"The only safe asset is actually human capital itself, and the best investment you can make is in the skills of your children."

“There's no living soul who believes we've only been through 23% inflation over four years. It's absurd…Once you take out government spending and take out government debt and then adjust those figures by a realistic measure of inflation…it looks to me as if we have not ever recovered from March 2020, that we might be in the equivalent of a Great Depression now. ”

This is how distorted our goofy economists' and their stenographers' thinking is:

"Consumer prices rose 0.2 per cent year on year in June...a retreat from an 0.3 per cent rise in May...The risk of deflation has not faded..."

Nobody in normal person world fears lower prices. The FT set me off last year with a similar article:

"Falling pork prices threaten to push China back into deflation”

As I noted at the time, notice the subtle assumptions in the article: “Deflation” (lower food prices) “would UNDERCUT officials’ efforts to restore CONFIDENCE in China’s economy.”

Therefore, higher food prices must make people confident!

It's insane thinking, and it's everywhere in the MSM.

Gallup Poll Results On Economic Confidence – Notable Excerpts

“Twenty-five percent of Americans describe current U.S. economic conditions as “excellent” or “good,” up three points from May. However, the percentage rating conditions “poor,” now 48%, also increased slightly, blunting positive movement in the index. The high proportion of Americans rating the economy as poor continues the dominance of this response in the trend since early 2022…

Americans have also been consistently more negative than positive since May 2021 in their assessments of the economy’s trajectory. The June 2024 survey finds that about seven in 10 Americans (69%) believe the economy is “getting worse,” while 26% say it is “getting better.” This is essentially unchanged from last month.”

CPI first hit about 5% in May 2021.

The stock market is off the charts (literally), but half of America owns none of it, and as for the rest of the little people:

“Over the last few years, as a result of the COVID pandemic and high inflation, small business sentiment closely resembles that of the Great Recession and its aftermath.”

”We compare the NFIB Small Business Optimism Index with the University of Michigan Consumer Sentiment Index. Again, we've plotted each index on a separate axis, however in this chart, we can see that the business measure is more volatile of the two. Despite the volatility though, we can see that these two measures of mood (business and consumer) have been highly correlated, falling and rising together for the most part.”

Everyone and their mother now really expects a rate cut (this time they mean it!) Be careful what you wish for.

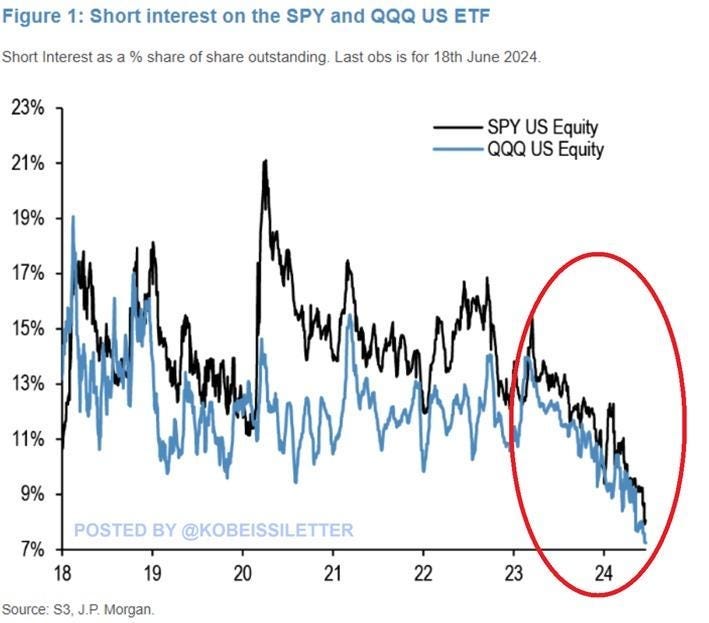

As of mid-June, (almost) nobody’s short.

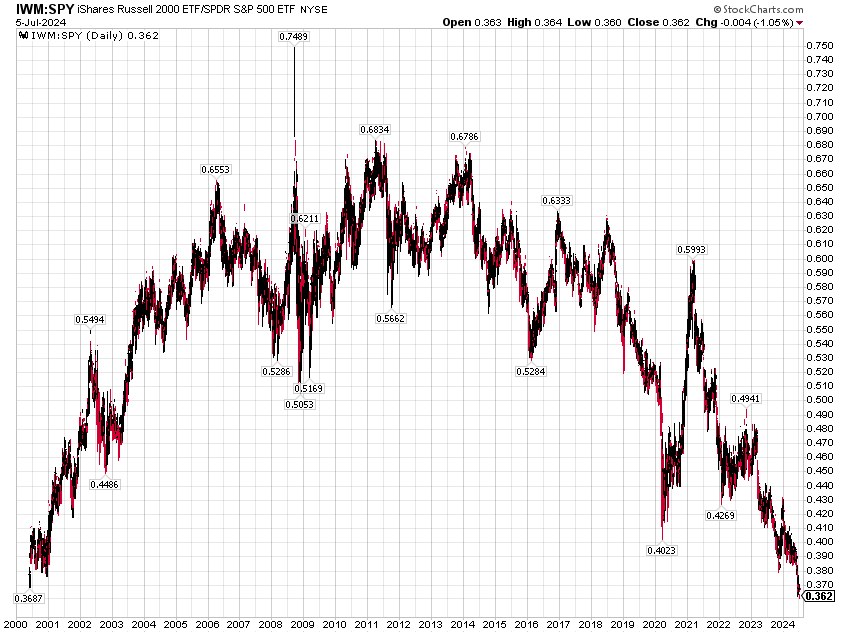

Russell 2000 vs S&P 500

J.C. Parets noted this on the Twitter

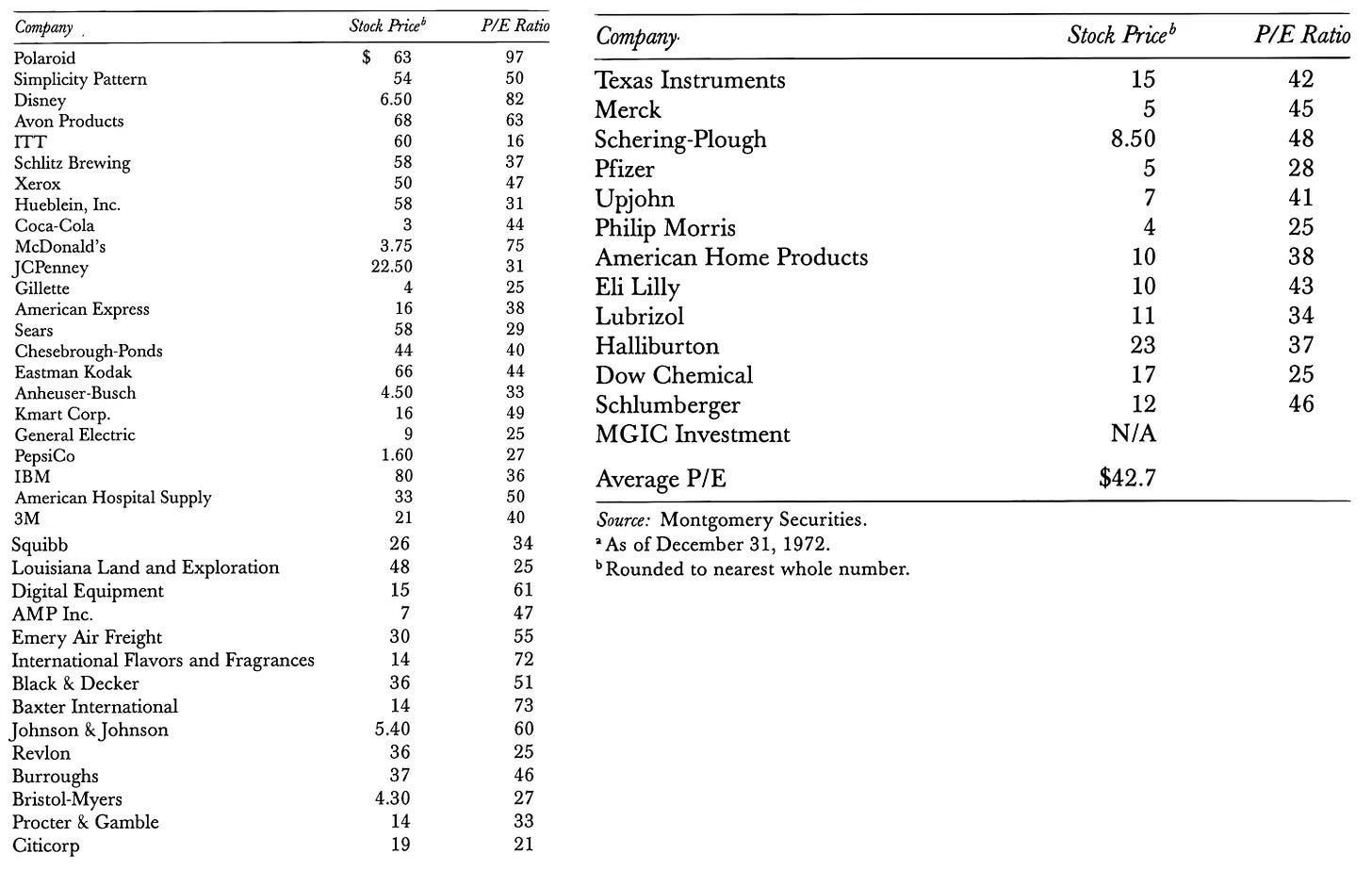

It’s the Nifty-Fifty1, except now it’s more like Nifty Five.

“There have been moments when real, live, hands-on professional investors have entertained dreams as wild as that-moments when the laws of probability are forgotten. In the late 1960s and early 1970s, major institutional portfolio managers became so enamored with the idea of growth in general, and with the so-called "Nifty-Fifty" growth stocks in particular, that they were willing to pay any price at all for the privilege of owning shares in companies like Xerox, Coca-Cola, IBM, and Polaroid. These investment managers defined the risk in the Nifty Fifty, not as the risk of overpaying, but as the risk of not owning them: the growth prospects seemed so certain that the future level of earnings and dividends would, in God's good time, always justify whatever price they paid. They considered the risk of paying too much to be minuscule compared with the risk of buying shares, even at a low price, in companies like Union Carbide or General Motors, whose fortunes were uncertain because of their exposure to business cycles and competition.

This view reached such an extreme point that investors ended up by placing the same total market value on small companies like International Flavors and Fragrances, with sales of only $138 million, as they placed on a less glamorous business like U.S. Steel, with sales of $5 billion. In December 1972, Polaroid was selling for 96 times its 1972 earnings, McDonald's was selling for 80 times, and IFF was selling for 73 times; the Standard & Poor's Index of 500 stocks was selling at an average of 19 times. The dividend yields on the Nifty-Fifty averaged less than half the average yield on the 500 stocks in the S&P Index.”

“Nobody gets fired for buying IBM”2

“A New Age of Finance”

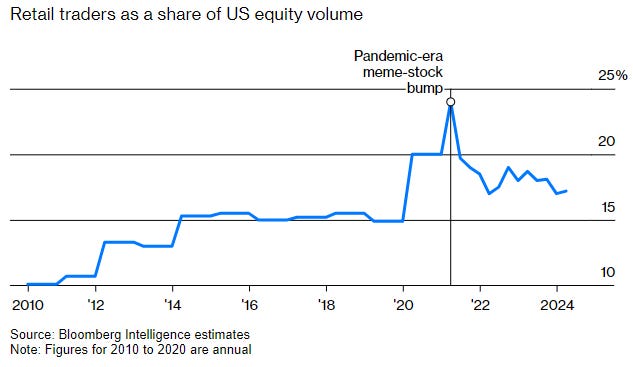

“Legions of retail investors flooded the stock market in 2021, eager to chase volatile “meme stocks” with strong social media followings and weak financials. This passion to own a piece of companies such as GameStop Corp. and AMC Entertainment Holdings Inc. seemed like a fever that was sure to break. Fueled by pandemic stimulus checks and pre-vaccine boredom, newbie traders had nothing better to do than funnel their cash into shares championed by internet investing gurus including Keith Gill and Ryan Cohen.

Flash-forward three years, and it’s abundantly clear: We’re living in a new age of finance. It’s never been easier to bet your money—anytime, anywhere—and meme-stock craziness is here to stay. A wave of technological advancements has coincided with new apps and platforms to create a thriving ecosystem where everyday people can trade stocks with the ease of swiping for dates on Tinder.”

From Grant’s: “the S&P 500’s 10 largest stocks have generated 58% of the index’s 55% return from its fall 2022 lows, pushing that cohort’s share of the market cap-weighted gauge to some 37%. For context, the top 10 names collectively commanded 27% of the S&P 500 at the climax of the dot-com boom in March 2000, JPMorgan Asset Management pointed out last month.”

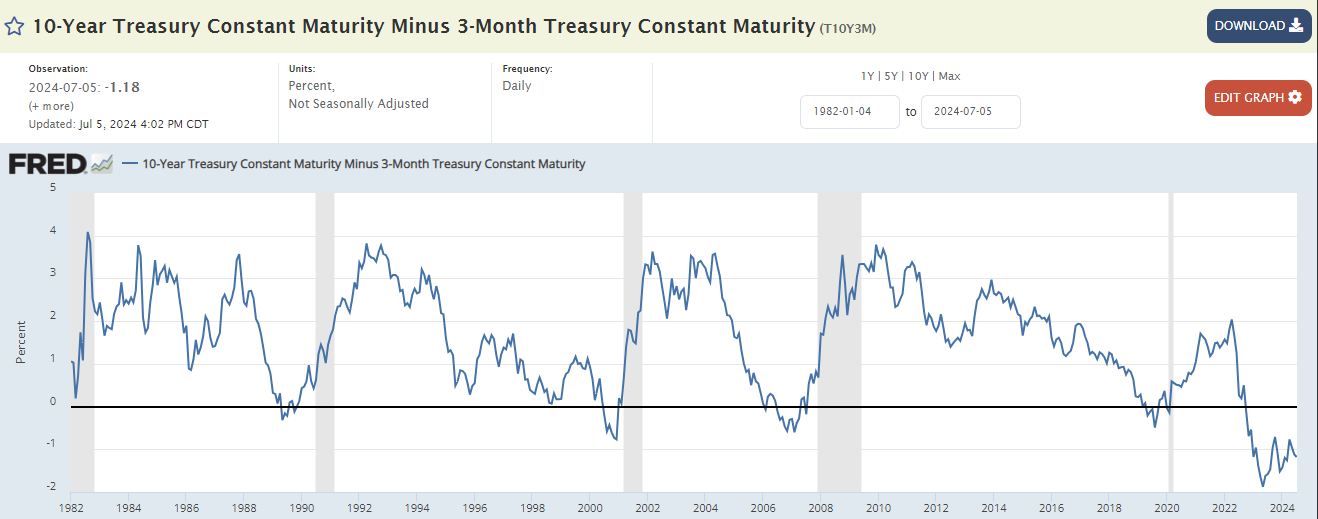

Nevertheless, the yield curve inversion persisted.

Rates

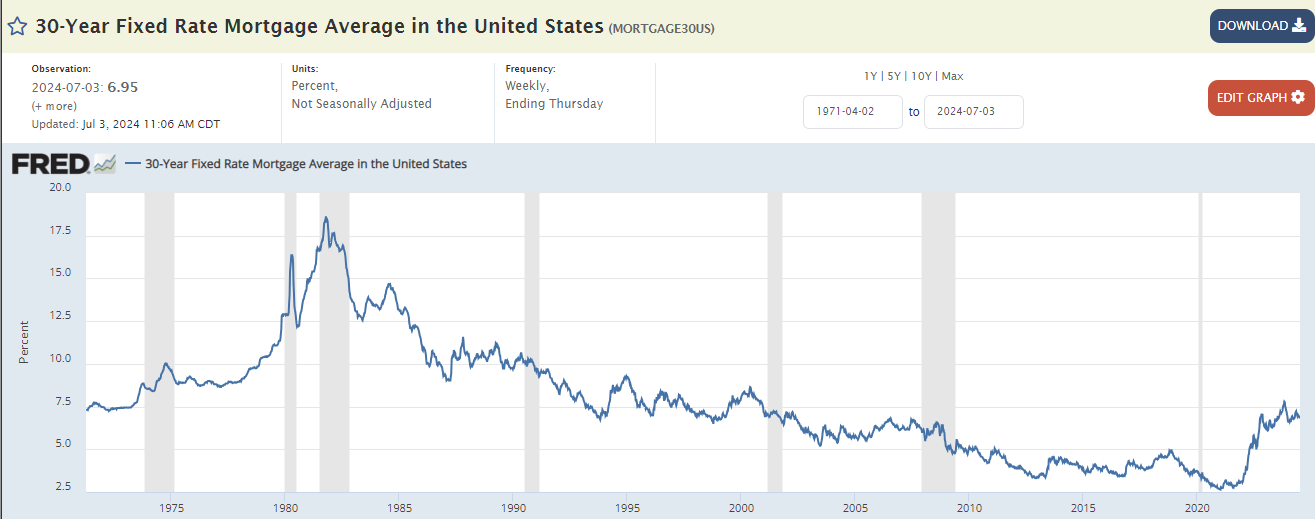

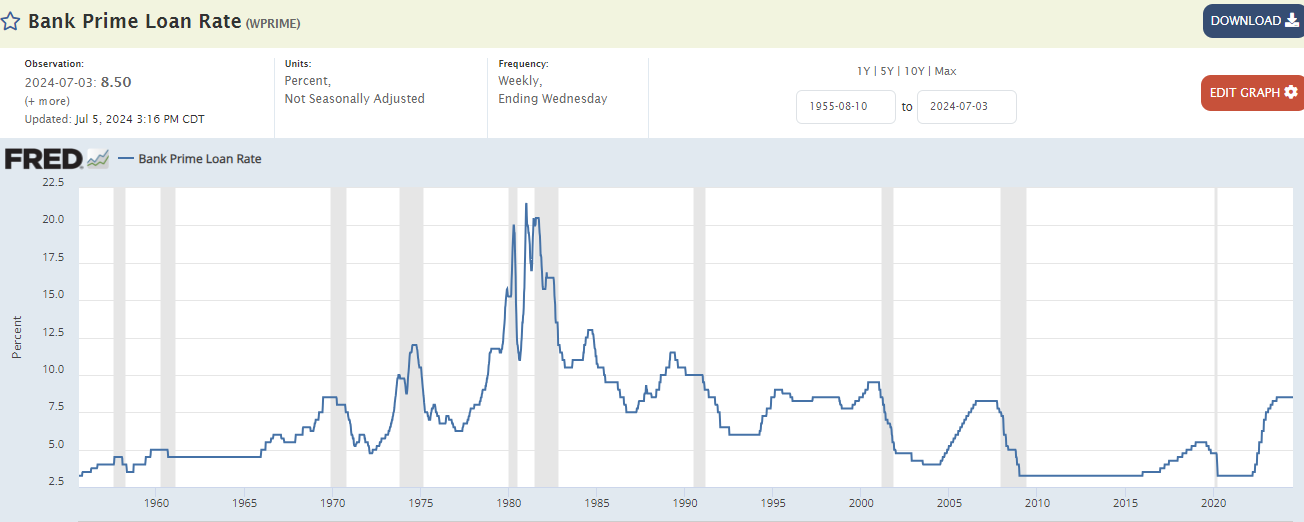

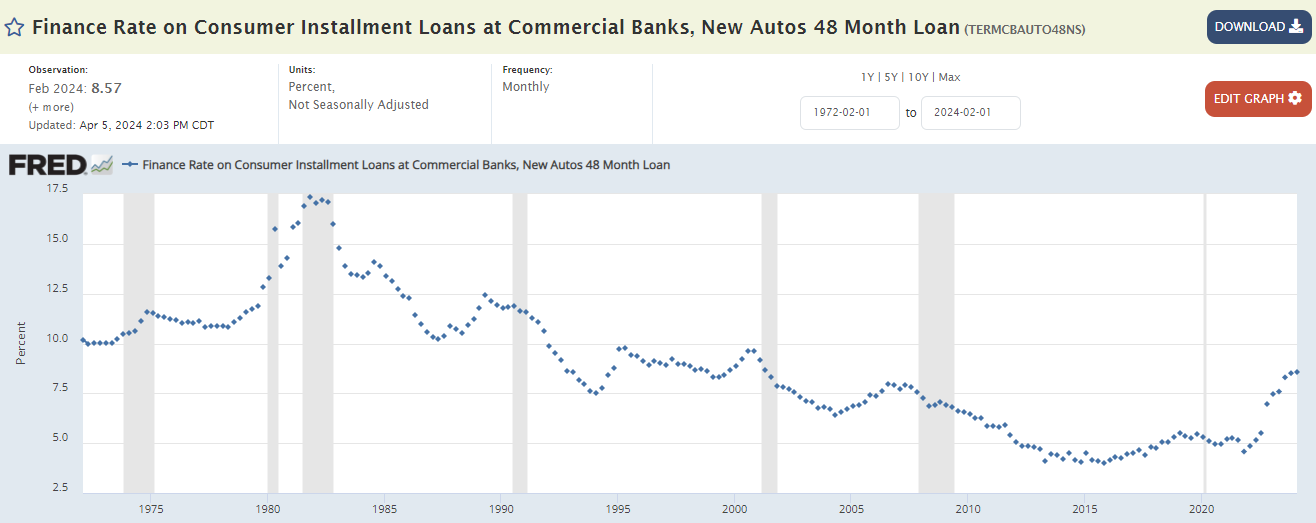

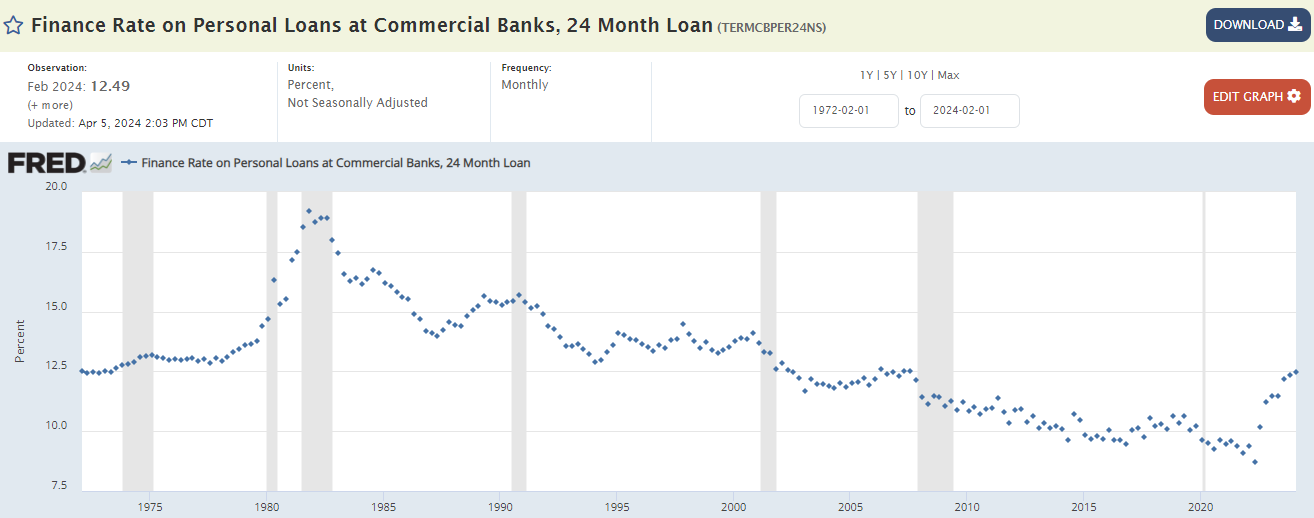

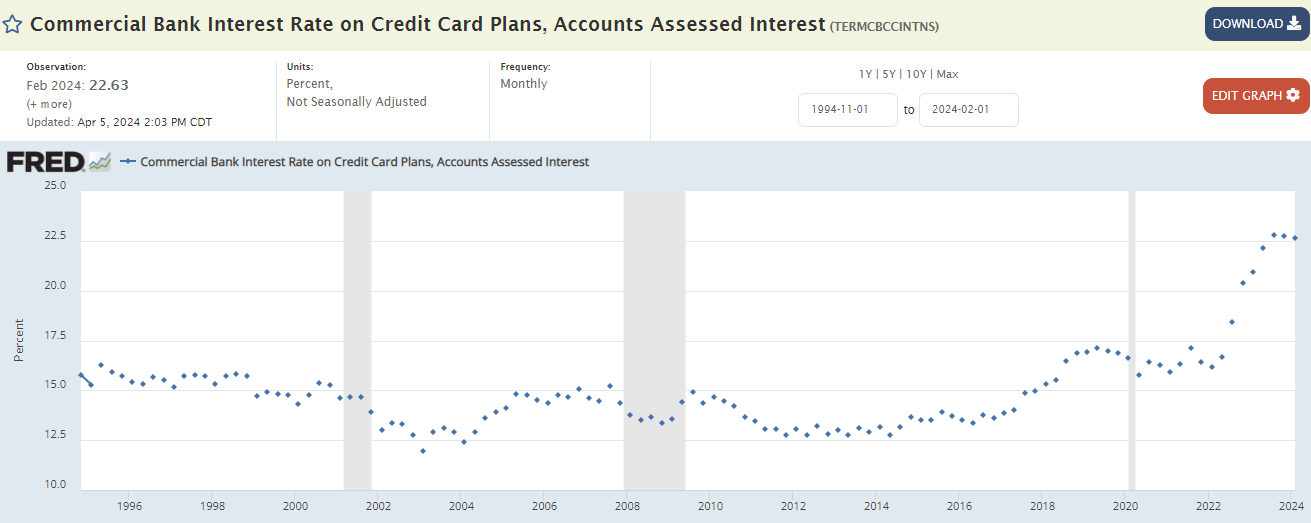

A mixed bag. Some rates are historically normal (e.g., mortgage rates, new auto loans), and some are high (credit cards, Bank Prime Rate).

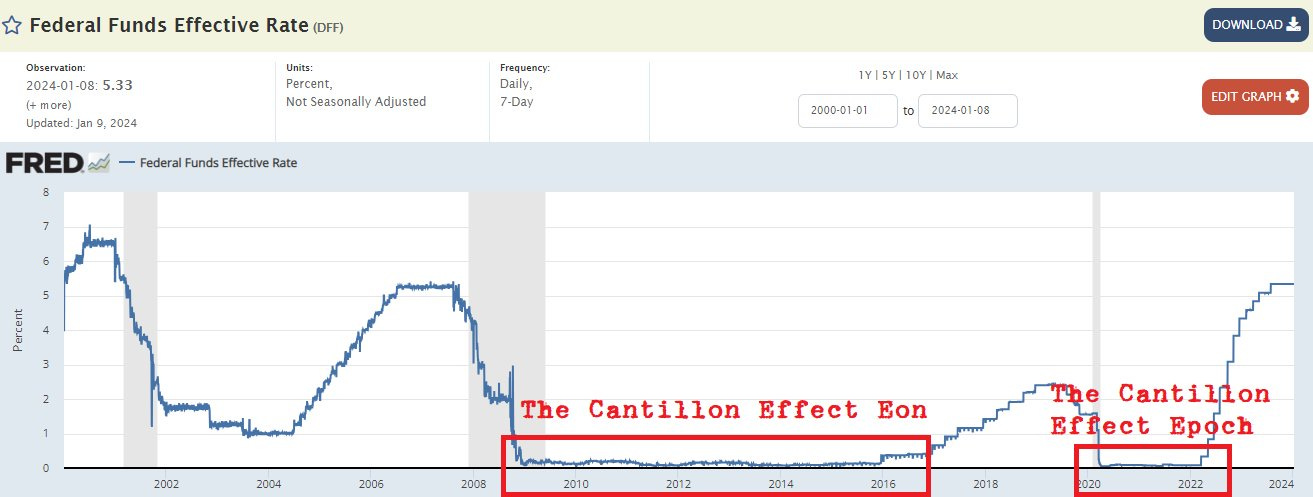

Remember, we recently lived through the most insane period of global monetary policy, ever (so far!):

Personally I don’t care if the Fed cuts a couple points if they ramped up QT beyond the joke that it is (and get rid of the MBS, where they still hold $2.335 TRillion, versus $0 in 2008.)

30-year Mortgage: 6.95%

Bank Prime Loan Rate: 8.5%. 69-year average: 6.83%, median 6.0%.

Bank, New Autos, 48-month loan: 8.57% (average since 1972 is about 8.9%).

Personal Bank Loan, 24-months: 12.49% (average since 1972 is 12.9%).

Credit Card Rates on Accounts Assessed Interest: 22.63% (Average since 1994 is 15%).

10-Year Treasury Yield

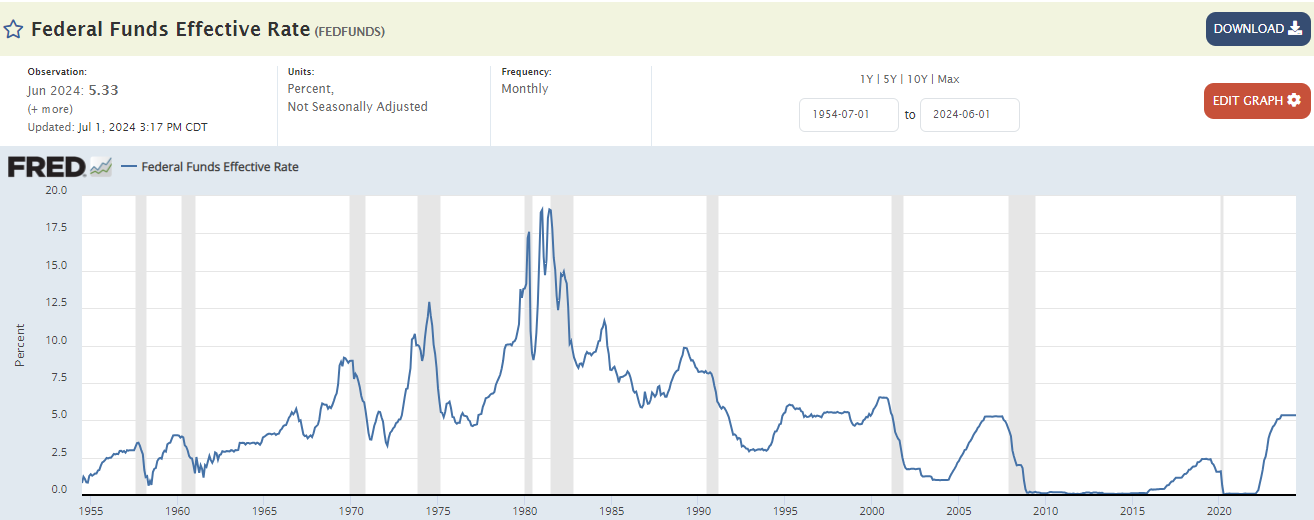

Fed Funds Rate

"Who is buying 4.3% 10-year Treasuries when the federal government alone is driving 5% nominal GDP growth? I would love them on the other side of all my trades. It would be awesome. It makes no sense to me."

"You know, three years ago - it sounds crazy - but people were paying for the honor of lending to France for 10 years."

I posted this on July 8, 2021:

Personal Saving Rate

3.9% as of May 2024. The 65-year average is 8.5%, and the median is 8.4%.

Real Estate

Thousands of homeowners are about to get slammed with higher monthly payments

“Last year, when Jennifer Hernandez received notice that the mortgage payments on her Houston home would jump about $2,000 per month, she was stunned. Hernandez refinanced her home loan in 2016 using an adjustable-rate mortgage loan, which has a low introductory rate for a fixed initial period…

According to data from Intercontinental Exchange, a global provider of technology and data, 1.7 million homeowners have bought homes with adjustable-rate mortgages since 2019. Many buyers who bought 5-year ARMs – one of the more popular offerings – will graduate into significantly higher monthly payments this year…

Hernandez, who is herself a loan officer, had misremembered the terms of her $1.1 million loan: rather than a 10/1 ARM, which has a fixed rate for the first ten years and resets every year after that, Hernandez had taken out a 7/1 loan.”

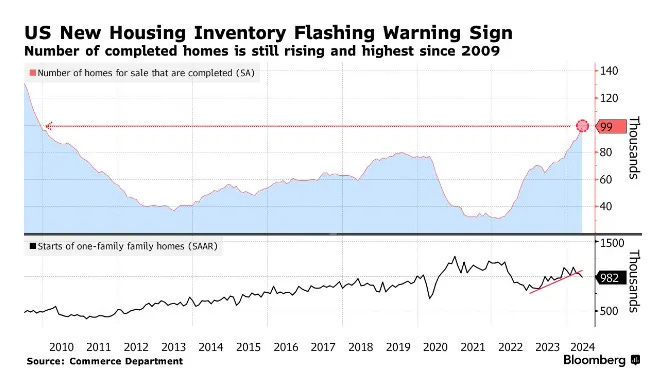

The inventory of new US homes stands at the highest since the bursting of the housing bubble more than a decade ago, raising the risk that builders will dial back production in a market longing for cheaper borrowing costs. The total number of one-family homes for sale rose to 481,000 in May, the highest since 2008, according to fresh government data released Wednesday. Nearly 100,000 of those have already been completed and are still awaiting a buyer, the most in more than 14 years.

Real Estate Brokers Todd Sachs (Maryland) and John Hoffman (Illinois)

Todd: “We're going to play a couple videos here and talk about the reality of what John does a lot of, and that is dealing with foreclosures.”

John: “These modifications - I know their intentions are great - but it isn't going to work. We're going to have all this fallout from this. These people can't afford it to begin with, and the maintenance items are the first things to go.”

They talk for over 2 hours, but here’s a sobering 14 minutes:

Melody Wright’s comment on this video:

“Besieged” by requests for drive-by appraisals which are required at 90 days delinquency. Just because you can’t see it in the data sources you KNOW about does not mean it isn’t happening. Hidden delinquencies.

”Poor doesn't mean dirty.”

“It's time to go and let a new buyer who, you know, is ready, excited and able to buy as their first home. Let them take a swing at this place now, you know, but we just keep these people - it's just dumb at this point, you know, and it's getting worse…We’re keeping them in too long. That's my number one complaint. We're kicking the can down the road on all this stuff.”

If you like Sachs, check out this discussion from last month on the new Freddie Mac second mortgage program. Basically, besides being a (small) bank and credit card bailout, it’ll allow “underserved” people to turn non-recourse debt into a foreclosure.

Phoenix Evictions

Of course, it has been hot.

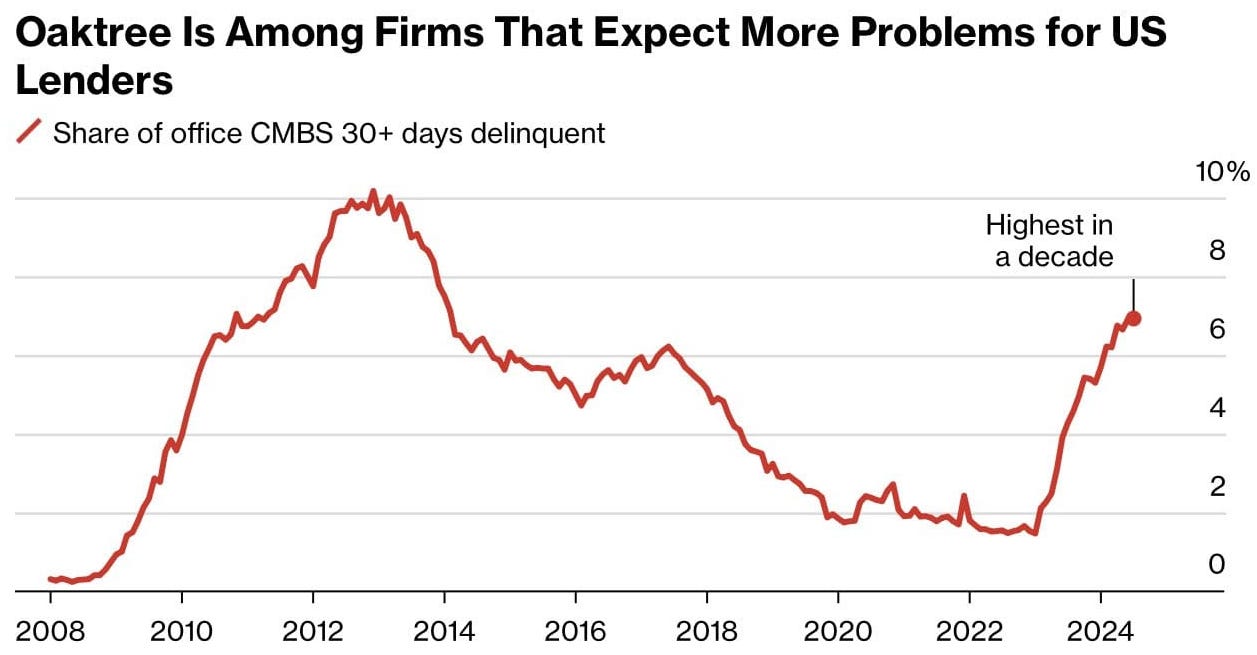

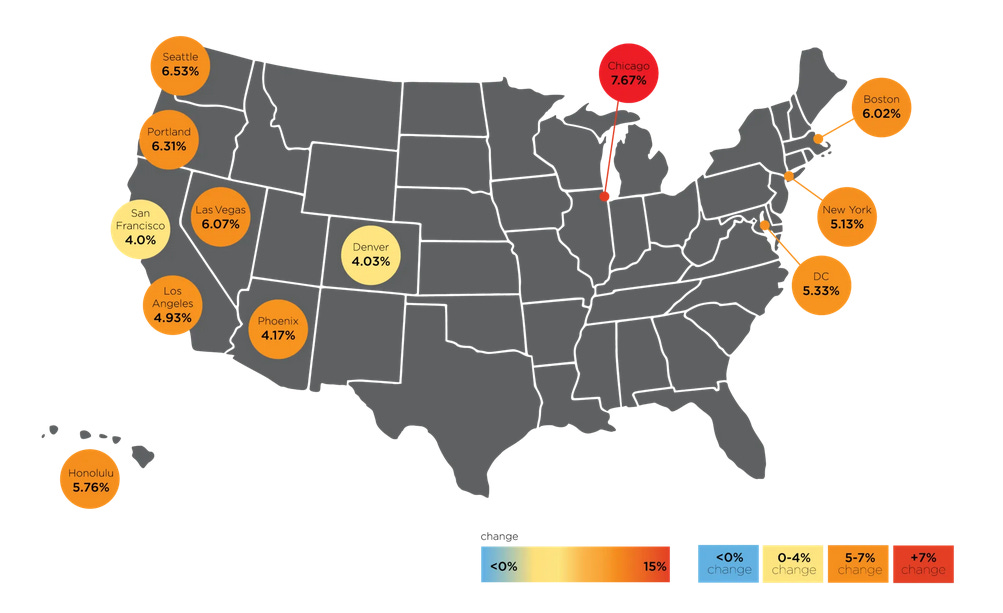

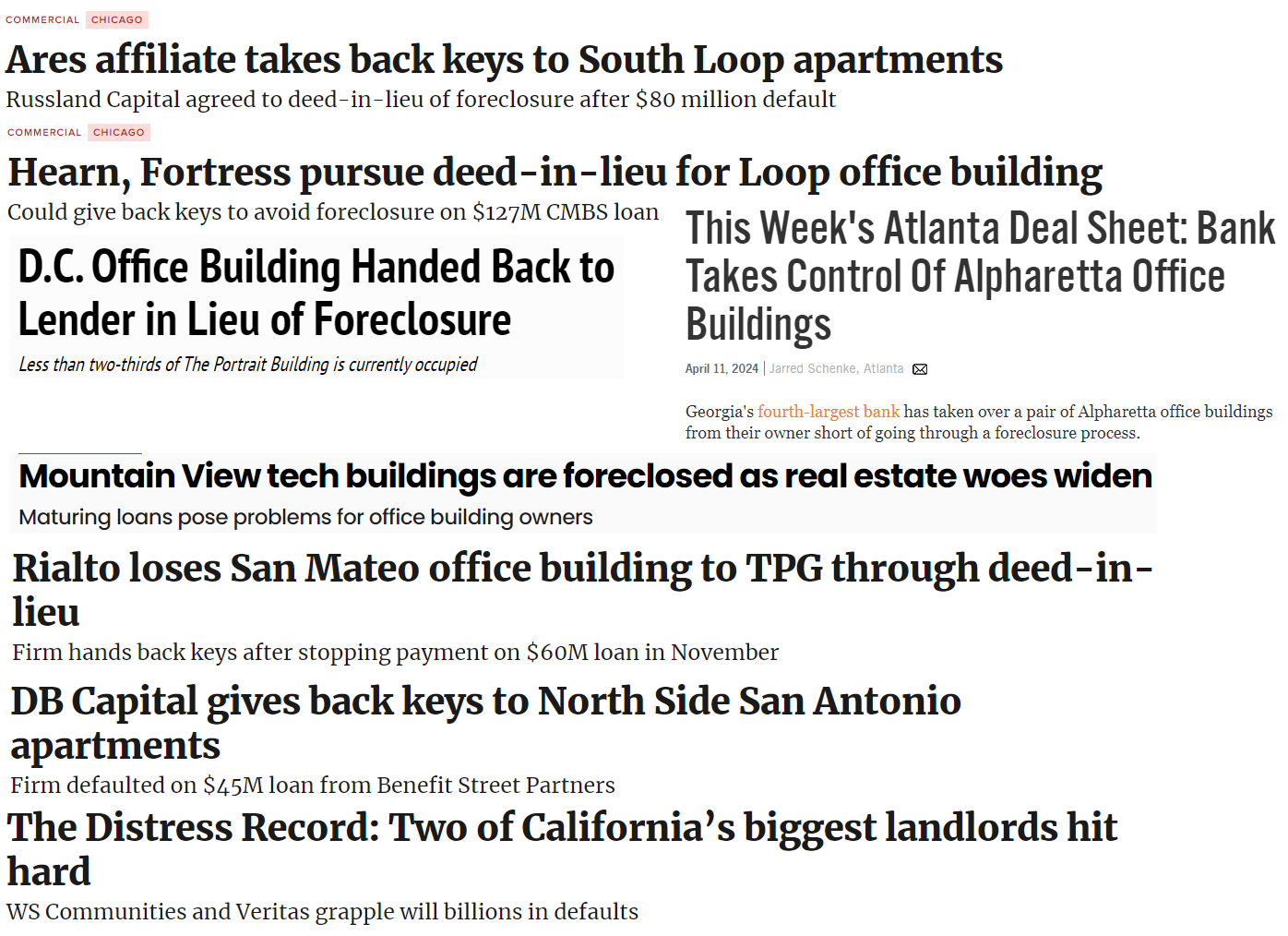

CRE

“Compared with the Savings & Loans crisis and 2008, we’re still in the first or second innings” when it comes to troubled assets

“Distressed investors see one of the best opportunities in a generation to buy troubled US real estate assets as the commercial property crash continues to roil the market. Private equity firms are already positioning to take advantage. About 64% of the $400 billion of dry powder that the industry has set aside for property investment is targeted at North America, the highest share in two decades…”

“Based on Oaktree analysis, the number of US banks at risk would exceed levels seen in the 2008 financial crisis levels if CRE values fell by only 20% from their peak. Office values there fell 23% last year, according to the IMF.”

Construction Costs

“Year-over-year, the U.S. national average increase in construction costs is approximately 5.41 percent.”

The overall vacancy rate in DFW’s industrial market rose to 11.2% in Q2, up 7.6% YoY. This marks the area’s highest industrial vacancy rate since 2011. At the same time, 14 MSF of industrial space hit the market, with an additional 21 MSF currently under construction.

Big Banks Are Taking Hits From Commercial Real Estate “Commercial real estate is often talked about as a problem for smaller banks, but big banks are emerging with the most evident scars so far.”

From the comments: Overheard at a recent structured credits conference, "We are not overbuilt, we are under demolished".

Property Fraud Allegations Snowball as Commercial Real-Estate Values Fall

“Regulators and federal prosecutors say that property loans based on doctored building financials and valuations have been rising. This type of fraud became more widespread between the mid-2010s and 2021, federal investigators and real-estate brokers say, when commercial property prices surged to new highs and landlords had much to gain from such maneuvers. Now, the drop in property values caused by higher interest rates and a rise in defaults is exposing more of these schemes…”

From the WSJ comments:

"Commercial real estate and private equity are magnets for grifters - somewhere Charles Ponzi is green with envy."

As Warren Buffett said in his 1992 shareholder letter, “It's only when the tide goes out that you learn who's been swimming naked.”

"If you're in commercial real estate you certainly do want inflation, thank you very much.”

Barry Sternlicht of Starwood Capital Group predicted a regional bank failure “every day or every week.”

MetLife Investment Management foreclosed on an El Segundo office building owned by Starwood Capital and Artisan Ventures “Starwood and Artisan owed $83.9 million under a roughly $85 million loan from MetLife on the property, provided in 2020, records show.”

“The general public does not have a sense of the severity of the problem.”

Fearing Losses, Banks Are Quietly Dumping Real Estate Loans

Some Wall Street banks, worried that landlords of vacant and struggling office buildings won’t be able to pay off their mortgages, have begun offloading their portfolios of commercial real estate loans hoping to cut their losses…“What you are seeing right now are one-offs,” said Nathan Stovall, director of financial institutions research for S&P Global Market Intelligence…these steps indicate a grudging acceptance by some lenders that the banking industry’s strategy of “extend and pretend” is running out of steam, and that many property owners — especially owners of office buildings — are going to default on mortgages. That means big losses for lenders are inevitable and bank earnings will suffer…

“The banks are going to a select number of brokers, saying, ‘I don’t want this public’”…Jonathan Nachmani, a managing director with Madison Capital, a commercial real estate investment and finance firm, said hundreds of billions in office building loans were coming due in the next two years. He said banks hadn’t been selling loans en masse because they didn’t want to take losses and there wasn’t enough interest from big investors. “It’s because nobody wants to touch office”…“What I have been seeing is the cockroaches are starting to come out,” said Mr. Hamilton3. “The general public does not have a sense of the severity of the problem.”

Office Building Losses Start to Pile Up, and More Pain Is Expected

“There is a lot more trouble coming,” said Mark Silverman, a partner and leader of the CMBS Special Servicer group at the law firm Locke Lord, who represents lenders in disputes with commercial mortgage borrowers. “If we think it’s bad now, it’s going to get a lot worse.”…

“When you see delinquencies rising and foreclosures rising, that means we’re approaching the acceptance stage of the grieving process for office properties — and that’s healthy,” said Rich Hill, head of real estate strategy and research at Cohen & Steers, an investment firm. “But we’re not at the bottom yet.”…”We went so long without any transactions that it created a lull,” said Alex Killick, a managing director at CW Capital Asset Management…That could spell the end of a tactic often referred to as “extend and pretend,” which became popular in recent years…

“There has been a systematic holding of the breath, with everyone hoping that the rapid increase in rates by the Fed would be just as rapidly decreased, allowing people to breathe easier and rates would be restored to lower levels,” said Ethan Penner, the chief executive of Mosaic Real Estate Investors, a firm in Los Angeles. “But that hasn’t happened, and there is only so much time that a lender can provide a borrower in terms of patience and looking the other way, especially once lease income starts to shrink.”

You get the idea…These are from the last six months:

Private Equity

“Everything is not going to be OK,” Scott Kleinman of Apollo Global Management recently said. He compared the private equity investments that won’t pay off to a pig being digested by a python. In other words, investors will face fewer realizations and lower returns.

There are reports of pension funds not getting the big payouts they expected — or not getting anything at all, their money essentially tied up in “zombie funds.” Some pensions are short of money and need to take loans from the funds. Other pensions need to sell their stakes at a discount on the secondary market.

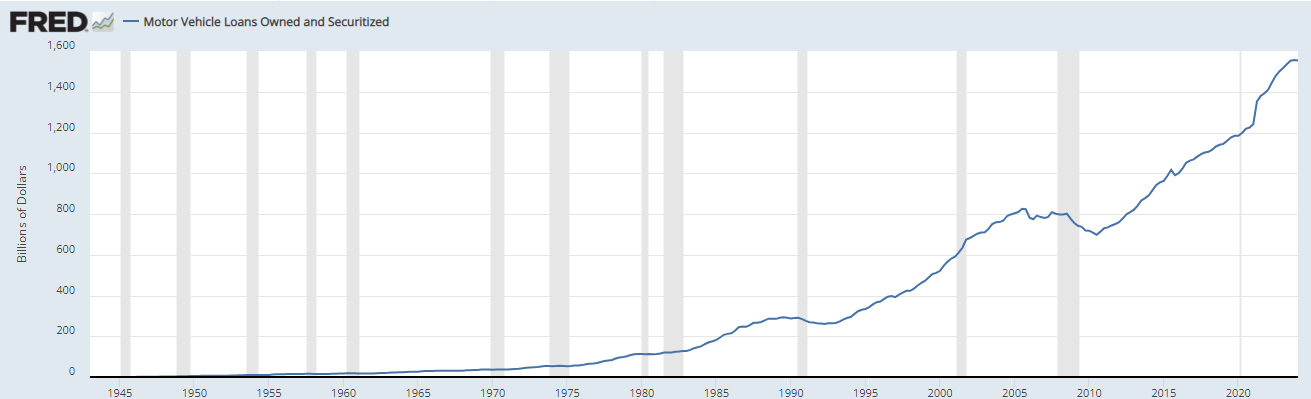

How Auto Loans Were Invented

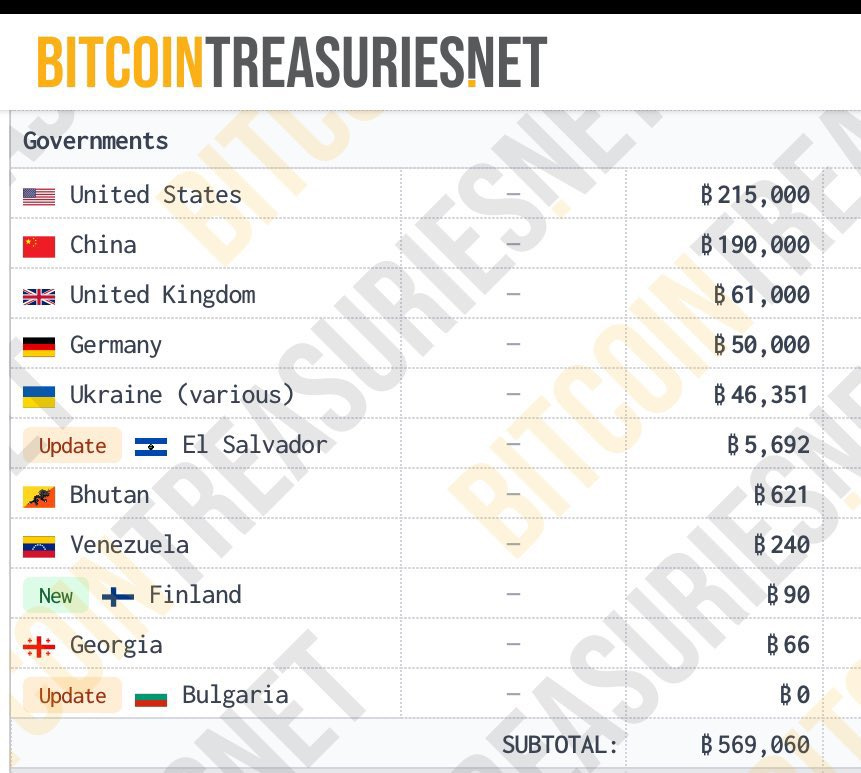

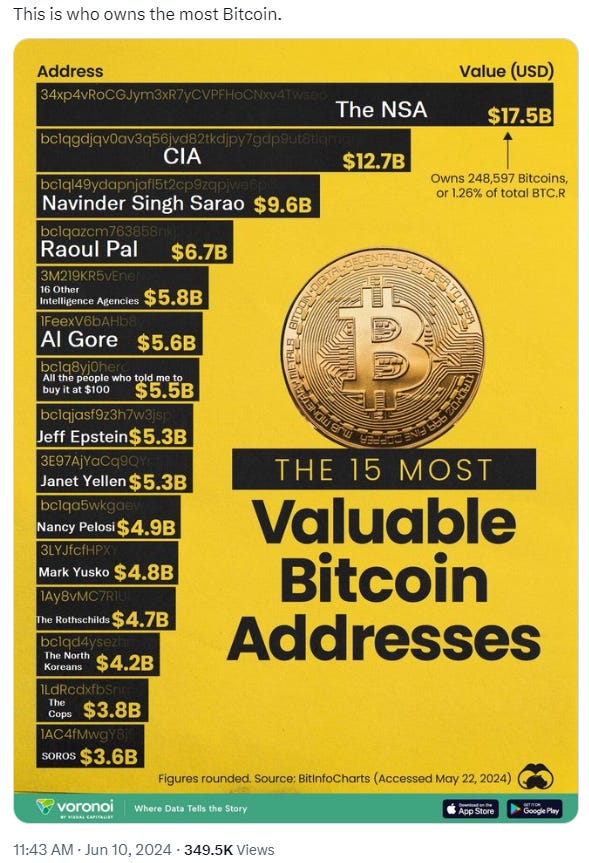

Countries that own Bitcoin (that we know of)

I made this up recently and a number of people thought it was “real”:

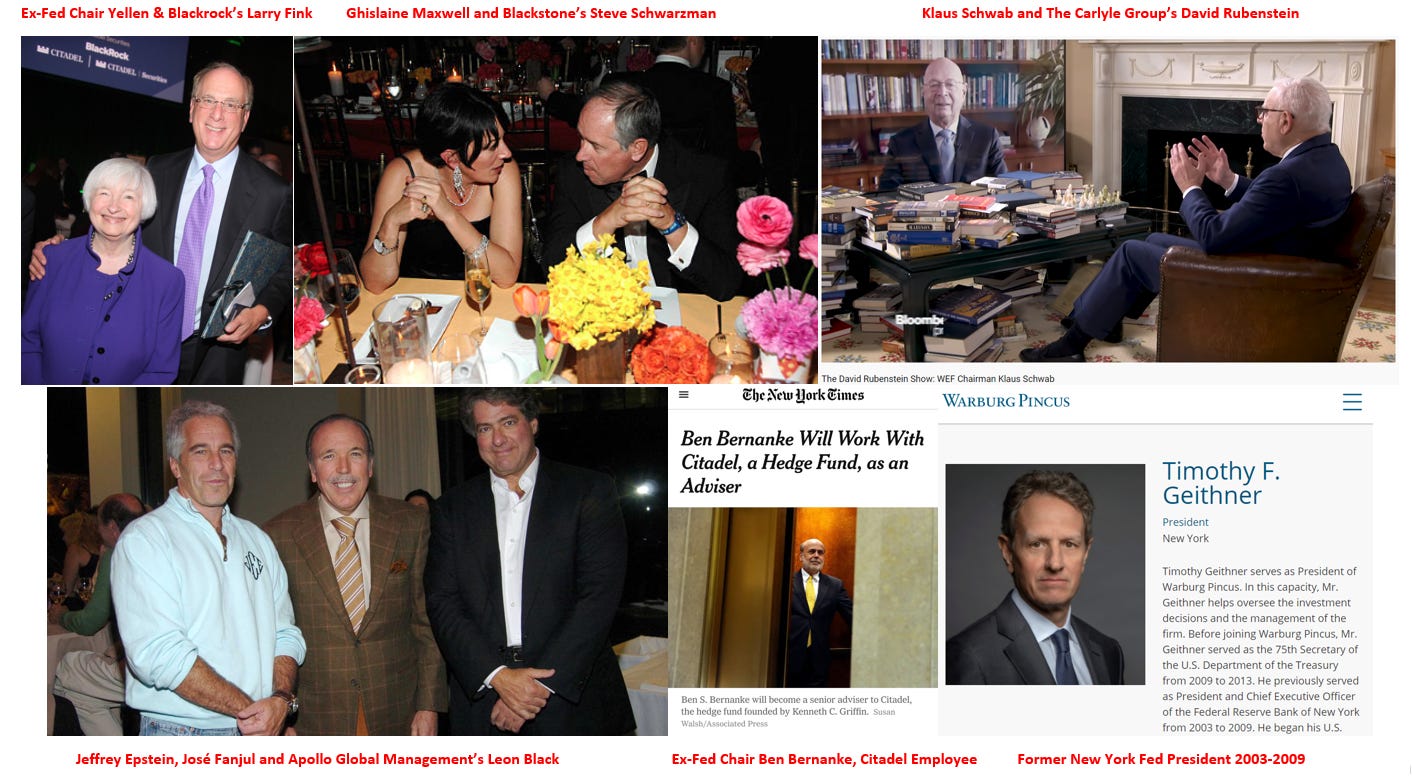

Crime and [No] Punishment

“Park Hotels & Resorts will shutter a 56-year-old Hilton hotel next to Oakland’s airport following closures of numerous local restaurants because of crime…Between 2019 and last year, four local businesses, the Chevron and Shell gas stations, a now-closed Black Bear Diner and a building that houses a Wingstop and a Subway sandwich shop had 2,773 reported crimes. The nearby In-N-Out Burger closed its doors a few months ago because of crime. Denny’s and Black Bear Diner have been boarded up.”

But yeah, sure, crime is down.

”While sitting in his truck, McElroy was shot at several times but hit only twice—once by a centerfire rifle and once by a .22 rimfire rifle. In all, there were 46 potential witnesses to the shooting, including Trena McElroy, who was in the truck with her husband when he was shot. Nobody called for an ambulance. Only Trena claimed to identify a gunman; every other witness was either unable to name an assailant or claimed not to have seen who fired the fatal shots. The DA declined to press charges, and an extensive federal investigation did not lead to any charges either. Missouri-based journalist Steve Booher described the attitude of some townspeople as “He needed killing.”

“Owning some of the finest companies in the world was a lousy deal if you overpaid and a worse deal if you bought the most expensive Nifties.”

https://www.lcp.com/en/insights/blogs/nobody-gets-fired-for-buying-ibm

Michael Hamilton, one of the heads of the real estate practice at O’Melveny & Myers

As always an excellent read enhancing the collective intelligence. Too bad most of our leaders don’t read nor understand such things. Thanks for sharing!

Fully packed with so much great stuff. Thank you. And that car video is hilarious.