Surely You’re Joking

Uncapitalized Risk

My chat with London Paul on January 12:

This is the article I mentioned writing.

This cartoon is from 2007:

“If you’re not accountable to the political system, then you’re accountable to career incentives, and the career incentives come naturally in the direction of pleasing Wall Street, because when you step down, you either work for Wall Street, or give speeches to Wall Street, which is a very profitable activity.”

Luigi Zingales on the Capitalisn’t podcast

"A bet on gold is really a bet that the people in charge don't know what they're doing."

- Matt O'Brien, 2015

I was thinking about gold’s recent run compared to it’s last runup.

2008-2012

2022-2026 (so far…)

From 2008 to 2011, gold went from a major low of $680.80 to a peak of $1920.30, up 2.82x.

From 2022 until today (1/14/26), gold went from a major low of $1613.60 to $4586.43, 2.84x.

I have no idea if this means anything.

“The monetary system is a Marxist communist system. You have this politburo, the Federal Reserve board, a bunch of academics, a bunch of PhDs. That’s exactly what Gosplan was in the Soviet Union, a bunch of really smart people sitting in offices doing calculations about how many toothbrushes needed to be manufactured in the Soviet Union. And of course, you couldn’t get a good toothbrush, because central planning doesn’t work.

And so in the U.S., or in the west, we entrust the number one controller of people making decisions, interest rates. We entrust that to a bunch of academics and other people in a centrally planned situation. And so they are politically influenced, whether you like it or not, whether they say they’re they are or not - they are. They don’t let anybody fail…They constantly intervene, because you have this revolving door between Wall Street and academia and the Federal Reserve. So, of course, they’re going to bail themselves out.”

Via Grant’s, re: U.S. Wealth:

“Equities held both directly and indirectly (i.e., via mutual funds and other such vehicles) accounted for just over 47% of financial assets, up 170 basis points on a sequential basis and easily surpassing prior peaks of 42.4% at the end of 2021 and 38.7% at the height of the dot-com boom in early 2000.”

$381 billion in cash and Warren Buffett “found no opportunities in 2025 large enough to move the needle at prices he considers sensible.”

To me, this sends a clear message about valuations, but then again I don’t get paid based on assets under management.

Interesting podcast with Larry Chiavaro: Tricolor collapse, servicing transition sparks industry changes Couldn’t find a transcript.

"Apollo chief economist Torsten Slok told Fortune that corporate investment-grade issuance could reach as high as $2.25 TRILLION in 2026, raising questions about who will absorb the new supply and how it could influence Treasury rates."

Average hourly earnings multiplied by average weekly hours chained in today's dollar using [cough] the Consumer Price Index.

Average Weekly Hours

WSJ: “Gen X & Millennials Set to Inherit Trillions in Real Estate from Parents”

“Over the next decade, roughly 1.2 million individuals with net worths of $5 million or more are projected to pass down more than $38 trillion globally, according to a new report from brokerage Coldwell Banker Global Luxury reviewed exclusively by The Wall Street Journal.

“Real estate is poised to play a significant role in the great wealth transfer. Gen Xers and Millennials are set to inherit $4.6 trillion in global real estate over the next 10 years, according to the report, which incorporated data from research firms Altrata and Cerulli Associates. Nearly $2.4 trillion of that property is located in the U.S.

“Real-estate brokers, attorneys and family offices say they are already seeing profound changes in who buys luxury homes and how purchases are structured. High-net-worth families are bringing children into conversations about inheritance earlier and making high-stakes real-estate decisions sooner.

“It isn’t a new phenomenon for well-off parents to give children a helping hand in securing a first home. But at the high end of the market, agents say more parents aren’t waiting for kids to inherit their wealth; they are buying them luxury properties sooner. It’s reshaping the definition of luxury real estate, as more sellers cater to the tastes and preferences of a younger generation of buyers.

“In Manhattan, for instance, family money is accounting for an increasing share of major transactions.

“‘The price points have just gone wild,’ said Ian Slater, a Compass agent who works with ultrawealthy families in New York. ‘I used to commonly see people buy $3 million to $5 million apartments for their 25- to 30-year-old kids. Now I see people buying $15 to $30 million apartments for their kids.’

“Local agents said the trend is most pronounced in neighborhoods such as Greenwich Village, the West Village and Tribeca, where younger buyers tend to gravitate. It’s also concentrated on condos, rather than co-ops.

“New York’s Greenwich Village is one of the neighborhoods where parents are spending big money on homes for their children.

“‘When you’re buying for children, co-ops are a real no-no,’ since many co-op boards want the occupants of units to be financially independent, said luxury agent Clayton Orrigo. By contrast, condos offer flexibility, which is especially valuable for globally mobile heirs.

Condos are ‘much easier for parents buying for their children in an LLC or a family trust. If their kid is working at Google, but then next year they get transferred to London, the family can rent the apartment out,’ Orrigo said.

Wow. What a rarefied world. Some comments from the hoi polloi:

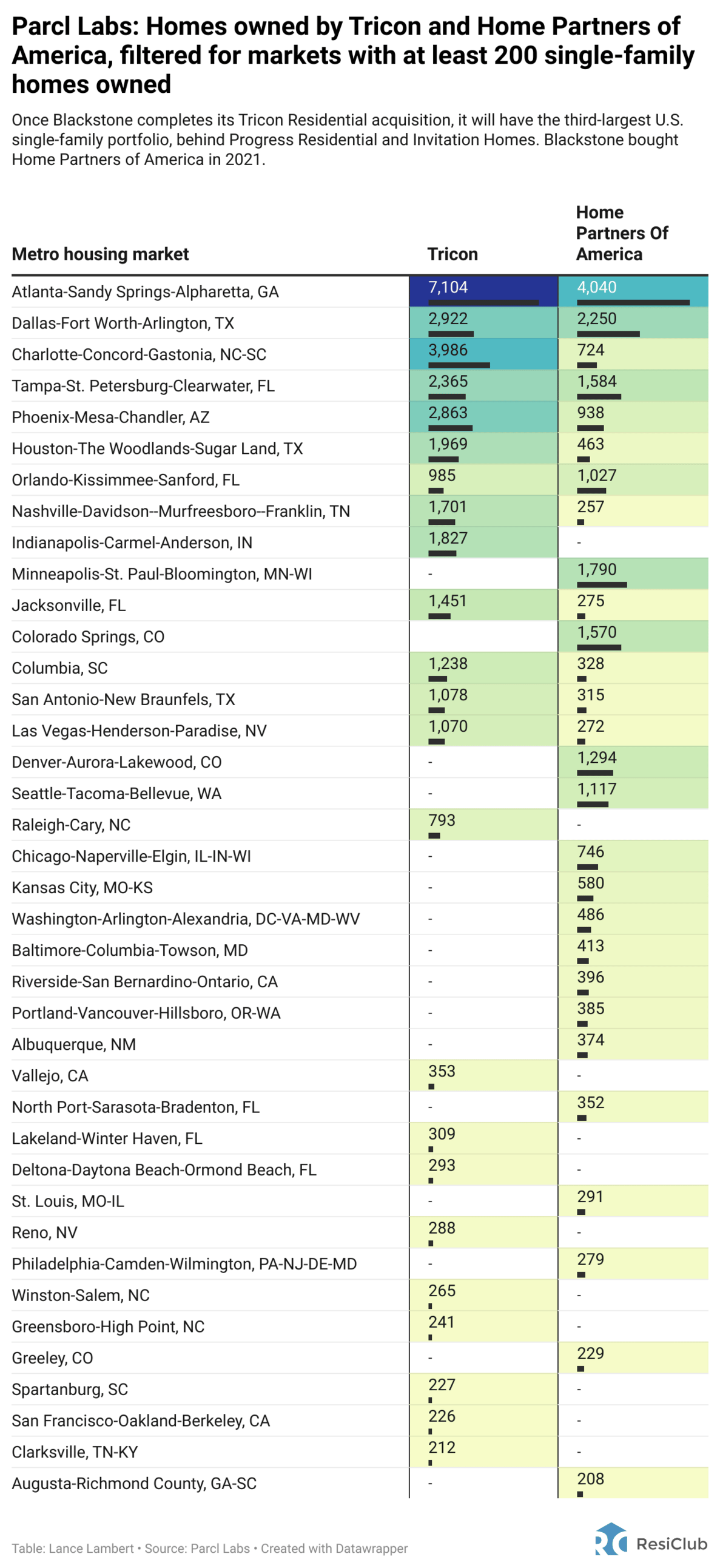

“Institutional ownership is absolutely a problem, especially in cities where there is a bunch of it like Atlanta & San Antonio. The below table from ResiClub highlights where the third largest institutional investor, Blackstone, owns the most single-family homes."

“According to Parcl Labs: Once the Tricon deal is complete, Blackstone’s single-family rental portfolio will be most concentrated in the following 5 housing markets:

Atlanta: 11,144 homes (7,104 Tricon; 4,040 Home Partners of America)

Dallas: 5,172 homes (2,922 Tricon; 2,250 Home Partners of America)

Charlotte: 4,710 homes (3,986 Tricon; 724 Home Partners of America)

Tampa: 3,949 homes (2,365 Tricon; 1,584 Home Partners of America)

Phoenix: 3,801 homes (2,863 Tricon; 938 Home Partners of America)”

“Because many of the players in this space are privately held, stories about these distressed sales are very hard to find. It takes combing through county records - which you sometimes have to do in person - to discover who actually owns the property. Often it is a maze of trusts and LLCs. Significant effort is required to sift through this data to identify the true owner. This is partly why many in the industry do not understand the role speculation has played.

While institutionals are a problem, they are not the problem in my opinion.”

Melody Wright on the next bailout

“They’re talking about phase one right now, which is banning them from purchasing, which none of them want to purchase them right now. None of them. None of them. If they’ve purchased any, they’ve bought them from their friends so their friends can make sure that the assets they have pledged to their lending facility are not degraded in value. They’ve been trading them like cards. Other than that, they’ve been net sellers.

I was in the room with one in September who said they are rehabbing the properties as soon as the lease is up, and selling them as quickly as possible, and they have been chasing price for months. And so, you know, I filmed in front of one in San Antonio a year ago, where they were cutting those prices left, right, and center because they’d gotten a massive property tax bill because they don’t get the homestead exemption. So, yeah, they want out. They absolutely want out. And so I think that this is the setup for a bailout where they’ll use one of these programs that they’re looking at in committee right now to either buy these homes explicitly from the institutions, or effect a way that some sort of nonprofit that’s on the edge, that public-private partnership can buy them at a certain price floor and then turn around and offer them through a an affordable housing program…"

Lonnie Hendry, Re: CREFC Miami: “I can tell you there was no measured approach…it was overwhelmingly, abundantly, hyperbolic-almost positive in terms of where people feel we’re headed in 2026.”

The CRE vibe is “deal-on, risk-on, busting at the seams on the availability of capital.”

Underwater car trade-ins are on the rise — and drivers owe a record amount, Edmunds finds

In the fourth quarter of 2025, 29.3% of trade-ins toward new car purchases had negative equity, according to new data from car website Edmunds.

The average amount owed on trade-ins with negative equity rose to $7,214 — an all-time high, Edmunds’ research shows.

A.I. Layoffs

“The primary motivation for this rebranding of job cuts appears to be investor relations. The report notes that attributing staff reductions to AI adoption “conveys a more positive message to investors” than admitting to traditional business failures, such as weak consumer demand or “excessive hiring in the past.” By framing layoffs as a technological pivot, companies can present themselves as forward-thinking innovators rather than businesses struggling with cyclical downturns.”

David Dredge

“The Sharpe Ratio is return over unit of risk, and they measure unit of risk as the volatility of those returns, and that is absolute nonsense.”

“Leverage means that you’ve got uncapitalized risk. If people are levering risk based upon bad mathematical metrics - and in the financial industry, in the fiduciary industry, that’s what everyone’s doing - they’re using things like value at risk and regulatory reporting and accounting nonsense and going out and taking massively asymmetric risks with other people’s money. So you get these accumulated undercapitalized tails in the system, and then it’s like a magnet, right? Once it starts going there, it’s an unstoppable train.”

“I’d be very cautious about being too enthusiastic about Tradfi getting their dirty little fingers into Bitcoin. I think it will inevitably bring leverage and danger to the process.”

“If I’m around a bunch of bankers or regulated financial fiduciaries, everybody always says, “Dave, what do you think the risk is? Do you think it’s geopolitics in North Asia, or do you think it’s recession in Europe, or do you think - you

know, all these random exogenous things out there?” And I say, “No, the risk is your balance sheet. Why are you why are you looking out there? All the risk is right in front of you.””

“We do have an aging demographic, more reliant on social security retirement schemes around the world, and becoming more heavily reliant on Medicare and the NHS here in the UK…they don’t have to [hyperinflate], but that is what they have chosen to do. I’ll argue this really goes back to 2000, but you accelerated post GFC, accelerated again post-covid - has really gone global - you could argue it started with my good friends in Japan who, added more fuel to that fire today with their own policy nonsense, and they’ve chosen this.”

“The true solution is productivity gains, right? You have to make the fewer workers more productive, so that there’s more productivity. They have to have higher real wages, not persistently lower real wages. You can’t constantly debase their earnings. Janet Yellen, you know, joking about it in 1996 when the Fed was talking about going to inflation targeting, and Alan Greenspan thought the inflation target should be zero, and Janet Yellen thought it should be 2%, because workers wouldn’t know they were having their real earnings debased, and the benefit to the employer would encourage him to hire more workers, because he’s kind of getting the 2% that they’re losing, and that’s literally in transcripts from the Fed.”

“I struggle to understand how A.I. learns, because the current A.I. doesn’t learn at all. It just expands its data set and gets a better probability of what the next word is, but it still hasn’t actually learned anything. And it only knows the average of what everybody already knows.”

“One of the things I criticize central bankers for all the time is because they seem to be incapable of learning…without accountability there can be no learning, right?”

“Nobody with their own retirement money was buying 30-year bonds that yielded zero. And yet all of the major governments in the world hit their peak all-time bond issuance when they yielded zero. Somebody was buying them. In fact, somebody was buying more of them than ever in history. Well, who was that? Regulated financial institutions.”

“I’ve long said that the next trigger is going to be Japan, that Japan is the likely spark, because of the fragility in the Japanese system after the longest period, 35 years of manipulating interest rates, manipulating the price that should balance between borrowers and lenders, savers, investors, speculators, hedgers, importers, exporters/ They’ve decided instead of you hundreds of millions of participants coming and finding an equilibrium balance where you’re happy to participate, we’re going to set it here, and we’re going to set it there, and keep it there for 30 years. And now the market’s decided they’ve had enough of that and the transition away from that is proving challenging, and I think still has a reasonable possibility of being the kind of thing that triggers some of these problems, because if Japanese investors are the largest net international creditors in the world. So Japan Inc. is the biggest foreign bond owner in every government bond market in the world, and if they decide they need to bring money back to buy their own bonds…” [bad things ensue]

New interview: Benny & The Squirrel with David Dredge

You may have noticed Sandisk in the news lately, probably because of this:

I remember Sandisk’s first incarnation, from almost 20 25 years ago, and dug up this post, from 2008:

As stated earlier in my blog, I once held a series 7. Not that that means anything. To be honest, I had series 7, and I didn't know my ass from a hole in the ground.

The stock market is extremely complicated. Not only is it extremely complicated, it has the tendency to illicit extreme punishment on stupid and smart people alike.

That said, I watched Wall Street Warriors Season 1 and thought it was interesting but not very remarkable. I couldn't really relate to any of the "characters" in the stories.

However, I just watched Season 2 and the dudes, who were selling Sandisk inspired me to write this.

They spent the entire Season pumping Sandisk, patting themselves on the back before watching that stock tank and seeing all their profits fly out the window.

I can only relate because I can definitely tell you I'm guilty of being that overconfident and stubborn, which is what I saw in these 2 dudes, who totally got fucked up. They broke one of the cardinal rules of being a stock operator. They married SNDK, and said "till death do us part." They actually took SNDK on a gay cruise. They were counting their money all the way to $54 a share and wept as they watched profits disappear into thin air. As it tanked, their clients lost a lot of money, they had to make the dreaded "I'm sorry I lost all your money" phone call.

As a broker, I pumped an IPO for about 4 months that was never even released. While there, I participated in a very similar activity to what these guys, who were selling Sandisk, were doing. This was back in 2000 when the bubble was in full bursting mode. I would call guys trying to sell Fudgepacker.com [not the actual name] and traders would laugh in my face. They would say shit like, "Are you fucking kidding me? Give me the ticker symbol so I can put my short in now."

But, some people, who I had never met before, would actually send me money.

Good times.

I worked for a small boutique firm that went bankrupt. I was one of the last one's to jump ship. In fact, I was the only smart ones to leave with office furniture, which was nice.

So, I'm not going to say those guys pumping SNDK were total idiots because I've been there-done that, and it would be like calling myself a douche. (I am a douche though for several reasons of which my ex-girlfriends can attest to.)

Clearly, the guys selling Sandisk just ran out of ideas. They didn't sell because they hadn't found their next Sandisk. They became their own self-imposed one-trick-ponies. Bush league. Mistakes like that kill most stock brokers.

Bulls and Bears make money. Sheep, pigs, and idiots get slaughtered. The allure is there because everyone thinks they have a big swinging dick only to find out their dick is just long enough to fuck themselves in their own ass. [sorry to be so crude]

But, here's a tip: Tiger Woods can shoot 65 in major and walk away pointing to some facet of his game that he feels he's struggling with. In other words, we are all striving for perfection, and that's only reflected by the rules and standards we set for ourselves. (Yes, that's a golf metaphor, and it relates to trading because trading takes practice.)

These guys on Wall Street Warriors made their big mistake back in Nov 2007. SNDK closed Friday at $15.69 a share. I enjoyed watching these guys because even though the market's atmosphere is completely different, it's nice to see the people playing the game haven't changed.

It would be interesting to know if these guys were able to shift gears enough to get out of their predicament. They were fucked then, but it would be interesting to see how they unfucked themselves. Did they sell? Were they able to rebound? My guess, they're selling used cars.

Successful traders find their next SNDK while closing out their current SNDK and banking profits. The cycle begins all over again. Their are more than a few guys driving Ferraris who trade this way. You build up a position and you sell without being too greedy. That's definitely a trading model that's workable. When the market's moving good, even retarded monkeys can make money.

Again, build a huge position, watch it go up, sell it off, move on to the next SNDK. It's funny how many people can screw up this up.

As seen in WSW 2, it doesn't always work out ideally because it's tough to time. When it doesn't work out, the stress and pain can cause a sprained vagina. Usually, people try to move on to some other job related to the market, "that's less stressful," which is a fucking joke because all work is stressful and risky. ...even jobs where you sit on your ass doing data entry are like this.

At the end of the show, these dudes tried to analyze, "what went wrong." They came up with a too simple answer, "We need to diversify," which is true.

They were victims of overconfidence. The moment they were absolutely positive SNDK could not be stopped, they should have realized that was the time to sell. There's group psychology at work in this scenario, and people were viewing Sandisk in a completely different light despite Sandisk's bright prospects. Fear set in. Investors sold. The stock fell. These guys, without stops, watched all their hard work fade away.

So, there's a lot of the same old classic lessons to be learned from their mistake:

•Exit stocks gracefully. Don't wait until the jugular is severed. "Averaging down" is good if your in a bull market, but in case you hadn't noticed, ever since George Bush has been in office, the market has moved sideways. Realize, no one's going to turn on a flashing neon sign that says, "It's time to sell."

•The market is always right. Don't waste time on stocks that aren't changing the way you want them to.

•Instead of counting profits, start taking profits off the table because that's what your competition is doing.

•If you don't have a profitable idea, don't do anything. Sit in cash. Learn how to short sell.

•A little bit of fear each day is a good thing. Don't get too confident, but don't be a fucking pussy either.

•Always, always use stops.

•Keep your head on a swivel so you can spot your next good idea." Personally, I won't have a good idea for an entire year. I've had some lengthy droughts before finding that golden opportunity. I'm currently experiencing one. In fact, the only good ideas I've had lately have been shorts.

Last, but not least, "Have fun!!!!"

This is information is just what I'm learning to believe: Learn how to make every single type of trade there is. Know short, medium, and long term trading strategies. Learn bull, bear, and stagnant market strategies. Don't be afraid to use them, and don't become obsessed with one particular idea because the market constantly changes.

Richard Brennan

“In physics, better models produce more consistent predictions. In markets, however, more traders using the same model make that model fail. Mean reversion systems, for example, cannibalize the signal over time as they are negative feedback processes. So it allows us to answer the question why more sophisticated models often increase fragility. You see the more precisely you try and fit a model to historical data, the more assumptions you embed about conditions remaining similar. But when conditions shift and in an adaptive system they always shift, the precision therefore becomes a liability.

So in a future that is not final, it also explains why responsiveness beats foresight. If the future is unfinished, the advantage goes to not to the trader who sees further but to the trader who responds faster and more appropriately to what actually emerges.”“If the forecast says I expect inflation to remain elevated, therefore bonds should sell off, the trade shouldn’t be short bonds because my forecast says so. The trade should be if bonds begin to sell in a way consistent with my hypothesis, align with that move. If they don’t, my hypothesis may be wrong or the timing may be wrong and I should wait. So this preserves the value of fundamental analysis while respecting the unfinished nature of the future.

So your analysis gives you a lens. The market gives you confirmation or denial. You trade the confirmation, not the lens. So the hard part is accepting that your well-reasoned forecast might simply be early or wrong or right but overwhelmedby other forces. The market is the final arbiter, not your analysis.”

William White

“For me the tipping point is purely psychological. Everybody sort of ignores the problem until all of a sudden they look at something that’s been hidden in plain sight, and at last they see. You know, as it says in the Bible, for those who have eyes to see, let them see and ears, ears to hear, let them hear. There comes a point in time where you can no longer avoid looking at the the hidden reality in the middle of the room.”

White’s comment above reminded me of this passage from the book, Dying of Money:

“As for speculators, the most extraordinary feature of the Reichsmark’s joyride was not any attack against it but quite the opposite, an incredible ("pathological,” it was later called) willingness on the part of investors at home and abroad to take and hold the torrents of marks and give real value for them. Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. The storage factor caused by the investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check. The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds. The German government strove mightily to outflood the sea.”

More William White:

“I dare say that we live in really unprecedented times. You look at the French fiscal situation, for example, that a lot of people are worried about, together with the political unwillingness of the governments to to do anything about it. You look at the French situation and say, “I’m out of here.” Well, where are you going to go? Going to go into the US dollar? Got exactly the same situation. Very, very high debt levels. No political will to deal with it. Underlying problems getting worse, not better. political division, the UK, Japan - so this is another element, and I have no idea how that will play out.

I suspect that some country will somehow attract the eye of the financial markets, and the bond vigilantes - absent for some decades - will reemerge and attack that one country, and then, like Southeast Asia during the Asian crisis, the markets will then sort of look at one country and say, “Wait a minute, it’s not just this one country that’s got a problem. They’ve all got a problem.” You can see the capacity for these underlying problems to metastasize and regenerate themselves in different places, because the underlying underbrush of debt is now so great that we’ve set ourselves up for a big problem.”“The belief that central bankers seem to have - and I guess others too - that inflation expectations are somehow anchored in the central bank’s target. There’s a guy at the at the Fed, the International Financial Group. Anyway, it was one of the Fed’s published papers, Jeremy Rudd, and he asks the question of why do we believe that inflation is anchored in inflationary expectations. And he then goes on to demonstrate that there’s in fact no theoretical ground for believing this to be true, no empirical ground for believing this to be true, and inflation in fact is anchored in past inflation.”

“I think the models that people have been working off of for the last 20 or

30 years have been simplified in order to make them tractable - mathematically solvable. They’ve basically been simplified to a point where… there is absolutely nothing in any of these models that is of significant interest to a central banker. I’ve used most of the models that you see that are being used by central banks and by many others as well. I mean the IMF and the OECD and whatever - they’re linear they’re deterministic. They’re based on the idea that the economy is simple understandable and therefore controllable. And all of this stuff is false. And that’s the fundamental problem.”

“In the leadup to the great moderation and even beyond, the importance of globalization in keeping inflation down - they totally missed it. If you’ve got a positive supply side shock, the appropriate answer is not to lean into it with lower interest rates. The appropriate answer is to react to the higher growth potential with higher interest rates. And they did the very opposite because their sort of simple, linear, deterministic, one-period model said we’ve got excess capacity now so the answer is you have to lower interest rates, and that led to the increases in debt that have plagued us ever since.”

“Income inequality…has been getting worse and worse for years, and, in large part, I personally put it down to monetary policy.”

Wesley Clark Explains

This is the paper, by John Mearsheimer and Stephen Walt, that Jeffrey Epstein and Alan Dershowitz, among others, tried to smear:

"Why has the U.S. been willing to set aside its own security and that of many of its allies in order to advance the interests of another state?"

The rather poignant story of Richard “Beebo” Russell:

“When people ask me what time is, I sometimes tell them - well, it's the stuff that stops everything from happening at once."“

Frank Close, 1998

Richard Feynman’s Cornell stories

“I’ve been restoring the original audio recordings that became the book Surely You’re Joking, Mr. Feynman! These tapes were recorded by Ralph Leighton in the 1970s and released on Bandcamp in 2013, but most people have only read the cleaned-up text version.

This 40-minute recording covers the stories from the “Dignified Professor” chapter: arriving at Cornell after Los Alamos with nowhere to stay, almost sleeping in leaves, the “damn liar” incident at student dances, and the wobbling plate story that led to his Nobel Prize work.

Hearing Feynman tell these stories in his own voice, with the pauses, the laughs, the genuine weight when he talks about post-war burnout, adds context you don’t get from the text. I’ve cleaned up the audio and added era-specific photos.”

Thank you, Rudy. Thank you for sharing that video on Russell. My nephew killed himself in 2018...I worry so much about our young - especially young men who feel hopeless. Very poignant indeed.

"Richard's situation was not unusual for what has morphed into a wage-slave economy. The fact that he had access to a plane makes it sensational."

https://www.thestranger.com/guest-editorial/2018/08/17/30824665/i-worked-with-richard-russell-at-horizon-air-and-i-understand-why-he-did-what-he-did#:~:text=I%20was%20a%20ground%20service,them%20out%20onto%20the%20taxiway.

When the evil violent mass murderer Woody Wilson and his horrid cabal of war profiteers pushed through the Feral Reserveless scheme in 1913 it cost $20 to buy one ounce of gold. Yesterday in response to great enthusiasm from buyers (Sydney and Hong Kong markets, our last night, their today) traders on the spot market set a brand new all-time intra-day (asking) price of $4,683 per ounce. As you can see, that means that the disgusting ugly Jerome Powell and his cohort have, in just 113 years, destroyed more than 99.57% of the purchasing power of the dollar, deliberately, purposely, and maliciously. They have never cared about inflation. They don't care about the American people. Their "agency" is not constitutional, is not any good, and should be destroyed. The buildings in which they work should be levelled, their personal assets and pensions should be confiscated for direct and immediate distribution to their victims, and there should be a small circle of salt three feet across and about a foot deep put down near the centre of where each of those buildings previously stood so nothing ever grows in that place, and a monument erected at each location explaining what horrid, evil, awful people they were, and how they were hurtful and mean-spirited for generations until people finally had enough and took them to task for their many crimes. Many things that should happen have not yet happened.