A World of Hurt

There’s almost a tsunami coming through

Most of my jokes end up being premonitions:

Can’t wait for taxpayers to bail out Ripple!

“Wall Street strategist Tom Lee is aiming to create the MicroStrategy of Ethereum”

“BlackRock's Rieder expects two Fed rate cuts this year.”

I'm glad I'm not alone in seeing through Rick Rieder's bullsh*t.

Here’s Ben Hunt in May 2024:

"The people who benefit from cutting interest rates are the people on Wall Street who own financial assets."

US banks announce big shareholder payouts as Fed eases stress tests

This will enable the banks to pay higher speaking fees to ex-FOMC members.

The Fed Balance sheet is - as I write this - $2.337 TRILLION higher than when Janet Yellen said this in June 2017:

“Since our 2014 normalization principles, that we wanted to reduce our balance sheet in a gradual and predictable way. And we have tried systematically to communicate more about how we would do that as our plans have evolved…My hope and expectation is that when we decide to go forward with this plan, that there will be very little reaction to it, that it’s clear how we intend to proceed, and that this is something that will just run quietly in the background over a number of years”

Core PCE - "the Fed’s preferred gauge" - has now been above 2.5% YOY since April 2021.

They're not even close to their made-up ‘2% target,’ much less their actual mandate of "stable prices.

And still we get propaganda like this:

CPI Nonsense #34,293

The BLS CPI weighting for "Health Insurance" - my biggest expense after taxes, which are not in the CPI - is 0.79.

The BLS CPI weighting for "Housekeeping supplies" is 0.81.

Their legal mandate is 0%.

Central banks are the enemy of most people.

No normal person on Earth worries that their annual cost of living increase might “undershoot” some PhD’s made-up “target.”

This is something Greg Weldon has been harping on for ages…

"Ulysses S. Grant and the Panic of 1873"

President "Grant did not bail anyone out, including his brother-in-law, which was consistent with the way he approached national finance in general; namely, by focusing on the real economy without regard to the consequences to speculative finance or any special interest, including partisan politics."

Boy, do we need this kind of leadership today!

Calandro notes that “the monetary base more than doubled from 1860 to 1865 (compounding at 20 percent).”

I note that the monetary base doubled from $3.2T in September 2019 to $6.4T by September 2021 - a Civil War-level monetary inflation, in just two years.

“These Soviet newspapers, they painted a rosy picture until the very end…media was used as a propaganda tool and no one believed it anymore.”

"The rules are simple: they lie to us, we know they’re lying, they know we know they’re lying but they keep lying anyway, and we keep pretending to believe them." -

Elena Gorokhova, A Mountain of Crumbs: A Memoir

Plenty of thought-provoking anecdotes below - some would say “too many,” as the most common reason paid subscribers give for un-subscribing is “time.”

You don’t have to click every link. I just do what I do, and post things that catch my eye during the week, and if that interests you, super, and if not, that’s ok too. I’ve been doing this format now since 2009 (the last few years on Substack), and since I search these often as a sort of database, I'd probably keep doing it with no readers.

Below the fold we’ve got some government data charts - for what those are worth, some music, the exodus, or non-exodus, from U.S. investments, bonds - which apparently some people own, CRE unpleasantness, some discussion of “overvaluation”- which sounds communist to me, various sober warnings everyone will ignore, H-1B visas (MAGA!!), Housing(!), Cape Coral, Melody Wright, Mike Green/Harley Bassman/John Comiskey, some guy who thinks American needs to lever up (into private credit!), hedge funds getting into private credit(!), the usual complacency, bailing out Peter Thiel again (probably), solar stills, and more.

There’s nothing new under the Sun.

I’ll get most of the government data out of the way. I normally try to ignore all this, but it’s been a while…

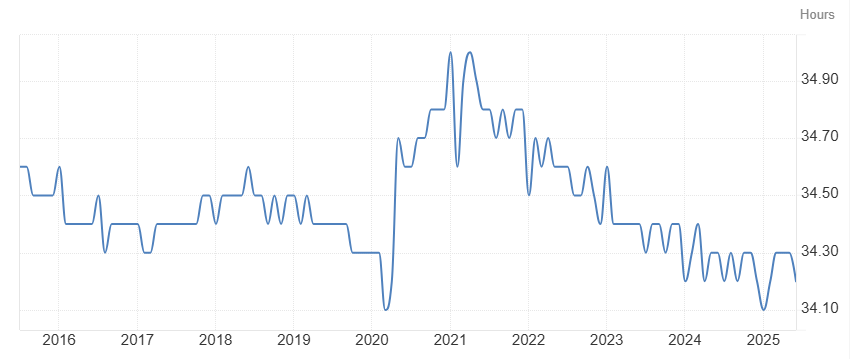

Average Weekly Hours are back to early 2020 levels though…

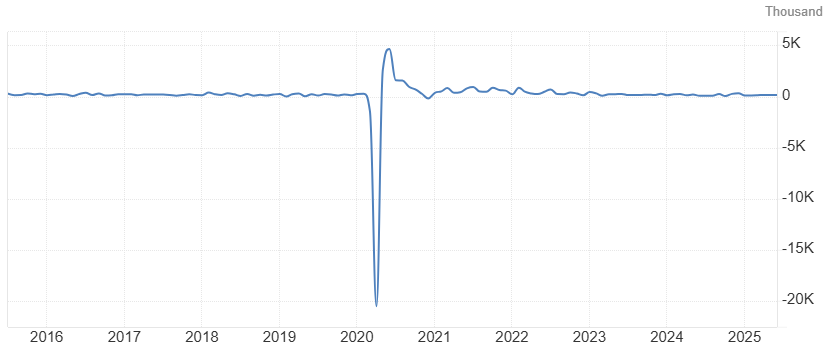

Quite a boring chart, most of the time: U.S. Non-farm Payrolls

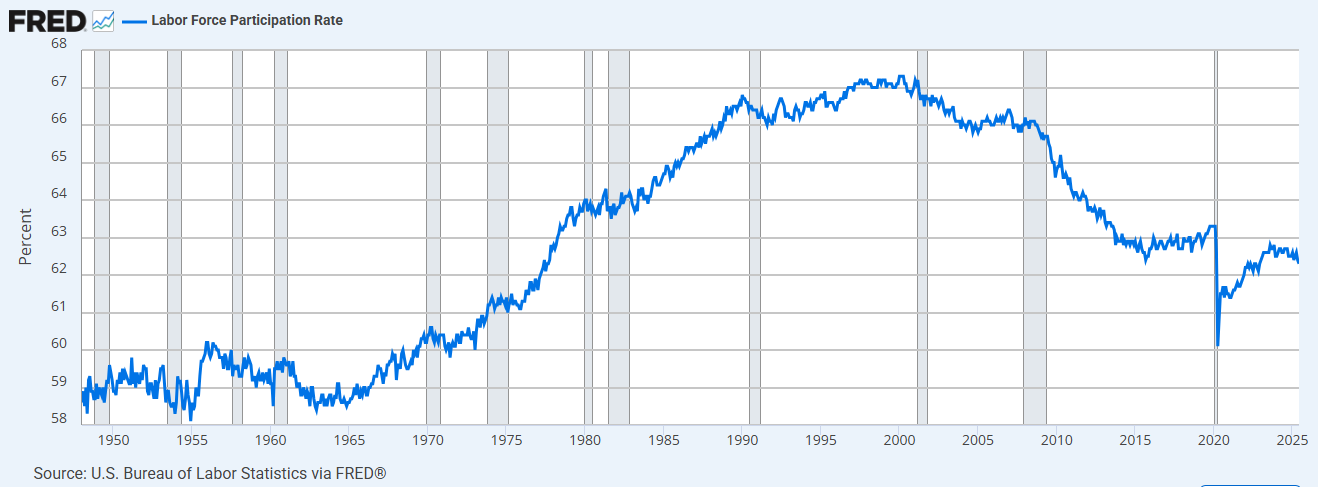

The “Participation Rate” fell…

Mid-day Thursday

"I'd like to believe that the Fed puts out real numbers that show you what the real CPI is, and what the real jobs number is...but that's not the world we live in, right?"

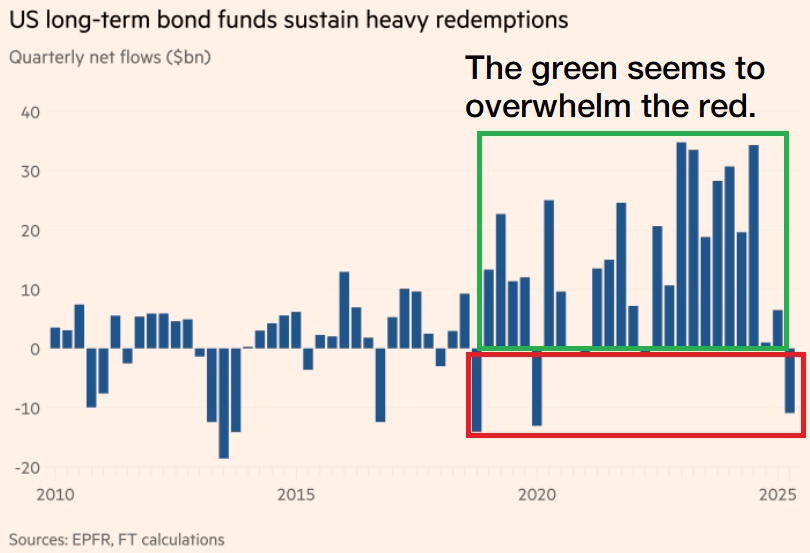

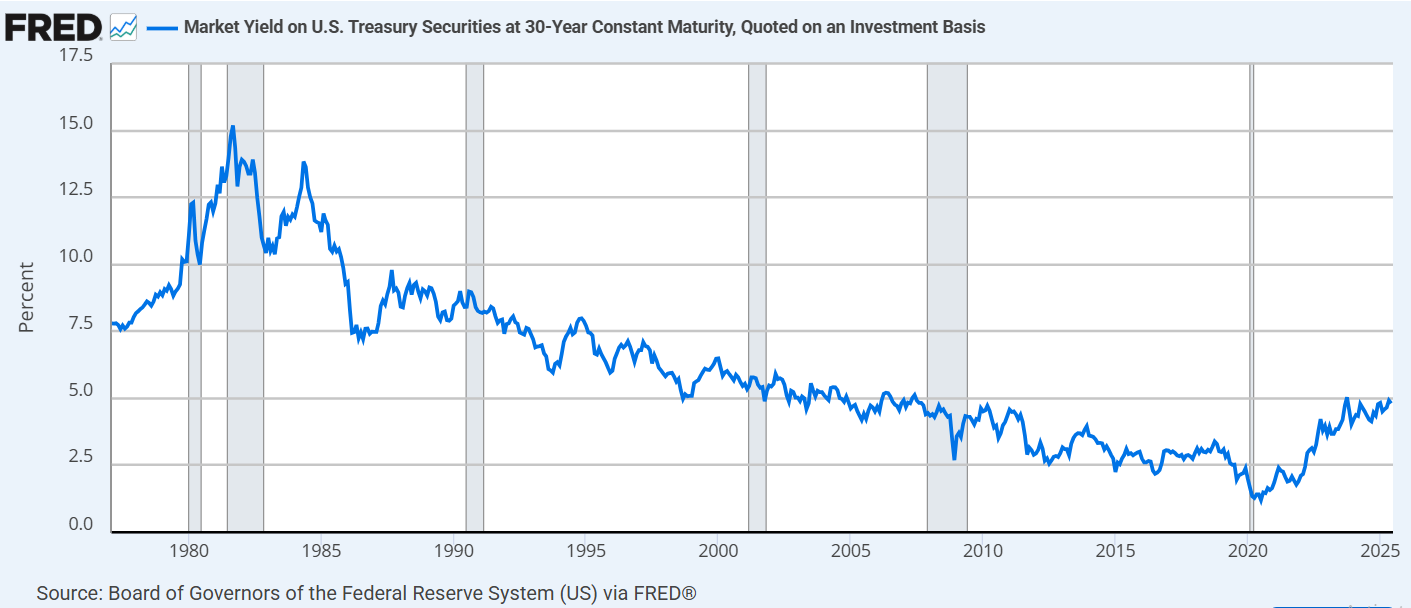

FT: “Fears over US debt load and inflation ignite exodus from long-term bonds”

The 30-year yield still seems historically subdued:

The U.S. 10-year is at 4.34%. I would not want to own 30-year (or 10-year) debt. I can understand buying those as a trade - e.g., you think rate cuts are coming due to a recession or mean Trump tweets - but other than that, nope.

"The guy who’s selling you the bond is publicly saying, “I’m going to debase these bonds.”"

- Dave Dredge

I also would not want to flee risky America for the safety (cough) of European junk bonds, but that’s just me: European junk bond sales hit record as investors cut US exposure

"Fed’s Powell Gets Love Bombed in Europe After Trump’s Taunts"

From ‘Tim Young’ in the FT comments:

Having read the article and down the comments (which I would urge every reader to do at least some of before commenting themselves, as a matter of good etiquette), I am amazed that no-one has mentioned what I would say, as a former investor in US treasuries, is a 500lb gorilla in the room. That is the numerous suggestions to impair foreign creditors to the USA, including Miran's proposals about forced conversion of foreign exchange reserves managers' holdings of treasuries to hundred year bonds, or a user-fee, and the ideas in Section 899 of the BBB. [I believe this has been taken out, but who knows]

To not consider lightening up on treasuries when your debtor is openly discussing such acts of bad faith, you would have to be negligent. I was warning about this likelihood over a year ago, before Trump was elected, because of his well-known casual attitude to paying his own debts.

People need to stop the denial here; under Trump, and with the arrogant attitudes of some Americans that he has brought to the surface, which remind me of an Argentine finance minister I once had a discussion with (along the lines of their creditors deserve abuse, for demanding such high interest). It is not unthinkable that the USA could strategically default. The crass fools currently running the USA are giving US creditors no choice but to reconsider. I would say that the genuine credit rating of the USA is much lower than Moody's recent gesture suggests.

In my experience, divestment decisions take some time, with papers, meetings and sign-offs required before any action is taken, taking different amounts of time in different organisations. But the leakage has begun, and will extend for a long time.

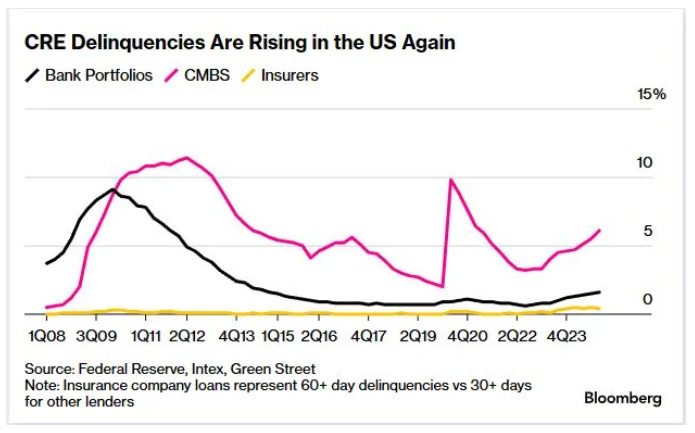

Commercial Real Estate Distress Is Spreading: Credit Weekly

Delinquencies continue to increase, though the rate has moderated, researcher Green Street said this past week. Distress is also climbing, rising 23% to more than $116 billion at the end of March from a year earlier, data compiled by MSCI Real Capital Analytics show. That’s the highest in more than a decade.

Investors including Victor Khosla of Strategic Value Partners LLC have warned that debt maturities will lead to a “tsunami” of problems for US offices in particular. There are signs that’s spreading. The past-due and nonaccrual rate for commercial real estate portfolios reached the highest since 2014 earlier this year, the Federal Deposit Insurance Corp. wrote in a report last month, citing multifamily as an increasing source of pain. Past-due and nonaccrual loans are so far past due that banks have stopped booking interest owed because they doubt they’ll ever receive it.

SVP’s Khosla Warns There’s a ‘Tsunami’ Coming for US Offices

There are “problems galore” in US office real estate and it’s so troubled that it’s difficult to underwrite, according to Victor Khosla, the founder of credit investor Strategic Value Partners LLC.

“There’s almost a tsunami coming through,” he said in an interview with Bloomberg Television on Thursday. “You don’t see it in the headlines quite as much, but underneath those debt maturities” are “causing a tsunami.”

Landlords for offices, apartment complexes and other commercial real estate have $1.5 trillion of debt due by the end of next year, broker Jones Lang LaSalle Inc. estimates, and many will have to refinance at higher rates. Offices are particularly vulnerable as demand has dropped following the rise of work from home and many of the buildings require substantial investment in order to make them attractive to tenants.

SVP has looked at 100 deals in the office sector over the past six to nine months and made just one, he said.

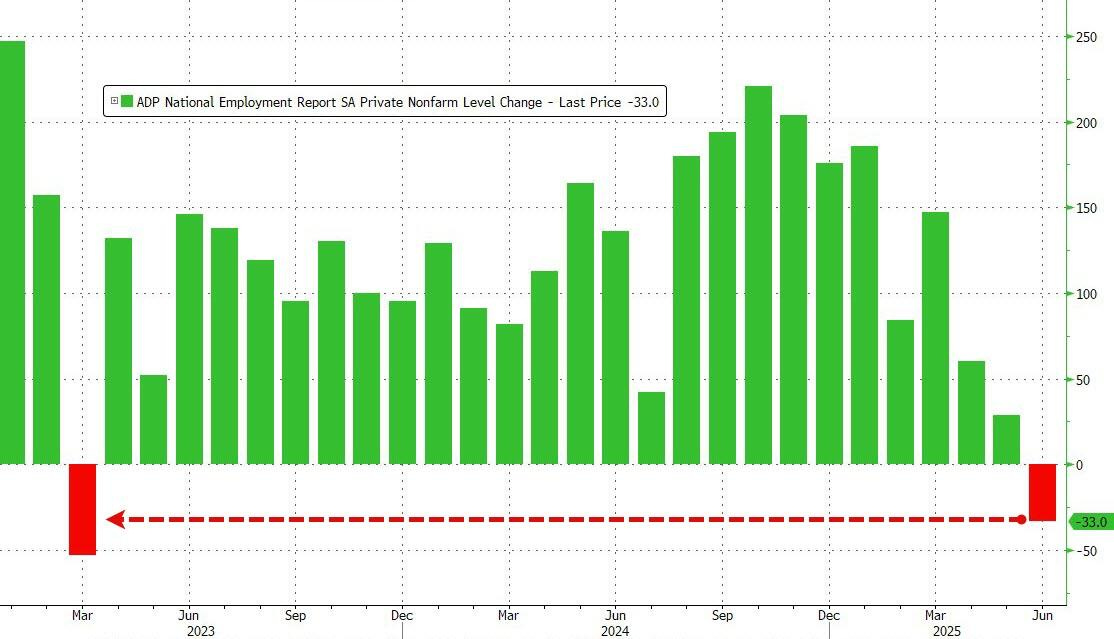

Earlier this week…the consensus was +95K, but it came in at -33K.

Apparently “That is a 5 sigma miss from expectations...”

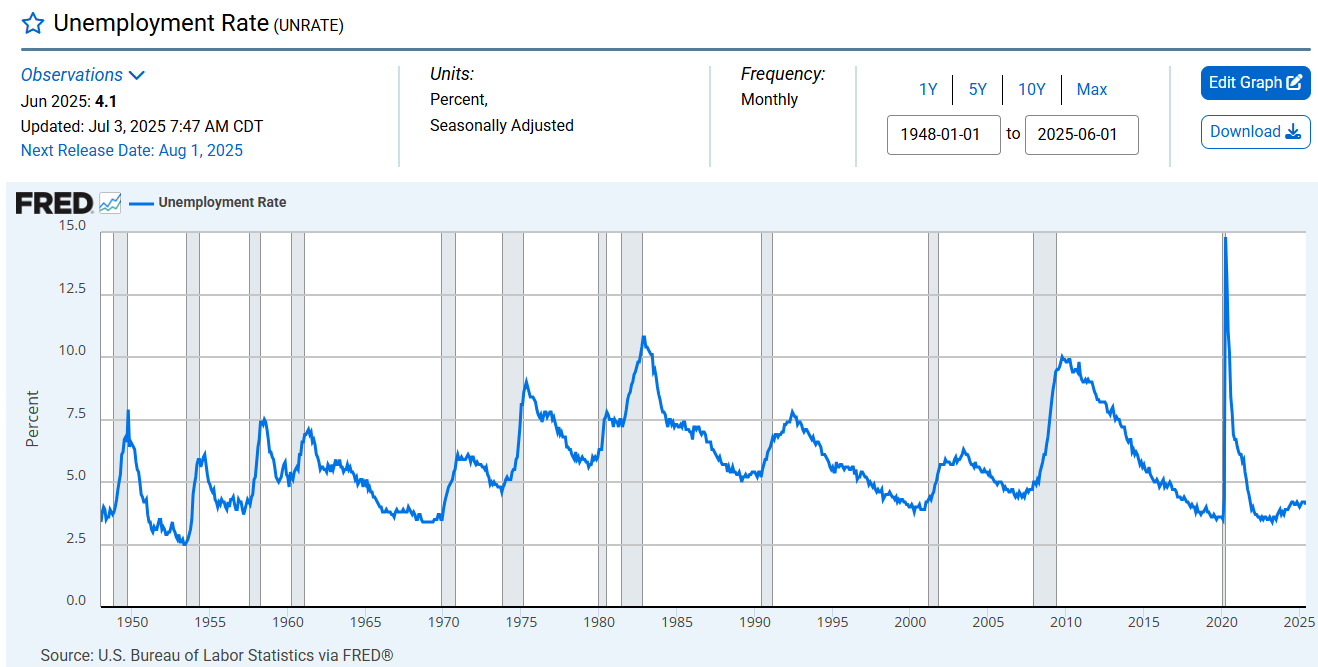

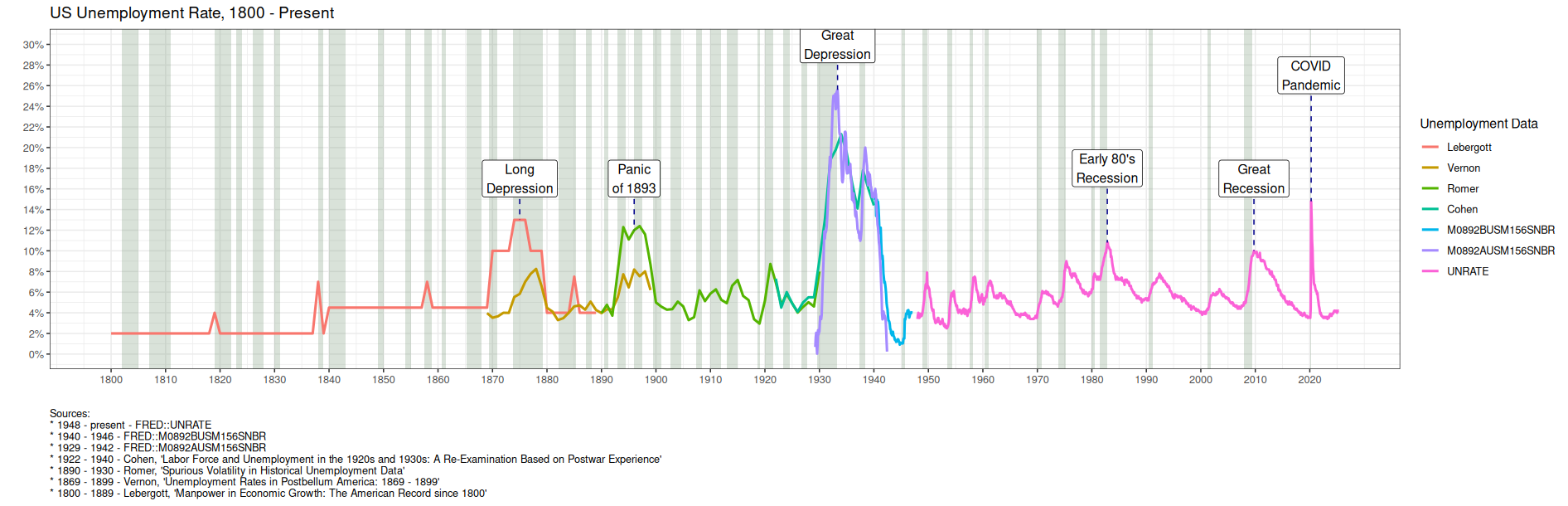

U.S. Unemployment Rate 1800-Present

Looks like a historically low unemployment rate (4.1% officially), yet the U.S. budget deficit is projected to be $1.9 trillion for the full fiscal year 2025.

May we live in interesting times.

I will note that even during severe downturns, unemployment directly affects 10%-12% of the population - even 20% in the 1930’s - and we now have safety nets for those affected, yet a higher cost of living affects 100% of the population, and is the most regressive tax.

Market Overvaluation?

When the majority of flows in a market are price-insensitive passive flows, is ‘overvaluation’ relevant?

I suppose if flows ever reverse, it will be.

This “chart gives a simplified summary of valuations by plotting the average of the four geometric series (the first chart above) along with the standard deviations above and below the mean. The latest value of 156% is up from 152% in May. The current geometric average is more than 3 standard deviations above its historical mean. Again, signaling an overvalued market.”

")

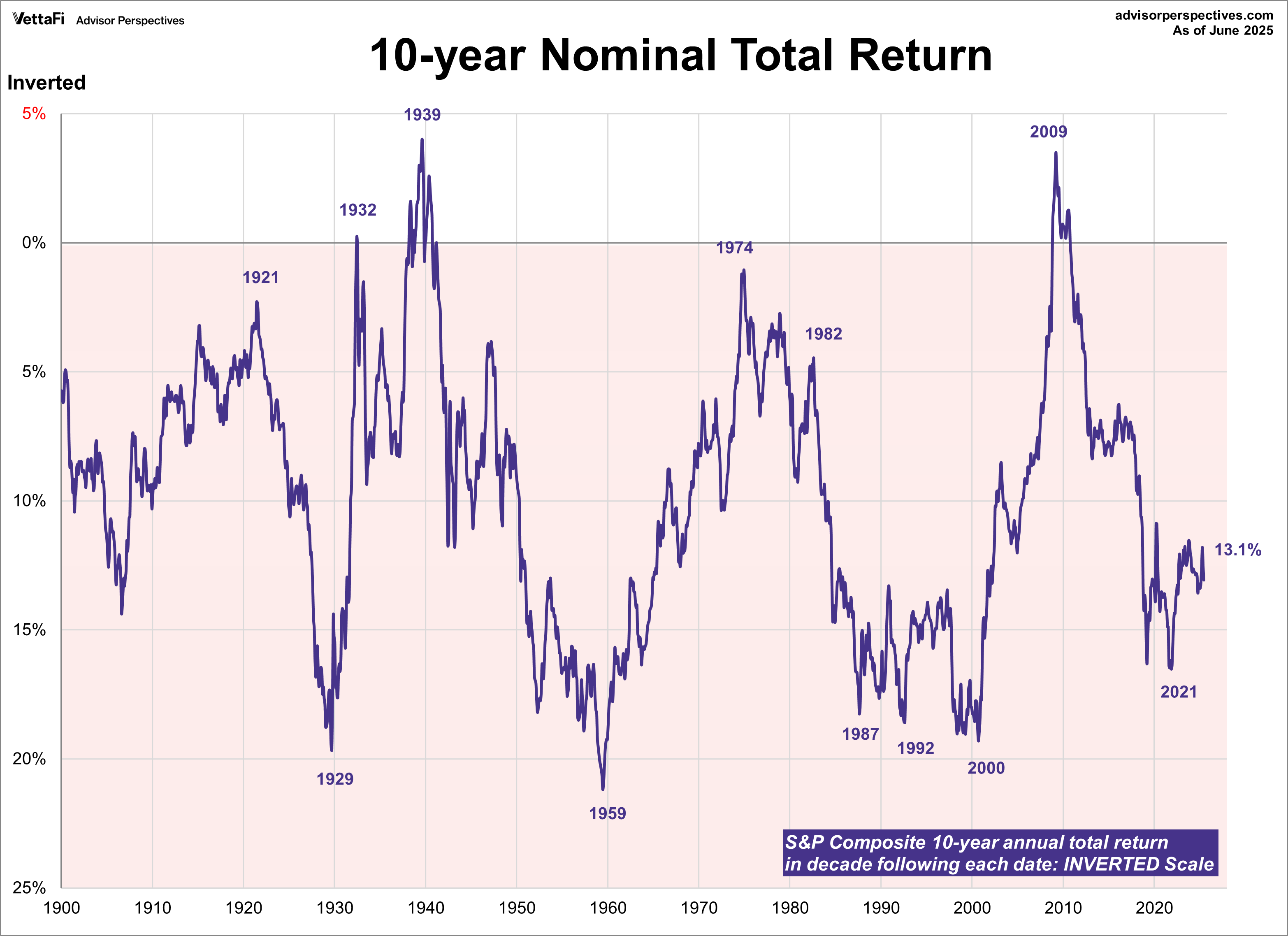

“Points of ‘secular’ undervaluation such as 1922, 1932, 1949, 1974 and 1982 typically occurred about 50% below historical mean valuations, and were associated with subsequent 10-year nominal total returns approaching 20% annually. By contrast, valuations similar to 1929, 1965 and 2000 were followed by weak or negative total returns over the following decade. That’s the range where we find ourselves today. Of course, we also won’t be surprised if the S&P 500 ends up posting weak or negative total returns in the 2007-2017 decade, which would require nothing but a run-of-the-mill bear market over the next couple of years.”

- John Hussman

For what it’s worth, here’s one person’s attempt to quantify market “overvaluation”: “a dashboard using 5 different metrics of stock market valuation (CAPE, Tobin's Q, modified Buffett ratio, Aggregate Investor Allocation to Equities, and detrended log[price]) to let me see how the stock market is doing. Today the stock market is at it's 3rd highest overvaluation in the last 150 years, right behind the dot.com bubble and the Great Depression bubble.”

“Equity investors exhibit zero concern about debt and deficits while Wall Street works overtime to stuff the economy with every conceivable form of debt even as increasing volumes of that debt fall delinquent or default. The S&P 500 trades at a P/E multiple of almost 30x while the Nasdaq trades at an even higher multiple of 40x, levels only reached before periods of sharp and painful declines. American companies are buying back their own stock at a near-record $4 billion a day – once again demonstrating their proclivity to buy high despite claims of disciplined capital management. The U.S. dollar traded down about 10% year-to-date as the least-dirty-shirt in the fiat currency club without causing any concern among investors at home or abroad, something on which to keep an eye (along with the price of gold which should be bought).

While I am usually the first to warn about overextended markets, I don’t see anything in the immediate future (three months) likely to stop this train. But while all is calm for the moment, we should that Hyman Minsky taught us that stability breeds instability. Signs of market speculation are everywhere in the loosest regulatory environment in memory. The longer things remain quiet, the more we will see risk rise in ways that will eventually turn out badly.”

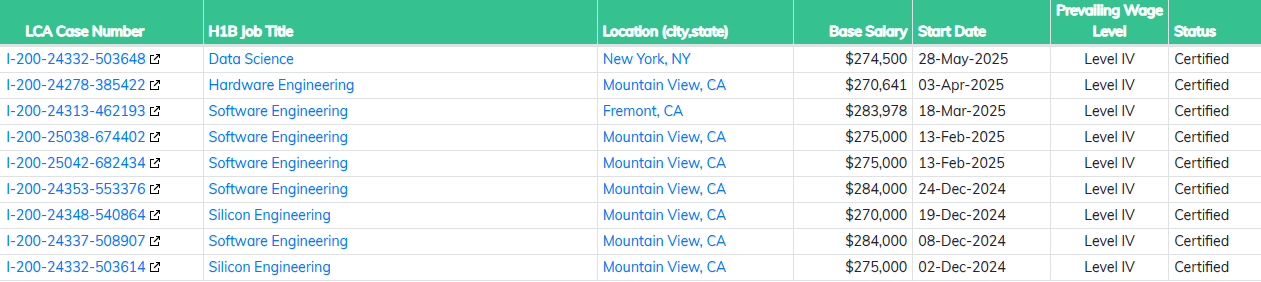

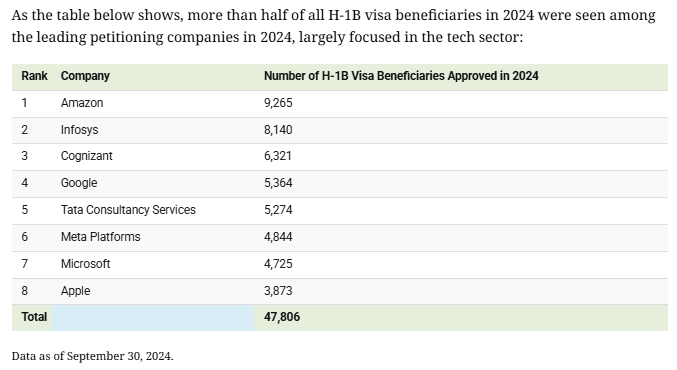

H-1B Visas

Microsoft to lay off about 9,000 employees in latest round

Meanwhile…

List of H1B Labor Condition Applications (LCA) for Microsoft Corporation - Fiscal Year* 2025

Thinking of Aristotle: “It is also a habit of tyrants to prefer the company of aliens to that of citizens at table and in society; citizens, they feel, are enemies, but aliens will offer no opposition.”

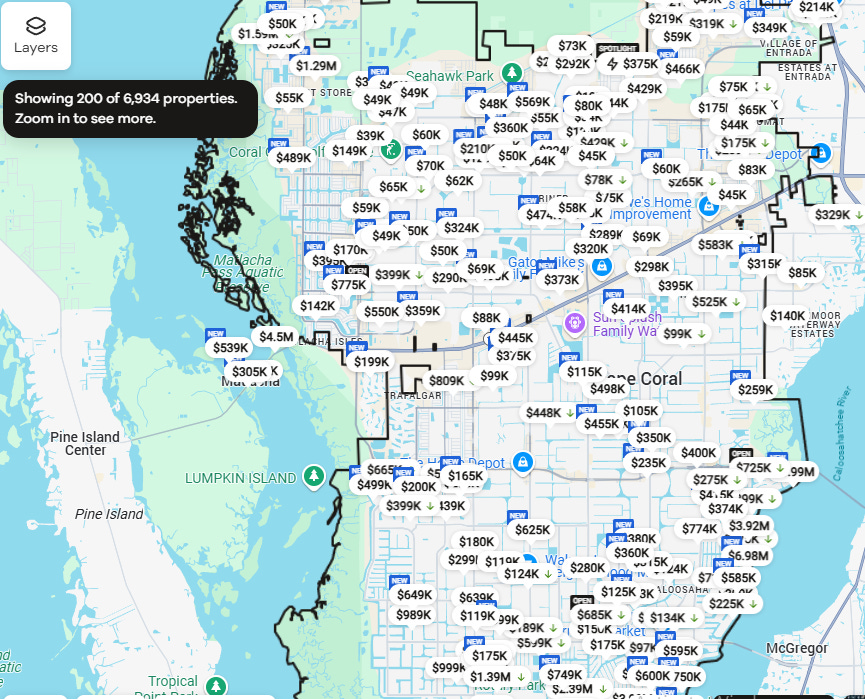

The Worst Housing Market in America Is Now Florida’s Cape Coral

Thousands found an inexpensive slice of paradise in Cape Coral, a city with more canals than anywhere else in the world. Househunters were so taken with this boating community on Florida’s west coast that many purchased homes sight unseen during the early years of the pandemic.

The median home price soared nearly 75% to $419,000 in three years, transforming the character of this middle-income community that for decades has catered to retirees and small investors.

Now, three years later, “For Sale” signs line every other block. Open houses are deserted for hours. Foreclosures are ticking up. Home builders are listing half-built shells at discounts as they abandon projects to cut losses. Locals say the lack of traffic has led to an increase in vehicles speeding through empty residential streets.

“Cape Coral is the worst housing market in America right now,” said José Echevarria, a Realtor. “I don’t think we’re at the bottom yet.”

Home prices for Cape Coral-Fort Myers have tumbled 11% in the two years through May, the most of any major metro area, according to an analysis for The Wall Street Journal by the listing site Homes.com.

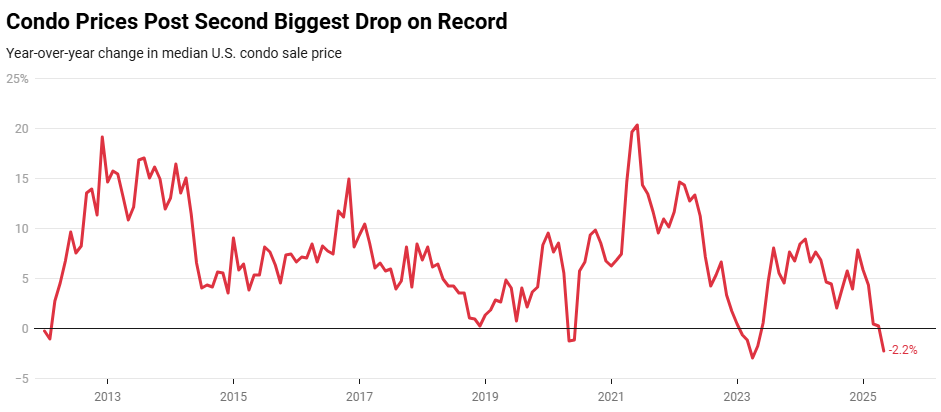

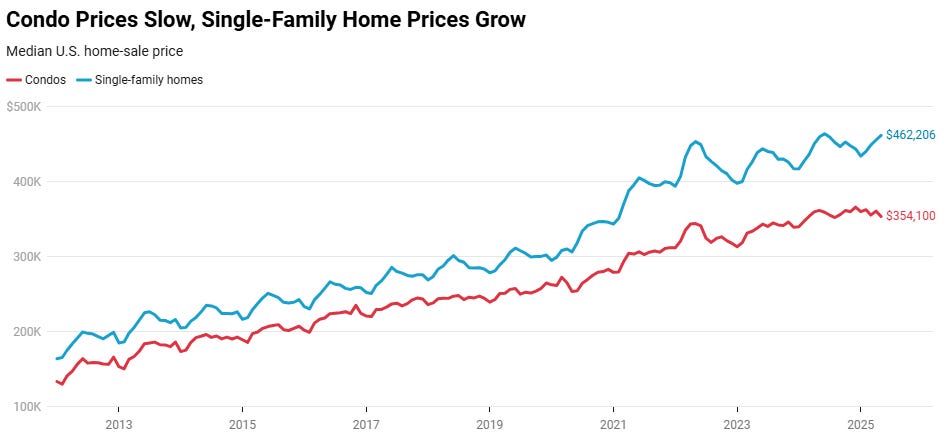

One man’s attempt to quantify housing “overvaluation”:

Condo Prices Dropped 2% in May—the Second Largest Decline on Record

Still…

Melody Wright

Housing today is about speculation, not shelter.

“There's no reason you have 15,000 short-term rentals in Austin there's no reason you have 12,000 in San Diego there's no reason you have 36,000 in little Hawaii…”

“We have 15 million vacant homes. We have 3.3 million vacant seasonal homes. What we've done is really try to get every Tom, Dick, and Harry either into a home, or get them another home, because our our Gen Z-ers our younger millennials can't afford anything. What's actually been happening is that average household size has been going down, as have our birth rates. As we know, our demographics are abysmal, and unless we want everyone to have one house each, we are way oversupplied.”

“The reason I got really, really concerned is when I went out on the road in 2023 to all these new-build communities all over the country - and don't say that

they're only in the South, that's simply not true, they they did it everywhere there was land - they overbuilt in small towns that made no sense, and so the builders are in serious trouble, but what I always caution people about with the builders is that they always s stand very close to a government handout.”

On house flippers and investors: “Speak to any millennial that had a decent job. They all have an extra home that they were going to fix and flip. I to out on the

road, I've I've driven over 10,000 miles, flown a lot more than that, to go to these local communities and talk to people, and you would just be astounded how many people went out and bought an extra home because they were going to

rent it out or do short-term rental.”1

“We’ve hyper financialized [housing] and it's about moving money through the system now, and not about shelter, and so it's not a game for the first-time home buyers. We had the fewest amount of first-time home buyers since 1981, and that's when they started tracking the stat, the National Association of Realtors, so this game is about speculation. It's not about shelter.”

“This is not investment advice, but let me tell you who you should be looking at is non-banks, so your Mr. Coopers, your Rockets, your Freedoms. These non-banks are in for a world of freaking hurt.”

‘Why we are shutting down our AirBnB, quitting the platform an selling our home’

Something I found on the Reddit…

“If you are thinking about starting an AirBnB please take some time to consider how they treat their hosts. You are not their partner, you are their product. Despite the fact that you pay them 14% of your revenue, you are not their customer - the guests are the customer. They are always going to side with the customer because that's who pays them.

They could care less about you or your business and they show it at every step. Be wary. You might be better off investing your money in a healthy mix of stocks and bonds and spending the rest of your time on the beach.”

I personally hope every AirBnb owner sells their neighborhood motels, and I hope that - instead of Stephen Schwarzman and Barry Sternlicht buying them - the homes drop in price to a reasonable level and are purchased by young people so they can start families. Crazy talk, I realize. I am not a communist.

Mike Green

“We effectively recreated a subprime-type crisis”

“Effectively what we're saying is is that for a long time we've heard that the consumer balance sheet is very strong. Part of your [John Comiskey’s] argument would be that's a natural byproduct of the pandemic era programs. Basically, you don't have to pay on your student loan debts, we're not going to report you if you're delinquent on payments and houses etc. That that effectively led to - maybe a reasonable phrase is FICO-free - effectively people became higher quality credits because we were not tracking whether they were not paying. This contributed to the narrative that we were seeing only strong credits add capability, add credit to their exposure, this is not the subprime crisis. I would introduce a chart very quickly that you shared with us which is basically saying no, that's that's pretty much exactly what it is. We effectively recreated a subprime-type crisis by suspending that reporting and making it very different. Now you're saying those are coming online, we're starting to get a much clearer picture of what things actually look like…the consumer balance sheet strong if we ignore the liabilities. Now the liabilities are coming back on.”

John Comiskey

“I don't view this - at least on the surface - as an existential risk to the mortgage insurance fund of the FHA. I think there will be some measure of loss, because if you look at their loss severity, the paltry amount of foreclosures that actually are taking place now, it's higher than you would think it would be given the rise in home appreciation, I think oftentimes because the properties that get to that point are in such poor shape.”

Harley Bassman on GSE Privatization

“My reaction is that GSE privatization is about as bad an idea as we could ever make up in this country, and its sole purpose is to pay off one person for his support in the election. It’s pure graft.”

“We buy stocks the way we buy toilet paper: high quality, on sale, and in bulk sizes.”

This is just for future historians:

When margin loans and levered ETF’s aren’t enough…

“It's always leverage that brings you down” - Danny Moses

“You are the owner of the LLC, and you have $2 in it, and then we give the LLC $8 financing, as term financing, non-mark to market, non-marginable, so now you have $10 of investable assets, and of that $10, right now, we put $9 in private credit, and $1 in the S&P 500” - Abdul Al-Assad

I’m reminded of the friends who lost 90% of their money being levered-up during the DotCom bust…

‘Investors will discover again that there are no new financial eras and excesses are never permanent.’

The trades that will shape a new financial crisis by Satyajit Das

Das is kind of wacky on some subjects, but he’s excellent on financial matters, and was very prescient before the GFC (Great Depression II). Below are all quotes from the op-ed.

First, investors have increasingly borrowed low-cost funds, often in foreign currencies, to invest in higher yielding investments in ubiquitous carry trades, that are now vulnerable to moves in asset prices and currency values.

Second, investors have wagered on stability by investing in options, either directly or via funds, which hedge a counterparty from volatility. While they pay a premium, they risk large losses when there is more volatility. Likewise, so-called risk parity funds must maintain a set risk level, necessitating liquidating riskier assets when volatility increases.

Third, relative value trades that bet on the relationships between assets have become very large, raising risks if they sour. The basis trade, where investors buy US Treasuries and hedge them with futures to lock in small gains, assumes high correlation between the two and price convergence. Investors also hold large positions on the increasingly unstable spread between interest rate swaps and government bond rates.

Fourth, exposure to illiquidity has increased with the migration to unlisted private equity and credit. The claimed higher returns are in exchange for unquantified liquidity risk.

Fifth, the repackaging of risky or illiquid assets via securitisations and synthetic risk transfer, a form of credit insurance resembling collateralised debt obligations, has grown again in recent years. These slice assets into tranches of varying risk through complex modelling . . . The adequacy of less-secured tranches of those assets to absorb first losses on the underlying loans and protect higher-rated securities created remains unverified.

These structures introduce vulnerabilities that will be ruthlessly unpicked in a crisis. The monetary volumes of these trades are substantial, well in excess of the around $1.3tn pile of US subprime loans that built up before the 2008 financial crisis.

The weakness overall is leverage, both in explicit borrowings but also financial engineering.

Hedge funds lured by private credit boom

Big hedge funds are pushing into private credit as they seek to establish themselves as diversified financial institutions, with Millennium Management, Point72 and Third Point all looking to launch new funds and strategies.

Third Point, a $20bn firm with a history as an activist investor, plans to launch a publicly traded private credit fund next month called Third Point Private Capital Partners, which will lend directly to businesses.

Millennium, which manages more than $75bn in assets, has been weighing whether to launch a separate fund to invest in less liquid assets, including private credit, its first new fund since it was founded more than three decades ago.

Steve Cohen’s Point72 earlier this year hired Todd Hirsch, formerly a senior managing director at Blackstone, to lead its private credit strategy. He has also recruited Alex Greeley from Linden Partners, Jay Ditmarsch from Carlyle and Rudder Zhang from Brookfield Asset Management.

“Hedge funds are in the asset gathering business,” said one leading banker to the sector. “The boom in private credit has really attracted their attention.”

Can’t wait to bail these guys out again.

March 2020

‘A Hot New Firm Opened the Private Market to the Little Guy. Now It Is in Big Trouble.’

In January 2023, the chief executive of the private stock investment firm Linqto announced a “Spike Day,” a one-day sprint to boost sales to its customers—small investors looking for a shot at buying shares of coveted private companies.

“Take no prisoners,” the now-former CEO, William Sarris, wrote in an email to staff, reviewed by The Wall Street Journal. “This is guerrilla warfare.”

Sarris was trying to unload shares of Ripple, a privately held crypto company, to Linqto’s 11,000 users, at a price at least 60% higher than what Linqto paid. The Securities and Exchange Commission generally prohibits markups above 10% but Sarris pushed ahead, not disclosing the price hike to customers, and the company pocketed $2 million, according to people close to the situation. An outside law firm later reviewed the transactions and warned that Linqto’s actions may constitute securities fraud…

Fraud is rather harsh. Why not call it “mis-selling”? e.g.,

"One thing that I know is true with respect to FSOC [the Financial Stability Oversight Council] is - at least my counterparts on that body - are in agreement that non-bank financial institutions don’t pose systemic risk to our markets."

So how long before taxpayers bail out Peter Thiel again at Erebor?

What mystery?

Intelligence doesn't want to punish the perps - they want to control them.

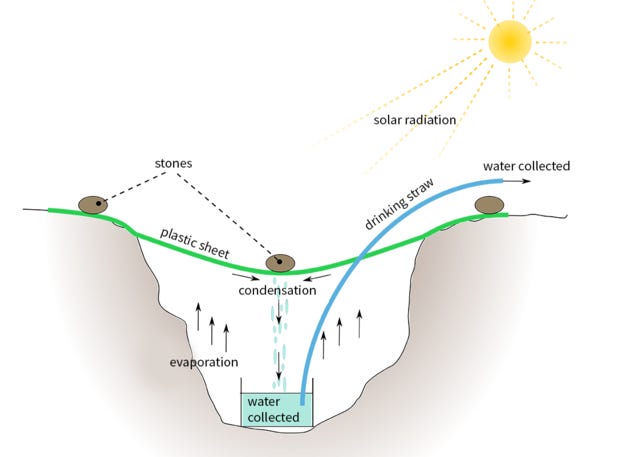

MIT's high-tech 'bubble wrap' turns air into safe drinking water — even in Death Valley

OK, so this article at first sounded like some hi-tech breakthrough I’d be very interested in, for natural disaster-type situations:

MIT researchers have created a high-tech "bubble wrap" capable of collecting safe drinking water directly from the air — even in Death Valley, the driest desert in North America…The water harvester is made from hydrogel (a highly water-absorbent material) that is enclosed between two layers of glass — much like a window. At night, the device absorbs water vapor from the atmosphere. During the day, the water condenses on the glass thanks to a coating that keeps the glass cool. The liquid water then drips down the glass and is collected in a system of tubes….

Researchers tested the new device for a week in Death Valley, a unique desert valley spanning across parts of California and Nevada. It’s the hottest place in the world and the driest place in North America.

So far so good…

It produced about a quarter to two-thirds of a cup of water every day (57-161.5 milliliters). In more humid areas, the device should produce even more water. This design is a lot more effective than some previous attempts to collect drinking water from air, all without needing electricity to power it, MIT representatives said

OK, so 50 years ago we were doing a low-tech version of this - in the desert - that I think produced more clean drinkable water than the MIT process described above. We called it a “solar still”:

CLO Primer from Trepp

Collateralized loan obligations, or CLOs, in a previous incarnation were referred to as collateralized debt obligations because they included not only loans in their collateral pools, but other debt instruments. However, following the Global Financial Crisis, the CDO acronym was retired, and the structure was refined so deals—at least in the commercial real estate world— would include only mortgages in their collateral pools…

CLOs are financing vehicles, unlike CMBS, which are sales vehicles. Lenders sell their originations to a CMBS trust, which is then carved up into bonds and sold to investors. Lenders who use CLOs for financing retain ownership of their loans, which typically are short-term in nature and are used to facilitate property acquisitions, fund sponsors' stabilization or renovation efforts. They'll turn to CLOs as a good source of matched-term, non-marked-to-market financing. A CLO could be among a handful of financing options for lenders. Others would include warehouse credit facilities and loan-on-loans.

Lenders also like CLOs because of their ability to substitute collateral loans in managed transactions. A typical CLO might have a life of, say, five years, but its collateral might have an average life of just more than two years. As loans are paid off, proceeds can be used to finance new ones, retaining the CLO as the funding source.

Lately, issuers of CLOs have been able to get up to nearly 88% financing for their originations.

But the market for CLOs, like all markets, is fickle. Issuance peaked in 2021 at $44.16 billion as investors sought yield in a near zero rate environment, which CLOs provided. That drove a lending craze, particularly against apartment properties. That year, $27.39 billion, or 62% of all CLO issuance, was backed by multifamily loans.

Issuance slowed in 2022 to $30.3 billion and fell off a cliff the following year, when only $8.71 billion of deals were issued. So far this year, more than $17 billion of deals have priced.

Investors in CLOs shied away from all but those deals backed by multifamily loans, which they view as relatively stable.

Among the big issuers of CLOs this year are MF1 Capital, a lending venture that was formed by Limekiln Real Estate Investment Management of New York and Berkshire Group of Boston, which has issued $3.42 billion of deals so far this year; and TPG Real Estate Finance Trust, a mortgage REIT that issued a $1.1 billion deal. Dwight Mortgage Trust, a new issuer, last month floated its first issue—a $925 million deal with an 87.9% advance rate and two-year reinvestment period. Its transaction is backed solely by short-term multifamily loans.

My version:

“Interestingly enough, pre-9/11, the agents that were the broken and misfit toys of the FBI's agent population were sent to terrorism, okay? So is it any wonder why those buildings went down? Not really.”

“Drenched in opiates and regret, I heard this song once and became besotted by it. It sounds like lost love, past lives, unforgiven mistakes and transgressions.”

Happy 4th of July!

A few years ago I went to a poker cash game at the house of a friend of a friend. I didn’t know anyone there, but I’d guess they were all in their early 40’s or so. I didn’t bring any of this up, but they ALL had one or more Airbnb’s, including some out of state! (I learned they were concerned about squatters, and how to change the Wi-Fi passwords remotely.) The host’s wife apparently worked for Snowflake, and the others all seemed like tech types, so they had some money. I mentioned in 2020 that “Every single person I know with the money to do it poured into real-estate because they couldn't get a 6% CD anymore”

Thank you so much Rudy. Never stop posting. Your stack is one of my important lifelines in these crazy times. It has felt very dark out there recently and I need your humor. Hope you had a happy 4th!

The push to dump unmarketable private equity assets into retail retirement accounts and the shear amounts of low quality debt out there is truly frightening. Thank you for shining a spotlight on these shenanigans for those who desire to avoid the icebergs. BTW - did you see Nightingale Associates’ post about 311 S. Wacker Drive? Purchased in 2014 for $302MM. Sold recently for $45MM. This is NOT just an Office problem! High rise apartments costing $500,000+ per unit trading in the low to mid $300,000’s. Unimaginable losses increasingly being forced to be realized.