A little perspective...

"Mass delusions are not rare."

Oh, no rate change today.

“Mass delusions are not rare. They salt the human story. The hallucinatory types are well known; so also is the sudden variation called mania, generally localized, like the tulip mania in Holland many years ago or the common-stock mania of a recent time in Wall Street. But a delusion affecting the mentality of the entire world at one time was hitherto unknown. All our experience with it is original.

This is a delusion about credit. And whereas from the nature of credit it is to be expected that a certain line will divide the view between creditor and debtor, the irrational fact in this case is that for more than ten years debtors and creditors together have pursued the same deceptions. In many ways, as will appear, the folly of the lender has exceeded the extravagance of the borrower.”

Garet Garrett

The Bubble That Broke The World (1931)

"For the past five years, valuations haven’t mattered a bit. Over the last five years in technology, deciding something is overvalued has been a terrible reason not to buy. Look at Microsoft, or Cisco, or Yahoo.”

- Henry Blodget, January 4, 2000

Henry’s timing was interesting:

"Valuation, I find, is a useless tool. If you base your investment decisions on valuation, you are never going to make money."

- Mark Schmehl, portfolio manager at Fidelity Investments, in an interview with the Globe and Mail (2020)

Recent history has prove Mark Schmehl correct.

“Don’t short price, short participation.”

I like the Shapiro quote. Now, how to determine participation… (he uses Commitment of Traders reports.)

So the other day AMD was in the news, and since I hadn’t looked at that one in a while (but remembering it from previous bubbles), I figured I’d look at a long-term chart (In both linear and semi-log form, so as not to upset anyone.) No position in any of these fyi.

Advanced Micro Devices

Also, by request, Nvidia…

And the S&P 500 since 3/9/09, when history began…

(Re: The cat photo. I’m still confused.)

The reason I think Tesla is important - forgetting its market cap and the fact it's down 50% - is that to me, it is like Cisco was in 1999-2000. It's the hopes and dreams large-cap tech stock where people can put any business model they want to on the back end of it, and say I can overpay for this company because they're going to implant chips in my brain, they're going to have a robot serve me breakfast every morning, they're gonna get me to Mars, and God knows what else. I keep saying he's gonna announce asteroid mining soon. If you look at if you look at options trading Tesla's number one almost every day, ahead of the S&P, ahead of Apple, and so this is the speculative vehicle of choice.

Tesla

"One of my jobs during the Covid housing boom was...I would get called in to look at personal finances, and the amount of Tesla-only portfolios I saw was just - it was staggering."

Real Disposable Income Per Capita Flat in December

“Disposable income is the amount of personal income that remains after income taxes have been deducted. Real disposable income is the post tax and benefit income after an adjustment has been made for price changes.”

Note that this is per capita. Stephen Schwarzman’s real disposable income may be skewing the results.

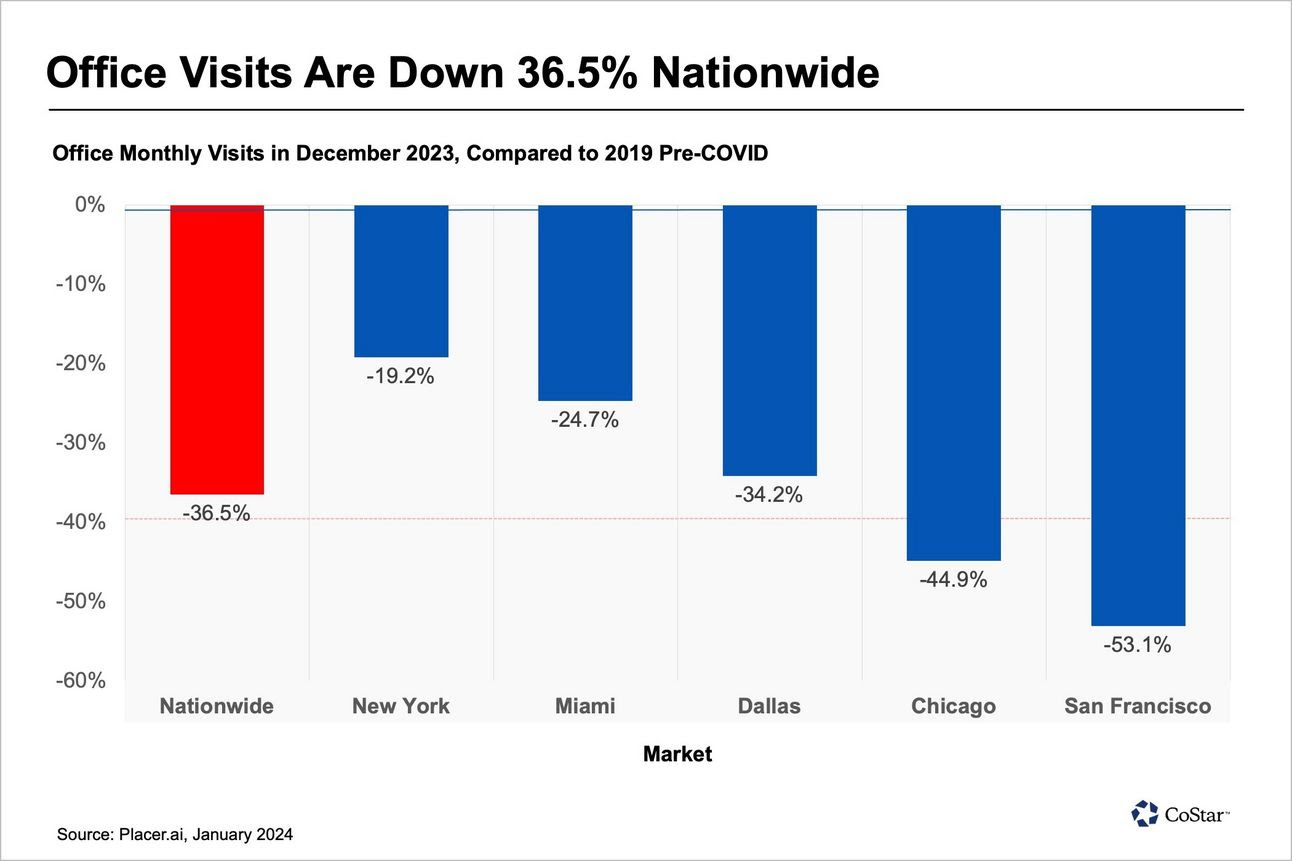

In a July 2023 office valuations report, Trepp showed that, in the first half of 2023, the oldest-aged buildings, or buildings that were built before 1950, had experienced an average total value loss of 60%, with the newest-aged buildings, or building built in 2000 or after, exhibiting a 52% average value reduction.

Ouch.

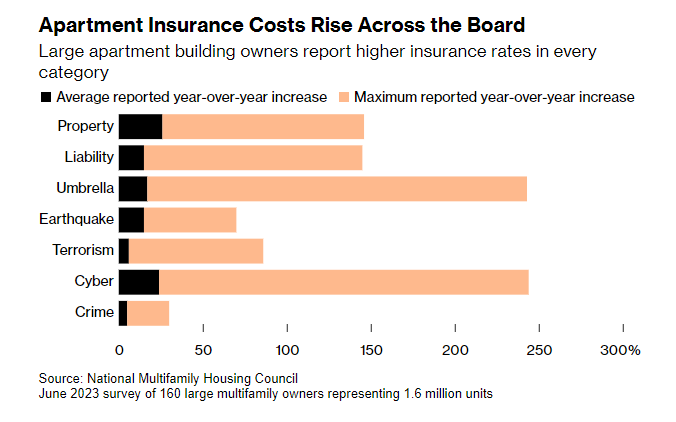

“According to a research report by NMHC, which surveyed 160 apartment investment firms representing 1.6M apartment units, owners have seen their property insurance rates go up by 26% on average since last year.”

Chris Whalen: “A slow-motion train wreck”

Whalen is very tied to what’s best for bankers, but is also very knowledgeable and has some great quips.

“I can tick off a number of situations like this where we know the bank is going to take a loss, but they haven't reported it yet. Again, this is the auditor partly, the regulators partly, but it's also they say, well, I may get a recovery, even if they know they won't. A situation we've written about with Texas Capital Bank - they're in the midst of litigation with Ginnie Mae. Are they going to win the litigation with Ginnie Mae? I don't think so, so eventually they're going to tell us about the failure of this reverse mortgage lender that occurred two years ago, so that's an example.”

“Cincinnati is fine, except downtown is empty, but downtown Dallas is empty too, so the use case for all of these assets has changed.”

“Low-income households are right now taking a shellacking in the credit markets, in terms of default rates. If you look at the bottom 20% of FHA loans, they're up in the mid-teens. If you look at the big servicers that handle a lot of delinquency, their delinquency rates are well above the average, so what we're worried about is will that become a more generalized recession? Are we're going to see consumer defaults go up generally for all banks? I haven't seen it yet, but I'm a little worried about volatility here, Jack, You know we could get a surprise and see defaults go up 40% in a single quarter…”

“It's pretty obvious that we're heading to a fiscal crisis, and yet nobody in Washington wants to talk about this at all. In fact, you know, Donald Trump wants to spend more money, I'm sure, when he beats Joe Biden. This air of unreality in American politics today that we can somehow pretend to ignore the Treasury situation, and just say, well, it's fine - I think some members of Congress are getting a little nervous about that.”

“Well, you're not going to do a ‘profiles in courage’ on this group, because none of the members of the Fed board have the political sand, and the the character really, to push back on the bull market chorus and the equity markets particularly. I think, to me, Powell is going to move very slowly…”

“They should should say less, Jack. I'm appalled by the Fed and the degree to which they overcommunicate. They should express the committee’s consensus and that’s it…It’s a media circus every month.”

Q: “If liquidity is good, what would the incentive be for the Federal Reserve to stop quantitative tightening?” A: “I think they're going to do they're they're going to do that in a couple of months.”

“When Treasury's operations are so large that the Fed has to include

them as part of monetary policy, that tells you what you need to know.”

"A good friend of mine at one of the reserve banks that has objected to the [Fed] board's focus on discount window lending said to me, 'When we see a bank at the discount window, we call the FDIC, you know? Case closed.'"

“The front [of the yield curve] will be low because Treasury is going to continue to fund there, even though they should be funding more on a long-term basis, but they can't because of the pricing. So yes ,I think you'll see short-term rates fall, and I think you'll see the yield curve normalized, so that everything from sevens on out it's going to be higher, imagine that. We won't have much help for the mortgage market here, because we, you know, sell mortgages today against kind of the 10 to 12 year portion of the curve, and it could be that it's not going to come in. Imagine a scenario like that, and that's a normal yield curve, Jack, you can see Fed funds down at four, and 10’s out at five and a half to six. Mention that - I don't think anybody on Wall Street would be very happy about that.”

“The short-term rates are a big pain point for the non-banks, because that's how they fund their production. They fund off 30-day money.”

“I spend a lot of time talking about commercial - what a big change this is, when now the conversation isn't, well, I'm going to roll the asset for you, you can

take some cash out, and I'll give you better rate. Today they want me to put cash in when I roll the mortgage, because the value of the property is falling. That's a huge change in dynamics and people are struggling with this.”

“I think Citigroup's either got to merge with another institution, or they should look at just selling the assets and liquidating the bank. They cannot answer the basic question - why is this bank here? Who does this bank serve? Why are we going to be able to deliver value to shareholders, because remember - shareholders since 2008 have lost 95% of the value of Citi. Why shouldn't we just end the misery now, and sell the assets. I think you’d do better. The bank’s trading at half a book. I think you can get well above book value if you liquidated the pieces. We've been watching the restructuring of Citi for 50 years, my entire professional career…I used to work with these people when I was at the Fed…they ended up losing a lot of money, they ended up failing, and going into a government conservatorship, so to me I think the story is over. I really think it's time to just sell the assets to stronger hands, and if it wasn't for the bank holding company act, and Fed regulation, Citi would have already been taken over years ago.”

Via Almost Daily Grant’s:

“Euphoria reigns supreme only 13 months after global bonds wrapped up 2022 with a 31% loss per data from Credit Suisse, the worst single-year performance on record going back to the start of the 20th century.”

Jim Grant

“I am going to tell you something surprising: between Treasury supply and corporate supply, there is simply not enough. I have not had a single conversation over the last couple of quarters with a client who said ‘oh, get me out of bonds.’ Every single one is saying, ‘how do I get in, when do I get in, where do I get in.’ And you see it everywhere.”

- Bob Michele, chief investment officer at JPMorgan Asset Management

"So we have the lowest interest rates in four-thousand and twenty years, and the ONLY observation of substantial volumes of negative nominal yields in 4,020 years, and we are maximum bullish on bonds, collectively. Now that, gentlemen, is a paradox."

Jim Grant on the Sherman Show podcast, November 2020

“Widespread FOMO aside, high-grade supply remains bountiful, reaching $188 billion today to top the prior January record of $175 billion from 2017 with two sessions remaining in the month. Meanwhile, price concessions for new issues have reached their lowest since 2021 while demand for lower-rated credits has been particularly strong, Dan Krieter, BMO director of U.S. investment grade strategy, observed last week, further demonstrating the market’s “insatiable appetite for risk”…

Speculative-grade corporate borrowers likewise enjoy the mild financial weather, as junk bond supply stands at $22.2 billion for January per Bloomberg, the strongest output in 26 months. Spreads on the ICE BofA US High Yield Index settled Friday at 339 basis points over Treasurys, equivalent to the seventh percentile of relative valuations going back to the financial crisis according to strategists at Bank of America.”

The 24/7 News Cycle

To the extent that propaganda is based on current news, it cannot permit time for thought or reflection. A man caught up in the news must remain on the surface of the event; he is carried along in the current, and can at no time take a respite to judge and appreciate; he can never stop to reflect. There is never any awareness—of himself, of his condition, of his society—for the man who lives by current events. Such a man never stops to investigate any one point, any more than he will tie together a series of news events.

We already have mentioned man’s inability to consider several facts or events simultaneously and to make a synthesis of them in order to face or to oppose them. One thought drives away another; old facts are chased by new ones. Under these conditions there can be no thought. And, in fact, modern man does not think about current problems; he feels them. He reacts, but he does not understand them any more than he takes responsibility for them. He is even less capable of spotting any inconsistency between successive facts; man’s capacity to forget is unlimited. This is one of the most important and useful points for the propagandist, who can always be sure that a particular propaganda theme, statement, or event will be forgotten within a few weeks...

This situation makes the “current-events man” a ready target for propaganda. Indeed, such a man is highly sensitive to the influence of present-day currents; lacking landmarks, he follows all currents. He is unstable because he runs after what happened today; he relates to the event, and therefore cannot resist any impulse coming from that event. Because he is immersed in current affairs, this man has a psychological weakness that puts him at the mercy of the propagandist.

Jacques Ellul, Propaganda (1973)

Mike Taylor’s Theory on the Illegal-Immigration Tsunami

(Talking with Grant Williams, Mike Green and Bill Fleckenstein)

“I have been in contact with some fellows who used to run some of the cameras on the border of Mexico, and their contract was pulled by the White House two years ago, and their cameras were shut off. In a surprise move, we’ve had five million illegals cross the border over the past two years. All of them looking for work, obviously, because that’s what they’re there for. And I am seeing it now on the ground floor. I think we’re going to see on the lower end, jobless claims lift materially because the illegals are competing for those jobs now. And I see it in my real estate businesses across the country where, for instance - I’ll give you a great example. Our prices on framing has dropped substantially, and that’s building house frames. And that is because we have, for instance, one guy that we’ll use that is legal, but he has a team and the team, sometimes - it changes all the time who it is. But I see this in many cases where the price of that team has gone down, and it’s illegals across the entire world, or entire country, rather, that are pressing the price down because these guys will work for peanuts and they’re illegal. And this has been part of the administration’s plan to get that wage growth down by getting all these illegals in and shutting off the cameras…

Skip the narrative and simply look at the facts. The facts are the cameras are off, and we have 50,000 illegals coming in every week for two years. That is not by accident. It can’t be by accident because it’s so big…

It’s to get yields down. I see it. I see it now, and I think we’re going to see it in the jobs numbers moving forward where a lot of the lower ends are going to get displaced at restaurants, things like that. You’re going to bring illegals in and these people are going to have a harder time looking for work. And I see it. I see it in my renters. I own a bunch of lower middle class things, and our rents since the end of last summer, a third of our rents have been three weeks late every month. And that’s a big number, and I see it nationally. So it’s happening. It’s happening. And this is my part of being a scientist. I don’t look at what’s being said. I simply look at what is being done and what the impacts are. And in my experience, the impacts are almost never by accident. They’re deliberate and they do think through this and how to do it. And I think it is all about getting yields down so that we can have a stock market that is up all the way till November of this year. And that is the only day they care about because it’s the only card they got. Remember, Yellen’s gone if Biden loses.”

I’m not sure of the motivation(s) for what’s going on, but as Mike says - letting millions into the country, with no vetting, is not an accident.

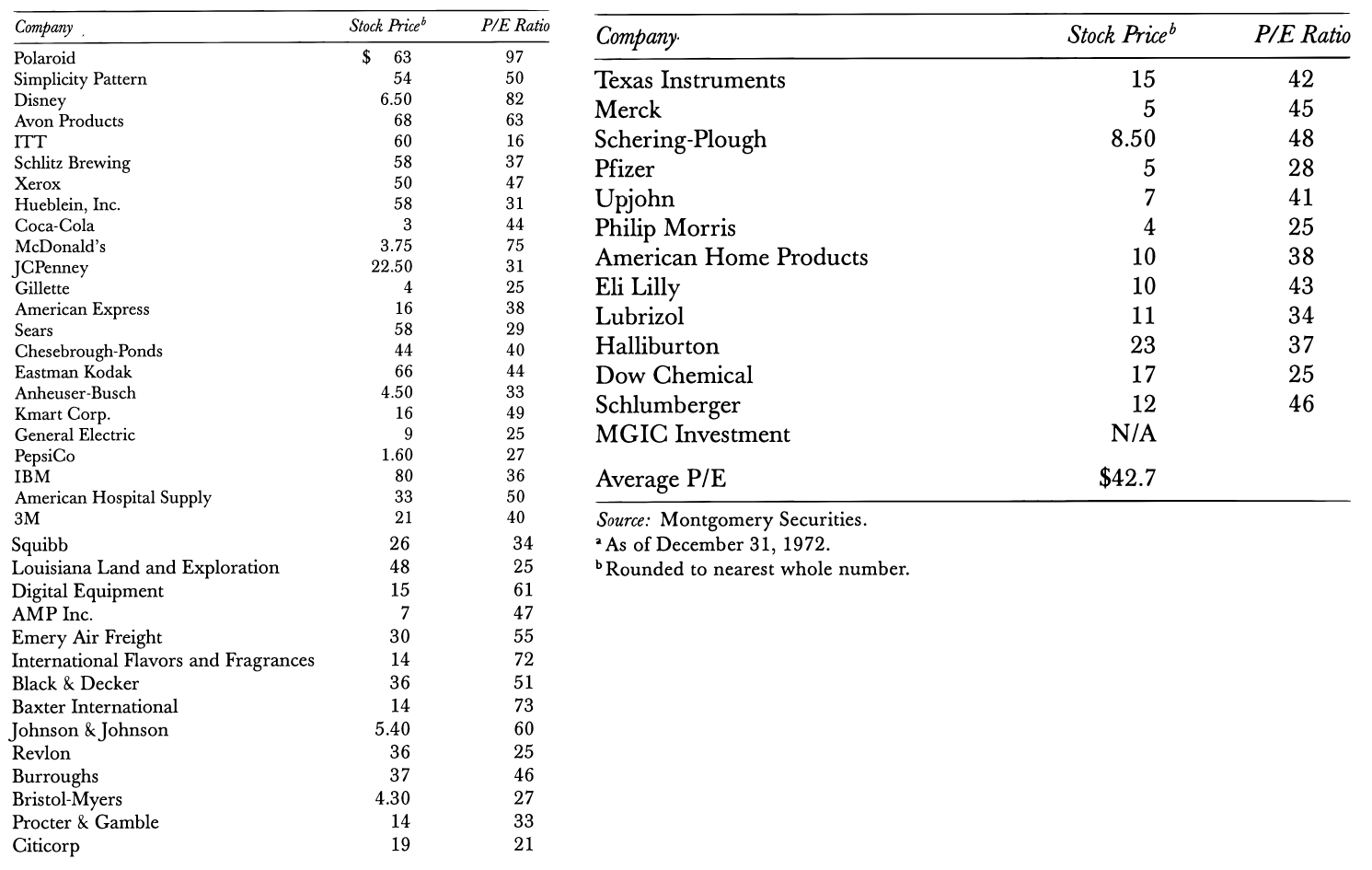

I thought the comments below were more interesting than the chart…

“In the late 1960s and early 1970s, major institutional portfolio managers became so enamored with the idea of growth in general, and with the so-called “Nifty-Fifty” growth stocks in particular, that they were willing to pay any price at all for the privilege of owning shares in companies like Xerox, Coca-Cola, IBM, and Polaroid.

These investment managers defined the risk in the Nifty-Fifty, not as the risk of overpaying, but as the risk of not owning them: the growth prospects seemed so certain that the future level of earnings and dividends would, in God’s good time, always justify whatever price they paid. They considered the risk of paying too much to be minuscule compared with the risk of buying shares, even at a low price, in companies like Union Carbide or General Motors, whose fortunes were uncertain because oft heir exposure to business cycles and competition.”

Peter Bernstein, Against the Gods

Jim Cramer a few decades later (January 2000):

Successful individual investors couldn't give a hoot about bargains. They don't want to speculate that a bad company is turning good again. They aren't drawn to a Xerox. They want a Cisco. There is a tremendous propensity among lower-performing individuals to want to jump off the Sun Micro1 and the Nortels2 for the next new hot stock. But those who have traditionally done well know that switching horses like that doesn't work.

“Yesterday Cramer Berkowitz paid 176 times trailing earnings for 10,000 Cisco. Frankly, as recently as three years ago, that would have been unbelievable. Every analyst would have downgraded the stock on price or valuation. More portfolio managers would be short the stock than long it. We would have sold every share.

How did this happen? How did the whole world (except the troglodytevalue managers) come to understand that the price-to-earnings multiple valuation work, the traditional work, didn't work anymore? How did it become routine to pay 100, 200 and 300 times earnings for some stocks, while totally avoiding other, much, much cheaper equities?”

Cramer, right at the 2000 DotCom peak:

You have to throw out all of the matrices and formulas and texts that existed before the Web. You have to throw them away because they can't make money for you anymore, and that is all that matters. We don't use price-to-earnings multiples anymore at Cramer Berkowitz. If we talk about price-to-book, we have already gone astray. If we use any of what Graham and Dodd teach us, we wouldn't have a dime under management…

We have a phrase on Wall Street. It's called raising the bar. If you can raise the bar, or brighten the outlook for your company, if you can see your growth accelerating, your stock will go higher and you will be given the currency to expand, acquire and do whatever you want. That's the secret of the quintessential New Economy stock: Cisco (CSCO:Nasdaq - news - boards). This giant networker has the ability to control its own destiny. It can, as my colleague Adam Lashinsky says at TSC, buy any company it wants to. It can pay any price. Because it has a currency that it better than U.S. dollars: It has Cisco stock. It can do that because it raises the bar every quarter!

Here is a chart of Cisco since Cramer published that gem twenty-four years ago…

The Original Nifty-Fifty

"It is very rare that you can be unqualifiedly bullish as you can be now."

Alan Greenspan, Jan. 7, 1973.

The Dow lost 50% by Oct. 1974.

Horizon Kinetics Q4 2023 Portfolio Update - January 24, 2024 I never miss these with refreshingly divergent analyst Steve Bregman. I own a little of their Horizon Kinetics Inflation Beneficiaries ETF.

Note for the kids and Larry Fink: The HK guys are very into Bitcoin, and have been for over 7 years (thanks to Murray Stahl).

“We lived the bulk of our professional lives, which date back to roughly the 1980 period, in a disinflationary environment. We didn't know it at the time, but it was the end of the inflationary era. History records that it ended because the Federal Reserve raised interest rates to an appropriately high level, slowing the economy enough that the pricing pressures relented. Murray never believed that argument at the time. We don’t believe it now, even though it is accepted history. The different story is that the world of 1982 and 1983—especially the industrialized world as it then existed—benefited from a series of economic miracles that had nothing to do with the Federal Reserve.”

“Another special investment attribute of hard asset investing: there is very little supply of such companies and almost no index presence. That, too, is an aberration of the past several decades of the financialization of investing, enabled by low, then artificially low interest rates.”

“Even in a historically benign inflation environment of 3%, even for a global reserve currency like the U.S. dollar, money loses over 85% of its value in the course of a 70-year lifetime”

“All of this can probably be reduced to a couple of paragraphs. It’s about scarcity investing in a world in which the geopolitical supply and demand forces and the competitive relationships of the past 40 years are being challenged, ending and even reversing.”

fyi Several people sent me this: Rules for the Ruling Class, on Tucker Carlson and others.

“In declaring war on the upper class that made him, Carlson joined a long, volatile lineage of combatants against the élite.”

Difficult to take seriously an article on elites written in The New Yorker, but go for it.

All I know is that Janet Yellen has been at the Fed on and off since 1977, and is now Treasury Secretary, Epstein-buddy Bob Rubin was quoted in the news the other day, Epstein-buddy Larry Summers is a daily fixture on Twitter and Bloomberg, Epstein-buddy Lynn Forester de Rothschild founded “Coalition for Inclusive Capitalism” with a straight face, and our President was first elected to Congress in 1973. Somehow we’ve had 40 or 50 years of the same sociopath “elites” running things. It’s a big club.

As of Dec. 31, 1999 Sun Micro had a market cap of $116B. Sold out to Oracle in 2010 for $7.4B.

At its height, Nortel accounted for more than a third of the total valuation of" the TSX.

The interesting part of the New Yorker article was the point that before the Fed was created, the elites had to self-fund bailouts to prevent the hoi polloi from rioting outside their Park Avenue penthouses. Post-Fed, the elites no longer had this “noblesse oblige” arrangement, creating another layer of remove from the general population while also preserving their wealth from costly bailouts. Not sure if entirely historically accurate.. but interesting. And reason #247 to end the Fed.

Open borders are simply a response to Trump. Trump ran on the platform of building a wall, then our response to that is opening the border. Trump was tough on Iran, so we'll throw money at them and eliminate sanctions. Trump put the Houthi rebels on a terrorist list, so we'll take them off (until we need to put them back on). It's a pretty long list opposite responses, and it doesn't matter if it makes sense or not.

Back to the market, didn't you have a chart a couple of articles back that indicated there is often a decline in the market after rate cuts start? And I thought cuts were typically a response to a slowing / worsening economy, as opposed to causing a worse economy? I get that lower rates increase the money supply, but given past history it doesn't seem very wise to be betting on the market once rate cuts start. What am I missing?