This is all narrative.

Real Estate anecdotes...

Melody Wright provides the best free housing-market insight on the interwebs.

“Census Bureau Revises Away 25% of Pandemic-Era Price Spike of New Single-Family Houses”

When the government doesn’t like the data, it revises it.

We need to talk about Austin

“I did a Zillow search and in Buda and Kyle I was seeing multi million dollar homes. Looking at some different listings, I saw properties listed 300% higher than the January 2021 value!!!!! Combine that absurd level of appreciation with stagnant incomes and rates closes to 7% and ya, I get it. Those prices are to damn high. Best of luck.”

“I'm a land agent in Austin, and the trend that I have noticed is that it takes about 12-24 months for sellers to get used to the market receding and price correctly. Many sellers seem to be smoking crack in terms of what they want or believe their property is worth based on 2021 pricing. Look at the latest and most accurate comps, and price 5-10% under if you are not getting hits.”

Melody Wright: Riding Bikes With Helmets

“Buyers should beware when it comes to these new-build sites. Recently, REWatchman found an example of exactly what I had feared - one of these institutionals focused on single-family rentals, First Key Homes, owned by Cerberus who was previously mentioned, has bought up a significant share of one of the new-build sites from Lennar after families had already moved into the neighborhood.” [This is in San Antonio, Texas]

I grew up in single-family rentals, so I can tell you that no one wants you as their neighbor. And, nearby rentals can quickly bring down your zestimate. Not to mention, you thought you were buying into a new, stable neighborhood where you wanted to plant yourself and grow with other families who had the same idea, not one where renters will come and go.

But, if that isn’t bad enough, now First Key needs to offload these and is selling at a steep discount - 24% below the 2022 peak. Just imagine if you were living next door and had bought in 2022. The scariest thing - American Homes 4 Rent is also selling homes in a large new-build site right around the corner, advertising a $0 down payment. There will be no honor among thieves.”

“…the median home price in Palo Alto increased by 10.5% over the past five years, and now sits at $3.4 million. Meanwhile, the median income for Palo Alto households is $179,707 — resulting in a price-to-income ratio of 19. This means the average Palo Alto family must invest 19 times their annual household income for the purchase of a home.

Newport Beach, which has a median home price of $3.2 million and a median household income of $127,353, topped the list with a price-to-income ratio of 25.4. Of the 20 U.S. cities with the highest home-price-to-income ratios, all are in California – including Sunnyvale, with a ratio of 11.8 ($2 million vs. $169,781) and San Jose with a 10.5 ratio ($1.4 million vs. $133,835)…

From 2000 to 2022, the median annual household income in the U.S. increased by 77.6%, from $41,990 to $74,580, while the median home price nearly tripled — a 170% increase — from $123,086 to $332,8261, according to data from the U.S. Census Bureau and Zillow.”

California’s lagging economy hinders efforts to close state budget deficit

“According to Employment Development Department data, there are 200,000 fewer Californians in the labor force – those employed or seeking employment – than there were in February 2020, just before the pandemic exploded. There are 500,000 fewer employed, and 200,000 more unemployed.

While California’s unemployment rate of 5.3% in March was just a third of what it was at the height of the pandemic-induced recession, it was still the highest of any state, markedly higher than the national rate of 3.9% and nearly two percentage points higher than it was before the pandemic…Newsom’s Department of Finance says it “has not modeled a recession scenario.”

I guess they didn’t model a $45 billion deficit either.

Sorry, kids!

California home prices just reached a new record high

Then again, Florida and Texas Show Signs of Home Prices Falling

Gary and Karen Steppe listed a condo in Indialantic, Fla., in February for $294,900. They expected the two-bedroom vacation home, which is in an oceanside town near Melbourne Beach, to sell quickly. But the couple initially received no bids.

One reason: A rising number of homeowners in the area were also looking to sell. With more properties on the market, “buyers didn’t have that fear of missing out like they did when the inventory was less,” Gary Steppe said.

The Steppes cut the price, then accepted an offer in April for about $275,000. “I wish I had…sold it two years ago,” when similar condos were selling for higher prices, he said…In Florida and Texas, “we’re starting to get into a buyer’s market”…

As I tried to explain last year:

OK, just some aberrant thoughts here on “value.” Say you have a neighborhood of ten identical homes. In 2019, they all sold for $100k, so the “value” of the neighborhood was $1 million.

Now in 2023, the last one sold for $500k, so the “value” of the neighborhood is considered $5 million. If one house in the next year sells for $600k, then everyone will consider the value of their house to be $600k, and the neighborhood would be worth $6 million. But is it right?

In many ways this type of “valuation” is similar to the way crypto coins, baseball cards, stocks etc. are “valued” in aggregate (although I do concede that with stocks and houses, there is some there there.)

When Dogecoin briefly hit 60 cents, could you value all outstanding Dogecoins at that value? Of course not, but people did. Any real selling drove the price down dramatically. No way all holders could get out at 60 cents, 50 cents or 40 cents. Same is true of Nvidia.

Valuing housing markets is somewhat similar. If five homeowners in the above neighborhood were to suddenly decide to sell, would they all get $500k? Maybe, but doubtful. Say one seller was desperate, and sold at $400k [still a $300k gain!]. Would the value of the neighborhood suddenly fall by $1 million? Just as on the way up, I think it might, in the minds of realistic sellers, and certainly savvy buyers. The next eager seller might list at $375k, and buyers might offer $350k. I saw this sort of thing during the last housing bubble. Homes would list at last year’s price, and slowly chase the market lower, finally selling at a massively discounted price (from the initial offer).

I’m reminded of what a realtor I talked to in June 2022 told me: “Better to sell a year too early than a day too late.”

This is also why I think investors - especially big investors, even if small in their number of purchases - dramatically spiked neighborhood prices in recent years, because they weren’t averse to bidding above every else (they had cheaper financing than your 3% mortgage).

OK, bizarre real estate article of the week:

“Using figures from online marketplace Zillow, the new report found that 61.3% of homes sold in Texas during recent months moved for less than their market value.

Researchers looked at the 950 most recent properties to sell in housing markets nationwide to determine which had the highest percentage of homes sold below the listed price. Texas ranked as the state with the seventh-highest number of home sales below market value. Florida took the top spot, with nearly 70% of homes selling for less than they're worth, according to the study.”

This bugged me. The houses are “worth” what someone wants to pay for it, no more no less. This sort of nonsense is far too common in RE.

Rentals

“Overpaying seems to have been a feature, not a bug”

“One curious case is a 1970s vintage apartment at 14949 Roscoe Blvd in Panorama City. According to Zillow, the property was listed for sale in October 2019 for $6.3 million, or $396/sq.ft. Less than two years later, on September 2, 2022 HACLA bought it for $10 million, or $633/sq ft. The building remained vacant for a year while the agency spent additional money on upgrades and ADA compliance. The final cost to taxpayers may exceed $1,000/sq.ft. for a 50 year old building in a neighborhood whose median household income is 33% below the City of Los Angeles as a whole…

Then there is the case of the former EC Motel at 3501 S. Western Ave in Exposition Park. In 2019 the decrepit 31-room motel was assessed at $3.6 million. In or around October 2020 HACLA purchased it for $5.3 million. When we visited the building on May 12, 2024 it was vacant. All the doors and windows were sealed up with plastic sheeting and bore signs saying “MICROBIAL HAZARD/DO NOT ENTER/AUTHORIZED PERSONNEL ONLY.” The building’s exterior facade is crumbling and covered in graffiti. People present on the property ignored attempts to speak with them.”

'Wasn't meant to be': What happened to the best place in Calif. to buy an Airbnb

“In the frenzied real estate market of 2021 and 2022, owning a short-term rental in the Coachella Valley seemed like the perfect money-making venture. In 2022, one study called Palm Springs, the valley’s most well-known spot, the best city in a large market to invest in an Airbnb property. Prices skyrocketed, contingencies vanished, and homes sold quickly for far over list price. But just two years later, that meteoric rise has halted…

All cities within the Coachella Valley now have strict rules for short-term rentals, with most limiting them to 20% of the overall housing stock. Neighborhoods in Palm Springs are subject to that set limit, and most have already hit the threshold, creating a long waitlist for the coveted permits. Some cities, like La Quinta, have banned new short-term rentals. Others, like Rancho Mirage, have banned them altogether. Indian Wells and Cathedral City have vacation rental bans in effect with few exceptions.

That’s changing the buyer pool back to what it was traditionally like in the area…”

Tides’ original investors may be wiped out by preferred equity deal

“For a few months, Tides Equities has been desperately seeking preferred equity to shore up its investments in 30 apartment complexes. The company has said the money would help it through this punishing stretch of high interest rates and prepare the properties for sale in the next couple of years.

But there’s a tradeoff: If Tides scores that lifeline, some of its original investors could lose everything they put in.

Tides, working with AMC Investments, pooled together $277 million from limited partners in 2021 and 2022 to buy 28 properties across Nevada, Arizona and Texas.

Now, if Tides hits its $69 million preferred equity goal, 88 percent of that original equity will be wiped out, according to marketing documents obtained by The Real Deal. Just $30 million will be returned to the original limited partners.”

It’s not just Arbor: Syndicator lender Ready Capital chokes on past-due debt

“Days after multifamily lender Arbor Realty Trust reported a surge in delinquencies and a multi-billion-dollar effort to plug those holes, Ready Capital disclosed parallel pain points with a similar origin story: multifamily syndicators.

In its first-quarter earnings release, Ready Capital, a go-to debt source for firms such as GVA and Tides Equities, reported 10 percent of its $6.6 billion bridge loan book — the short-term floating-rate debt favored by syndicators — was over 60 days delinquent. That’s a 284 percent increase from the same period last year…

Both lenders issue a niche investment product known as commercial real estate collateralized loan obligations, or CRE CLOs. The securities comprise pools of bridge loans, many of them made to multifamily buyers.”

CRE

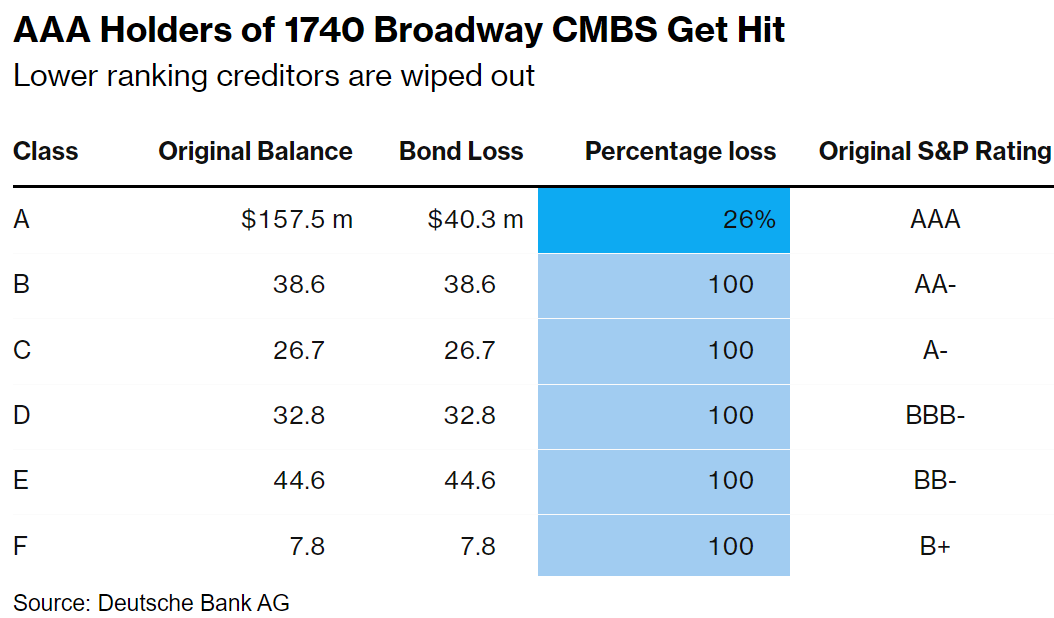

“For the first time since the financial crisis, investors in top-rated bonds backed by commercial real estate debt are getting hit with losses.”

“Buyers of the AAA portion of a $308 million note backed by the mortgage on the 1740 Broadway building in midtown Manhattan got less than three-quarters of their original investment back earlier this month after the loan was sold at a steep discount. It’s the first such loss of the post-crisis era, according to Barclays Plc. All five groups of lower ranking creditors were wiped out.

Market watchers say the fact the pain is reaching all the way up to top-ranked holders, overwhelming safeguards put in place to ensure their full repayment, is a testament to how deeply distressed pockets of the US commercial real estate market have become.”

For laughs, there’s the obligatory: “To be clear, no one is predicting a repeat of 2008…”

The above reminded me of this gem from Matt Stoller:

And, of course: “It [1740 Broadway] was bought for $605 million by Blackstone Inc. in 2014…While Blackstone spent tens of millions of dollars to modernize the building, tepid demand for office space made finding new tenants difficult. With no one paying rent, Blackstone stepped away from the property in 2022, defaulting on the loan.”

"Private equity firm the Blackstone Group remained the most active buyer of U.S. real estate for the past four years, between 2018 and 2022, with 233 deals."

From the preternaturally bullish Trepp CRE Podcast #258:

“Let’s not pretend we know what the worst case may be.”

“Starting out, my boss was extremely, extremely conservative. He could’ve looked at a 50% LTV loan and found something that he hated with it, right? He could find a reason to not do any loan, because he hated to lost money on loans. Anytime you hear, oh, well, don’t worry about this loan - it’s 50% LTV, it’s practically bulletproof - this loan [1740 Broadway, New York, NY] was 51% LTV as a senior mortgage on origination, and it still ended up losing 60%. The value declined 70% from origination. It’s tempting to bite on that narrative, to think, OMG, values of these assets have absolutely cratered, but - as my boss loved to say, we never know what the worst case scenario is - we can imagine what the worse case scenario - but let’s not pretend we know what the worst case may be.”

Wow, that takes me back to this from 2007: “To many strategists, stocks now discount an economic slowdown. Ian Scott, Lehman Brothers' London-based global equity strategist, says profits conceivably could fall as much as 45% if the U.S. slips into recession. But the stock market likely would fall no more than 10% to 15% from current levels even in this worst-case scenario.”

Ten to fifteen percent??? The stock market fell over 50%, and Lehman went bankrupt.

This is from Trepp. I’ll put it here for posterity, and maybe come back in a few years and re-read it.

“Depending on the gauge you look at, commercial property prices have declined by up to 17% from their early 2022 peaks. NCREIF, for instance, has values down 14.39% from their peaks. And the Trepp Property Price Index, which tracks repeat sales of a broader set of properties, is down at least 7%.

Values, however, still have a way to go before they hit bottom. Capital Economics, for one, expects they'll have dropped 27% from their peaks, when all is said and done, by the end of next year. But the London research outfit is even more bearish on the office sector, where values, it projects, would drop by 43% from their peaks.

That's all driven by the expectation that capitalization rates would need to climb by up to another 100 basis points. Office cap rates already are up an estimated 175 bps from their lows. Garden apartment cap rates are up about 80 bps.

We're already seeing some of that materialize. If you look at appraised values, office properties that back CMBS loans that have soured have seen a median drop of 45%. Granted, appraised values don't necessarily equal market values, but they're often calculated using market cap rates and discounts to actual net operating incomes.

Cushman & Wakefield recently pegged a 20.2% national vacancy on the office sector, which it said suffered 31 million sf of negative absorption during the first quarter, marking the ninth straight quarter where absorption was negative.

Meanwhile, you can argue that there's been relatively little in the way of price discovery. Take the apartment sector, which arguably has seen more sales transactions than any other sector. Still, volumes during the first quarter were down 28% from a year ago, according to CBRE. In Boston, 60% fewer deals took place during the first quarter than a year ago.

Meanwhile, Cushman & Wakefield had reported that new supply of apartments had outstripped demand during the first quarter, with 116,241 units getting delivered, but only 85,921 units getting absorbed. Granted, that's a sharp improvement from the 53,210 units that were absorbed during the same period a year ago, but it contributes to the sector's weakened fundamentals. The national vacancy rate, as a result, has hit 8.7%, the highest it's been since 2000.

But construction is ebbing, as only 285,000 units were started during the 12 months through April. That's down 50% from a year ago.”

“This index [Architectural Billings] usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment in 2024. Note that multi-family billing turned down in August 2022 and has been negative for twenty one consecutive months (with revisions). This suggests we will see a further weakness in multi-family starts.

Aby Rosen was New York real estate royalty. Is his office empire crumbling?

“Since 1991, Rosen has bought more than 50 buildings across Manhattan — including a half stake in the Chrysler Building. He has sold a few along the way, as well as diversified by buying buildings in Seattle, Tel Aviv and elsewhere. But the flashy purchases of a man with an equally showy social life may now be starting to catch up with him…

In 2018, Rosen told the Financial Times that the value of RFR’s portfolio had climbed to $14bn. Since then, the global real estate market has not been kind…

“Aby is at the top of the game in being astute, but even the people who were astute with their leverage are falling to these higher interest rates and being unable to refinance,” said Knakal at BK Real Estate Advisors.”

Was he really astute with his leverage though? Seems like the big CRE guys are always either billionaires or broke, and that’s fine, as long as Joe Six-Pack doesn’t have to bail them out.

Again, from a year ago, these classic Reddit comments:

Starwood Real Estate Income Trust, a $10 billion fund managed by Barry Sternlicht’s Starwood Capital Group, is taking a drastic step to preserve liquidity by imposing tighter limits on investors’ ability to pull money.

The vehicle, known as SREIT, will cap monthly redemptions at 0.33% of its net asset value, and 1% a quarter, according to a filing Thursday. Previously, the trust allowed withdrawals of up to 2% of net asset value in a given month, and 5% a quarter.

Red Lobster’s Demise Was Never About the Endless Shrimp “Blame private equity and a decade of mismanagement instead”

“Red Lobster has had a really rough last 10 years, maybe even worse than the rest of us; since 2021, the chain has had five different CEOs. In 2014, its parent company Darden sold Red Lobster to a private equity firm called Golden Gate Capital for $2.1 billion. That sale helped Darden pay off $100 million in debt and fueled significant growth for its other restaurants, like Olive Garden, in the ensuing years. Even when COVID hit in 2020, the company still managed to maintain positive cash flow as other restaurants floundered. Red Lobster, though, continued to struggle.

But again, it wasn’t because of the shrimp. Following the sale of Red Lobster to Golden Gate, the chain’s real estate assets were also sold off, which meant that the restaurants now had to pay rent on these locations to their parent company. As such, the company was stuck in leases for underperforming restaurants that it couldn’t afford. As with other private equity forays into industries like retail and media, Red Lobster’s new private equity owner saddled it with tons of debt…

That the endless shrimp could’ve spelled the end for Red Lobster is certainly novel, but the idea of private equity vultures swooping in to siphon every last drop of value from a beloved institution or brand before it inevitably dies? Well, that’s a tale as old as time.”

https://fred.stlouisfed.org/series/WSHOMCB

Rudy, you have quite a "Borgeshmord" (sorry Mason) to digest. One point. In The Free State of Florida, the same elected people bitching about the dopes in DC shouldn't control what happens in say, Alabama, decided that localities cannot regulate STR's. Coral Gables is a lit different than South Beach, but if their city councils decide to regulate them, too bad. Honest politicians are who once bought, stay bought. More to say, but let's kick it off there. Plus unique to Florida are new requirements for condos to have structural inspections done and keep reserves instead of kicking the can down the road until it collapses. Plus insurance. Lycky we're protected from darg queen bingo.

Melody and Tricia know this. You all Rock

Thought you might like this

https://substack.com/@thedutchinvestors/note/c-57918062?r=9wy0f&utm_medium=ios&utm_source=notes-share-action