Since I’ve seen infamous Strigoi Henry Kissinger mentioned lately (e.g., he’s currently at the Bilderberg Conference, for the 400th straight year), here is the definitive description of Henry Kissinger, from Christopher Hitchens:

“He’s a thug and a crook and a liar and a pseudo-intellectual and a murderer. OK? All of those things are factually verifiable. That he is an anti-communist is a speculation that he likes to encourage.”

Too harsh perhaps. What say you, Anthony Bourdain?

"Once you’ve been to Cambodia, you’ll never stop wanting to beat Henry Kissinger to death with your bare hands. You will never again be able to open a newspaper and read about that treacherous, prevaricating, murderous scumbag sitting down for a nice chat with Charlie Rose or attending some black-tie affair for a new glossy magazine without choking. Witness what Henry did in Cambodia – the fruits of his genius for statesmanship – and you will never understand why he’s not sitting in the dock at The Hague next to Milošević. While Henry continues to nibble nori rolls and remaki at A-list parties, Cambodia, the neutral nation he secretly and illegally bombed, invaded, undermined, and then threw to the dogs, is still trying to raise itself up on its one remaining leg.”

- Anthony Bourdain, 𝘈 𝘊𝘰𝘰𝘬'𝘴 𝘛𝘰𝘶𝘳: 𝘐𝘯 𝘚𝘦𝘢𝘳𝘤𝘩 𝘰𝘧 𝘵𝘩𝘦 𝘗𝘦𝘳𝘧𝘦𝘤𝘵 𝘔𝘦𝘢𝘭

The long con: Henry Kissinger, Klaus Schwab, and UK Prime Minister Heath at the WEF, 1980.

Nothing I had seen during my decade of legal work had prepared me for what I witnessed in just a few short months at the New York Fed. In those months I discovered a disorienting world full of hidden clues, where people said one thing but meant another.

Beneath the public face of the Fed laid a web of incompetence, corruption, rampant mismanagement, secrets, and lies. In the “fake work” culture of the Fed, where supervision was a job title, not a job, the most important thing was to control the process to serve the ultimate master. The New York Fed was not simply failing to stop the banks; it was actually enabling their bad behavior.

Carmen Segarra, Noncompliant

Remember when every single FOMC member was complaining that inflation (i.e., your cost of living) was too LOW, and that they actually wanted higher inflation?

I remember.

Credit-card balances hit $986 billion in the fourth quarter last year and remained largely unchanged in the first quarter of this year, the Federal Reserve Bank of New York said in its most recent quarterly report on household debt. It looks increasingly likely that credit-card debt is on track to hit the $1 trillion mark this year, and experts say that this number could be an indicator of a looming economic downturn.

This has raised eyebrows among some observers, because people typically pay off their debts from the holiday season in the first quarter of the year. That did not happen this year. This was the first time credit-card debt did not make its customary dip between the fourth and first quarters since the end of 2000 and the beginning of 2001, New York Fed researchers said. That was a recession marked by the end of the dotcom bubble.

Read the comments here. I doubt anyone at the Fed ever hears about normal life like this. They’re too busy angling for jobs at Goldman:

The average credit card rate (according to the Fed) is over 20%

There was never any “ZIRP” for the people commenting above.

So the guy I’m talking about in this archived thread is cheerfully talking about his stocks again…fair warning.

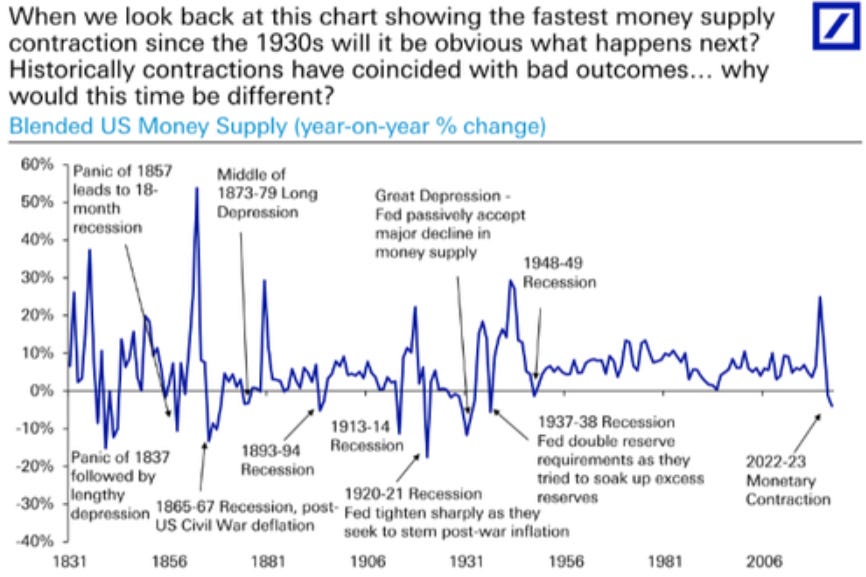

This is floating around again from Deutsche Bank - this time going back to 1831. Yes, year on year % drops in money supply are rare (especially since we switched to a completely unanchored currency):

I still think that comparing today with, say, the 1930’s is a bit of a stretch:

As Jeremy Grantham and too few others point out - these asset bubbles central banks create are very dangerous, especially when they pop.

Ten years ago the 10-year Breakeven Inflation rate - “what market participants expect inflation to be in the next 10 years, on average” - was 1.57%. Since that time, I calculated that over the next 10 years the CPI rose an average of 3.58% a year (I think my calculation is close enough for government work - and remember, this is the understated CPI.

3.58% vs. 1.57% is a fairly huge difference, and also why I smile whenever these “breakeven” rates are mentioned.

”The RecessionAlert weekly leading economic index (WLEI) is a composite for the U.S economy that draws from over 20 time-series and groups them into the following six broad categories which are then used to construct an equally weighted average.”

Really interesting discussion between Adam Taggart and Lucky Lopez on the auto market

Prime customer is I believe, now at 4.9% hovering almost a 5%, which is double that the 2021 and 2022. So it’s starting to get up there. The one thing that’s that I’ve seen, it’s really scaring me is I’ve talked to a number of banks, and a lot of their - how do I say it - a lot of their management is starting to figure out ways to work out some sort of programs, like a forbearance.

Now, a lot of these people we talked about bought these cars, and literally didn’t make a payment for a whole year - they called in, claim the whole pandemic thing. Well, now they’re starting to make these payments, and the banks are noticing that people simply can’t afford them…one thing that that they started talking about is they’re actually working out programs where they could put payments from the front of the loan to the back. So this way, they could give people a fresh start, so they don’t have negative credit. They could just start back over.

And so instead of repossessing a car, which traditionally most banks they just want to get their collateral and get it out of the customer’s hands and sell it. They’re taking such big losses at the auction that they decided to make up these new programs where they would add on months to the end of these auto loans and give customers a break or breathing room to get back on track. Now, this is the first time I’ve ever seen this done by any bank, like they’re, that’s how scared they are, is they’re so afraid that if they don’t do this, they’re gonna have record high defaults.

And if they do, the banks that give them the money, like Wells Fargo, Bank of America, or some of these other hedge funds are not going to continue to give them money because their their books are going to be so in shambles, because what their portfolio is worth to what it’s actually truly worth is going to be, you know, a significant number apart.

And as I talk to these banks, they’re really, really scared. One local bank here in Nevada, they literally just hired 400 collection agents, and they’re running out one of these companies that just went out of business, this telemarketing company and literally, they’re just going to fill a full of collection agents, they know that the worst is coming. We’ve only seen the tip of the spear, they think it’s just going to go all the way downhill. They’ve already started collecting several investors to have money on the side. So they can keep lending just in case if like Wells Fargo or Bank of America pull their lines. It’s it’s pretty significant. Like I said, the credit crunch is finally here.

…we’re starting to see customers actually starting to walk away from their cars. This is something I haven’t really, I talked a little bit about in our last thing. Remember in the 2008 recession, people sort of walk away from their houses because what are you thinking? Yeah, and so I’ve actually heard, and I’m not even joking about this, when we were at an automotive conference here in Vegas people are talking about doing short sales with cars. It blew my mind I never thought in a million years I would hear people talk about this.

Extend and pretend.

…customers of SVB’s Cayman Islands branch, [were] left out of the First Citizens deal and placed under FDIC receivership. The branch in the offshore tax haven was set up to primarily support the bank’s activities in Asia, according to SVB. Its depositors, which include multiple Chinese investment firms, haven’t been able to access their funds—and have been in limbo since SVB’s collapse.

On March 31, the FDIC notified SVB’s Cayman Islands depositors that they wouldn’t be covered by its deposit insurance, and that they would be treated as “general unsecured creditors,” according to documents reviewed by the Journal as well as interviews with employees of multiple firms.

Good. They should not be taxpayer-backed.

Wall Street on Parade provides more color:

As Wall Street On Parade has previously reported, under statute, the FDIC cannot insure deposits held on foreign soil by U.S. banks. What it can do, however, is to sell those deposits to the bank that acquires the collapsed bank. In the case of Silicon Valley Bank, the acquiring bank was First Citizens Bancshares which, apparently, declined to purchase the foreign deposits in the secrecy jurisdiction of the Cayman Islands, a jurisdiction most notable recently for housing Sam Bankman-Fried’s crypto house of frauds.

The Journal reported that as of December 31, 2022, Silicon Valley Bank held $13.9 billion in foreign deposits…What the Wall Street Journal has actually done with this report is to open a Pandora’s box regarding the vast sums of foreign deposits held in foreign branches of JPMorgan Chase and Citigroup’s Citibank – none of which are covered by FDIC insurance. It further raises the question as to why the banking regulators of these two Wall Street mega banks have allowed this dangerous situation to occur…

JPMorgan Chase and Citibank also have exposure to uninsured domestic deposits – that is, deposits exceeding $250,000 per depositor in their bank branches on U.S. soil. At year end, JPMorgan Chase held $1.058 trillion in uninsured deposits in domestic branches while Citibank held $598.2 billion in uninsured deposits in domestic branches. Combining domestic and foreign uninsured deposits versus the $1.4 trillion Citibank held in total deposits at year end, means that 87 percent of Citibank’s deposit base lacked FDIC insurance protection.

Meh.

(The problem I have with ‘adjusted for inflation’ numbers is that they magically assume that your income has kept up even with the official CPI. It’s levels that people have to live on, more than rate of change. Even if the median household income nationally is around $75k, $339k for a house is still 4.5x that.)

Hang on - $1.25 million for this on the outskirts of Orlando? I guess it’s a big house, and Disney may factor into it, but come on. Again, read the comments (not the political ones though.)

If you - after everything - decided to still invest in WeWork, next time just send me your money and I will set it on fire in front of the charity of your choice.

I’m basically a market historian. I chronicle mass insanity.

Nicholas Glinsman on Banks, Commercial Real Estate, and China Harald Malmgren’s partner. Particularly sobering on China, and Glinsman’s description of China’s Xi as a “Stalinist.”

In other news…I get most of my news nowadays from Weibo.

Chinese comedian arrested after joke about army What is China becoming, the UK??!!

Imagine being so insecure that jokes make you want to cancel someone!

Durham Report Reveals the Real Threat to “Democracy” – The FBI Weaponized by Democrat Party Affiliated Elites Note that this is from a “Black Left” website. Left, right and middle should always strive to find common ground.

Stalin: "Let's wrap this up, they ain't gonna kill themselves. "

Those forbearance solutions and payment deferrals are how we hid the fact that a great deal of equity has just been withdrawn from millions of mortgage borrowers. I’m trying to find out how that 2nd lien is currently being reported to the Fed. I have a feeling we may not be looking at a true picture of mortgage credit. To do that with cars is just ummmmm - bad. We are in for one hell of a headache.