That permanency of value

The mindless bid

“Almost everywhere you look, most issues today, especially things like affordability of housing, are driven by inflation. And who brought us the inflation? Our friends on the Federal Reserve Board. So, you know, they have totally failed in their mandate to control prices.”

Some excerpts from Warren Buffett’s latest:

Looking back I feel that both Berkshire and I did better because of our base in Omaha than if I had resided anywhere else. The center of the United States was a very good place to be born, to raise a family, and to build a business. Through dumb luck, I drew a ridiculously long straw at birth…

Berkshire has less chance of a devastating disaster than any business I know. And, Berkshire has a more shareholder-conscious management and board than almost any company with which I am familiar (and I’ve seen a lot)…

One perhaps self-serving observation. I’m happy to say I feel better about the second half of my life than the first. My advice: Don’t beat yourself up over past mistakes – learn at least a little from them and move on. It is never too late to improve…

Remember Alfred Nobel, later of Nobel Prize fame, who – reportedly – read his own obituary that was mistakenly printed when his brother died and a newspaper got mixed up. He was horrified at what he read and realized he should change his behavior. Don’t count on a newsroom mix-up: Decide what you would like your obituary to say and live the life to deserve it.

Greatness does not come about through accumulating great amounts of money, great amounts of publicity or great power in government. When you help someone in any of thousands of ways, you help the world. Kindness is costless but also priceless. Whether you are religious or not, it’s hard to beat The Golden Rule as a guide to behavior. I write this as one who has been thoughtless countless times and made many mistakes but also became very lucky in learning from some wonderful friends how to behave better (still a long way from perfect, however). Keep in mind that the cleaning lady is as much a human being as the Chairman.

Tony Deden: The Illusion of Progress

So good. These are excerpts - read the entire piece.

This essay was born out of revulsion to an accidental summer reading that paraded progress as virtue and private equity as its high priest. Every paragraph spoke the same pious language of “sustainable improvement,” “societal benefit,” and “long-term value creation,” as though leverage, asset-stripping, and balance-sheet cosmetics had become moral acts.

I found myself revolted not merely by the hypocrisy, but by the vacuousness of it.

In our hyper-financialized society, we have come to mistake valuation for value, and activity for achievement. The word ‘progress’ has been exploited to justify anything that moves—no matter what it destroys. What follows is an act of refusal to bow to the idea that more money is progress. If this essay has a motive, it is contempt for the trivial slogans that pass as thought, and for the hollow theory that confuses financial engineering with human improvement…

The real advances of mankind—from cultivation to industry—were not the gifts of invention alone but of moral order: the discovery that property, family, and saving could bind effort to consequence and turn scarcity into sufficiency. Progress was an achievement of character before it was a measure of output. It was the steady improvement of life through virtues that bound action to consequence: thrift, property, responsibility, and the protection of what one built.

Yet, by the early twentieth century, this older meaning of progress—rooted in work, discipline, and the tangible improvement of life—was already beginning to fade. The moral foundations that once joined virtue to growth began to erode. The word itself was captured by a new creed—one that mistook abstraction for achievement, and motion for improvement. Slowly, the means of creation turned into the means of speculation…

Two revolutions hastened this separation. The first was monetary: the gradual abandonment of money’s anchor in real value. Convertibility yielded to confidence; credit creation replaced saving. As Hans-Hermann Hoppe observed, when money ceases to be anchored in real value, society’s time preference inevitably rises: the future is discounted, patience gives way to immediacy, and the long view of the builder yields to the short view of the trader.[iii]

The second revolution was institutional: the rise of corporations whose worth came to rest less on what they produced than on what others believed they were worth. Accounting, once the record of fact, became the medium of expectation.

By the mid-twentieth century, profits no longer required production in the traditional sense. Balance sheets could expand through debt; share prices could rise through mergers, acquisitions, and later, buybacks. Speculation in financial instruments grew to rival the industries whose securities they represented.

Murray Rothbard warned that such monetary inflation does not enrich society as a whole but transfers its substance—quietly and systematically—from producers and savers to those nearest the source of new credit. What appears as growth is, in truth, redistribution masked by rising prices and expanding balance sheets…

GDP measures the speed of activity, not the value or purpose of what is done. It tallies every transaction as growth, whether it builds a bridge or bombs one, whether it cultivates soil or strips it bare. The cutting of a forest, the repair of its flood damage, and the lawsuits that follow each adds to the total. Destruction and recovery register as twin booms. As stupid as it sounds, in this arithmetic, a society may spend itself into apparent wealth…

GDP cannot distinguish between creation and consumption, between genuine capital formation and the liquidation of the past. It registers motion, not meaning. When a company borrows to buy back its shares, GDP rises. When financial speculation multiplies without adding a single good or service, GDP rises again. In this way, the volume of transactions is mistaken for the creation of wealth…

Private equity is the purest expression of this new creed. Its tools—leverage, optimization, and exit—belong to a world where time has been conquered and consequence deferred. Businesses once built to last are now built to sell. The craftsman’s slow accumulation of goodwill is replaced by the manager’s quick extraction of yield. When every enterprise must justify itself through “enhanced shareholder value,” the distinction between stewardship and exploitation collapses. The result is not creation but conversion of substance into symbols, and of permanence into liquidity…

Here lies the moral inversion of our age. Money, which was once the servant of purpose, has become its measure. The larger yacht, the faster airplane, the greater “net worth”—these are not symbols of abundance but of dislocation. They mark the distance between possession and peace. The pursuit of more has displaced the question of what it is for. And when a civilization forgets to ask that question, it continues to advance in technique while it declines in wisdom.

An honest investment policy for such a time cannot be built upon forecasts or leverage, but upon conscience. The real measure of return is endurance: what remains when the fashion has passed, what serves when speculation ends. Capital that sustains meaning—institutions, skills, and relationships—outlasts all that merely inflates price. To invest rightly is to align money with purpose, to treat gain as the servant of continuity rather than the substitute for it.

If there is to be progress again, it will come when we understand that it is not the endless acceleration of change but the maintenance of meaning through time. It is not a line on a graph that ascends, but a circle that endures.

Only when money measures service, and success is judged by what is built and preserved rather than what is traded or displayed, will progress cease to be an illusion—and become, once more, an achievement of character.

Chesterton’s Fence

In the matter of reforming things, as distinct from deforming them, there is one plain and simple principle; a principle which will probably be called a paradox. There exists in such a case a certain institution or law; let us say, for the sake of simplicity, a fence or gate erected across a road.

The more modern type of reformer goes gaily up to it and says, ‘‘I don’t see the use of this; let us clear it away.”

To which the more intelligent type of reformer will do well to answer: “If you don’t see the use of it, I certainly won’t let you clear it away. Go away and think. Then, when you can come back and tell me that you do see the use of it, I may allow you to destroy it.”

GDP “reveals almost nothing about how...prosperity is shared...if a small slice of the population is awarded the great bulk of the bounty from economic growth while everyone else remains unenriched, GDP would rise... And that, to a crucial degree, is exactly what has happened.”

Albert Gallatin, 1831

“Gold and silver are the only substances which have been, and continue to be, the universal currency of civilized nations. It is not necessary to enumerate the well-known properties which rendered them best fitted for a general medium of exchange. They were used not only as ornaments and objects of luxury, but also for that particular purpose, from the earliest times.

We learn from the most ancient and authentic of records that Abraham was rich in cattle, in silver, and in gold ; that he purchased a field for as much money as it is worth, and in payment weighed four hundred shekels of silver, current (money) with the merchant.

And when we see that nations, differing in language, religion, habits, and on almost every subject susceptible of doubt, have, during a period of near four thousand years, agreed in one respect ; and that gold and silver have, uninterruptedly to this day, continued to be the universal currency of the commercial and civilized world, it may safely be inferred that they have also been found superior to any other substance in that permanency of value, which is the most necessary attribute of a circulating medium, in its character of the standard that regulates the payment of debts and the performance of contracts.”

(US-1988).jpg - Wikimedia Commons")

Daniel Oliver

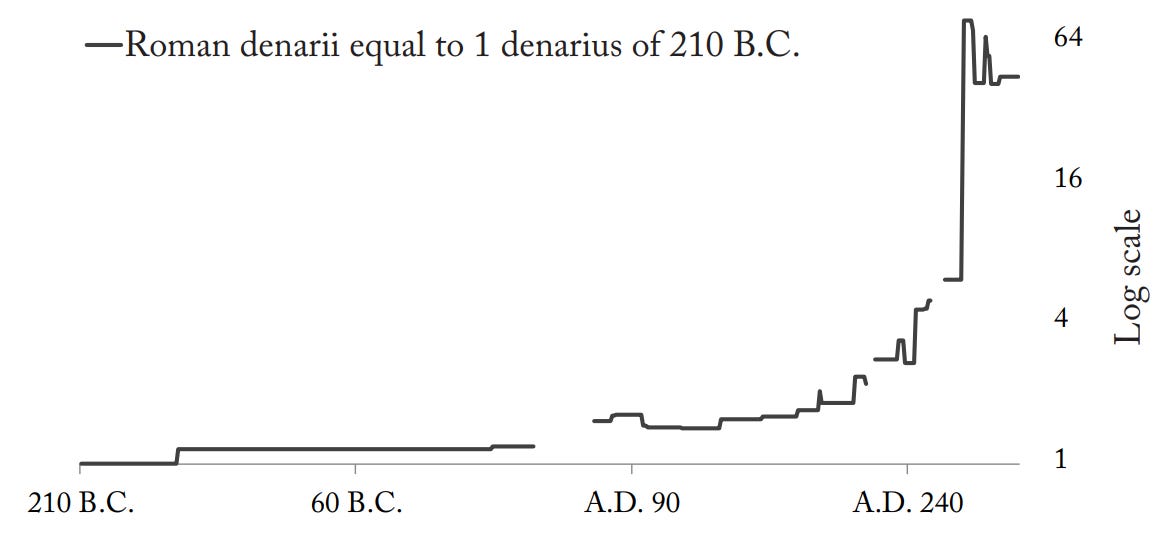

“I am not aware that Hank Paulson or Bernanke ever specifically credited Tiberius Caesar as the genius behind TALF and TARP. But the very purpose for the Federal Reserve was to prevent bank runs using the same methodology as Caesar.

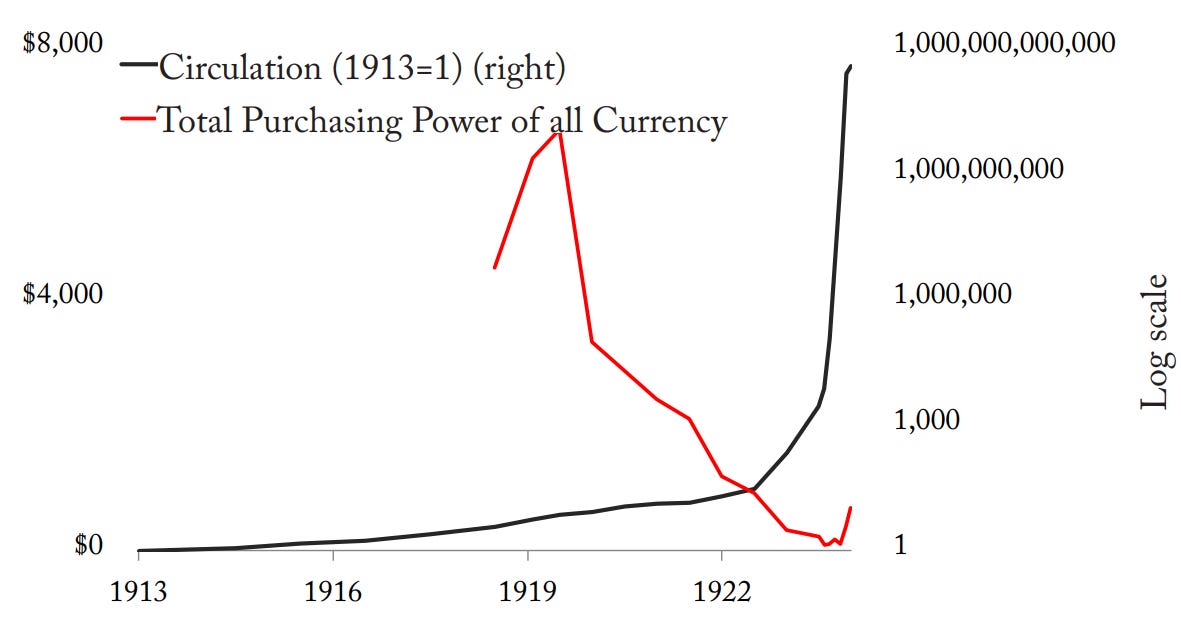

As we know, the solution worked too well. Once the banks and the economy got used to the low interest rates, they became dependent upon low interest rates. And soon the state was debasing the currency in order to create more. As Rome reduced the silver content of the coinage, prices went vertical. Note the logarithmic scale: once they started printing, they had to keep printing at a faster rate.”

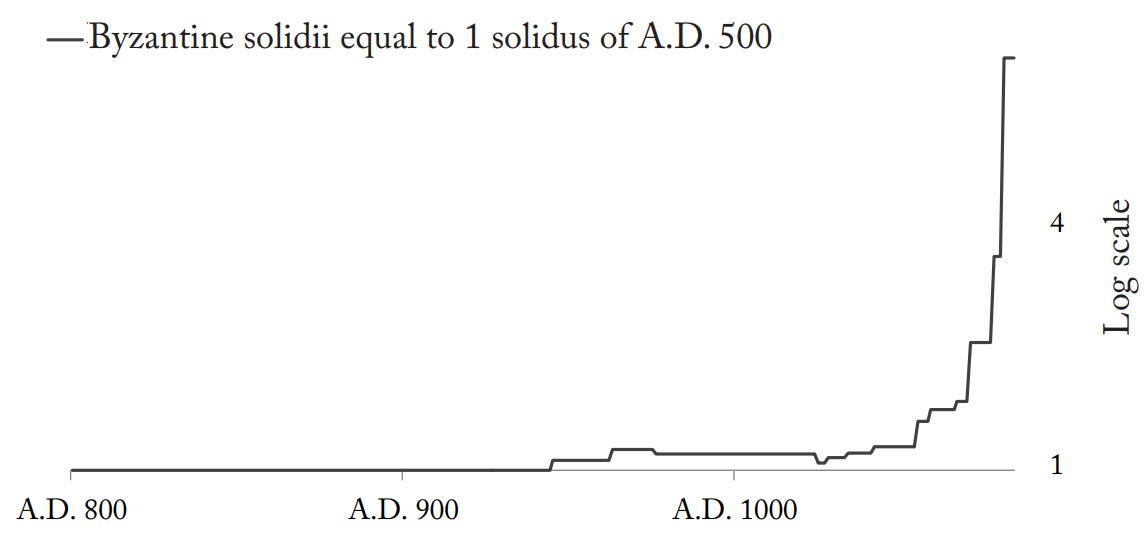

“This phenomenon is ubiquitous. The Byzantine solidus, for example, remained stable at 4.5 grams of twenty-three-karat gold from the fourth century AD until the tenth century—six hundred years—but once they started debasing, the rate of debasement kept accelerating.”

“And, of course, the famous German example. In this case, we do have more math: the red line shows the total value for all German marks in U.S. dollars. In other words, it wasn’t just that as the Germans printed, each mark became worth less—the value of the entire circulating medium became nearly worthless. This is why—in the midst of hyperinflation—the authorities kept worrying about the scarcity of money, driving them to print money ever faster.”

“Monetary stimulus is only half the story. The other half is fiscal stimulus. And, again, we have some ancient examples. By the reign of Diocletion in AD 290, the Roman economy was in tatters from all the debasement. So what did he do?

The Roman historian Lactantius tells us:”

He built Palaces for himself, for his Wife, and for his Daughters: and to these he added a Hippodrome, an Arsenal, and a Mint house: And when he had finished a Building at the cost of ruining some of the Provinces by it, he found some fault or other in it, and then he pulled it down, and gave orders to rebuild it in another manner: nor was this second Building secured from a new caprice, upon which it might be likewise perhaps leveled with the ground.

“Observe how closely these words of Lactantius track what Paul Krugman blurted out three days after the World Trade Center was destroyed: “Ghastly as it may seem to say this, the terror attack—like the original day of infamy, which brought an end to the Great Depression—could even do some economic good. . . . Now, all of a sudden, we need some new office buildings . . . [and] rebuilding will generate at least some increase in business spending.”

Krugman actually wrote that, as if tearing down buildings could be a good thing…

Everyone expected a so-called peace dividend when the Cold War ended: instead we got two Middle Eastern wars and then the war on terror and now war in the Ukraine. We have to keep on inventing reasons for war…

Here is Biden’s Secretary of State, Tony Blinken, boasting that the Ukrainian war spending helps the American economy:

“If you look at the investments that we made in Ukraine’s defense to deal with this aggression, 90 percent of the security assistance we provided has actually been spent here in the United States, with our manufacturers, with our production, and that’s produced more American jobs, more growth in our own economy. So this has also been a win/win that we need to continue.”

Think about that: we need to continue war to grow our economy.

Frank Chodorov wrote in the 1950s: “war is the state’s escape from a collapsed internal economy.” This is why we nearly always find war at the end of a credit cycle.

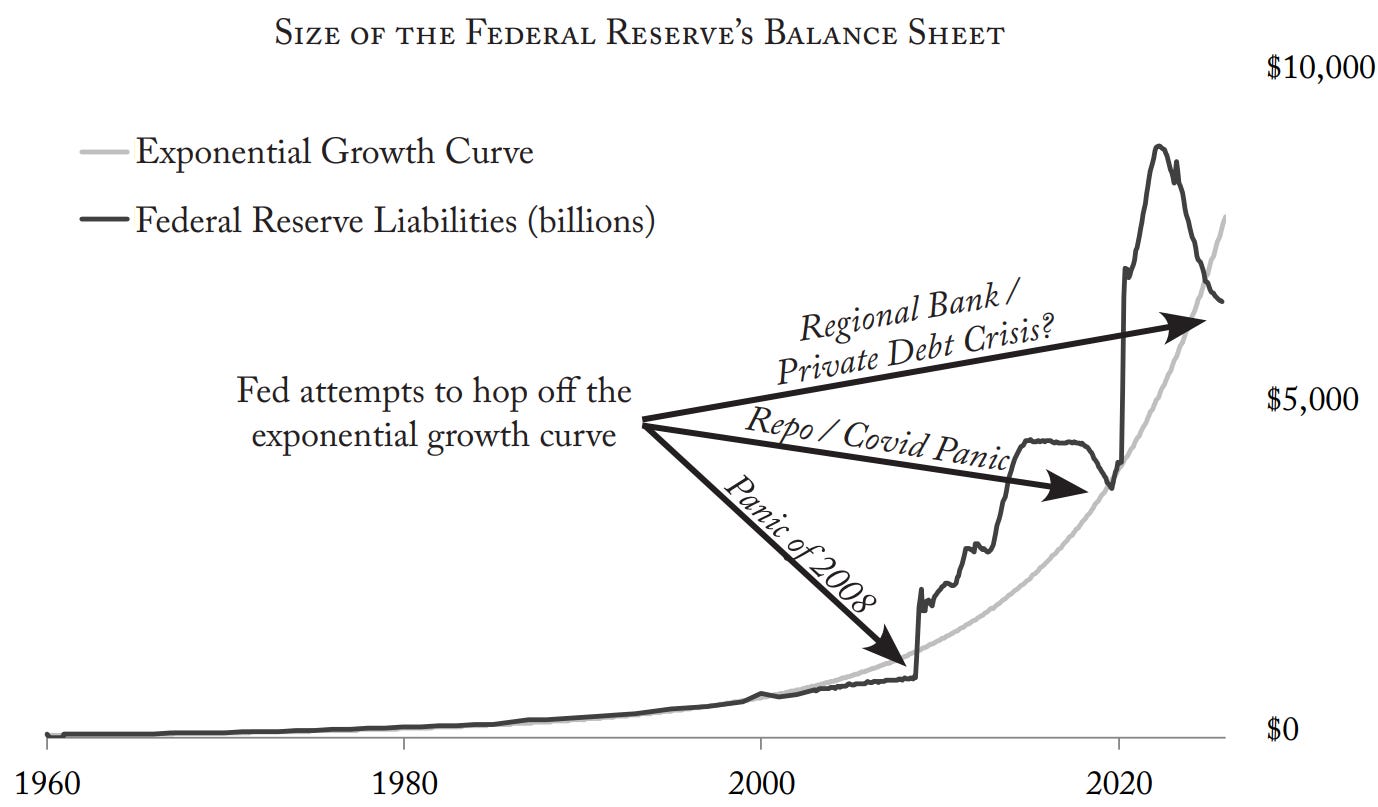

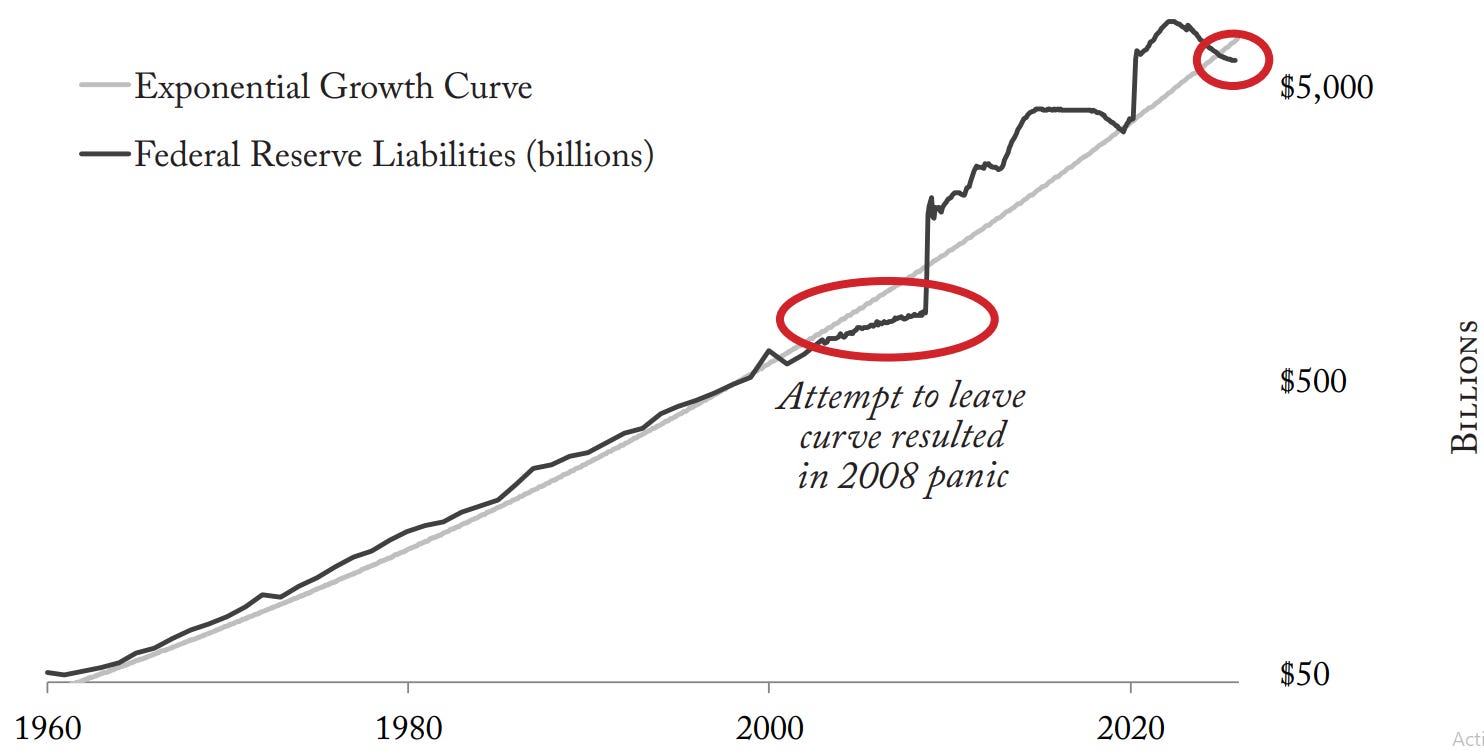

Sadly, the U.S. is following the path forged by many failed empires before it. We see on the chart that every time the Fed tries to hop off the exponential growth curve of money, there is a financial crisis.”

“We’ve just crossed the line again, and already the Fed’s repo lines are ramping up— it had to deploy $80 billion into the banking system last Friday. We’re not lost yet. If we look at that same graph on a log scale—to compare against the others—we are still some distance from the bend in the curve where things go crazy.”

“Perhaps there is still time to defeat history, to hop off this curve.

It would be painful. It was, in fact, the Fed’s attempt to do just this that resulted in the 2008 panic: too much debt demanding payment by currency that didn’t exist. That would happen again: We would have to accept widespread default1, a 1930s style crash.

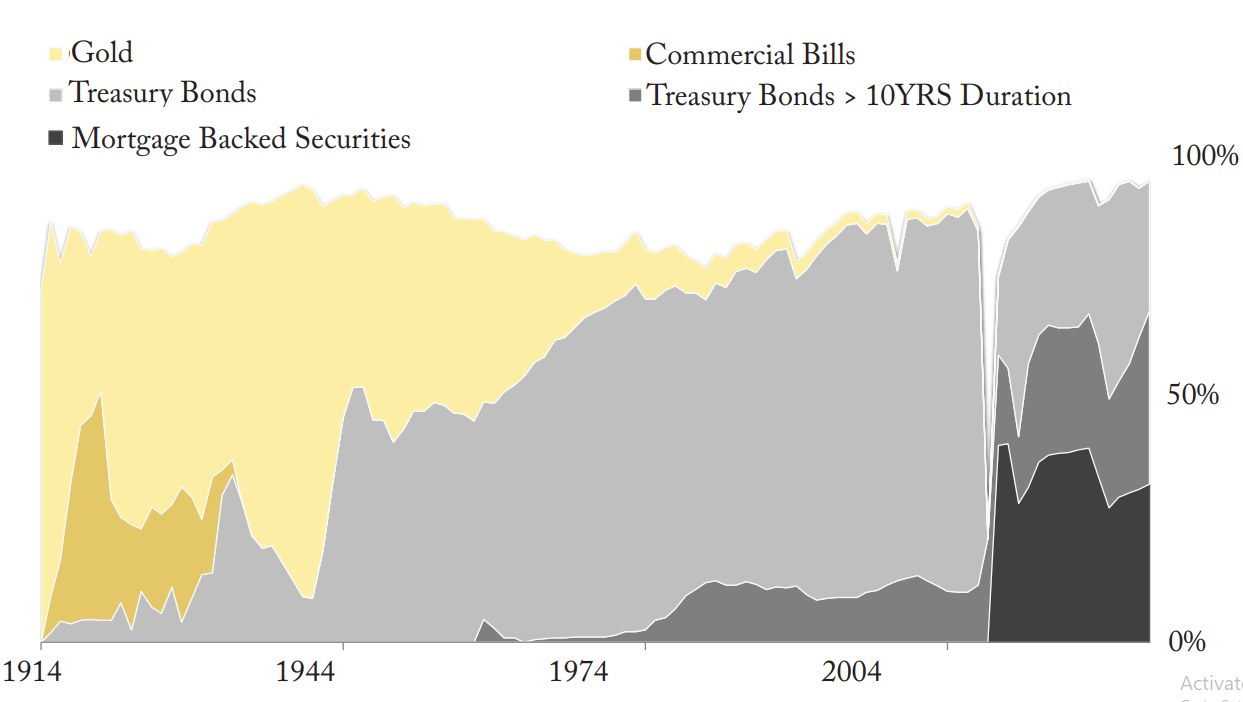

And there’s a second problem: It’s not just that the Fed has been creating more dollars at an exponential rate. It prints dollars by buying assets, and the new assets on the Fed’s balance sheet are supposed to give the new liabilities value. But we see from the chart that the Fed is buying assets of ever less quality, in the same way that the roman coins had ever less silver.”

“This chart assumes gold at the official price of $42.22 per ounce. With gold at $4,000 per ounce, gold represents 15% of the Fed’s balance sheet.

Historically, in normal times, gold covered between a third and half of bank balance sheets, both public and private. At the current size of the Fed’s balance sheet, gold coverage of a third would be $8,500 per ounce. Half would be $13,000 per ounce. The market price of $4,000/oz is still a bargain.

And there are three big caveats. First: those coverage ratios—of between a half and a third—were when the other assets were solid: 90-day commercial bills or short-term government bonds—not 30-year government bonds of a bankrupt Congress.

Second, we know that the balance sheet is going to get bigger in the next crisis, which may already be arriving as private credit starts to wobble.

Third, unlike other central banks, the Fed doesn’t own the gold on its balance sheet—the Treasury does, from when Roosevelt confiscated the nation’s gold in 1933. So revaluation helps the Treasury, not the Fed.

This fact opens up two possibilities: one is that a gold revaluation grants the Treasury new funds, which it spends, making inflation worse.

The second is that, at some point, the U.S. could cut the Fed loose. We’ve done it before. America has had two previous central banks that were abolished.

Perhaps, in a crisis, with diminishing options, the government will find the courage to shutter a third and reissue Treasury notes backed by tax revenue and gold. It’s a thin hope. But history tells us that the alternative is escalating monetary and fiscal stimulus, economic chaos, and war.”

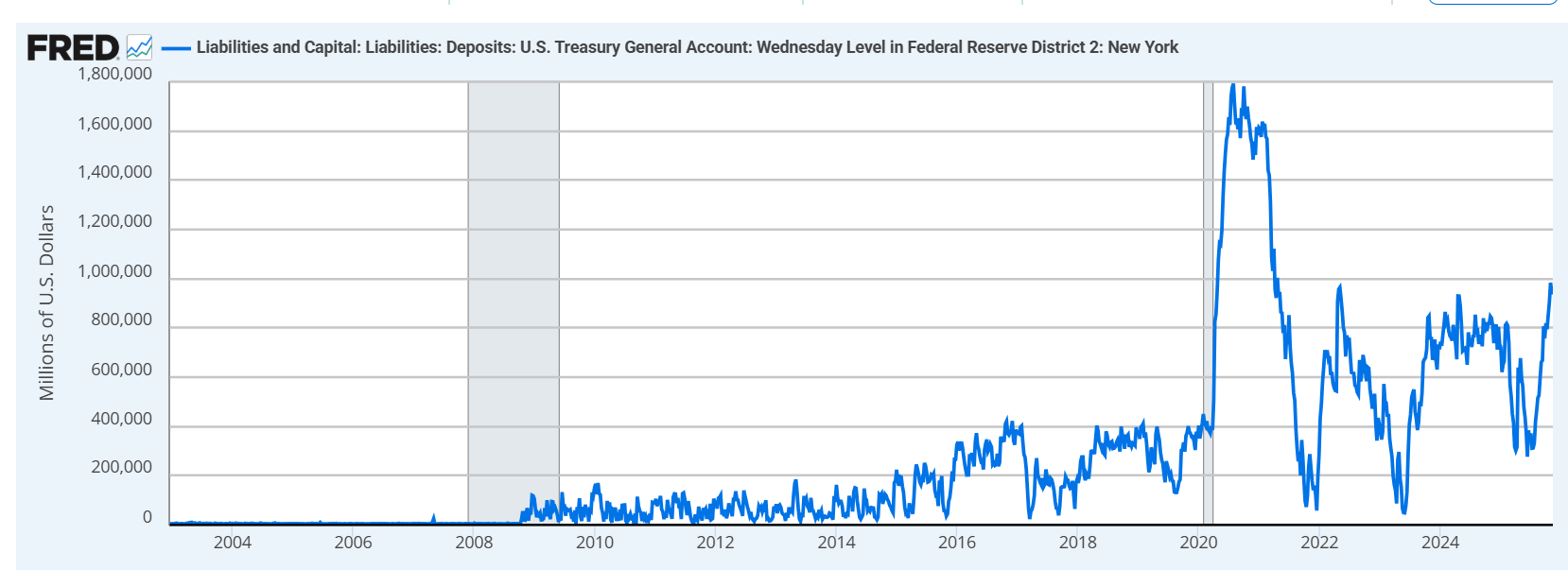

“TGA (The Treasury General Account) goes up, bank reserves go down, financial conditions tighten. The TGA goes down, bank reserves go up, financial conditions ease.”

Julia La Roche (Chris Whalen agreed)

Luke Gromen and Danny Moses

Moses: “John Williams, head of the New York Fed - I’m sure you saw this, you probably wrote about it - spoke in Germany last week, and it was to marry what you just said about the stock market wealth effect, and what it might be, he said, quote, “I am closely monitoring a variety of market indicators related to the Fed funds market, repo market and payments to help assess the state of reserve demand condition.” He cautioned that buying bonds to maintain the right amount of liquidity is not stimulus. I argue it is stimulus…what are your thoughts on that?”

Gromen: “It is 150% stimulus, he’s full of crap is my reaction. The reason I say that, and this is where I disagree with a lot of the purists on this - they say, “Well, QE is technically bringing down rates, you know, at at the mid to long end to drive.” What they all almost all uniformly failed to mention is where it does bleed into the economy.

We’re running still nearly $2 trillion deficits and we’re financing a big chunk of it in bills. And so if you’re buying bills to prevent rates at the short end from from rising, be that on a spot basis through standing repo or be that on some sort of program to make sure bank reserves are high enough, because, oh, by the way, bank reserves get drained down when banks buy this stuff. You are financing deficits and those deficits are being spent into the economy.

Oh, by the way, when you are buying, you know, when a government runs a deficit and then finances it in short-term markets, that is very cash-like, right? So a dollar bill is just a 0% yielding bond of zero duration. That’s why it says Federal Reserve note on it. And so if you’re issuing bills and the Fed’s buying those bills with money they’re creating, you are essentially funding the government with a close relative of cash. Particularly the closer the rate on those bills gets to zero. What’s the difference between a bill yielding, you know, 25 basis points for three months and cash yielding 0% now? My point is that’s Weimar-like. That’s banana republic-like. If you’re going to run 7%, 6% of GDP deficits, and you’re going to finance it heavily in bill markets that the central bank’s going to buy, that’s as stimulative as it comes.”

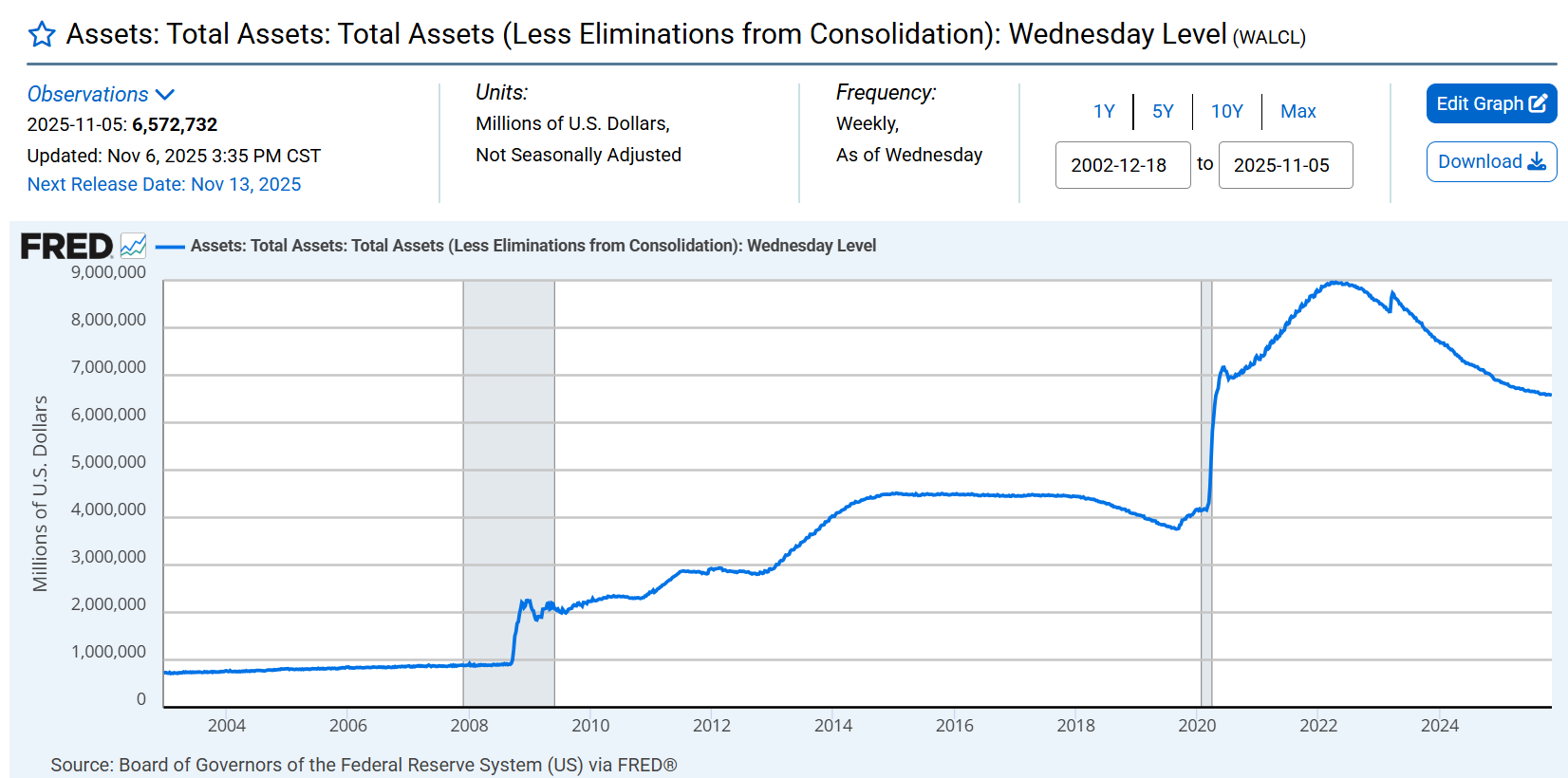

“QE is happening as we speak. I mean, I don’t have to look at the Fed balance sheet. By the way, if you look at the chart of the Fed’s balance sheet from the St. Louis Fed, it looks like the best chart you want to own. It’s kind of smoothing out here, flattening. It looks like it’s going to move higher at 6.6 trillion.”

“There is a massive gap between western policy makers and most western market participants and the reality of what it takes to build a supply chain.”

2025 Financial Stability Report

For insomniacs. Here are a couple charts that jumped out at me:

Melody Wright

“…the numbers that were being published for what was available for sale or permitted in no way matched what I was seeing on the road. We also had heard from an anonymous xTwitter account who claimed to be in new home sales that the builders were urging sales folks to get the initial contract signed even if they knew the borrowers would not qualify. In builder world, sales are tracked by that initial contract signing versus a closed sale. Shockingly as well, those at the Census who gather the information in the Survey of Construction don’t go back and revise those numbers for cancellations. The reason? Too hard to independently verify. Just as FRED relies on Realtor.com to provide listings for sale for its data series, the Census relies on industry insiders to tell them the state of things in the new home market…

Government has been intervening in housing for quite some time. We have reached the point where we have moved from the law of diminishing returns to one of no returns. This market has been subsidized to death. If indeed we are living in the strongest economy ever, why would we need a 50-year mortgage? As I asked on xTwitter are we now admitting we are in a silent depression?

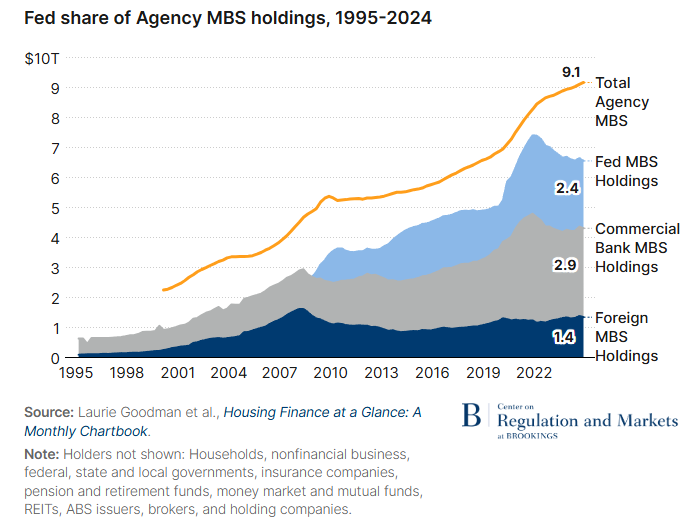

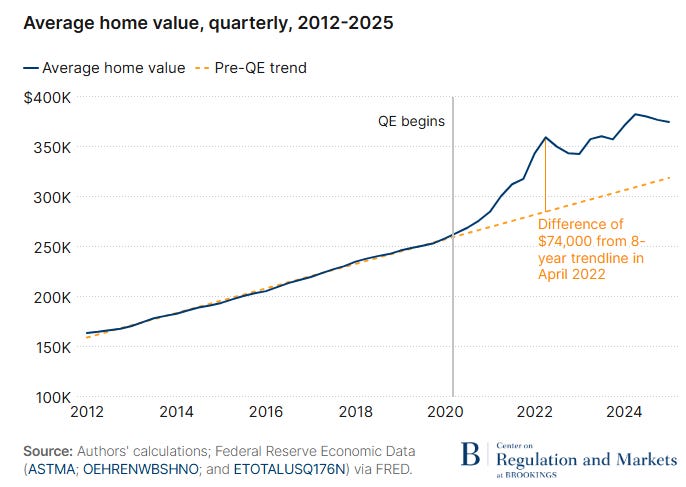

Quantitative easing and housing inflation post-COVID

The Fed’s quantitative easing (QE) resulted in the Fed buying nearly 90% of the increase in eligible mortgages from 2020 to 2022

A massive increase in house prices coincided with the Fed’s QE, translating into higher housing inflation

Housing was a key component of the post-COVID inflationary episode and kept overall inflation above the Fed’s 2% target

The assumption that buying mortgages as part of QE has no relationship with house prices should be reconsidered for future monetary policy responses to recessions

Remember, this is from Brookings, which is about as pro-Fed as it gets:

This paper argues that one factor that has been underappreciated in causing housing inflation is the Fed’s large-scale purchases of MBS. The Fed purchased nearly 90% of the growth of GSE MBS during the two-year period of QE. The purchases depressed mortgage rates, leading to increased housing demand and house price appreciation. During this period, American home values rose sharply, with the average home value rising nearly $100,000, of which nearly 75% was above the pre-pandemic trend. MBS purchases through QE highly correlate with this period of above trend house price appreciation. Following the end of QE and subsequent interest rate hikes, house prices plateaued.

The theory behind QE largely ignored the asset-specific price effects from asset purchases, possibly because economists assumed investors would rebalance and spread out yield impacts evenly to other assets. However, actual implementation of QE by the Federal Reserve during the COVID pandemic resulted in a near total purchase of the available market of MBS by the Fed. It is difficult to set aside the basic laws of supply and demand and not suppose that an over $1 trillion purchase of a financial product, nearly 90% of the growth in the available supply, did not cause the sharply higher asset valuations observed, especially when the underlying housing stock is constrained in the short-term.

If correct, the Federal Reserve needs to reconsider how it operates QE, taking into account the impact of purchasing MBS on the housing market and the feedback loop between housing and inflation. Housing is the largest component of inflation, itself meriting special attention. In less than the first quarter of this century, QE had gone from a theoretical debate to a “break the glass” implementation response to the last two recessions. Given the frequency of QE and the unique nature of the first recession’s epicenter on housing and the second’s inflation episode, it is critical that more work be done to understand the ramifications of large-scale mortgage asset purchases by the Federal Reserve.

No accountability, ever.

Great News!

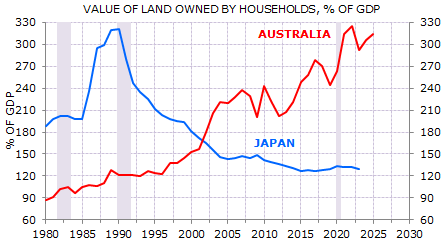

Meanwhile, in Australia…

“As illustrated below by independent economist Gerard Minack, Australia’s total residential land valuation as a percentage of GDP is now on par with Japan’s at its peak during the late 1980s land bubble:”

Cockroaches

Scaramucci’s ‘Opportunity Zone’ Bet Likely to Be a Loss for Clients

Hedge fund investor Anthony Scaramucci’s firm sent a letter to clients in his so-called opportunity zone fund with a sobering message: You’re likely facing a total loss.

The fund’s one investment, a Virgin Hotels property in New Orleans’ Warehouse District, had already been underwater. But in September, Scaramucci’s SkyBridge Capital learned the asset was valued at less than half of earlier appraisals. It wasn’t practical to refinance, and the hotel had to be sold.

If the property fetches its broker’s estimate of roughly $43 million, then clients “will likely suffer a complete loss of invested capital,” SkyBridge wrote in the letter….

The poor performance has caused some tense moments among investors and hedge fund executives. One client sent a one-sentence email to two SkyBridge employees in August asking about the results of the share sale and how much it would dilute current holdings, according to messages seen by Bloomberg News.

The investor received this response from SkyBridge President Brett Messing: “given your intemperate and unprofessional communications and false and offensive accusations, we will not be responding to your inquiries, questions or requests anymore.” [Wow. Sounds like an Enron or Lehman call.]

UBS Winds Down O’Connor Funds in Sign of First Brands Strain

UBS Group AG is liquidating two invoice finance funds with exposure to First Brands Group, in an early sign of how large financial institutions are dealing with the fallout from the bankrupt auto-parts supplier’s collapse…

UBS emerged as one of the largest creditors to First Brands, which filed for bankruptcy in September and revealed that its sprawling network of auto-parts factories and distribution centers was on the hook for over $10 billion…

“It’s always unfortunate when clients suffer losses”

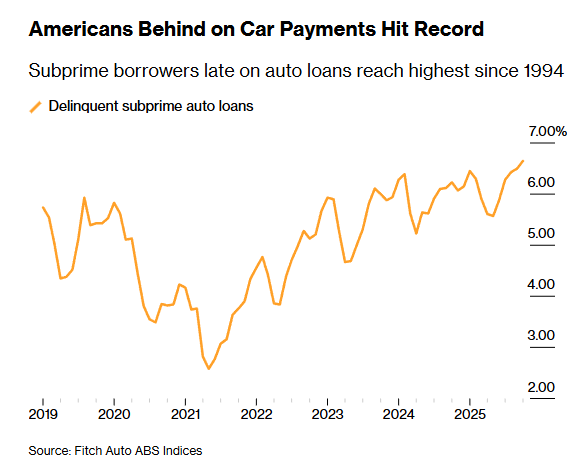

Car Loan Delinquencies Hit Record for Riskiest Borrowers

“It’s been a little bit difficult maintaining it with the car insurance, the maintenance and my car loan,” Neal said. “I’m usually about 30 days late.”

“My principal hasn’t even really moved in two years,” said Langhoff, who works as a manager at McDonald’s. “Because once you fall behind, then you have the late fees and it’s hard to catch up.”

The FT tackles the recent First Brands, Tricolor, etc. kerfuffles2:

Here is Michael Arougheti, the CEO of Ares Management:

These events appear to be idiosyncratic and isolated and not the sign of a turn in the credit cycle. From our vantage point, our credit portfolios also remain healthy, and we’ve not seen any deterioration in credit fundamentals or changes in amendment activity that would indicate a turn in the cycle is coming . . . we continue to see healthy year-over-year double-digit Ebitda growth across our US direct lending strategies

And here is Marc Lipschultz, CEO of Blue Owl Capital:

Broadly speaking, we do not view the events that have unfolded for those companies as canaries in the coal mine for the health of the private credit markets…

The health of our credit portfolio remains excellent with an average annual realised loss of just 13 basis points and no signs of meaningful stress. In direct lending, the modest level of non-accruals we have seen are not thematic in nature…

Finally, here is Marc Rowan of Apollo:

From my point of view, credit is credit, whether it’s originated by a bank or an asset manager. It makes almost no difference to me. There are fundamentally good underwriters of credit and there are less good underwriters of credit. The observed outcome of the number of articles and the focus on a couple of isolated incidents in the marketplace is nil. Ten basis points of spread widening is essentially nothing.

Private Credit and Insurance Companies

By value, global private assets under management came to just over $13tn in 2023, having more than doubled in size over the previous five years, according to a recent report by financial data firm Preqin. It estimated that this figure is on track to almost double again by 2030. The vast majority of these holdings are private equity assets, though the growth of private credit has been explosive. To put these numbers into perspective, Bain & Company estimates that the total assets under management in the global asset management industry for 2023 totalled $115tn.

But while the lack of data transparency makes it hard to say anything with confidence, it’s not obvious that this growth poses immediate direct risks to the banking system. Good data as to how much banks lend to private market entities in general, or even private credit firms specifically, is scarce. However, the IMF’s Global Financial Stability Report from April 2025 highlighted a Moody’s report that estimated bank exposure to private credit funds was $525bn at the end of 2023.

That $525bn sounds a lot. But global banks are huge. As Moody’s puts it, exposures are moderate with private credit loan commitments about 3.8 per cent of total loans on average in 2023. So sure, private credit managers could start making terrible loans that default but this scenario doesn’t look like it would immediately blow up the banking system — although the use of “synthetic risk transfers” which enable banks to transfer credit risk on diverse loan pools to investors (typically credit funds and asset managers) may complicate the picture.

If there is a problem, it looks more likely to crop up in the insurance sector. Private credit now accounts for more than 35 per cent of total US insurer investments and close to a quarter of UK insurer assets.

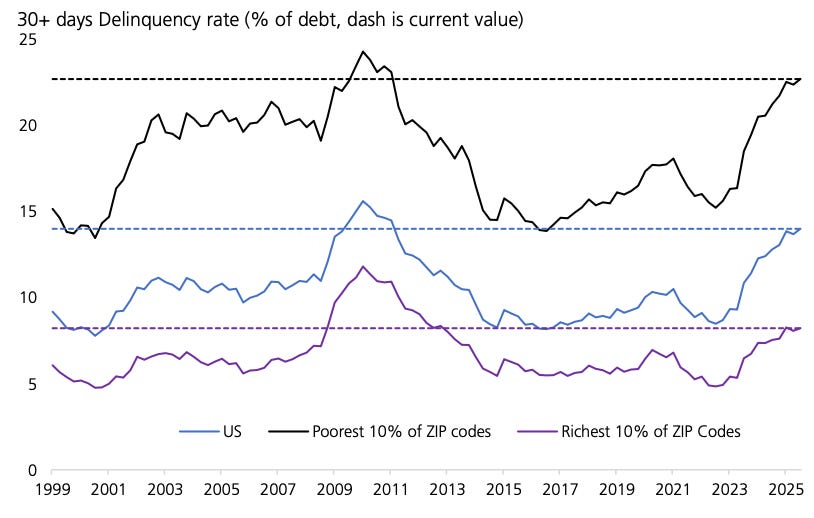

“Federal Reserve credit card delinquency data, which shows financial stress for lower-income households and even the U.S. average now topping Great Financial Crisis levels. Yet among the wealthiest households, those same signs of strain have yet to materialize.”

Blackrock is “facing heavy losses after its shadow banking business fell victim to an alleged $500m (£380m) fraud. BlackRock’s private credit investment arm, HPS Investment Partners, has started legal action to recover loans it made to a US telecom firm, which has been accused of faking payments from customers.”

BlackRock Eyes 100% Loss on Private Loan Amid Debate Over Marks

“About a month ago, BlackRock Inc. deemed the private debt it had extended to Renovo Home Partners, a struggling home improvement company, to be worth 100 cents on the dollar. As of last week, the firm had a new assessment: zero.”

Whenever I see a company go bankrupt, I look for two words:

“The drastic revision comes as Dallas-based Renovo — a roll-up of regional kitchen and bathroom remodeling businesses created by private equity firm Audax Group in 2022 — abruptly filed for bankruptcy last week, indicating it plans to shut down.”

“While the Renovo debt represents a sliver of total assets for the three lenders, its sudden collapse strikes at the heart of what critics see as a major vulnerability in the private credit market: the disconnect between the valuation of illiquid loans and the performance of the underlying companies…

“We view this outcome as a result of issues specific to the issuer, rather than a reflection of broader sector weakness””

A post from LinkedIn by a guy whose dad founded Reborn Cabinets:

Some posts are hard to write. This is one of them.

💔The End of One Chapter — and the Beginning of Another

In 1983, my father had a dream — to build a small kitchen remodeling company in Southern California.

That dream became Reborn Cabinets.

Over 42 years, we grew from a family business into one of the largest kitchen and bath remodeling companies in the country.

We built something special — a company grounded in craftsmanship, integrity, and care for people.

Today, I woke up with a heavy heart realizing that Reborn Cabinets, along with several sister companies founded and led by close friends, has come to an end.

💔Over 2,500 employees and their families will be impacted.

💔 Thousands of homes are left unfinished.

💔 Vendors and partners we’ve known for decades will walk away empty-handed.

When we sold Reborn Cabinets to private equity in 2022, we truly believed it was the best way to secure its future — for our people and the legacy my father built.

Sadly, that’s not what happened.

This is what happens when leadership loses sight of what matters most.

When people think they’re “smarter” than those who built the foundation. When money and a spreadsheet become the only focus.

To every employee, customer, and partner affected — I am deeply sorry.

This is not how this story was supposed to end.

I stepped away as President of Reborn Cabinets and Dreamstyle Remodeling at the end of 2024, unable to keep watching what was unfolding.

Over the past few years, I’ve learned how private equity really works — and how easily great companies can be destroyed by the wrong hands.

Alternative hospitality company Sonder Holdings will immediately wind down operations and plans to file for Chapter 7 bankruptcy, it announced Monday. The operator of short-term rentals, which had about 8,300 units at 152 properties as of June, cited “severe financial constraints” from factors including challenges integrating its systems and booking arrangements with Marriott International…

Launched in 2014, Sonder sold short-term stays in hotels and apartments. Its business model has been to enter long-term leases with apartment and hotel owners, taking up blocks of rooms or whole buildings, then renting those out as short-term rentals on its platform. A guest staying at the Sonder Flatiron in New York received an email Sunday afternoon asking him to vacate the property by 8 a.m. Monday…

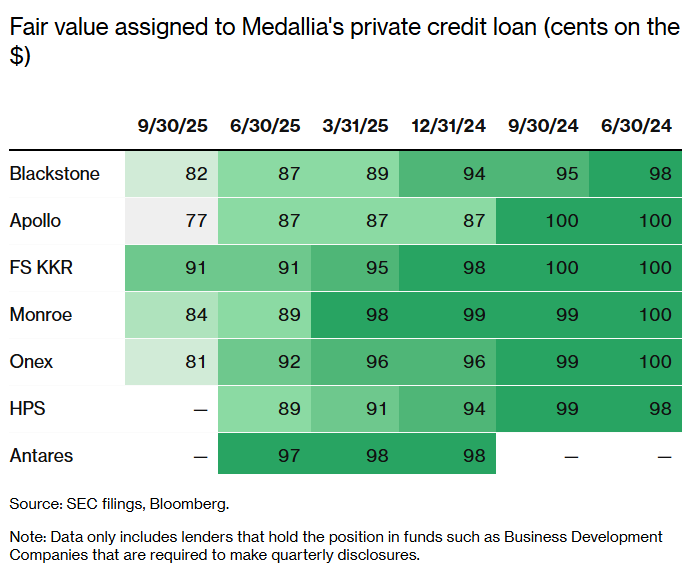

Apollo, KKR See Record-Wide Gap on Valuing Stressed Private Loan

An Apollo Global Management Inc. private credit fund deemed a loan to Medallia Inc. worth 77 cents on the dollar, a level typically considered distressed. A rival fund co-managed by Future Standard and KKR & Co. offered a very different assessment: 91 cents.

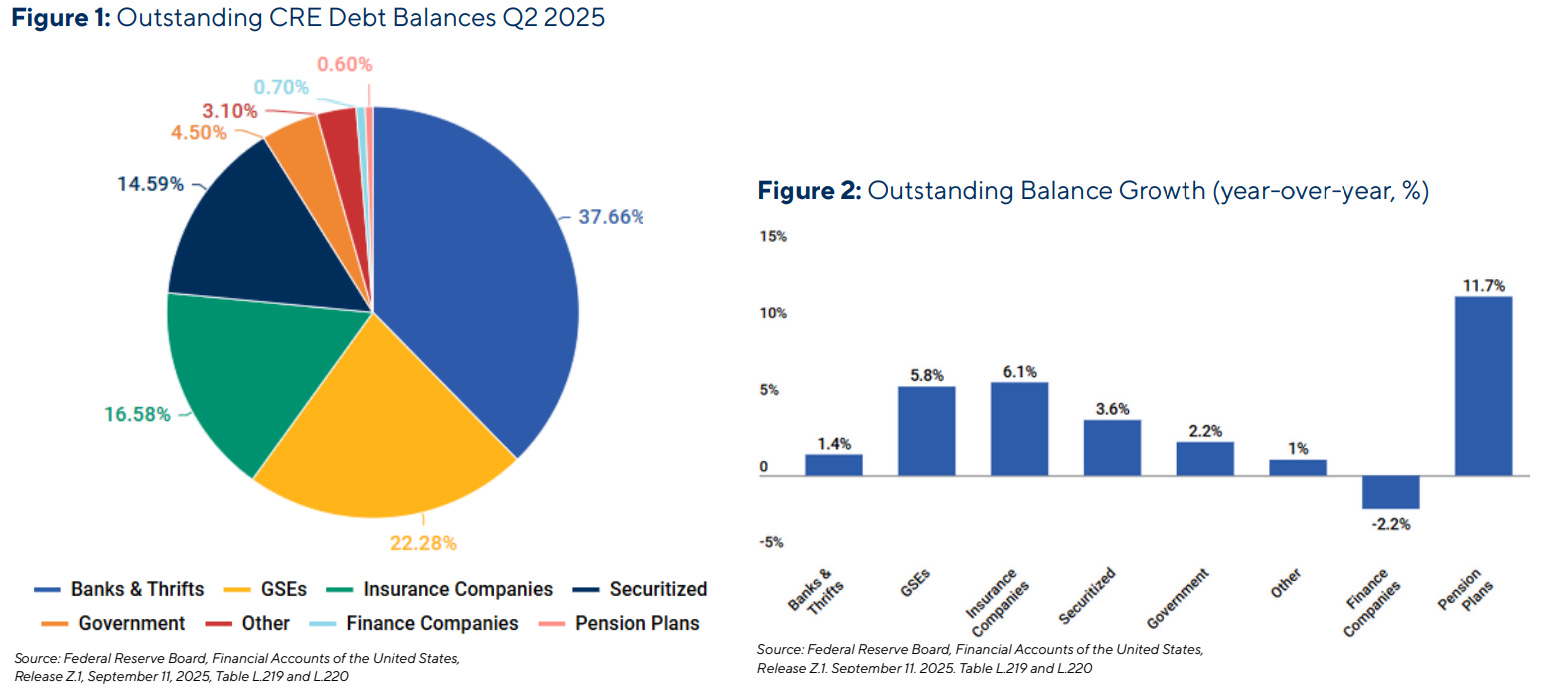

Inside the $4.8T CRE Debt Universe

Dan Zwirn

“The latency between the diminution of value…and when it is known to stakeholders involved or invested in that value, has never been longer, and the innovation that has been employed post-GFC to obfuscate the realization of value diminution has been really broad and multifaceted.”

“What happened in late 2021 will be stretched out over an enormous period of time, because that’s in the interest of policy makers and financial

sponsors. In the absence of something really extraordinary in terms of the left tail…it’s going to be very difficult for that not to be the case, because it’s in too many people’s interest, and you’ll just basically see continued debasement.”

“It turns out that if you’re a special kind of investor, like a bank, or sometimes an insurance company, you don’t have to recognize reality. You can say that I’m going to hold it till maturity, and I’m going to decide that this will never go down, even though the market’s telling you it is going down.”

US layoffs for October surge to two-decade high, Challenger data shows

“U.S.-based employers cut more than 150,000 jobs in October, marking the biggest reduction for the month in more than 20 years, a report by Challenger, Gray & Christmas said on Thursday as industries adopt AI-driven changes and intensify cost cuts…Not only did individual companies announce large layoffs in October, but a higher number of companies announced job cut plans, Challenger said, tracking nearly 450 individual job cut plans in October compared to under 400 in September.”

An A.I. gem via RealStockCats, who y’all should follow. Builder.ai:

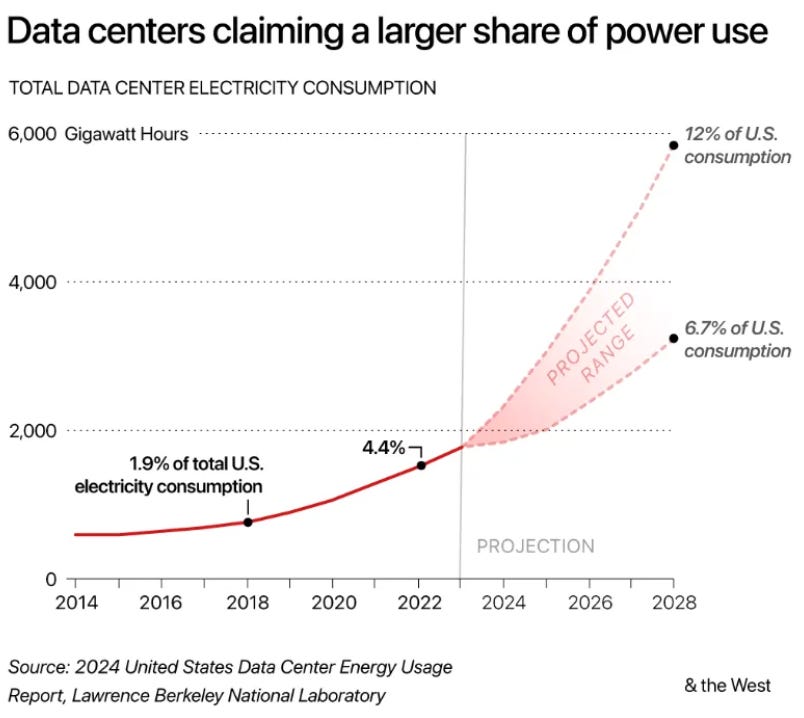

AI’s $5 Trillion Data-Center Boom Will Dip Into Every Debt Market, JPMorgan Says

You have to put all those Indians somewhere.

Nice thread from the excellent Unicus Research account:

“PSA: A.I is less likely to take your JOBS and more likely to take your BASIC NEEDS like water, electricity and land.”

New interview with Laks Ganapathi, founder and CEO of Unicus Research. I like her.

Has Ed Zitron Found the Fatal Flaw with OpenAI and Its Flagship ChatGPT? “If his finding is valid, large language models like ChapGPT are much further from ever becoming economically viable than even optimists imagine. No wonder OpenAI chief Sam Altman has been talking up a bailout.”

“A.I. bubble trouble talk is overblown”

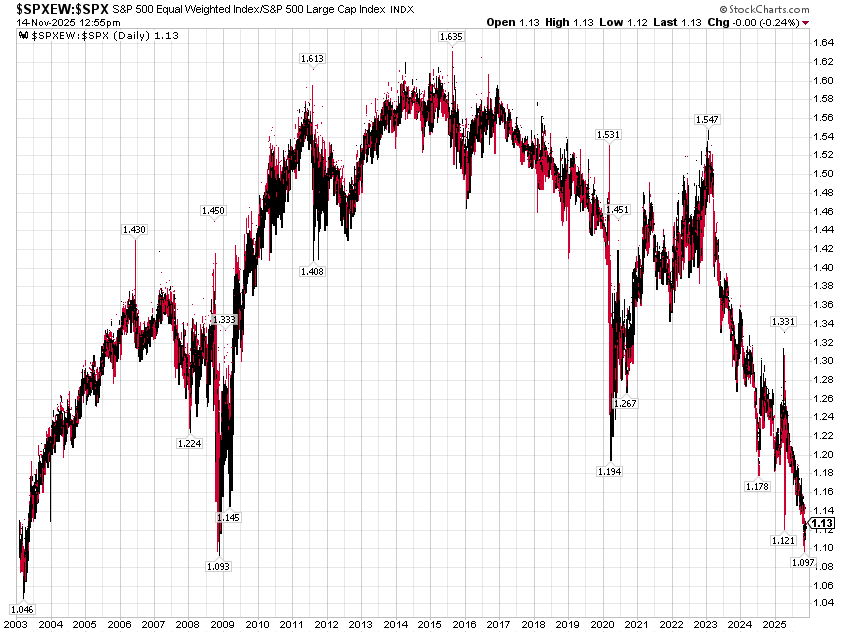

S&P 500 Equal-Weight vs S&P 500

As Dave Collum puts in, Mike Green has his passive pitch down to a science. Here it is from Macrovoices this week:

Well, I think the thing that you know I’m going to talk about is ultimately the most important factor that exists in the market. It’s just the mindless bid that continues to come from 401, K contributions, IRA contributions, money flowing into ETFs, mutual funds, etc. You know that money largely flows into the broad indices, the total market index, or the s&p 500, is really the single biggest beneficiary of this, and powers equities higher in a framework that is driven largely by momentum, but actually has some interesting characteristics, slightly different than pure momentum. It’s what I’m calling the passive factor, and my math suggests, unfortunately, that that is now adding about1200 to 1300 basis points a year in excess performance versus what you would expect under a mean reversion or a valuation dominated market.

And so, you know, a lot of what we are seeing is, unfortunately, just a statement of how we invest, which is passively through broad indices into retirement accounts. We don’t take that money out. That how we’re investing is a big deal. And then the fact that so many people are investing under a government sponsored enterprise is driving the price of financial assets higher regardless of what the Federal Reserve does, regardless of the money printer goes burr, etcetera. Those can have real market impacts, but they’re not the primary feature that’s behind all of this.

“Robinhood wants to allow amateur traders to invest in A.I. start-ups”

Robinhood plans to offer tradeable shares in a new fund managed by its subsidiary Robinhood Ventures, which will invest in a highly concentrated portfolio of five or more “best in class” private companies — and may borrow money to boost its return.

AAII Sentiment Survey. “AAII Bears is at 49.1%, while $SPX is within 1% of an All Time High. This is very rare: only happened 1 other time before this year. April 10, 2013 - $SPX rallied 18% over the next 12 months.”

But wait!

The Bitcoin

“For months, a small company in San Francisco has been pursuing a secretive project: the birth of a genetically engineered baby. Backed by OpenAI chief executive Sam Altman and his husband, along with Coinbase co-founder and CEO Brian Armstrong...”

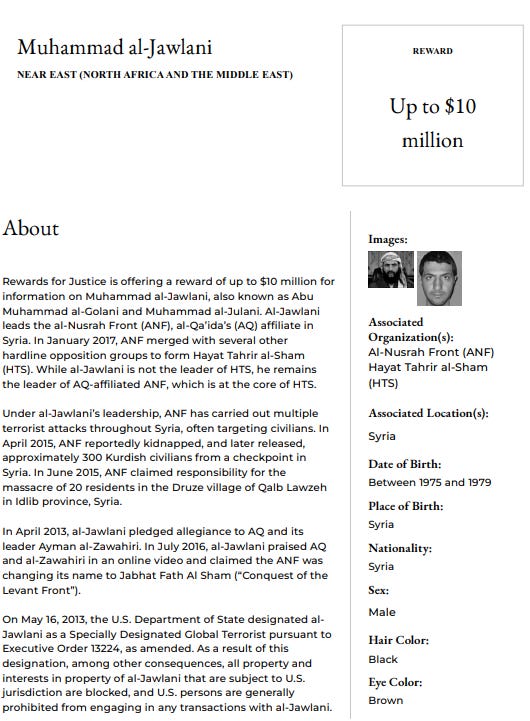

Al Qaeda invited to the White House

…In my opinion, you all are in the middle of a what I can only describe as a major and repetitive counter-intelligence operation by unknown multiple operators or organizations, and for unknown reasons.”

Please Gamble Responsibly

All three of these men were very close to Jeff Epstein:

The Blast Radius of Jeff Epstein

“The single most important neoliberal thinker of the last forty years - economist Larry Summers - had an extensive and deep political and personal relationship with Epstein…Summers and a bunch of powerful political elites are enmeshed in a scandal involving a network of, well, there’s no nice way to put it, globalist pedophile billionaires.”

Summers is like a particularly obnoxious Zelig character, who has promoted so many bad policy decision over the decades:

Under Clinton, Summers bonded with Alan Greenspan and Robert Rubin, the three men nicknamed the ‘Committee to Save the World’ by Time Magazine due to their ability to bail out U.S. banks involved in the Mexican and East Asian financial crises. Summers eventually worked his way up to Treasury Secretary, where he organized the deregulation of derivatives and the end of Glass-Steagall, helped broker the transformation of the Soviet Union into an oligarch dominated Russian state, and served as a key administration lobbyist for NAFTA and China’s entrance into the World Trade Organization.

After the Clinton administration, Summers became the President of Harvard University, perhaps the single most influential role in U.S. civil society, before serving as a managing director of the hedge fund D.E. Shaw for a few years. He was still heavily involved in central banking policy, influencing financial regulators to ignore speculation and fragility in the financial system. In 2005, at the Jackson Hole conference of central bankers, he famously mocked the idea that the U.S. financial system was heading for a fall, calling one prescient economist who predicted the crisis a “Luddite.”

Today, Summers is a professor at Harvard, the Vice Chair of the immensely influential Peterson Institute for International Economics, a distinguished senior fellow at the Center for American Progress, and a contributing writer at the New York Times. He’s also a board member of OpenAI, and has a well-trod path in finance and crypto.

And his disciples are everywhere. Sheryl Sandberg was his student and chief of staff. He mentored Obama CEA Chair Jason Furman. Former Treasury official Natasha Sarin was his student. The rumors were that he controlled access to a number of key economic journals, which meant that he was in charge of the careers of young economists.

Summers serves as the most important validator for capital, never wrong but never in doubt, an excellent organizer and politician whisperer, and deeply corrupt.

“Now, however, there’s a scandal that is hard to deny. Summers had a longstanding and well-known relationship with Epstein…Summers asked Epstein for helping raising money for his wife’s poetry nonprofit. He flew to Epstein’s island four times on Epstein’s private jet, nicknamed the “Lolita Express.””

I’ve been ranting against Summers forever. Great write-up by Stoller.

“All-in works until it doesn’t.”

Attributed to Chip Reese

If anyone has too much Bitcoin and would like to send me some, I’m willing to help.

Thank you for your attention to this matter: bc1qkvxy0f8tnxnjddwtyg3jshwgck4e9haw8e8kf9

Inflation is also a default.

I’ll just note that over the years I’ve found FT columnist Robert Armstrong to be one of the most insufferable financial “journalists” around, and that’s saying something.

See also More High Strangeness

Thank you! Just what I needed to start my Monday morning!

Around halfway through, when you quoted two execs from Ares Capital and Blue Owl, I thought, the simple solution to all these shenanigans is 'skin in the game'. This should be applied to both the private and public sector.

Those involved in decisions that go bad should feel some part of the pain, otherwise the incentives for preventative risk mitigation simply can't be aligned. Even dreadful instruments such as private equity could be beneficial in specific circumstances, provided those involved know the risks. The breadcrumb trail leads back to the limited liability idea and false equivalence of corporations being persons'. All this is wishful thinking unfortunately.

It's hard to see an easy way out. Perhaps if the policy prescriptions of the 07-08 GFC had been different, if the boom and bust cycle had been allowed to play itself out, the risks today would be in a range of a different order of magnitude.

I think the idea of abolishing the Fed to create a new Fed has legs. Like issuing a new currency, if the sinking of the ship gets out of hand, at some point they'll start throwing everything at it in the hope something sticks.

Great stuff!

Excellent and thank you! Packed with great stuff but that Tony Deden excerpt was stellar.