An unhinged post

A pandemic-without-virus logic

Have a good weekend amigos. Godspeed.

Quarter-End Tape-Painting Tuesday!

Oracle

Your alarm goes off at 6 AM. There's an email from "Oracle Leadership." You've never gotten a message from that sender before. It says your job is gone, today is your last day, and severance details will arrive by DocuSign. By the time you finish reading, your company laptop is already locked.

This happened to up to 30,000 Oracle employees this morning. Oracle reported $17.2 billion in revenue last quarter, its best in 15 years. And it still fired nearly 1 in 5 of its people. The stock went up 6% today.

Oracle owes over $108 billion. The company signed a $156 billion deal to build AI data centers over five years, mostly for OpenAI (the company behind ChatGPT). That requires buying roughly 3 million specialized computer chips. Two years ago, Oracle spent $6.9 billion a year on this kind of construction. This year it's $50 billion.

The 30,000 people who got that email are funding the gap. Investment bank TD Cowen estimates the layoffs will free up $8 to $10 billion in cash flow, money going straight into chips and construction. Oracle filed a $2.1 billion restructuring plan with regulators in March, and nearly $1 billion had already been spent before the emails went out.

Lenders are getting nervous. The cost to insure Oracle's debt against default has spiked to levels last seen during the 2009 financial crisis. Barclays downgraded Oracle's debt in November, warning the company is one step from "junk" status, the point where lenders consider you a serious default risk. Some banks have stopped lending to Oracle for these projects altogether.

The gamble gets worse. CNBC reported on March 9 that OpenAI, Oracle's biggest customer for all of this, is already looking at newer, faster chips from Nvidia. Oracle ordered the current generation and spent billions building out a massive Texas facility. OpenAI may not fully expand into it. The chips improve faster than the buildings go up.

Larry Ellison, Oracle's founder, owns 41% of the company. In September 2025, Oracle's stock hit $346, and Ellison briefly became the richest person alive at $393 billion. Today, the stock sits around $146. His fortune has dropped to roughly $201 billion in six months.

Oracle is spending borrowed money to build data centers that could be outdated before they're finished, for a customer already shopping for newer equipment. 30,000 people woke up to a 6 AM email because that's what it costs to fund a $156 billion bet when your lenders are running out of patience.

Oracle laid off between 20,000 and 30,000 employees Tuesday morning, roughly 18% of its global workforce, via a single email sent at 6am EST with no prior warning. System access was revoked almost immediately after. The cuts are expected to free up $8-10 billion in cash flow. Oracle’s stock has lost more than half its value since September 2025 and the company now carries over $124 billion in debt, up from $89 billion a year ago, with free cash flow running negative $10 billion last quarter.

My Take

Oracle posted a 95% jump in net income last quarter and still eliminated 18% of its workforce by email before most people finished their morning coffee. This is not a company in distress in the traditional sense. It’s a company that made an enormous debt-funded bet on AI infrastructure and is now converting its workforce into cash flow to service that debt.

We’ve covered Oracle’s AI gamble for months. The $300 billion OpenAI deal through Stargate, $50 billion in capital expenditure this fiscal year, over $124 billion in total debt. Multiple US banks have pulled back from financing Oracle-linked data center projects. Bondholders have sued Oracle claiming it concealed how much additional debt the OpenAI deal would require. The credit default swap spread hit a three-year high earlier this year, meaning debt investors are genuinely nervous about getting paid back.

The workers who got that 6am email built the products Oracle has monetized for decades. The bet that eliminated their jobs was made by people who were already paid regardless of how it turns out. That is the part of the AI infrastructure race that doesn’t show up in the capex announcements.

I always wonder who the counterparty is on these…

Headline o’ the Day (Wednesday)

A couple good podcasts:

BCA’s Iran Conflict Daily Dashboard

All of those countries that can’t get jet fuel because of the Strait of Hormuz, like the United Kingdom, which refused to get involved in the decapitation of Iran, I have a suggestion for you: Number 1, buy from the U.S., we have plenty, and Number 2, build up some delayed courage, go to the Strait, and just TAKE IT. You’ll have to start learning how to fight for yourself, the U.S.A. won’t be there to help you anymore, just like you weren’t there for us. Iran has been, essentially, decimated. The hard part is done. Go get your own oil! President DJT

"We need demand destruction." - Jeff Currie, CNBC, 3/30/26

“Be careful what you wish for in this world, for if you wish hard enough you are sure to get it.”

We’ve seen these benchmark crude prices before. We’ve never seen these product prices before.

Gasoil1 in Asia (Singapore-FOB) is trading above $250/b, up 3.3x where we started this year.

At the peak in 2022 ~ $185/b

At its highest in 2011-14 ($100+ crude) - it traded ~$144/b- Karim Fawaz, Director - Energy Advisory @ S&P Global.

I've stopped reading Gulf war headlines. Here's what I track instead.

We run an India-focused equity fund. 85% of India's crude comes from imports. Half of that normally passes through Hormuz. So yes — this crisis is personal.

But the information environment right now is garbage. Trump says the war ends tomorrow. Iran says Hormuz is shut forever. One analyst says $150 oil, another says $60. You can't build a portfolio view on this.

So I've narrowed it down to 4 signals. These are priced by people with real money on the line. They don't lie.

1. Ship insurance premiums through Hormuz

This is the single best signal. Lloyd's underwriters have billions at stake on every pricing call. Before the war, insuring a tanker through Hormuz cost 0.25% of the ship's value. Today it's 3.5–10% — and almost nobody is buying. A $100M tanker that cost $250K to insure now costs up to $10M. When this drops below 2%, the people with the most to lose are telling you it's getting safer. No press conference can replicate that.

2. How many ships are actually crossing

Every ship carries a GPS tracker (AIS). You can count exactly how many cross Hormuz each day. Before: 100+. Now: 8. That's a 92% collapse. You can't spin a ship being somewhere it isn't. Iran is letting some Chinese and Indian ships through, but it's a trickle. When this number crosses 30–40, trade is resuming. You can track this free on the WTO Hormuz Trade Tracker.

3. Paper oil vs real oil

This one most people miss entirely. Brent crude (the headline price) is at $112. But Dubai physical — what Asian buyers actually pay for delivered oil — is at $126. That's a $14 gap. It exists because Trump's comments keep pushing paper prices down. Traders call it jawboning. But the refiners buying cargo aren't getting any discount. If you're looking at Brent to assess India's oil bill, you're looking at the wrong number.

4. The mid-April cliff

Multiple emergency measures expire around the same time. The 400 million barrel SPR release runs dry ~April 15. The US waiver letting India buy Russian crude expires. Formosa Plastics has declared force majeure from April 1. Right now these stopgaps are keeping the supply gap at ~5 mb/d. Without them, BCA Research estimates it doubles to 10 mb/d — the largest crude disruption ever. If Hormuz doesn't reopen by mid-April, we're in uncharted territory.

Bottom line: track the insurance premium, the ship count, the paper-physical spread, and the April timeline. Everything else is noise.

"The mainstream narrative should therefore be reversed: the stock market did not collapse (in March 2020) because lockdowns had to be imposed; rather, lockdowns had to be imposed because financial markets were collapsing."

Fabio Vighi, 2021

Energy Lockdown : War, Oil, and the Coming Financial Reset

The conditions for another global systemic emergency are being engineered into place. The latest escalation in the Middle East began with an Israeli strike on Iranian energy infrastructure carried out with the strategic backing of the United States – an attack that violates fundamental principles of international law on the targeting of civilian infrastructure…

By striking directly at the physical foundations of the global energy system, the operation has caused a shock whose consequences extend far beyond the battlefield. The violence of war and the resulting oil crisis are already triggering a macro-financial tsunami that clears the path for what increasingly appears as an attempt to reset the debt-based system, while intensifying a dog-eat-dog competition among drowning geopolitical actors. A crisis of this magnitude functions as a moment of heavily manipulated transition – a criminal act cloaked in market logic – attempting to sweep away the current financial dysfunction while preparing the institutional foundations of the next iteration. Those who are better positioned stand to gain from it – at least in the short term – while others will bear the consequences…

During the Covid emergency, large-scale monetary intervention began even before lockdowns were implemented. In September 2019, the US repo market crisis forced the Federal Reserve to inject massive liquidity through daily auctions. When the “pandemic” arrived months later, the emergency provided political justification for expanding those interventions dramatically. The crisis did not cause the intervention – the intervention was already primed, and the crisis provided the cover. Energy shocks can play a similar role. By destabilizing debt and equity markets, and threatening recession, they create the conditions under which large monetary responses become both politically acceptable and economically unavoidable. As with Covid, this is not merely crisis management – it is another case of crisis deployment…

One of the clearest signals of how quickly this crisis could reshape policy comes from recent recommendations by the International Energy Agency. In response to escalating supply risks, the agency has proposed measures that would have been familiar during the Covid lockdowns: working from home where possible, cutting highway speed limits, limiting air travel, increasing car-sharing, and restricting car access in major cities. The justification is energy security rather than public health, yet the logic is strikingly similar to pandemic-era policies. Faced with a shock to the energy system, authorities may again be turning to behavioural constraints on mobility and consumption as tools of macroeconomic control. In fact, a pandemic-without-virus logic is already being operationalised.

John Dizard: Watch for Rationing of Oil, Gas & By-Products “Unless there's some miracle within the next few days, we're heading towards diesel rationing in Europe, jet fuel rationing, serious shortages. And, also, lower fertilizer application this year, which means lower food production next year. But it's the fuel products, I think, that are going to cause the most immediate severe shortages.”

“Everybody use cash. I can’t tell you what a huge difference it would make. It would be wonderful. So use cash.”

Trump to take first steps in opening retirement funds to private markets

The Trump administration on Monday made its first step in opening the more than $10tn US retirement marketplace to complex and illiquid private markets deals such as corporate takeovers and direct loans…it would offer administrators of retirement plans like large asset managers a “process-based safe harbour” when selecting alternative investment options for ordinary savers so long as they considered six factors to safeguard investors.

The new rule could help open savings plans to private equity deals and private credit loans. These plans, which currently manage more than $10tn in assets, have almost no exposure to unlisted assets and instead are composed mostly of publicly traded bond funds, mutual funds and broad index funds. While there has been no explicit rule against offering private investments in such investment accounts, managers of 401k plans have been reluctant to do so out of fear of being sued.

The safe harbour proposed by the DoL could defray some of these litigation fears, accelerating the push of private assets into the savings of millions of ordinary Americans.

"If it's such a great trade, why are you offering it to me?"

Leyla Kunimoto, founder of Accredited Investor Insights

Jack: “What are you more worried about? Private credit or private equity?

Leyla: “Private equity by far.”

Banker Next Door (Joe Bergquist)

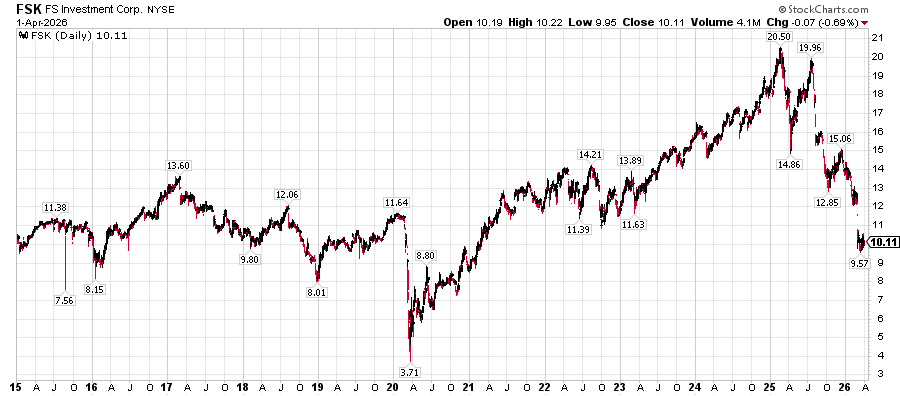

Moody’s “lowered the debt rating of FS KKR Capital Corp one notch to BA1 from BAA3, pushing it into junk territory. Moody said the fund’s underlying asset quality had worsened more than its peers. Nonaccrual loans, meaning loans that borrowers have stopped making payments on, climbed to 5 and a half % of total investments at the end of 2025, one of the highest rates among rated business development companies according…5.5% is astronomical. That is a ridiculously high number. Ridiculously high number. That basically puts them in financial jeopardy. And that’s why Moody’s is downgrading it to junk.”

Bergquist then quotes this passage, from Greg Hertrich, managing director and head of US Depository Strategies at Nomura:

Hertrich argued in the latest Street Talk podcast that banks’ exposure to nondepository financial institutions is not a time bomb waiting to be discovered. He noted that bank managers and their regulators have paid close attention to the growth in those portfolios, which accounted for close to half of the growth in the banking industry’s loan growth in 2025. Hertrich further noted that bank loan portfolios are backed by much stronger capital and higher levels of reserves, and institutions operate with lower loan-to-values and meaningfully different credit culture than in prior stress cycles.

“How concerned am I about it? I don’t think that it would rise to a top three.

Bergquist’s response:

“If anybody wanted to go back and look at my private credit discussion from last week, I talked about the exposure of private credit. I talked about how it is concentrated in the largest banks. Not much of a private credit exposure to community banks, but the top 10, top 15, top 20 banks in the United States all have significant exposure to private credit. So, if that blows up, that’s a problem. That’s a bailout city right there. That is bailout city. Tell the Fed to turn the printing presses back on, because the big banks are going to need a bailout. That’s what’s going to happen. So, again, I mean, to sit there and say that this wouldn’t even rise to my top three in terms of things I’m looking at, that’s just crazy to me.”

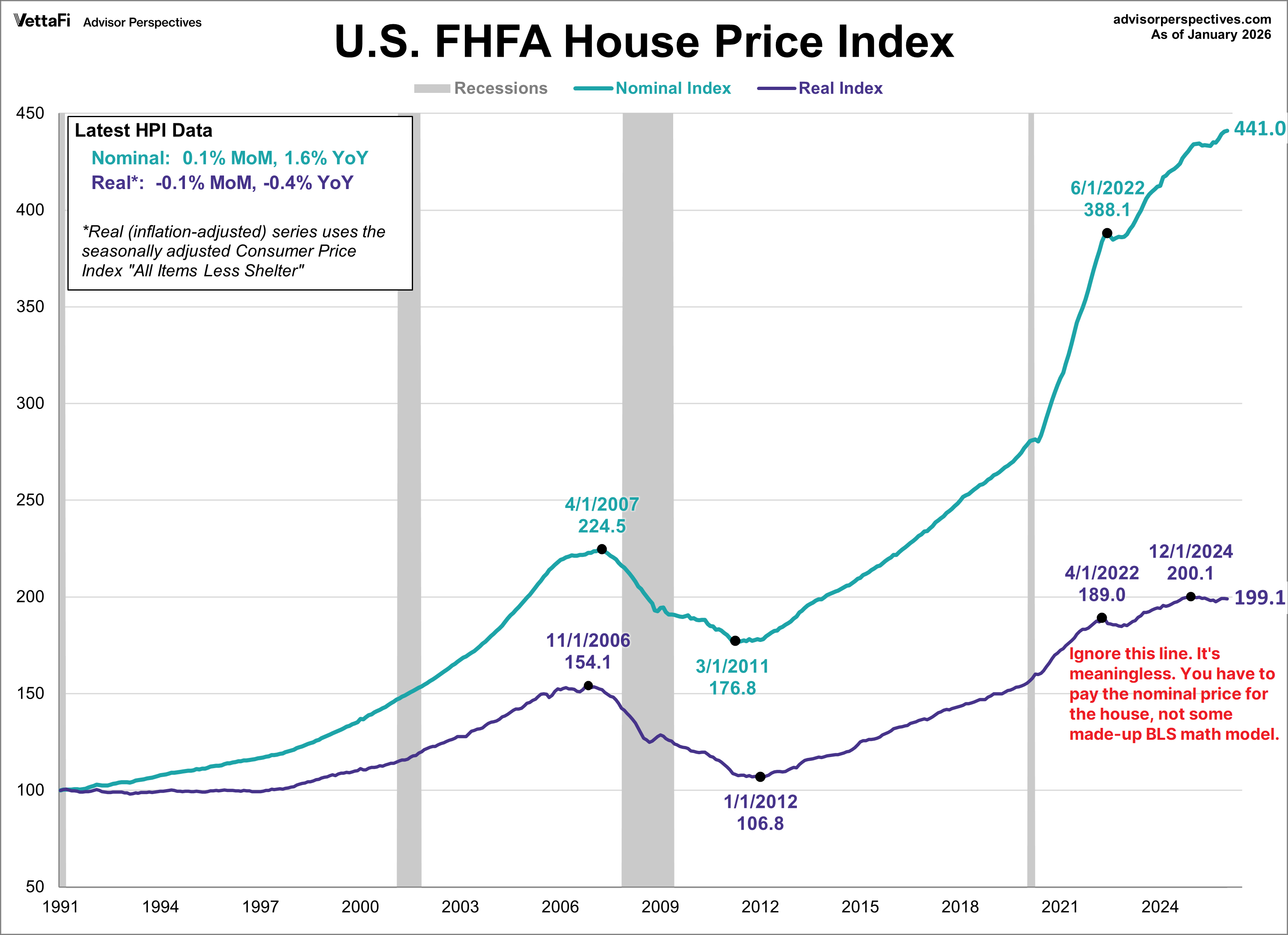

FHFA House Price Index Reaches Record High in January

Walmart vs Global Luxury Retailers

“Gasoil, or "red diesel," is a red-dyed, lower-taxed diesel fuel primarily used for off-road vehicles (agricultural, construction, marine) and heating.”

Another good one Rudy. Who needs the WSJ? I get the real financial news from Rudy!

This war on Iran, together with reading history largely written before the 1950s, has led me to the very isolating opinion that the West has not been "the good guys" for at least 100-years.