Chancellor and Hunt

Financial Oppression

Gee, how did legacy media get so discredited?

Most ‘reporters’ seem to hate normal people…

They HATE you!!

"Mass delusions are not rare."

Garet Garrett, 1931

Today I highlight a couple new interviews with two favorites, Edward Chancellor and Lacy Hunt, plus a few other eclectic items as usual.

I am on day 4 of a nice long weekend with friends, and hope I don’t mess up, since I’m doing this on my phone and not a desktop as usual…

Edward Chancellor

Chancellor is one of a small group of perceptive market historians, along the lines of Jim Grant, Jeremy Grantham, Howard Marks, and others who have a memory and an understanding of the broad swath of history, and how we keep, as Grant says, stepping on the same rake.

Some highlights:

“The Central bankers and monetary policy makers don't tend to consider consider the distributional consequences of their actions, and it's pretty clear that if you take interest rates down to very low levels, you will boost asset prices, which benefits those who already own assets, and you will make it harder for people who don't have assets to acquire them, to save. And if you lower the returns on savings, it would take longer to acquire wealth. If you throw into the mix the fact, as I argue, that the very low interest rates distort the allocation of capital, lower productivity growth, and therefore lower income growth, you can see that the ultra low rates were very damaging to the less well off.”

“If you remember that central banks justified their ultra-low rates - the zero rates, the negative rates - on the grounds that they were fighting deflation, but actually, deflation or falling prices benefits the working family, and actually it's not so good for corporations, so the battle against deflation really could be seen as a battle against working people in favor of corporations. So, again, it doesn't come as a huge surprise that this last decade was one of very low income growth, but very bloated profits. Now none of the this is comprehended by Central bankers, because their model doesn't have a representative investor. It has a single investor to account for an entire society, so there are no distributional consequences to the model, and the central bankers get very shirty1 when asked about this. They always reply, oh well, these are issues for the politicians to deal with, not for us, so they'd like to take credit when things go well, if inflation is low, if the economy is recovering, if the financial crisis comes to an end, you pat your central bankers on the head and say, you know, what a good boy you've been. If things go badly, the central bankers say, well, don't blame us - these are political issues to be discussed, to be dealt with by your politicians - so they have their cake and eat it too…”

“The more we've interfered with the rates, the lower interest rate, economic productivity growth has fallen, and then again, as you know, you have these extraordinary persistent imbalances in the financial system, massively inflated asset prices, huge amounts of debt, and an unknowable quantum of financial instability in the system. So yes, I think that we need to get back to market rates if you will - market rates, or genuine natural rates. I think it probably is impossible to get to an ideal position under our current monetary system. I think a fiat money system in which central banks are free to create money out of thin air, in which commercial banks can create money through their active lending - that type of system is always going to require a committee of people with PhD’s sitting there trying to determine what the market rate would be. You would have to change the monetary system to get to, if you will, a proper market rate of interest, but even under the current system I think you could do a lot better job, and not least by never having your policy rates below - I mean, they should never really be below 2%, I would have thought.”

“Very low rates encouraged an extraordinary government profligacy.”

“If you take interest rates very low, the government has an incentive to push up debt very high. Once debt is very high, and interest rates return to more normal levels, the debt becomes unsupportable, and instead of defaulting, you go through the process of inflating the debt away, or what's called financial oppression.”

“I actually quite like energy stocks. and I didn't even mind the commodity stocks, you know, not withstanding China's overhang. I think that you move from an era of financial wealth to, if you will, things of real value ,and that does push one more towards commodities, towards gold, towards hydrocarbon energy.”

Lacy Hunt

Lacy Hunt, who I often call “my favorite deflationist,” is one of the few central-bank types (he did work at the Dallas Fed decades ago after all) who seem to understand the immense damage that our unelected apparatchiks have to the country, along the lines of William White and even post-Bank of England Mervyn King.

TL;DR:

Kofinas: First of all, when you look across the global economy today, what is your assessment of how it's doing?

Hunt: Poorly. Very poorly.

“The National Bureau of Economic Research, which is our business cycle dating authority and probably the preeminent research organization in economics...what they do in assessing changes in the business cycle, they take the average of GDI and GDP. So in the 20-year moving average to 1970, it was growing at 2.2% per annum. And in the last 20 years ending 2023, we're growing 0.9% per annum. We've lost 1.3% per annum in the 20-year growth rate. And by the way, if you look historically, from 1870 to 1970,and we have data, pretty good data - not perfect - for that 100 years, the real per capita growth rate was also 2.2%. So, in the last 20 years, we're down to 0.9% per annum. If we had stayed at the 2.2% just in the last 20 years, the average real economic activity per person would be $78,000 or so. Whereas, in actuality it's only $66,000.”

“So we've really dug a deep hole for ourselves. The problems are basically worse everywhere else; there are some minor differences, perhaps, but the budget deficits are just simply too large.”

“Additional monetary growth does not correct the problem of negative net national savings. You can increase the money supply, but that will just have an inflationary impact. There's no way to inflate our way out of the problem. Inflation just has a devastating impact on the modest and moderate income households, which then means that inflationary policies increase the income and wealth divides. We're seeing that big time in all the major economies of the world. So you could conceivably use fiscal policy to reverse negative net national saving, but there is no one that has that agenda, no one, none whatsoever. And it would require a great deal of political goodwill and shared sacrifice, and there's just no pathway to achieve it. So we're stuck with it now unless something fortuitous happens. But it is going to be very hard to alter this downward trend in the standard of living. This means that the income and wealth divides are going to get worse and it's not a wholesome development at all.”

“Ultimately inflation is so hurtful to so many people that the Federal Reserve had to reverse themselves, which is what they're now doing. And even with the $6 trillion of debt that was taken on during the pandemic, that did not bring the rate of growth in real per capita income back to the trend line, it just brought it back to the trend line. However, because of the Federal Reserve's operation, it produced all of this excessive inflation, which had a devastating impact. And so the economy has been left in a very difficult position. If you look at the real average weekly earnings of the full-time hourly and salaried people, which is about 120 million people. In the last 14 quarters of the expansion, there's been a decline at a 1.5% annual rate, that's the average. But within that average, you've got some skew. At the very high end, there was some excellent performance.”

“There was a pre-Adam Smith economist by the name of Richard Cantillon who understood that when you have rapid monetary growth, you get excessive inflation, a damaging impact on more moderate income people, which exacerbates the income and wealth divides. Which is what the pandemic did. And we're seeing that today very, very evidently.”

“2023 was only the eighth year in which we had negative national savings since 1929. And the other seven years they were all when we were in serious economic contractions, four of the negative net national savings occurred in the 1930s. And then we had three negative national savings in 2008, 2009 and 2010. Very, very rare, but it was not a persistent condition. But now we have a very, very difficult problem and one that, at least to me, appears very difficult to resolve. Before now, we had an excessive indebtedness problem using the production function, which indicated the debt was bringing the growth rate down the law of diminishing returns. But now, however, when you have negative national savings, what it means is that we collectively are living beyond our means, but we don't have the resources to increase the capital stock.”

“When the inflation, however, surged out of control, Burns discovered that the fiscal policy partners were no longer there. And so, guess who had to clean up the inflation of the early 1970s? Burns, and he didn't do a very good job of it, and it was only partially done. And we suffered rising inflation all the way until Paul Volcker came in. And it took him two years to finally get the job done, two or three years to get the job done. So now we go into the pandemic and there's no recollection of major past policy mistakes. That's just the character of the way things are. So, no one remembers that the last coordination ended in a disaster of too much inflation. And a decade of rising inflation and just worsening of the income and wealth divide. So the Powell Fed cooperates with fiscal policy. To do so, he engineers an unprecedented increase in money supply. Which was even greater than what Burns had done during the early 70s. But the same thing happened to Powell, which happened to Burns. When the inflation problem arose, the fiscal policy partners were no longer present. And that left the Federal Reserve to clean up the problem by itself. And so, one of the great challenges that the economy faces is for the Federal Reserve to operate independently. And those who tell you that we can somehow solve our problems of this declining rate of growth and the standard of living by adopting some sort of inflationary outcome, in my view, are gravely wrong.”

“I think that the Federal Reserve has created the image that if anything goes wrong, the Fed will come to the rescue, there's a Federal Reserve put, and the Federal Reserve will take care of the problem.”

“The problem is that, for a free enterprise system to work overtime, I think you have to have two things. One, you have to have moral hazard. In other words, if people are going to take chances, it's fine if they guess right and they have a profit, they should keep their profit. But many people assume that if they guess wrong, they'll be bailed out. In other words, the gains are individualized, but the losses are socialized, in other words, accepted by the body as a whole. And I think that we have to reintroduce moral hazard. And I don't think that that is present.”

“Another critical requirement of a free enterprise system is Schumpeter's creative destruction. That you have to find a way to move resources to the most efficient parts of the economy. Well, if the Federal Reserve is going to constantly be there to bail out any of the losers, then you don't get a reallocation of capital.”

“If you're going to shift into government activity, the government activity has a negative multiplier, this is based on a lot of academic research. The private sector has a positive multiplier. So, over time, in the short run, you may get a benefit, and if you try to reverse it, you'll get a detriment over the short. But when the government share goes up, you get further and further into command and control, and economic activity gets weaker and weaker. As the economic activity gets weaker and weaker, then the income and wealth divide gets more divergent.”

“…talking about the young people, we saw this very recently that one of our major jewelers is experiencing quite weak results. And what they said was that the young people are postponing marriage. They didn't say that they were giving up on it entirely, but they were postponing. But I think that the fact that the standard of living is sagging, is postponing and it may even be eliminating marriage, because I think the youngsters realize their economic future is not that good. It is a very, very sad situation because then you undermine your growth rate. And family formation or household formation is a very significant variable, very stimulative. I believe demographics are destiny.”

“I don't think the economy is the stock market. I don't believe the stock market is that important to economic activity. The stock market has done very well since 1970, but what happened to the real per capita growth rate? You come down from 2.2% to 0.9%. The stock ownership is too heavily skewed to the top two deciles, and, therefore, it's important for them, but it's not a solution for the vast majority of the American people, or for the people of any economy that I'm aware of.”

Below are some Fed Rate-Cut Calls. I particularly liked this comment:

Strong Economy Narrative Is Farcical with Matthew Piepenburg

“The US in particular is so divided on politics, the woke movement, identity politics, arguing about transgender holidays on Easter at the White House, versus a huge sucking death sound right in front of us, but you know politicians are good at distracting us…”

“The difference between the French and the National Assembly in 1789, and the Fed in 2024, is that the U.S. dollar, unlike the French Assignat, is the world reserve currency, so we've been able to postpone the inevitable hangover.”

“Powell needs inflation to be higher than the yield on the 10-year, here realistically in terms of actual math, but politically and publicly he has to misreport inflation and grossly misreport inflation”

“I'm almost indifferent to the DXY2 because again you're just measuring donkeys and horses on their way to the same slaughterous. I'm not that interested in comparing equally sick animals.”

“Be informed. Look at your currency, look at the inflation, look at the debt in your country, and ask yourself honestly how they're really going to fix this. Question the wars they want to send you to, and question the narrative on who's the real good guy and real bad guy. I'm not going to tell you who I think it is, but do some deeper thinking than just what the left or right media tells you. Use your own common sense.”

“Using T- bills to take the pressure off the 10-year is just the last desperate QE-like attempt before we go to direct QE”

“When it becomes serious, you have to lie.”

Steph Pomboy pointed this out:

Via S&P:

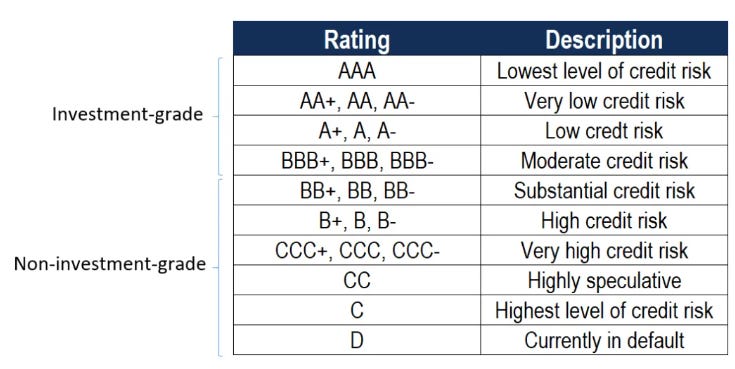

“S&P Global reported that the highest one-year default rate for AAA, AA, A, and BBB-rated bonds (investment-grade bonds) were 0%, 0.38%, 0.39%, and 1.02%, respectively. It can be contrasted with the maximum one-year default rate for BB, B, and CCC/C-rated bonds (non-investment-grade bonds) of 4.22%, 13.84%, and 49.28%, respectively.”

So it looks from the first chart that people don’t see much difference in risk between B and BB bonds at this time, although the risk of default by B’s is over 3x greater. i.e., complacency.

Does this make any sense?

The Hadley North Scottsdale, a 240-unit community in Scottsdale, Ariz., has recently changed hands. IMT Capital acquired the asset for $96 million from a private owner…The property previously traded in May 2022, when Liv Communities sold it for $145 million or $604,167 per unit, the same source shows. The buyer financed the transaction with an $87.3 million loan

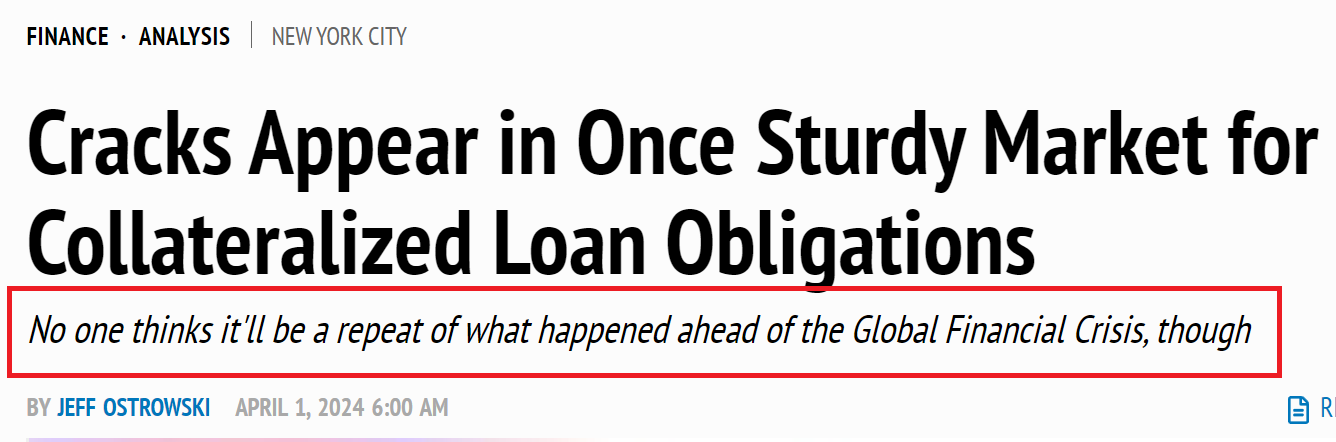

‘Cracks Appear in Once Sturdy Market for Collateralized Loan Obligations’

I love that they felt they had to add the next sentence…

“In recent months, commercial real estate collateralized loan obligations, or CRE CLOs, have flashed warning signs. In one example, Moody’s Investors Service reports that CLO loan impairments soared from just 0.3 percent in the second quarter of 2023 to 2.9 percent in the first quarter of 2024.” (all I have)

The ABC’s of CLO’s Jim Grant with John Kerschner, head of U.S. securitized products at Janus Henderson

Deja Vu All Over Again

''Technology has been evolving since the days of the telegraph...the telegraph seemed as exciting as the Internet, and indeed it was. So it's important to separate the promise of technology with the occasional exuberance, over-exuberance, indeed, manias of speculation."

Jim Grant, January 2000

“annoyed or angry, especially in a rude way“

Legacy media wasn't killed, they committed suicide.

Seeing the demise of the WSJ during my lifetime is sad. You would think there would be a market for unbiased news (on either side of the aisle), but I guess that's too boring for most. Financial Times is actually pretty good, but I only have a beer budget.

I could get the WSJ for only around $1 per week, but I can't in good conscience support them even for that amount.

Great comments by Lacey Hunt. The Fed deserves even more blame than it gets here. It has become a pure lapdog, wagging its tail as it does govt bidding by monetizing debt which prevents the public from seeing how expensive Congress and Biden's programs are as long as possible. Looks like game is up finally.

Both parties are at fault, but Biden's use of the Strategic Oil Reserve and the Debt Forgiveness to buy votes disgusting. And LH also points out that symptoms like not marrying, not having children etc, are caused by the realization of most people that things are very badly wrong. They may not know exactly why, and may even think govt will actually help them, but they know something is wrong