Subprime America

People live on price levels, not on rate of change.

A favorite quote:

“It is difficult to get a man to understand something,

when his salary depends upon his not understanding it!”

Upton Sinclair, I, Candidate for Governor: And How I Got Licked, 1934

Was the stock market open today?

I didn’t pay much attention. I browsed Substack’s notes a bit when I could. A number of people in Notes seem terrified they might at any moment be exposed to mean tweets/notes/posts, and are demanding “content moderation.” It feels like middle-schoolers demanding tougher hall monitors.

I haven’t really seen any dangerously mean tweets/notes/posts myself yet (what’s the exact definition again?) but I know they’re out there, coming to get me/us/he/she.

I see pleas about the need to “identify harassment vectors and toxic communities and proactively shut them down,” which sounds like something taken from a Pol Pot poster.

My point has always been that - other than actual threats or incitements to violence - block and mute work fine. Others strongly disagree, as is their right.

I’m used to being out of the mainstream, but how can you ever hope to change minds if you just hang out with people who think exactly like you?

I used to be sort of a neo-Con. Now I’m about as anti-war as they come. That only happened because over time I read, and talked to, people who disagreed with me (and I started paying attention.)

Now it seems that if you are the least bit nuclear war-hesitant, or suggest something beyond the pale, like, say, the U.S. shouldn’t be in Syria, or Ukraine, you’re suddenly a traitor(!) to many. People have lost their minds.

Wake me when Dick Cheney and Bill Kristol get deplatformed.

The Substack angst is sad to see, especially from those who I’m sure self-identify as free-thinking creative “writers.” I just wish everyone wasn’t so insecure.

I have a (semantic) bone to pick with Wall Street Journal headline writers…

While the official CPI rate of change may be at lowest level since May 2021, consumer prices will never return to May 2021 levels.

TSS Episode 137: Ken Shinoda on Mortgage Investing and the Housing Market

Subprime really picked up steam starting in the early 2000’s, then it exploded into the kind of mid-2000’s going into the GFC, largely because of collateralized debt obligation (CDO) market. Since the GFC…there really is no more subprime in the non-agency market. There are subprime loans being made - they’re being made by the government, through the GNMA programs, so the largest subprime originator in America is now the government, backstopped by our taxpayer dollars.

Michael Belkin on 2Q Outlook for Markets

They [the Fed] are the bank regulators, and they gave these banks glowing pass ratings on their stress tests, they didn’t test them for higher interest rates. This is a crackup. I mean these guys need to be held personally responsible, Powell and Yellen.

The Commercial Real Estate Default Cycle Has Only Just Begun | Dan McNamara

Now, when you can buy T-bills at almost 5%, a little lower now - paying 5% to get insurance exposure to a house that’s already on fire - to me seems like a gift.

White Paper: Inflation Will More Than Double “Seriously Delinquent” Mortgages in 2023

We seem to be at Q3 2006 delinquency levels currently:

So there’s this: Fed Balance Sheet Shrinks For 3rd Straight Week.

Why not:

Fed Balance Sheet Still $4.855 Trillion Higher Than August 2019

or

Fed Balance Sheet Still $7.71 Trillion Higher Than September 2008

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel committee must’ve overlooked this exchange.

Regardless, QT marches inexorably on.

In the above podcast, Ken Shinoda mentions CDO’s, which reminded me of a key passage from The Big Short:

That's when Steve Eisman finally understood the madness of the machine. He and Vinny and Danny had been making these side bets with Goldman Sachs and Deutsche Bank on the fate of the triple-B tranche of subprime mortgage-backed bonds without fully understanding why those firms were so eager to accept them. Now he was face-to-face with the actual human being on the other side of his credit default swaps. Now he got it: The credit default swaps, filtered through the CDOs, were being used to replicate bonds backed by actual home loans. There weren't enough Americans with shitty credit taking out loans to satisfy investors' appetite for the end product. Wall Street needed his bets in order to synthesize more of them. "They weren't satisfied getting lots of unqualified borrowers to borrow money to buy a house they couldn't afford," said Eisman. "They were creating them out of whole cloth. One hundred times over! That's why the losses in the financial system are so much greater than just the subprime loans. That's when I realized they needed us to keep the machine running. I was like, This is allowed?"

There was also a Meb Faber podcast with Bill Martin that prompted this:

If some of the most sophisticated, tech-savvy and wealthy investors in the world took apparently zero interest in their counterparty risk at Silicon Valley Bank, it makes me wonder if that sort of reckless disregard for counterparty risk is widespread elsewhere.

It’s a strange world in which two parties can carry out a paper transaction that each can promptly report as profitable.

In the 2005 Berkshire Hathaway annual report, Warren Buffett describes at length the perils of unwinding a derivatives position at Gen Re. I think it remains timely.

Long ago, Mark Twain said: “A man who tries to carry a cat home by its tail will learn a lesson that can be learned in no other way.” If Twain were around now, he might try winding up a derivatives business. After a few days, he would opt for cats.

We lost $104 million pre-tax last year in our continuing attempt to exit Gen Re’s derivative operation. Our aggregate losses since we began this endeavor total $404 million.

Originally we had 23,218 contracts outstanding. By the start of 2005 we were down to 2,890. You might expect that our losses would have been stemmed by this point, but the blood has kept flowing. Reducing our inventory to 741 contracts last year cost us the $104 million mentioned above.

Remember that the rationale for establishing this unit in 1990 was Gen Re’s wish to meet the needs of insurance clients. Yet one of the contracts we liquidated in 2005 had a term of 100 years! It’s difficult to imagine what “need” such a contract could fulfill except, perhaps, the need of a compensation conscious trader to have a long-dated contract on his books. Long contracts, or alternatively those with multiple variables, are the most difficult to mark to market (the standard procedure used in accounting for derivatives) and provide the most opportunity for “imagination” when traders are estimating their value. Small wonder that traders promote them.

A business in which huge amounts of compensation flow from assumed numbers is obviously fraught with danger. When two traders execute a transaction that has several, sometimes esoteric, variables and a far-off settlement date, their respective firms must subsequently value these contracts whenever they calculate their earnings. A given contract may be valued at one price by Firm A and at another by Firm B. You can bet that the valuation differences – and I’m personally familiar with several that were huge – tend to be tilted in a direction favoring higher earnings at each firm. It’s a strange world in which two parties can carry out a paper transaction that each can promptly report as profitable.

I dwell on our experience in derivatives each year for two reasons. One is personal and unpleasant. The hard fact is that I have cost you a lot of money by not moving immediately to close down Gen Re’s trading operation. Both Charlie and I knew at the time of the Gen Re purchase that it was a problem and told its management that we wanted to exit the business. It was my responsibility to make sure that happened. Rather than address the situation head on, however, I wasted several years while we attempted to sell the operation. That was a doomed endeavor because no realistic solution could have extricated us from the maze of liabilities that was going to exist for decades. Our obligations were particularly worrisome because their potential to explode could not be measured. Moreover, if severe trouble occurred, we knew it was likely to correlate with problems elsewhere in financial markets.

So I failed in my attempt to exit painlessly, and in the meantime more trades were put on the books. Fault me for dithering. (Charlie calls it thumb-sucking.) When a problem exists, whether in personnel or in business operations, the time to act is now.

The second reason I regularly describe our problems in this area lies in the hope that our experiences may prove instructive for managers, auditors and regulators. In a sense, we are a canary in this business coal mine and should sing a song of warning as we expire. The number and value of derivative contracts outstanding in the world continues to mushroom and is now a multiple of what existed in 1998, the last time that financial chaos erupted.

Our experience should be particularly sobering because we were a better-than-average candidate to exit gracefully. Gen Re was a relatively minor operator in the derivatives field. It has had the good fortune to unwind its supposedly liquid positions in a benign market, all the while free of financial or other pressures that might have forced it to conduct the liquidation in a less-than-efficient manner. Our accounting in the past was conventional and actually thought to be conservative. Additionally, we know of no bad behavior by anyone involved.

It could be a different story for others in the future. Imagine, if you will, one or more firms (troubles often spread) with positions that are many multiples of ours attempting to liquidate in chaotic markets and under extreme, and well-publicized, pressures. This is a scenario to which much attention should be given now rather than after the fact. The time to have considered – and improved – the reliability of New Orleans’ levees was before Katrina.

You will note(!) that in the OCC Q3 2022 Quarterly Report on Bank Trading and Derivatives Activities Credit Suisse had a mere $186 Billion in total derivatives - peanuts! For example, completely safe and competent bank Citigroup had $47 Trillion in derivatives, but that’s NOTIONAL, which means everything is FINE, because all counterparties will always be solvent.

I always get a kick out of this stuff.

I mean, who’s the counterparty on U.S. Credit Default Swaps, Deutsch Bank?

Good thing copper mining is carbon-neutral!

California made a stunning decision last year—that by 2035 all new cars sold in the state must have at least 2½ times as much copper as conventional cars today. That’s not literally what the mandate said, of course, but it’s the practical effect of ordering all cars to be electric in the next 12 years.

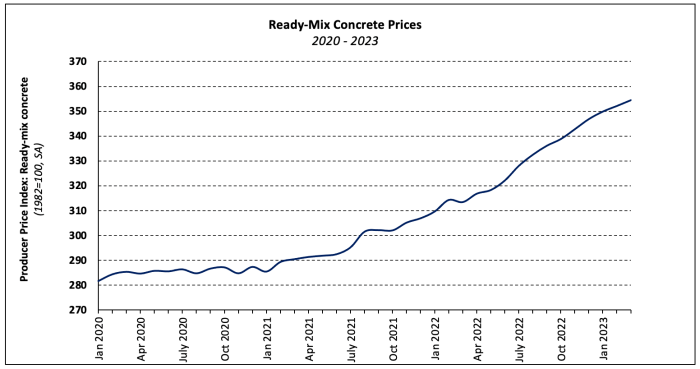

While lumber prices have come down off the highs, other things involved in construction have not:

Shadow Lenders to Bridge Real Estate Void Left by Banks, Bonds Carlyle, Castlelake, King Street, HighVista, Palladius Eye CRE

“Over a longer time horizon, [this] will likely shift CRE lending from the banking system to private capital at higher spreads,” hedge fund Ellington Management Group said in a report

Total Mortgage Debt Increases to $11.2 Trillion in 2022

Nation’s Top Mortgage Lender Launches a 1% Down Payment Home Loan This will end well.

San Diego County All-Cash Purchases by Zip Code

JPMorgan knew about Epstein accusations by 2006, lawsuit claims

JPMorgan Chase was aware by 2006 that Jeffrey Epstein had been accused of paying cash to have underage girls and young women brought to his home — seven years before the bank dropped him as a client, legal filings in New York on Wednesday alleged.

Of course they all knew.

At best - at best - they just didn’t care.

New Bombshells Filed in Court in the Jeffrey Epstein/JPMorgan Child Sex Trafficking Case Read this article. Very serious charges against St. Jamie Dimon and his outfit.

JPMorgan Compliance Urged Bank to Drop Epstein, Revised USVI Suit Shows

I finished my annual deep dive into family finances last night. It's hard to compare costs year-to-year because of lifestyle changes, but inflation on the staples of family life - food, clothes, etc. (we're incredibly lucky our housing costs are fixed) - must be up 15% from last year. Just thousands and thousands and thousands of more dollars needed per year to keep everyone clothed and fed and happy. We're fortunate that we can deal with the bleeding, for now... but sooooo many people in America must be crashing into destitution. Every day.

I think East Palestine paints a grim picture of the help we can expect from the government.

"I just wish everyone wasn’t so insecure." If somehow we could rectify this I honestly believe we would make so much progress. But, instead, we pump our chests or cry victim instead of doing the hard work.

UWM is going to crash and burn....and after I get through doing the 500 other things I've promised people I plan to spend significant time figuring out how it will happen.

And, now everyone is disputing where the "booked" CRE leverage is (https://www.axios.com/2023/04/12/commercial-real-estate-regional-banks-loans-maturing)....don't fool yourselves people, we have NO IDEA where the REAL re-hypothecated leverage is. We had a business at ResCap called CapRE (re-insurance) that I saw wiped to 0. These derivatives are air. And, we can see from what is happening in the Treasury markets that there is real distress. I just wish everyone would stop arguing about stupid details and get to the work of figuring out how we reasonably get out of this mess.