We fought Stein's Law...

And so far we're winning!

"I am reminded of the economist Herb Stein, who once said that, if something cannot go on forever, it will stop. To which Rudi Dornbusch quipped: Yes, but it will go on for a lot longer than you anticipate."

“You've had [national debt] compounding at over 8% a year, with a growth in the GDP of about 4% a year, so you've got about a 4% per year gap over the last 50 years almost, so this is not sustainable. This is what you call insanity.”

"The press is saying delinquencies are at all-time lows. I think that's largely because we are missing huge chunks of the picture." - Melody Wright

Melody knows how the mortgage sausage is made. Very informative. (She only says "bloodbath" once by the way.)

"If you were using floating-rate bridge debt to get your deals to pencil in 2022 and 2023 - toast. Gone. Garbage. Complete garbage." - Michael Zuber

Via The Mad King, who I found through Grant Williams. Give his service a look.

“I've concluded that inflation could be a very misleading metric. Simply because we are looking at growth while ignoring levels…If inflation is under control, then why do consumers still feel priced out of everything? Answer: Because economic inflation data is calculated in a way that does not represent reality.” - TMK

“For instance, the US CPI equivalent of rent is up 22% since 2020, but median asking rent is up 41%. The price of a single-family house is up 40%, while financing costs are up 90%...”

“We need to get back to the Fed's actual statutory target which is 0% inflation.”

“…the “magnificent seven” of Apple, Amazon, Tesla, Alphabet, Meta and Microsoft along with Jensen Huang’s outfit [Nvidia] command 31.4% of the S&P 500’s market capitalization. That’s a record share per data from Bank of America, topping the 29% logged in late 2021 and double the group’s representation in the broad index at the end of 2017.”

This was going to be a short post and now it’s a longer post. Today, below the fold, we have Matt Mattison, Jeff Gundlach, Jim Grant, Jason Shapiro, Danny Dayan, The Credit Strategist, H.L. Mencken, Atlanta, Boston, Dallas and Australia, capitalism, Skynet, and private equity, among other things.

Podcasts

Weak Disclaimer: I don’t necessarily agree with all of these opinions, but I don’t necessarily not agree with them either. Often I could argue either way. Other times I’m just confused.

Matt Mattison

If Powell “needs to sacrifice his 2% target, I think he will.”

“Some of these things have happened. If you look at when we went off the gold standard in 1971, what happened to the gold price over the next 10 years is it went up 25 times. It went from $35 an ounce to $875 an ounce, in essentially a 10-year period.”

“Once we went off of the gold, you know, it was all fiat. That was the final straw to basically put this debt spiral into place that people have been talking about since before you were alive, before I was alive, and basically what's happened is it's now I believe reaching a crescendo.”

“I think we could easily see S&P 6000 within the next 12 months, and S&P 7,000 in the next 24 months, and at at a certain point it's going to basically get so blown up that people are going to realize, hey, this can't go on forever. Once people start searching for the exits, it's going to like a game of musical chairs, and it's going to start crashing down, and this in turn is going to lead to people to realize we cannot have the dollar as the world's reserve currency, and we need to come up with something along the lines of what John Maynard Keynes suggested in Breton Woods, which was a basket of currencies, something like a special drawing right, he called it the Bancor, which was a gold-based basket of currencies based on trade.”

Here comes Van Eck:

“The US government can always print its own money, and the demand for dollars is so high. Basically interest expense has gone up because interest rates have gone up, because the Federal Reserve has raised interest rates. The U.S. can afford it, because you can always just issue more bonds - and some people would compare this to a Ponzi scheme - but I think the US government has special privileges that no other private-sector actor has, above all other governments. It has an even higher privilege, because everyone wants dollars, and no one wants the Argentine peso, sorry. Why can't this continue?”

Back to Mattison:

“The propensity for the U.S. to continue to print money is a lot greater than a lot of doomsayers have talked about.”

“The government is like an addict. It has to inject more and more and more spending and liquidity and bonds, and it's going to keep doing that to stall off a recession as long as it can, and the side effect of that is going to be inflation of financial assets, housing, gold, stocks.”

“There's going to be some investors that - you know, it's a tipping point - and they say, you know, I'm taking my money out. Once people start running for the doors, that's how you're going to get the collapse, which is, by the way, the traditional modus operandi of bubbles throughout history. Whether it's tulip,s or anything - people think you can't lose, and then everybody gets in, and then when everybody's in, all of a sudden some people start saying hey, I'm cashing out, and once a certain critical mass of investors start cashing out, then you're going to start seeing the collapse.”

“I believe that the Federal Reserve is going to cut rates this year. I believe they're going to be forced into it regardless of what inflation does, because of the global macro picture…They're going to need to be cutting in Europe, and they need to be cutting in the UK, and if if they don't cut, that the dollar is going to get too strong ,and so this is going to inject the liquidity this is going to fuel the animal spirits, and we're going to continue this melt up into the election, and then whoever wins is going to obviously want to continue this in the beginning period. So they're not going to upset the apple cart, whether it's Trump or Biden, they're not going to say okay, we need austerity, we need to cut spending. They're going to keep that spending going and the markets are going to see all this. They're going to see lower rates, they're going to see continued fiscal deficits at high levels, and they're going to say, this is just great for the market, this is great phenomenal GDP. We could also get a bump from A.I. productivity, so we've got this A.I., fiscal spending, lower rates that that's going to fuel this rally, I believe until about 2026 or 2027, and what I think is going to happen at that point is that people are going to be looking at the Social Security trust fund.” [Like Gundlach below, he pegs 2028 as the social security crisis year]

“Yellen is very political, and doing things blatantly to keep the yield curve in check, but I think that Powell - if the economy needs it, and there's going to be a collapse, or a Treasury auction is going to go bad, he will keep Treasury market stability. He will keep moderate long-term yields, and he'll do what he needs to do, and if he needs to sacrifice his 2% target, I think he will.”

Jeff Gundlach

“I think that rates will rise, in a trend sense, for the rest of my career.”

“So I got into a PhD program at Yale, and I learned very quickly that that was a dead end, because you would be a professor. I thought that a professor would be a very idealistic, a good place to be without a lot of politics and all the stuff that go goes on in business. I was so wrong. It was the most political thing ever, so I left.”

(Janet Yellen got her econ Ph.D. at Yale in 1971)

“I'm going to say that Social Security runs out of money without a restructure by 2028 would be my guess, so we're getting very close to that.”

“The general wisdom was that rates would never go positive again. That was

actually what the narrative was in 2016. I saw an article on the Bloomberg wire that really shocked me, and it made me get a lightning a light bulb above my head, and that was a guy said rates will never rise for my entire career, and

I have an intention of having a very long career, and I was like, uh-oh.”

“I handled the credit crisis [GFC] better than any other fixed income investor in America - by a lot - and this one’s going to be just as hard.”

“They should have done nothing but 100-year bonds in 2021, but they were too short-sighted, which is typical in politics.”

“I think Jay Powell - he's done a couple of things wrong. The first was introducing supercore, which did at Jackson Hole in, I think, 2022, because that was looking favorable at the time. Well, supercore PCE is not so bad, but supercore CPI is at 4.8% year-over-year. 4.8 doesn’t sound like two. The other problem is, if you take those recent inflation prints and annualize them - this is the other mistake Jay made - he justified the November 1st rhetorical pivot by annualizing three months numbers and six-month numbers. That became that became very fashionable in financial media at that time. Well, the reason to do that was that as of November 1st, annualizing those numbers it was 2%, you had 2% inflation three-months annualized, but that's not working anymore.”

“Jay Powell - I think he tries to be honest, but he does do a little prevarication, and he said inflation was at 2.7% - of all the numbers you could pick, that's the lowest one. That's the PCE, the lowest number, 2.7. Supercore CPI is at 4.8. There's plenty of threes and fours out there depending on what series you want to look at, how you want to slice and dice them. I have much less confidence than Jay Powell seems to exude that we're going to see that 2% inflation number during J.P.'s term. In fact, we might not even see a single year-over-year with the two handle on this CPI…”

“I think Jay wants to continue to represent his approach, his ideas, not

change them at the bottom of the ninth inning, because he's going to be gone. I don't think he wants to come back.”

“I think that rates will rise, in a trend sense, for the rest of my career.”

Jim Grant

“Let us not forget the Fed is explicitly is wanting inflation. It defines price stability as a 2% rate of inflation, which I think is, first of all, it's Orwellian, and is unhealthy. It's a matter of language. It's kind of a a sneaky and unworthy deceit on the part of the Feds, but we as a people seem to want - we vote for inflation. What was the last time you cast a ballot for the balanced budget and gold standard restoration party? It's hard to find in the ballot. So I think the electorate has voted for it. It might not admit it in just those words, but we elect the people who give us inflation…whoever is gonna win is all for inflation.”

“Commercial real estate - which by the way was an asset that was forbidden on the balance sheets of a nationally chartered bank until with some exceptions about 1935…so the national banking system was founded on the old-time bankers prejudice against real estate as being inherently illiquid, and therefore inherently unsuited to an institution that was susceptible to to runs.”

“Remember in 2020 at Jackson Hole the chairman of the Federal Reserve board said we are now going to resolve to get our 2%, and to ensure that is going to happen, we are going to compensate for any shortfalls from 2% by allowing it to rise above 2% just to compensate. So, you know, at the time I thought, do they really want to do that? They are summoning the gods of irony. Do they want this? They did make it so. H.L. Mencken once said that the American electorate gets what it wants, good and hard. Well, we're definitely getting that on inflation right now.”

"Democracy is the theory that the common people know what they want,

and deserve to get it good and hard."

Danny Dayan

“The 10-year yield started the year at 3.70, made a move to 4.70, now is about 4.40, so rates have moved substantially higher and yet we have not tightened financial conditions. There was a two-week period where the S&P had a mini-correction, which is something you would see every year. We really have not been able to tighten financial conditions, no matter what the Fed says or does, and so I think they've lost control of financial conditions…the ten-year is artificially too low, and, in my opinion, is not doing enough to restrain the housing market or other interest rate sensitive parts of the economy”

The Fed screws up again and again, and is never accountable (my quote)

“They were buying $120 billion of bonds a month. They had another 80 to 100 billion of reinvestments from their portfolio, and then they changed the regulations, which encouraged the banks, who were being flooded with reserves from all this QE, to buy bonds, and obviously that was a major mistake for the banking sector, and so you what we had was approximately $300 billion of systematic buying [a month] that was not price-sensitive. It was completely price-insensitive. It was just buying every day consistently, and you had 10 year yields go from 1.75% in the end of March to 1.1% at a time when the economy was was roaring ahead.”

“The fact is if they're artificially compressing the ten-year because the deficit is too large. There's no fiscal consolidation happening. So what does buying time do? It just makes the problem worse down the line.”

“The ten-year is what matters. They never talk about it. They never talk about the ten-year yield, they always talk about the Fed funds rate, and they never considered asset sales, despite many people saying they needed to [me!], so my base case is they haven't figured it out yet, and hopefully they will soon, but there is a plausible alternative explanation, which is that they're worried about the banks, and that they're buying time for the banks.”

“I think we start to worry about the deficit in a bigger way when the bond market is selling off, even when the data doesn't tell it to sell off.”

“I think we start to worry about the deficit in a bigger way when the bond market is selling off even when the data doesn't tell it to sell off. So if we're getting weaker data, and the bond market is just selling off, this is the flip side of what happened in 2021, where we had extremely hot data and the bond market rallied every day. If we have the flip side of this, where the bond market is just a no confidence vote by investors at the time when the dollar is getting sold, then you know that this is just a pure no confidence vote, and they probably need to get the fiscal side in order. I don't think we're there yet, but we'll see in the next couple years.”

“They [China] own a ton of us treasuries, right, and these bonds have taken a nasty hit in the last few years. They're not traders. They're buy and hold investors. They're parking their reserves, about a trillion in in treasuries, and their reserves are about three, three and a half trillion I believe. You know a lot of it is in treasuries, and seeing how badly bonds can get hurt - which is a new thing for them - is maybe a sign that they need to diversify their reserves away from bonds, and frankly, they could be looking at the inflation and debt trajectory of the United States and saying, you know, we need to diversify our reserves. So they're buying things like gold, obviously. They're buying industrial metals like copper, and they'll need these metals anyway, copper in particular, aluminum, palladium, iron ore. They will need these for industrial purposes anyway, so from their perspective, maybe they're just saying let's diversify our reserves into physical assets away from these bond markets, and have things that we'll need in stockpile for the eventuality when we need to use. We won't need to go out and chase them in the markets.”

“I viewed that [Fed] move in December as irresponsibly dovish, and that's, in a nutshell, the environment you want to own precious metals in.”

Jason Shapiro

Key Shapiro takeaway: “Personally, I love building macro narratives. I think it's fun. I think it's interesting. I think it's great to talk about. I also think it's probably the biggest money loser that there is.”

Yep, same here. As I joke, I am bearish in theory but not in practice. I haven’t shorted since 2009. When I want to hedge against capital gains I might on rare occasions buy puts. Hard to fight an entity that can and will create unlimited currency, plus my long-term macro view - while terrible for society as a whole - probably means stocks do well, nominally at least. I don’t do bonds - I can’t imagine doing bonds except as a trade, but I’m a caveman.

Jason’s a straight-shooter who has some views very similar (or exactly similar) to me, but he clearly says he doesn’t know if the endgame is next year, or 40 years from now. Either do I, but I do believe it will end, someday. Hank Paulson, Neel Kashkari, Bob Rubin, Larry Summers, Ben Bernanke, Janet Yellen and Jay Powell and hopefully you readers will be fine no matter what, but I do worry about a couple hundred million Americans who may not do so well. This is bizarre thinking for Wall Street folk, I understand. - RH

“They will just print money”

“We have got to a point it seems in economic history where you can't have a recession, right? The consequences are just too dire at this point. There's too much debt out there, and you just can't have a recession. So what do you do? Anytime there's weakness, they just print money. Lower rates, print money, whatever you want to call it. They try to create more liquidity. This all started after the 2008 thing, where capitalism essentially failed and so governments took over, so they are in charge now. This whole MMT idea, you can print as much money as you want, it's not inflationary - well, we found out that that's not true. Inflation got up to whatever it was - 9% at one point - after all that money printing post-Covid, so that's what they do now. That's the new thing now, they they will just print money.”

“It's a Ponzi scheme, and while Ponzi schemes run by individuals are pretty short-lived, a Ponzi scheme run by a government that owns a printing press can clearly last a lot longer. We don't know how and when that will end, but it will end, and when it ends it's going to end badly.”

This was a funny exchange:

Jason: Everyone talks about how you can't have a 2008 again because the bank balance sheets are so much stronger now. Yeah, because all the debt that the banks were guilty of taking on back then that blew them up has now been transferred to government balance sheets, right?

Jack: Right.

Jason: So that's a much bigger problem. I understand the government bails out the banks - who bails out the government? There is no one, right?

Jack: The Central Bank

Jason: Who bails them out? I mean how does the central…

Jack: They print money.

Jason: OK, it’s great. I get it, print money, print money, print money. Eventually that doesn't work, and that's why I'm saying we don't know the timing, but eventually that doesn't work. Go ask Zimbabwe if that works. I know the U.S. is not Zimbabwe. I get it, okay, but it doesn't matter. There are certain natural laws to the world that come through anything: physics, economics, supply and demand. If you print, eventually too many dollars - eventually, people are going to reject them. There's a limit to everything, including how much money the US government can print. Are we there now? I don't know the markets will tell us, and they'll tell us when this happens: if we should go into recession, and they print money to get us out of it, and that doesn't work, and the dollar starts going down. So it's a huge risk out there, and and I never say something's definitely going to happen, but it just seems inevitable to me.”

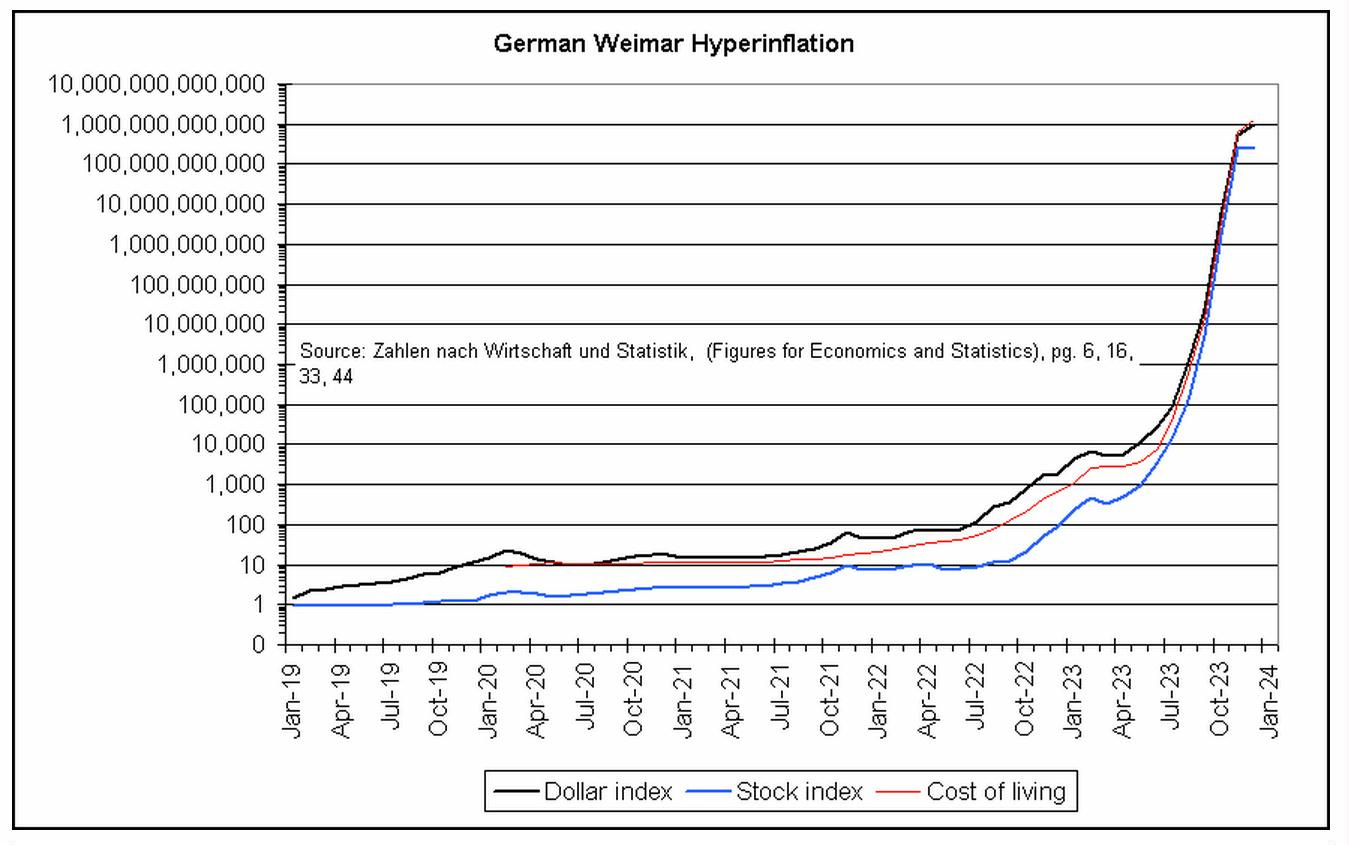

The above exchange reminded me of this passage from Dying of Money:

“The most extraordinary feature of the Reichsmark’s joyride was not any attack against it but quite the opposite, an incredible ("pathological,” it was later called) willingness on the part of investors at home and abroad to take and hold the torrents of marks and give real value for them.

Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. The storage factor caused by the investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check.

The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds. The German government strove mightily to outflood the sea.”

The real endgame risk is not “high inflation” - although that will further destroy most Americans - it is a currency collapse, a panic out of a currency.

More Shapiro:

“Central banks have really painted themselves into a major corner, and there's just no way out. You can delay it, because you're a central bank, but I really think that it's bad… I called it the biggest shitshow in Central Banking history, and I truly believe that. That says nothing about timing, but there is, to me, an inevitability about the end-game”

“I'm not saying there's going to be an economic slowdown, therefore metals are going down, right? I'm saying there's a high probability from what I look at that the metals are going down, therefore the narrative, once they do, is probably going to be that there's an economic slowdown coming. I do it backwards.”

“Go look at the NASDAQ over TLT chart. It's one of the greatest charts in history. All it does is make new all-time highs.”

Oh Canada

“Canadian investment manager Ninepoint Partners LP is temporarily suspending cash distributions in three of its private credit funds. Unitholders of funds with about C$2 billion ($1.5 billion) of assets won’t be able to receive cash payouts, in order to preserve the funds’ liquidity…The Toronto-based firm, which oversees about C$7 billion of assets, is not winding down these funds (or presumably their fees - rh), according to the statement. “Investors will continue to have access to the ongoing benefits of being invested in private credit as we remain focused on ensuring the sustained performance and stability of our current portfolio.””

Counterpoint:

“Private capital firms have taken more money from investors than they’ve distributed back to them in gains for six straight years, for a total gap of $1.56tn over that period…You might think that in a ruthless, meritocratic industry like private capital, this might have had an impact on compensation? Ahahaha no, of course not you sweet child.”

“There just seems to be too big a mismatch between what private equity and venture capital have paid for a lot of assets, the returns their investors expect, and what public markets or other potential buyers are willing to pay.”

From The Credit Strategist:

Steward’s bankruptcy, the largest hospital company bankruptcy in years, is bringing more attention to the damage wrought by some private equity transactions to the healthcare industry. In a recent “Heard on the Street” column, The Wall Street Journal argued that the consolidation resulting from private equity deals is also raising healthcare costs: “Years of deal making have led to sprawling hospital systems, vertically integrated health insurance companies, and highly concentrated private equity-owned practices resulting in diminished competition and even the closure of vital health facilities.” “High Health Bills? Thank Private Equity,” May 31, 2024) The Journal described the problems that resulted from Welsh, Carson, Anderson & Stowe’s roll up of anesthesia practices into U.S. Anesthesia Partners, a company that was sued by the Federal Trade Commission last year for anti-competitive behavior (the case is still pending and like many government suits may prove to be unfounded). Regardless of the merits of that case, there is no doubt that the “private equity playbook” applied to healthcare involves adding more debt and cutting expenses in these businesses, often at the expense of patients.

As the Journal writes: “During the past decade, private equity has spent hundreds of billions of dollars acquiring healthcare businesses from emergency care to anesthesiology to nursing homes. Where private equity has gone, studies show, prices have tended to increase.” Private equity is attracted to healthcare because the government throws nearly one trillion dollars at the sector every year (much of it wasted or stolen). And one of the reasons America’s healthcare system spends more than other developed countries’ with no better (or worse) patient outcomes is that it is based on profit-seeking behavior that may not necessarily be the best model for this particular industry. Blind faith in markets is still blind faith with an emphasis on the word “blind.” It’s time we ask whether it is optimal public policy to allow private equity firms to leverage up businesses whose priority is saving lives. The experience so far has been decidedly mixed.”

Hotel, Motel

Atlanta

“In the first three months of 2024, the total value of Atlanta-area residential property purchased by real estate investors surpassed $1 billion, according to a recent report from national real estate company Redfin Corp. The Atlanta Business Chronicle reports that the metro area joins Miami, Phoenix and several California markets in seeing more than $1 billion worth of homes purchased by investors from January to March. Investors bought more than 20% of all homes purchased across metro Atlanta during the quarter, per the report.”

Boston

“Boston could enter an “urban doom loop” as a result of reaping more than 30 percent of its tax revenue from commercial property, which stands well above other major cities across the country…The bottom appears to be falling out of Boston’s office market. Property sale prices in Boston’s central business district fell by more than 30 percent year-over-year in the fourth quarter, according to MSCI, the steepest drop among the major cities the investment data provider tracked…The vacancy rate of Boston’s offices is hovering around 20 percent and last year, the city set a record for the largest one-year increase in new office space availability…Mayor Michelle Wu’s proposal isn’t helping either. She’s proposed a tax hike on commercial holdings, which would likely get passed on to the tenants trying to stick it out in Boston.”

“After eclipsing office during the pandemic, the once-booming lab real estate market is falling back to Earth. As recent reports and data show, life sciences space is now showing many similarities to other struggling real estate sectors…

“I think this could be the most challenging Boston life sciences market in quite some time,” said JLL Executive Managing Director Chad Urie, who focuses on lab real estate. “It’s just a completely overbuilt situation.”…“It’s the tertiary submarkets in Boston that have a lot of people scratching their heads,” Urie said. “I mean, people are thinking, ‘Should we actually even go ahead and complete some of the construction taking place?’””

Dallas

“Dallas and all its concrete, to me, exemplifies hyper-financialization. Home to one of the very first skyscrapers, it is likely to be the home of many bulldozed ones soon.”

“Current multifamily vacancy is so bad in Dallas, RealPage won’t even give you the %’s on its main summary page. They show the actual numbers and percentages on the summary pages for most of my 82 cities, but not for key cities like Dallas, Austin, etc. Instead they blow a lot of sunshine.”

Phoenix

Australia

“Figures from CoreLogic show a record 16 per cent of sales early this year were properties that had last changed hands less than three years prior.”

“Typically, this can be a sign of a hot property market, where investors are flipping houses and apartments to make a quick (and tax-effective) buck. There's probably a bit of this going on, with property prices back at record highs across much of Australia. But the proportion of quick resales is notably higher than in previous boom markets, so it looks like there's another factor at play.”

“What went wrong with capitalism?”

“Most Americans don’t expect to be “better off in five years” — a record low since the Edelman Trust Barometer first asked this question more than two decades ago. Four in five doubt that life will be better for their children’s generation than it has been for theirs, also a new low. According to the latest Pew polls, support for capitalism has fallen among all Americans, particularly Democrats and the young. In fact, among Democrats under 30, 58 per cent now have a “positive impression” of socialism; only 29 per cent say the same thing of capitalism.”

“The era of small government never happened. Government has been expanding for nearly a century in virtually all measurable respects, as a spender, borrower and regulator; the one brief retreat, under Bill Clinton, proves the trend. In the US, government spending has risen eight-fold since 1930 from under 4 per cent to 24 per cent of GDP — and 36 per cent including state and local spending. What changed under Reagan was that as spending rose, tax collections remained steady, so government started paying for its own expansion by borrowing. Deficits went from rare to routine and as a result public debt has quadrupled in the US to more than 120 per cent of GDP today.

…America is displacing Europe as the society least tolerant of financial distress for anyone, up to and including the super-rich…Today’s policymakers are status quoists, indulging the same old impulse to rescue, regulate and spend, and hoping for better results. Instead, they are likely to get the same results: gravy days for markets and billionaires, not society as a whole. Capitalism’s premise, that limited government is a necessary condition for individual liberty and opportunity, has not been put into practice for decades.”

“Google Cloud error erases $135B pension fund”

It’s ok, they found some backups they’d missed.

“Google Cloud says it’s fixed the issue that led to one of its servers wiping out a multi-billion-dollar pension fund in Australia — all because someone forgot to fill in one box on one form.”

Private Equity Locusts Have Come For Baseball

“Diamond Baseball Holding’s business model is clear once you get past the puffery and the popcorn: Consolidate the minor league market and foist costs onto taxpayers, with the ever-present threat of moving teams out of communities that don’t comply. It’s a tale of consolidation and extraction running right underneath America’s pastime.”

Owned by Silver Lake.

Discussions about inflation and interest rates ignore the reality of inflation, using BLS rates which have been beaten into submission. As in hedonic adjustments which credit nifty improvements while ignoring the far greater reductions in quality in the life of assets. Appliances are a joke, cars have been an exception but many can no longer be fixed—EVs a travesty. Your old GE stove or refrigerator lasted 50+ years. Try to get 7 out of one today. Further hidden inflation

Unfortunately for capitalism, today the definition seems to be, “Suck out every piece of marrow that you can.” You need look no further than rental real estate and the use of Real Page’s Yield Star software to “optimize” rents… https://www.propublica.org/article/yieldstar-rent-increase-realpage-rent.

It’s no wonder that socialism is gaining popularity amongst the up and coming generation. It certainly is not the solution but, who’s setting an example on the virtues of capitalism?