“I write so that knowledge of these important matters may not fade away like the fleeting memories of a passing dream.”

- attributed to Thomas Hooker, 1586-1647, but I couldn’t find any original source

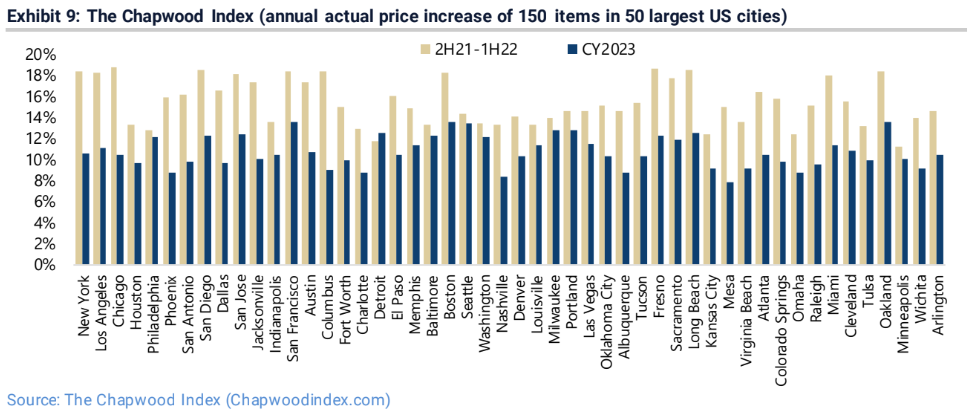

"The Chapwood Index’s actual costs on the top 150 items Americans buy in the 50 largest cities rose by between 7.8% and 13.6% last year. In 2022, the range was 11.3% to 18.8%."

No subjective hedonic nonsense, no substitution, no seasonal adjustments…

Sure, everything costs at least 50% more now, but the rate of change is down to just 3.3%!

Now you take that paper dollar

It's only that in name

The way that buck has shrunk

It's a lowdown dirty shame

That's why I got the blues

Got those inflation blues

"Hey Siri, show me one graph proving how the biggest and most pronounced legacy of Barack Obama’s entire presidency was giving corporations get-out-of-jail-free cards in the form of non-prosecution and deferred-prosecution agreements”

Tell me again how tight financial conditions are.

Via Grant’s.

A long, hot financial summer is at hand: investors poured a net $8.7 billion into U.S. tech funds over the seven days through Tuesday per data from EPFR, the largest weekly inflow on record. Growth-oriented mutual funds attracted upwards of $10 billion over the same stretch, likewise its most bountiful week since at least 2017.

Also:

The MarketVector Meme Coin Index, composed of the half-dozen largest digital assets “often named after characters, individuals, animals [or] artworks,” is up 116% for the year-to-date through Thursday, compared to a 44% gain for bitcoin.

The St. Louis Financial Stress Index measures the degree of financial stress in the markets and is constructed from 18 weekly data series: seven interest rate series, six yield spreads and five other indicators. Each of these variables captures some aspect of financial stress…Values below zero suggest below-average financial market stress.”

Doesn’t anyone have a memory?

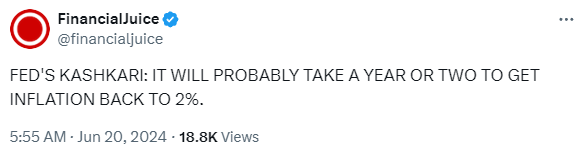

CPI's been above the Fed’s MADE-UP 2% target for over 3 YEARS.

Kashkari & the FOMC were all calling for ABOVE 2% inflation a few years ago. Neel even mocked those who expressed concern.

Neel and the Fed permanently harmed a couple hundred million Americans.

“The really great investors have a deep capacity for pain.”

Inflation is a Default

“There are actually built-in shock absorbers created by the reforms of 1986, which is the last time we worried about Social Security going bankrupt. The benefits will automatically be cut once we start running out of the revenues, and they're on target to be cut by about 40%. Now think about the cruelty associated with that.”

At the same time, a number of prominent (and very wealthy) people are calling for a "4% inflation target," which would cut 𝘦𝘷𝘦𝘳𝘺𝘰𝘯𝘦'𝘴 purchasing power - young and old, rich and poor - by 40% in about 12 years.

Now think about the cruelty associated with that.

Welcome to new paid subscribers. As an aside, the last five people to unsubscribe from paid listed “Time” as the reason (as is their right.) Maybe they’re just being kind.

So, at my own peril, below is another fun-filled post with curated and transcribed brain-candy from Jeremy Grantham, Bernard Baruch, Jesse Livermore, Mike Green, Nassim Taleb, Fred Hickey, Jim Reid, Chris Bloomstran, Charles Mackay, Jared Dillian, Barry Knapp, Phil Bak, Jeff Gundlach, and more!

Money managers must never, ever be wrong on their own.

“The central truth of the investment business is that investment behavior is driven by career risk. In the professional investment business we are all agents, managing other peoples’ money. The prime directive, as Keynes knew so well, is first and last to keep your job. To do this, he explained that you must never, ever be wrong on your own. To prevent this calamity, professional investors pay ruthless attention to what other investors in general are doing. The great majority “go with the fl ow,” either completely or partially. This creates herding, or momentum, which drives prices far above or far below fair price. There are many other inefficiencies in market pricing, but this is by far the largest.”

Bernard Baruch

From Jim Grant’s biography: “A memo to himself on the basics of investment and speculation, dated only 1930, was found among his papers. It went as follows:”

“SELF-RELIANCE: Do your own thinking. Don’t let your emotions enter into it. Keep out of any environment that may affect your acting on your reason.

JUDGMENT: Consider all the facts—meditate on them. Don’t let what you want to happen influence your judgment.

COURAGE: Don’t overestimate the courage you will have if things go against you.

ALERTNESS: To discover any new facts that change the situation; or which may affect public opinion.

PRUDENCE: Be pliable or you won’t be prudent. Become more humble as the market goes your way. It is not prudent to buy when you think the bottom has been reached. It is better to wait and see, and buy too late. It is not prudent to wait for the top of the market to sell—it is better to sell “too soon.” (Never buy so that your margin will be less than 85, or hold if it drops below 80. In a particularly “clear sky” situation with[out] “buts” or “ifs,” one can lower these margins to 80–75%.)

PLIABILITY: Consider and reconsider the facts, and your opinions. Stubbornness as to opinions—“cockiness”—must be entirely eliminated. A determination to make a certain amount within a certain time absolutely destroys pliability. When you decide, act promptly—don’t wait to see what the market will do.”

“The retirement wealth in our economy is presumed to be much higher and much more liquid than it actually is”

Mike Green: “We've created conditions under which people are increasingly going to be trapped into the market right now. It's a very scary phrase, trapped, right? So I just want to be clear that as long as those [passive] flows remain net positive, you're actually participating in what's called a Ponzi scheme, right? So you are driving valuations higher as you participate. That's raising your perceived wealth. Those who are exiting now are being bought out by new entrants, right? That's a Ponzi characterization.

There's a brand new paper by Van der Beek and Bouchaud called “Ponzi Funds” that actually highlights the impact of these types of flows on the performance of funds. It makes a point of highlighting the behavior of ARKK, the Cathie Wood vehicle which was one of the most notable examples of this type of impact. What that means is when people try to get out of these strategies, that you're actually - if the paper is correct, and I think it is - you'll actually see an accelerated reversal all of these valuation gains.

So I would highlight for people that the flip side of the price that we see in the public markets, where extremely large companies like Apple - which is largely ex-growth, to be clear, right? They're trading at 30-plus times earnings - that's not a rational valuation for something if you were to take it private, for example. If you were to decide that you were going to buy something without growth you can't pay 30 times earnings for it. You can maybe pay something like 10 times earnings for it in an environment like we have today with 5% interest rates. As a result, you know, the next bid for Apple in the event that these funds start to sell could very well be down 70%, right, and that's a big problem, because it means that the retirement wealth in our economy is presumed to be much higher and much more liquid than it actually is.”

Julia: “It could be down 70%??”

Mike: “Yeah, I think that's right.”

I keep thinking back to this great Rick Rule quote:

"I learned that my assets were ephemeral, while my debts were money-good."

Jesse Livermore

“It never was my thinking that made the big money for me. It always was my sitting. Got that? My sitting tight! It is no trick at all to be right on the market. You always find lots of early bulls in bull markets and early bears in bear markets. I’ve known many men who were right at exactly the right time, and began buying or selling stocks when prices were at the very level which should show the greatest profit. And their experience invariably matched mine—that is, they made no real money out of it.

Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money. It is literally true that millions come easier to a trader after he knows how to trade than hundreds did in the days of his ignorance.”

Reminiscences of a Stock Operator

A slightly different perspective than Bernard Baruch.

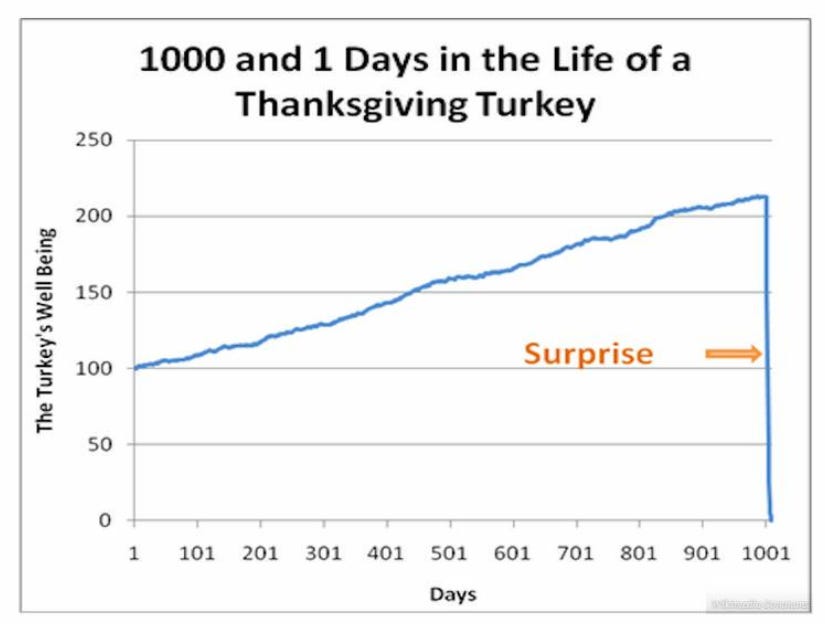

A Revision of Belief

“Consider a turkey that is fed every day. Every single feeding will firm up the bird’s belief that it is the general rule of life to be fed every day by friendly members of the human race “looking out for its best interests,” as a politician would say. On the afternoon of the Wednesday before Thanksgiving, something unexpected will happen to the turkey. It will incur a revision of belief.”

- Nassim Taleb, The Black Swan

Fred Hickey has seen this movie before

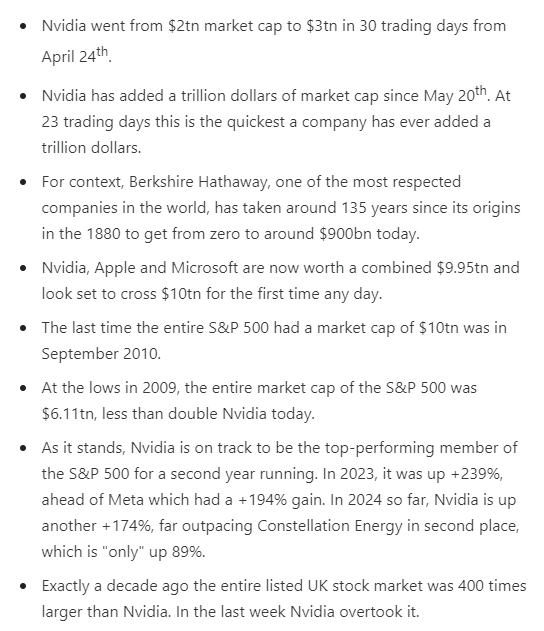

"Intel was as dominant today in the microprocessor market, the CPU market, in 2000 during the dotcom bubble, more so than Nvidia is dominant in GPU’s. Intel's market cap peaked in 2000 at $500 billion. We're seeing now Nvidia is $3.3 trillion, six plus times that now if you inflation-adjust...what happened to Intel? Well, Intel peaked at $76 in August, September of 2000, and fell 80-something percent when that bubble broke, and it never recovered. It's $30 today.”

Hickey knows his stuff. Worth watching or listening to the entire interview.

“In generative A.I. there's no intelligence. It's great at regurgitating the contents of the internet but it gives you wrong answers. It gives you hallucinations.”

“The honeymoon phase for generative A.I. is over. Companies just aren't seeing the payback. The costs are enormous for them to use to use these large language models, and they're not getting the payback. There was another survey just a couple weeks before that said that of those who are initiating this, they're only

seeing paybacks in 5% of the cases, so what's happening is they're slashing spending. These companies are slashing spending on this stuff…it's very reminiscent to me of the internet, which was real, just as A.I. is real, but in this case it's “Gen A.I.”, it's this large language model stuff, and I liken that more to, you know, tulip bulbs.”

“You know, VC funding peaked in the second and third quarter of last year at like $500 million. It's down 75% - even they aren't putting money into it anymore, so the question now is how long can this go on? How long before before investors - seems like the joke's on everyone. Everyone now knows that it's a joke except for investors on Wall Street, who just keep pouring into the same names.”

“One of the misconceptions I keep hearing - it bothers me - they say, well, it's different this time. Famous saying - it's different this time - because those companies back then in 2000 weren't making profits like these companies, and I say that's bull crap. All the major companies were making money. Microsoft, Cisco, Intel - they were all making tons of money in that buildout of excess equipment. It turns out they were all making money, just as these companies are, but when the growth rates fell, then the stocks collapsed”

Deutsche Bank’s Jim Reid

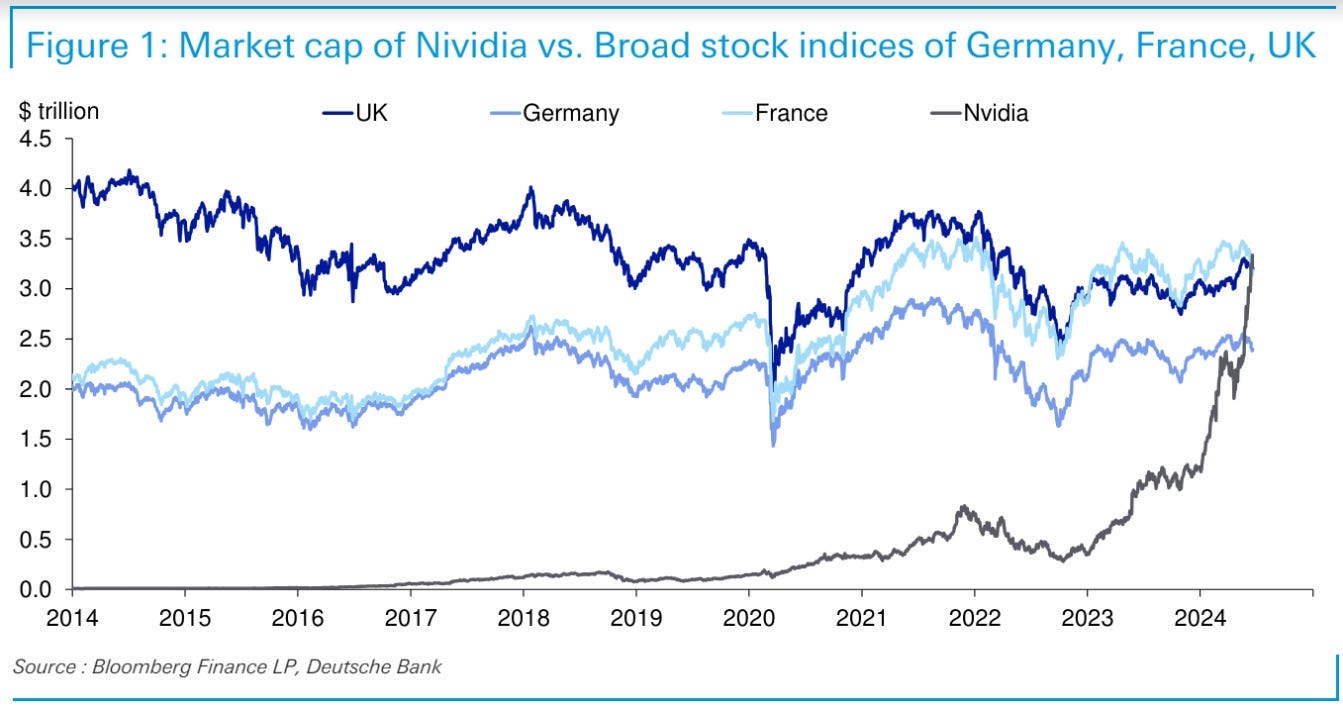

“Stunning. Nvidia passes Microsoft and Apple as largest market cap. Combined, the three are valued at $9.9 trillion, 21.5% of the entire market capitalization of the S&P 500. The three are today LARGER than the capitalization of the ENTIRE S&P in September 2011, not a market low.

Including Google, Amazon, Meta and Tesla, the Magnificent 7 have a $16 trillion combined market value, 34% of the S&P 500 and LARGER than the ENTIRE S&P as recently as February 2016, just over 8 years ago and most definitely nowhere near a market bottom.

Nvidia is valued at 42x and 78x trailing sales and earnings on an unsustainable 54% net profit margin.

Microsoft is valued at 14x trailing sales and 39x earnings on a 36.4% net margin.

Apple is valued at 8.6x and 33x trailing sales and earnings on a record 26.3% net margin. These are crazy valuations for very large companies that can grow sales and earnings nowhere near as rapidly as they did over the past one and two decades. Microsoft and Apple traded for less than 10x earnings at various points over the past 20 years.

This is the goofiest and likely most dangerous concentration of overvaluation I’ve seen in 34 years investing and throughout financial history. The extremes extend beyond the three and seven to companies like fellow Nasdaq 100 member Costco, now with a $386 billion market cap on $254 billion in sales. Costco has a 2.8% profit margin, up from 1.7% when I first bought the stock. With $7.1 billon in earnings, the P/E multiple is an incredible 54x. How do you make money with an initial 1.8% earnings yield, 2.5% growth in systemwide square footage (down from 7.5% growth 20 years ago), double inflation same-store sales growth and modest potential to increase margins? You are looking at seven to eight years of no change in the share price for the stock to trade at 25x earnings.

Mr. Market is very good at rewarding business success but to a fault. In the short term, stocks can trade at extremes relative to fundamentals, both on the low side and the HIGH side. At 23x 2024 expected earnings, the market-cap weighted S&P 500 is froth with excess and in my judgment uninvestable. Under the hood, the majority of stocks are not overvalued. The bifurcation between the dear and the cheap reminds me of March 2000. From that point the index has returned 7% per year, spending much of the subsequent decade in the red. You can have extremes of over or undervaluation in the short and even intermediate terms. But in the long run, Mr. Market gets it right.”

I have no position in Nvidia. I’ve just seen this movie before.

“Money, again, has often been a cause of the delusion of multitudes. Sober nations have all at once become desperate gamblers, and risked almost their existence upon the turn of a piece of paper. To trace the history of the most prominent of these delusions is the object of the present pages. Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

Charles Mackay, 1852

Jared Dillian on Private Equity: “An Enormous Bubble”

Tony: “Ten to 15 years ago, I noticed a massive massive intellectual capital flight into private equity, and I would imagine that a lot of them, and what they're doing, is getting stale right now. So tell me about your view on that, JD?…Give me the elevator pitch.”

Jared: “Let me put it this way - people send me stuff all the time. I got an email this morning. An article that private equity is rolling up bakeries, like making bread, bowling alleys, car washes, pizza places, dental practices. Look - there's no exits, there's no IPO’s, there's no M&A. LP’s are not getting distributions, they're not getting cash distribution, they're actually getting cash calls, and they're actually doing dividend recaps. They're borrowing money against the portfolio to pay LP’s. The leverage keeps going up, and you know, as a result, private equity is getting to be a bigger percentage in pension funds and endowments. Dude, this is an enormous bubble. It is an enormous bubble”

Recent headline: "Bakeries ripe for consolidation, modernization: 6 recent PE-backed deals"

Federal Reserve criticises ‘living wills’ of Bank of America, Citi, Goldman and JPMorgan

US regulators have found weaknesses in the plans laid out by Bank of America, Citigroup, Goldman Sachs and JPMorgan Chase for how they would handle their own failures…Citi’s rebuke was the most severe, with the FDIC saying the bank’s resolution plan was not credible or would not facilitate an orderly resolution under the US bankruptcy code.

From the FT comments:

Barry Knapp

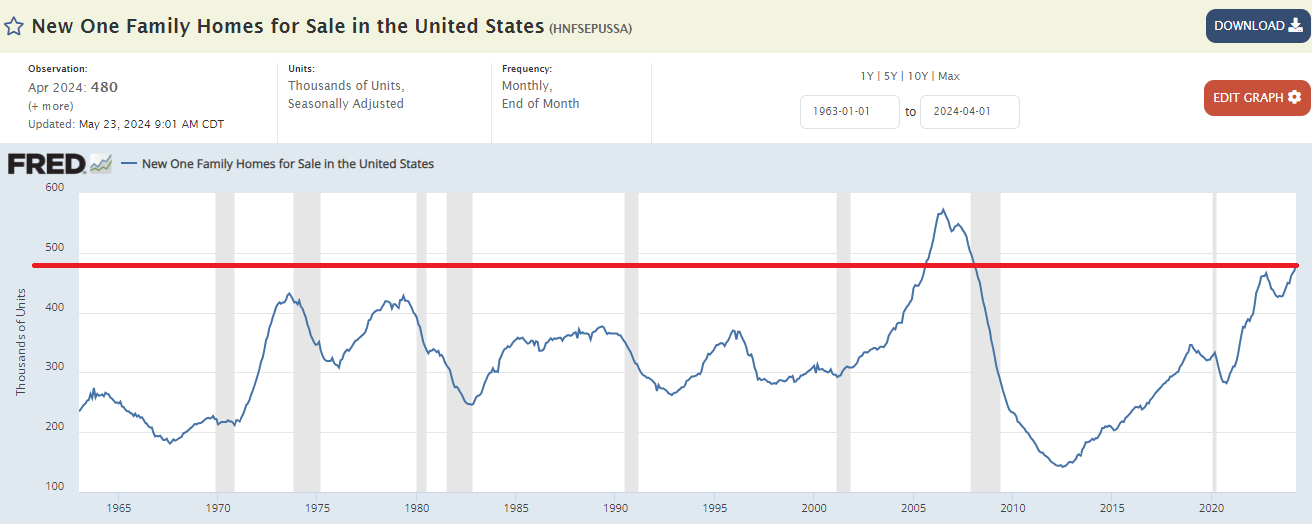

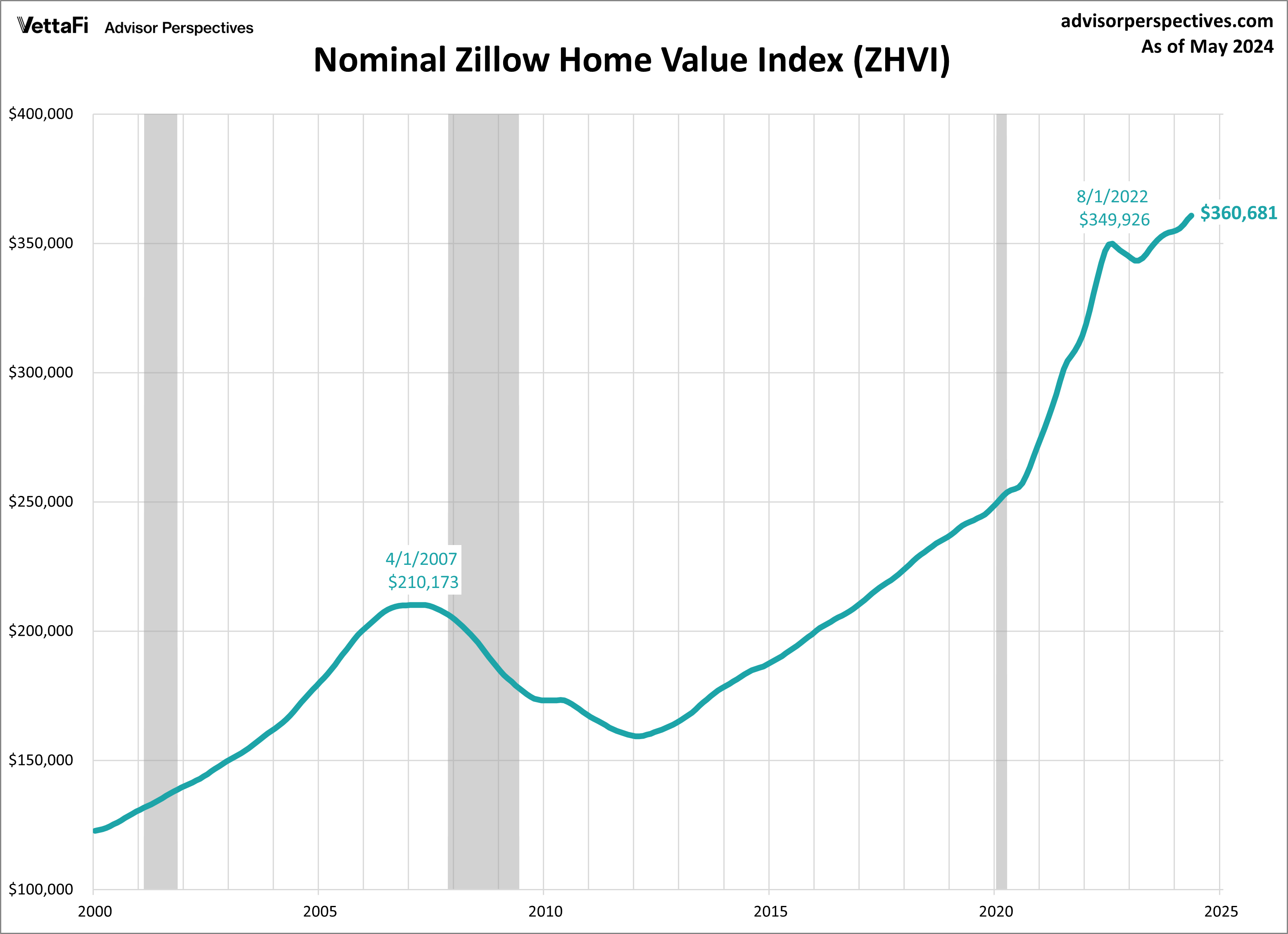

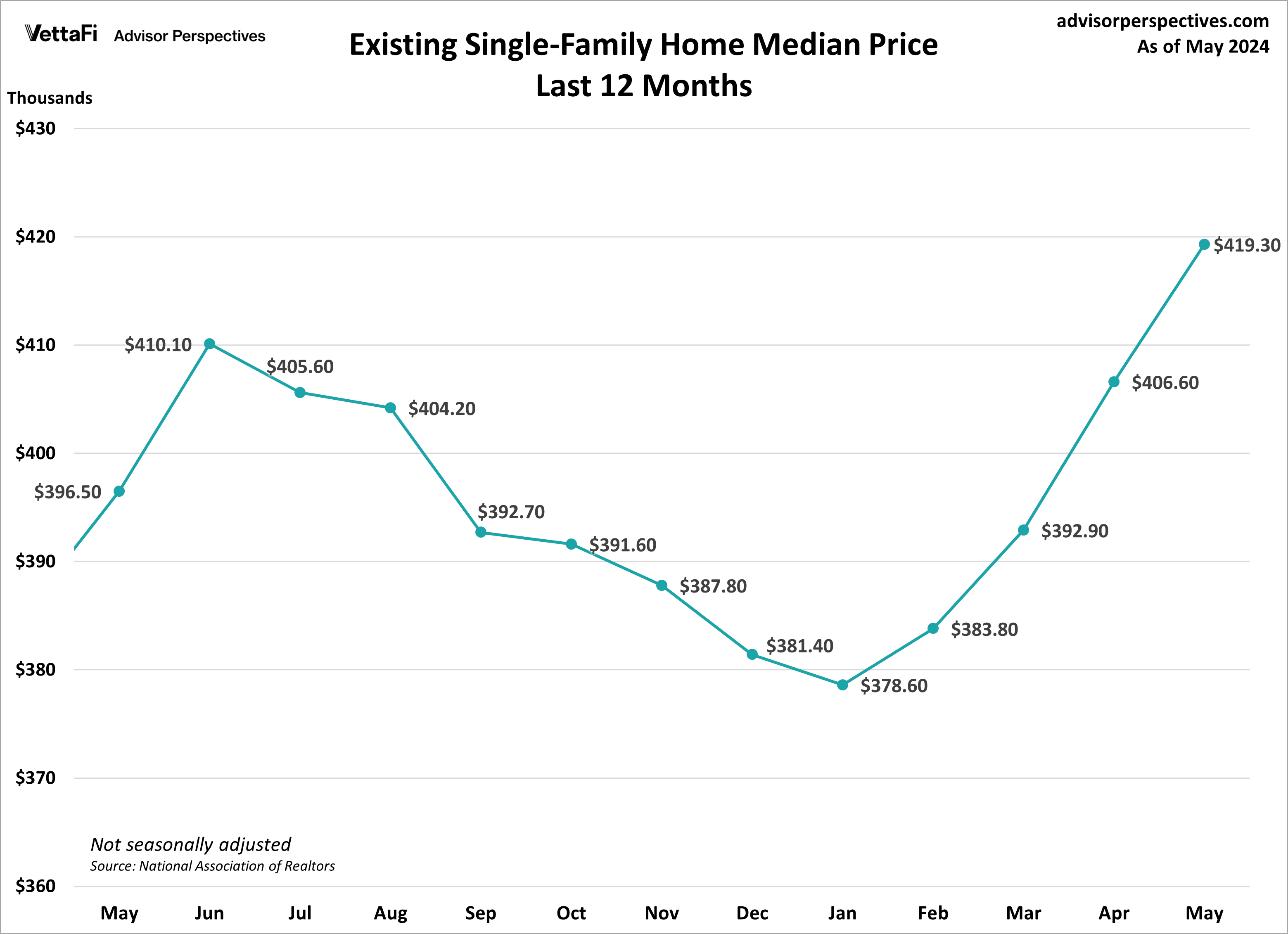

“When the Fed was buying $40 billion of mortgage-backed securities per month and reinvesting something like $55 or $60 billion during 2021, when we had an absolute refi-boom, the spread of mortgages to treasuries went to all-time lows, so it wasn't just that individuals got to refinance their mortgages - this was an absolute panacea for Blackstone, for any of the big REITs, mortgage REITs, untraded REITs or otherwise. They could raise money cheaply. and go ahead and buy residential real estate. We had a 46% spike in that Case-Shiller 20 City composite home price index, now we're higher…we drew in REIT money to buy residential real estate to turn them into rentals, crowding out Millennials who are forming households at the fastest rate since Boomers in the 1970s. If that's not capital misallocation, or what the Austrians would call malinvestment, I don't know what is.”

Blackstone is now offering seller-financing at below-market rates AND free corndogs when you buy a portfolio of student dorms!

Phil Bak

Phil Bak takes on Blackstone’s BREIT

“Here’s the BREIT Story in a nutshell: They’ve reported an annual return since inception for its Class S investors north of 10% with real estate investments that have a gross current rate of return of less than 5% on their cost. They’ve been buying assets at a 4% cap rate, paying a 4.5% dividend and reporting 10+% returns. And nobody has called bullshit.”

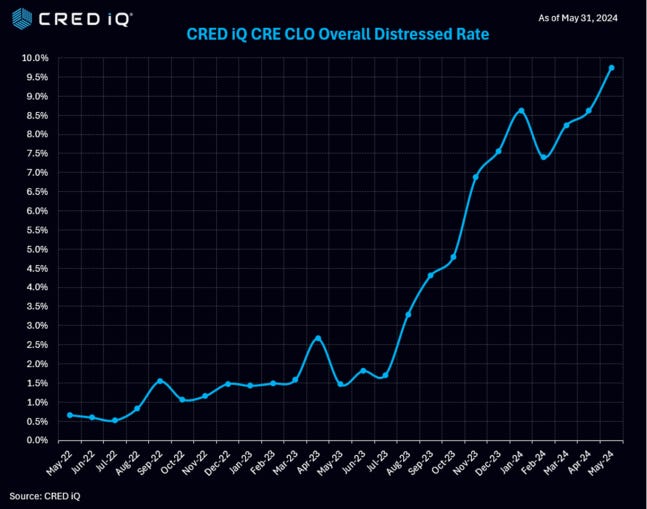

CRE CLO’s!

Here’s a rather surprising chart from Trepp:"

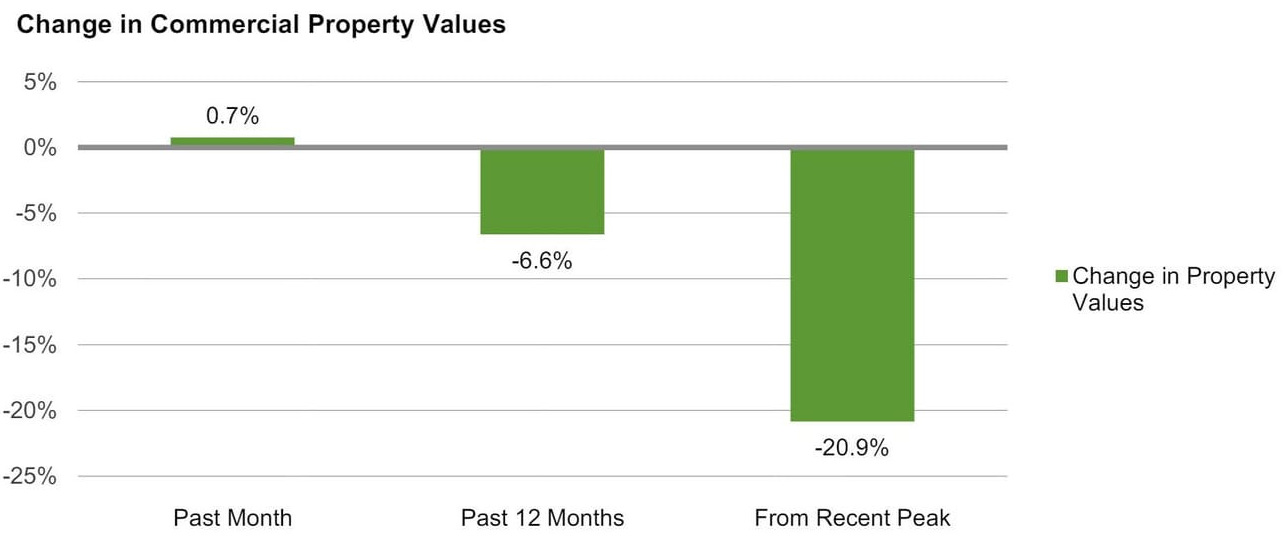

Are they telling me office prices are UP since mid-2022? So why all the whining from all the office people?

Or is it just extend and pretend: “This [office] resilience, despite broader market challenges, may be due to the sector's illiquidity and reluctance of owners to sell at lower prices.”

Then again, this is from Green Street:

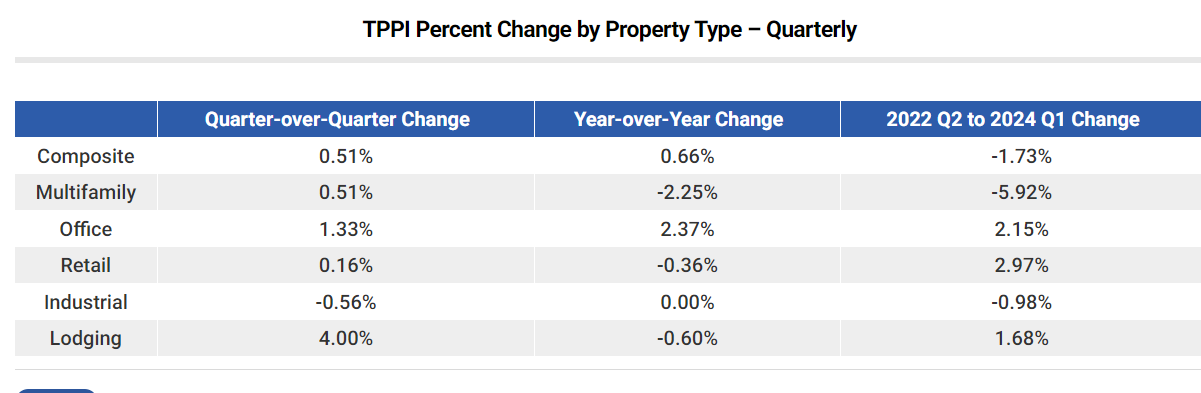

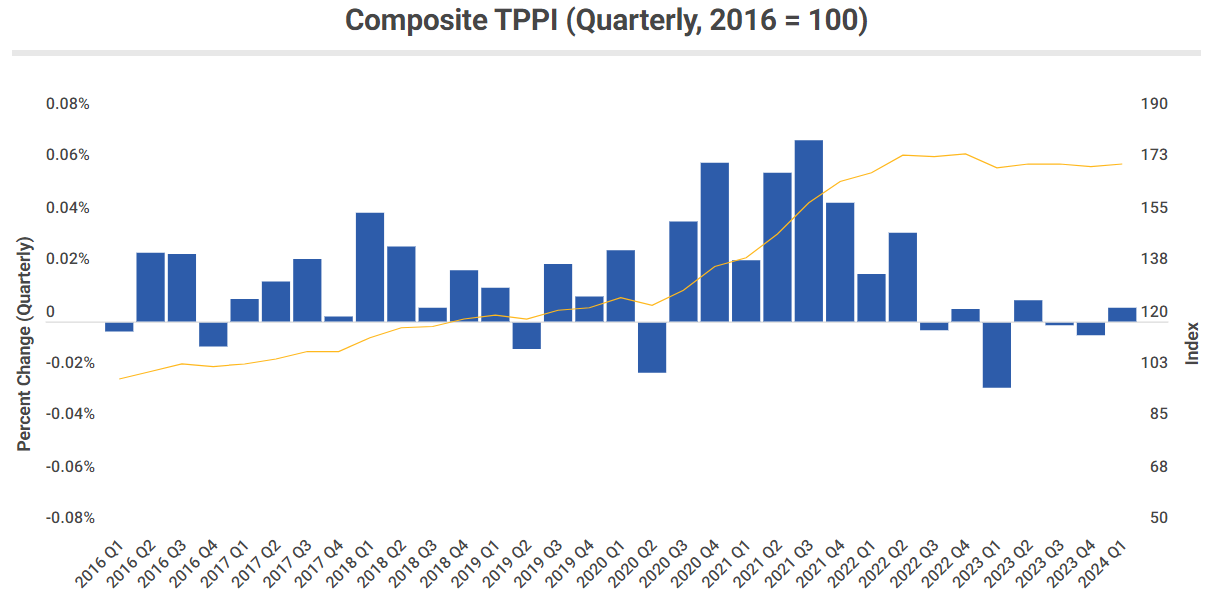

Grant’s: The “dim state of play in the office realm”

Nationwide vacancy rates approached 20% in the first quarter, data from Moody’s show, up from 16.8% over the last three months of 2019, while delinquencies among U.S. office commercial mortgage-backed securities will reach 8.4% this year and 11% in 2025 if recently issued projections from Fitch are on the beam, up from 8.1% and 9.9% guesstimates issued earlier this year…

The Financial Times reported Friday that credit agencies have “mis-rated” upwards $100 billion of debt tied to so-called single-loan deals, with at least a dozen such transactions maintaining upper-tier investment-grade ratings even with the borrowers slipping into default. [I mentioned one-such case, 1740 Broadway in New York, back in March]

“The integrity of the ratings process has improved very little” since 2008, says former Moody’s credit analyst turned economics commentator Rod Dubitsky.

“Special servicers have been very, very aggressive about not giving in to the reality of the situation”

When a 145K SF suburban Maryland office building sold for just $5.7M at an auction this spring, it brought a resolution to a three-year-long spiral that began when its sole tenant, the Montgomery County government, terminated its lease in 2021.

The CMBS loan tied to 255 Rockville Pike in Rockville, Maryland, once valued at $56M, still had a $33.6M unpaid balance. The years it spent in special servicing and the pennies it ultimately sold for meant the investors in the loan suffered $33.7M in realized losses, according to a report by Trepp.

It's one of a growing number of examples of CMBS loans that are resolving for increasingly greater losses, sometimes larger than the total balance of the debt.

“At 7%, those payments are $1,350,564 per month!”

Other Podcasts

Russell Napier with Kiril Sokoloff Worth it. 38 minutes.

Trepp Episode 263. Consumer Spending Dip, Sunbelt Multifamily, Ground Lease Valuation, & Industrial Sales For the morbidly curious.

Matt Piepenburg “The evidence is overwhelming that the Fed has led to the greatest wealth disparity in our history, so their policies do matter. Their ignorance is pretty inexcusable.” Short version: Prepare for worse, permanent inflation.

Economic Crisis "Much Worse than 2008" Imminent with Henrik Zeberg

Jeff Gundlach

“Inflation has really changed in my view. Prior to the pandemic, inflation was relatively uniform in the economy, and it was very range-bound. You remember that the inflation was below 2%, and they were bemoaning the fact they were having trouble getting UP to their “2% target,” and then all the money printing came, and ironically the Fed, with its 800 PhD economists, missed the inflation on the CPI just like they missed the entire credit crisis. In those days, there were 700 PhD economists in 2006. I guess they thought they needed 100 more, since they missed the credit crisis, but I think the biggest black eye of my career on the Fed is that nonsense of the inflation rate at three and a half-percent is transitory, when of course the CPI for a moment went to 9.1%, and what is the inflation rate now is starting to be a really interesting question, because unlike pre-pandemic, the inflation rate is variable across the economy in a large way.”

“We're in the endgame here for this debt-finance scheme, and I believe that the way to fix all of this will make it so that we're in a better world going forward, maybe in the 2030’s, because we're not going to be able to borrow anymore. We're going to have to run a sound economy. That's so outside of the psyche of consumers today. Consumers today are borrowing money like crazy at 23% interest rates.”

“I've got this crazy idea that I want to buy only the lowest coupon treasuries, zeros if possible, because if I have a very low coupon treasury, I don't have to worry about being restructured. I worry that the federal government might be forced to restructure the Treasury debt. People say that's impossible, that a contract, it's illegal, and I say, well, don't you remember the mortgages back in 2007, 2008, 2009? It was illegal to modify those mortgages. It was in the prospectus of trillions of dollars of mortgage-backed securities that these mortgages cannot be modified, but they did it. The Federal Reserve Act of 1913 says it is illegal for the Federal Reserve to buy corporate bonds. In 2020, they started doing it. They didn’t have to do very much, because just by doing it, the market repriced aggressively, because they said, well, the Fed's got an unlimited balance sheet, or perceived to be a huge buying power, so they can right this market, and so so that happened. It's illegal, it's un-Constitutional to cancel student debt, but $7.7 billion of student debt was canceled yesterday in one day alone, so the fact that something is viewed to be a contract doesn't mean it won't happen, because it's been happening with regularity over the last several years. I'm not predicting this, but what if the Treasury says, hey, we got all these bonds out there, and some of them are quite old, and some were paying 4%, 5%, 6% - we're in a jam, so what we're going to do is every Treasury bond that has a coupon above one, we're resetting the coupon of one.”

“My entire investment thesis for the last couple of years - and it's been working quite well - is fundamentally around dealing with the idea that what we think we know from the 40 years into 2021-2022 is informed by falling secular interest rates. Junk bonds didn't default. They would refinance, you know, the spread might have been wider, but yields fall during recessions, and junk bonds, shaky companies, instead of defaulting, they could refinance, so they never matured. With interest rates where they are now - junk bonds were issued at coupons of three and a half-percent in 2021. Those will never be refinanced, so those companies, if they run on hard times, they're going to have to default, so I believe with rising interest rates default rates will be higher than what we've experienced.”

“One thing we're in the last mile of is this debt-fueled situation”

“Make sure that you don't go out of business. Make sure you survive. No fatal

mistakes. You're going to make mistakes - just not fatal mistakes. That's really important, and that's why I'm around so long.”

“Higher for longer starts to take people out. It doesn't happen overnight.”

“I'm allergic to momentum investing, and just don't want anything to do with it.” [same here]

Gundlach on Private Credit

“Almost everything about the family from number 35 Primožičeva street was a carefully constructed lie, according to Slovenian and Western intelligence officials. Gisch’s real name is Artem Viktorovich Dultsev, born in the Russian autonomous republic of Bashkortostan and an elite officer in Russia’s foreign intelligence service, the SVR, according to the officials and court documents.

Mayer Muños is Anna Valerevna Dultseva, a more senior SVR officer than her partner, from Nizhny Novgorod. The couple’s computers contained hardware to communicate securely to handlers in Moscow that was so encrypted neither Slovenian nor U.S. technicians could crack it. In a secret compartment inside their refrigerator, they kept hundreds of thousands of euros in crisp bank notes.”

I watched the series The Americans, and while it was very well done, I didn’t really care for it (especially the ending). I didn’t like the characters. In fact, the one character I did like, Oleg Burov, [spoiler alert] ended up in an American prison.

Same sort of thing happened with Mel Sattem in Ozark and Peter Quinn in Homeland. It’s like national elections - the people I like never win.

LBJ

Several people mentioned Robert Caro’s book(s) in regards to the LBJ story I cribbed from Grant Williams last time. Reader NR mentioned Brown and Root as a big factor in boosting LBJ’s career. I found a 2000 article that succinctly describes their relationship:

Johnson’s “symbiotic relationship with Brown & Root occurred before campaign finance laws required candidates to reveal the sources of their funding. Indeed, by Johnson’s own admission, according to his biographer Ronnie Dugger, much of the money he got from Brown & Root came in cash. In return, Johnson steered lucrative federal contracts to the company. Those contracts helped Brown & Root become a global construction powerhouse that today employs 20,000 people and operates in more than 100 countries.

“It was a totally corrupt relationship and it benefited both of them enormously,” says Dugger, the author of The Politician: The Life and Times of Lyndon Johnson. “Brown & Root got rich, and Johnson got power and riches.” Without Brown & Root’s money, Johnson wouldn’t have won (or rather, been able to steal) the 1948 race for United States Senate. “That was the turning point. He wouldn’t have been in the running without Brown & Root’s money and airplanes. And the 1948 election allowed Lyndon to become president,” said Dugger

The Anti-library

“The writer Umberto Eco belongs to that small class of scholars who are encyclopedic, insightful, and non-dull. He is the owner of a large personal library (containing thirty thousand books), and separates visitors into two categories: those who react with “Wow! Signore professore dottore Eco, what a library you have! How many of these books have you read?” and the others—a very small minority—who get the point that a private library is not an ego-boosting appendage but a research tool.

Read books are far less valuable than unread ones. The library should contain as much of what you do not know as your financial means, mortgage rates, and the currently tight real-estate market allow you to put there. You will accumulate more knowledge and more books as you grow older, and the growing number of unread books on the shelves will look at you menacingly. Indeed, the more you know, the larger the rows of unread books. Let us call this collection of unread books an antilibrary.”

Nassim Taleb, The Black Swan

"We can’t have a real conversation with central bankers because they are both guards and prisoners of the island of policy and thought that they’ve created."

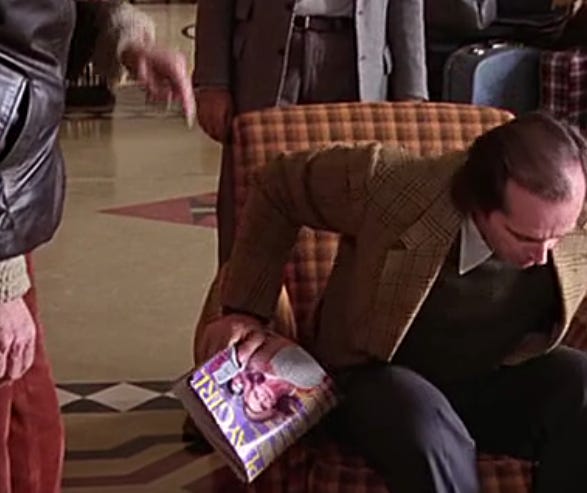

Never noticed until now that Jack Torrance was reading Playgirl magazine in the lobby of the Overlook Hotel.

"We think buying long term US treasuries at negative term premiums while global Central Banks buy record amounts of gold may come to be seen as buying AAA-rated subprime mortgage bonds in 2006, even as home prices were already falling nationally: Something that should have been obvious at the time, but was only obvious in hindsight for many."

Luke Gromen

As a paid subscriber to you, Rudy (unlike those who cancelled their paid subscription), I understand that I must make the time to read what you curate. The Price (and Value) of Time. Excellent!

On inflation….I was listening to CNBC a little while ago, and the spokesmodel asked Liesman (sp?) if he knew what the average cost of a bag of chips was…..he said that he had just paid a couple of bucks for one last week….she said ha! The average was + 6 dollars.

He did go on to say that he really didn’t pay attention to what kind of chips he had when he was “out on the water”.

I wonder if he notices what they charge for fuel at the marina……