Inflation is not a partisan issue, it's a class issue.

BLS "Hedonic-quality adjustments" are a comforting lie.

“Is there any good reason to believe that inflation

hits low-income households especially hard?”

- Paul Krugman, December 11, 2021

“The consumer’s not healthy,

especially at the lower income scale.”

Maybe stagnant wages wouldn’t matter as much if our Fed wasn’t so busy always debasing the currency.

CBS Poll analysis: If the economy is recovering, why don't people rate it better?

Maybe the economy is not “recovering” for most. Maybe “the data” is misleading.

Oh, the official explanation for the disconnect between data and sentiment is “the reason lies not so much with the pandemic as it does with partisans.”

Republicans are too hard on Biden, or something, but inflation doesn’t care whether you have a D or an R after your name.

Some angry comments on the CBS piece:

Maybe inflation - as reported by the BLS CPI model - is grossly understated compared to the real-world cost of living? Ever consider that?

Below are actual comments from registered Wall Street Journal readers back in 2015, when official CPI was sub-1%, and even NEGATIVE some months.

As I've shown many times, CPI is an understated nonsense model, but the point here is just look at the anger back then. Today, it's much worse.

Meanwhile, we get this crap:

There's a profound and peculiar national disconnect on the economy alright, but it's on the part of unaccountable, inbred, multimillionaire elitists like Paul Krugman.

My hypothesis is that much of the "the data" that people like Paul Krugman and Justin Wolfers study, and cite as fact - data which is often intentionally manipulated with subjective adjustments - does NOT accurately reflect the way most Americans perceive their economic condition to be.

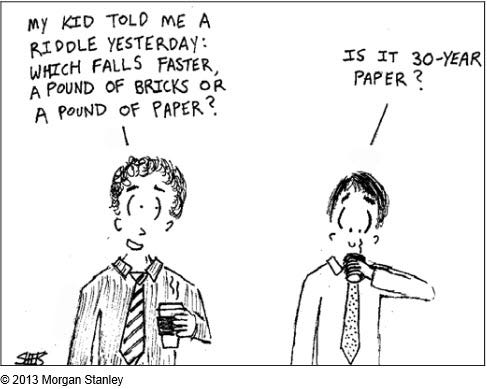

Hedonic-quality adjustments are a joke.

The way hedonic adjustments work is that the BLS says that something more expensive is actually less expensive, even though it’s more expensive, because it’s “better.”

This is how economists actually think, and why CPI is way below the actual "cost of living." For kicks, print this out and take it with you next time you go men's shirt shopping.

Here's a fun BLS "hedonic quality adjustment" lesson on how $1,250 televisions are cheaper than $250 televisions.

So, a $1,250 (admittedly much nicer) television is 7.1% CHEAPER than the old $250 TV, "after the quality adjustment is applied."

The BLS is saying that something that costs 5-times what an older model cost is actually 7.1% CHEAPER, and that's in the CPI.

For 25 years - according to the math geeks at the BLS - car prices in the CPI did not go up.

That is a huge lie, in plain sight, and no one ever mentions it.

Incomes are never hedonically-adjusted higher.

It doesn’t matter if your new car can do brain surgery if you can’t afford it.

No wonder Joe Six Pack is angry, while Paul Krugman thinks everything is great.

You: How much is this thing I need?

Cashier: It's $20.

You: But last year it was $15?

Cashier: Yes, but now it's cheaper because it's better.

You: But it's not cheaper. It's 33% more. It's $20.

Cashier: No, it's 50% better and $20.

You: What?

Cashier: Do you have an econ PhD sir?

You: Can I just buy the old one for $15?

Cashier: No.

”I think the data that we all think of, that’s…accurate?

I think it’s crafted. I think the government does nothing unintentionally.”

Wolfers: Do you see?

Yes.

Wolfers: The disinflation. Do you see?

Yes.

Wolfers: Average grocery prices are roughly unchanged over the last six months. Do you see?

Oh, my God.

Democratic Party Platforms 1972-1984

“There must be an end to inflation and the ever-increasing cost of living. This is of vital concern to the laborer, the housewife, the farmer and the small businessman, as well as the millions of Americans dependent upon their weekly or monthly income for sustenance. It wrecks the retirement plans and lives of our elderly who must survive on pensions or savings gauged by the standards of another day.” (1972)

“The economic and social costs of inflation have been enormous. Inflation is a tax that erodes the income of our workers, distorts business investment decisions, and redistributes income in favor of the rich, Americans on fixed incomes, such as the elderly, are often pushed into poverty by this cruel tax.” (1976)

“inflation still erodes the standard of living of every American.” (1980)

In the 1984 Democratic Party Platform they mention "inflation" 25 times.

People are trying to make inflation a partisan issue. It's not.

If anything, inflation - i.e., the cost of living spiking ever higher - is a class issue.

Those with lots of assets - especially leveraged assets - should do quite well. Everyone else will not.

Real median household income fell by 2.3 percent last year, according to the Census Department, the third year in a row of declining real incomes.

"All of their [Fed] minutes are fabricated to create a message, so it is all Kabuki theater."

- Mike Taylor

"Over the last 30-something years, the Fed has become like the rest of the economic organizations in Washington DC, where they're given an answer and they justify it."

- Former Fed economist and bond trader Alan Boyce, 2016, on Realvision

Jonathan Smoke, Chief Economist of Cox Automotive

“About half can only afford about a $400 a month [car] payment, and it is really difficult to produce a $400 payment in either the new or the used market today”

Two and a half years ago…

"...we want to see inflation move up to 2%. And we mean that on a sustainable basis. We don't mean just tap the base once. But then we'd also like to see it on track to move moderately above 2% for some time."

- Jay Powell, April 2021

It’s now been 2 1/2 years they’ve been well above their made-up “2% target.”

“The centrals banks desire to control markets is insatiable.”

“We have this really disconnected view of what’s really happening out there. It’s not good. There is too much inventory, but we have structural issues. Everything that’s being built is for people who don’t exist, meaning we don’t have enough Americans who can afford what’s out there on the road, in what I’ve seen...”

Highly recommended. Melody also writes on Substack. Here’s her latest.

“How about getting two houses with an friend and renting the 2nd house out for AirBB?”

AirBnb

Wow. Austin has 12,127 whole-home units listed on Airbnb (h/t NotoriousAirbnb)

“The remote workers have left, but the housing havoc they created remains”

I used to routinely go to the north GA and further into the Smokey Mountains. I’ve had a borderline obsession with Zillowing mountain cabins. 150k used to get you a smaller one, 250k for a cabin with everything you could ever want. Like everywhere else, they’re at 500k and up now. I’ve seen some triple in price. And this is in towns where they give you directions based on where the Walmart and Wendy’s are. I knew we peaked when one of my friends was promoting an AirBnB investing course for her Blue Ridge cabin rental.

For what it’s worth:

I stayed at a beach house a friend booked over Labor Day weekend and ended up talking with the agent that let us into the place. He said their bookings were down 60% compared to last Labor Day weekend and the house we got for $800 went for $2200 the previous year. Even better, I popped on realtor.com and the house was listed for $700,000 (there was a sale sign out front), down from 1.1mil 18 months ago. Drop after drop. I also realized that they were renting the garage for RV storage. Someone's taking an absolute bath on that place, and apparently a LOT of places in the tourist town I went to.

There’s apparently no housing supply problem in St. Louis

Land in areas that are not as in demand in north St. Louis will be dropped to as low as $500 for a building or pennies per square foot for a lot, according to a price list included with the proposal.

The previous pricing policy had not been substantially revised since 2011, according to the board meeting documents. Prices in the new policy under consideration are based on 2021 property valuations.

If approved, new prices for properties in the Hyde Park neighborhood will run as low as 18 cents per square foot, compared with more than $7 per square foot for the same type of site in Lafayette Square and other neighborhoods that are more in demand with developers and builders. Buildings or houses would be sold for $500 in most north St. Louis neighborhoods, compared with $1,000 in most north St. Louis neighborhoods under the prior policy.

“Why More Baby Boomers Are Sliding Into Homelessness”

A large portion of older adults now homeless have lived on and off the streets or in shelters during younger phases of their lives, often with mental illness or drug addiction…But researchers said about half of the homeless older adults they spoke to in Oakland, Calif., New York and elsewhere were unhoused for the first time after their 50th birthday and can point to a precipitating event that destroyed what had previously been a relatively comfortable life.

Those newly homeless were more likely to cite the death of a spouse or a medical emergency as the cause, and they often felt shocked—even betrayed—that they were homeless after thinking they had done everything right to earn a decent retirement, homeless advocates said.

Social Security payments are adjusted for “inflation,” but average rents don’t work for the BLS.

In Naples, a typical rental cost $2,833 in July, according to Zillow data. The average Social Security payment for retired workers and their dependents that month was $1,791, according to federal data.

One thing to note is that almost every single thing the Federal Reserve and government have done this century has been to try to make/keep real estate prices (and therefore rents) higher than they otherwise would be.

Also:

Yardi Systems and 18 property management companies were named in a federal class-action lawsuit accusing them of engaging in a scheme to fix apartment rents across the country. Seattle-based law firm Hagens Berman alleged in the suit that Yardi and the property management firms used Yardi’s RENTmaximizer tool to eliminate competition by automating rent increases. The suit alleges that the use of Yardi’s tools created a cartel of organizations that leveraged the tool to raise rents across their properties while keeping vacancies low.

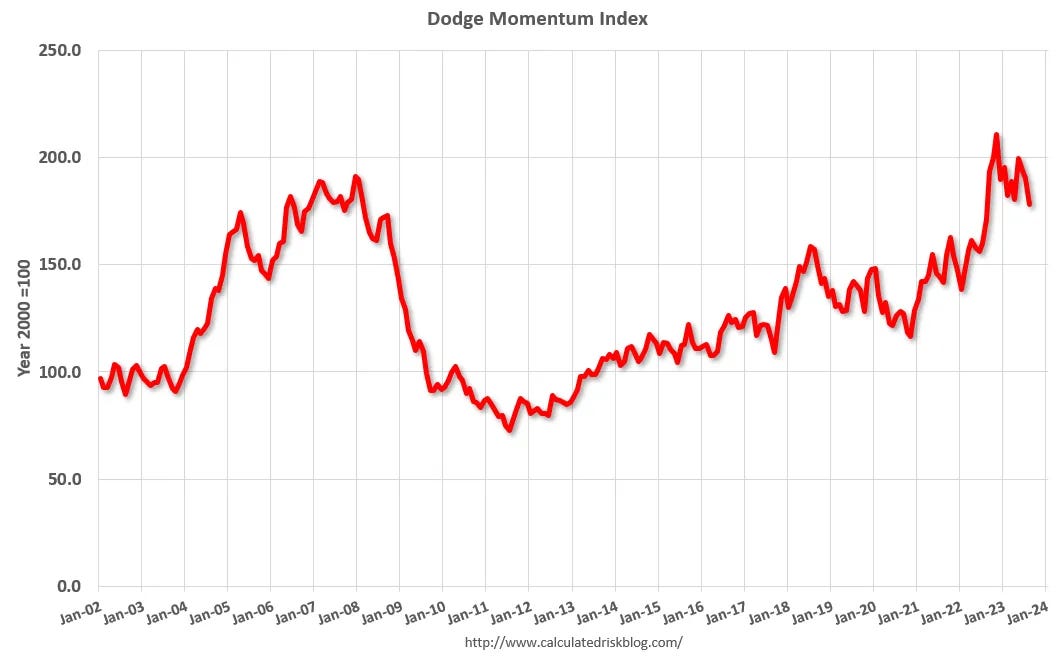

“According to Dodge, this momentum index leads "construction spending for nonresidential buildings by a full year". This index suggests some slowdown towards the end of 2023 and in 2024.”

“Help, I’m under water before making my first payment”

That quote reminded me so much of 2007.

“Property Ladder” was a hilarious show that just screamed “housing bubble.” Another fave a few years later was “Jungle Gold,” which was nothing but a series of bad ideas, one after another. Should be required viewing in schools.

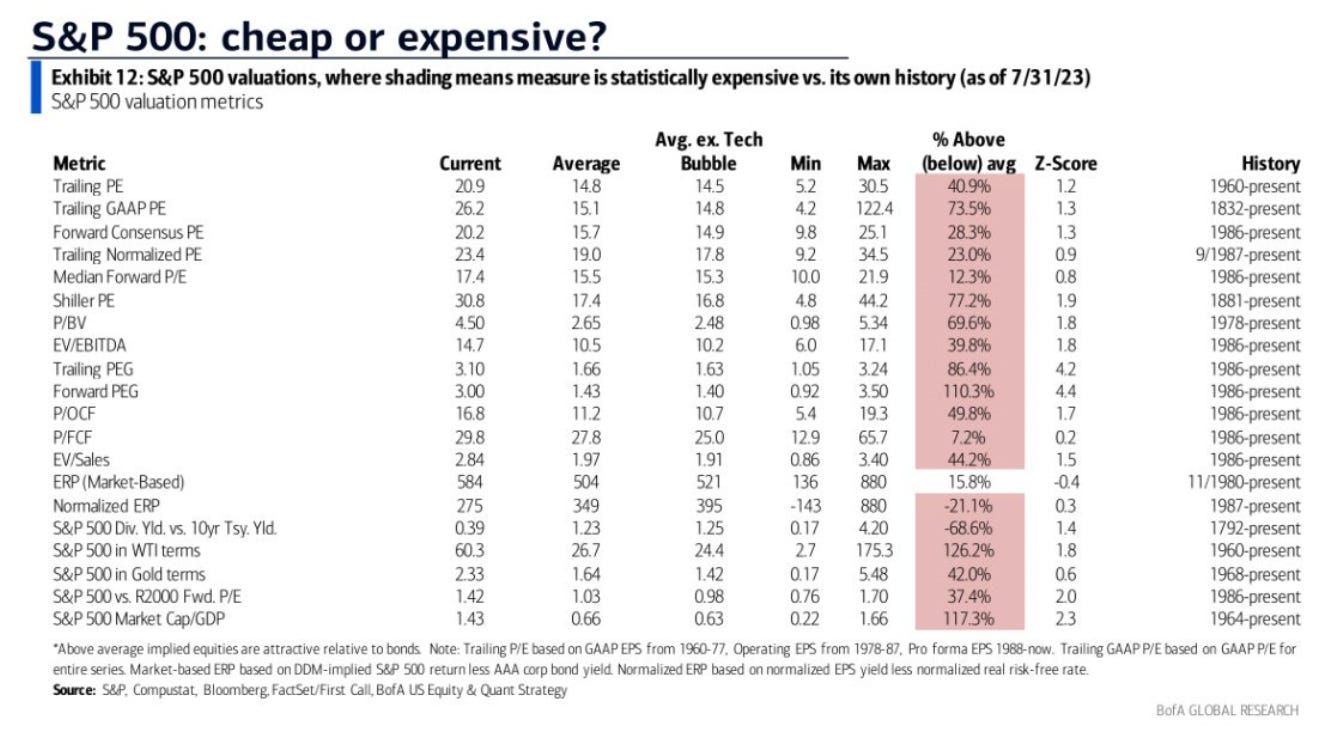

Maybe these S&P 500 valuations pencil out at 0% rates, but at 5%+?

“When your risk-free rate drifts higher, and all of a sudden it stays higher, then there’s a whole audience of stocks that have to be revalued.”

The S&P 500 index has declined by 20% or more 11 times since 1950

Odds of cash outperforming stocks

Frogs slowly boiling

Small Business Optimism

Twenty-three percent of owners reported that inflation was their single most important problem in operating their business, up 2 points from last month.

Owners expecting better business conditions over the next six months deteriorated 7 points from July to a net negative 37 percent. The net percent of owners raising average selling prices increased 2 points to a net 27 percent seasonally adjusted. The net percent of owners who expect real sales to be higher decreased 2 points from July to a net negative 14 percent.

FDIC Finds Selling Some Bank Assets Trickier Than Expected

Just last week, the FDIC announced that the $33 billion CRE loan portfolio that came out of Signature Bank’s failure this year was now for sale. But a Bloomberg report says that $12.7 billion in mortgage-backed securities that had come from Silicon Valley and Signature hasn’t been gaining traction with potential buyers…

Reportedly, the FDIC has considered different options. One would be to cut the prices to get the securities to move [what a novel idea! - rh]. Another would be repackaging the debt into new “more complicated instruments,” although it is hard to see how that could fundamentally change the market realities. The mortgages wouldn’t suddenly throw off more cash, although perhaps the idea is to break them up and repackage them with a mix of securities that are currently more valuable to get a better average price. [make it easier to confuse buyers? - rh]

KBRA releases a report on the magnitude and change in distress rates of the largest metropolitan statistical areas (MSA) in U.S. private-label commercial mortgage-backed securities (CMBS) 2.0 between June 2022 and August 2023. The study population includes nearly $600 million of collateral across KBRA-rated and nonrated conduit, single-asset single borrower (SASB), and large loan transactions…

Key observations from the report are as follows:

The distress rate across the 20 largest markets was 7.2%, which is slightly above the national CMBS 2.0 rate of 6.8%.

Seven of the top 20 MSAs had a rate under 2% (Orlando, San Jose, Phoenix, Miami, Boston, Seattle, and San Diego).

All but one MSA experienced an increase in office distress rates; conversely, lodging rates decreased in 16 of 20 markets. Retail, multifamily, and mixed-use assets exhibited varied performance across the 20 markets, while only three markets (New York, Chicago, and Philadelphia) have distressed industrial loans.

The MSAs with the highest distress rates by property type include New York (retail, 17%), Denver (office, 40.2%), Houston (mixed-use, 75.5%), and San Francisco (lodging, 59.3%; multifamily, 22.7%).

“I think the conversation that GP’s (general partners) are having with their LP’s (limited partners), and that people should be having, is ‘would I rather do a capital call, or would I rather sell for 85 cents on the dollar, 70 cents on the dollar' - whatever the number may be.’” - Old Capital Podcast

Apparently just a 3% chance of a Fed hike next week, according to traders…

Euro Area Interest Rate (ECB)

Euro Area Official Inflation Rate

Real rates are still negative in the EU.

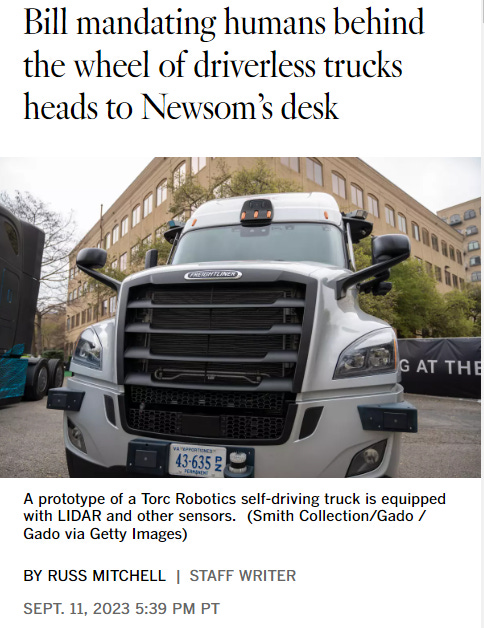

“Driverless” trucks with…backup drivers?

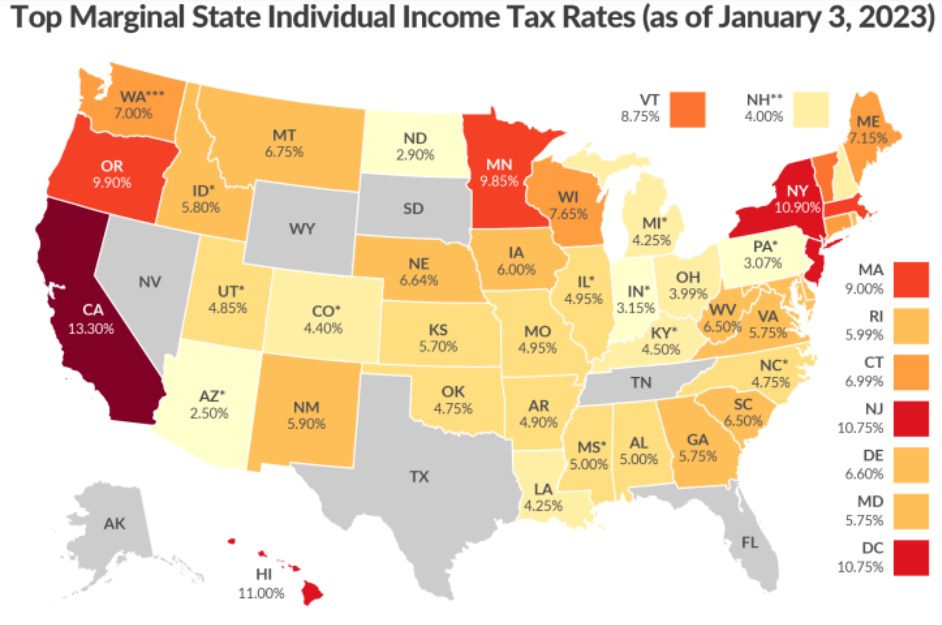

Yesterday I learned that Tennessee has no income or capital gains tax.

I live and grew up in Tennessee. It's mind-boggling to see some of the jumps in housing costs. I've seen a house jump from $50,000 in bfe nowhere to $300,000! It's ridiculous. Some of these houses last sold in 2022 for that much, and they're expecting 200-300,000 for them. Not to mention, some people want $200,000 for a house that is literally falling apart at the seams. Heck, I walked into a house where every room tilted a different direction, and the brick had collapsed and been put back up due to foundation issues. It sold for $250,000. That price might not seem like much to some states, but here that used to be a very nice house with a big yard, now it might get you a house with foundation issues. Yeah you might still be able to get something really nice further out, but there is no cell service, no cable, you might be on well water, and you will be in the middle of nowhere. With the average household income of $65,380, most locals are being priced out. You can see evidence of that in a lot of local businesses. I haven't been to a restaurant recently that hasn't had some staff shortages. Some of that might be people not wanting to work in a restaurant anymore, but I can't blame them. We're probably gonna see that in a lot of areas that locals have been priced out of by retirees or remote workers because no one is going to be willing to drive over 40 minutes to get to a job they will be spending most of their income on the gas to get there. Things are getting interesting here, and I'm not sure what it's going to take for things to correct.

"I really believe bond holders are going to be the sacrificial lambs of this terrible fiscal situation we’ve gotten ourselves in." - David Hay

“Why did we do the bailouts?” she went on. “It was all about the bondholders,” she said. “They did not want to impose losses on bondholders, and we did. We kept saying: ‘There is no insurance premium on bondholders,’ you know? For the little guy on Main Street who has bank deposits, we charge the banks a premium for that, and it gets passed on to the customer. We don’t have the same thing for bondholders. They’re supposed to take losses.”

German scholar Victor Klemperer's early 1920's diary entries: "Germany is collapsing in an eerie, step-by-step manner."

Via author Richard J. Evans.

Not untypical was the experience of the academic Victor Klemperer, whose diaries offer a personal insight into the larger sweep of German history in this period. Living very much from hand to mouth on temporary teaching contracts, Klemperer, a war veteran, was pleased to receive a small additional war gratuity in February 1920, but, as he complained, ‘what was earlier a small income is now just a tip’. Over the following months, Klemperer’s diary was increasingly filled with financial calculations as inflation gathered pace. Already in March 1920 he was encountering ‘foragers, little people with rucksacks’ on the train outside Munich. As time went on, Klemperer paid increasingly fantastic bills ‘with a kind of dull fatalism’.

In 1920 he at last gained a permanent appointment at Dresden Technical University. But it did not bring financial security. Each month he received an increasingly astronomical salary with back payments to make up for inflation since the last payment. Despite receiving nearly a million marks’ salary at the end of May 1923, he was still unable to pay his gas and tax bills. Everyone he knew was working out how to make money speculating on the Stock Exchange. Even Klemperer had a try, but his first gain, 230,000 marks, paled into insignificance in comparison with that of his colleague Professor Eorster, ‘one of the worst anti-Semites, Teutonic agitators and patriots in the university’, who was said to be making half a million marks a day playing the markets.

A habitué of cafes, Klemperer paid 12,000 marks for a coffee and cake on 24 July; on 3 August he noted that a coffee and three cakes cost him 104,000 marks. On Monday, 28 August Klemperer reported that a few weeks previously he had obtained ten tickets for the cinema, one of his main pleasures in life, for 100,000 marks. ‘Immediately after that, the price increased immeasurably, and most recently our 10,000-mark seat has already cost 200,000. Yesterday afternoon,’ he went on, ‘I wanted to buy a new stock. The middle rows of the stalls already cost 300,000 marks’, and these were the second cheapest seats in the house; a further price increase had already been announced for the following Thursday, three days later. By 9 October he was reporting: ‘Our visit to the cinema yesterday cost 104 million, including the money for the fare.’ The situation brought him, like many others, to the brink of despair:

‘Germany is collapsing in an eerie, step-by-step manner…The dollar stands at over 800 million, it stands every day at 300 million more than the previous day. All that’s not just what you read in the paper, but has an immediate impact on one’s own life. How long will we still have something to eat? Where will we next have to tighten our belts?’

“The study of history is a powerful antidote to contemporary arrogance. It is humbling to discover how many of our glib assumptions, which seem to us novel and plausible, have been tested before, not once but many times and in innumerable guises; and discovered to be, at great human cost, wholly false. It is sobering, too, to find huge and frightening errors constantly repeated; lessons painfully learnt forgotten in the space of a generation; and the accumulated wisdom of the past heedlessly ignored in every society, and at all times.”

How the Toadies Turned a Lovely Texas Lake Into a Ghostly Song

I’ve camped at Possum Kingdom Lake.

Boy you sure pack a lot of material into each of these posts!

I subscribe and/or follow a lot of substacks but I always save your writings for last because they’re too good to end too soon