The Sound of Silence

Central Bankers have no idea what they're doing

"When the President does it, that means that it is not illegal."

“Bush II, as president, legalized torture by Executive Branch agencies, and Obama, as president, confirmed that power by failing to prosecute Bush. Obama, as President, ordered an American killed, and neither Trump nor Biden rolled that example back. And naturally, both parties love calls for “increased security.”

All of these acts, and more, are available to an unscrupulous president. Problem is, most presidents are unscrupulous. Certainly all recent ones are. What did our elites think was going to happen — that only angels would win power?”

“One does not decide the truth of a thought according to whether it is right-wing or left-wing.”

So what happened to this guy?

Jimmy Kimmel's sole crime is that he wasn't funny.

More importantly, the Trump Administration's assault on the First Amendment is disgusting, and I will fight them on this until they come for me (again).

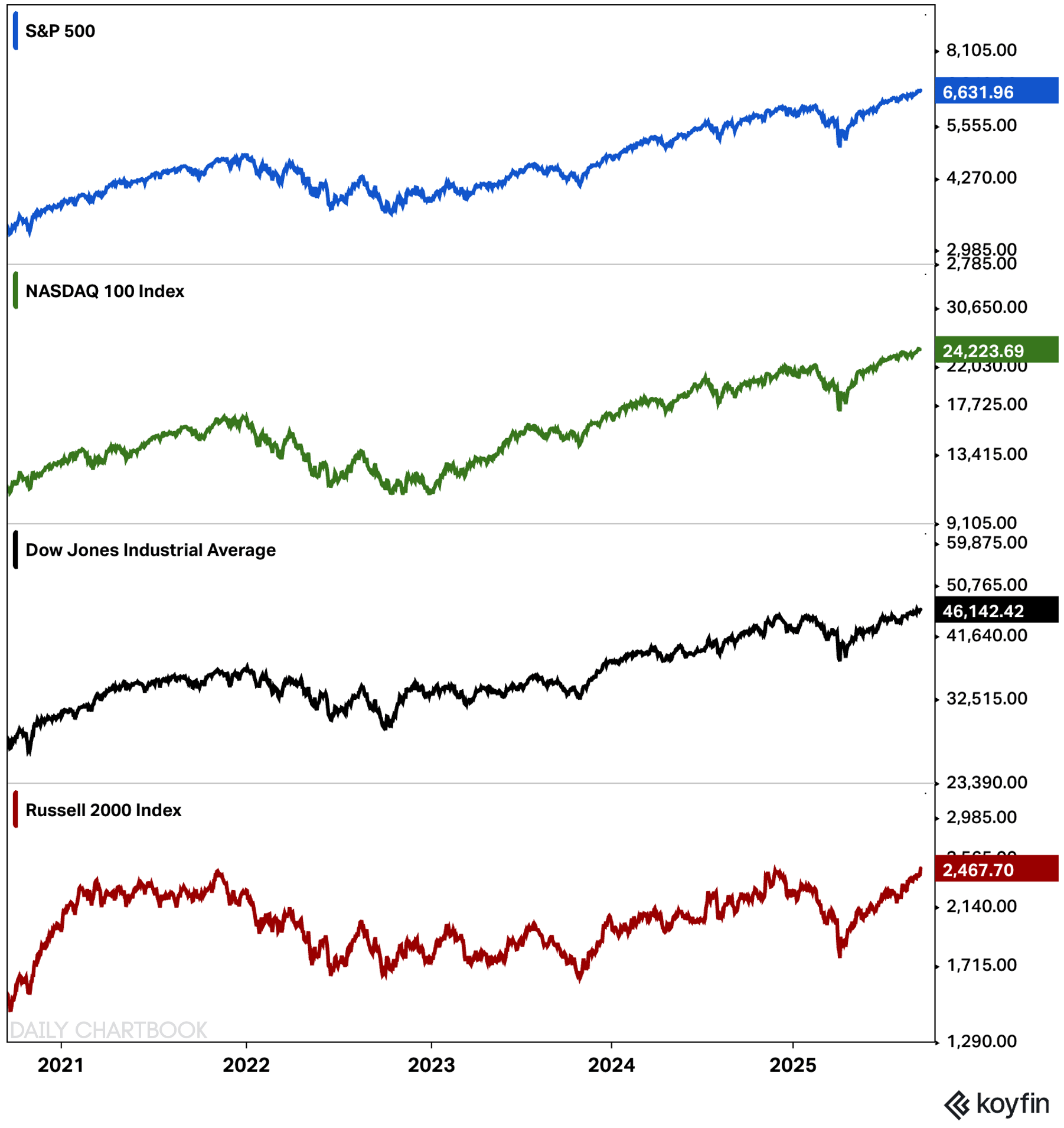

Meanwhile, “Quadruple all-time highs”…

”All 4 major indices hit new all-time highs today in unison for the first time since 2021.”

An update on Tricolor, which I mentioned in my last post:

Potentially massive fraud at Tricolor Holdings!

What Tricolor “was doing in effect was they were using government funds, government guarantees. They were using BlackRock money and other banks’ money to basically go out and sell overpriced used cars that were all beat up - basically pieces of crap - to take advantage of illegal immigrants. Okay?”

“BlackRock took a $90 million stake in Tricolor in 2021, which is about to be worthless”

Tricolor Bankruptcy Sets Up Fight for Auto Lender’s Assets After Alleged Fraud

In Dallas, the regional bank Triumph Financial Inc. has dispatched teams of employees to used-car lots, where they’re identifying and whisking away to safe locations the vehicles they believe are the collateral to their loans. In midtown Manhattan, a boutique investment firm that built a position in Tricolor’s asset-backed bonds, Clear Haven Capital Management, has been calling other bondholders, urging them to band together and fight to keep the big banks away from the assets that belong to them. Those banks, including JPMorgan Chase & Co. and Fifth Third Bancorp, have begun to forensically examine their own collateral to try to ascertain the magnitude of the losses…

Was there fraud, as federal investigators are now looking into, and how prevalent was it?

Signs are emerging that it may have been widespread. Banks are exploring whether the same collateral was pledged to multiple lenders, while Fifth Third said last week that it believes the so-called master loan tape — the files that list key information like outstanding balances, credit scores and vehicle types — was “corrupted.” People familiar with the probes say the suspected manipulation stretches back months, possibly longer. The final answers will go a long way in determining not just how much creditors will recover of the billions they’re collectively owed, but also which of them get paid first.

U.S. 30-Year Yield

Japan 30-Year Yield

Germany 30-Year Yield

S&P 500/S&P 500 Equal Weighted

The Value Line Geometric Composite Index is an "equally weighted index using a geometric average. Because it is based on a geometric average the daily change is closest to the median stock price change."

CRE

Adam Gower: “Are you seeing any distressed assets come to the market? What are you seeing?”

Reid Bennett: “We've completed over 455 BOVs (“broker’s opinion of value”) for lenders just in the Chicago market, in the Midwest market, because a lot of times lenders or banks want to reach out to brokers to get that. They don't want to necessarily pay for appraisals on these, especially when you're talking about hundreds and hundreds of units and buildings. So the 455 broker opinions of value that we've done in the last 18 months is 450 more than I've done in the previous 5 years. Right? So that could kind of tell you what's going on with the marketplace.”

On BOV’s: “I think they're trying to start getting a sense of where they sit in today's market, and what they're going to do. We've seen a lot of ‘um, alright. Thank you for the information.’ And then not much going on yet. They haven't figured it out yet. But it's coming…a couple of the deals that we're underwriting, we're not even coming to, you know, 60% or 70% of the loan on the books, and that's a problem.”

“Even here in Chicago, the asking prices on homes are 30% higher than they were three years ago.”

“This bill, that's now a law, one of the one of the things that it did was it it locked in the 100% bonus depreciation, which we saw in 2019, 20, 21, and 22, when it was at 100% bonus depreciation. We saw groups come in and stretch just to buy an asset that they could depreciate and wash some of their other gains and their other assets. We're seeing a little bit once that was was locked in, we saw a little bit of an uptick of excitement because people could take advantage of that which drives a little bit more activity.”

“We just sold a deal that had an assumable HUD loan that was 2.37% fixed until 2055. We got so spoiled with those rates that everybody's complaining and belly aching about 6% rates, which if you were talking to me in in 2006 or 2007, everybody'd be bragging about they got a six and a half percent rate.”

“We saw it in the GFC where it was the whole extend and pretend, right? We're seeing that now as well.”

“I will never invest in somebody that hasn't been through at least one downturn, right?”

“We always talk about 7 to 10 year amnesia in real estate. We all have it, right? We all we all forget like how painful it was seven or 10 years ago.”

“In Chicago right now, you see virtually zero tower cranes building apartment buildings, because they make it so difficult for the developers to develop deals, thinking that they're protecting their their constituents…in actuality, you want to have overbuilding…the rents drop when you overbuild, because now the developers have to compete with each other for tenants, so they have to provide better amenities, better service, at a lower cost for the tenants, which actually helps the affordability crisis in this country.”

“Office is, as a general rule, not the best thing going on right now. The values have gone down. Last number I saw since its peak right before Covid, property values nationally - this is nationally, US - down about 40% on an unlevered basis. So if you had some leverage on those investments, basically wiped out, right? In large part, which is why you've seen this absence of transactions for a long time in the office market, because if you're down basically all of your capital, there's a big incentive to say, well, let me just hold on and see if it comes back, because if I sell now, I've locked in this 100% loss.”

Single-Family

Only 24% of all buyers were first-time homebuyers in 2024, down from 32% in 2023 and well below the historic high of 50% in 2010.

Younger buyers are significantly impacted, with the average age of first-time homebuyers rising to 38—the highest on record.

“The typical homeowner now has a net worth that’s 43 times greater than that of the average renter, according to an analysis of federal data by the National Association of Realtors.”

“For a decade, the NY Fed has been asking renters about their probability of owning a home “at some point in the future.” The latest reading, from February, is the lowest on record. The typical renter pegged their chances of the American Dream coming true at just 33.9%.”

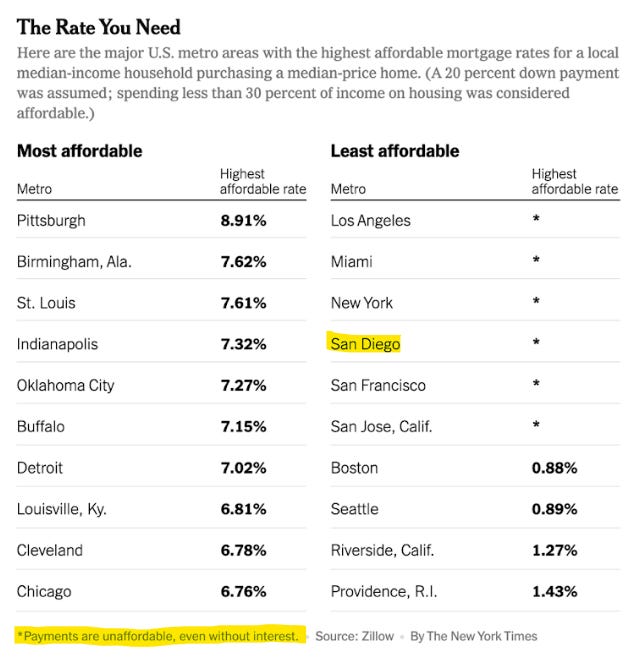

Prices are too high.

“Even if mortgage rates were zero, regular people could not afford to buy a home in San Diego” (and a number of other cities.)

“The NSDCC median sales price for July-August, 2025 was $2,399,500, which is 26% HIGHER than it was for the same two months in 2021.

It means our local real estate market is is totally dependent upon buyers coming from more-affluent areas, and those who inherit some the generational wealth transfer. How’s that coming along?”

‘They Couldn’t Afford Homes in the Big City. So They Left.’

“Some first-time home buyers, facing high interest rates, are trading their metropolitan lifestyles for lower-cost living.”

Pet Peeve: Rates are normal. Prices are high.

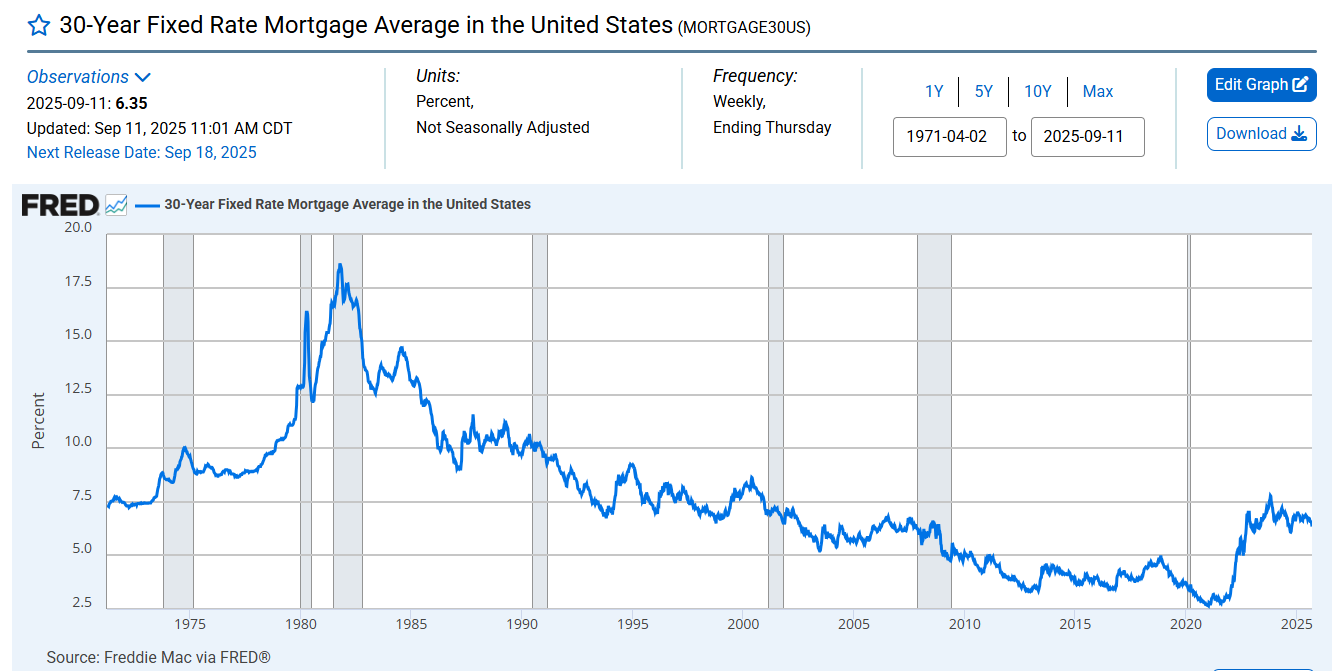

Mortgage Rates Are at an 11-Month Low. Will That Save This Housing Market?

Save the housing market?? Prices are still hitting record highs.

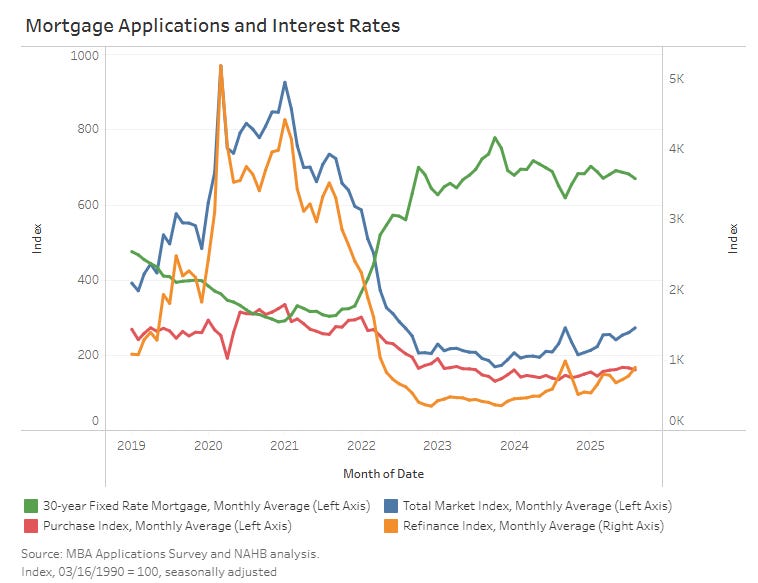

“The average 30-year fixed mortgage rate fell to 6.35%. That’s the lowest level since October and a notable drop from January, when rates were above 7%, according to Freddie Mac.”

“The average contract interest rate for 30-year fixed mortgages fell 13 basis points to 6.70%, the lowest level since November. Despite the decline, purchase applications slipped 3.0% month-over-month, while refinancing activity rose 15.6%. Compared to August 2024, purchase and refinance applications were up 19.4% and 16.9%, respectively.”

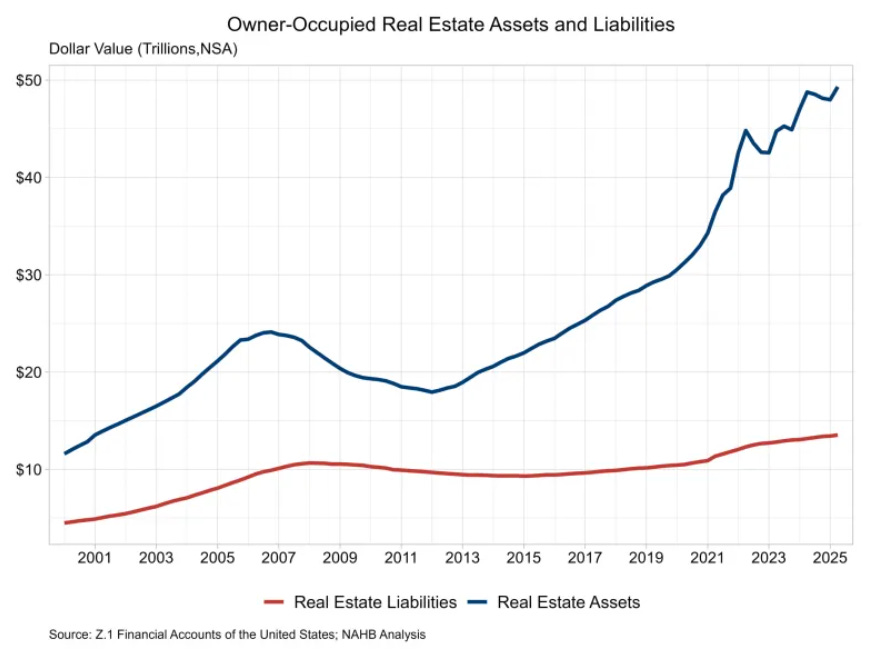

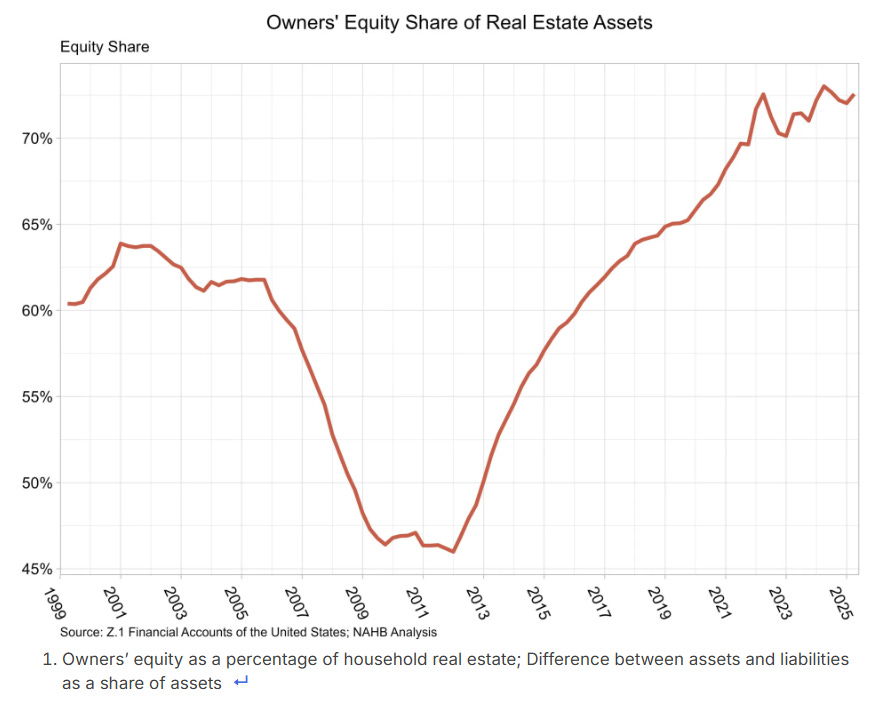

Household Real Estate Asset Values Reach New High

“Owners’ equity share of real estate assets was 72.6% in the second quarter, marking an increase in owners’ equity share from the first quarter. The share in the second quarter of 2024 was 73.0% and has been above 70% for 14 consecutive quarters, the longest stretch since the 1950s. Owners’ equity in real estate was $35.8 trillion in the second quarter.”

Cotality: House Prices Increased 1.4% YoY in July Annualize that!

Here's what happens when private equity buys homes in your neighborhood

When institutional investors first started buying single-family homes, the U.S. government laid out the welcome mat.

Before the Great Recession, major investors hadn't had much interest in the suburbs. In the early 2000s, a firm called Redbrick Partners tried buy-to-rent. It ultimately abandoned the effort. Unlike in an apartment building, its leadership noted, where corporate management is common, fixing faucets and other maintenance were much less efficient when dealing with geographically dispersed homes.

But during the Great Recession — just before the decline of new starts in Erb's chart — the U.S. had a glut of single-family homes in foreclosure. Many were auctioned off en masse, including by the federal government, which organized auctions for investors like Blackstone and even provided a $1 billion loan guarantee to encourage Blackstone to buy.

This allowed private equity firms (which raise money from wealthy families, pension funds and other organizations to seek out profits, often by buying private companies) and real estate investors to efficiently and cheaply buy, say, a dozen similar homes located in the same Phoenix suburb…

Blackstone then introduced a financial product that supercharged the buy-to-rent sector: the rent-backed security. It was a bond, or IOU. Investors bought them, providing Blackstone with more money to buy and renovate homes. In exchange, investors were entitled to a cut of future rent payments.

Wall Street could now buy homes by paying with the rent they would collect in the future. Per the Federal Reserve Bank of Philadelphia, the number of homes owned by Blackstone and similar firms increased from almost nothing in 2010 to around 400,000 by 2021…

The buy-to-rent strategy was hurting the middle class. Creating rentals aided lower-income families and nudged rents down. But reducing the supply of homes available for sale also pushed home prices up, hurting families on the cusp of homeownership…

Middle-class families are right to worry about private equity displacing them from the housing market. She worries about fewer families achieving homeownership and gaining control over this intimate part of their lives, which has also been the dominant path to building wealth in America.

"President Trump says he wants ordinary Americans to be able to invest in private equity. But in reality, the industry needs your cash."

FOMO Made Him Buy a House in 48 Hours. Now He’s Struggling to Sell.

Navarro is among the Americans who rushed to buy during the pandemic’s housing-market frenzy, when mortgage rates were lower than anybody could remember and people were embracing a radical new work-from-home era…

It costs him about $2,950 a month to maintain the house, including the mortgage, home insurance, utilities and lawn care. By comparison, he had been paying around $1,200 a month in rent.

About two years after he bought it, he also started smelling sewage. Navarro, who travels frequently for work, learned a pipe wasn’t connected to the sewer. It cost him more than $13,000 to fix it and make related repairs.

Navarro is eager to rent an apartment with a friend as soon as he can sell his home.

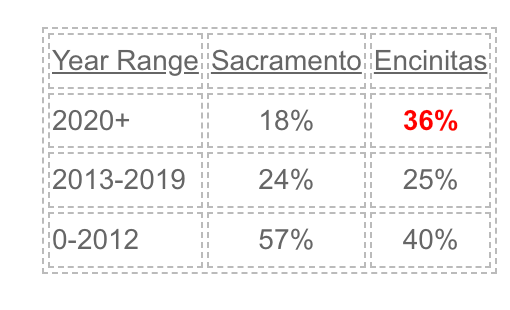

“Our friend Ryan the appraiser (and the only other daily blogger left) ran a post today on the current sellers in his market around Sacramento.

I like doing similar posts so we can compare!

He is one of those sophisticated gentlemen who can analyze his whole MLS, so his research covered the entire 6,000+ properties in his system. I do mine manually, so I just looked at the 76 houses for sale in Encinitas:

When Did Today’s Sellers Buy Their Home?

As expected, the majority of sellers are long-time owners who are cashing out.

But surprisingly, more than a third of today’s sellers are recent purchasers!

Three of those have a chance of selling for less than they paid.

Nine of the 76 are flippers.”

“…among the 50 most vulnerable county housing markets in Q2 2025, California led the way with 14 entries, followed by Florida with seven, New Jersey with five, and Louisiana with four. Risk levels were assessed using a combination of key factors, including home affordability, foreclosure rates, the share of seriously underwater mortgages, and local unemployment figures.”

Foreclosures

“The August 2025 U.S. Foreclosure Market Report reveals a continued upward trend in foreclosure activity, marking the sixth consecutive month of year-over-year growth and the third straight month of double-digit increases. A total of 35,697 U.S. properties had foreclosure filings during the month, representing an 18% increase compared to August 2024, despite a slight 1% decline from July 2025. Both key components of foreclosure activity rose year over year: foreclosure starts jumped 17% to over 24,000 filings, while completed foreclosures (REOs) surged 41%, totaling more than 4,000 nationwide. Despite remaining below pre-pandemic levels, the persistent rise in both foreclosure starts and completions may signal increasing financial strain for some homeowners amid elevated home prices and interest rates.”

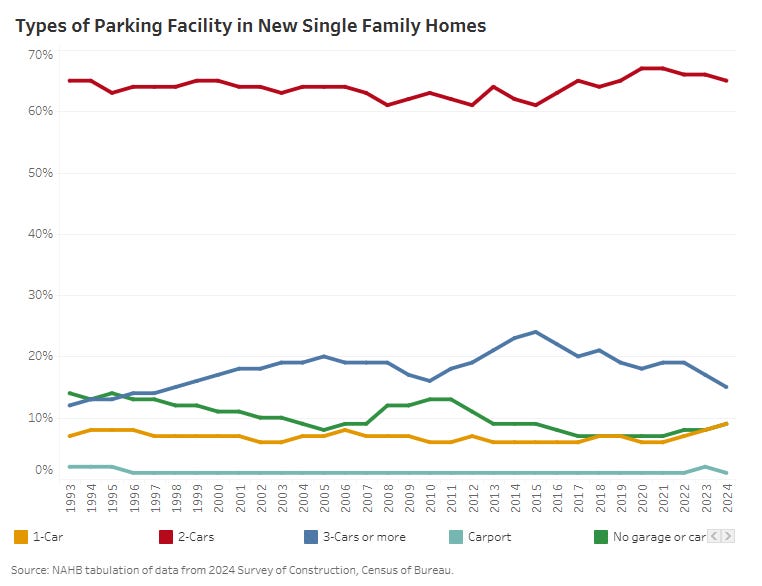

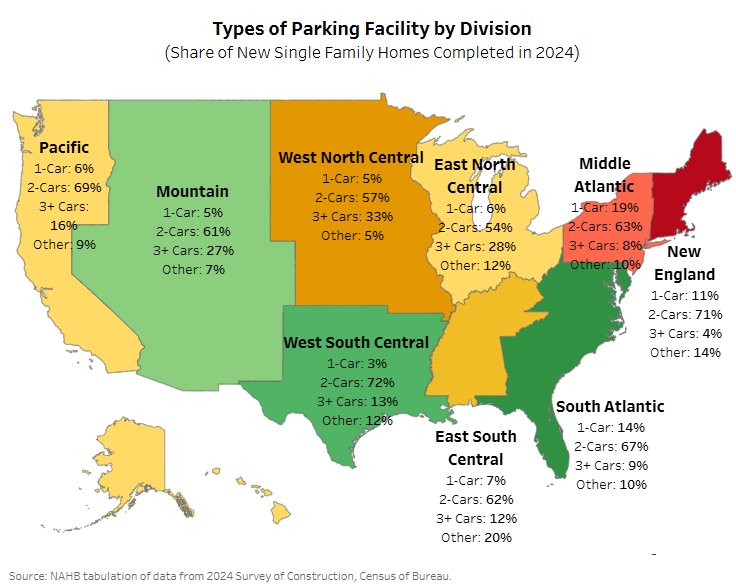

Parking

How are the serfs faring?

Via Grant’s:

Beyond those wealth-effect beneficiaries in the upper crust, signs of strain grow more visible. Average 30- and 60-day delinquency rates among subprime automobile lenders stand at 11.1% and 5.2%, respectively, Bloomberg relayed last week, marking the highest for each data series since at least 2018 and far above the 4% and 1% levels seen during the Covid-era stimmie-fueled sugar rush.

“Elevated vehicle prices continue to support bonds backed by auto loans but are squeezing affordability, leading to more late payments,” Bloomberg strategist Rod Chadehumbe wrote last week. Average new vehicle prices tip the scales at $49,100 according to Cox Automotive, up nearly 33% from the summer of 2019, while the tally of new models offered at $25,000 and below has shrunk to just five from 25 a decade ago.

Consumer Sentiment

This is a remarkable chart.

I think Brent Donnelly was talking about it so I looked up EUR/USD.

A couple of podcasts I caught this week with two faves:

Bill Pulte accused Fed Governor Lisa Cook of fraud. His relatives filed housing claims similar to hers.

“Mark and Julie Pulte, the father and stepmother of Bill Pulte, President Donald Trump’s appointee as director of the Federal Housing Finance Agency, since 2020 have claimed so-called “homestead exemptions” for residences in wealthy neighborhoods in both Michigan and Florida, according to the records. The exemption is meant to give a discount to homeowners on taxes for properties they use as their primary residence.”

I know, I know - Pulte’s parents aren’t in a position of power at the Fed. I just don’t care for Bill Pulte.

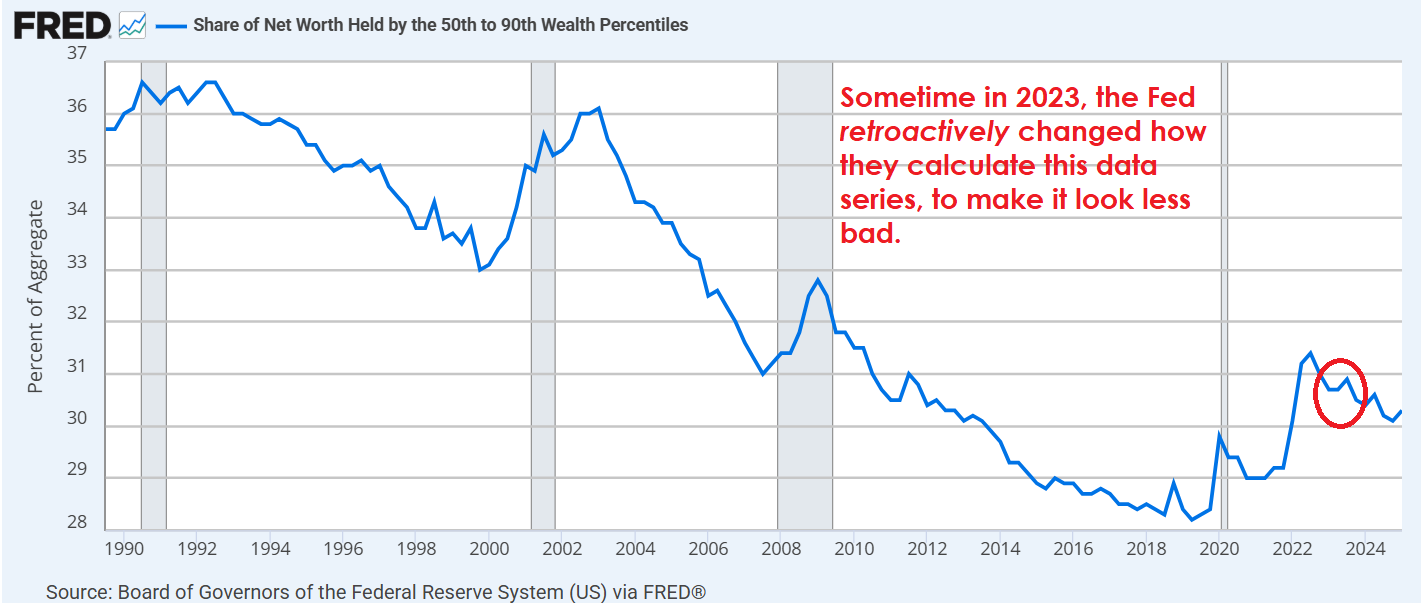

"I think if you had the public actually sit through Jackson Hole, they'd be aghast at what's going on. Aghast. Central Bankers have no idea what they're doing."

“Trump and Powell have been acting out a performative charade regarding when and to what extent artificially low interest rates should go even lower in the midst of persistent inflation. The supposed sparring between Trump and Powell merely guarantees the result both want—more easy money.”

‘Fed could tolerate high inflation to ease tariff effects, says BIS’

We've tolerated high inflation already.

Sure - tariff inflation is what has destroyed most Americans over time. Nothing else led to a massively higher cost of living.

We now need to "tolerate high inflation"?

Central Banks are the enemy, folks.

No one in power cares about most Americans, who are getting killed by the high and rising cost of living.

Economists are like the "royal court at Versailles before the French Revolution."

The Age-Herald, Birmingham, Alabama, September 12, 1913

"The Curious Case Of George Zinn"

"One of the things that's interesting to me about silence is how difficult it is to start, and then how enveloping it becomes as you go through it."

"The realization that life is absurd cannot be an end, but only a beginning."

In 1913 your family could buy an ounce of gold for $20. Today the same ounce of gold would sell for $3,682 on the spot market. Put another way, a millionaire in 1913 could buy 50,000 ounces of gold with a million dollars. Today that amount of gold sells for $184,100,000. So now you know why "millionaire" was a big deal. Put yet another way, over 99.5% of the value of your family's dollar's purchasing power has been deliberately destroyed by the evil men and women of the Feral Reserveless scam. However much you want to End the Fed you should want it much more.

For those of you playing along at home, please print out the U of M Consumer Sentiment Index chart, take a #2 pencil and shade in the unsanctioned recessions 3/22- 11/22 and 3/25 to the present. Thanks for playing, and good luck.