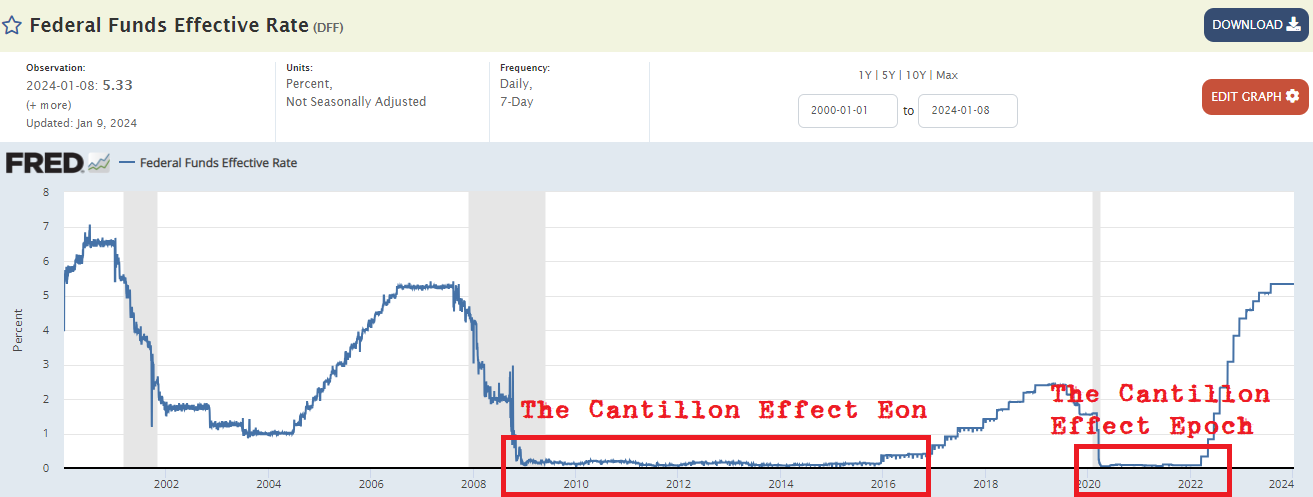

This was where the math all changed.

When there's too many lenders in the space, it's a race to the bottom.

Redfin: “The median U.S. asking rent fell 0.8% year over year in December to $1,964.”

America is running out of home-owners insurance Premiums for US homeowners’ insurance jumped by an average of 21% from May 2022 to May 2023, according to a study by online insurance marketplace Policygenius…US property insurers are hurting following three straight years of underwriting losses—including $6.7 billion in 2022 alone, according to insurance credit rating agency AM Best. One 200-unit waterfront condominium in Long Island saw its insurance premium more than double to $461,000 for this year…Those costs, which get passed on to residents through their homeowners’ association (HOA) fees, could easily translate into a doubling or tripling of monthly outlays for each apartment owner. There’s added consequence if condo owners can’t afford to pay up – or simply don’t. If more than 15% of a building’s owners are delinquent in their HOA payments, no unit at the property can qualify for a mortgage…“Now all of a sudden, you’re seeing numbers of 12, 14, 20% of unit owners delinquent on their maintenance by more than 60 days,” Tomaselli said.

UK fund snaps up 85% of Dublin 17 housing estate originally aimed at individual buyers

Private rental firm Occu [owned by Sw3 Capital] has acquired 46 homes in Belcamp Manor for €21.5 million, and is seeking to rent each out for €3,175 per month [$3,471, fully furnished]…

It came a month after the Business Post reported that Round Hill Capital and its partner SFO Capital had completed a deal to purchase 135 of 170 houses at the Mullen Park estate in Maynooth in Co Kildare. The two companies, both headquartered in the UK, also bought 112 homes at the Bay Meadows estate in Hollystown, Dublin 15 the previous month.

Private parties—namely the uninsured depositors—that were otherwise on the hook to absorb SVB and Signatures’ losses did not take those losses thanks to extraordinary action by the FDIC; instead, thanks to that extraordinary action, those losses were borne by others. That’s a bailout.

“The US Financial system is built in a way to protect the rich at the expense of the vast majority of working class people in the country. Poor and working people never get bailed out by the government, but rich capitalist oligarchs do get bailed out by the government, while they ironically lecture poor people about how they have to work harder, and pull themselves up by their bootstraps.

It is quite literally a system in which capitalism exists for the vast majority of working people but there is socialism for the oligarch capitalist billionaires who don't have to worry about risk. They pocket all of the private profits but then the risk is socialized. It is a system that is the worst of both worlds.”

Benjamin Norton, of the left-wing Geopolitical Economy Podcast

“I'm a a casual but sincere fan of Jeff Snider.”

The Infamous Jobs Report

Part-time jobs increased by 762,000 for the one and a half million full-time jobs that disappeared. Some businesses were cutting hours to the point that some employees who used to be full-time were converted to part-time. It's a defensive measure that companies take when the business climate isn't good. You start cutting costs, and if you don't want to lay off people, the first thing you can do is cut back on their hours, and according to the household survey this is not just a one-month thing either.

How bad was this December number? As I said, one and a half million decline in December alone that followed a 225,000 gain in November, 357,000 in October, but there was 122,000 decline in September, so again, the same four month stretch - even though you have monthly variation back and forth - over the last four months it's the largest four-month drop outside of March and April 2020. Go back six months - over the last six months full-time positions have crashed by 1.6 million, so the last half of last year 1.6 million fewer full-time positions at the end of it than when it started, and again, we don't see this type of behavior to this degree outside of recession.

NFIB Small Business Survey: Inflation Returns as Top Problem

“Small business owners remain very pessimistic about economic prospects this year,” said NFIB Chief Economist Bill Dunkelberg. “Inflation and labor quality have consistently been a tough complication for small business owners, and they are not convinced that it will get better in 2024.”

Insiders are Selling

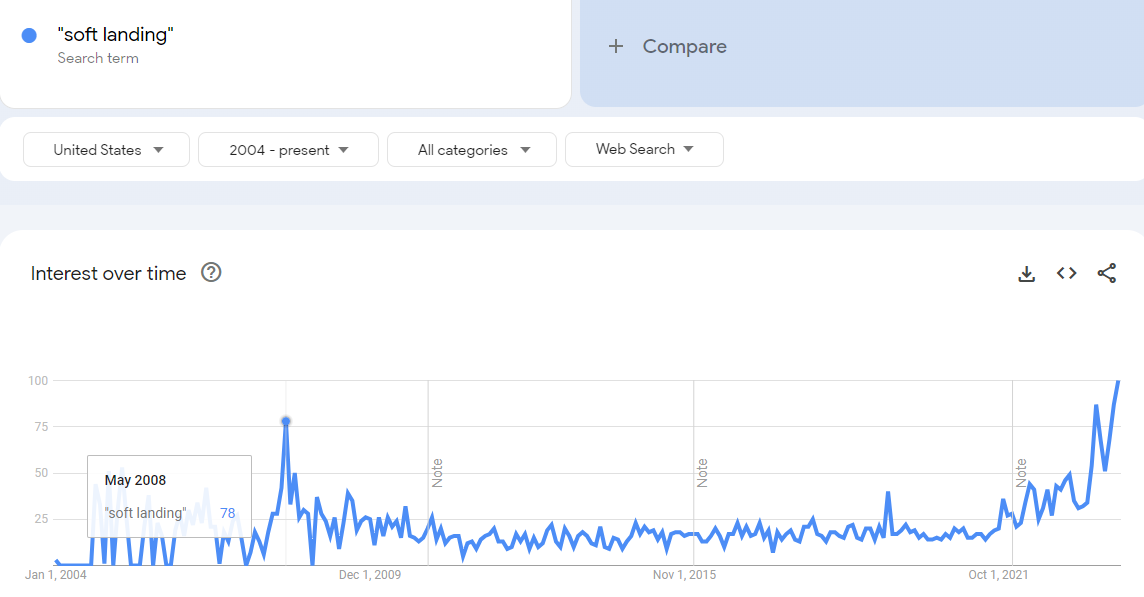

The last time “soft landing” trended this hard was in May 2008.

“So, in summary, I think the most likely outcome is that the economy will move forward toward a soft landing.”

- Janet Yellen, FOMC Meeting, Halloween 2007

“What we’re seeing now I think we can describe as a soft landing, and my hope is that it will continue.”

- Janet Yellen, January 2024

Fed chairman projects 'soft landing' for U.S. economy

- New York Times headline, February 15, 2007

IMF Survey: Soft Landing Ahead for U.S. Economy

August 2007

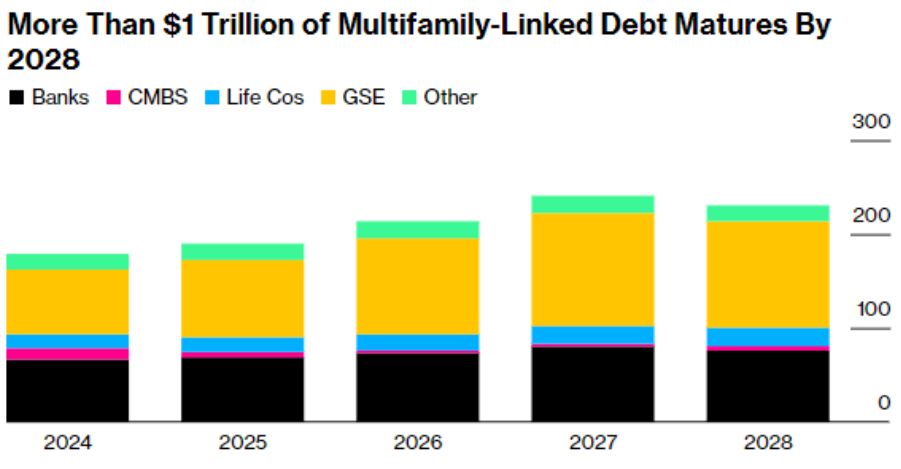

James Eng of Old Capital Lending in Texas explains how multifamily went insane

The entire podcast with Eng is worth listening to. Too many great quotes to share (also, the GowerCrowd podcast, which I just discovered, has some great CRE guests). James Eng (and the Old Capital crowd in general) are very informative. The interview is from October 2023.

“I started really in the business in 2015, and the majority of the people were doing agency loans, so that was Fannie, Freddie, fixed-rate, five, seven, ten year loans. It's pretty stable. I felt like rates were around four and a half to five and a half percent, and you could put 75%, 80% leverage, and you got maybe a year or two interest-only, and that's how people bought deals. If you needed to do a bridge loan, a shorter term bridge - let's say it didn't qualify for agency. It needs to be 90% occupied for the last 90 days, and that's how you get an agency loan. If the property was just broken, mismanaged, then maybe you do a bridge. It was a higher interest rate, and it was a shorter term.

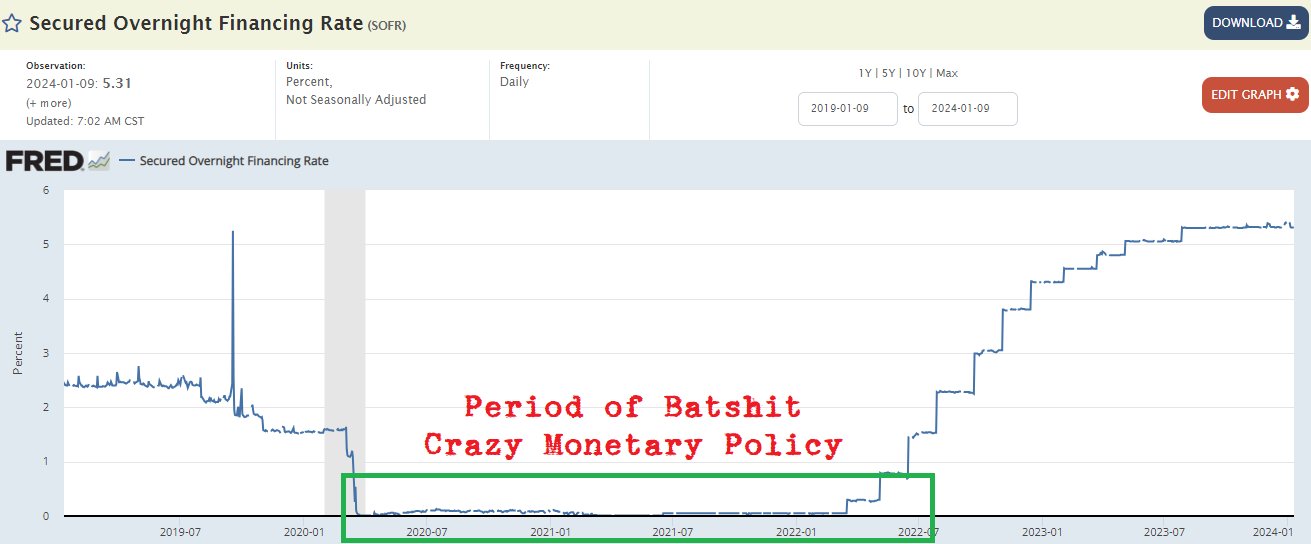

So everything was going well, and then boom, Covid hits in 2020. All the bridge lenders go away. The only thing you can do is agency, and they made you put up huge reserves, so if your loan was, say, $10 million, they were like we'll give you the loan, but we're going to need five to ten percent set aside. So not only did you get get a lower leverage loan, but you had to put up a big reserve - but during Covid you couldn't go out of the house, and so that was the only lender in town. So that's really what happened - the majority of our volume in 2015 to 2019 was fixed rate agency loans, 2020 more of the same, and in 2021 basically the Fed took the rates down to zero.

You know, people don't really remember that, but in 2021 rates came down to zero. Ten-year Treasury went down basically to 1%, and, you know, you had the option of going and getting an agency loan, or you could do a floating rate bridge loan, and this is where the math all changed.

“Let's say a deal was $10 million, okay, and you said, James, get me a loan from Fannie and Freddie, and I said, all right, yep, we can do a $6 million loan on this deal, so 60% leverage and you're like, okay, that's pretty good what does the bridge lender give me on a $10 million purchase? Uh, the bridge lender give you eight million, so they were at 80%, Fannie and Freddie were at 60%.

Wait, we're not even - it gets better. So $10 million was the sort of the whisper price - you know, the broker was saying all right, come tour the property, it's $10 million. Okay then you know you put in the offer at $10 million - guess what? There's 20 people at $10 million. So then it goes to the next round, best and final, 11 then 12 then 13 - okay, it's 13 million. Then they say, all right, you've come up to 13 million the agency loan is still, what, $6 million? So now you're under 50% leverage. You're like 45% leverage on the deal. The bridge lender, they move up with you, so not only were they doing the eight million, they're saying all right, you're at - and let me try to do the math - let's say you're at 13 million or 14 million, they said yep, we can do $10 million, yep, we can do $11 million, yep, we can do $12 million, so your equity check was the same even as your price was going up, right?

On the agency side they were saying, you're at $14 million, the loan that I can give you is $6 million, because it's based on in-place cash flow. Every time you went up, you had to raise more equity, and so people - we just stopped quoting agency.

So the bridge was not looking at DSCR, the bridge was projecting forwards to future proforma, so it was not based on in place cash flow, it was based on year three cash flow projected. So then so let's say the bridge lender said, all right, you're paying $14 million and now your loan is $10 million, $11 million, and then you said, well, I need a million dollars for rehab, okay, we'll add a million dollars on top of that. So now the bridge lender is at $12 million, and so that's what happened in 2021 and 22 on every deal.

There was so much money chasing. Okay, so when you ask as, all right, what was the volume in 21 and 22, what was the mix? 80% of our loans were bridge, and almost 95% of the bridge loans out there were floating rate, and so this was going on across all the major markets. Everything that could be securitized really into what was called CLO’s, or collateralized loan obligations.

They would do a billion dollars worth of these loans, and then they would securitize it, and people would buy it, because you could buy a treasury at 1%, or you could buy this loan against the multifamily property, and it was paying you anywhere from 3% to 4%, because it was a loan based on SOFR plus, let's, say 3% spread.

So SOFR was zero, so you could get three percent, or 4% on a loan backed by multifamily, or you could buy the Treasury and get 1%. Which one do you want to buy?

And so much money - it was easy to sell that paper, and so it just kept going on and on. From 2021 January 2021 all the way up until probably summer of 22, that 18 months it was that bridge lending environment that pushed values up significantly.”

“They would package 30 of those [bridge loans] together and then sell them in a securitization of close to a billion dollars, and then people would buy the tranches of that securitization, so very similar to, you know, 2007-08 in the residential space…the investors who invested in those tranches, depending on what tranche you invested in, if those deals start going bad, then they will be taking the losses, not necessarily the people who originated those loans."

Maybe it’s not as bad this time…

James Eng

“Most of the stress is going to be a major markets $10 million and higher and I only focus in on multifamily, but multifamily seems to be where majority of these loans were done.”

“So right now, if you buy a three-year rate cap, it's close to 9% of the loan amount. So on $10 million, it'd be $900,000. [And it was really $20,000 three years ago?] 2021, yeah. And now it's nearly a million dollars to do, or more.”

So if you liked the above, or are interested in the topic, here’s another CRE guy I discovered, Jeremy Roll:

How to navigate real estate market chaos (December 2023). He’s a rare bird who talks positively about investing in rent-controlled buildings.

Real Estate Investment Strategies and Risks Presentation (October 2023) Part 1 Part 2 (the host is a little goofy but Roll is good)

Arbor was one of the biggest bridge lenders.

“There is no rate cut large enough, no rate caps cheap enough, and no investors dumb enough to save Arbor.”

Here is the author of this Arbor short report, Gabriel Bernarde, Viceroy Research.

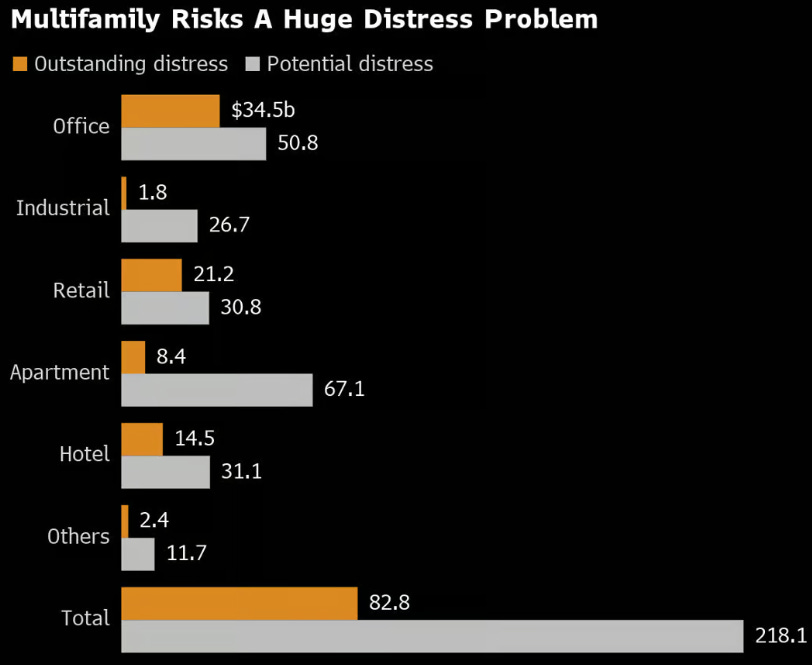

The alarm bells are ringing loud in the multifamily sector, with MSCI Real Assets pinpointing over $67 billion at risk – the highest in any property asset class. This includes high-end complexes and downtown high-rises, where lower occupancy rates are being observed. Investors like Viceroy Research are targeting prominent lenders in the apartment market, such as Arbor Realty Trust Inc., due to their distressed loans. Meanwhile, Lennar Corp. is considering selling more than 11,000 apartments to mitigate losses.

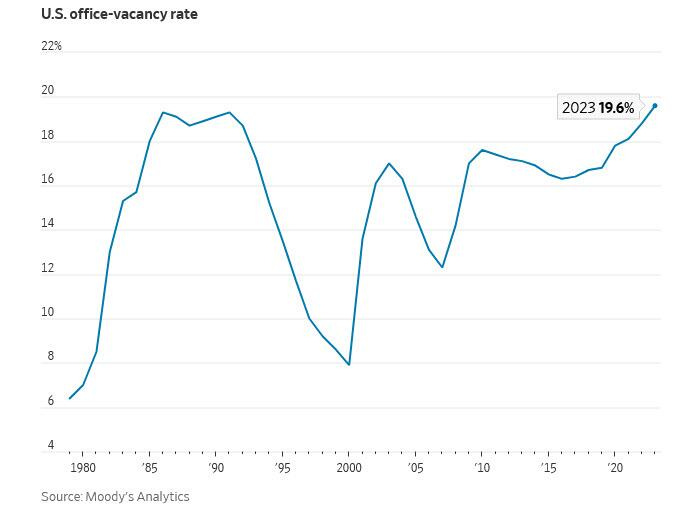

Office Vacancy Rate

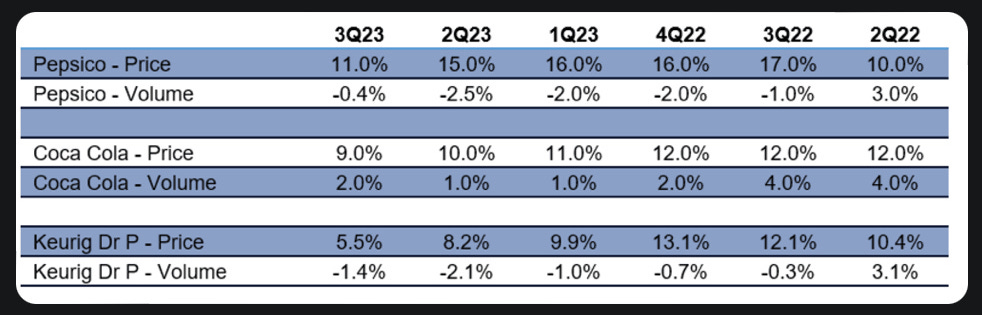

Price and Volume

Carrefour pulls PepsiCo products over price hikes

Carrefour is telling customers in four European countries it will no longer sell products, such as Pepsi, Lay's crisps and 7up because they have become too costly, in the latest tug-of-war over prices between retailers and global food giants. From Thursday, shelves for PepsiCo products at Carrefour stores in France, Italy, Spain and Belgium will carry signs saying the store will no longer be stocking the brands "due to unacceptable price increases", a spokesperson for the French supermarket giant said.

Customers in the supermarket broadly cheered the move. "It doesn't surprise me at all," shopper Edith Carpentier told Reuters. "I think there will be lots of products left on the shelves because they have become too expensive, and they are all things we can avoid buying."

I mentioned back in July how much Coca-Cola prices had risen, and I expected volumes to drop as a result. A new article by Herb Greenberg highlights this trend:

This is remarkable. Compare elderly Reagan to Biden.

Congress appears to have again met low expectations by reaching agreement on discretionary spending limits for fiscal 2024. Spending will remain at $1.59 trillion as specified by the ludicrously titled Fiscal Responsibility Act agreed to by former Speaker Kevin McCarthy and President Biden in May (which cost McCarthy his speakership and led to his departure from Congress). Some, like the Wall Street Journal’s editorial page, are calling this a “minor victory” because many in Congress wanted to spend more money. This is a version of the soft bigotry of low expectations whereby we lower our standards to justify and enable failure.

This budget agreement is not any kind of achievement; it is an admission that Congress has no intention or ability of addressing the burgeoning debt crisis caused by years of failed fiscal management.

Curious to see how this Pepsi/Carrefour plays out. Mind you, the French have lots of alternate pretty cool snacks and tasty real food. I still have fond memories of what seemed like a mile long cheese counter in a French supermarket. Is there a Pepsi Index like the Big Mac Index ?

This is definitely where the math has changed! Just read this this morning. Never mind the locals and their needs. “. . . huge income streams are available to those involved in migrant accommodation and the asylum system in Ireland is now an entirely new economic sector. . . . massively funded overseas corporations, some of them partnered with Irish companies, have seen this as a lucrative area, surpassing even in some cases their other interests in buying up Irish property that then becomes unavailable for working people even with mortgage approval . . . “. https://gript.ie/who-are-the-companies-who-regard-ballsbridge-and-other-asylum-centres-as-prime-investments/

So it’s not just US taxpayers funding unwanted, excessive immigration. What’s so amazing is that a reliable poll (pew) has determined 75% of the Irish public say there is enough, there have been many peaceful protests aswell, yet Trudeau wanna be Varadkar admonishes them and tells the people no one has a right to veto who comes into their communities.

And at a big birthday party last weekend a smoked salmon liberal lamented that there are now fewer democracies than some decades ago - I felt like saying, yeah, no kidding. But he wouldn’t have gotten the joke.