This complete divorce of incentives

The QE drug is wearing thin.

Actionable Information!

The Fed's "Core CPI" model, at 2.8% YOY, has been above their made-up 2% target since April 2021.

"European banks spend €1.1bn axing senior staff"

"The €1.13bn severance pot was shared between 2,100 material risk takers across the seven lenders"

'Risk takers' lol.

That's $1.307 Billion US, divided 2,100 ways = $622,512 EACH on average.

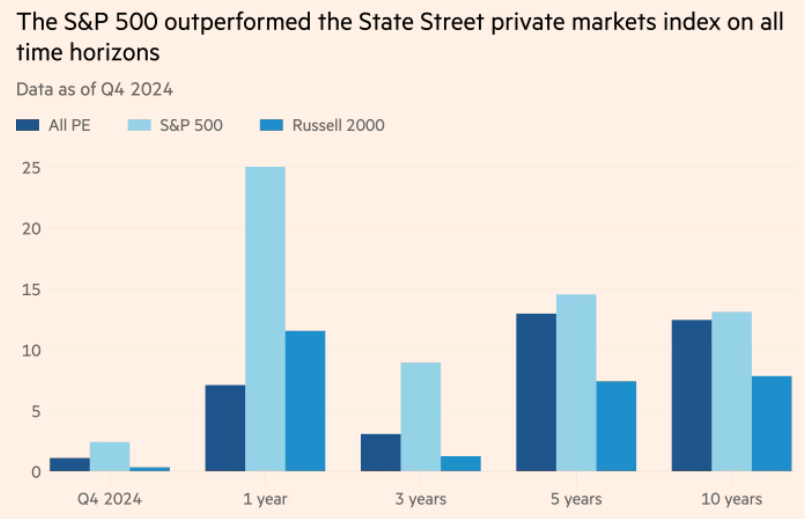

State Street’s private equity index — which tracks returns from private equity, private debt and venture capital funds — delivered a 7.08 per cent return last year, compared with a 25.02 per cent total return for Wall Street’s blue-chip S&P 500 index.

The data shows that the S&P 500 outshone private markets funds for the last three months of 2024, as well as on a one, three, five and 10-year basis. That marks the first calendar year that private markets funds have underperformed the stocks index across all measured time horizons since 2000.

Many critics of the article in the comments:

Private Equity in Media

A nice angry 2019 rant from Megan Greenwell, formerly of Deadspin

A metastasizing swath of media is controlled by private-equity vultures and capricious billionaires and other people who genuinely believe that they are rich because they are smart and that they are smart because they are rich, and that anyone less rich is by definition less smart. They know what they know, and they don’t need to know anything else…

The question I hear the most about the owners of this company is “Why did they buy a bunch of publications they seem to hate?” I and my colleagues have asked Spanfeller only slightly more diplomatic variants of that question on several occasions. The answer he has given is that the publications didn’t cost him much and that he liked their high traffic numbers. The unstated, fuller version seems to be that he believed he could simply turn up the traffic (and thus turn a profit), as if adjusting a faucet, not by investing in quality journalism but by tricking people into clicking on more pages. While pageviews are no longer seen as a key performance indicator at most digital publications—time spent on the site is increasingly thought to be a more valuable metric—Spanfeller has focused on pageviews above all else. In his first meeting with editorial leaders, he said he expected us to double pageviews. Several weeks later, without acknowledging a change, he mentioned that the expectation is in fact to quadruple them. Four months in, the vision for getting there seems less clear than ever.

How Private-Equity Billionaires Killed the American Dream

The central tension of the book is about the disconnect between what serves private-equity firms and what serves the communities that surround the businesses they buy. I’d love you to spell out how that disconnect manifests.

Leveraged buyouts are a huge percentage of what private equity does. The basic way leveraged buyouts work is that the private-equity firm bundles together money from their outside investors—university endowments, pension funds, ultrawealthy individuals. But that only ends up making up a small minority of the total money they use to acquire a company. The rest of the money is bank loans, and those bank loans are assigned not to the private-equity firm that made the decision to borrow that money, but to the company that they are acquiring.

So if I make an offer for your company, and I’m borrowing money to buy it, I’m not responsible for paying that money back; only you are. You end up with this complete divorce of incentives, where what is good for the private-equity firm is not necessarily what’s good for the portfolio company.

In industries that are real estate heavy—hospitals, retail, newspapers—private-equity firms will sell off the real estate assets of those companies to pocket the proceeds themselves. Then the portfolio company has to pay rent on the same land that they may have owned for years or decades. Now you have a situation where the private-equity firm is doing great because they’re collecting their management fees, plus they got this tidy little profit from the real estate sale, but their portfolio company is buried under debt from the acquisition and also rent payments where they previously owned their land outright.

You see the two paths start to diverge. The private-equity company is winning, and the portfolio company is getting weaker and weaker and weaker. That was the thing that really broke my brain.

The one stat that’s really lodged in my brain is that 20% of companies acquired by private equity enter bankruptcy proceedings within 10 years, compared to 2% of other types of other companies. There is this narrative that the private-equity industry is made up of, essentially, superheroes who can come in and save struggling companies, and the data just shows that it is the opposite.

If you ask private-equity people about this stat, they will say, “But we buy companies that are already struggling!” But they’re buying companies that are struggling while claiming that they are the people who can save the company. It doesn’t make sense that there would be such a vast difference between the number of companies that go out of business under any other kind of ownership versus what happens when, allegedly, the smartest people in the finance world take over. We’ve been sold a story that isn’t remotely true.

Data Center Boom May Turn Into Long-Term Glut Risk, Goldman Warns

Remember the fiber optics companies of 25 years ago? They laid a ton of infrastructure and then went bankrupt.

In “the decade of the 1970s…the US dollar in absolute terms lost 75% of its purchasing power over 10 years…and I think the dollar will lose 75% of its purchasing power in the next 10 years”

Below the fold, Dan Myrmikan on "the dollar’s demise as the primary international reserve asset," and "gold reestablishing its positive correlation to nominal rates," central bank swap lines, the BOJ rate mess, Williams White on complex adaptive systems, fallacious Zestimates, housing stats, carpetbaggers, poor Barry Sternlicht, D.C. office fire sales, CRE reality checks, Fannie and Freddie redux, bailing out Bill Ackman again, exploding mortgage securities, multifamily woes, rent disinflation(!!!), rich people problems, straight-shooter Sam Faddis on Chinese spies and Facebook and Youtube censorship, brain-eating amoeba, A.I. hallucinations, A.I is making us dumber, A.I. Kuru(!), George Washington and imaginary Thomas Jefferson quotes, Matt Stoller on Harvard, Nick Bryant on Pam and Kash ("LIARS"), Herb Alpert, and more.

Happy Father’s Day!

Keep reading with a 7-day free trial

Subscribe to A Havenstein Moment. to keep reading this post and get 7 days of free access to the full post archives.