We are all frogs boiling slowly in a fiat pot.

"Best in class."

I had CNBS on in the background of my ThinkorSwim app (I know, I know,) and they spent seemingly about 14 hours today promoting the WWE/UFC merger, before Scott “Leave Jamie Dimon Alone!” Wapner disclosed that he is in fact represented - along with other CNBS personalities" - by “talent” agency William Morris Endeavor (WME), which - in a bizarre coincidence - owns WWE!

So apparently the new Twitter Vice President of Trust and Safety also used to work for - you’re never going to believe this - Jamie Dimon and Brian Moynihan for over nine years.

Since my primary raison d'être has been to highlight the destructive influence of men like them, I found her history (or herstory) amusing.

Thanks for the info, Occupy the Fed.

“One certainty in politics is that the Federal Reserve will never accept responsibility for any financial problem.”

When you’ve even lost the Wall Street Journal’s editorial board…

When monetary policy creates perverse incentives with negative real interest rates for years, regulators have a particular obligation to watch for banking mistakes and rising risks. And when interest rates suddenly turn upward to correct the Fed’s monetary mistake, examiners have an obligation to impel bankers to hedge or unwind their interest-rate risks.

Shifting Downward: How a Change in Fed Culture Hurt Bank Supervision

We agree that the explanation of systematic breakdowns in supervisory oversight over time must include the shift in Federal Reserve culture during and after the 1990s. In the late 1970s and throughout the 1980s, William Taylor, a tough-minded supervisor, rose through the ranks to become the director of the Division of Banking Supervision and Regulation (BS&R) at the Fed’s Board of Governors. Taylor was a dominant figure, and under Taylor, BS&R was a force to be reckoned with in internal Board politics.

The exit of Taylor from the Board, following his appointments by President George H.W. Bush as the first head of the Resolution Trust Corporation in 1990 and as FDIC Chair in 1991, left a power vacuum in BS&R and shifted supervisory policymaking power at the Board from BS&R to the Division of Research and Statistics (Research), home of most of the Board’s staff economists. Under the leadership of Fed Chair Alan Greenspan during the comparatively stable banking environment of the 1990s, the Fed’s supervisory culture moved from an audit/compliance model toward a more consultative approach. This consultative approach became known internally as “value-added supervision.”

The growing influence of Research at the Fed occurred while innovations in computing and information technology were transforming risk management in large financial firms. By 1997 supervision of what eventually become known as Systemically Important Financial Institutions (SIFIs) began to use a more model-based approach focused on leveraging the SIFI’s own risk modeling to supervise them, using data submitted by the SIFIs. Traditional on-site field examinations were curtailed. The problems with this approach are that the institutions’ own models might be easy to influence or alter, important institutional structural details might be ignored, and over time institutional knowledge would be lost.

The PhD’s took over bank regulation and started using MODELS - using data submitted by the SIFIs - instead of on-site real work. They replaced Columbo with a math nerd.

This narrative fits in exactly with Alan Boyce’s comments I posted just the other day, and with Neel Barofsky’s revealing account of Neel Kashkari’s attitude towards regulation during the 2008 coup:

We met with Kashkari the day after the inauguration to tell him about the audit, and beforehand I asked Kevin if he thought that maybe we had misjudged him. If Treasury had decided to probe into how much lending the banks were doing, it might be appreciative that we were going out and painting a more complete picture for them.

Kevin told me he thought the Costa Rican sun must have melted my brain.

He was right. When we told Kashkari about the letters, his response was even worse than Kevin had expected.

“You can’t do this, you can’t,” he warned.

When I asked him why not, he rolled his eyes and snapped back, “Because it will destroy the program.”

“How will it do that?” I asked.

“Banks will run away from it. Your audit will scare them off,” he responded.

I explained to him that it shouldn’t be a shock to the banks that a survey like this was coming. After all, I said, Treasury had already sent its own survey, and a bill that had passed the House that day required even more robust reporting than what we would call for in the audit. In addition, the banking regulators, to varying degrees, had also indicated that they would launch some type of initiative to measure uses of TARP funds.

“It’s different,” he argued. “The banks view you as the TARP special prosecutor. They’re terrified of you. They view their regulators differently. They know them. They trust the regulator who is on site all week with them. You are a lot different than the guy who has a beer with them every Friday night.”

Unbelievable, I thought. [Kashkari] actually seemed to be arguing that the banks’ comfort with their thoroughly captured regulators was a good thing.

Make sure you check out my post of Fed Vice Chair for Supervision Michael Barr testifying last week before the Senate. He reminded me a bit of this restaurant manager:

Wall Street on Parade again puts things in understandable terms: After Being Criminally Charged for Rigging Precious Metals, JPMorgan Chase Controls 53 Percent of All Precious Metals Contracts Held by Banks

Stupid annoying article of the day: Is Apartment-phobia Driving America’s Housing Crisis?

OK, first of all there’s this common claim: “Over the past ten years, the number of housing units per 1,000 people in the U.S. has actually fallen.”

If you click the link he uses to justify this claim, you get send to a second stupidly annoying article of the day: The Anglosphere needs to learn to love apartment living (remember - “you will own nothing and be happy” is the mantra of the people these financial writers work for.)

Both articles are just dripping with the sort of smug, condescending sense of superiority all too typical among today’s media propagandists.

We hear all the time about the “housing shortage.”

Because I’m skeptical and simple, I think - why not look at the census bureau’s quarterly, “Total Housing Units in the United States,” and divide that by the population?

The data only goes back to 2002 on the Fed’s FRED site, but it seems to me that - just being simple here - housing units per capita is at a 20-year high, so maybe the “housing shortage” that everyone talks about as fact is, in fact, not a fact.

That said, I’d agree there is an “affordable housing shortage,” (which I blame more on prices - massively inflated by the Fed’s ridiculous QE and ZIRP - than rates, or Americans’ apparently weird fetish for private homes), but I’m afraid I question the premise of annoying article of the day #1.

As an aside, I can’t afford to live in Monaco. Does that mean Monaco has a housing shortage?

The author then goes off to write florid prose like:

What is it about living in an English-speaking country that turns people against high-rises? Burn-Murdoch posits that England’s colonies inherited the motherland’s peculiar fetishization of private, country living…an inherited cultural affinity for single-family housing…apartment-phobia

Fetishization! I want to throw a tomato at this guy.

Maybe there’s a reason so many people want to come to America. Part of it is the ‘American Dream’ of homeownership. Maybe the author and many others don’t want that, and that’s fine, but his peculiar antipathy for people who don’t want to live in an urban apartment is annoying. Has he been to downtown L.A. lately?

The author wrote another article recently titled, “Is AI Turning Me Into an Obsolete Machine?” I for one hope so.

The FT article is similar:

when asked if they would like to live in an apartment in a 3-4-floor block — picture the elegant streets of Paris, Barcelona or Rome — Britons and Americans say “no” by roughly 40 per cent and 30 per cent respectively, whereas continental Europeans are strongly in favour.

The FT author is apparently appalled by this, but maybe there’s a reason my ancestors and so many others left Europe.

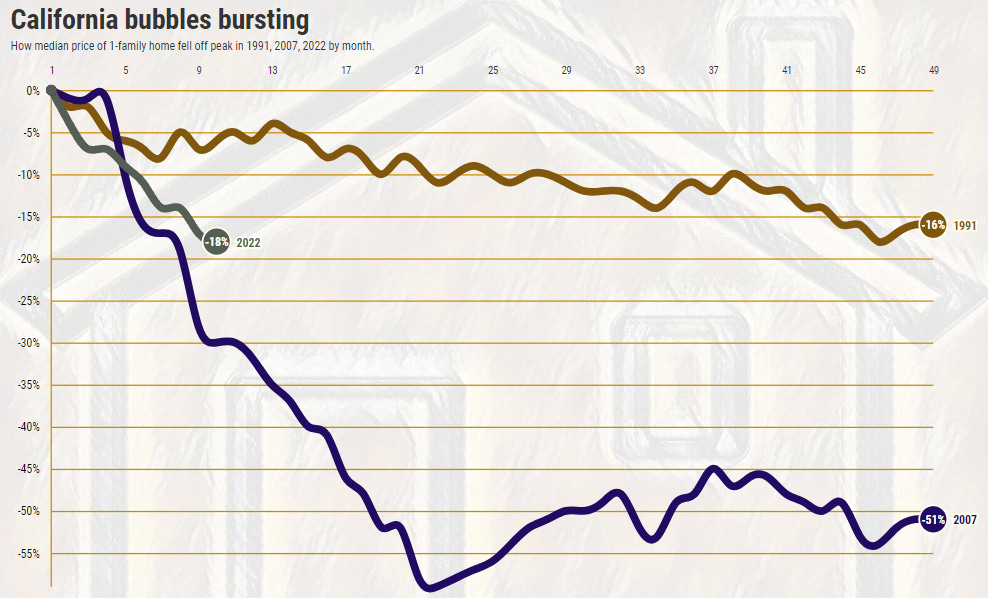

California’s housing bubble pops as Fed shuts the pump Median price of single-family home in California is 18% off May 2022's high.

It’s like saying we came down from Mt. Everest and now are correcting on K2.

I remember emailing the Times author Lasner during the run-up to the prior housing bubble, with examples of housing insanity. I don’t remember him being interested.

Also, define “popped”: Black Knight Mortgage Monitor: Home Prices Increased Slightly in February; Prices Up 1.9% YoY

Investors purchased about 30% of all single-family homes in the Dallas-Fort Worth area last year. Wow, even in 2022 investors were still going nuts.

High inflation boosts public finances, IMF says It sometimes seems like the headlines are targeted specifically at me (but I can’t prove it...)

Because I’m a glutton for punishment, I listened to Peter Stella & Joseph Wang on Debt Death Spirals, Monetarism, and The Fiscal Theory Of The Price Level. Wang and Farley are ok, it’s ex-IMF people I can do without (and I’m sure they can do without me.) Regardless, Peter Stella meant well.

The TL;DR version is out of the MMT playbook. Stella seems to suggest that the more debt you have in your own currency, the less inflation you need to debase the debt. And boy, do they really want to debase the debt. Putting our fiscal houses in order isn’t even on their radar. The mental gymnastics going on in this interview is impressive (but I’ll give Stella credit for at least recognizing the MBS monetization was stupid.) Down is up.

The real takeaway is that central banks and governments - in our fiat world, WANT high inflation - just not so high that you revolt.

They think they're much, much smarter than the central bankers of 100 years ago.

We are all frogs boiling slowly in a fiat pot.

On a related note, a tidal wave into bonds?

I’m reminded of Porter Stansberry’s comments recently:

"The idea that as a retired investor you should have a substantial investment in bonds, in my opinion, is ridiculous, in a world of paper money and negative real yields. Absolutely horrible advice."

None of anything I write is investment advice, just thinking out loud.

Note how we were well on our way to recession long before Covid hit.

I’m reminded again of one of my favorite newer conspiracy theories:

A SELF-FULFILLING PROPHECY: SYSTEMIC COLLAPSE AND PANDEMIC SIMULATION by Fabio Vighi

"The mainstream narrative should therefore be reversed: the stock market did not collapse (in March 2020) because lockdowns had to be imposed; rather, lockdowns had to be imposed because financial markets were collapsing."

I’m not a Bitcoin guy, but Elizabeth Warren makes about as much sense as Kamala Harris in this anti-Bitcoin rant. Calm down, grandma!

Someone sent me this by one of my favorite financial writers:

How to Wreck a “Big Old” GSIB Bank…

Here goes…here’s my one sentence, layman’s summary:

“Silicon Valley Bank experienced huge amounts of money coming in (deposit inflows) of unknown/questionable origin over the last three years, forcing management to ‘invest’ this cash…and because of our wonderfully safe, highly regulated fractional reserve banking system, they were allowed to keep only about 5%+/- of deposits in cash (2%) and ‘equivalents’ (3%) on hand to maximize their returns/leverage, and they ‘invested’ the rest.. which, unfortunately, they often ‘invested’ in less than liquid ‘stuff’ that they could try to sell if they needed money….but, sadly they couldn’t sell this ‘stuff’ for what they paid for it, and …so when (almost all) of their depositors wanted their money back in a big hurry, they had to sell a bunch of ‘stuff’ at gigantic losses, and that was that….. and even after all of that, they still couldn’t pay the depositors their money back ….and the FDIC came in all pissy, yelled at everybody for a little while, and closed ’em down and paid all of the depositors and sold off what was left to other banks and dudes for pennies on the dollar.”

There you have it….that’s exactly what happened….one poorly constructed sentence…explained in a way that you and I…. and a bank regulator or Central Banker can understand it.

Bob’s posts have to be more studied than passively read - that’s a compliment, by the way. He’s very blunt and funny too.

Someone asked for Classical Music.

A SELF-FULFILLING PROPHECY: SYSTEMIC COLLAPSE AND PANDEMIC SIMULATION by Fabio Vighi was a fascinating read!

You outdid yourself on this post....and my neighbors may have already called the paddy wagon (a little benefit of apartment living) as I was laughing so loudly - that camel bedspread on Nick....priceless. If asked, I'm sure they will tell my other neighbors "it was a general disturbance". Both of those articles on housing are shockingly bad, but can you blame Eric? He's a failed fiction writer trying to make a buck ;). This shilling of "low inventory" at some point should bring criminal consequences. Someone told me that they were reading something from NAR from 2008 that blamed everything again on inventory. I mean, don't we have cutting-edge technology that could tell us actually how many people inhabit certain cities, etc.? Sigh.

Amazing work as usual!