“Banks don’t go out of business taking risk, they go out of business levering the things that they’re told aren’t risky.”

If you missed my discussion on December 1 with Demetri Kofinas, here’s the first hour. I will post the second hour for paid subscribers when Demetri gives the ok (Hiddenforces is a part-subscription podcast).

The CBOE Volatility Index (VIX), which measures anticipated 30-day volatility across options tied to the S&P 500, settled at 12.07 on Tuesday for its lowest close since fall 2019 [when the Fed restarted QE after rates spiked - rh] and marked its 19th consecutive session south of 14 today (the gauge’s average reading over the past three decades stands near 20). That preternatural calm marks a striking contrast with last year’s experience, as realized S&P volatility registered at its sixth-highest annual clip going back to the Great Depression, analysts at Bloomberg find.

The shrunken VIX “point[s] to a degree of over-confidence” in the market, strategists at UBS write, as market expectations of several rate cuts alongside brisk earnings growth in 2024 leaves limited room for error. “Economic data will need to walk a fine line in the coming months to sustain the recent rally. . . equity markets are already pricing in plenty of good news. As a result, we expect a return to more normal levels of volatility.”

I’ll just note that this headline is during a period universally hailed as “the greatest economy in the history of the universe,” (and also because I can’t stand Gavin Newsom). Also, states can’t print money like the Feds: California Has a $68 Billion Budget Deficit With Only $30 Billion in Reserves

More Dave Dredge with Grant Williams:

When interest rates fall, they fall really fast. When they go up, it’s a grind. My explanation, that’s pretty simple. Most of the guys who are short bonds are on mark to market accounting. The guys that are long all the bonds don’t mark them to market. It’s hard to squeeze them out of their position. Takes a really long time for Bank of America to make the hard decision to start reducing that exposure. And I don’t mean to pick on Bank of America, they’re just the one who announced the shittiest numbers.

My argument is they want the recession. We talked about it a year ago, that they will keep the yield curves as inverted as they possibly can to convince people the recession is nigh, and keep people from selling off the backend. We saw finally, amazing, I listened to it earlier, yesterday, we talked last year that the pain, the thing that would trigger the real pain was a bear steepener. September, October was the ultimate pain, and the whole narrative shifted. And Janet Yellen came out and reduced her backend issuance because of the pressure from the treasury borrowing advisory committee, which I wrote about, which is the only place other than my babbling, the treasury borrowing advisory committee made up of the biggest dealers, buyers of treasuries, told Janet the same thing. “We can’t buy anymore. We’re full, stop it.” Now funny, they never write that in their sell side research, but when they’re trying to influence her issuance, they laid out the pictures of the great stop loss.

There’s the picture of how much banks are reducing their bond holdings quarter, after quarter, after quarter as opposed to, obviously haven’t been other than central banks, the biggest buyers because zero risk weighted assets, maximum leverage, hold to maturity, no accounting, accrual accounting. Riskless. I mean, literally from an accounting perspective, riskless. And you could pay yourself bonuses on the accrual interest against the financial repression of depositors forced to accept zero on deposits. And now they’ve been reducing, as we all know, the relative scale of foreign reserve managers has been declining on a relative basis. And so, I think exactly what you said, I think the recession is the good outcome because it gets people to buy the bonds. And if that good outcome includes declining other asset markets, equity markets, well that’s a loss into the end capital owner that’s acceptable. If it’s a loss recognition, a forced great stop loss, a forced recognition of the losses in fixed income, well, it wipes out the banking system. It destroys pension funds. That’s systemic. The systemic risk is there.

Harley Bassman: “Let me say this clearly for the record: Do not be distracted by bright shiny objects such as economic numbers. The FED will not be cutting rates anytime soon without a COVID style catastrophe.”

Tell me more about the disinflation…

“Core CPI” has now been above the Fed’s made-up 2% target for two-years and five-months.

Obligatory Jim Grant article: “The Fed watcher who called the 2007 housing bubble expects interest rates to stay high for ‘much, much, much longer.’ It’s payback for the unsustainable ‘free money era’”

Jim Grant has been tracking the ins and outs of Federal Reserve policy and its effects on the economy and markets in his famed newsletter, Grant’s Interest Rate Observer, for over 40 years…

“We’ve never seen anything like this level of total debt and leverage in the system. It’s an experiment,” he warned. “But we know that credit bubbles have to pop. We don’t know when, but we know they have to.”

…“It is the historical track record, it is the pattern, that interest rates exhibit a tendency to trend over generation-long intervals,” Grant explained, arguing we may have entered a “new regime.” “We seem to have hit some major point of demarcation with interest rates in 2020 and ‘21,” he added. Based on history, he said, this new regime should last 40 years. Still, Grant clarified that the generation-long uptick likely won’t be a straight line up. If a recession hits, there could be a “substantial,” although temporary, pullback in interest rates.

If Grant is right, that would mean an era of low economic growth, relatively high inflation, and high interest rates—an economic combination that’s often labeled stagflation—may lie ahead. And that’s not exactly a recipe for investing success. It could even be an environment where corporate defaults rise, with the credit markets paying the overdue price of the free-money era.

Sounds familiar: "It is hard to imagine any time in history when such rampant pessimism about the economy has existed with so little evidence of serious trouble."

“The problem is that by forcing prices into unnatural places for too long the manipulators interfere with this thing we call reality.”

Felix Zulauf

“Many of those numbers are not really true - look at inflation. If there is anybody who believes that inflation is what they publish, you know, you cannot be serious. Of course inflation is another number. My inflation is probably 10% of my basket of goods and services I consume, and so it is for many other people, so I think the numbers are made up, you know. The shelter part of the CPI is a problem, and it is exaggerated on the downside, and recently they exchanged what was it health care insurance premiums for healthcare insurance profits of those companies - I mean, it's it's ridiculous. So I think inflation is in fact higher, and that would mean that a higher and higher percentage of the US consumer is struggling, is struggling more than what the statistics tell us, and credit card delinquencies are probably pointing in that direction.”

“I once asked the head of major Central Bank why they publish inflation rates that are not true, you know, because they are just not true, and he said, well, you say it's not true, but we have to operate with the statistics they give us, and I said, but it's not true, everybody can tell you it's not true, and he said my wife tells me the same thing when she goes shopping, so they know, but they have no other tool to work with.”

“I recently listened to Niall Ferguson, the famous historian, and I was amazed he gave a talk to a small group in Zurich. I attended, and I knew his opinion from six months before, and when he spoke, he was about as as bearish on geopolitics as I was, so he was almost giving my speech, and I asked him what about diplomacy? This setup that we are in in the world should really call for high-caliber diplomats to solve the problems, and he said there aren't any, and and I agree with him. There aren't any. Therefore the risk of military conflict is much higher than people assume.”

Something to think about:

“China doesn't want to rule the world. China doesn't need to intervene in other governments, they never interfere in domestic policies - the U.S. does, and that's the difference, and that's why many parts of the world have turned away from the U.S. towards China.” - Zulauf (who is Swiss)

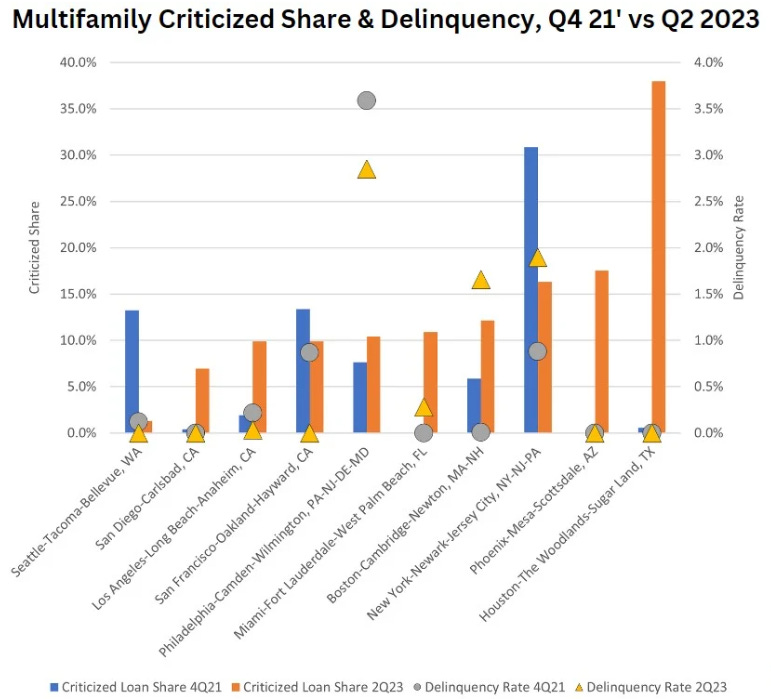

Multifamily

TREPP: A Risk Assessment of the Multifamily Market: Through the Lens of Bank CRE Loans

As part of the data collection and anonymization process for Trepp's Anonymized Loan-Level Repository (T-ALLR) data set, Trepp translates contributors’ internal risk ratings to a standardized risk rating that ranges from 1 to 9. A risk score of one indicates the lowest probability of default, a risk rating score that is above six is considered a “criticized loan,” and the highest risk score of nine means that the loan is in default.

We are seeing two stories play out across U.S. geographies. Some markets were hit hard by the pandemic and are starting to show glimpses of strong fundamentals in favor of rental growth.

Other multifamily markets proved to be hotspots of strong rental demand when the rest of the nation was more strongly impacted in 2020 and 2021 but are displaying soft spots now. This weakness is coming from a combination of supply-and-demand imbalance putting downward pressure on rent growth, higher expenses putting strain on property owners’ bottom lines, higher-for-longer interest rates becoming a concern for loan maturities, and anticipated economic recession.

As of Q2 2023, more than 30% of multifamily debt is held by banks.

CRE Podcasts

I know I tend to be a glass half-empty guy, at least on markets, but I know long-term I’d rather be in real estate than, say, bonds, so this period too shall pass (Jay has a printing press after all…)

However, that doesn’t mean that we won’t on occasion have grey swans (e.g., office and work from home, national or statewide rent-control, etc.), and there can be extended periods where prices go nowhere, or drop.

Most real estate podcasts are super-promotional, ‘get rich with no money down’ stuff, audio TikTok, NAR promos etc., but a few are more sober.

Apartment Trends with Chief Economist Jay Parsons at RealPage Particularly useful if you’re interested in Texas. Count the number of times they say, “...assuming rates drop.”

2024 Self Storage Investing & State of the Market with John Lindsey

Treppwire: “Lending & Leases & CRE Sales (Oh My!) But Still Plenty of CRE Bears” If you want the most bullish take possible on CRE, you can always count on Trepp (still a very good source of info.) I quietly bookmarked their episode #96 in August 2021 as the peak of CRE. Of course, that and 50 cents(?) might get me a phone call, if I could find a pay phone.

Other Podcasts

Value After Hours S05 E 45: Forensic analysis with Stephen Clapham on BABA, TSLA, LVMH and RACE. Also wine. I like the whole bunch here: Tobias, Jake & Stephen.

How Can We Make Sense of the UAP Conspiracy? | Diana Pasulka

I just finished listening a great podcast with Mike Taylor and Mike Green, where I took so many notes I’m going to save that one for my next missive. Sorry.

New Car Inventories

“There are around 2.5 million vehicles just sitting on dealer lots right now, according to data from Cox Automotive…You can color me absolutely shocked that new cars, as unaffordable as ever, aren’t selling quickly right now. I just cannot believe that in a time where everything costs a lot more than it used to, new car sales are being hurt.”

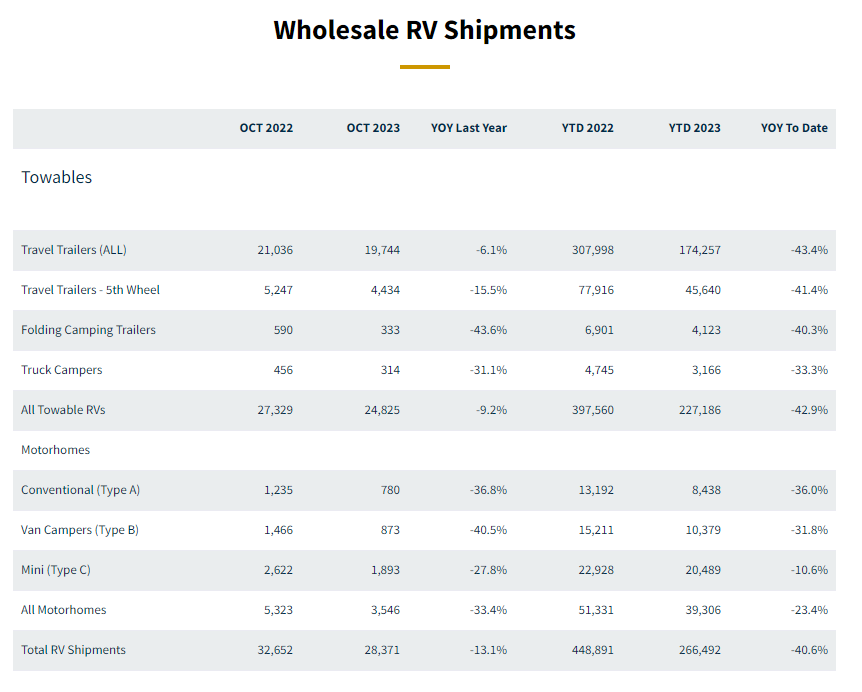

RV Shipments

I saw the above chart, which is pretty interesting, but I couldn’t find the original source, so I went looking elsewhere and found this at the RV Industry Association website:

Those are some pretty huge declines over 2022. I’m sure rising rates had a lot to do with it, and the Covid YOLO mentality.

For what it’s worth, here are Some random unedited comments:

I was R.V. Technician for 10 years up until December of 07, we started seeing huge slump in sales and well we all know what happened in 08! Btw recession was so bad for the rv industry i had to start a new career and never went back

Yeah this graph brought me back. My family owned a used RV business… had to sell around 09, because we had three straight years where we didn’t sell so much as a pop up trailer! Sigh. We never went back into the biz.

Im here in Central Florida specifically Tampa (born and raised) watched alot R.V. places crumble and one the biggest (Lazy Days) which i worked for right before everything went to shit, layed off hundreds of technicians, service writers, salesman, etc. etc.

I just drove up to orlando to buy a cheap beach baby stroller. There's a stretch of RV sales lots between Tampa and Orlando just filled with these things. One of them had units parked off lot down a service road street.

A slump in RV sales has long been considered an early warning sign of a broader economic downturn, this is now the 2nd worst downturn since sales have been tracked only surpassed by the slump in 73.

I've seen that data. Yes, inventory has grown, and they are well aware of it. Yet, denial that prices have gotten too high, citing high interest rates as the culprit. They don't think that, just possibly, the consumer is getting close to tapped out. Couldn't possibly be that now, could it? Sounds similar to the story behind real estate. Blame the rates, not the prices.

This bunch of folks got really entitled, quickly, during the pandemania, shop till you drop era of late 2020-2022. Reality is either going to wake them up, or they will scream and kick until the free money spigot is turned back on.

People shop big ticket things, houses, cars, RV's, boats, based on monthly payment. That's why interest rates matter in the first place. Trouble is, when the price of X outstrips what the consumer can and will pay, any upward pressure on interest rates is going to kill the demand. We simply can not go forward with the idea that 0% is all we will tolerate in financing things.

A generation of money printing is going to cause a huge hangover. We as a country shouldn't have mixed tequila, wine, and beer. Bad America.

Regardless of whether or not you think this RV data means anything, or it just part of the “doomzer agenda,” I often find the comments of random people on public forums to often be far more interesting anything on CNBC, Bloomberg or in the WSJ.

“The percentage of companies with strong/healthy Altman Z-scores (which combine account profitability, leverage, liquidity, solvency, activity ratios, etc. to measure bankruptcy risk) has dropped below 10% for first time on record”

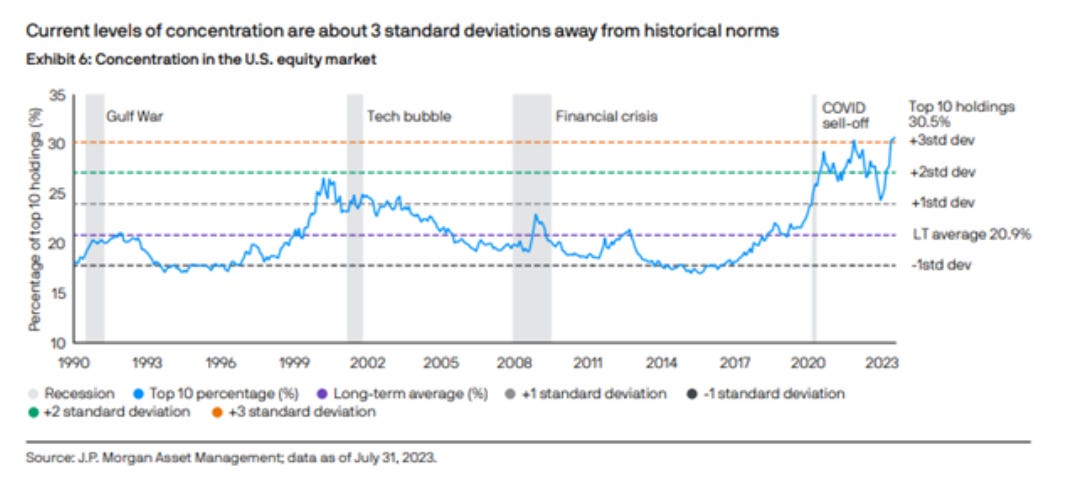

I don’t have a link to this JPM chart below, but check this out - the top 10 holdings “in the U.S. equity market” comprise 30.5% of its value (as of July 31)?! I guess price-insensitive (i.e., passive) flows can do that.

Berkshire Hathaway is constantly attacked by the so-called “ESG” movement, with vacuous shareholder initiatives presented at every annual meeting. I have to wonder whether these activists have even read BHE’s presentations and other disclosures.

I suspect that many activists do not really care so much about actual progress on decarbonization. They are more focused on using climate change as a political cudgel to attack capitalism.

Meb Faber, tell us how you feel about CALPERS?

A recent analysis of home values in Dallas found that no neighborhoods lost value over the last five years, which is pricing out potential homebuyers who earn the city’s median income of $58,200. The most new housing construction in Dallas are single-family homes that sell for a median of $1.4 million.

I understand new homes are always ‘expensive’ to most, but 25x median income? It wasn’t always this way. We need more ZIRP, inflation and Fed MBS monetization!

The Fed's probably-illegal1 MBS holdings have fallen $293 billion over 19 months, about $15.4 billion a month. At this rate, the Fed will get back to their 2008 MBS levels of $0 sometime around the year 2036. We're all very proud of the QT, especially realtors.

I was listening to one of the too few realistic realtors and he made the point that what the higher rates are doing is forcing buyers to actually look at the ridiculous prices. I found this to be a very good podcast by the way.

I keep hearing “FHA is the new subprime” - it’s ok though, because Uncle Joe is bailing them all out with new programs. Also, Todd Sachs makes a good case against being a residential landlord today, at least in places like New York. It’s long and rambling, like a lot of the podcasts I mention, so maybe wait until you’re on a long drive or walk. He seems to be Maryland-based, so your mileage may vary. (Here’s another informative one from this guy, with a real estate attorney and title company owner.)

Electric Trucks?

A different topic, but in the podcast I mention above they have a few listener call-ins, including this excerpt from a trucker:

Sachs: What do you think about it having an electric truck?

Trucker: No, no, I would never own an electric truck. I don't even want an electric car, that's why I just bought myself a V8, well it's a 2008 V8, so it's not like I spent that much on it.

Sachs: I can't even imagine the power that's required to, you know, how many pounds do you haul in a a big truck?

Trucker: So the requirement is you can't hold haul anything heavier than 80,000 pounds all together for the truck weight, the trailer weight and everything in it, so probably you can't really go over like 47,000, and trailer weight, and already the EV batteries - I was talking to a Walmart driver that was driving a hydrogen truck, and I'm like I hope that doesn't blow up on you, and then he said that for the hydrogen truck, I think it's the hydrogen truck, it's also for the EV’s, that there's been that's an extra 5,000 pounds, and already companies have got the big companies have gotten waivers to haul up to 85,000 lbs all together with the battery, and these batteries don't last all day.

We have two electric trucks in Southgate, L.A. - I don't work out of LA, but I do load to and from L.A., and they have only have four of them. They keep two in the charger, and then whoever is using electric trucks that day will probably have to swap out midday and then grab the other two trucks, put those trucks back on the charger, and then go either finish their routes or whatever, so I'm assuming they only last for like 6 to 8 hours, and I myself work like 13 hour a day, so that's never going to work for me.

Small Business

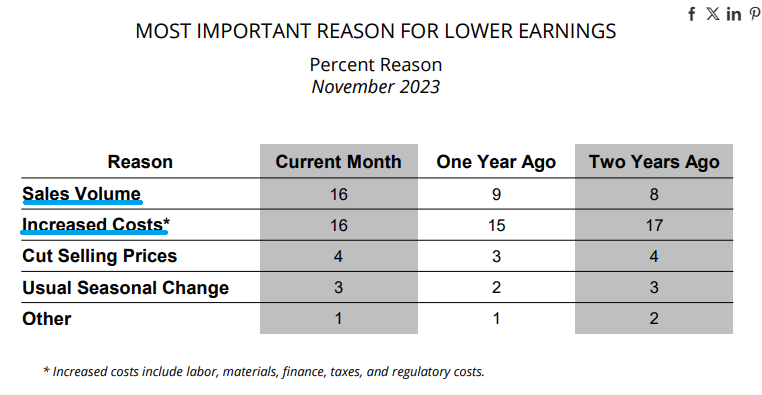

Sales volumes are hurting, which I’d guess is largely due to price increases. e.g., I don’t buy diet coke any more unless it’s so on sale that it’s not that much higher than the price of a few years ago. As for “increased costs,” that’s been a problem for ages.

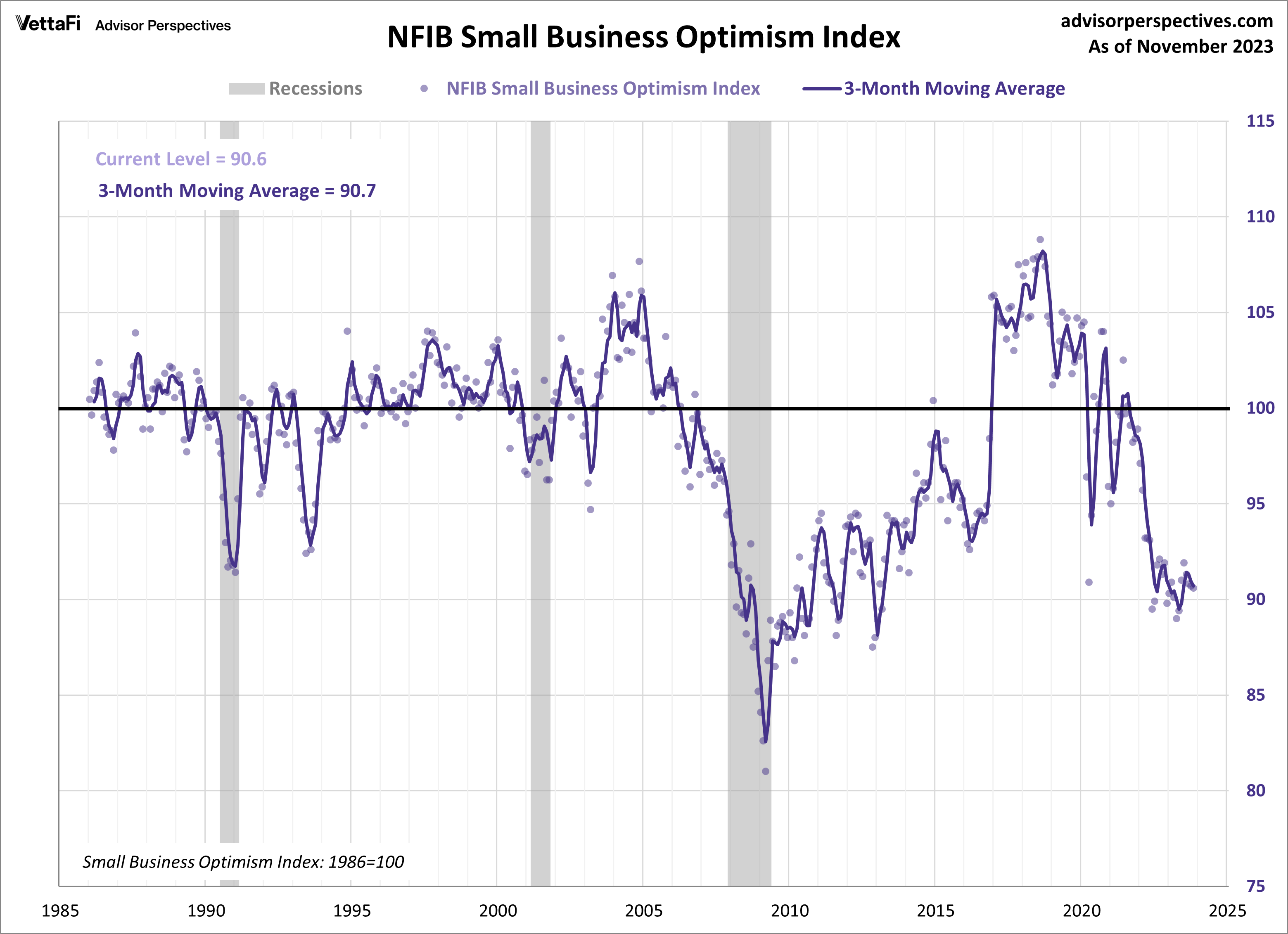

The headline number for the NFIB Small Business Optimism Index fell to 90.6 in November, as small business owners remained pessimistic about future business conditions. The latest reading was better than the forecast of 90.7 and marked the 23rd straight month the index has been below the series average of 98.1. The index is at the 9th percentile in this series.

Uncle Sam's #1 financial asset is student loans, a relatively new phenomenon. Easy taxpayer-backed money led to an explosion in loans, and allowed colleges and universities to bloat and price-gouge.

When Biden "cancels" a student loan, all that means is that the taxpayers like you and I pay for someone’s gender-studies degree. That's just a fact, don't get mad at me.

Why should taxpayers back student loans at any of these institutions?

The Cantillon Effect

An interesting book review.

The Missing Billionaires by Victor Haghani and James White asks a simple question. Given the incredibly large fortunes in history, why are there so few families with inherited multi-generational wealth on the Forbes 400? They cite the example of Cornelius Vanderbilt, who died as the world’s richest man in 1877, leaving everything to his heirs with no estate taxes.

Following the Vanderbilt family tree, the authors note that if the family fortune were managed according to now-well-known wealth management principles — diversification and risk management — this wealth would have grown faster than the Vanderbilt family, at least so far (and especially with smaller modern family sizes), and we should see dozens of Vanderbilt billionaires on the Forbes 400 today. In reality, the Vanderbilt fortune was dissipated by the 1960s.

I particularly enjoyed this part about asset-gatherers:

What’s clear from the experiment is that most wealth management professionals, like most other professionals, are careerists with low levels of intellectual curiosity compared to chain-smoking blackjack card counters. They’re smart enough to input a few parameters for “financial planning” software that spits out pretty reports. Since most of their clients are highly irrational, the main way they earn their fees is by keeping clients from doing really dumb things like selling at the bottom or going all-in at the top. They operate according to semi-reasonable rules of thumb concerning asset allocation (100 minus your age for stocks/bonds) and retirement consumption (the 4% rule).

Lou: We had a guy on the boat, liked to smoke cigars for breakfast. Picked up the habit from his granddad, he said. This was on the Bo De river, seventy...four.

So I'm on the wheel. This kid comes out. 'Cause what could he have been? 19? Lights his shit stick, and then...Never even saw it coming. Shot him right through the cigar. A one-in-a-million shot. And the look on his face when he fell - just like the cook. Bafflement…

War stories.

Hank : [laughing] Different now, though. After WWII, we went six years without a-- without a murder here. Six years. And these days, well...Sometimes wonder if you boys didn't bring that war home with ya.

“If America's soul becomes totally poisoned, part of the autopsy must read: Vietnam.”

Martin Luther King, April 4, 1967

…when the reparations bill in the May 1921 London ultimatum was accepted, the exchange value of the mark began to fall again, at first slowly, then beginning in October with increasing rapidity. By December, the exchange rate was 217 to one against the dollar. At the same time, German unemployment was at 1.6 percent. In his New Year’s editorial, Georg Bernhard of the Vossische Zeitung wrote, “It’s become a slogan in Germany that inflation has to be reduced.” Yet no one had seriously tackled the task, for reasons that were universally known:

“Inflation is a gigantic swindle that dangles pleasing images before people’s eyes. All the economic activities, the rises in prices and wages may actually entail a below-value sellout, an inundation of the masses as consumers, and an underpayment of all working people as producers. But because the sums to which the old ideas cling are rising, people are slow to notice, or don’t notice at all, and because everyone who wants to work finds a job and a wage, the positive employment figures increase the smoke and fog that surrounds us.”

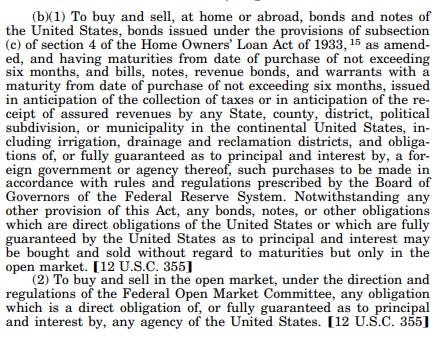

“What is the legal basis for the agency MBS purchase program?

Purchases of agency MBS in the open market, under the direction of the FOMC, are permitted under section 14(b) of the Federal Reserve Act.“

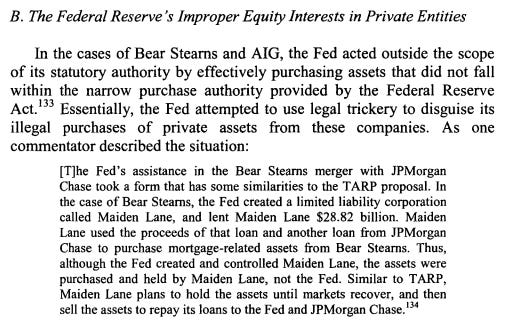

There is this paper from 2010:

Rudy, You must spend all day, 7 days a week, listening to podcasts and reading reports, and then distilling the most compelling material for your readers. And you do it better than many readers, including me, can do it for themselves. I, for example, am a lifetime subscriber to both Jim Grant and Grant Williams, and you posted material from them that I had missed. Very valuable! jpm

I get the stock market, they don't take Powell or the Fed seriously. They know that Powell is weak and will cave in to the political pressure to accommodate during an election year. What I don't get is bonds. Who could possibly trust these clowns? They've demonstrated over and over that they have no clue what they're doing, and the first hint of economic pain you know they'll reflate like crazy. Baffling.