The Hollow Men

"The ultimate result of shielding men from the effects of folly, is to fill the world with fools."

A relatively short note tonight. I will hopefully be posting a new podcast tomorrow, which I intend to annotate, so stay tuned…

We identify occupancy fraud — borrowers who misrepresent their occupancy status as owner-occupants rather than investors — in residential mortgage originations. Unlike previous work, we show that fraud was prevalent in originations not just during the housing bubble, but also persists through more recent times. We also demonstrate that fraud is broad-based and appears in government-sponsored enterprise and bank portfolio loans, not just in private securitization; these fraudulent borrowers make up one-third of the effective investor population. Occupancy fraud allows riskier borrowers to obtain credit at lower interest rates. These fraudulent borrowers perform substantially worse than similar declared investors, defaulting at a 75 percent higher rate. Their defaults are also likelier to be “strategic,” suggesting that they pose a risk in the face of declining house prices.

"The Fed had unique authority...since 1994 to regulate every single mortgage lender in America."

Thank you, Tyler Cowen.

The Obama Factor : A Q&A with historian David Garrow I will be referring to this gem in the future.

What do the Obamas and their circle have in common with each other? They are Ivy League people, who ran away from whatever they came from in order to become members of the credentialed elites, whose loyalty is to the system that gives them prestige—or rather, gives prestige to their degrees, of which they are the holders. Once they pair off and reproduce under the seal of Harvard or Yale, they may find it seemly to donate money to an NGO that offers microloans to female entrepreneurs in Pakistan. So why should Obama, the ultimate winner, carry on the charade that he’s part of a community, whatever that means, with these people? He’s happy to go on NPR and talk about meaning or Marilynne Robinson novels or whatever, to make the wine moms identify with him, so he can put one over on them. Just don’t ask him to visit the hospital when you get cancer, because he’ll be hanging out on someone’s yacht, with the other winners…

They’re all hollow. That’s what the system produces.

Between the idea

And the reality

Between the motion

And the act

Falls the Shadow

"According to Redfin, the cost of a starter home in San Francisco decreased 13.3% to $910,000; in Austin, decreased 12.2% to $347,300; and in Phoenix, decreased 9.7% to $325,000."

That’s roughly >7x, 4x & 5x median household incomes.

A $900k "starter home. Meanwhile, not long ago…

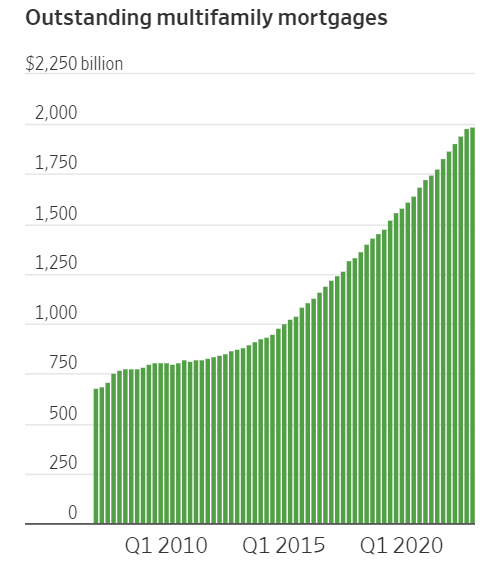

Apartment buildings, long considered a real-estate haven, are emerging as the next major trouble spot in the beleaguered commercial-property world. Investors bid up the prices of multifamily buildings for years, attracted by steadily rising rents and the prospect of outsize returns. Many took on too much debt, expecting they could raise rents fast enough to pay it down…

The sudden surge in debt costs last year now threatens to wipe out many multifamily owners across the country. Apartment-building values fell 14% for the year ended in June after rising 25% the previous year, according to data company CoStar. That drop is roughly the same as the fall in office values…

Outstanding multifamily mortgages more than doubled over the past decade to about $2 trillion, according to the Mortgage Bankers Association. That is nearly twice the amount of office debt, according to Trepp. The data provider adds that $980.7 billion in multifamily debt is set to come due between 2023 and 2027…

Inflation also allowed landlords to raise rents higher than usual, which boosted the values of their buildings. Asking rents rose 25% over 18 months spanning 2021 and 2022

This is why Barry Sternlicht wants a return to ZIRP and QE - to massively raise your rents again.

Bank Stocks Slide After Moody’s Downgrade “The ratings firm also pointed to the prospect that a recession in early 2024 could erode demand for loans and lead to loan defaults. Banks could be hit by problems in commercial real estate, the firm said, including higher interest rates, vacant offices due to the shift toward remote work, and reduced availability of credit.”

Delinquency Rate on All Loans, All Commercial Banks

Chris Bloomstran's Berkshire Hathaway 2023 Q2 Earnings Thread

Chris is one of the sharpest analysts around.

Berkshire reported 2Q results this morning. As always, there's more under the hood than the reported results. A few thoughts on what is a very mixed bag. BRK is a good proxy for the US economy. The industrial economy is weak, consistent with what other companies are reporting. 1/

For starters, operating income was $10.0 billion for the quarter, up 6.7% over 2Q 22 and up 9.2% for six months. However, properly excluding forex gains on non-US denominated debt, profit rose from $8.3 billion to $9.6 billion in the quarter, up 15.2% and 17.9% for six months. 2/

However, much of the increase came from income on Allegheny's acquired assets in October and from BRK's now 80% investment in Pilot, up from 38.6% (5 months consolidated and 1 month equity method). Higher interest income on a larger cash balance further drove much of the gain. 3/

Headlines report on BRK's cash mountain, $147.4 billion up from $128.6 billion at yearend. For perspective, at 14.2% of total firm assets (now over $1 trillion for the first time!!!), cash as a proportion of assets is in line with the past 25 years and below 2016-2021 levels. 4/

The railroad is noticeably weak with revenues down 11.6% on 11.1% lower volumes, driving pre-tax earnings down 25% and 18% in the quarter and six months, respectively. Labor increased 14% in 2Q. BNSF volumes shipped were down across the board. Intermodal weak on lower imports. 5/

Trucking taking share from rail on lower spot rates. Industrial, ag, coal vols all down. Chemicals, plastics, lumber shipments all weak. Higher interest rates are hammering residential construction. You can also see it in BRK's housing-related subs, Clayton, furniture. 6/

The new vehicle auto market is strong. BNSF auto shipping volumes up. Can see it at BH Automotive, new auto sales up 13% though used car sales down over 8%. Overall BNSF was weakening in 2022 and still declining. The industrial economy and consumer are weaker than believed. 7/

Profits flat and durable in BH Energy. Continued growth capex in renewables driving a higher asset base with good subsidized returns. The tax rate remains remarkably negative at -61%, though not as negative. BHE's real estate broker volumes (down 26%) and profit way down. 8/

In insurance, GEICO positive $1 billion swing in underwriting profit in 2Q, earning $514 million versus a $487m loss y/y. 6-month profit $1.22 billion v $665 million loss. Higher pricing driving the improvement. Huge correlation between advertising spend and policies in force. 9/

Premiums written in dollar terms flat. Premiums per policy up 16%. Lower ad spend drove 2.7 million decline in policies in force, down a stunning 14.4%! GEICO cut ad spend 40% in 2022 and continues to shrink. PGR also cutting ad spend. Expect higher spend as profit evolves. 10/

Alleghany's 3 insurers, TransRe, Cap Specialty and RSUI all adding premiums to the BRK reported numbers. BH specialty and direct also growing. In reinsurance premiums written up 12% excluding TransRe. Pricing remains favorable. Nicely profitable in reinsurance and primary. 11/

Precision Castparts turning the corner and a bright spot. Sales up 29% and profit up 32%. Materially higher demand in aerospace and even the energy/turbine business. Volumes down at Lubrizol, Clayton Homes, building products (Shaw, Johns Manville, Acme, Benjamin Moore. 12/

Also weak comp volumes at Forest River. Backside of demand surge in pandemic. RV sales down 34%. Apparel and footwear down 13%. Duracell weak - down consumption and also market share loss to cheap battery brands. Home furnishings volumes down with sales down 5%. 13/

A bit of useless but fascinating trivia- With Pilot now consolidated, Pilot and McLane revenues of $27.6 billion are 30% of $92.5 billion quarterly firm revenues. Low margin, high volume businesses of course. Profits are less than 3% of pretax income of operating businesses. 14/

On capital allocation, share repurchases down from $4.45B in Q1 to $1.4B in Q2. Over $1B of the quarterly repurchase was in June at higher share prices than in April or May. June's purchases at an average $504k per A share. Friday's close $533,600. Less opportunity elsewhere? 15/

Small additional repos in July to 7/26 of ~$100 million. Net sales in the equity portfolio $8B and $18.4B year to date. $7.4 billion purchases v $25.8 billion sales through June 30. Chevron trimmed by ~7 million shares. ATVI also trimmed. Additions to 5 Japanese trading cos. 16/

Debt outstanding at holding company reduced by net $4.1 billion. Issued $1.2 billion in Japan. Pilot $5.8 billion syndicated loans at 7%, not guaranteed by BRK, ditto for BNSF and BHE debt. Total firm debt now $84 billion. Against $147.3 billion firm cash, net cash is $63.4B. 17/

BRK is earning over $7B/year in interest income on its T-bill holdings, up for nearly nothing two years ago. Interest expense on debt outstanding is less than $4B pre-tax. Investments in fixed-income securities down to $22 billion from $25B at yearend. Included bonds from Y. 18/

Perhaps tells you what Omaha thinks about interest rates and inflation? BHE in particular continues to absorb growth capex. BHE+BNSF capex $5.7B 6 months to June. Expected full year $14 billion for the two. Capex at BHE still 2x depreciation expense. 19/

The stock portfolio earned about 20% to June 30, a return of roughly $59 billion with dividends, nearly all of which was Apple. Given net equity portfolio sales and the gain in Apple, the $177.6 billion AAPL position is now over half of the $353.4 billion equity portfolio. 20/

If including KHC & OXY common held but not OXY warrants, AAPL is > 48% of total equity investments. At 30x to earnings and weakening revenues, I'm back to baking in a ~$50 billion haircut to the valuation of the stock portfolio, all of which is Apple. High-class problem... 21/

All in strong insurance, little to do on cap allocation outside growth capex. Modest share repos. Net equity sales. Weak industrial and housing volumes. Growing dry powder. You get the sense Berkshire is waiting around for something to happen. It always does. Great quarter, guys.

The Case for Recession Is Wrong, 2008 Edition

We were already in recession when Donald Luskin wrote this in January 2008.

According to my model, stocks are dirt cheap on a valuation basis vs. rock-bottom bond yields. That tells me that even if Rosenberg is right, the coming recession could be a winner for stock investors.

United States NFIB Business Optimism Index

Home REIT sells 40 properties at hefty loss as crisis worsens

Home REIT sold 1.6% of its property portfolio for £4.8m, or an average loss of 61%

The company remains locked in a series of disputes with tenants about the state of its properties, while others tenants have been unable to pay their rent due to financial problems…Home REIT, which marketed itself to investors as a socially responsible investment, is also facing allegations of misleading shareholders.

It's a shame that Sachin Khajuria - as a longtime former partner at Apollo - wasn't asked about the firm's close ties to Jeffrey Epstein.

I prefer Tyler Durden to Tyler Cowen. Just sayin'

I think Olive Anthony follows your work. His viral song Rich Men North of Richmond has the following line in it: "I wish politicians would look out for miners and not just minors on an island somewhere". When I first heard it I thought, damn!, Rudy is writing songs now!

https://www.youtube.com/watch?v=sqSA-SY5Hro