'Homes are meant to be a place to live, where you spend your time and raise a family'

They financialized everything.

The leading finance publication (Doomberg) on Substack has decided to stop using X, aka Twitter. In my opinion, Elon Musk misunderstands the value of content creators on his platform. His goal is to keep people doom scrolling forever, so links to external content, especially on Substack, are punished heavily. This is short sighted. People go to Twitter to discover new content. If they consistently discover great new content, even if it takes them temporarily away from Twitter, they will eventually return to Twitter for more.

Another week of free-market capitalism gone by. Despite Apple’s bankruptcy 4.8% drop today, the SPX is about 28% above the horrific lows of late 2022, and a mere 7% below all-time highs.

CPI is not Cost of Living

Bourbon and Bubbles

Interesting take on bourbon and housing I came across…(highlighting is mine)

I know this is a bit of a stretch, but hear me out. I became interested in bourbon in approximately 2010; a family member had turned me onto Pappy Van Winkle. At that time where I lived, you could walk into most large liquor stores and find Pappy sitting on the shelves at MSRP; by bourbon standards it was very expensive and thus often went unsold. Within a few years bourbon (Pappy specifically) had started to gain a reputation but still remained available if you knew where to look. I think Anthony Bourdain (RIP) prominently featuring Pappy Van Winkle on his shows was the death knell of that bourbon, and by 2011-12 you really couldn't find it on store shelves anymore. Regardless, there were still tons of great, small-batch, limited-edition bourbons available for purchase at MSRP. Between 2012-2016, however, the popularity of bourbon really began to ratchet up, and bit by bit, bourbons which were once low-price daily drinkers were now popular and no longer showing up on store shelves. By 2017 I could still stumble onto some very good, limited allocation bottles on occasion, but since then even the bottles which would have been considered cheap, basic bourbons (Eagle Rare, Blanton's, E.H. Taylor small batch come to mind) are now near-impossible to find.

The irritating thing is that it's not because individual buyers like myself are out looking to pick up a certain bottle of bourbon. Groups of bourbon aficianados started sprouting up on facebook and instagram, and it soon became in vogue to procure massive collections of limited allocation bourbon. Whereas the bottles themselves were made to be opened and consumed, these limited allocation bottles were becoming commodities and even investments to some. A cottage industry around second-hand selling of limited allocation bourbons developed, and I realized that single buyers would visit every single liquor store in certain distribution areas, buy up every single bottle available of whatever limited allocation was available, and then sell them second-hand for profit or trade bottles with other collectors to "diversify their portfolio." Certain bottles were commanding huge price markups; Pappy Van Winkle bottles that MSRP'd for $100 were being sold for $1,000, then $2,000, and now in some cases $4,000 - and people were spending the money because they believed the hype! Soon the liquor stores caught on and realized there was profit to be made, and either they started reserving select bottles for their highest consuming customers, or they would mark their bottles up to the secondary prices themselves. If you go into a liquor store nowadays, especially in a HCOL city, often times you will see a display case filled with rare and limited allocation bottles, all marked up 5x, 10x, sometimes 20x, just looking for someone with more money than sense to benefit from.

What had been an enjoyable activity for me, to walk into a random liquor store and "hunt" for a limited allocation bourbon, had been destroyed by this brown liquid becoming a commodity, and I just stopped. I now have a collection of about 20 bottles that sits in my home, many partially consumed and many completely unopened; I haven't had a sip from any of these bottles for over 4 years, because once I finish a bottle, the likelihood that I will ever be able to taste that bourbon again without being price gouged is low. I probably spent around $1,000 on these bottles, all at or near MSRP; to sell them on the secondary market I could probably sell them for over $10,000. But I won't, because that's not why I purchased the bourbons. I bought them to enjoy, and they are no longer able to fulfill that purpose. There are hoarders out there with hundreds or even thousands of these bottles that they have bought up en masse, restricting the supply, and using them as "investments." Similarly, the bottles in the windows of the liquor stores just sit there, unopened and unconsumed, because they are too expensive. There are still some people out there (on social media at least) finding these bottles and enjoying them, but most of them either have a large amount of disposable wealth or an inside connection to facilitate their purchases.

Does this all sound familiar? To me it does. I thought bourbon was a bubble that would crash; I've been waiting since 2017 for people to lose interest and for the prices to fall, but nothing has really changed - the landscape of 2010-2011 is probably never going to return. It's supply and demand - the bottles that everyone wants are limited (on purpose) to drive up desirability and in turn this drives up the price. However, I do expect that things will ultimately change. Bourbon is like houses - it takes awhile to get new supply on the market. The manufacturers have responded to the increase in bourbon demand by increasing supply, but because of the aging process, it can take 10-15 years for that supply to hit the market. If that new supply comes online at a time when the population of bourbon drinkers is declining (people growing out of it, moving onto another spirit, dying of alcohol-related disease, etc), then all of a sudden there may be a glut of bourbon for sale, supply will far outpace demand, prices will crash, and the cycle will be over.

It's my two cents that this will be how the housing market plays out. Supply is constrained right now, with contributions from my generation (millennials) having young children and being in our peak homebuying years, the boomers refusing to sell and downsize, and the majority of homeowners being locked into their homes by crazy low interest rates. Things may stay this way for 10 or so years unless there is a major downturn in the economy (which could still certainly happen). But eventually, the glorification of home ownership (inspired by HGTV, Chip and Joanna Gaines and the like) won't be a thing, people will lose interest, and as the massive number of homes currently being built coincides with a declining population, the supply will outpace demand, and the market will fall back to earth, probably reverting to the mean. I don't foresee the massive price appreciation that our boomer parents enjoyed in their houses playing out the same way for our generations - you might make a little money, more likely you'll break even or lose some when accounting for inflation. But that's why homes are meant to be a place to live, where you spend your time and raise a family, just as bourbon is made to be drunk, not to sit on a shelf collecting dust.

Thank you for attending my TED talk!

Coincidentally, Meb Faber had a podcast this week with “Anthony Zhang, founder and CEO of Vinovest, which gives investors the ability to invest in wine and now whiskey….Vinovest now has over 100 million dollars invested and 150,000 registered users…we dive into their entrance into the whiskey market and talk about the investment profile of whiskey, how it compares to wine, and what else is in store for this rocket ship startup.”

We’ve financialized everything.

San Francisco Market Street, July 2023 Shocking. A failed state. You can find similar video of Los Angeles, Baltimore etc. The implications in this video for SF real estate - commercial and residential - are ominous.

America’s most-robbed Walgreens was the victim of at least three thefts within 30 minutes in July, according to CNN Senior National Correspondent Kyung Lah — one of the latest examples of brazen crime at the location. The thefts were witnessed during the filming of a televised report at the Walgreens in San Francisco’s Richmond neighborhood. According to Lah, Walgreens has identified this location as having the “highest theft rate” — hit more than a dozen times a day — of the pharmacy chain’s nearly 9,000 U.S. stores…Real estate investing expert Patrick Carroll said the commercial real estate market is tumbling toward a crash that could be as devastating as the 2008 crisis. “The party’s over, unfortunately,” he said. “The office market’s going to be destroyed, hotels are going to be destroyed — it’s going to be ugly.”

“An inescapable frustration seems to have imbued life in San Francisco,” said Fuller. “People feel frustrated and want change: They are tired of vandals and vagrants on sidewalks, police that are absent or too aggressive, ineffective city leadership, the expensive cost of living, and the continuing closure of longtime favorite restaurants, breweries, and shops.”

Houston: “You had players that came into multifamily that didn’t understand how to operate properties, so the bad deals came from speculation,” said Oney. “There’s a lot of talent and skill that goes into maintaining an apartment complex, keeping it up, promoting it, and some of the deals that have gone bad you saw people focused on the financing side, but they didn’t think about the operation side, and now they’re getting bitten because the property is less desirable.”

Nearly a Quarter of Homeowners Intend To Sell Their Home in the Next Three Years Hang on there - aren’t 90% of mortgages under 6%? I’m having cognitive dissonance.

I always hear people say, "Japan has been in deflation for years," but the reality seems much more like stable prices with a definite upside bias.

Apropos of nothing…

Jacob Williams: General Manager and CEO of Florida Municipal Power Agency The Biden Adminstration seems to want civilization to return to a pre-industrial level.

If you haven’t, I encourage you to try a 7-day free trial, or not - I’m not your dad. There’s a lot of stuff below the fold you may find interesting. Or go read through my old posts. It’s 27 cents a day, or - say I do only two posts a week - that’s 104 posts a year. 96 cents a post. Since each post is at least worth a dollar (though I’m biased), you’re actually making money by subscribing. This is not investment advice.

The Soft Landing®

I went off on a mini-RFK Assassination tangent the other day, because I think it is fairly certain that the shot that killed Robert F. Kennedy did not come from Sirhan Sirhan’s gun. Nobody cares.

Robert F. Kennedy Jr. explaining that his father was murdered by a CIA-affiliated security guard who worked for Lockheed, Eugene Thane Cesar, not Sirhan Sirhan.

At three inches from the right mastoid area, I discovered we had a perfect match of the tattoo pattern of unburned-powder grains on Kennedy’s right ear. At that distance, the shape of the entrance wound was also duplicated, and it accounted for the carbon particles found in Kennedy’s hair. I now knew the precise location of the murder weapon at the moment it was fired: one inch from the edge of his right ear, only three inches behind the head. But I also realized that this evidence seemed to exonerate Sirhan Sirhan. Eyewitnesses are notoriously unreliable, but this time their sheer unanimity was too phenomenal to dismiss. Not a single witness in that crowded kitchen had seen him fire behind Kennedy’s ear at point-blank range.

But even apart from the autopsy findings of a close-range wound, there was other evidence to challenge the belief that Sirhan Sirhan had acted alone. For example, four bullets were fired at Kennedy; three of them struck him, and one passed harmlessly through his clothing. Five persons behind Kennedy were also struck by bullets, which were recovered in their bodies. And three bullet holes were found in the ceiling. Thus, the tracks of twelve bullets were found at the scene, and Sirhan’s gun contained only eight. Police believed that the extra tracks could be accounted for by ricochets. But to the day he died (the victim of an assassin’s bullet himself), Allard Lowenstein, one of Senator Kennedy’s strongest supporters for the Presidency, said that Sirhan had not acted alone. And such professional homicide investigators as Vincent Bugliosi, the deputy DA who convicted the Manson killers, insisted there was a second gunman in the room.

What was the truth?

…the testimony of the most strategically placed witness is daunting. Karl Eucker, the maitre d’, led the Kennedys into the pantry. He was the man actually standing between Sirhan and the Senator. In fact, it was Eucker, not Roosevelt Grier or Rafer Johnson, who actually grabbed Sirhan and first wrestled him onto the steam table. Eucker was perfectly placed, and even years later he insisted, “I told the authorities that Sirhan never got close enough for a point-blank shot. Never!” Then he warned that an investigation of a second-gunman theory would get nowhere. “It was decided long ago that it was to stop with Sirhan,” he said, “and that is what will happen.”

"The fact that no official body has ever made the effort to honestly examine all the evidence in this case is nearly as chilling as the original crime itself, and points to a high level of what can only be termed government involvement."

We have now exposed the grand illusion. Sirhan could not have shot Kennedy. Indeed, there is a great deal of evidence to suggest that Sirhan was firing blanks. If Sirhan did not shoot Kennedy, who did? Why? And how is it that Sirhan’s own lawyers did not reveal the evidence that he could not have committed the crime for which he received a death sentence?

Before one considers the above issues, one larger issue stands out. If Sirhan did not kill Kennedy, how has the cover-up lasted this long? In the end, that question will bring us closer to the top of the conspiracy than any other. No matter who was involved, if there were a will to get to the bottom of this crime, the evidence has been available. The fact that no official body has ever made the effort to honestly examine all the evidence in this case is nearly as chilling as the original crime itself, and points to a high level of what can only be termed government involvement. In the history of this country and particularly the ’60s, one entity stands out beyond all others as having the means, the motive, and the opportunity to orchestrate this crime and continue the cover-up to this very day. But the evidence will point its own fingers; it remains only for us to follow wherever the evidence leads.

It has often been said that a successful conspiracy requires not artful planning, but rather control of the investigation that follows. The investigation was controlled primarily by a few LAPD officers and the DA. Despite Congressman Allard Lowenstein’s efforts, no federal investigation of this case has ever taken place. The Warren Commission’s conclusions were subjected to intense scrutiny when their documentation was published. Evidently the LAPD wanted no such scrutiny, and simply refused to release their files until ordered to do so in the late ‘80s.

- The Assassinations: Probe Magazine on JFK, MLK, RFK, and Malcolm X

Heritage Tri-State Bank: “We declared the bank insolvent because of a scam”

Heartland Tri-State Bank was a very small institution, with just $139mn in assets. It was purchased by Dream First Bank, a bank with $511mn in assets based in Syracuse, Kansas (and formerly known as First National Bank of Syracuse). But notably, the closure’s cost to the FDIC’s deposit insurance fund — $54mn — eclipsed the size of its entire $48mn loan book.

Here’s the bank’s website as of June 2023.

These next two charts are from Piper Sandler:

Average Weekly Hours

“Foreign Purchases of U.S. Homes Slump to All-Time Low” Foreign buying of U.S. homes fell for a sixth straight year, sinking to the lowest level on record

2023 International Transactions in U.S. Residential Real Estate

42% of foreign buyers paid all-cash (compared to 26% among all existing-home buyers)

50% of foreign buyers purchased a property for use as a vacation home, rental, or both (compared to 16% among all existing-home buyers)

Top Foreign Buyers

China (13% of foreign buyers $13.6B)

Mexico (11% of foreign buyers, $4.2 B)

Canada (10% of foreign buyers, $6.6 B)

India (7% of foreign buyers, $3.4 B)

Colombia (3% of foreign buyers, $0.9 B)

Top Destinations

Florida (23%)

California (12%)

Texas (12%)

North Carolina (4%)

Arizona (4%)

By region of origin, Asian buyers returned as the largest group of buyers, with a higher market share of 38%. Latin American buyers were the second largest group, with a 31% share. (Mexico is included in Latin America/Caribbean, although it is geographically part of North America). European buyers accounted for 14% of foreign buyers, while Canadian buyers alone accounted for 10%. Measured by the number of homes purchased, China returned as the top country of origin among foreign buyers during April 2022-March 2023, accounting for 13% of the number of homes purchased by foreign buyers (6% in the prior period). Mexico remained the second largest origin of foreign buyers, with an 11% share (8% in the prior period). Canada, which was the top country of origin of foreign buyers in the previous survey period, was the third most common, with a 10% share. India was the fourth largest foreign buyer, with a 7% share. Colombia maintained a 3% share…

Chinese buyers continue to have the highest average purchase price at $1.2 million, as buyers purchased in expensive states: 33% of Chinese buyers purchased a property in California, and 6% purchased in New York. Chinese buyers also had the highest median purchase price of $723,200, followed by Canadian buyers at $572,900. Canadian buyers were more likely to purchase in common vacation destinations: 55% purchased in Florida, and 14% purchased in Arizona. Mexican buyers typically purchased the least expensive properties, with Texas as the preferred destination…

The share of foreign buyers who made all-cash purchases was 42% compared to 26% among all buyers of existing homes…More than half of Colombian (67%), and Canadian (51%) buyers made an all-cash purchase, compared to just under half of Chinese buyers (47%). Asian Indian buyers had the lowest share of cash sales, at 15%, as most buyers (88%) reside in the U.S. and can obtain mortgage financing.

Private residential construction spending

With all of the MBA indices below, it seems we are roughly back to 1990’s levels.

MBA Mortgage Market Index

MBA Purchase Index

MBA Mortgage Refinance Index

30-Yr Mortgage Rate

United States Total Vehicle Sales

Equity Commonwealth (EQC) Q2 2023 Earnings Call Transcript

EQC is a weird REIT until recently run by Sam Zell. They’ve been selling their office buildings for years, building cash, and waiting for exactly the type of opportunities that should exist at times like these. However, they are up against a government that is excellent at can-kicking, and determined to keep failed business models going as long as possible - and, if not possible, maybe the taxpayer can take the loss.

Turning to the capital markets, things continue to be slow and our pipeline is modest. Transaction volumes are down across all asset classes, with just $35 billion in total investment sales for the second quarter or nearly 70% lower on an annualized basis. With so little trading, there has been limited price discovery and assets are difficult to value. To-date, there has not been a catalyst creating actionable investment opportunities. Owners do not want to transact at today’s pricing and lenders are often willing to work with the borrowers.

In terms of potential investments, we continue to evaluate a wide range of asset classes. We still like industrial and residential with operating conditions remaining relatively strong, though decelerating. For other asset classes, fundamentals range from decent to challenging and the lack of debt availability is a significant issue. Against this backdrop, it’s difficult to know where we might find a compelling opportunity to invest. A prolonged period of this challenging credit environment may create such an opportunity or perhaps it’s a large private real estate company that believes a deal with us is the best way to access the public markets. It could also be a business with a broken balance sheet or one that needs meaningful growth capital. We remain hopeful that such scenarios or others will be a catalyst for a transaction. In the meantime, we will continue to be patient. If we do not find an opportunity during this cycle, however long that might last, we will likely sell the remaining properties and return the capital.

Venture Capital

…Industry’s founder and CEO Hans Swildens told Venture Capital Journal earlier this week: “There is more than $130 billion of supply, and supply keeps building, but the bid prices are averaging 40% to 65% off net asset value, and this is holding back any sellers in the market from transacting.” - Grant’s

So “Net Asset Value” is probably the wrong number.

“everyone is hoping that the market will [rebound] so that they don’t have to acknowledge how far their portfolios have fallen.”

CRE

“It seems to be that CBD [central business district] office, in all our cities, New York included, has fallen victim to the same emotional and short-sighted view from the investment community.”

Spoken like a man whose stock chart looks like this:

On the other hand: “Firms that are launching today are taking the long view,” Institute for Portfolio Alternatives CEO and President Anya Coverman said, speaking generally about nontraded REITs. “That's what real estate investors do — they're not looking to time the market based on a cycle.”

Better call grandma and get her into “Nontraded REITs.” What could go wrong there?

Blackstone Inc.’s giant real estate trust for wealthy individuals saw redemption requests ease to the lowest point this year as it limited withdrawals for a ninth consecutive month.

Investors sought to cash out $3.7 billion in July from Blackstone Real Estate Income Trust, according to a letter Tuesday. BREIT returned about $1.3 billion, or about 34% of what was requested.

Withdrawal requests in July fell for the third consecutive month, dropping from the $3.8 billion that investors asked to pull in June. Since Nov. 30, when BREIT began limiting withdrawals, it has returned $9.4 billion to investors. The $68 billion Blackstone trust has been working through redemption requests that picked up last year.

(MF1 CLO, SASB = Single Asset Single Borrower, BX = Blackstone, LTV = Loan to Value, DSCR = Debt service coverage ratio)

When the Tides go out

Last summer, well before multifamily syndicator Tides Equities would show its troubled hand to investors, economists warned that the Federal Reserve’s rapid rate hikes could trigger a wave of defaults. Meanwhile, MF1 Capital, one of Tides’ favored lenders, was doling out loans like it was 2021.

The debt fund, led by Scott Waynebern, originated at least $7.4 billion in debt between 2020 and 2021, giving high-leverage loans to multifamily syndicators looking to act on aggressive fix-and-flip plans.

Though the loans were floating-rate, they were short-term, the benchmark federal funds rate was near zero, and most real estate players did not expect inflation, then dubbed transitory, to set off the Fed’s aggressive rate hikes. But industry observers say that by 2022, with the fight against inflation in the spotlight, a downturn was apparent to anyone willing to notice it.

“You could make an argument the writing was on the wall by the end of 2021, and especially the first quarter of 2022,” one Sun Belt-focused investor said. Through summer 2022, however, MF1 kept issuing floating-rate loans on deals that hinged on the ability to substantially raise cash flows. Now, across MF1’s almost $11 billion amortizing loan book, almost half of the deals are either watchlisted or delinquent…

In August 2022, the same month Fed Chair Jerome Powell acknowledged that higher rates would “bring some pain to households and businesses,” MF1 loaned Tides $55 million for a Phoenix-area acquisition.

The floating-rate loan on the property, Tides on Country Club, was made at 79 percent loan-to-value and a debt-service coverage ratio of 0.8, meaning that cash flow could not cover debt payments…

Worth reading the whole article above. I’ve been mentioning these “syndicators” recently, who enticed yield-starved small investors in recent years with the opportunity to buy multifamily at 3% cap rates. Now many small timers - assuming they haven’t been wiped out yet - are getting hit with “capital calls,” and probably more than a few are balking.

I’m reminded of a line from “The Big Short”:

If it's such a great trade, why are you offering it to me?

Crowdstreet

Developers pay fees to advertise their deals, and investors can buy slivers of equity for as little as $25,000. Sponsors of more than 770 deals have raised more than $4 billion on the platform.

A Wall Street Journal review of 104 completed deals and other deals that were aborted or still in process found that many failed to meet returns suggested in sales pitches. When developers fell short of funds, they asked investors to pony up more cash or risk losing their investments…The Journal analysis found that more than half of those investments promoted on CrowdStreet’s platform failed to meet their target returns. Hundreds of CrowdStreet users lost some $34 million on 19 deals that underperformed as of this July, according to the Journal’s analysis. A dozen of those deals lost nearly 100% of investor funds.

CrowdStreet also hosted successful deals. More than 20 deals outperformed projected return rates by at least 10 percentage points. Hundreds of others are still outstanding. It often takes at least three years before investors can realize a return on their investments…

CrowdStreet assessed Nightingale in its highest tier as an “enterprise” sponsor, indicating it had a national footprint and a portfolio worth more than $5 billion. The listing projected an internal rate of return of 28.1%, among the highest for a project on the platform. “All that kind of worked together to create a feeding frenzy around this investment,” said Peter Campbell, a Louisiana neuroscientist who put $100,000 into the deal last summer… [This high rate of interest reminds me of some of the crypto scams - RH]

“If you decide to steal $70 million, I’m sure if it was from Goldman Sachs they would think twice,” he said. “When you have a small and dispersed investment base, it’s much easier to think, ‘I’m going to misappropriate these funds and good luck to them.’”

The balance of distress in the U.S. commercial-property market rose to USD 71.8 billion at midyear, marking the fourth consecutive quarter of increase. Distress, which encompasses both financially troubled assets and assets taken back by lenders, outpaced workouts between property owners and lenders by about USD 8 billion during the quarter. Not since Q2 2020 at the onset of the pandemic has distress grown by as much in a single quarter.

Offices constituted more than 80% of the distress added during Q2 2023, with USD 6.7 billion of net inflows. By the end of June, the office sector was responsible for the largest share of marketwide distress, making it the first time since 2018 that neither the retail nor hotel sector was the biggest contributor.

Potentially distressed assets totaled USD 162.3 billion at the end of the second quarter. Not all potential distress leads to full-blown financial trouble: Of those assets classified as distressed at midyear, 35% had previously been deemed potentially distressed. In late June, federal regulatory agencies issued a policy statement on commercial-property loans and workouts, urging lenders to work with creditworthy borrowers who may be facing financial strain.

JLL, the world's second biggest commercial real estate brokerge, said its earnings dropped 99% as sales, leasing and financing declined because of higher interest costs hitting the industry.

U.S. bank regulators proposed a new set of rules that would impose stricter capital requirements on banks, requiring them to hold more assets for each loan they hand out and preventing them from using their own internal risk models. Though it will be years before a finalized rule takes full effect, it still discourages banks from the behavior that several sectors of CRE had depended on for years.

How Much Are Office Buildings Worth? A Scary Amount Less Than They Used To Hey, that’s Trepp’s headline, not mine. “Trepp used maturing office loans to make some estimates that ran between 52% and 60% loss.”

So who lent on all this commercial real estate?

So banks are the #1 CRE lenders, in spite of what I sometimes hear, #2 are insurance companies, with U.S. taxpayers coming in strong at #3.

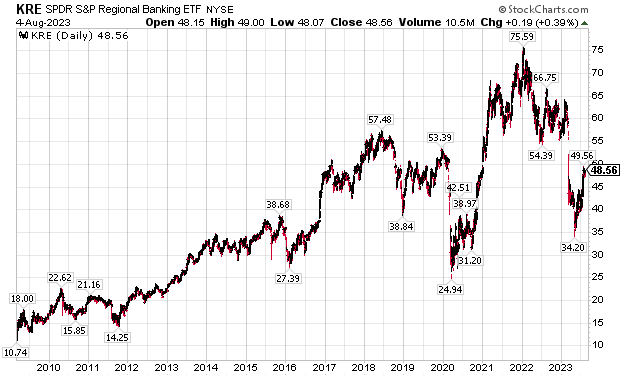

There are a few insurance company ETF’s. Their charts all look fairly similar, lower left to upper right, in contrast to, say, the S&P 500 regional banking ETF.

“More respondents believe cap rates are peaking”

This made my brain hurt. Via Grant’s…

Also from Grant’s:

Here’s JPMorgan CEO Jamie Dimon, commenting in a Wednesday CNBC interview on Fitch’s decision to trim its U.S. sovereign credit rating to double-A-plus from triple-A:

I would point out to the rating agencies if I could that there are a bunch of countries rated higher than us, like triple-A, but they live under the American enterprise military system. To have them be triple-A, and not America, is kind of ridiculous.

I always wonder - who the counterparty on U.S. credit default swaps, Deutsche Bank?

Anyway…

“Here Comes the Tsunami of Longer-Term Treasury Notes & Bonds: Monthly Auction Sizes +60% by August Next Year”

According to Power Failure, almost every time GE made a major decision that destroyed shareholder value, the obsession with manipulating earnings was front and center in the thought process. GE lost a lot of money in insurance, but why was a manufacturing company in the insurance business in the first place? Well, insurance companies offer a lot of accounting leeway, in terms of the way reserves are taken and assets are sold for profit, and could act as “shock absorbers” that let Jack Welch report smooth earnings when other divisions stumbled.

- Philo

One friendly but sharp-eyed commentator on Berkshire has

pointed out that our book value at the end of 1964 would have

bought about one-half ounce of gold and, fifteen years later,

after we have plowed back all earnings along with much blood,

sweat and tears, the book value produced will buy about the same

half ounce. A similar comparison could be drawn with Middle

Eastern oil. The rub has been that government has been

exceptionally able in printing money and creating promises, but

is unable to print gold or create oil.

- Warren Buffett, 1979

Thanks for another great read. If you replace the “H” with a “D”, you could sell a bunch of those T-shirts! While the distress in the Office sector and highly leveraged private syndicators get the headlines, other property types with “normal” leverage face the same refinancing gap mentioned above. As these loans mature, it will become evident; however, I am hearing reports of banks extending so they can avoid taking these problem assets. Much like the Fed loaning against long-dated securities at par when they’re worth substantially less. We’re so damn over-leveraged everywhere we can’t afford the purge that’s necessary.

Where in world do you find the time to put this all together 🙈! 🙏👍✅