It doesn’t matter what you pay!

If you've got kids, you think of the world differently.

“One of the things about securities fraud lawsuits is they don’t tend to happen until people have lost money from them.”

GMO’s Ben Inker on Realvision, 2020

“A KPMG report on how A.I. is being used by businesses across the world exaggerated adoption of the technology with bogus case studies that appear to have been based on AI hallucinations.”

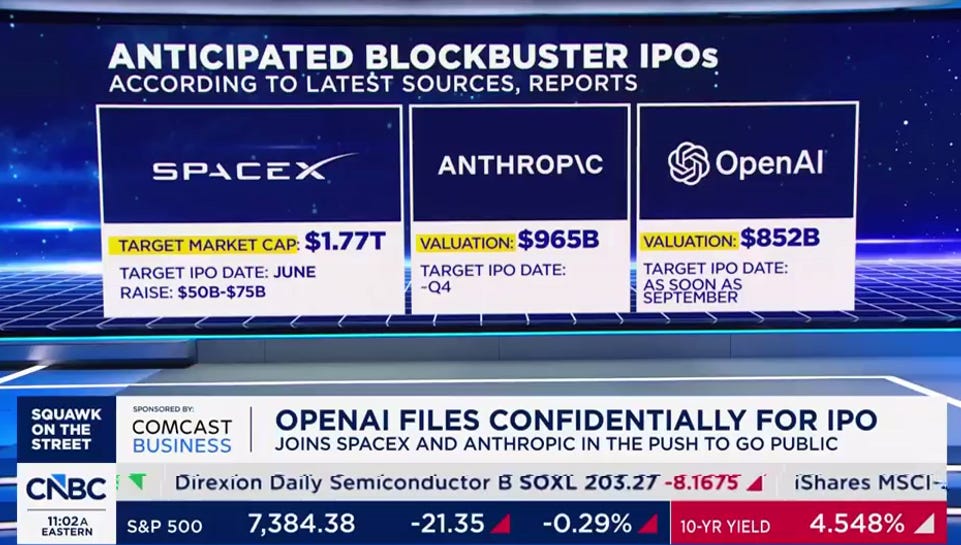

A trillion dollars used to be a lot of money.

The numbers involved with these IPO’s is staggering, $1.819 TRILLION just for these three by my math.

That’s equal to the amount of mortgage-backed securities the Fed bought using fun coupons from 2013-2022!

An unimaginable number.

OpenAI loses money on every deal, but they make it up in volume!

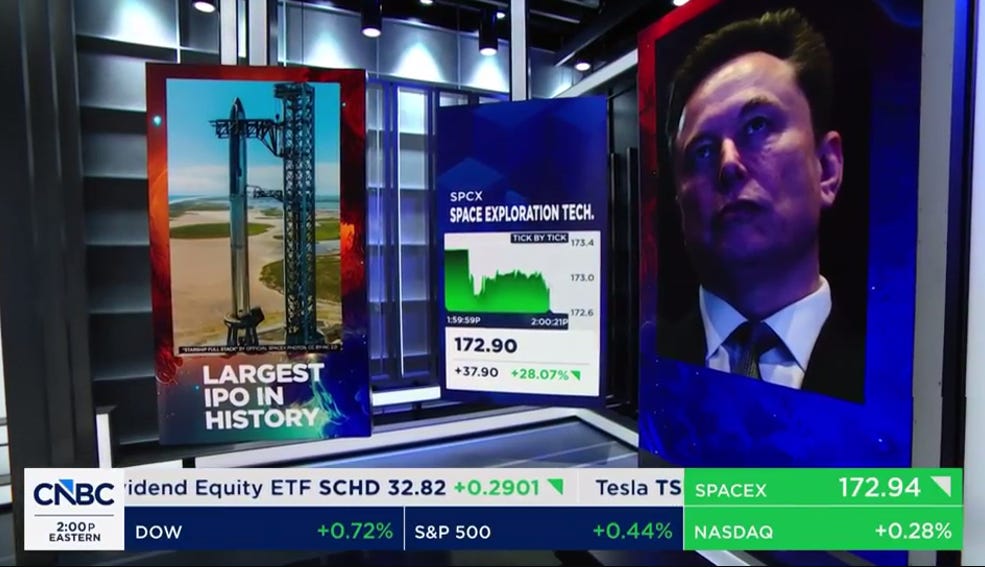

If SpaceX’s valuation hits $3 trillion, it’ll be equal to the amount of fun coupons the Fed squirted into Wall Street in just 3 months in Spring 2020.

An unimaginable number.

“The massive write-downs of goodwill by Nortel Networks and JDS Uniphase begin to suggest how far from viability it is possible to wander. In the case of JDS, $ 44.8 billion of acquisitions made during “The Fabulous Decade” (to borrow the title of a new book on the 1990s by Clinton Fed appointees Alan Blinder and Janet Yellen) turned out to be worthless.”

Jim Grant, Mr. Market Miscalculates

The Money Crisis, Its Causes and Remedies by Alfred Yaple (1873), a book on the Panic of 1873, which Yaple blamed largely on the post-Civil War use of paper money.

Plus ça change, plus c'est la même chose.

“Such issues being superabundant, lead the people into feverish schemes of wild speculation and enterprises, to carry out which they issue their promises based upon the anticipated gains of such undertakings. They call these promises “stocks,” etc.; and all are soon deceived by the supposition that such debts are wealth…”

“The almost daily contraction and expansion of the value of such promises, as compared with coin, tempts to “betting” on the value upon a given future day, which buying and selling “short” simply is. Combinations —” rings “—are then formed to affect values at given times, from which real interests suffer. More grain and pork, gold and produce of all kinds, are, in form, bought and sold than there is in the land, the parties never expecting to deliver or receive any of the article, but only to pay or take the difference between the contract and the then market price. With a fixed measure of values, fluctuations would be too little to admit of heavy gambling. But, with the credit standard, all real business, that founded upon the actual gold and property of the country, is at the mercy of such gamesters, when the actual property of the land, affected only by the laws of supply and demand, ought to regulate markets.”

“…people under such circumstances always become more extravagant. This extravagance reaches the producing classes as well as others, while many turn mere gamblers, cloaking their real calling under the respectable appellation of business. But sooner or later the system must fail; a settlement forces itself; a crash is the result, and suffering, misery, and ruin are wide-spread and everywhere.”

“They therefore cherish the delusion that, in the given instance, their affairs are exempt from the operation of inevitable and unchanging laws. But, after the system of anticipating or borrowing from the future has been carried beyond reasonable limits, then every new resort to it by issuing further promises produces immediate and very observable evils. Such additional promises merely lessen the purchasing power of the aggregate mass of promises already out to an amount equal to the increased issue, and nothing is really gained in the present, while the burden for the future is increased just so much. This is not the case so long as the limit to which debt may be safely incurred, has not been reached. One terrible consequence follows—the best part of the productive classes are immediately injured.”

“I hasten to laugh at everything, for fear of being obliged to cry.”

Pierre Beaumarchais, The Barber of Seville

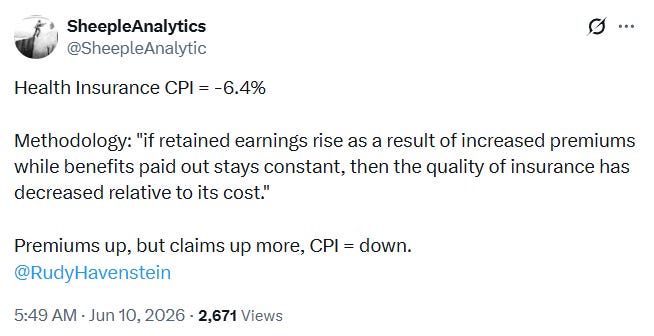

“Core” CPI (ex-food and energy)

Health insurance went down??? CPI is a cruel joke.

Here's Arthur Burns, the previous Jerome Powell, in September 1987.

This was back when central bankers (allegedly) had an "abhorrence of inflation," whereas today's clowns want inflation, the cruelest, most regressive tax.

“In monetary policy central bankers have a potent means for fostering stability of the general price level. By training, if not also by temperament, they are inclined to lay great stress on price stability, and their abhorrence of inflation is continually reinforced by contacts with one another and with like-minded members of the private financial community. And yet, despite their antipathy to inflation and the powerful weapons they could wield against it, central bankers have failed so utterly in this mission in recent years. In this paradox lies the anguish of central banking.”

“Statements in favor of a 2% target were non-existent before 2007”

“From around 2000 until the Great Recession, there was general consensus among participants that their inflation target should be about 1½%, significantly below both average inflation over the period and survey measures of longer-run inflation expectations.”

“Our basic trouble was not an insufficiency of capital. It was an insufficient distribution of buying power coupled with an over-sufficient speculation in production. While wages rose in many of our industries, they did not as a whole rise proportionately to the reward to capital, and at the same time the purchasing power of other great groups of our population was permitted to shrink.”

Franklin D. Roosevelt, May 1932

NFIB Small Business Economic Trends, May 2026

Part of the economy is on a sugar rush – almost all related to A.I. investment spending and it’s flying high. The stock market is posting new highs, but again, mostly due to that one soaring sector. Meanwhile, gas prices have spiked reflecting a reduction in the global oil supply, but also the risk premium that war has produced. Oil is a cost component in just about everything, so its rising price shows up in just about everything. A net 36% (seasonally adjusted) of the owners reported raising their selling prices, well above the historical average of net 13%. This leads right into CPI inflation, which is too strong to give the Fed license to reduce rates. It may even consider raising its policy rate.

The employment picture looks increasingly gloomy, as job openings continue to decline. Openings fell to 2020 levels as did hiring plans— recession numbers without a recession. Sales prospects are not strong, but not falling apart. Perhaps the economy is becoming bifurcated, one piece driven by AI spending, rising asset prices (e.g. stocks) and spending by higher income consumers benefiting from AI, while the other piece suffers from rising costs.

Uncertainty is the enemy of growth and investment, and it is high. Much is related to the Iran War and its impact on the global oil supply and other commodities, the sooner it’s resolved, the quicker some “normality” will be restored.

Xi Jinping to the rescue! As the Iran war serves to choke off a material chunk of global oil supplies, downshifting demand from China serves to keep a lid on global energy costs: the Middle Kingdom imported 7.82 million barrels per day (mbpd) in May per freshly released customs data, down from 11.6 mbpd on average last year to mark its lowest single-month total since October 2017. For context, the Strait of Hormuz’s de-facto closure serves to eliminate some 15mpbd of global supply, natural resource investors Leigh Goehring and Adam Rozencwajg estimate.

“China’s backing off from the crude market has played a crucial role in attempting to rebalance the global market [and] cap oil prices,” Warren Patterson, head of commodities strategy at ING Group, told Bloomberg. “The extent of [this downshift] has taken most of the market by surprise.”

In a rare moment of inter-hegemonic harmony, the world’s other economic superpower likewise works overtime to balance the supply-versus-demand equation: U.S. crude exports reached a record 5.6 mbpd in May, according to the Energy Information Administration, up 7.6% on a sequential basis and 56% year-over-year. Thanks to ongoing releases from the Strategic Petroleum Reserve, meanwhile, domestic oil stocks fell to 433.7 million barrels on May 29. That’s down 8 million barrels from the prior week (double the average estimate from Reuters-surveyed analysts), bringing the total war-related drawdown to 63.9 million barrels.

How much longer can the Sino-American balancing act persist? “Sometime in the next few weeks we will reach a level where the U.S. can’t go much lower,” warned Richard Joswick, head of oil pricing and trade flow analytics at S&P Global Energy CERA, in a June 4 webinar.

Stocks at the Cushing, OK. storage hub – the delivery point for West Texas Intermediate crude – ebbed to 22.4 million barrels, approaching the 20 million figure which represents the facility’s operational minimum. Below that threshold, “there is not enough oil to pump out and transfer between tanks and blending becomes a challenge, which could delay or cut outbound flow of oil from Cushing,” Jeremy Irwin, global crude lead for analytics firm Energy Aspects, told Reuters on Saturday.

Even a prompt return to the pre-March status quo would leave the world oil market in a hole. Some 500 million barrels of crude and refined products will be required to replenish global stockpiles used since the U.S. and Israel attacked Iran on Feb. 28, a recent analysis from S&P concludes. For each day that the conflict persists, that figure grows by a further 5.8 million barrels.

Delinquencies Down? Not So Fast...

A Conversation with Bill Moreland from BankReg Data (April 6) Love this guy.

On FDIC-insured bank loans to NDFI’s (non-Depository Financial Institutions.:

“To be charitable, these loans aren't traditional, right? Some of these things are difficult to classify. Maybe that's by design, maybe that's as a result, but, net net, what's happening is these NDFIs are eating the call reports. I mean, some banks now are upwards of 40%, 45% of their loan book is NDFIs, and we really don't know what they are, right?”

Very insightful paragraphs here:

“The problem is we had scraped down into the bottom of the barrel, so where do you lend? Well, lo and behold, $5 trillion of new money gets dumped into the system in 2020, 2021, and 2022.

So to give you a reference point, we had $14.5 trillion of deposits in the U.S. banking system at the end of 2019, $14.5 trillion. So all the money that comes in, whether it's earnings, or it's inheritance, or just all the money that flows, flows into a bank. Well, within two and a half years, the number climbed to $20 trillion. So if you wonder why everything's 35% more expensive, it's monetary. We want to call it supply chains, and I'm not saying supply chains weren't part of it during that time, but it's money, right? We printed 35% more money and 38% more money and dumped into the system.

So my wife keeps saying, is housing going to come down so we can get a second house in our retirement? I'm like, no, because it's already in the system. Unless you have value destruction, and we start destroying that money, it's in the system, right? Everything's going to be elevated. The problem for banks is they now had to do something with that money. So the ones that didn't have a history, and we kept interest rates at zero for a mighty long time, which means we raised a whole generation of people who were 34, 35 years old that had never lived in non-zero [world].

So at the time that we threw a bunch of money in the system and depressed risk, we basically threw a bunch of money and said, you got to go do something with it. So what ended up happening was a huge amount of lending that took place. But banks aren't stupid. They knew that they were already at the bottom of the barrel. (But what happens when you get rid of, hey, you don't have to make student loan payments? Is student loan payments a political issue? No, it's an economic issue. When everybody fills up their cup of debt, their ability to service debt, right, to pay their minimum payments, when you fill that up, economic growth stalls.

So what do we do? We empty people's cup of debt, right? And you do it by suspending mortgage payments, suspending rent, suspending student loan. So you emptied out everybody's cup of debt. But what you also did is you wiped out all the negative credit events on the marginal buyer. You no longer had delinquencies. You no longer had charge-offs. So just at the time we printed all this money and said, banks got to do something with it, everybody's credit scores, businesses and consumers started to get better. Great, we can go lend to them. Lend them some more money. And it's what we call the artificial consumer. It was fake.

And so what ended up and happened is that gave us two and a half, three years of great growth. But once again, we're back to the bottom of the barrel. So why am I bringing this little history lesson up? NDFIs are a way for us to continue to have banks lend to people they wouldn't normally lend to.”

What’s happening is a lot of financial engineering is taking place to try to buy time out of this.

“I've got NDFI clients, right? I got people on all sides of this. They say, you keep talking about how Wells Fargo and Bank of America modifying tons of loans. I got three hotels, each one of them $6, $7 million in loans, and they're not working with me. I keep telling them this ain't working.

And I'm like, stop making payments. The reason they're not working with you is because you're paying. But what happens is - and I'm not an advisor - but sure enough, a couple of months later, they call back up. I'm like, ah, I want to hear the story. They're like, oh yeah, all we did was threaten to stop making the payments, and they automatically lowered our payment. So I ask them, hey, are those hotels going to work now with your lower payment? No. They need about a 35% to 40% reduction on the loan for it to work. So eventually, but we're trying to sell them. So I think what's happening is a lot of financial engineering is taking place to try to buy time out of this.”

“So what they did in 2024 Q1 was we changed the rules around what we call a loan modification. The big bank lobby, the BPI, the Bank Policy Institute, lobbied FASB to change the rules in FASB. And I'm old enough to remember GAAP only. I'm old enough to remember back in the early 90s, we weren't taught non-GAAP, right? So if we think FASB is the arbiter of honesty and truth, I think those boundaries get pushed because of lobby.

So FASB changed the rules and said, there's no longer a life-to-date Ferris wheel. You get on, you make 12 payments, you get off. Well, that's pretty clever. Bill Moreland at Wells Fargo in the 90s would have loved that rule, almost like Bill Moreland in the 90s would have designed the rule that way. Because now what's happening is you're lowering payments, but no one ever knows it. And if you do it the right way, for everybody that gets off the Ferris wheel, you add another group. So your modifications look like they're 1.5%, 2%, 3%, but in reality, they're upwards of 6%, 7% cumulative.

So I think Bank of America is, and I can make a pretty convincing case, not 8.5%. They're close to 11% to 12%. And that's a completely different perspective. But here's the problem. If you look at the rules, it sure looks like the rules allow for serial loan modifications, which is what we're seeing now.”

If you’ve got kids, you think of the world differently.

“Look, I've got kids, right? And if you've got kids, you think of the world differently. And I don't know how, on one hand, you solve an overvaluation problem without value destruction. And that's really what we're talking about here. I mean, every asset class is overvalued. And you can say, well, it's not overvalued. Dude, paying 38, 40 PE on Microsoft, that seems rich to me. But basically, on one hand, we need value destruction. We do. But we don't want to take that. But on the other hand, we all want our kids to be able to buy a house. We all want our kids to be able to get married. We all want our kids to be able to get a job. And so I can flat out tell you, I see the world through my lens. Kids are having a much harder time finding jobs. And I'm talking computer science kids. I mean, we have a ton of them in our house always. I'm talking aerospace engineers coming out of Purdue. I mean, these are pretty high-level kids, right? They're struggling.

And so what is happening is, I think we're going to avoid a 2008-9. They will do everything they can to avoid this. We cannot have value destruction. Well, stop overvaluing. Stop inflating everything, and this won't happen. But they don't want to do that. But the other flip side to this is they won't let that happen. But we're going to have an economic malaise. So my thing is, I used to say, hold on. 2024, it's going to happen. Hold on. 2025, it's going to happen. Now, I'm pretty much going to say, look, I think we're going to have an economic malaise of not a lot of economic growth while we grow into these valuations. And it could take five years or seven years, right?”

There’s a coordinated effort to give the perception that things are getting better

“Don't be afraid to take some risk, right? But don't make those decisions based upon anything you read in the Wall Street Journal or CNBC or American Banker or Bloomberg that, hey, delinquencies are magically getting better in consumer and commercial real estate. Go lend in commercial. It's what I call the wealth effect for chief risk officers and chief lending officers.

There's a coordinated effort to give the perception that things are getting better and they're much better, and they're using data, manipulated data from the largest banks, to make the case. So I get $10, $12, $15 billion asset banks that call me up. They say, man, you're the Pied Piper of doom. I'm like, I don't want to be a Pied Piper of doom. I hate that. But they're like, you're so negative, not in a bad way. You're cautioning us, but you're skeptical of what's going on in commercial real estate. But we look at the national numbers that delinquencies look like they're getting better. We look at our local market. We look at our book. I think we want to lend more.

And what I'm saying is, is if two of those numbers are manipulated, be careful, right? That's it. Is not saying don't, but if you're hearing things that are trying to reinforce what you're kind of wanting to do, understand that somewhat of the story is very much a manipulated story. If we're modifying 38% of mortgages, a second or third time, housing is not as great as we think it is, right? And finally, exposing your borrowers to interest rate risk is also another problem that should rates go up.”

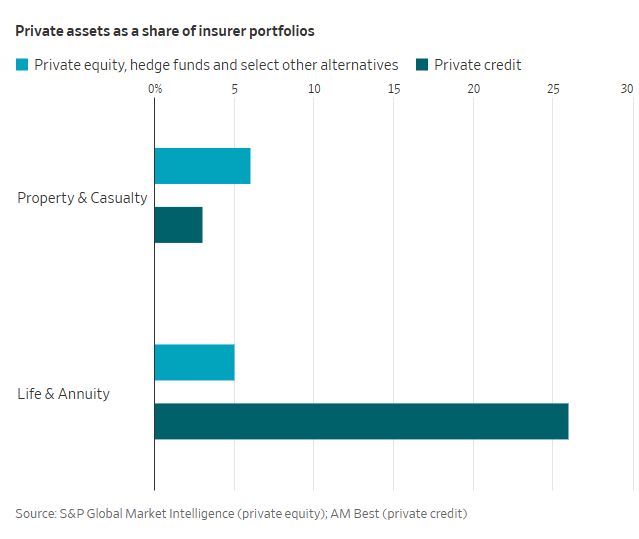

Property Insurers Are Piling Into Private Assets, as Other Investors Hit Pause

Home and car insurers are joining other deep-pocketed institutions from life insurance companies to university endowments in snapping up private investments. They are late to the party…Property and casualty insurers’ moves into so-called alternative investments have picked up just as many pensions and endowments have started to question whether the returns those funds can generate will be as attractive as they have been in decades past.

From the comments: “six or seven years from now we will be reading about how insurance carriers got caught short and needed to be bailed out because they didn’t have the funds to pay claims.”

‘Rent now, pay later’ loans target US consumers squeezed by housing costs

Fintech groups are seeking to capitalise on the growing number of Americans who struggle to pay for housing, offering “rent now, pay later” loans as the cost of living pushes up demand for short-term financing.

Affirm, a Nasdaq-listed company that is one of America’s biggest “buy now, pay later” lenders, recently partnered with fintech Esusu to pilot so-called rent-split loans. Three other companies that specialise in these housing loans told the FT that their customer bases were rapidly expanding.

Rent-split lenders cover a tenant’s monthly payment to their landlord and receive the money back in instalments spread over the course of the month, in effect splitting up the borrower’s rent bill into smaller sums.

Wemimo Abbey, co-founder of Esusu, said the loans serve a growing number of people who work freelance or gig economy jobs with irregular pay schedules. “People can make [rent payments], it’s just the timing,” he said.

“Recent inflation has been really sticky, but incomes are not going up,” Abbey added. “So that’s what makes us think this is going to be a massive, massive market.”

Freddie Mac is auctioning off 1601 Royal Crest Drive in Austin, which features multiple apartment buildings, on June 24. The starting bid for the auction is $9.5 million.

The previous owners, Mia Riverside, allegedly defaulted on a $50.2 million loan granted in March 2024, which the mortgage giant subsequently took over. Freddie Mac foreclosed on the property and won it at a January foreclosure auction with a $50 million bid, according to the Austin Business Journal. The complex on the site holds 526 apartment units, and is completely vacant, according to the publication.

Melody Wright

“I needed to go out and prove my theories to myself of what I thought was happening, and that’s when I took my first road trip. So, you asked me what did I learn, John? You know, this time around, it’s important because what I learned last time around is that the data does not match reality in any way, shape, form, or fashion. And

I couldn’t understand why the permits didn’t match. I couldn’t understand why the listings for sale didn’t match. I couldn’t understand why there were all these missing listings on even the new home sites that you know. So then I came back and I just started digging and figuring out how all this data was collected. And you know, every time you come back from one of those trips, you start to wonder, did I really see what I saw? Did I really see what I saw?

So what did I learn? This trip was more just a a confirmation that nothing has changed. It’s the same, and the data is not accurate at all. And so you have to figure out why. And now I have such a background in why all of that data is missing. But it’s a difficult message because it’s not one thing. Everybody wants it to be it’s subprime or it’s the ARMs or whatever. No, this is a massive macro story that also is micro in many ways, so you have to be able to go look to put those two things together. I hope that made sense.”

“You go to somewhere like Lakewood Ranch and, you know, realtor.com might say there’s a hundred new homes for sale, but no, there’s thousands of them. Thousands.”

“Everybody’s going to go look at the mortgage delinquency schedule on the FRED site and they’re going to see this super low delinquency. Read the title. It’s for commercial banks. Commercial banks don’t do the majority of lending and mortgage anymore, and you can’t forget that the agencies sold off a lot of their non-performing assets to people and hedge funds that don’t report to credit. There is distress out there that’s happening right now that no one knows about.”

Oh Yeah?

Compiled from Newspapers and Public Records by Edward Angly (1931)

OCTOBER 26, 1929.

”Conditions do not seem to foreshadow anything more formidable than an arrest of stock activity and business prosperity like that in 1923. Suggestions that the wiping out of paper profits will reduce the country’s real purchasing power seem far-fetched.”

—Wall Street Journal

“We’ve never had a deflationary bust because inflation was too close to zero, or 1.5% instead of 2% - we’ve had them because we’ve had these tremendous ASSET BUBBLES...”

- Stan Druckenmiller, 2021

"Jim Grant: What the Fed calls 'deflation' is actually progress"

Nice little substack podcast I came across, Debt Serious. Here are a couple podcasts I recently listened to:

Hidden Risks in PE-Owned Life Insurance | Tom Gober of Thomas Gober Forensic Accounting

The Fed, Liberty, and Private Credit | Jim Grant of Grant’s Interest Rate Observer

Dan Rasmussen

“So the consensus was very clear. There was a wonderful survey that Preqin did in maybe 2018, and the survey question was, “Do you expect private equity to outperform by zero to 2%, two to four, or greater than four,” or something, and something like 91% of institutional investors thought it was at least 2%. Underperform was not even an option. It was literally complete consensus.

They were plugging historical returns, and saying, hey, private equity is quote unquote the best performing asset class, and therefore we should have as much money in the best performing asset class as we can. The number that they sort of circled in on was 40%. We should be 40% in privates. That’s what Yale and Harvard ended up at, and a bunch of other smaller endowments, even though the market-cap weighted size of private equity as an asset class is probably about 4% of the market cap of the public equity market. So if you’re 60% public equities, you should be, you know, 3% private equity at market cap weight. But that’s not how they thought about it. They thought, well, it’s the best performing asset class, we should follow the endowment model and always should be 40% in it.

Then within private equity, you were saying, well, I want to invest in the best performing managers. Well, who were the best performing managers? The ones with the most software exposure, because that was what was hot. And software was supposedly eating the world at the time.

And then what sort of capped it all off, the sort of thing that created the final frenzy, the extinction burst, was there were a bunch of deals done in 2018 and 2019 at very high prices, and a lot of the skeptics were saying, hey, this stuff is crazy! Even for software we shouldn’t be paying these type of multiples.

Then Covid hits and all of a sudden all tech is valued like an insane amount, so all those expensive deals in 2018-2019 were golden, right? There were huge winners, and so then that was the moment where the lights went on and people said it doesn’t matter what you pay. If you’re buying a great software business, it doesn’t matter what you pay, because it didn’t matter in 2018-2019. Look at the returns we made. We actually could have paid two or three, four, five turns more for that business and we still would have made 3x our money at current valuations. The key thing we need to do is put the most money into the ground in software as fast as possible. Forget the valuations. These are just great businesses.

And that that was sort of the peak, right?”

Jim Grant

“Today is one of the greatest bubbles of all time…this one is much bigger, much more lurid, I would submit to you, than almost any other preceding cycle.”

“The excitement surrounding the potentialities of artificial intelligence dwarf the excitement generated by the worldwide web, by the internet by fiber optic cables, and I think the dollars - even when adjusted for inflation - are larger today.”

Meb Faber: “A small part of me wants to take out the 1999 highs on the final CAPE ratio1 just to say we we lived through it again.”

On the Panic of 1873: “what set prices tumbling, what set real wages rising was human progress.”

“I submit to you that air conditioning is as transformative in its way - it changed human migration patterns, it made habitable the great sunbelt, it gave us the year-round Congress - isn’t that great? But you look back, these air conditioning stocks in the 1950s were four, five, six times, eight times earnings.”

The GFC was “the greatest failure of ratings and risk management ever…”

“Bernanke, I think, did not do any of us a great turn by single-mindedly invoking the experience of the 1930s to address the problems of 2009 and 2010and 2011 and 2012 and on, when the funds rate was pushed down and when all manner of distortions followed from that suppression of that interest rate.”

Powell “got behind the powers that were intent on barring Judy Shelton from a place in the Board of Governors. She was the person who wanted to have a different way of thinking of things. She likes gold. She likes the gold standard ways in some form, and she’s not really a gold standard advocate, but she wanted the Fed to have something to do with gold. Monetary affairs to have some grounding in the discipline of gold. That was her own line. I believe that J. Powell actively resisted her candidacy as he should not have done. Political malpractice if you ask me, which you did. So that’s my take on Jay Powell.”

“It’s up against the valuations it does not discuss. It’s up against the margin debt it does not discuss. It’s up against the now gently accelerating aggregates for M2 and C&I loans, commercial industrial bank loans. It is up against, most of all, the leverage that its own manipulated and suppressed interest rates instigated in the past five or six or seven years. That’s what the Fed is up against. Much of it is its own doing.”

“Never queue up for an investment, right?”

"The proposition that I sell a dollar bill for $10 is awfully appealing to many clients & potential clients, until the $1 bill starts trading at $12, & then the view is why can't it go to $15? And the answer is of course it can, but it's still a $1 bill at the end of the day..."

Jim Chanos, 2020

The Cattle Empire That Turned Out To Be A Giant Ponzi Scheme

Classic.

“There are two sides of me,” Brian McClain scrawled on a piece of paper to his wife.

One that loves you, he wrote. “The other that stole from people.”

For years, McClain had kept cattle here in his hometown and on the Texas Panhandle, buying calves at auction and selling them for profit three months later. His 80,000-head operation—powered by a $50 million loan from an agricultural bank and $120 million from investors—appeared to be a blowout success for the former chemicals plant worker. He lived in a 4,100-square-foot brick home surrounded by a manicured lawn, with gold-framed photos from his recent wedding in the entryway.

He also had a big secret: Most of the cattle were imaginary.

Once the lender got around to a physical check to count cattle and value McClain’s collateral—the first full inspection after more than four years of sending him money—it enumerated only 8,916 animals.

In the end, the rancher burned through the $170 million taken in from the bank and investors—some of them friends from his small Kentucky town. He managed to placate the bank when it occasionally raised concerns about financial figures that just didn’t make sense—including how his feed costs were wildly out of tune with the number of animals he claimed. And he kept his investors on board by paying out “shares of the profits,” which often stayed on paper as they rolled them into new investments.

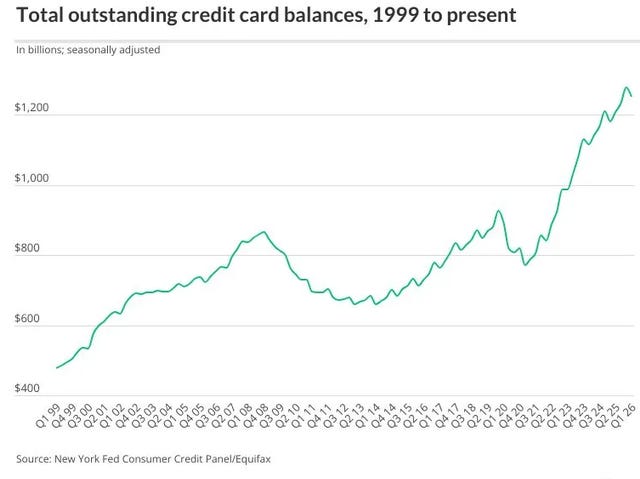

Credit Spreads

Credit Card Balances

“Forced Repositioning”

Bob Dylan on 60 Minutes, 2004

Bob Dylan: I don’t know how I got to write those songs.

Ed Bradley: What do you mean you don’t know how?

BD: All those early songs were almost magically written. Ah… “Darkness at the break of noon, shadows even the silver spoon, a handmade blade, the child’s balloon…” Well,

try to sit down and write something like that…EB: Do you ever look back at the music that you’ve written and look back at it and say

“Wow! That surprise me!”?BD: I used to. I don’t do that anymore. I don’t know how I got to write those songs.

EB: What do you mean you don’t know how?

BD: All those early songs were almost magically written. Ah… “Darkness at the break of noon, shadows even the silver spoon, a handmade blade, the child’s balloon…” Well, try to sit down and write something like that. There’s a magic to that, and it’s not

Siegfried and Roy kind of magic, you know? It’s a different kind of a penetrating magic. And, you know, I did it. I did it at one time.EB: Do you think you can do it again today?

BD: Uh-uh.

EB: Does that disappoint you, or…?

BD: Well, you can’t do something forever. I did it once, and I can do other things now. But, I can’t do that…

EB: Why do you still do it? Why are you still out here?

BD: Well, it goes back to that destiny thing. I made a de…bargain with it, you know, long time ago. And I’m holding up my end.

EB: What was your bargain?

BD: …to get where I am now.

EB: Should I ask who you made that bargain with?

BD: [laughs] With the chief commander.

EB: On this earth?

BD: [laughs] In this earth and in the world we can’t see.

Jimmy Dore

Dore is a liberal, to the left of Schumer and Pelosi. Carlson is right-wing.

Both have come to realize that these labels are meaningless, and that common ground on shared issues is key. Ron Paul and Dennis Kucinich understand this, as do Ro Khanna and Thomas Massie.

“In the United States, capital is above the government, so the economy doesn’t work for the people. It works for a handful of international globalist billionaires, which is why we have homelessness everywhere. We have the biggest prison population in the world, and we get go bankrupt just to get educated. You get bankrupt when you get sick.”

Tucker Carlson: “It’s a hard jump for your average right-winger - me, for example - to accept the fact that corporations are even more malicious than government.”

Dore: “Way more.”

Dore: “The people who slaughter people for profit - which is what the last 25 years Since 9/11 has been, just slaughtering people for prophet - they wouldn’t rig an election? Of course, they would.”

Carlson: “By the way, that's the one thing you're not allowed to say.”

“People who consider themselves liberal - the last thing they want is to be challenged from their left.”

“The Democrats say they hate Trump, but they love him because their biggest fundraiser is Donald Trump.”

“Bernie Sanders tucks his tail. He endorses Hillary Clinton, and he extracts not one concession for doing so. Nothing. He didn’t ask for anything for him, for his supporters, to vote for Hillary Clinton.”

“People immediately say, well, if you’re going to criticize the Democrats, you must be a Republican. You must be a Trumper. I’m like, no, the Republicans never asked for my vote. Democrats did, and I got tricked by them. I got tricked by Bernie Sanders. I got tricked by AOC hard.”

Carlson: “Is [Newsom] in any sense different from Chuck Schumer or Pelosi or anybody like that?

Dore: “No, you don’t get to be there if you are.”

Carlson: “I actually [campaigned for Trump]…then to wake up, and substantively he’s no different from Chuck Schumer on economics and foreign policy…”

Dore: “Or Lindsey Graham.”

“We had an anti-war rally in Washington, DC and Code Pink wouldn’t join in. Their whole thing is to be against war, and they wouldn’t join it because there were certain speakers on the lineup that they didn’t feel agreed with their views on LGBTQ…that organization just proved themselves to be a bunch of cosplaying women.”

“January 6, which we now know was an FBI psy-op…”

“Just like Governor Whitmer. They were going to kidnap her, turns out nine out of the 13 people in the van were FBI.”

“You got people who consider themselves liberal repeating don’t do your own research, don’t look into things, just trust the government. Trust the government and trust Big Pharma. And now we know they lied about everything, and those people still don’t know anything.”

“Liberals, the people I know in Hollywood, they’re not spiritual, religious, and so they turn science into a religion, and they turn Fauci into their deity.”

“Liberal democracy has turned out to be neither liberal nor democratic. They're illiberal. They're illiberal and undemocratic. Just like they proved during COVID.”

"I just have this principle that when the government breaks the law, I realize that's bad for me."

Matt Smith

Under the Trump crypto playbook, the family always wins. Investors don’t

Risking little of their own money, the US president and his sons have added at least $2.3 billion to the family fortune from their main crypto ventures, while the investors they've wooed have taken a $2.3 billion hit, a Reuters examination found.

Luke Gromen: “I would say [inflation’s] probably 8% right now, and has been for probably 20 years.”

Dave Collum: “Which means we’ve been in a recession the whole way.”

Gromen: “Yep. On a real basis. And how would we know that? Well, we would see record political divisiveness in this country.”

I got some abuse for quoting Luke’s comment above, but 8% is certainly no more ridiculous than the official CPI, and I’d argue much closer to reality - but I have no econ PhD.

“It wouldn’t be the worst thing if the 350 million of us in the United States discovered that bombing the living shit out of other people has a real downside to it.”

“One of the saddest lessons of history is this: if we’ve been bamboozled long enough, we tend to reject any evidence of the bamboozle. We’re no longer interested in finding out the truth. The bamboozle has captured us. It’s simply too painful to acknowledge, even to ourselves, that we’ve been taken. Once you give a charlatan power over you, you almost never get it back. So the old bamboozles tend to persist as the new ones rise.”

USS Liberty

Cyclically Adjusted Price-to-Earnings

No way inflation is 8% currently. Housing would have to be about 40% or so of the sample, and housing definitely hasn't doubled in the last 9 years.