Wars are expensive.

"For the eleven quarters since the pandemic/recession ended, real average hourly earnings (which cover 119 million full time wage and salaried workers) FELL at a 2.9% annual rate."

Wow.

During the July – September 2023 quarter, Treasury expects to borrow $1.007 trillion in privately-held net marketable debt, assuming an end-of-September cash balance of $650 billion. The borrowing estimate is $274 billion higher than announced in May 2023, primarily due to the lower beginning-of-quarter cash balance ($148 billion) and higher end-of-quarter cash balance ($50 billion), as well as projections of lower receipts and higher outlays ($83 billion)

Q2 2023 interest of $969.9B, on $31.5T of debt. Yellen's outfit just announced another $1 trillion of new debt by end of Q3. Maybe the problem is too much debt?

Wars are expensive. Dwight Eisenhower, 1953

Every gun that is made, every warship launched, every rocket fired signifies, in the final sense, a theft from those who hunger and are not fed, those who are cold and are not clothed. This world in arms is not spending money alone.

It is spending the sweat of its laborers, the genius of its scientists, the hopes of its children.

The cost of one modern heavy bomber is this: a modern brick school in more than 30 cities.

It is two electric power plants, each serving a town of 60,000 population.

It is two fine, fully equipped hospitals. It is some 50 miles of concrete highway.

We pay for a single fighter plane with a half million bushels of wheat.

We pay for a single destroyer with new homes that could have housed more than 8,000 people.

This, I repeat, is the best way of life to be found on the road. the world has been taking.

This is not a way of life at all, in any true sense. Under the cloud of threatening war, it is humanity hanging from a cross of iron.

These plain and cruel truths define the peril and point the hope that come with this spring of 1953.

After $700 Million U.S. Bailout, Trucking Firm Is Shutting Down

As of the end of March, Yellow’s outstanding debt was $1.5 billion, including about $730 million that is owed to the federal government. Yellow has paid approximately $66 million in interest on the loan, but it has repaid just $230 of the principal owed on the loan, which comes due next year.

I had noticed this deal, back in July 2020: “this is the government picking winners (and losers - YRC's competitors and private investors who likely could've cut a better deal). Big Corporate/Govt combos are basically fascism.”

I also noticed this, from September 2019: Apollo Leads YRC Worldwide $600MM Term Loan Refi

YRC Worldwide has completed a refinancing of its term loan obligations and entered into a term loan agreement with funds managed by affiliates of Apollo Global Management.

Apollo acted collectively as the lead lender for a $600 million facility which provides additional liquidity and has a less restrictive financial covenant.

I think this failed bailout - which taxpayers are now on the hook for to the tune of $730 million - was perhaps a bailout Leon Black and Apollo.

(Some have told me that this firm has assets of $3 billion and debt of $1.5 billion - or something like that, I’m paraphrasing here and haven’t looked it up - so all is well. We’ll see.)

A few days ago…

TL;DR: Invitation Homes - which owns 82,837 homes you will never own - in the past 3 quarters sold 311 of them, total.

Same day the above was posted…

"A portfolio" of 1,900 single-family homes that no family will own. This is all new, post-Bernanke, Paulson, Geithner. Their legacy is feudalism.

Oh - they bought the homes from Barry Sternlicht fyi.

If anyone would like to unsubscribe, here’s how you do it.

I’m not necessarily encouraging this, but I want people to be happy. The most common reason someone unsubscribes is “time,” which I understand. There’s a lot here if you follow all the links. The second reason is price, which is fine. The third reason I assume is that I’m boring, which I’m working on.

fyi All paid subscriptions are automated by Substack and Stripe (which is why Substack takes 10% off the top, and Stripe takes another 3%-6%.)

“When I started out the Belkin Report in 1992, hedge fund mafia were my clients, right? The Tigers of the world, the Steinhardts - all those kind of people, and I would see these guys and I thought to myself, “I’m such a great advisor, I have the biggest investors in the world, my clients” and then the more I saw how they trade, these guys at extremes, I would always see these guys - instead of buy low, and sell high, they’re always cramming into shit at the end, and pushing it, pushing it, pushing it.”

Mike Taylor talking about markets. Mike’s probably my favorite stock market guy to listen to. This is not investment advice.

"Disney has to fire everybody - every single person below the CEO needs to get let go, and they need new people to come in and start making new everything. A new vision, a new plan, a new movie portfolio, new writers - they basically have to take the politics out."

- Mike Taylor

Top active fund managers say they are struggling to attract money from large investors who are holding back in the face of volatile markets and cash accounts offering the best yields in years.

Oh so sad. The asset gatherers finally have some competition.

"Wall Street is not really about investing. It's about asset gathering...Indexes don't just come about because they're good investments, they come about because it's an opportunity for a management company to gather assets.." - Steve Bregman, 2020

Untangling the Complexities of Austrian Economics with Peter St. Onge “I felt like mainstream economics does not run on realistic assumptions of how the world really works.”

Lacy Hunt Opines

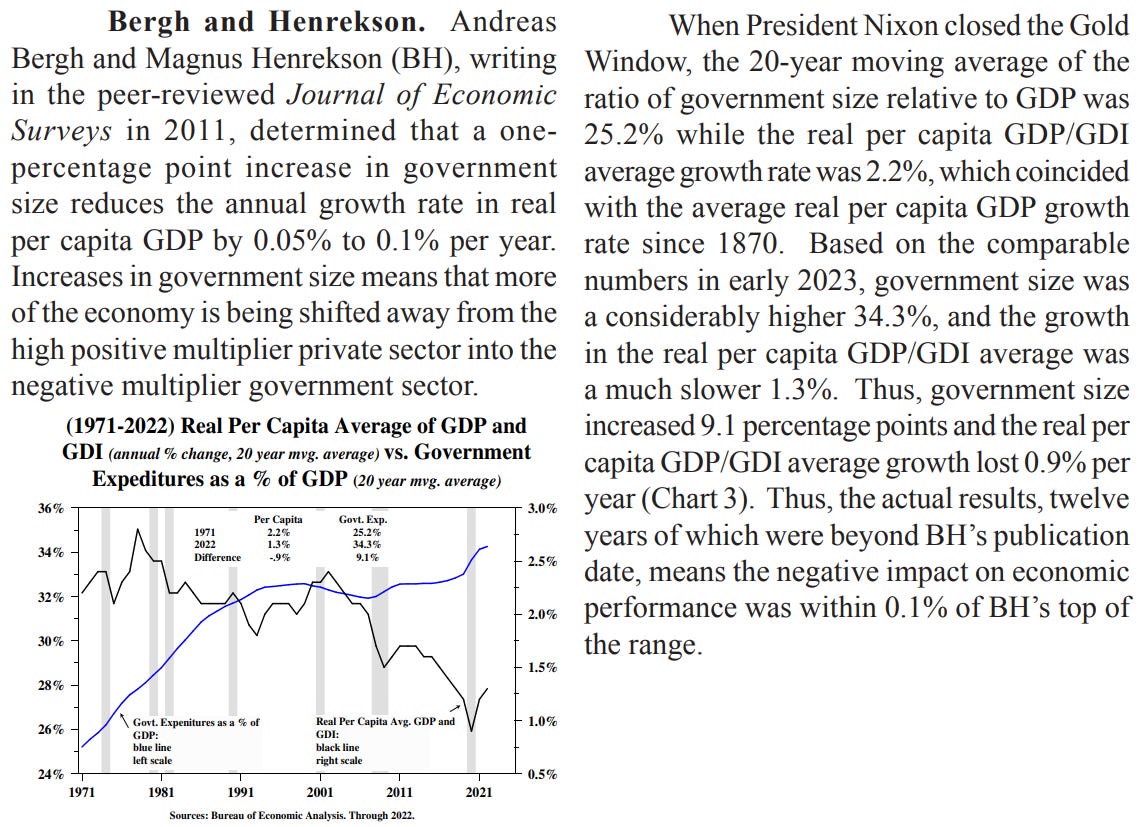

Since 1971, through the present, the government share has increased from about 25% of GDP, to about 34% of GDP. Now, there were a couple of very bright economists, Swedish econometricians Hendrickson and Berg, writing in the Peer Reviewed Journal of Economic Studies, who estimated in a paper written in 2011 that for each one percentage point increase in government size, that we would lose .05% to .1% of real per capita growth per year. And this outstanding work has actually been been validated by the time period since their work was published, we have lost nine tenths of 1% per year, we’re at the very upper end of their range. In other words, if we increase the government share through either direct deficit or by cooperation with the Federal Reserve, you get a bigger government share, you get a bit smaller private share, the per capita growth rate comes down. And it’s been historically shown time and time again that when the per capita growth rate comes down, you exacerbate the income and wealth divides.

Lacy Hunt, my favorite “deflationista,” mentions the United States Chicago Fed National Activity Index as one he closely follows:

“The Chicago Fed National Activity Index (CFNAI) is designed to gauge overall economic activity and related inflationary pressure. The CFNAI is based on a weighted average of 85 existing monthly indicators of national economic activity.”

And also U.S. government current tax receipts:

Hunt’s Second Quarter 2023 review

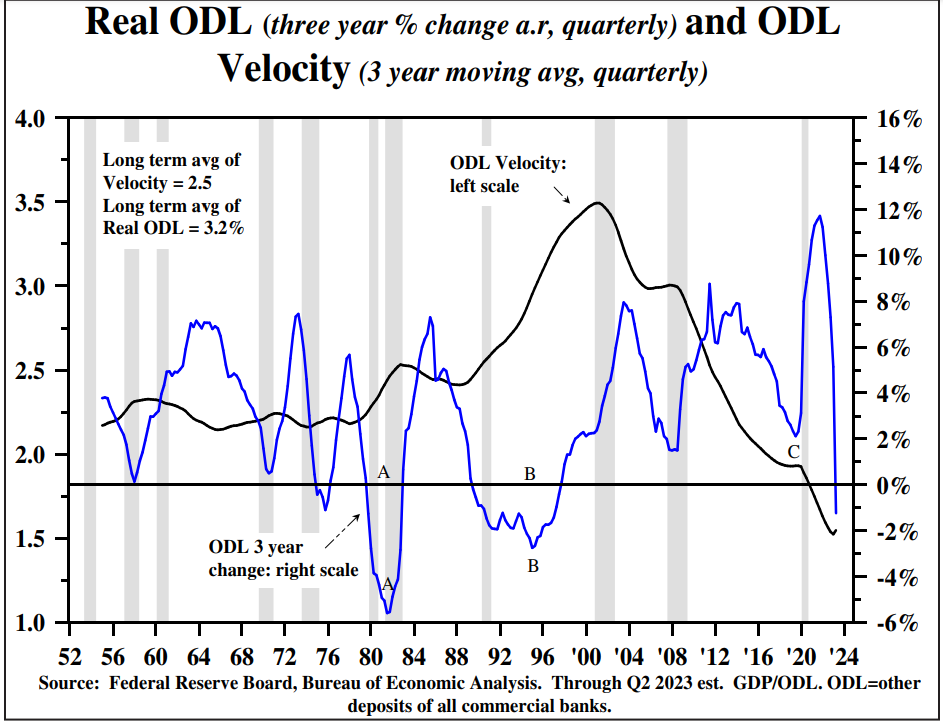

Lacy’s big on the “Other Deposit Liabilities” number (ODL):

Hunt: “Even a stable ODL-V will severely limit the Fed’s capabilities to stimulate economic growth. Monetary policy could be thwarted even more if V’s dominant determinants (the bank loan/deposit ratio and the marginal revenue product of debt) turn down.”

I have a problem with the assumption that the Fed has the wisdom to know how to stimulate economic growth. Almost no one at the Fed has ever grown anything other than their bank accounts and staff size.

Some may remember that we did have a $5 trillion pop in ODL in just two years, 2020-2022. Maybe that was ridiculous and needs to be corrected, as painful as that my be. A spiking cost of living has been very, very painful to a couple hundred million Americans lately.

Lacy Hunt’s final thoughts:

Other major considerations indicate that the U.S. economy is far weaker than recognized. Productivity, or output per hour in the nonfarm sector, declined by a record pace over the past ten quarters. Neither a rising standard of living nor increasing corporate profitability are achievable over time without higher productivity. For the eleven quarters since the pandemic/recession ended, real average hourly earnings (which cover 119 million full time wage and salaried workers) fell at a 2.9% annual rate. This is the largest decline registered in any economic expansion of comparable length since the earnings series originated. While firms continued to add employees, the rate of increase in wages have lagged inflation. Moreover, while establishments have continued to add employees, they have simultaneously reduced the number of hours that their staff are working. Since January, non-farm payrolls have increased by 1.2 million, but the average workweek has dropped from 34.6 hours to 34.4 hours, leaving aggregate hours worked virtually unchanged. To restore productivity, firms will need to rationalize their workforce, which will simultaneously reduce labor costs, inflation and household purchasing power.

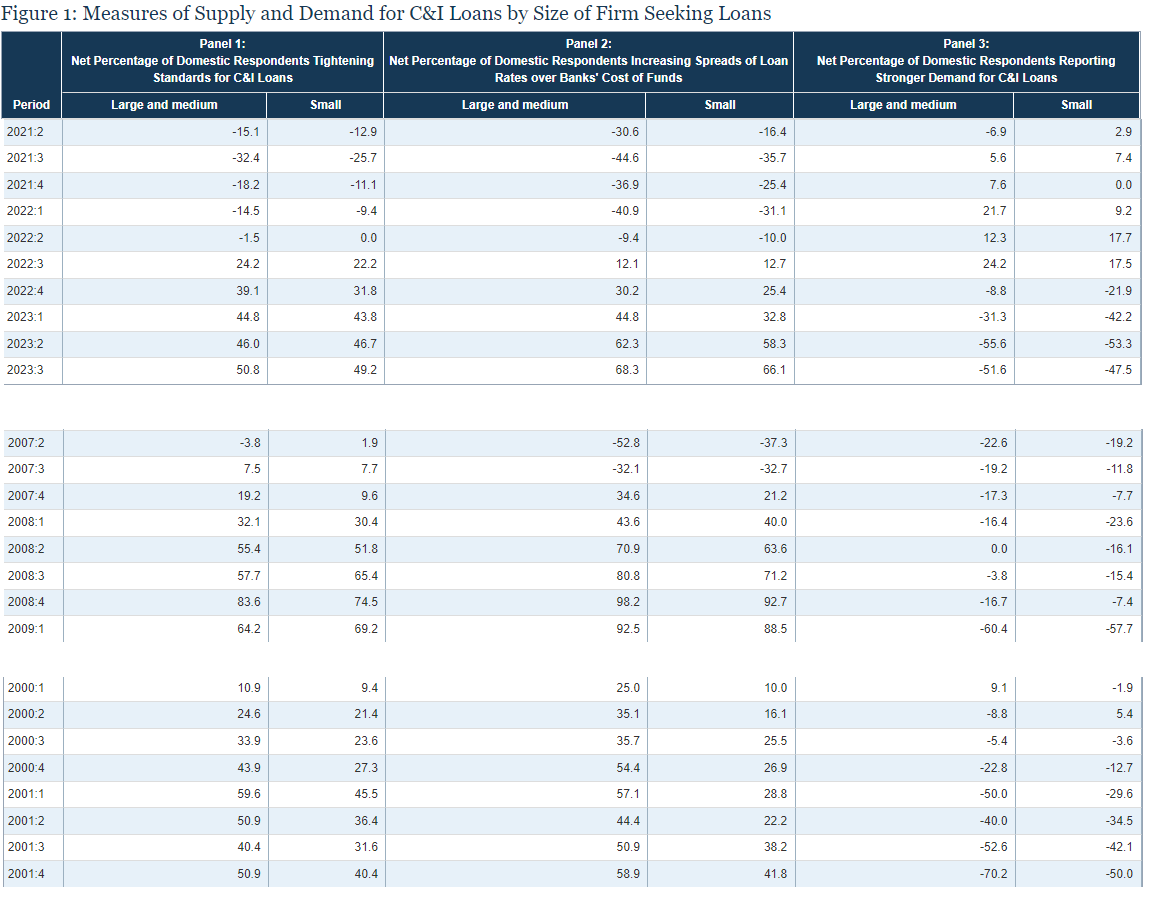

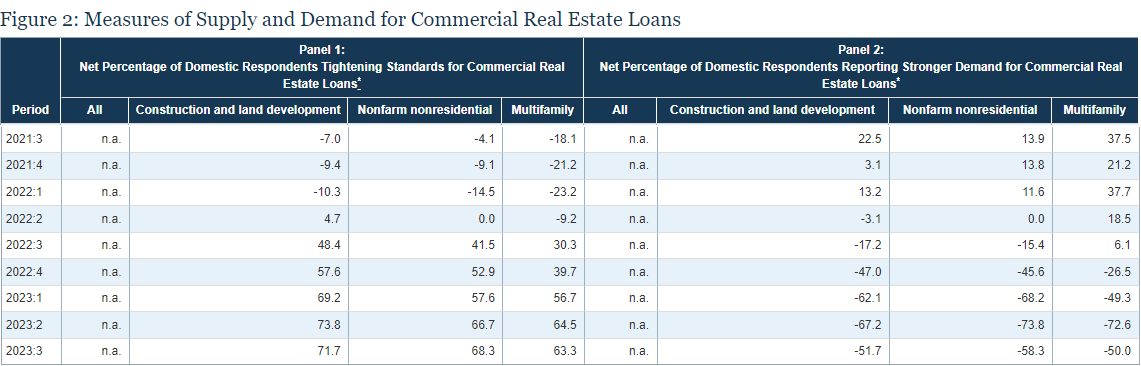

Senior Loan Officer Opinion Survey on Bank Lending Practices

Note that the total number of respondents is (I think) small (about 60).

This page comparing various years was most interesting to me. The C&I (commercial and industrial) loans had the most historical data.

CRE loans don’t have data apparently back from 2008. You can see how sentiment can move from one extreme to another fairly quickly. Human nature, something economists can never, ever seem to model (or consider).

“We see rapid value deterioration when you look at pricing changes across property types and regions,” said Chad Littell, national director of U.S. capital markets analytics for CoStar and author of monthly report on the indices. “No region has been spared. All four U.S. regional indexes fell into negative territory year over year for the first time in this cycle."

You can see a few (very few) signs of the dreaded “rental deflation” every tenant is terrified of here:

Credit Cards

Particularly in the US, plastic functions as both payments infrastructure and a source of credit. About 30 per cent of accounts are either new or inactive, and 21 per cent of accounts are transactors — they use the card and pay it off within the month. Almost 50 per cent, however, are either light revolvers or heavy revolvers.

It’s the revolvers who are paying the higher rates. They tend to have lower credit scores and lower incomes. Banks cherish heavy revolvers, who make up 20 per cent of accounts but hold 67 per cent of revolving balances, and pay 72 per cent of the banks’ total interest income on cards. Heavy revolvers aren’t responding to higher interest rates by backing off on debt because their balances are medium-term loans, not month-to-month choices.

Without heavy revolvers, the cards don’t make sense for banks.

Guess the date of this WSJ article…

A funny thing happened to the economy on its way to recession: It's taken a detour.

That, at least, is the view of a growing number of economists -- including some who not long ago were saying a recession was all but inevitable. They note that stock and credit markets have steadily improved since the Federal Reserve intervened to keep Bear Stearns Cos. from bankruptcy in early March, while a series of economic reports have been stronger than expected…

Global Insight's Brian Bethune says that while the firm is still forecasting a recession, "it's conceivable we could avoid it," thanks to "the massive policy response we've seen"

In hindsight, imagine thinking that what the Fed had done by May 14, 2008 was a “massive policy response,” compared to the tsunami of corrupt corporatist-bailouts that was yet to come.

Did I mention that Bernanke now works for Ken Griffin?

Case-Shiller Home Price to Gold Ratio

I think this chart simply shows that gold has retained its purchasing power re:housing for the past 130+ years, which is all one could ask.

Home Price to Median Household Income Ratio

What’s Barry Sternlicht’s household income?

The 1920’s Florida Housing Bubble

Again I’m reminded of Rick Rules maxim:

"I learned that my assets were ephemeral, while my debts were money-good."

Continental came up with a plan. It would offer short-term promissory notes to ordinary men and women at an extremely attractive 12 percent rate of interest. In exchange, these ordinary investors would contribute at least $10,000, and after four years of monthly interest checks they would get their principal back.3 In other words, $10,000 went out and over a four-year period some $14,800 came in. It was an incredible deal, but the beauty of it, insisted Aten, wasn’t just the high rate of return, which doubled what banks were offering. It was that the notes were collateralized by valuable installment lots that Continental itself owned, but on which buyers were making payments, hence the term “first mortgage.” In fact, Aten told Phil that Continental had a policy in which it backed every dollar invested with at least twice that in land, so if he gave the company $10,000, Continental would secure the investment with $20,000 in lots. Bottom line: the Profitas couldn’t lose.

Thus convinced, in 1972 the couple handed Aten their life’s savings, $21,000, and for more than a year, checks arrived like clockwork. But, in early 1974, with no warning whatsoever, they stopped, and in April, the federal Securities and Exchange Commission (SEC) accused Homestate, a different brokerage firm in Fort Lauderdale named Hartwell & Associates, Continental Land Management, and four other Continental-owned companies of fraud. A court named a receiver, and in the fall of 1974, Homestate and Hartwell lost their licenses while Continental went bankrupt.

History repeats…

Easy money, whether legal or illegal, fuels every investment boom. One of the most important sources of cash throughout Florida’s frenzy was an “accommodative” Federal Reserve. The Fed lowered its key lending rate, the fed funds rate (the rate at which the Fed lends to other banks), from 4.5 percent in 1920 to 3.0 percent in 1922 and then raised it again, but only modestly, to 3.5 percent in 1925. From then on, the central bank let the US economy roar.

The Fed went even more insane post-2008.

Corrugated box demand continues to disappoint.

Good news for cheap housing?

PPI Watch

Year-over-year performance. I crossed off the things that aren’t real. Oil is down about 11%, but gasoline is up 32%.

To search my substack posts for something, e.g., “Jeremy Grantham”, try this in Google:

jeremy grantham site:rudy.substack.com

Works a lot better than the general Substack search.

"Garry Nolan’s talk at SALT last week was blunt. It is “100% certain” that we are not alone and that this “other” has likely been with us since the beginning of time."

Saw a meme somewhere in the last couple of days. Something like, "I believed in aliens and space vehicles until the govertment started telling me they are real." I'm come to the place that if any governmental organization tells me anything . . . literally anything . . . I assume it's a lie.

Love that Tighten Up! -- a soundtrack for yield curve inversion, but Rudy Havenstein you need the music video dance steps too....https://youtu.be/U239gi6cQFU?t=198 so we can all be Chuck Prince.