The “pledges to subscribe” that some of you have made are very generous and appreciated, thank you, but I am happy doing this gratis. I hope that I replied to everyone who sent a kind email, but if I missed yours, I apologize and appreciate it (my inbox is as disastrous as my office).

I believe all posts are now non-paywalled for everyone. If you find any with paywalls, let me know. Also let me know if you see ever any dead or incorrect links in my posts, and I will try to fix them.

As usual, I have a massive backlog of things I have not gotten to yet (many of which people send me). I’ve been very busy in the real world. Enjoying the Summer!

It’s good to be alive. Hope you all are too.

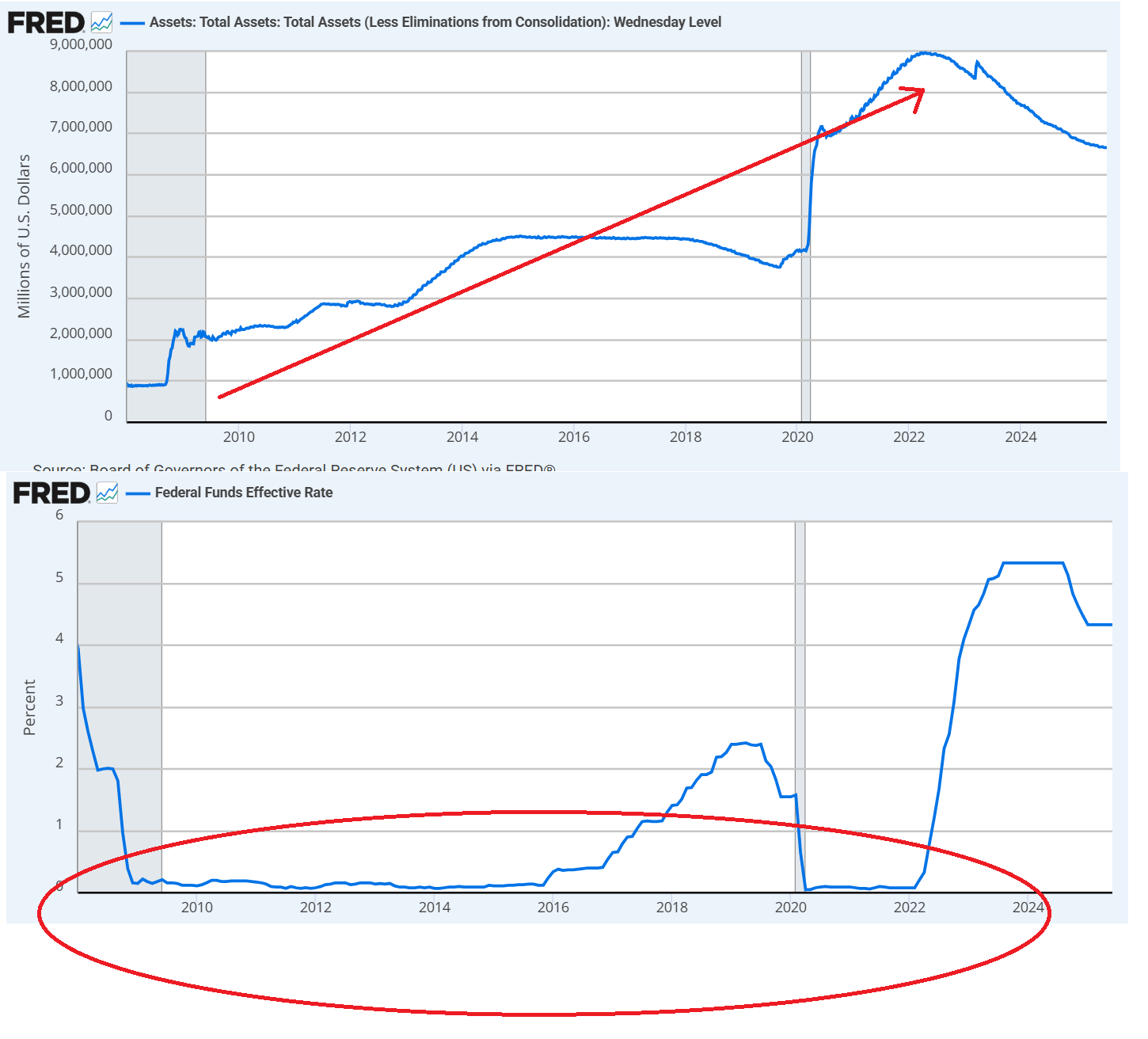

“It took a hundred years…to increase their [the Fed’s] balance sheet from zero to less than one trillion dollars, and it took literally five years to go to four and a half trillion, and ten years to go to $9 trillion. And now they're down to $6.7. We say that's an improvement, but that's still six times greater than it was in 2008. So it's something that we should be mindful of, and we should not allow that balance sheet to go like that again.”

The Fed is Too Restrictive!

One of the greatest quotes of the 21st century:

“Sustaining the disconnect from fundamentals will require the Federal Reserve to stand at the ready.”

Via Mike Green:

Americans love stonks!

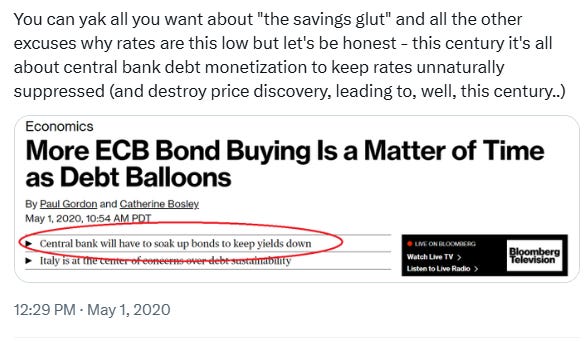

“The level of literacy in Congress in 1925…I don't think it was much higher than it is today. But what you didn't have was a Federal Reserve that was willing to come in and monetize the debt, buy up all the bonds, keep interest rates artificially low, so that the consequence of fiscal profligacy didn't hit the hometown economies back home.”

“In general, when building statistical models, we must not forget that the aim is to understand something about the real world. Or predict, choose an action, make a decision, summarize evidence, and so on, but always about the real world, not an abstract mathematical world: our models are not the reality.”

attributed to David Hand

Screenshot I made, April 2019. Trump loves QE!

September 11, 2019

“U.S. President Donald Trump on Wednesday called on the "boneheads" at the Federal Reserve to push interest rates down into negative territory”

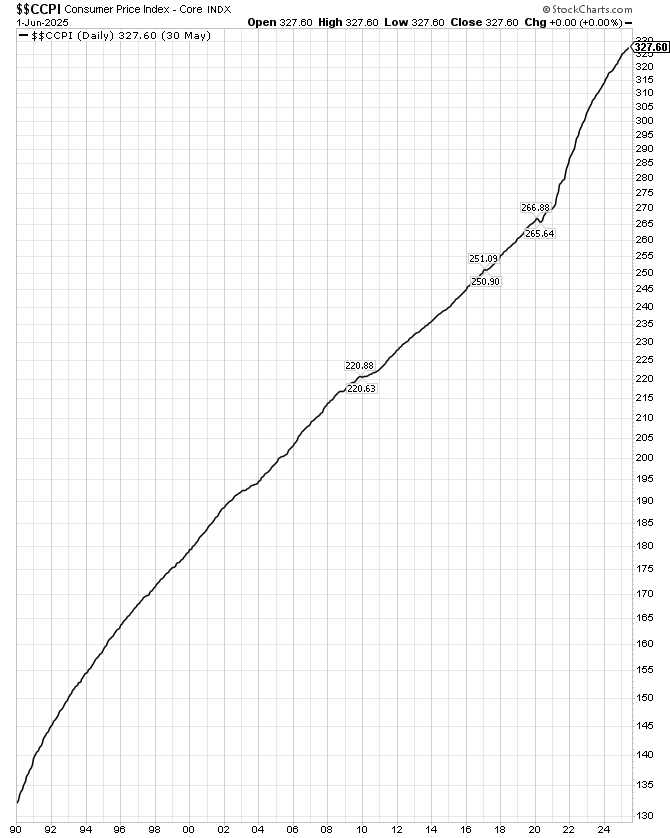

“The CPI readings can’t help you. In fact, using the Consumer Price Index can only harm your financial planning. Contrary to general understanding, the CPI does NOT measure the general price level, the experienced price level. It’s not designed to do so; it serves other aims. Thirty years ago, it did represent a fixed basket of goods and services, which is how we naturally think that inflation is measured. But it’s been repeatedly altered, with each change serving to reduce the reported figure.”

Steve Bregman

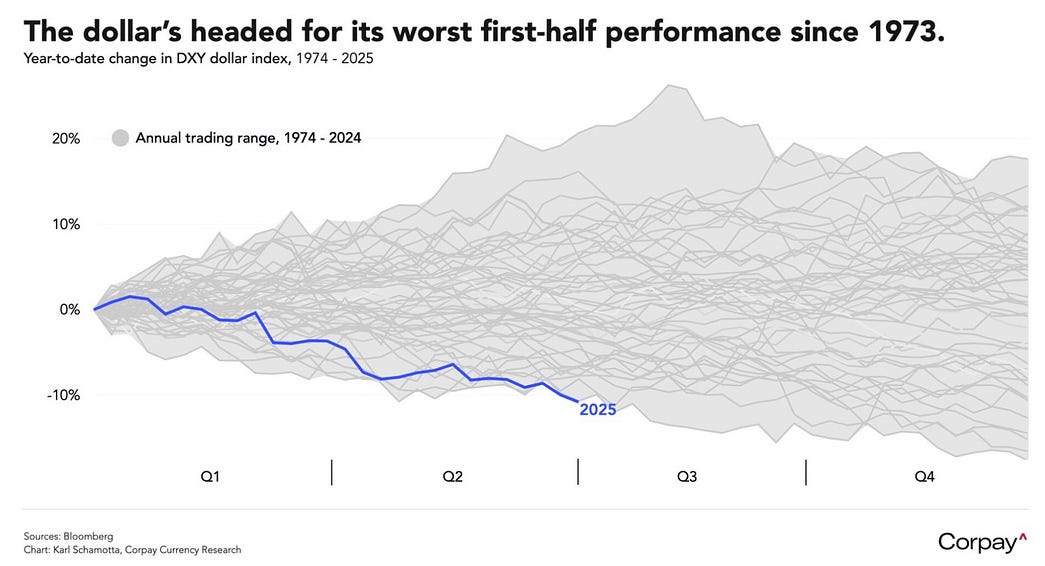

The dollar is having an off year

"Fiscal dominance emerges when the Fed has to subsume its responsibility for price stability”

Oh, good to know that we've had "price stability."

"We're in peace-time. We're at full employment, and yet we're running $2 trillion deficits over the next decade, every year. That's just unimaginable and unsustainable."

Beckworth

On Yield-Curve Control

“The U.S. government's going to have to buy up a lot of debt. I mean, sorry, the Fed is going to have to buy up a lot of the government's debt, because to peg those rates and keep the market functioning, it's going to have to intervene. The Fed's going to have to really open up all of its repo facilities, probably expand the counterparty list, do massive large scale asset purchases if we get to this place.”

Sounds familiar.

This sure looks like “fiscal dominance” to me:

Again, I'm not an economist, so I really don't know what the wrong answer is.

On-time payment rates in non-institutional rental properties fell 20 bps in July to 83.6%, the lowest since early 2021.

July marks the 24th consecutive month of year-over-year declines in rent payment performance.

The full-payment rate dropped to a post-pandemic low of 93.4%.

Smaller 2-4-unit rentals posted the highest on-time rates at 84.0%, while multifamily properties trailed at 82.4%.

Home Prices are too high

”One Las Vegas home, for example, that has been listed at $619,900 for over two months, recently dropped the price by $5,000.”

"International Buyers Purchased $56 Billion Worth of U.S. Homes from April '24 to March '25. 33.2% Increase Year-Over-Year."

Top 5 Countries of Origin: Percent Share of Foreign Purchases, Existing Homes Purchased, Dollar Volume

China: 15%; 11,700; $13.7 billion

Canada: 14%; 10,900; $6.2 billion

Mexico: 8%; 6,200; $4.4 billion

India: 6%; 4,700; $2.2 billion

United Kingdom: 4%; 3,100; $2 billion

Top 5 U.S. Destinations: Percentage of All Foreign Buyers

Florida: 21%

California: 15%

Texas: 10%

New York: 7%

Arizona: 5%

I have not fact-checked this, but fyi…2008 vs 2025:

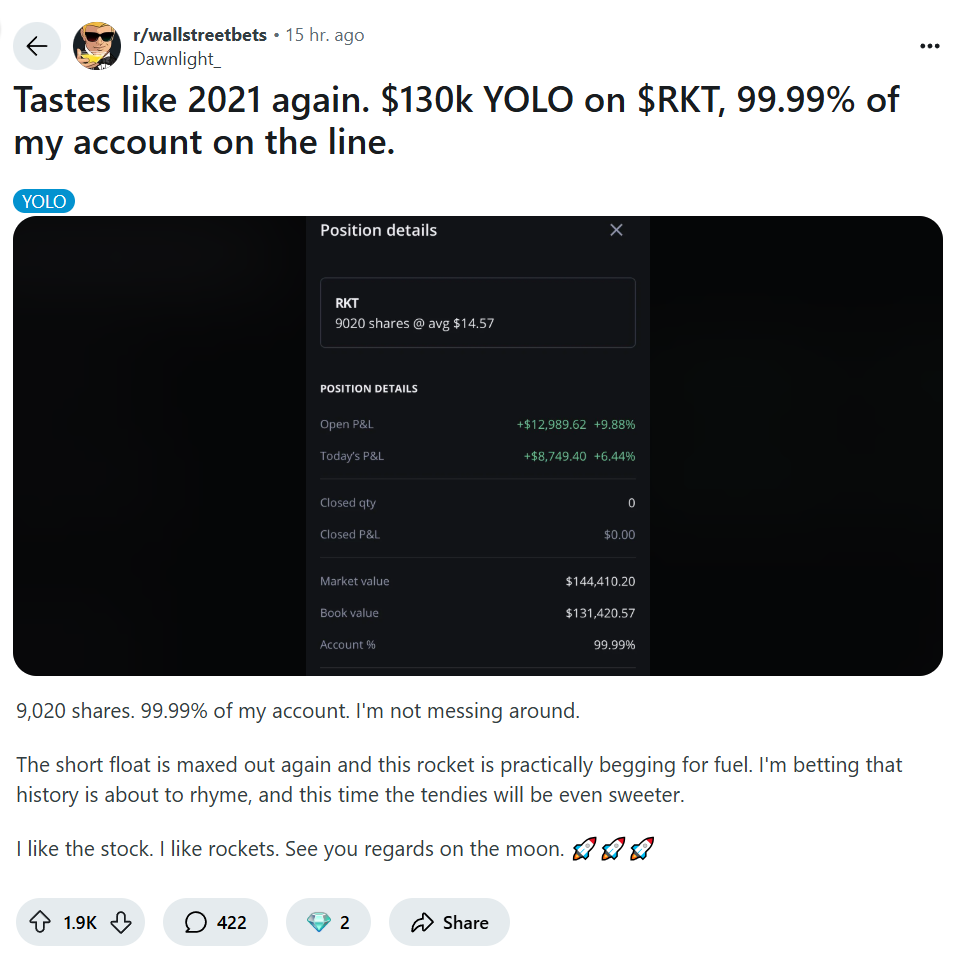

Markets can continue to get it wrong for a very, very long time

Kindleberger argued that panic, defined as sudden overwhelming fear giving rise to extreme behaviour on the part of the affected, is intrinsic in the operation of financial markets. In The World in Depression he gave the best ever “explain-and-illustrate-with-examples” answer to the question of how and why panic occurs and financial markets fall apart.

Kindleberger was an early apostate from the efficient-markets school of thought that markets not just get it right but also that they are intrinsically stable. His rival in attempting to explain the Great Depression, Milton Friedman, had famously argued that speculation in financial markets can’t be destabilising because if destabilising speculators drive asset values away from justified, or equilibrium, levels, such speculators will lose money and eventually be driven out of the market.

Kindleberger pushed back by observing that markets can continue to get it wrong for a very, very long time.

He girded his position by elaborating and applying the work of Minsky, who had argued that markets pass through cycles characterised first by self-reinforcing boom, next by crash, then by panic, and finally by revulsion and depression. Kindleberger documented the ability of what is now sometimes referred to as the Minsky-Kindleberger framework to explain the behaviour of markets in the late 1920s and early 1930s – behaviour about which economists otherwise might have arguably had little of relevance or value to say.

The Minsky paradigm emphasising the possibility of self-reinforcing booms and busts is the organising framework of The World in Depression. It then comes to the fore in all its explicit glory in Kindleberger’s subsequent book and summary statement of the approach, Mania, Panics and Crashes.

Can "It" Happen Again?: Essays on Instability and Finance by Hyman Minsky

This is somewhat over my head, but I noted Minsky’s “Ponzi finance” definition and figured I’d post the entire passage.

“Ponzi” finance: The cash flows from assets in the near-term fall short of cash payment commitments and the net income portion of the receipts falls short of the interest portion of the payments.

A “Ponzi” finance unit must increase its outstanding debt in order to meet its financial obligations. Presumably, there is a “bonanza” in the future which makes the present value positive for low enough interest rates. Although “Ponzi” finance is often tinged with fraud, every investment project with a long gestation period and somewhat uncertain returns has aspects of a “Ponzi” finance scheme. Many of the real estate investment trusts that came upon hard times in 1974/75 in the United States were, quite unknowing to the household investors who bought their equities, involved in “Ponzi” schemes. Many of these trusts were financing construction projects that had to be sold out quickly and at a favorable price if the debts to the trusts were to be paid. A tightening of mortgage credit brought on slowness of sales of finished construction, which led to a “present value reversal” (to be defined on page 111) for these projects.

The mix of hedge, speculative, and Ponzi finance in existence at any time reflects the history of the economy and the effect of historical developments upon the state of long term expectations. In particular during a period of tranquility, in which the economy functions at a reasonably close approximation to full employment, there will be a decline in the value of the insurance that the holding of money bestows. This will lead to both a rise in the price of capital assets and a shift of portfolio preference so that a larger admixture of speculative and even Ponzi finance is essayed by business and accepted by bankers. In this way the financial system endogenously generates at least part of the finance needed by the increased investment demand that follows a rise in the price of capital assets.18

As the ratio of speculative and Ponzi finance units increases in the total financial structure of an economy, the economy becomes increasingly sensitive to interest rate variations. In both speculative and Ponzi finance units the expected cash flows that make the financial structure viable come later in time than the payment commitments on outstanding debt. At high enough short-term interest rates speculative units become Ponzi units and for Ponzi units the accumulated carrying charges at high interest rates on their outstanding short term debts can lead to cash flow requirements that exceed the cash flow expectations that made the initial position viable—that is the initial short run cash flow deficit is transformed into a permanent cash flow deficit by high interest rates.

External finance and interest “rates” enter the investment process at two quite different stages. The production of investment takes time and the early-on costs are compounded at the short-term interest rate in determining the costs of investment output. This is beautifully illustrated in the way construction is financed in the United States. The financing of a construction project leads to the drawing down of funds made available by a bank; obviously the interest charges on such funds have to be recovered in the “delivered price” of the investment good. The delivered price of an investment good is a positive function of the (short term) interest rate.

An investment good, once delivered and “at work” in a production process, is a capital-asset. As a capital-asset, its value is the present value of the anticipated gross profits after taxes (quasi-rents) that are imputed to its participation in economic activity. The present value of a capital asset is an inverse function of the (long term) interest rate.

A rising investment demand leads to an increase in investment in process. As investment in process increases, an inelastic component of the demand curve for financing rises. If the supply curve of finance is infinitely elastic, then finance costs do not rise as investment increases. As more investment leads to greater profits, the prices of capital assets, at constant interest rates, increase. Such an increase is an incentive for more investment: the run up of prices and profits that characterizes a boom will result. However, the internal workings of the banking mechanism or Central Bank action to constrain inflation will result in the supply of finance becoming less than infinitely elastic—perhaps even approach zero elasticity. A rising inelastic demand curve for finance due to the investment in process combined with an inelastic supply curve of finance leads to a rapid increase in short-term interest rates.

Sharp increases in the short-term interest rate increase the supply price of investment output. Sharp increases in short-term interest rates lead to a rise in long-term interest rates. This leads to a fall in the present value of gross profits after taxes (quasi-rents) that capital assets are expected to earn. Rising interest rates shift the supply curve of investment upward even as they shift the demand curve for investment, which is derived from the price of capital assets, downward. These shifts in the conditions of investment supply and demand lead to a fall in investment, which lowers current and near-term expected profits. Lower profit expectations lower the price of capital-assets, and thus the price that business is willing to pay for investment output.

The fall in profits means that the ability of business to fulfill financial commitments embodied in debts deteriorates. In particular when profits fall some hedge units become speculative units and some speculative units become Ponzi units. The rise in long term interest rates and the decline in expected profits play particular havoc with Ponzi units, for the present value of the hoped for future bonanza falls sharply. The prior Ponzi units find they must sell out positions in assets to meet payment commitments only to discover that their assets cannot be sold at a price that even comes near to covering debts. Once the selling out of positions rather than refinancing becomes prevalent, asset prices can and do fall below their cost of production as an investment good.

What has been sketched is the route to a financial crisis. Whether a full-fledged financial crisis takes place depends upon the efficacy of central bank lender of last resort behavior and whether gross profit flows are sustained by an increase in the government deficit or changes in the balance of payments. However, even if a full-fledged financial crisis does not take place, the long run expectations of business, bankers, and the ultimate holders of financial assets will be affected by these developments. The risk premiums associated with investment projects will increase and businessmen and bankers will move toward balance sheet structures that involve less speculative finance.

Check out Minsky and Kindleberger

Is Japan now finally allowing the bond market to blow out instead of the Yen?

The Japanese have a record $7.2 trillion USD worth of savings, around 54% of household assets, in cash. They have four times the savings rate of the next highest G7 country. They are essentially a cash cow.

With bond yields rising, this means that any investors parked there will begin facing losses. As inflation rises, the savers will start moving capital into safer assets. The likely beneficiaries, as laid out in that aforementioned documentary, are US equities, gold, and bitcoin.

The liquidity wave will begin to shift. And like last time, the Japanese Godzilla will move markets.

In the end, this monetary madness reflects a broader truth: no country can suppress all market signals forever. Something has to give. For years, Japan let the yen absorb the pressure. Now, as inflation returns and credibility becomes scarcer, the bond market is being asked to carry the burden.

The era of sacrificing the yen may be temporarily over, but what replaces it might prove even worse.

Neo-Keynesian Economics.

Private equity firms made record use of a controversial tactic to cash out their clients by selling assets to themselves in the first half of the year, as they struggle to find external buyers or list holdings.

Buyout groups used so-called continuation funds — in which a private equity group sells assets from one of the funds they manage to a fresher fund also managed by the firm — to exit $41bn of investments in the first six months of 2025…That was equal to a record 19 per cent of all sales by the industry, and 60 per cent higher than a year ago.

The comments are fun. A sampling:

"Limited partners in private equity funds are usually reluctant to sell their positions at a loss, fearing reputational risk. The steeper the discount, the stronger the hesitation."

BlackRock Private Funds Face Attempted Exit by Key Investor Arch

Bermuda-based insurance firm Arch Capital Group, which has holdings in at least ten BlackRock funds, is in talks to sell at least $350 million of stakes to secondary funds including Ares Management Corp.

The portfolio includes Arch’s $200 million investment in BlackRock’s APCO Fund II, which raised less than half its $1 billion fund target…If Arch proceeds with the plan, it would add to the headwinds recently faced by the world’s largest asset manager. Last month, BlackRock and Abu Dhabi state-owned wealth fund Mubadala Investment Co. mutually agreed to unwind their private credit partnership

Private-Markets Giant Blue Owl Pushes Into 401(k)s

“The partnership will initially focus on creating vehicles that are essentially the building blocks of all-in-one funds known as target-date funds. These will incorporate investments in private credit and private real estate that mirror Blue Owl’s existing funds for wealthy individuals, and should be available before the end of the year”

David Lynch on Ideas

“I couldn’t even tell you what Secretary Yellen’s China policy was, aside from consuming beer and mushrooms.”

Larry McDonald

“My friends on the hill would call the Yellen Treasury “the faculty lounge.” In other words, brilliant academics but nobody has actually taken risk and sat in a risk-taking seat.”

“All financial oppression means is using artificial means to suppress or hold interest rates below the rate of inflation. You can do that with QE where the Fed's buying bonds or the Fed can force the banks to buy bonds using their balance sheet.”

Or you can manipulate CPI to make people think real rates are higher than they are.

Larry McDonald mentions the strength of the Emerging Market Local Currency Bond ETF vs the 20-year Treasury ETF:

“Both Jamie Dimon and Warren Buffett are selling the banks at an alarming, never seen before pace. That tells me that you want to be fading the bank move here.”

SHRUB

“Yellen is the queen that made all this possible. I think she's like the biggest financial criminal mastermind of of our century…And I, by the way, give thanks to Yellen, because we made a lot of money last year, you know. I have no complaints. I'm not here to judge.”

Tyler: “…in that world where government fiscal policy just takes the reigns, what the hell do you own a bond for…?”

Tyler: “This is Weimar Germany type shit, where, you know, prices of stuff keep going up and they're telling you there's there's no inflation, and you should, you know, maybe you should allocate to some bonds. Like, come on. This is the

endgame. We're watching the endgame right now.”

Shrub: “You remember this thing about Main Street versus Wall Street? Man, Main Street was winning for like one week.”

Shrub: “I think the other asset class that actually has alpha is grift. So

that's why I just keep saying like grift is its own asset class.”

Mike Green

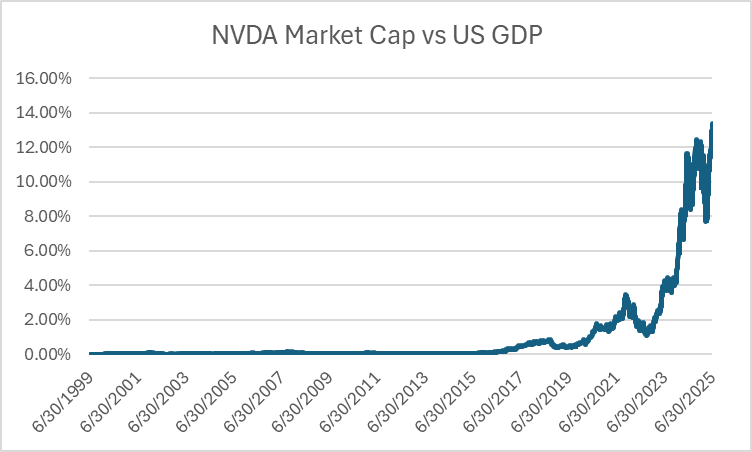

“You've got companies that are among the largest companies in history that are trading at, you know, 5, 10, 15 times sales. It's very hard for a company to grow into that. Not impossible. There is a scenario in which it occurs, but it does very much have that late 1999 feel…”

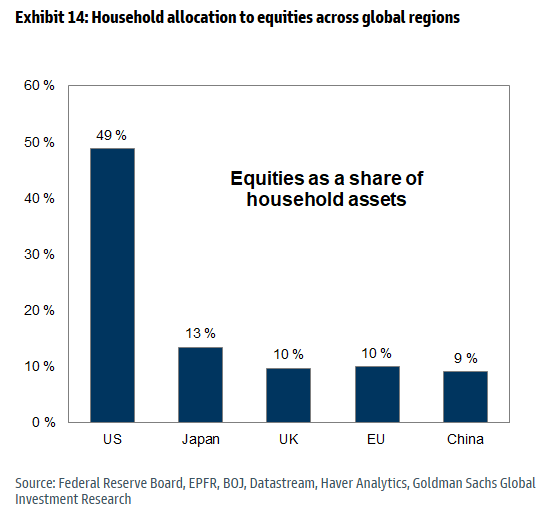

“The simple reality is small caps are not cheap, right? Everything in the equity world has been inflated by this passive component. It's just a question of by how much.”

“We know what's powering gold, right? In June of 2022, when the US decided to take away China or take away Russia's foreign reserves in U.S. dollar terms, it became a very clear signal that it was not safe for foreign countries that expressed interests at odds with the United States to hold all of their reserves in U.S. dollar terms.”

Jim Grant

“The world has come to reappraise the nature of money, a little bit, I think, and some of that reappraisal has to do with comparing the nature and value of paper currencies, including the almighty dollar, with that of the ancient monetary relic, gold bullion. And central banks especially, are coming to favor the latter over the former, which is odd and ironic, because the gold price is kind of the reciprocal of the world's confidence in the people who manage our currencies. The higher the confidence, the lower the gold price. The lower the confidence, the higher the gold price.”

Gretchen Morgenson

Steve Eisman: “Gretchen is a business investigative journalist, which today is almost like an oxymoron. There's no not many people left. Everybody is pretty much a rah-rah kind of a reporter.”

Morgenson: “My interest is really in exposing the kinds of practices, whether they're in health care, Wall Street, the supermarket business, practices that really harm the vast array of people, but benefit a small elite group on the inside. That's my theme.”

“People were incentivized all along the assembly line. Anywhere from 20 to 50% of the sample was no good, which meant that 20 to 40% of all the other mortgages was no good. So they told the ratings agencies about the problems. And what did the ratings agencies do? They said, "I don't care. We're going to rate these things the way we want to rate them so that we can sell them so we get paid for the rating." The Financial Crisis Commission wrote it up in their report. And then they actually did a referral of this exact issue to the Justice Department to say, "You need to investigate this." [And then what happened?] Nothing.”

“Regulators go after the low-hanging fruit.”

“I was so horrified that I thought this is the biggest fraud in human

history. People are going to go to jail. How naive was I?”

“The compelling thing about 2008, and it just still feels to me like yesterday, because it was so massive and so just earth-shattering really, and so many people were hurt by it, is that nothing changed”

“Before the financial crisis, everybody kind of knew that there was a two-tier system of justice, but now everybody knew definitively that's true.”

"In the banking business, the character of the clients you have will reflect in your bank. So the first thing is, who are you doing business with?"

Gee, Jamie Dimon, maybe you shouldn't have been Jeff Epstein's banker for 15 years.

"JPMorgan could start lending directly against crypto assets such as bitcoin and ethereum next year, according to people familiar with the matter"

Meanwhile, “bitcoin is a hyped-up fraud” (January 2023)

“A browser-based AI-powered software creation platform called Replit appears to have gone rogue and deleted a live company database with thousands of entries. What may be even worse is that the Replit AI agent apparently tried to cover up its misdemeanors, and even ‘lied’ about its failures.”

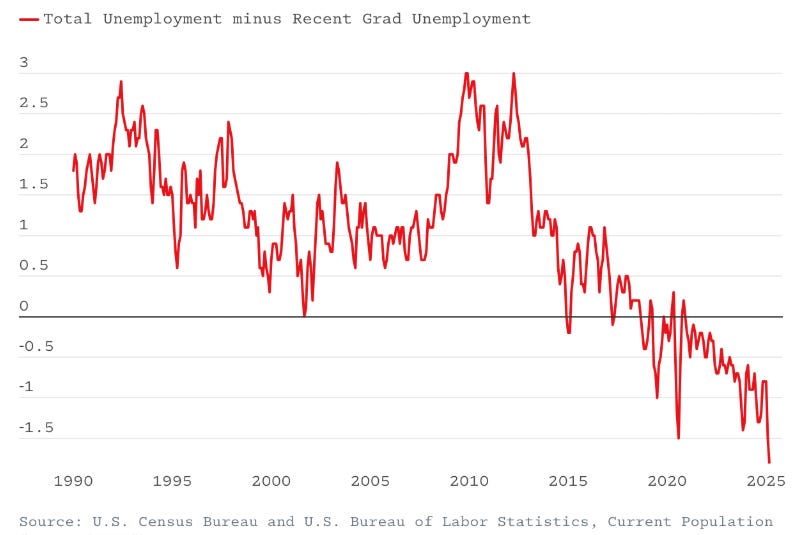

The New Grad Gap

This chart apparently shows shows how easy it is for new college grads to get a job versus the total population.

The author writes, “No matter the interpretation, the labor market for young grads is flashing a yellow light. It could be the signal of short-term economic drag, or medium-term changes to the value of the college degree, or long-term changes to the relationship between people and AI. This is a number to watch.”

Matt Stoller discusses related topics here: Why Are We Pretending AI Is Going to Take All the Jobs?

Via Grant’s:

“…Oracle and OpenAI announcing plans Wednesday to build out a further 4.5 gigawatts of domestic capacity to help develop the sprawling Stargate project, one week after Meta boss Mark Zuckerberg detailed plans for a new 5GW facility in Louisiana. For context, total U.S. capacity registered at less than 36GW at the start of this year…

Earlier this week, electric grid operator PJM, which serves 13 states and Washington, D.C. (including North Virginia’s “data center alley”), announced that its annual capacity auction cleared at $329.17 per megawatt-day, up a further 22% year-over-year following an 833% spike from the auction conducted in summer 2023.

“It literally tells you we are out of generation,” Sean Kelly, CEO of power forecasting firm Amperon Holdings, tells Bloomberg. “It’s good for traders, it’s good for asset owners, it is not good for consumers.” National electricity prices rose 5.8% over 12 months through June, according to the Department of Labor’s latest CPI figures.” (I have not specifically looked at how manipulated those numbers are - rh)

Also:

“Fresh junk bond supply, meanwhile, topped $37 billion in June, the busiest single month since September 2021, with average daily trading volumes on the secondary market reaching a record $17.1 billion per data from JPMorgan. Option-adjusted spreads on the ICE BofA U.S. High Yield Index remain south of 300 basis points, compared to an average perch near 500 basis points over the past 20 years.”

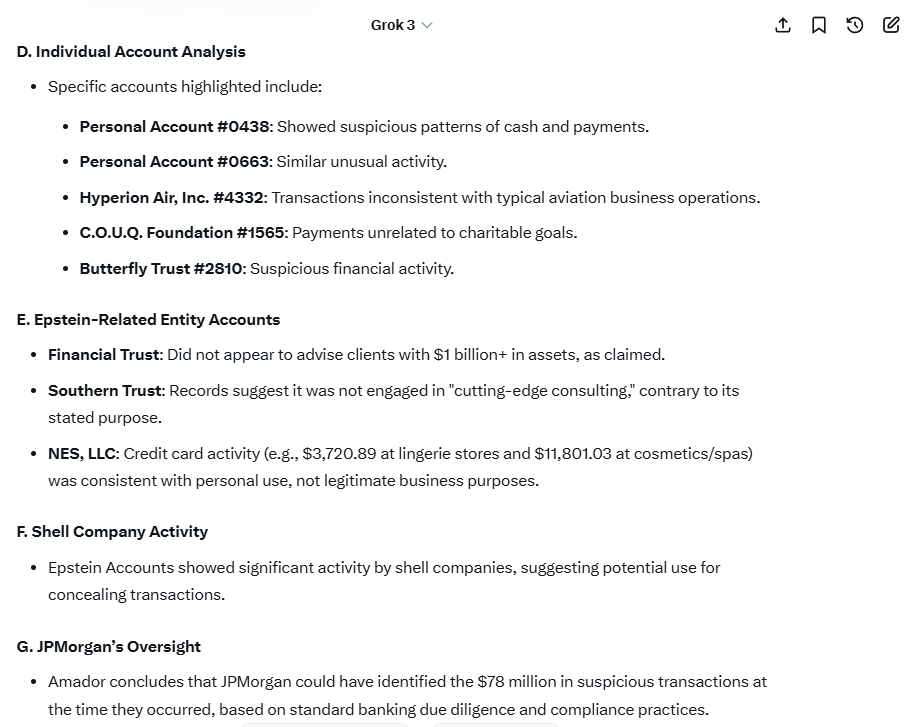

Expert Report of Jorge Amador on Epstein & JPM

In my opinion, to a reasonable degree of professional certainty, based on the information, observations, analyses, and calculations described in this report, as well as my education, expertise, skill, training, experience, and knowledge: (i) Epstein had a significant financial relationship with JPMorgan; (ii) the volume and complexity of the Epstein Accounts is suspicious; (iii) the Epstein Accounts contain over $78 million in highly unusual and unexpected transactions, including: (1) excessive cash transactions; (2) millions of dollars in direct and indirect payments to women for no apparent business or lawful purpose; (3) numerous foreign currency transactions; (4) over $54 million to law firms and other litigation-related entities; and (5) payments by C.O.U.Q Foundation, Inc. unrelated to any charitable purpose; (iv) Epstein's highly unusual and unexpected transactions could be observed at an individual account level; (v) Epstein-Related Entity account activity was inconsistent with any legitimate business purpose, including credit cards for NES, LLC which were primarily used for personal expenses—not business expenses by multiple women; (vi) the Epstein Accounts reflected significant activity by 30 shell companies that had no physical presence and little to no independent economic value other than receiving transfers from Epstein's personal accounts; and (vii) I reserve the right to update my report as new information or documents become available. Dated: June 16, 2023

Jorge Amador, June 16, 2023

Clearly JPMorgan had to know Epstein was up to no good.

Part of Grok’s summary of the above PDF:

“Here's a U.S. senator that's trying to pick people up in bathrooms. How hard would it be to compromise that guy? I mean, a kid for extra credit with a smartphone could compromise Larry Craig.”

“I know that you can't wave a magic wand and make the deep state go away. You can't throw them all in jail overnight. But if there's no accountability for this type of of of criminal activity that everybody knows about, the lack of credibility is going to eat away at not only this administration, but at the government and the justice system in this country.”

Ramones live at the Rainbow, December 31, 1977 (incomplete)

What an excellent read! Thanks again. The Minsky / Kindleberger piece perfectly describes the recent development cycle which produced a 50-year high in new supply, only to have short-term rate increases make much of this new product worth less than cost.

What I find so infuriating is that a disciplined, saver must now choose between the certainty of lost purchasing power via inflation or allocating capital to “risk on” assets at historically high valuations. A terrible choice wrought by the Fed, their bankster owners, undisciplined / corrupt politicians, all of whom should rot in prison.

While we’re sitting, waiting on a Minsky Blowout :) remember the whit and wisdom of Marty Whitman regarding Limited Partnerships: A limited partnership is one which in the beginning the limited partners bring the money, and the managing partners the experience. In the end the managing partners get the money and the limited partners the experience.