Unwinding insane monetary policy can be painful.

"Now the smart people have to not do smart things because they're absorbing stupid people risk."

[That quote above is either from Bill Brewster or Charlie Munger.]

“Language needs to alter by evolution, not by imposition,

because to do so is to defer to authoritarianism…

I think we’ve been a bit too indulgent with lunacy.”

Understanding the Hoax of the Century

Typically good podcast from Demetri Kofinas of Hidden Forces, this time with Jacob Siegel, author of the epic Understanding the Hoax of the Century, which I mentioned in my post, The War on Dissent.

“There's a reason why in this very long essay I just wrote, I never do what is sort of the standard proforma move in all of these pieces and define disinformation versus misinformation. The reason why I don't do that is that I think that they are ersatz technical signifiers. They have no real meaning beyond the ways in which they serve the interests of the party in power.”

Jacob Siegel

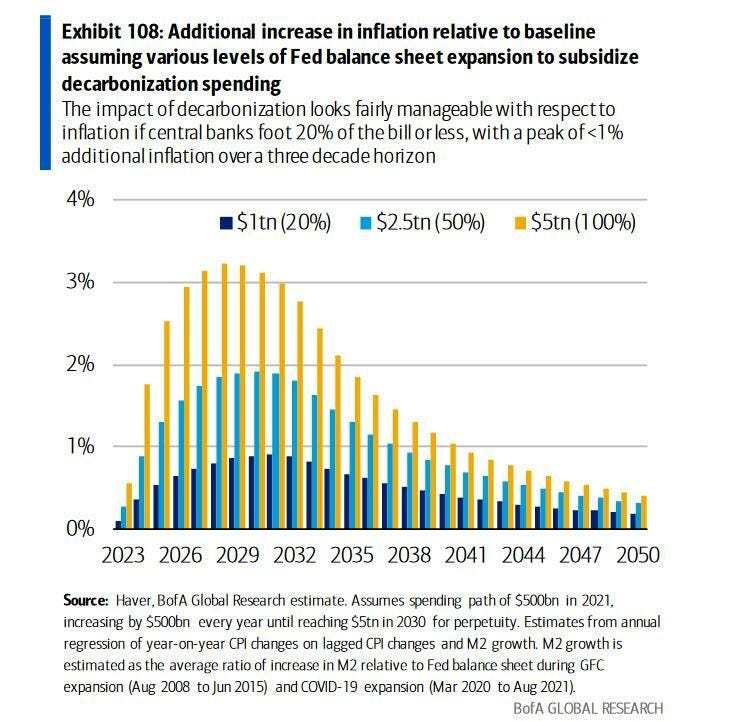

Whoa, whoa, whoa!

Check this out, via Zerohedge…

I don’t have a link, but doesn’t this chart suggest a 5% (2%+3%) TARGET CPI in the future? (I think we clearly should take the upper estimate with this crowd.)

And explicit debt monetization? Citadel Ben said we would not do that. Did he lie?

The middle-class and poor will get beat over the head with a rake by this, but the private jet crowd will be fine.

Americans had better hope that “reserve currency status” holds up, at least until we’re out of office.

As for green decarbonizing yada yada, I think the biggest beneficiary of the whole ESG scam is going to be people like Larry Fink, not the planet. I don't think the planet will see much difference, but dictator-loving Larry Fink will be much, much richer. If you’re serious about decarbonization, you have to use nukes (and nat gas as a bridge fuel). Otherwise, you’re just advocating a return to the middle-ages.

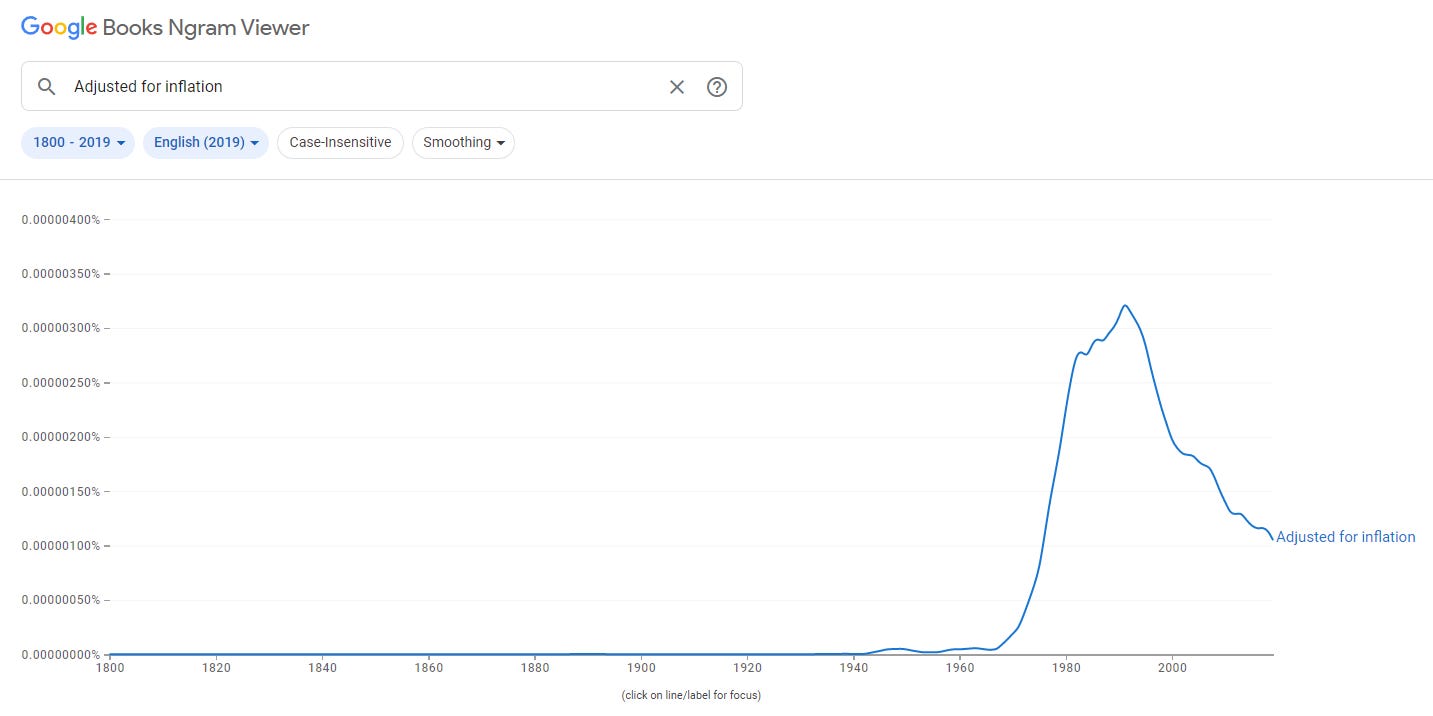

Isn’t it odd that almost no author wrote, “adjusted for inflation” before the United States went off the gold standard in 1971? (And note that this chart only goes to 2019!)

By the way, our homes in general are larger than they were years ago, but…

Heck, the Fed was monetizing well over a trillion dollars of MBS as the median price per square foot rose 47% between March 2020 and June 2022.

For the historians out there, here is a letter that “Father of the Fed” Paul Warburg wrote a month before the Federal Reserve Act was made law in December 1913. It’s actually available on the St. Louis Fed’s FRASER website:

LETTER TO A FRIEND CONCERNING FIAT MONEY. November 3rd, 1913.

DEAR FRIEND : I have received your letter this morning, and I consider it almost a joke to receive a letter from you, emphasizing your position of loyalty to your government and its institutions, and upbraiding me as favoring the issue of "fiat" money. It would lead too far to enter upon a controversy in writing upon this subject, but all I want to say is this: I do not believe that any one in this country has given more time, thought, and energy to this fight for sound money than I have, and as you may have noticed from my pamphlet, I am as heartily opposed as you are to the issuance of elastic currency by the government. There is a great difference, however, between a guarantee and a direct issue. Nobody would call the notes of the German Reichsbank "fiat " money, if the German government would decide tomorrow, that it wanted to guarantee those notes. I agree with you, and I think I made that clear enough in my pamphlet, that all direct connection between the government and the banking business is undesirable, but you must not go to extremes and call "fiat " money what is not "fiat " money. By overdoing the matter, we simply weaken our position. I have always believed that in order to secure legislation in the United States, we would have to concede a guarantee by the government of the notes, and I even expressed this in my pamphlet, which was published, I believe, in 1910 or 1911, before the Aldrich Plan was published, and before the Owen-Glass discussion began, so I have not given way, as you appear to think, but, in this respect, I simply stand where I stood long before the question became acute. Before I sailed for Europe, we sometimes had the good habit of lunching together. How would it be if we solved the question of "fluidity" and very "liquid" assets by taking a cocktail together, this or next week?

P . M . W .

My point is simply that even the founders of the Fed would be appalled (and impressed) by what it has mutated into.

We live, for the first time in history, in a world where all global Central Banks are monetizing debt and equities via entirely un-anchored fiat currencies. (See Ben Hunt’s The Three-Body Problem.)

While we’re at it, I should point out that the co-sponsor of the Federal Reserve Act, Carter Glass, explicitly states that the model for the Federal Reserve was…wait for it…the German Reichsbank!

When the Aldrich plan was before the country, the European bank which its sponsors most often cited as a helpful example for the United States and the one to which they gave more attention in their report than to all the others combined, was the Imperial Bank of Germany. The following brief description of the control of the Reichsbank is taken from an interview with two of its officers, which was published by the monetary commission:

Here we have one of the most successful banks of Europe - a bank which possesses practically every power that the bill before Congress would confer upon the Federal Reserve Board and upon the regional bank boards combined, and which, in addition, does a regular banking business with the public, competing with other banks. It has a practical monopoly of note issue, it is the depository of government funds, it holds the bulk of the bank reserve money of the empire, and it performs for banks and public alike most of the transfer and exchange business of the country. Yet this situation is controlled almost absolutely by politically appointed boards. The administration's plan does not begin to go so far in the direction of government control, since the real banking functions in the proposed plan are entrusted to the boards of the regional banks, two-thirds of whose members are elected by bankers, the functions entrusted to the Federal Reserve Board being almost entirely supervisory functions except a few carefully guarded ones which will be exercised only in times of great emergency, and then in the searching light of publicity.

[LOL. This rumored ‘Fed transparency” is a joke. Ask Bloomberg how the Fed responds to FOIA requests. Almost everyone who reports on the Fed is merely a stenographer and publicist. And talk about Fed mission creep! - rh]

Although the members of the Federal Reserve Board will all be appointed by the President of the United States, the board will not be a political board in any narrow sense of that term.

[Tell this to Lael Brainard and Janet Yellen - rh]

It is my earnest conviction, based upon long and serious reflection, that no man can conceive - as none has yet pointed out how any part of this system can be perverted to political uses.

I should point out that in just 13 years, the country Nelson Aldrich lauded as having “one of the most successful banks in Europe” - the same bank he modeled the Fed after - would start a horrific war in Europe and destroy its currency, paving the way for Hitler.

"The incredible fact is that Imperial Germany’s conservative finance officials never levied a single mark in extra taxes to pay the gigantic costs of World War I."

[Sounds familiar. - rh]

Otto Friedrich, Before the Deluge

(As an aside, many of these old books and documents are very difficult to find, so if it seems like I sometimes provide too much info, I figure I took the time to dig them up, and I hope this may make things easier for others who want to read original sources in the future.)

“I think the big problem going forward–the epic battle–is to wrestle control of the Debt-to-GDP ratio (mentioned above). It can’t keep going up; that would be mathematical nonsense. How it flattens and turns down is the huge unknown. Whether we have a Minsky moment (straight down), a Havenstein moment (straight up), or a combo (soar then crash) is unclear. We are, however, on a collision course with destiny.”

- long-time friend of the show Dave Collum, October 18, 2010

A Havenstein Moment is synonymous with what Ludwig von Mises calls a “crack-up boom”

But if once public opinion is convinced that the increase in the quantity of money will continue and never come to an end, and that consequently the prices of all commodities and services will not cease to rise, everybody becomes eager to buy as much as possible and to restrict his cash holding to a minimum size. For under these circumstances the regular costs incurred by holding cash are increased by the losses caused by the progressive fall in purchasing power. The advantages of holding cash must be paid for by sacrifices which are deemed unreasonably burdensome. This phenomenon was, in the great European inflations of the 'twenties, called flight into real goods (Flucht in die Sachwrte) or crack-up boom (Katastrophenhausse). The mathematical economists are at a loss to comprehend the causal relation between the increase in the quantity of money and what they call "velocity of circulation."

As I’ve said before, I do not see this happening in the U.S. in the foreseeable futures. We remain the healthiest horse in the glue factory. Hyperinflation is NOT very high inflation - which is bad enough - it’s a currency collapse, a panic out of a currency into real goods.

I still accept dollars. People have been calling for the end of the dollar for at least 50 years. Someday, at the rate we’re going, sure - but not today.

“Part of me pounding the table on the whole “dollar-milkshake” theory has not been to convince everybody to go all-in on the U.S. dollar…a big part of me pounding the table on it is to convince everybody not to go all-in against it.”

This is a favorite passage from Dying of Money:

As for speculators, the most extraordinary feature of the Reichsmark’s joyride was not any attack against it but quite the opposite, an incredible ("pathological,” it was later called) willingness on the part of investors at home and abroad to take and hold the torrents of marks and give real value for them.

Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. The storage factor caused by the investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check.

The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds. The German government strove mightily to outflood the sea.

Office sales in the Dallas-Forth Worth area are down 80 percent — $227 million from $1.1 billion — from January to February year over year, the Dallas Morning News reported, citing data from Yardi Systems’ CommercialEdge. The silver lining, if there is one, is that North Texas still ranks ninth in the country for office sales so far.

This sounds like a bad idea. To me at least, maybe not you.

If the underlying mortgage servicer discovers the AITD [a wraparound mortgage], the servicer could call the mortgage due. This is called a “due on sale” clause (within the note and the deed of trust).

—Burden and risk fall on the buyer should the mortgage servicer call the note. That means the buyer would have to obtain another type of financing.

—Buyer could have good or bad credit. Buyers with poor credit may need some sort of seller financing (AITD or seller carryback note) because they can’t obtain institutional financing.

if the seller stops making payments and goes into default on the existing mortgage, the original lender can put the mortgaged property into foreclosure and take it away from the new buyer, even if the buyer has stayed current on their payments to the seller.

“Fairstead is a purpose-driven real estate firm dedicated to building sustainable communities across the country.”

Also Fairstead:

“Fairstead laid off 10 percent of its 700-employee workforce within the past few months, outsourcing much of that work to an India-based subsidiary.”

To be fair, they didn’t say exactly which country they were dedicated to.

Individuals bought a net $77.7 billion in equities and ETFs on U.S. exchanges in the first three months of the year, according to Vanda Research data, which excludes contributions to 401(k)s and other retirement accounts. That sum trails only the first quarters of 2021 and 2022, when they bought about $80 billion.

Like I’ve said, no fear. We’re still in the center of a mania.

“I’m comfortable with volatility. When I see a good name getting beat up, I jump on it,” Mr. McGahey said. “And normally I don’t have to wait long to be rewarded.”

The Fed’s got your back!

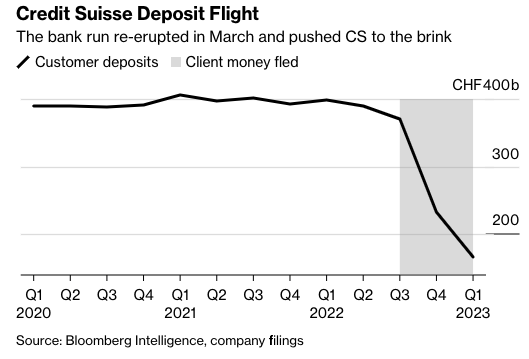

Silicon Valley Bank: the multiple warnings that were missed

More than a year before the bank failed, outside watchdogs and some of the bank’s own advisers had identified the dangers lurking in the bank’s balance sheet. Yet none of them — not the rating agencies, nor the examiners from the US Federal Reserve, nor the outside consultants that SVB hired from BlackRock — was able to coax the bank’s management on to a safer path.

Someone please forward the above to San Francisco Fed President Mary Daly. The Fed has clearly not improved in this area since 2008. I like the use of the word “coax”. You’re supposed to be grown up bank regulators, not Animal Control officers trying to get a kitten out of a tree. You don’t “coax.”

Here’s former bank regulator William K. Black testifying in 2010:

In the context of the FDIC, Secretary Geithner testified

today that this event pushed the financial system to the brink

of collapse. But Chairman Bernanke testified we sent two people

to be on site at Lehman. We sent 50 credit people to the

largest savings and loan in America. It had $30 billion in

assets. We had a whole lot less staff than the Fed does. We

forced out the CEO. We replaced the CEO. And we did that not

through regulation, but because of our leverage as creditors.

Now, I ask you, who had more leverage as creditors in 2008;

the Fed, compared to the Federal Home Loan Bank of San

Francisco 19 years earlier? Incomprehensibly, greater leverage

in the Fed, and it simply was not used.Black’s entire testimony is worth watching if you never seen it:

The Federal Reserve should be embarrassed (and accountable).

Then I see this and nearly lost it:

That such obvious dangers went unheeded has dismayed the survivors of previous moments of financial peril. “I generally don’t second guess what someone should or shouldn’t have seen when I have the benefit of hindsight,” says Lloyd Blankfein, who was chief executive of Goldman Sachs during the 2008 crisis. “I’ll make an exception in this case, because the [problems] were very apparent.”

Lloyd Blankfein should be living on a desert island eating rats.

If his failing hedge fund hadn’t magically been turned into a taxpayer-backed bank in 2008 (coincidentally, largely thanks to a former CEO of the same hedge fund), he’d have less relevance today than Dick Fuld.

“Goldman CEO Blankfein later dismissed the importance of the loans, telling the Financial Crisis Inquiry Commission that the bank wasn’t “relying on those mechanisms.” But in his book, Bailout, Barofsky says that Paulson told him that he believed Morgan Stanley was “just days” from collapse before government intervention, while Bernanke later admitted that Goldman would have been the next to fall.”

Matt Taibbi, Secrets and Lies of the Bailout (2013)

Apropos of nothing…

No, inflation isn’t back Hard to believe in 2023 nonsense like this still gets published. Actually, not hard. Also, any article that starts with “No,” is best ignored.

Commercial mortgage brokers, what’s been your experience for the past year? Check out the comments.

Unwinding central bank insanity is painful: A $3 trillion threat to global financial markets looms in Japan

Significant cracks in the $12 trillion private equity business are emerging Good! (Mute the stupid video that autoplays)

Central banks load up on gold in response to rising geopolitical tensions Tradition!

I see a trend…

JPMorgan’s Ties to Jeffrey Epstein Were Deeper Than the Bank Has Acknowledged

JPMorgan had close ties to Bernie Madoff too.

This part (among others) ticked me off:

Epstein had ties to ultrarich JPMorgan clients such as Leon Black, the co-founder of private-equity firm Apollo Global Management. Over the years, Mr. Black paid Epstein a total of $148 million for trust- and estate-tax advice, an independent review found.

The linked article said, “The months long review by Dechert LLP found no evidence that Mr. Black was involved in the criminal activities of the late Epstein”

As Ray Donovan would say, sure. I refer you to this excellent 2021 report: Apollo Global’s Jeffrey Epstein problem, part 1

“But looking deeper, that report raises as many questions as it answers. At TrueHoop, we are dissatisfied:"

The Dechert attorney who led the investigation has reportedly known Epstein since the 1980s.

The report makes conclusions based on evidence (interviews, documents, and Black’s text messages) which is not included.

Leon Black was exonerated, as far as the report goes, but nevertheless stepped down as Apollo’s CEO. Why?

Epstein, the report notes, was fixated on using Black to reach others at Apollo, including co-founders like Josh Harris. How far did that go?

…The Apollo conflicts committee was charged with exploring the well-hidden secrets of the extremely wealthy and powerful, especially Leon Black and Jeffrey Epstein. Is a master of secrecy, a former CIA executive with evident active current conflicts (equity in Apollo, ties to Blackwater), and a history of “outrageous” apparent conflicted interest, the person you’d pick if you actually wanted to unearth and disseminate the truth?

“This is an Emotional Dysregulation problem.”

I had to look it up: “Emotional dysregulation is an inability to manage your emotional states. This means you’re unable to control feelings of sadness, anxiety, or anger.”

We used to just say a kid had “an anger problem,” but it was maybe two guys. Apparently there’s an epidemic of it right now. Ridiculous that teachers (and people in downtown Chicago) have to deal with this.

DEVLIN: (resumes) Everybody's got a theory on the increasing violence in our society.

EMMERICH: My wife thinks it's the artificial hormones in beef.

DEVLIN: (chuckles) Seriously, is it true that some of your people think it's because of some greater evil out there?

KANE: Yeah, I mean, that sounds almost like a religious thing.

FRANK: Yeah, some people have that belief.

DEVLIN: What's your take?

FRANK: (pauses) I don't think it's the beef.

A theory I have is that our endless wars are very psychologically damaging.

Grandpa - are you a good guy?

I want to be.

I want to be, too.

No, your mother-in-law isn't secretly complaining about you behind your back.