Consumers are collapsing

Not the ones on CNBC though, yet.

“What you see, son, is a man who never measured success by the size of a man’s wallet.”

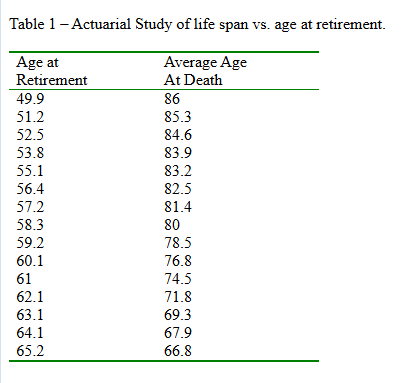

The Boeing experience was that employees retiring at age 65 received pension cheques for 18 months, on average, prior to death. A similar experience was discovered at Lockheed Martin, where on average, employees received pension cheques for just 17 months.

Apparently the experiences at Ford Motor Company and Bell Labs were similar to those of Boeing and Lockheed. Statistics at a pre-retirement seminar illustrated that the average age of retirement at most large corporations in the US was 57. So people retiring at age 65 are a minority, but it is still a startling statistic.

The thought is that the hard working late retirees (65) are more than likely putting too much stress on their ageing bodies and minds and due to the stress, they develop a variety of health problems. The associated stress induced health problems lead to them dying within two years of retirement.

Another startling statistic from the same Corporations is that those who retire earlier, say age 55, tend to enjoy their retirement on average for more than 25 years.

Some people questioned the veracity of the above article, but I found the study, from March 2002. Rebuttals are in the comments if you’re interested.

The Truth is Out There

“Although I am regarded by many people as a ‘conspiracy theorist,’ which is more often than not utilized as a pejorative term, I do all of my research through very mainstream channels.

I am a big believer in the notion that ‘the truth is out there,’ but don’t expect it to be delivered to you in a tidy package by any mainstream media outlets. Finding it involves assembling a jigsaw puzzle of sorts, with the goal being to gather up all the bits and pieces of information that other writers tend to present as throwaway facts and/or interesting anomalies.

Sometimes those bits and pieces end up being no more than interesting anomalies, but past experience has taught me that if those divergent facts are properly assembled, a new picture often begins to emerge that is strikingly at odds with what is widely accepted as our consensus reality.”

“It is always a net negative when the government shuts down, we don’t have data, and our decision-making process is handicapped in a big way.”

Now that during the shutdown the government has stopped releasing economic data, how will we know what the wrong numbers are?

Food for thought

Nomi Prins

“The Federal Reserve was created to help Wall Street…It wasn’t created to help individuals who couldn’t get their money out of banks in the panic of 1907 in New York City. It was for people like JP Morgan, who wanted to make sure that his literal friends who ran other banks and insurance companies had a source of help should another panic happen.”

”When I wrote Permanent Distortion - it came out in October 2022 - the debt was about half of what it is today…Now that debt hasn’t necessarily gone to make people’s lives better. It hasn’t reduced inequality. Much of it hasn’t even built bridges or roads or highways or hospitals, because, from the United States perspective, our grade from the American Society of Civil Engineers is a C- in our infrastructure. It’s been created to do things, but it’s not specifically accountable to real people or to Main Street or to the real economy. And that relationship or that anti- relationship continues to expand when we think about what the next crisis could be, whether it’s a disease, whether it’s a meteor hitting part of the planet, I mean, whatever it could be, in a massive way, the solution right now will be the same, which will be to print money, and that money will continue to flow into the financial system more so than the real economy.”

“We’re gonna have to find people that want to learn, which is gonna be impossible.”

“It’s even more difficult to teach people how to give a shit.”

How Congress Should Oversee the Federal Reserve’s Mandates by Alex J. Pollock

In my view, the Fed in monetary affairs is “independent” in the limited sense of being independent of the Executive, but it is fully accountable to Congress, and indeed Congress has plenary power over it. As is often observed, this derives from the Money Power given solely to Congress under Article I, Section 8 of the Constitution. It also derives from the Taxing Power given solely to Congress by the same section, since the inflation created by the Fed is in fact a tax on the people.

A good historical statement of the Constitutional relationship was by a prominent Democratic Senator, Paul Douglas, who told Fed Chairman William McChesney Martin, “Mr. Martin, I have typed out this little sentence which is a quotation from you: ‘The Federal Reserve Board is an agency of the Congress.’ I will furnish you with Scotch tape and ask you to place it on your mirror where you can see it each morning.”

Like any good boss, the Congress should not meddle in too many details of its subordinate’s work, but it should be responsibly involved in the major policy issues and strategic directions. For example, should the United States commit itself to perpetual inflation and perpetual depreciation of its currency at some rate? I suggest that the Fed does not have the authority to regulate the value of money in this fashion, or to pick a particular rate of its constant depreciation, without approval from Congress.

Then again, it seems Congress did approve.

”On another occasion Chairman Martin clearly explained why the Fed must be independent of the Executive: the Treasury is the borrower and the Fed is the lender. You should not have the borrower be the boss of the lender (a dangerous monetary situation known technically as “fiscal dominance”).”

“Inflation is a tax. Inflation is simply taking purchasing power away from the people and giving it to the government. The Fed creates inflation. The Fed is taxing. The Fed is responsible to Congress for its taxing activity.”

Whitney Webb and Mark Goodwin join Marty Bent “to examine how surveillance infrastructure expands under the Trump administration through Palantir contracts and digital ID implementation”

Webb:

“Now you have the former head of Al Qaeda being given a diplomatic welcome in New York. David Petraeus is like, ‘How you holding up?’”

After 9/11, “Americans were told we have to give up all of our freedoms because we have to destroy the guys who did that. This is one of the guys who did that.”

“Ultimately a lot of the “war on terror” infrastructure was meant to be used domestically at some point.”

“Who are some domestic terrorists we could investigate? What about Dick Cheney or Leslie Wexner? Why can’t we investigate them with all the power of DHS and Palantir and NSA? Why can’t we go after people like that? Instead it’s all pointed at regular people.”

“I really wish that more people that actually cared about liberty and civil liberties and freedom and individual sovereignty would actually pay attention to the political philosophies of people like Peter Thiel and Curtis Yarvin1…because they’re not libertarian.”

Goodwin:

“What are they doing in Venezuela right now? They’re like, oh my god, all the drugs are pouring in from Venezuela. Let’s go bomb these people, as if the US government hasn’t been bringing in drugs and trafficking drugs in the United States and financing their black book operations. Now we got to go blow up a fishing boat in Venezuela and start an act of war? It’s just absurd.”

“I hate both parties, but this was an issue I had with some of the people that were giving a free pass to Trump for 2.0. He printed a ton of money and locked everybody down. He was a big part of the bailouts the first time around, the “going direct” plan, which you could argue maybe was even the point of the pandemic - to print a ton of money when the repo market fails in fall 2019, and then shut everything down so there’s no demand, and we print trillions of dollars and hand it to Blackrock.”

“Those who go beneath the surface do so at their peril.”

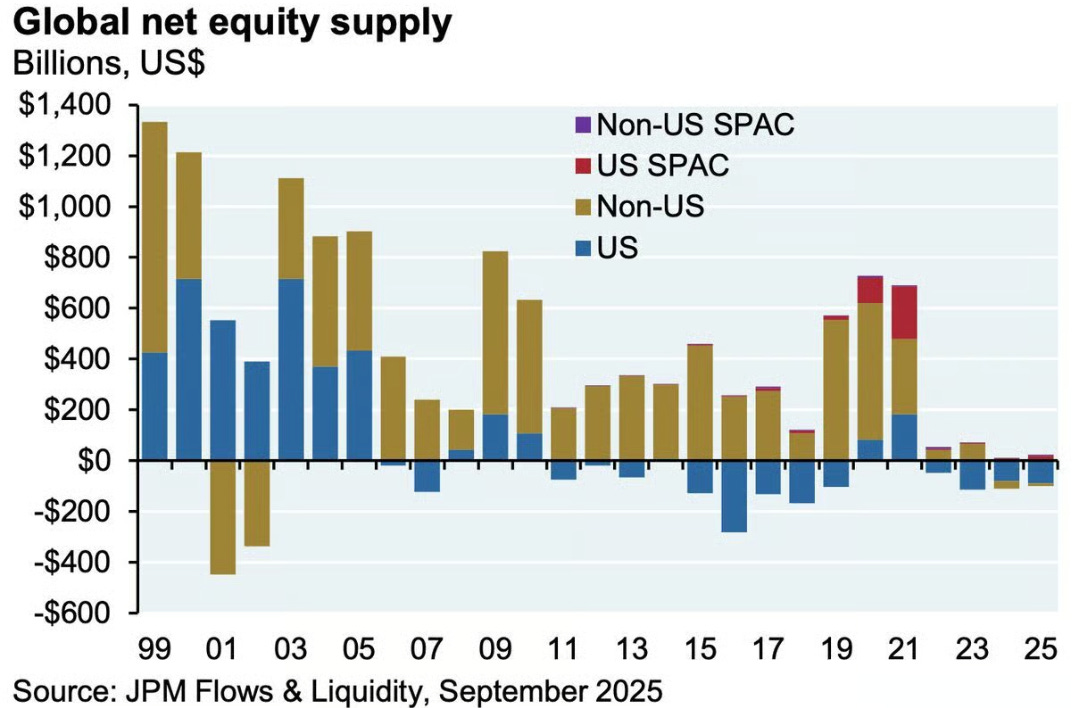

“I’m not a market technician but I do believe that declining net equity supply conditions since 2011 have contributed to US equity market resilience in the face of various shocks. If you believe that supply and demand conditions affect the price of goods and labor, there’s every reason to believe such conditions can affect financial asset prices as well. At the end of the day, $1.5 trillion in annual defined benefit and defined contribution payments into qualified plans by households and employers has to end up invested someplace. While such contributions have declined as a share of market cap from their 2009 peak, they’re still running at 3%-4% per year while the supply of US equities continues to shrink (blue series in first chart).”

Cracks to Emerge in Old Private Credit Deals Oaktree’s Poli Says

“There are 19,000 private equity funds in the US. There are 14,000 McDonald’s in the US. How are there more private equity funds than McDonald’s? That’s actually crazy, right?”

Vincent Daniel and Porter Collins

Vincent Daniel: “No one should be able to play in the futures market and get umpteen amounts of leverage to express a position. They shouldn’t. But they do. And as a result, that’s why you see so much frothiness in trading in markets.”

Porter Collins: “And go back to the GFC. You can see why we’re so scared of leverage, because we saw it firsthand, the danger that it produces. And the quant shops know that. When vol goes up, they shrink their books as quick as they possibly can.”

VD: “This company, a DAC - their asset - is Solana. And I had the president give me the pitch, and it frightened the shit out of me, because because his pitch was, well, we’re trading at a discount to to Micro Strategy. We should trade at a premium to Micro Strategy, and once we get there, we could just issue capital and buy more Solana. I go, like, that’s your pitch? That’s your pitch?”

VD: “We’ve been studying the Genius Act in stablecoins, and I have to tell you, you got to give a golf clap to how clever these people can be from time to time, right? Which is they effectively have tied Bitcoin and Ethereum into the

potentially too big to fail argument. If you walk through the mechanics of it, now we’re tied and and the buying and selling of treasuries de facto is tied to the level of Bitcoin, Ethereum or whatever qualified asset that is backing stablecoin. It’s pretty frightening when you think about it.”

VD: “For a bunch of cynics and bears, we’ve been running net long, right? And it has served us well. But we all know this game has to end at some point, right? And while we’re playing micro bulls, our macro is like crushing us down and we’re like, “How do we get off? When do you know you get off?” And sadly I don’t have the answer. So thankfully you didn’t ask. But it’s the question we keep asking ourselves, right? Because we know at some point this is probably going to end and we probably don’t want the exposures we have when it does.”

PC: “We’re cutting rates, but we’re nowhere close to the “2% target.” I think gold’s kind of telling you that, you know, you guys are cutting rates again, and you’re nowhere near the the 2% target. You got Fed’s Trump’s guy calling for six more cuts, and he’s only the first Trump governor in. He’s getting like three more soon. So are they gonna run this thing so hot where inflation takes off, and that’s going to kill the market?”

Kevin Muir: “Do you think that private equity and private credit are a disaster waiting to happen? Are you as worried about that as some of the commentaries that you hear?”

PC: “Well, they’ve done a good job of hiding it, right? They’ve suspended mark to market accounting for four years, right? They’ve done a beautiful job of that, right?”

PC: “All these big universities aren’t getting their distributions, right? Ah, you’re flat again this month. You know, when you don’t have price discovery, lo and behold, it’s not a problem.”

VD: “Just think about what crazy cockamamie thing they’re going to come up with to try and get the housing market going.”

I love this Ben Bernanke anecdote. What a horrible person he is:

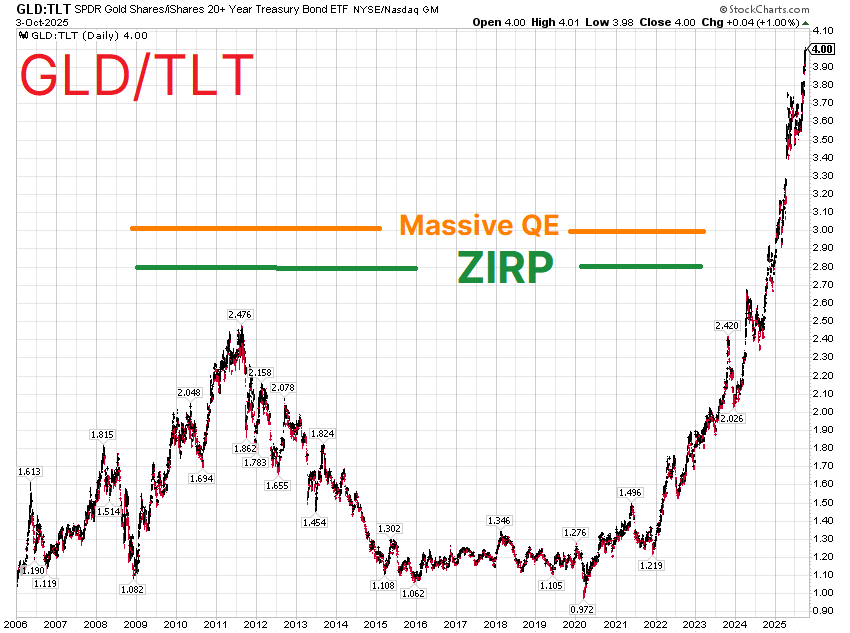

Pollock: “How much gold does the Fed own?”

Whalen: “None.”

Pollock: “Zero. Not one ounce. I think it’s one of the few major central banks that doesn’t own any gold.”

FAFO

“How are inflation expectations anchored if they’re 50% above the Fed’s target and have been there for almost five years running?” - Greg Weldon

“Commercial bank consumer loans have fallen over a hundred billion since the end of the third quarter of 2024. Over $100 billion. That’s more than 10%. Finance companies down $17 billion. So, you know, go to the bank, they won’t lend you money. You go to the finance company, you’re going to pay more, they won’t lend you money. Where do you go? You go to the credit union. Credit union loans to consumers up $71 billion since the end of third quarter of last year, almost a year 11 months. The only source of growth is credit unions. We saw this in first quarter, second quarter 2008 - same thing - because that’s the last place you can get credit. That is the easiest place you’re going to get credit, and when we see that number turn down, that’s going to be a bad bad sign for the consumer, a bad sign for the Fed.”

“Here is the final kick in the in the stones from the Beige book: Hotel prices rose despite decreased occupancy rates. How do you spell stagflation?”

“Powell was asked, “What will the Fed do if prices pick up more?” “Here’s Powell’s response. I’m Jerome Powell now. So what will we do? …We’ll do what we need to do, but we have two mandates and we try and balance them. All right. This is quite an unusual situation. How do we decide what to do? Because our tools can’t do two things at once. What? Hold on. Stop the presses. Jerome Powell just said, “We can’t fight the stag and the flation at the same time. We have stagflation.” And he used the word. He used it. I’ve been saying it for 18 months. It’s coming. It’s here. Our tools cannot fix stagflation. We’ll have to choose one. And you will choose to reflate. Hands down.”

Paraphrasing Powell: “We cannot say that the risks are clearly tilted to inflation, but I would say they’re moving towards preliminary equality. What the hell is preliminary equality? Again, this is central bank Fed speak at its finest, at its worst.”

“Consumers Are Collapsing”

A short, very good podcast this week with Steve Eisman and Lakshmi Ganapathi from Unicus Research.

Someone on Twitter named Mike did a nice summary so I don’t have to! These bullet points are all from him:

Lakshmi Ganapathi from Unicus Research said sometimes next year or 12-18 months the weakness in consumers will show up!

The U.S. economy’s real growth rate is estimated to be only 50 basis points (0.5%) when deducting massive AI infrastructure spending, indicating underlying pockets of weakness [02:30].

The primary focus of the weakness is the consumer, who is described as “broke” due to the monthly budget math no longer working [03:17].

Credit card 90-day delinquency rates have doubled since 2021, now approaching 7% [07:26].

“Hidden inflation” in mandatory expenses like auto service, insurance, property taxes, and health insurance is a major factor dragging down consumer finances [04:12].

The re-reporting of student loan defaulters to credit rating agencies is causing consumer credit scores to drop by 200 to 250 points [04:49].

COVID-era stimulus checks gave many subprime consumers a temporary, illusive “prime” credit score, leading them to take out loans that are now distressed [05:42].

These illusionary “prime” loans were bundled into Asset-Backed Securities (ABS), meaning technically subprime loans are classified as prime on the books [06:05].

Over one in five new car borrowers currently face monthly auto payments exceeding $1,000 [06:54].

Auto loan modifications now include terms up to 84 months with interest rates as high as 22% to 23% [07:04].

Banks are avoiding repossessions by modifying loans and adjusting them to “current” status, essentially kicking the can down the road [07:42].

Many consumers are upside-down on their auto loans because they paid above the sticker price during the period of high liquidity [08:34].

OEMs and dealers have “stuffed the channel” with inventory, leading to “lot rot” where both 2024 and 2026 model year cars sit unsold [10:09], [13:19].

CarMax reported poor results, increasing their loan loss provision for older vintages, which signals significant distress in the used car market [10:50]. Consumers can no longer afford 0 to 5-year-old used cars and are being forced to buy older vehicles that are 5 to 10 years old or priced below $10,000 [11:51], [13:33].

People are surrendering their cars, and the recovery rate on repossessed vehicles is less than 30%, which is the heaviest repo backdrop seen since the Great Financial Crisis [12:13], [16:31].

The consumer pain is expected to spread across the board to retail, credit cards, and Buy Now, Pay Later (BNPL) [15:27].

69% of the U.S. population is living paycheck-to-paycheck [18:22].

25% of those living paycheck-to-paycheck are using BNPL to buy groceries, effectively making it a form of “layaway for food” [18:58].

BNPL companies are using AI models to track consumers’ real-time financial health, monitoring things like bank overdrafts and student loan defaults, leading to credit throttling and declined transactions [20:37].

The meme stock craze, specifically Open Door (a house-flipping company that was reportedly losing $15,000 per transaction), is viewed as a manifestation of consumer stress where people look for “get-rich-quick schemes” to solve their financial problems [25:09], [31:06].

Paulo Macro

“The economy had been rotting for some time ahead of the 1929 crash, from the bottom up, which is very similar to what we’re seeing in terms of the bottom end of the pyramid of the income of Americans, rotting and kind of hanging on by a thread.”

“I regularly take Ubers where the driver has the RobinHood app open on his phone while he’s driving, and he stopped at the light. It wasn’t like this even a few months ago. We had a a bit of this with crypto back in 20 and 21 going, into the kind of GameStop meme mania, like around ARKK - you know, Cathy Wood - high in early 21. But we are right back there. And what’s crazy is that we’re doing this, you know, less than five years after a pretty nasty bear market in 22 and 23, in both equities and debt. And the brevity of financial memory just keeps getting shorter.”

“I appreciate to no end the sort of strategic vulnerability that America has put itself in through the relentless outsourcing over the last 40 years and especially the last 25 years since China joined the WTO, where we sleepwalked into a situation where…there are some things where there’s no margin for error, and if the magnets don’t show up, the missiles don’t get produced, and the bullets don’t get made.”

“2008 - classic example. Bear Sterns goes to the wall. It took six months, but people were quietly asking who’s next, and the answer that kept coming back was Lehman, because Bear was 50 to1 levered on equity, Lehman was like 35. And then once Lehman went to the wall, the who’s next was instantaneous. It was literally next day. It’s the order is Merrill Lynch, which ended up going to Bank of America. The next day, Morgan Stanley and Goldman, and in the background, what the hell is AIG Financial Products and what did Joe Cassano do over there, right? All in a week. So, you have this like fuse - something happens, and then all the dominoes suddenly topple at once, because people wake up”

Dan Rasmussen

On private-equity: “The reality is that this is really small companies with a lot of debt that are obviously really risky. Why people are taking this asset class that’s, you know, $2 trillion, it’s 4% of the S&P 500, and putting 40% or 50% of their assets in - it is crazy to me.”

“Private equity has just stopped being able to sell all the things that they bought 3 or 4 years ago…All the money that those private equity firms put to work in 2020 and 2021 now is sort of coming up for that time, and they should be selling it, and it turns out they can’t really sell it because they overpaid, and they can’t really sell it at a price that’s profitable. So they’ve just stopped distributing money.”

“A few years ago, there was a survey that showed that something of like 90% of investment allocators thought private equity would outperform by 200 basis points a year or more, right? Complete consensus that this could only win. And now it’s losing. And not only are they losing, but their money’s trapped. And the additional problem is that it’s really hard for the private equity firms to explain why the money is trapped. You know, you sort of say, aren’t U.S. equity markets at all time highs? Isn’t this right. I mean, how can you not sell? I mean, walk me through why when the S&P 500 is trading at 30 times PE or something, you’re finding it difficult to sell your assets…you could have come around to this view that clearly their assets are just not worth what they’re saying they’re worth. Otherwise they’d be able to sell them at an attractive price and this whole app cycle would continue.”

“There’s this wonderful study from 2004 called the Persistence and Predictability of Growth Rates, which we updated with 20 years of additional data. And that study definitively proves that growth, revenue growth and earnings growth does not persist. It is not predictable. So just because a company has grown fast in the past does not mean they’re predict grow fast in the future. If slow in the past doesn’t break from slow in the future, that the best prediction of future growth tends to be that growth will follow a random walk.”

“…if anything, what you want to do actually is focus on the lower growth firms where you’re more likely to be surprised to the upside. But I think what this sort of shows is that there’s this sort of persistent resorting happening, this this continued friction between prediction and reality, between expectations and surprises.”

Bill Brewster: “What I took away from the book, which is probably too simplistic, but if Vol is low, and spreads are tight, maybe people are overly confident.”

S.F. housing giant Veritas defaults on $652M debt. 66 buildings now face foreclosure.

Veritas Investments, the real estate giant that owns thousands of housing units across the West Coast, has defaulted on $652 million in debt and is facing the foreclosure of 66 buildings in San Francisco…Those 66 buildings house 1,566 units, according to a review of records with the San Francisco Office of the Assessor-Recorder. Because Veritas’ loan is secured by the buildings, all 66 could be sold at foreclosure within 90 days to pay off the debt…

Veritas has faced serious financial strain in recent years. It defaulted on $1 billion in loans in late 2023 and subsequently sold significant chunks of its real estate empire. In January 2024, it sold 2,150 units, reportedly a third of its San Francisco housing stock, for $464 million. Last year it sold another 762 rent-controlled units, and this March sold 1,770 units for $540.5 million. Earlier this year, Veritas defaulted on a separate $450 million loan…

After the 2024 sales, Veritas was dethroned as San Francisco’s largest landlord. Its CEO saw the irony at the time: He founded Veritas in 2007 and, after the housing crisis, made his mark buying foreclosed-upon properties.

“I got them in the same way that I lost them,” Au told The Real Deal last year.

Sorry, kids. FHFA home prices up 2.3% YOY.

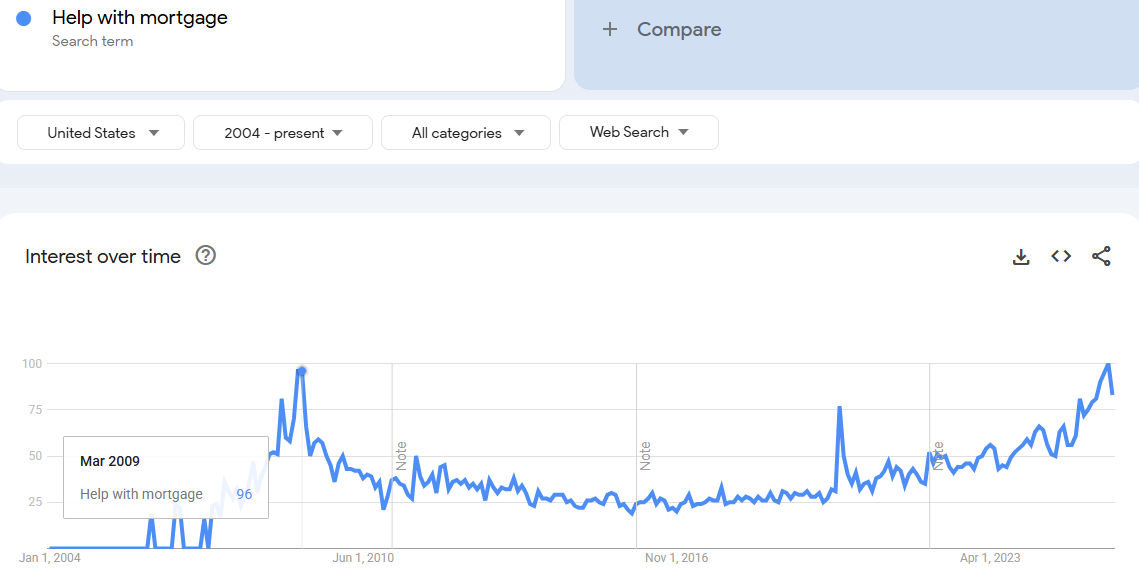

Since this was floating around lately, I fact-checked it.

”By the end of Q4 2025, there will be more 6% mortgages than sub-3% mortgages.”

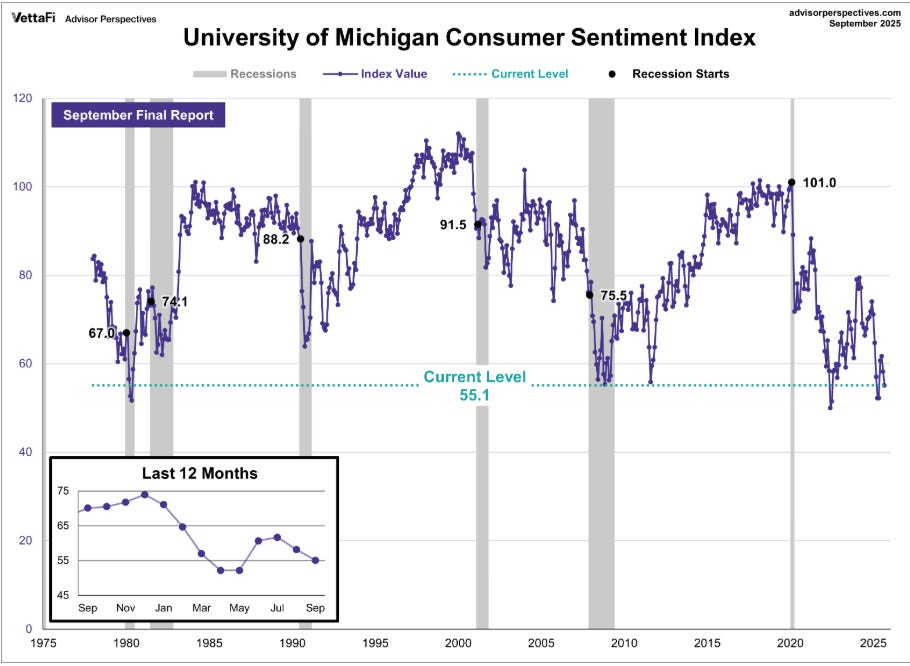

Sentiment levels are at deep recessionary lows (like 1980 and 2009). Don’t these people know stocks are at all-time highs?

Wait, What?

Evangelizing for Rembrandt

The billionaire philanthropist, financier and collector Thomas S. Kaplan is in advanced discussions to fractionalise his Leiden Collection, the world’s largest private collection of Dutch Golden Age paintings, and launch it as an IPO (initial public offering).

“I’m looking to see whether I can take the entire collection public,” he tells The Art Newspaper: “I think assets, such as really great art, are going to multiply manyfold because they are truly scarce, and there’s so much money sloshing around that will need a home and this is a great value proposition. To my mind the best way to evangelise for Rembrandt is by giving millions, maybe tens of millions, of ordinary people the opportunity to own a Rembrandt.”

“The biggest risk right now is underspending, especially if you are a category leader.”

Via Grants:

Bloomberg points out that Nvidia’s recently-announced $105 billion of combined investments in OpenAI and Intel spurred a $320 billion, three-day updraft in the chipmaker’s own market capitalization. Yesterday, Alibaba enjoyed a 10% share price bump – tacking on $35 billion in market cap – after saying it would exceed its prior $50 billion AI spending bogey, without specifying a new figure.

“The market has been super friendly to allow these companies to go on this investment spree, [on the belief that] AI presents a foundational opportunity not only for these companies but for the broader economy,” Tejas Dessai, director of thematic research at Global X Asset Management Company, told Bloomberg. “The biggest risk right now is underspending, especially if you are a category leader.”

“When there’s a lot of capital and the emotion is greed and there’s fear of missing out, bad deals get done.”

Michael Gatto, Silver Point Capital (via Grant’s)

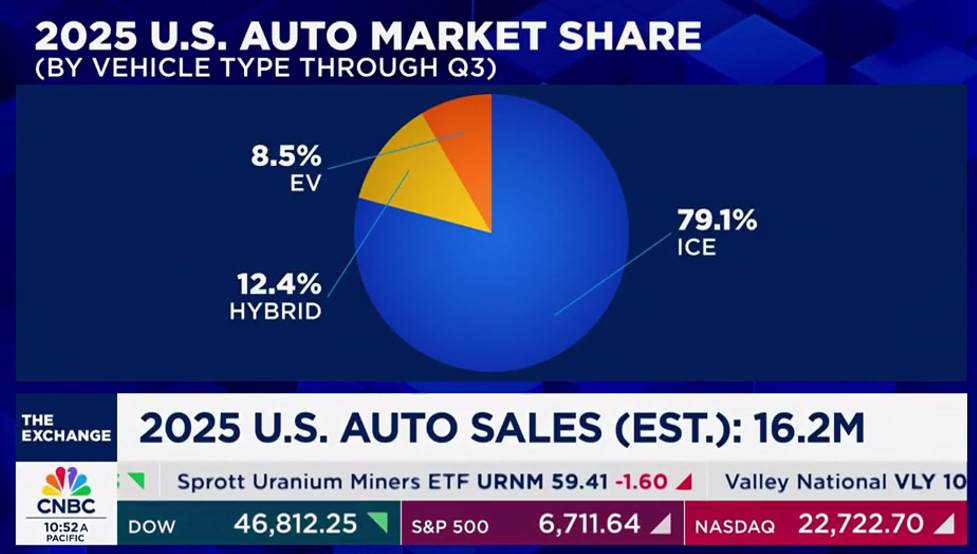

2025 U.S. Auto Market Share

Mr. Skin, on Tricolor:

“Hard to imagine how any fool could actually “invest” in a pool of “sub prime” automobile loans made to illegal immigrants, with no credit score, to buy used cars at inflated prices. Seems like leveraging a depreciating asset like a used car is about as stupid as you can get. But calling these things “assets” and pooling them into a AAA security constitutes criminal fraud.”

”The Credit Market Is Humming—and That Has Wall Street On Edge”

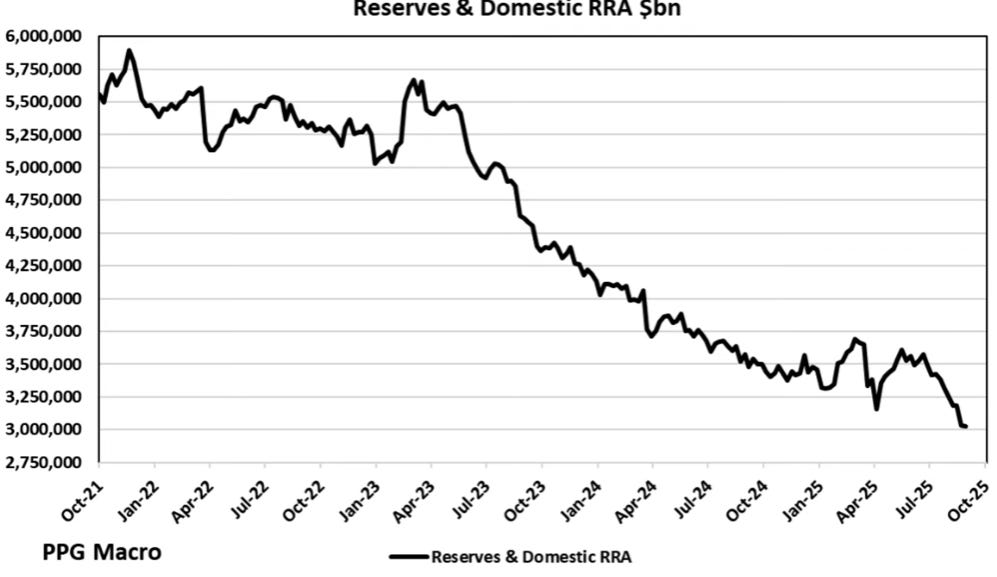

Patrick Perret-Green of PPG Macro

“The non-bank lending is all the stuff that goes into private equity, and mortgages, and the the markets, but the real lending to the economy is basically flat. The non-bank loans are basically zero growth this year, so that’s that’s a little bit of a warning sign.”

“This is the opacity of private credit - pirate credit really. No one really knows what it’s worth…We can see the the amount that’s in PIK notes now - I think it’s something like 11 or 12%. I mean the euphoria - you read the stuff in the media, and of course it’s the same people pumping the same thing up, and it does remind me of CDO’s2.”

The Bloomberg Barclay’s high yield bond index, the OAS - I looked at it yesterday, it was somewhere at 266 basis points, which is pretty much down at the lows that we saw in ‘05 and ‘06 and in ‘21 when we had super easy monetary conditions"

“There are a lot more First Brands and Tricolors out there than people will admit.”

“The regulators themselves don’t have a clue, and it’s not that not only that - we know for damn sure that the accountants of these companies don’t have a clue.”

“The Fed doesn’t know what is the adequate level of liquidity. If it did, it wouldn’t have screwed up so much in the past”

“If you look at the way that most central banks operate, your 1970’s car probably is more efficient than a modern-day central bank in terms of its technology and understanding of things, and I just wonder if they’ve even got an oil light on their dashboard at times.”

Jack: “Now in the US we’re in an ample reserve regime…”

Patrick: “They say ample. That’s the point. They say ample until it isn’t.”

“The non-bank system is so much bigger than it was, so US commercial banks - they have recourse to the Fed. They can go and tap liquidity. I’m a non-bank. I can’t. Non-banks don’t have access to Fed. They don’t have access to swap lines.”

“We see these strong consumer numbers, but then a lot of the stuff within the personal consumption has been on things like health and education and insurance and it’s not really been on enjoying life.”

“People aren’t going to buy US exports. I mean, you know what? When

Trump comes out with 'buying US exports, he ignores all your services. So your whole trade situation is completely farcical. No one’s going to buy an F-150.

We couldn’t fit one on a road in the UK or in anywhere in Europe as a whole, or Japan, most of the most the rest of the world.”

“When dollar liquidity gets worse, or shrinks, and the dollar goes stronger, that is the source of pain for people, because their dollar liquidity gets worse. So how do they finance themselves?”

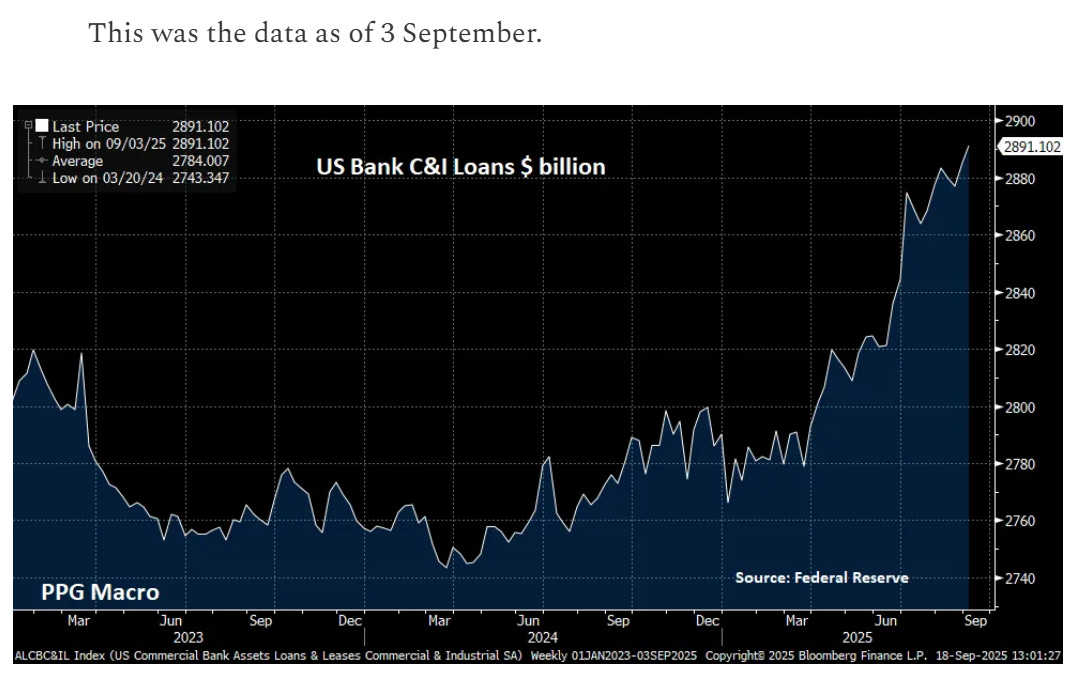

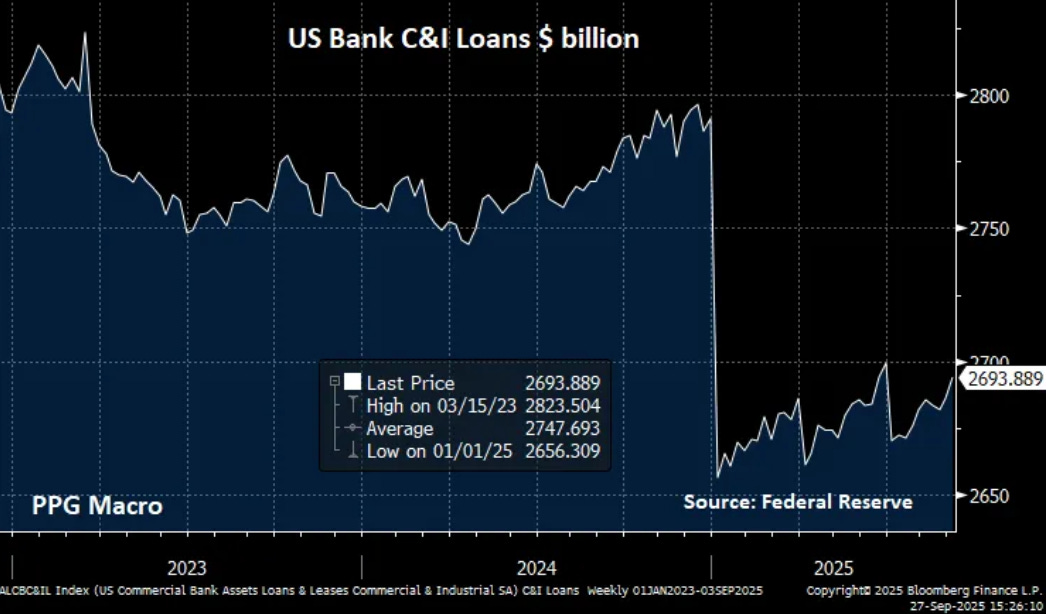

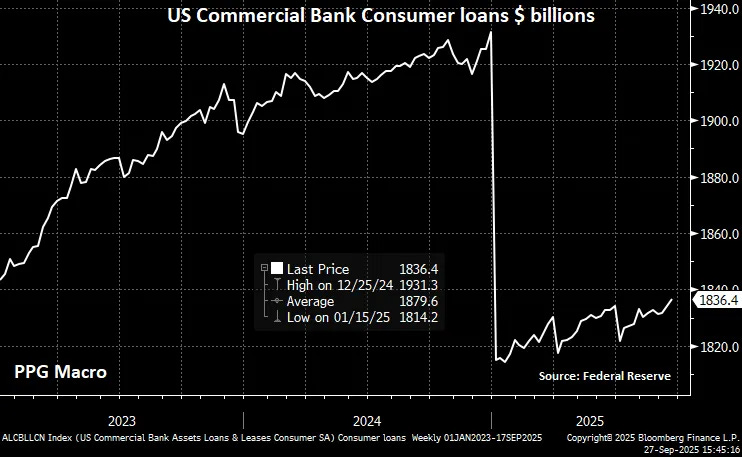

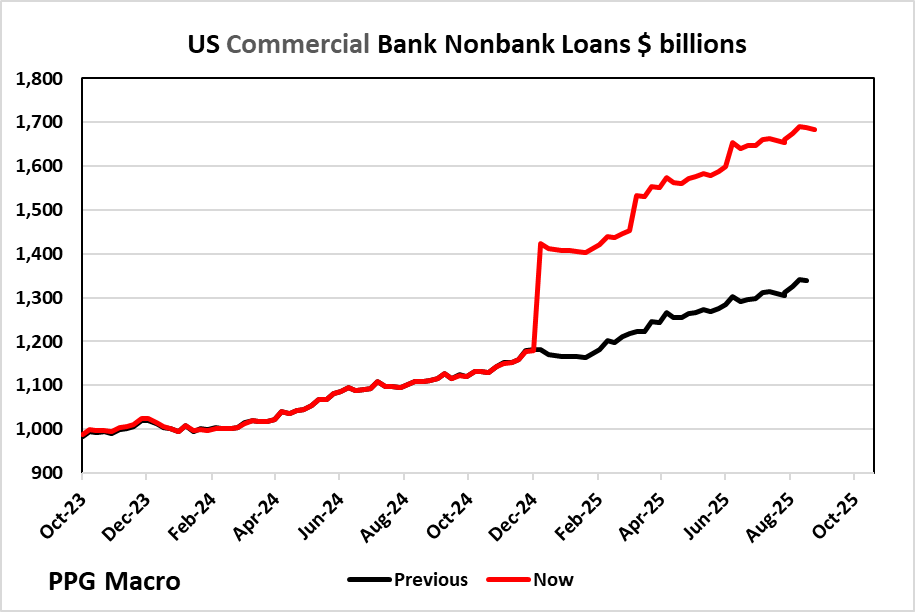

From his substack: Fed Reclassifies Billions of Bank Loans

Commercial and Industrial Lending

Then…BOOM!

In its latest H.8 report, published yesterday, the Federal Reserve suddenly reclassified hundreds of billions of dollars of commercial bank loans.

The main change was between C&I lending and that to non-depository financial institutions, AKA nonbanks.

Tricolor may have been the trigger.

First Third, Chase and Barclays are all reported to have lost hundreds of millions. My presumption is that they were reporting the loans as C&I rather than NDFI. I don’t know the micro details but were they lending to a lending subsidiary?

In turn an order must has gone out from bank supervisors to banks to review the classifications within their loan books.

This is the latest C&I data. They are $200 billion lower than we thought they were.

“The other major revision came with consumer loans which were revised $117bn lower from the presumed year-end level.”

“This brings me to the nonbank loans.

In the previous H.8 report for lending up to the 10th banks, supposedly had $1,398 billion of such loans. Suddenly, as of the 17th, they have $1,684 billion of them. $286 billion more. Wow!”

”The Fed’s reclassifications is further proof of my long-running gag: Most bankers think ethics is a county in southeast England.”

“What’s a financial red flag that people don’t take seriously enough?”

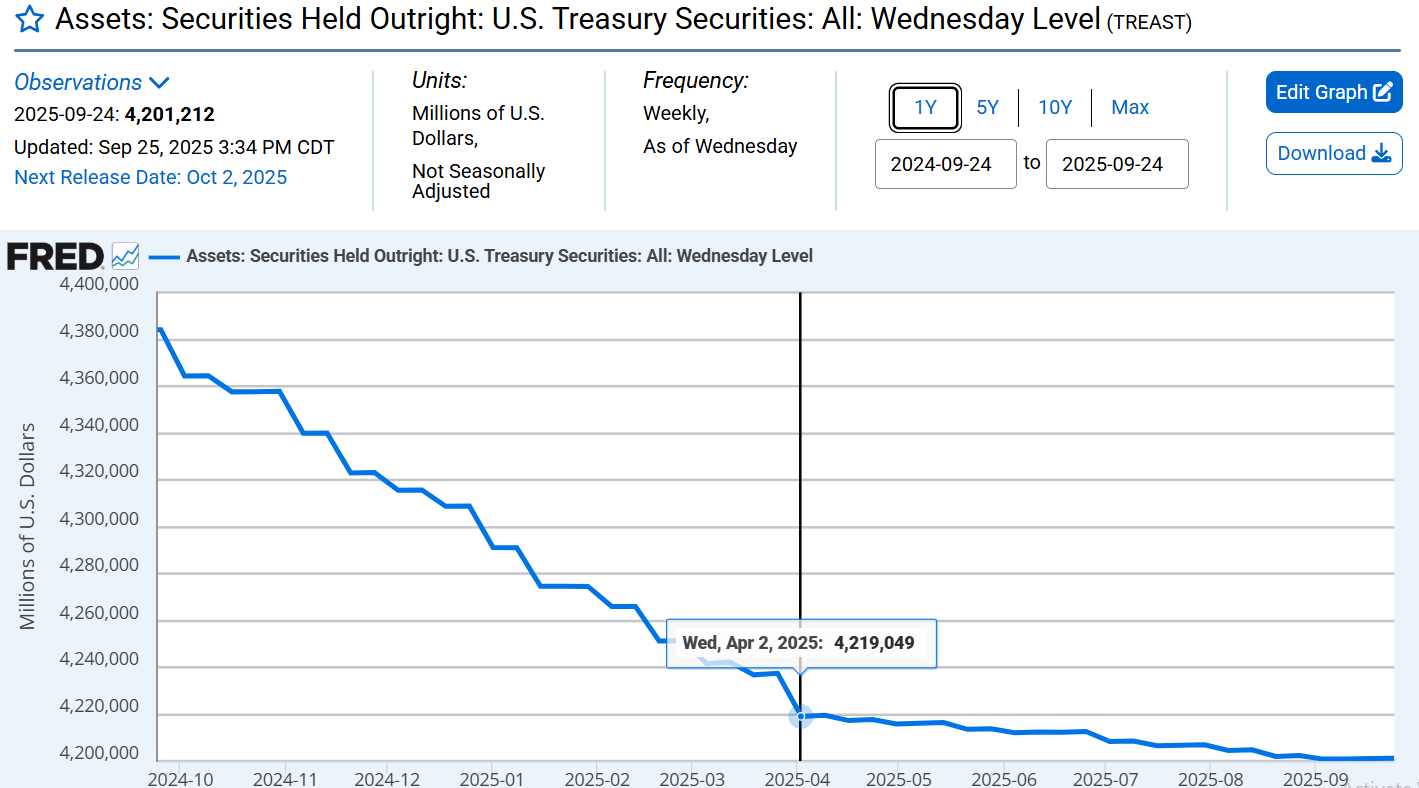

Treasury “QT” is Over

Countries with a lower infant-mortality rate than the United States (2024)

Argentinian Peso vs U.S. Peso

I liked this:

“Large language models are about mimicking people.”

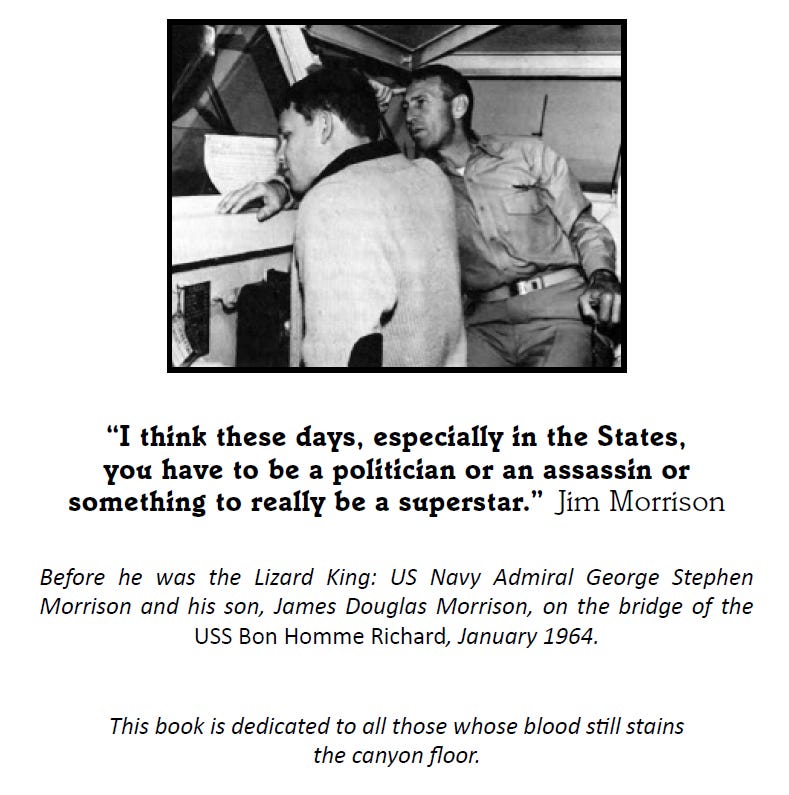

“As one scrolls through the roster of Laurel Canyon superstars. What one finds, far more often than not, are the sons and daughters of the military/intelligence complex and the sons and daughters of extreme wealth and privilege—oftentimes, you’ll find both rolled into one convenient package...

What if the musicians themselves (and various other leaders and founders of the ‘movement’) were every bit as much a part of the intelligence community as the people who were supposedly harassing them? What if, in other words, the entire youth culture of the 1960s was created not as a grass-roots challenge to the status quo, but as a cynical exercise in discrediting and marginalizing the budding anti-war movement and creating a fake opposition that could be easily controlled and led astray? And what if the harassment these folks were subjected to was largely a stage-managed show designed to give the leaders of the counterculture some much-needed ‘street cred’? What if, in reality, they were pretty much all playing on the same team?”

David McGowan

If anyone has too much Bitcoin and would like to send me some, I’m willing to help out. Thank you for your attention to this matter: bc1qkvxy0f8tnxnjddwtyg3jshwgck4e9haw8e8kf9

e.g., Yarvin, writing under a pseudonym in 2008:

“Our goal, in short, is a humane alternative to genocide. That is: the ideal solution achieves the same result as mass murder (the removal of undesirable elements from society), but without any of the moral stigma. Perfection cannot be achieved on both these counts, but we can get closer than most might think.

The best humane alternative to genocide I can think of is not to liquidate the wards—either metaphorically or literally—but to virtualize them. A virtualized human is in permanent solitary confinement, waxed like a bee larva into a cell which is sealed except for emergencies. This would drive him insane, except that the cell contains an immersive virtual-reality interface which allows him to experience a rich, fulfilling life in a completely imaginary world.

The virtual worlds of today are already exciting enough to distract many away from their real lives. They will only get better. Nor is productive employment precluded in this scenario—for example, wards can perform manual labor through telepresence. As members of society, however, they might as well not exist. And because cells are sealed and need no guards, virtualization should be much cheaper than present-day imprisonment.

I like virtualization because it can be made to scale. I don’t think there is any scenario under which San Francisco is burdened with more than a few thousand wards. Many other regions of the earth, however, contain large numbers of human beings whose existence may well prove an unequivocal liability to the owners of any ground on which they would reside. If so, they can be virtualized, creating giant human Wachowski honeycombs of former bezonians, whose shantytowns can be cleared and redeveloped as villas for retired oil-company executives.”

From “The Big Short:

“Enter the CDO. They may not have known what a CDO was, but their minds were prepared for it, because a small change in the state of the world created a huge change in the value of a CDO. A CDO, in their view, was essentially just a pile of triple-B-rated mortgage bonds. Wall Street firms had conspired with the rating agencies to represent the pile as a diversified collection of assets, but anyone with eyes could see that if one triple-B subprime mortgage went bad, most would go bad, as they were all vulnerable to the same economic forces. Subprime mortgage loans in Florida would default for the same reasons, and at the same time, as subprime mortgage loans in California. And yet fully 80 percent of the CDO composed of nothing but triple-B bonds was rated higher than triple-B: triple-A, double-A, or A. To wipe out any triple-B bond--the ground floor of the building--all that was needed was a 7 percent loss in the underlying pool of home loans. That same 7 percent loss would thus wipe out, entirely, any CDO made up of triple-B bonds, no matter what rating was assigned it. “It took us weeks to really grasp it because it was so weird,” said Charlie. “But the more we looked at what a CDO really was, the more we were like, Holy shit, that’s just fucking crazy. That’s fraud. Maybe you can’t prove it in a court of law. But it’s fraud.””

Perhaps we need a constitutional amendment freezing all government pay and benefits (including congress and its staff) at current dollar amounts.

Willing to bet inflation would be gone in a hurry.

"large numbers of human beings whose existence may well prove an unequivocal liability to the owners of any ground on which they would reside"

When doing genealogical research of my Irish side, I used to wonder how people near starvation could afford boat tickets to America.

The answer is that the English landlords paid for the tickets, because the removal of the native Irish improved the value of the land more than the cost of the ticket.