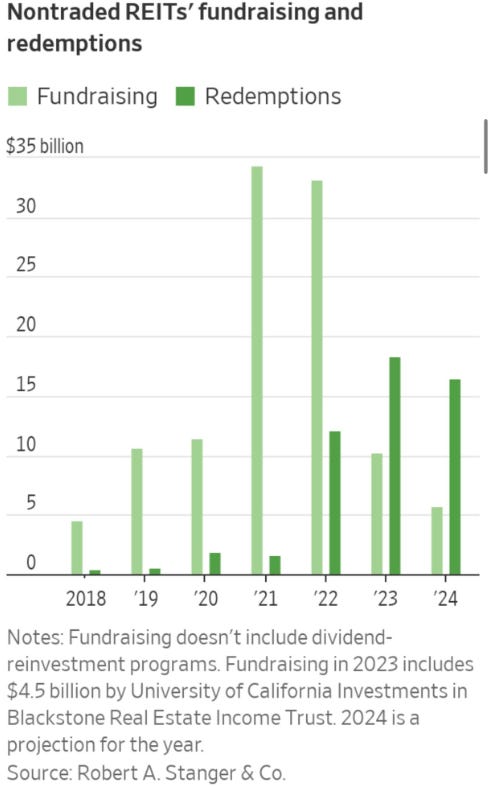

A Real-Estate Fund Industry Is Bleeding Billions After Starwood Capped Withdrawals

“Starwood Capital Group’s move to severely tighten restrictions on investor withdrawals from its $10 billion real-estate fund is rippling through the $90 billion private real-estate fund business.

After the giant investment firm announced the new restrictions in May, sponsors of similar funds said they experienced a jump in redemption requests. Investors in these funds, mostly individuals who paid as little as $2,500, appear worried that their funds might also tighten the withdrawal spigot, forcing them to wait indefinitely in line if they want to cash out.”

"If it's such a great trade, why are you offering it to me?"

a line from 𝘛𝘩𝘦 𝘉𝘪𝘨 𝘚𝘩𝘰𝘳𝘵

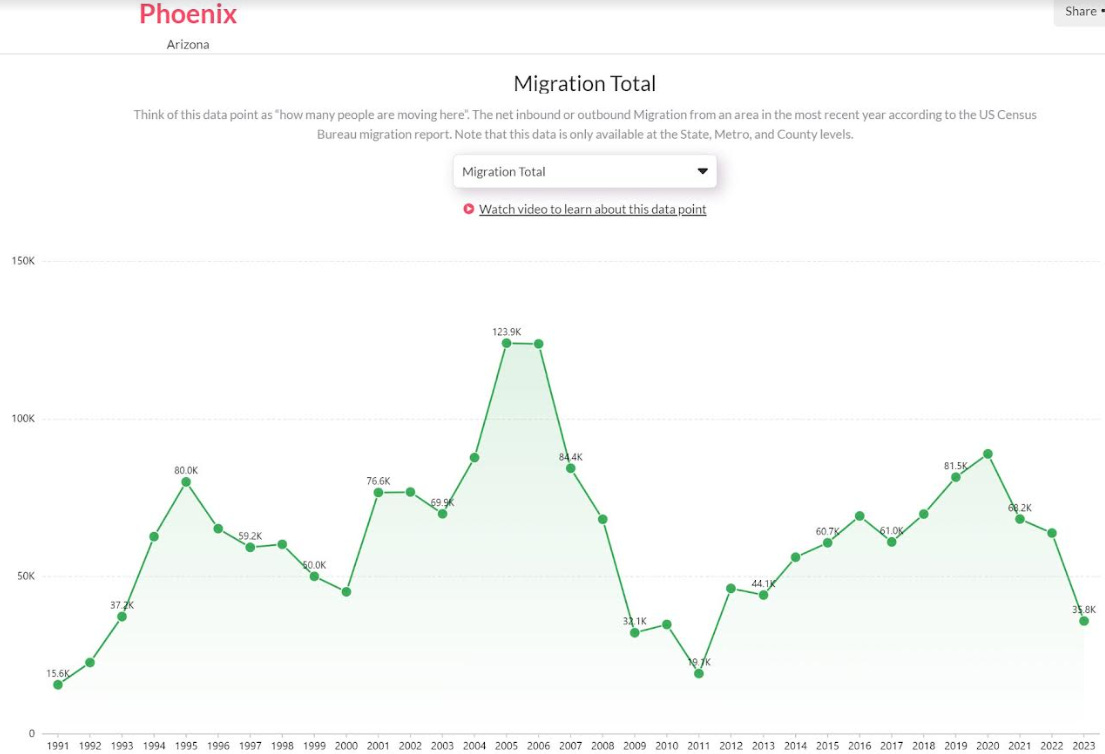

Phoenix

Nick Gerli

“There's this perception out there that once home prices start dropping, all the buyers are going to flood back in, but that's actually not what's happening. In a city like Austin, home prices are down almost 20% over the last two years, there's been no bounce-back in buyer demand, and inventories are continuing to increase. Prices now in Florida are really starting to go down in many markets. Buyer demand is not going up. In Boise, prices went down by quite a bi,t buyer demand really didn't go up.

Another thing to understand is that when when it becomes obvious in a housing cycle that we’re in the down cycle, buyers all of a sudden realize that they have time on their side, and all of a sudden there's this this FOMO or this competition that's gone, and rather it's kind of like, let's see how far the the values could drop. It's a bit of a long-winded answer, but I would be very skeptical of thinking that a couple rate cuts is all of a sudden going to propel the housing market forward, when we're already seeing this big spike in inventory occur in about half the states in the U.S.”

Inventory

“When you think about a housing shortage, this most certainly does not apply to Arizona. Inventory here is skyrocketing. The same goes for Florida. Inventory is up 70% year over-year, and you can see in many of these states like Texas, for instance, the number of homes for sale is now at the highest level it has been in the last seven years”

Gerli on Investor Single-Family Home Selling

Trivia: FirstKey Homes is owned by private-equity locust Cerberus.

A Bifurcated Market (there’s that term again)

“I want to show you what's going on in Houston, because it really confirms this point you're trying to make. We're looking at a a data point called the inventory surplus or deficit - how much inventory is higher or lower than the long-term average, and what you can see in these ZIP codes in red is inventory is like double the long-term average already. Let me just show you here in 77026. Before the pandemic we had 36 homes on the market for sale. Now we have 110. This is an investor concentrated zip code in Houston where there's a massive selloff occurring right now, and what you can see is that there's a big concentration, in this case to the north and to the east. Meanwhile, take a look at this bifurcated housing market and some of the wealthier areas to the west of Houston, you can see inventory still in a shortage, down 40% from normal, down 20% from normal, down 45% from normal. So this is a perfect picture of the housing market we are facing right now. If someone's a buyer on the west side of Houston, they are still experiencing bidding wars, they are still experiencing a rising price environment. If someone's a buyer in these areas in red on the north side of Houston all the way kind of up to the northern suburbs, it is not that way at all. It is a housing downturn. Prices are going down, and inventory is skyrocketed.”

We didn’t always treat our homes as lottery tickets.

“Someone commented on my YouTube Channel, I thought it was super smart: he said, if I'm living in a house for 30 to 40 years, and I don't plan on selling it, I actually don't want to see the value go up, because if the value goes up I know my taxes and insurance are going to go up...I thought that was super interesting. It's a very counterintuitive point, because I think most people want to see the value of their house go up, but from a pure dollars and cents cash-flow and expense angle, rapid appreciation like we saw in the Sun Belt during the pandemic actually has high costs and consequences to homeowners in the long run.”

Melody Wright

Melody Wright with Rosanna Prestia. (I know I keep quoting her but she seems to have the most interesting things to say!) Here she is talking about FHA loans:

“I'm personally of the opinion that we have been in a silent depression - which is an Emil Kalinowski term from 2007 - that something broke. All of our trendlines broke. We have all these missing people from the workforce. We have all these missing men from the workforce, and people may say maybe they're taking care of kids - that's not what the data has borne out. The problem is is that we are just not producing like we used to produce, and I think that a lot of that has to do with companies are no longer interested in investing in productivity, investing in research and development - they're only interested in buybacks and making sure that their stock price looks good. Anybody who's been in Corporate America can tell you that by just telling you their story, so I think that's a lot of it.

It has been very important in mainstream media to pretend that things got better, and that all this policy worked. All that quantitative easing worked - all that these shenanigans, you know, ZIRP - but in reality, sure, we had more service jobs, you could go get a job at Chick-fil-A, but you could not get a job or career that was going to sustain the American dream, and I think that this has been going on way longer than most folks want to admit or recognize, because it's been more politically palatable to say jobs are great, booming, but when you have to have multiple jobs, that's not the American dream I think most of use grew up wanting to obtain.”

“You can go to the south of San Antonio all the way very far north to Austin, and all around this huge perimeter, and it's just one big new build site. I don't care if most of Mexico moves there, that's how much is being built out there, and it is insanity, and if you haven't seen it, it's hard to explain.”

“Something I used to talk a lot about right after my first trips was called salting the lots, and what they do is they try to make it look like everything's sold. So all the construction cars will park in the driveways, they'll pull the garbage cans down to the front, you might even see wreaths on doors, but if you go at night, you know nobody's living there, so I saw this all the time”

Melody does not buy the low-inventory mantra

“I do believe we are we are turning a corner, where fundamentals are starting to be in control, and not just FOMO, and I feel like enough people have kind of realized - they're not falling for these tricks anymore, they're not paying these ridiculous prices - but the Wall Street Journal, and their article about hitting that [price] record - and it is a record, I mean this is the highest we've seen home prices - all they talked about was the shortage of inventory. Again, I really believe that this has been one big snow job, based on what I have seen out there. They're going to continue with that narrative until the very end, until there is absolutely no way that they can deny it.

Stay focused, stay tuned, because we are seeing fundamental shifts in that inventory, and and people can say, oh, not back to 2019 levels - you go into these cities, many of them are already way blowing past 2019 - but, again, if pocket listings and private note sales are as big as I think they are, then that's why inventory looks down.”

Oh Canada!

Greg Weldon on Retail Sales

“The only other times we've seen real retail sales in negative territory was in the tech bubble crash, the global financial crisis, and the pandemic. That's it. And now.”

“The fact of the matter is people feel much worse off, and it's because of inflation, and because income is barely keeping up, savings are gone. Credit cards are maxed out, and delinquency rates are skyrocketing like we haven't seen since 2007.”

China is no longer the cheapest option.

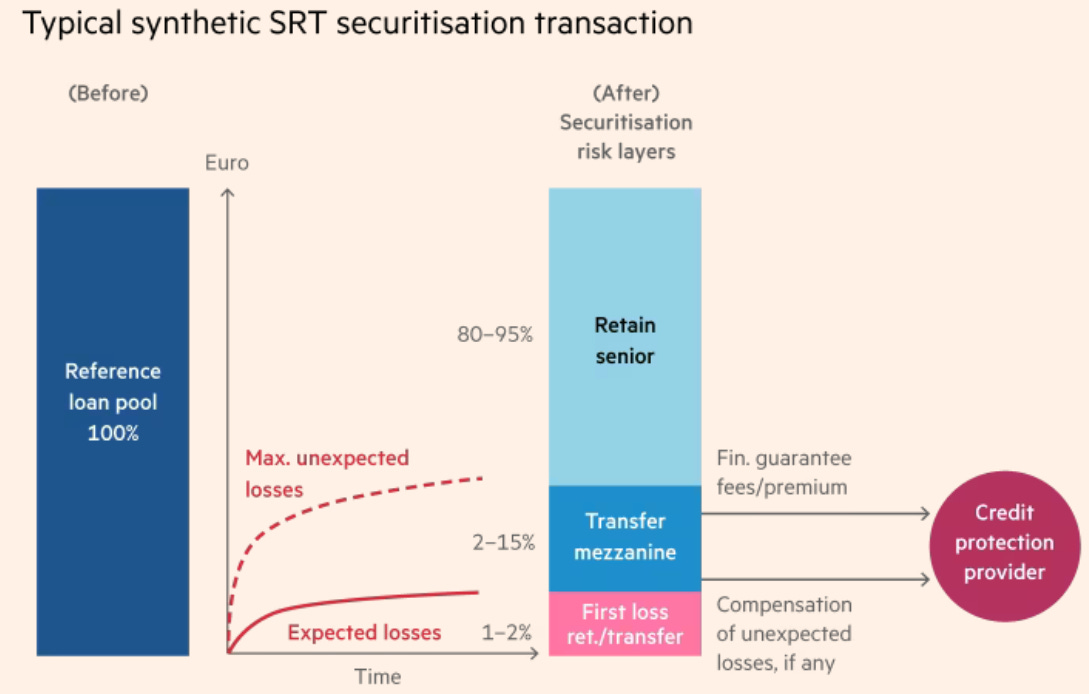

AIG 2.0?: Blackstone snaps up ‘circular’ private equity credit risk

This sort of complexity is over my head - Mike Green territory - but I hear bells ringing.

Blackstone Group has become one of the biggest buyers of a type of bank loan that has become a lifeline for the private-equity industry, exposing the company to risks generated by its own business.

The world’s largest buyout group, which manages more than $1tn in assets, has in the past year emerged as a big investor in risk transfer products that are underpinned by short-term loans used by private equity fund managers to close deals as they wait to receive cash from their backers.

Because of its sheer size, Blackstone has assumed risk on credit lines attached to its own buyout funds, though the firm said they only constitute “a single-digit percentage” of the portfolios on which it has exposure.

Such transactions magnify the private equity behemoth’s exposure if an investor were unable or unwilling to fund their commitment.

“The unusual thing about Blackstone is that it is a bit circular,” said one large SRT investor. “They are providing protection on themselves.”

We know that the Fed will save entities like Blackstone when they screw up.

e.g., Chris Leonard on September 2019: “the Fed stepped in, almost instantaneously, and initiated a $400 billion bailout. This bailout was unprecedented, and it benefitted a small group of hedge funds that had essentially hijacked the repo market and used it as a vehicle to make risky bets. The Fed saved them from the consequences of those bets.”

“Blackstone disputed the circular nature of the risk, saying its investors were “the ultimate risk counterparty the lender is exposed to”. It noted that its investors had never missed a capital call in its 40-year existence.”

Never missed a capital call…so far!

From the comments:

“A complex area of risks, hard to cover in full in an article like this. The SRT diagram is what one needs to look at, and recall the mindset of Steve Eisman in The Big Short: are the underlying loans/risks sufficiently independent/unconnected/uncorrelated? Maybe - if so, the “reinsurance tower” structure is valid. However, if they are not a diversified collection of risks like a large North American insurer’s property book, then this structure has potential contagious catastrophe risk. Like the US prime lending ABS exposures. What are the components of the underlying pools and how interconnected are they?”

Another comment was from someone who thought this was much ado about nothing and was very indignant:

“I recommend the FT journalists to start reading RTRA intelligence and Structured Credit Investor to avoid future embarrassment.”

“With correct discipline low levels (debt vs uncalled investor capital) and with good quality investors (pension funds not private individuals) default risk is low (it’s as much a liquidity tool as operating leverage for the PE Fund) but it is all quite opaque and this kind of financial alchemy is both difficult to track and historically ends up being abused.

I think that’s the gist of it but am no expert.”

"Isn't it interesting that he was a nuclear war strategist but was not a doomer?"

CBS, talking about Herman Kahn

"On the one hand, the doomsters say that there are too many of us; on the other hand, they warn that we are in danger of most of us being wiped out."

Melody Wright’s comment about homebuilders “salting the lots” for some reason reminded me of the Stephen King short story, “Jerusalem’s Lot,” which later became the novel, “‘Salem’s Lot.”

This poem was the prologue to the book:

Old friend, what are you looking for?

After those many years abroad you come

With images you tended

Under foreign skies

Far away from your own land.GEORGE SEFERIS

A 1979 TV miniseries was made, and I still consider it to be the scariest made-for-TV movie ever. Of course everyone knows vampires don’t exist, but what if they did? Check it out if you’re a slow-burn horror fan (I hate slasher flicks and the like).

Great post as usual. Thank you so much. Hopefully your readers don't think I'm "overdone". Did a new series you might like and first interview is with Marley Price, a citizen activist who is reporting illegal STRs. By the end of the week I'm figuring out the podcast thing for that and DNN :)

"Raymond W. McDaniel Jr. is still CEO of Moody’s." You really should pin this to your X profile, says everything we need to know about crony-world.