Just a reminder to ignore everything Atlanta Fed President Raphael Bostic says:

Still plenty of liquidity.

The Rise of Jamie Dimon

Whitney Webb is the bravest investigative report around.

As JPMorgan’s ties to Jeffrey Epstein are being scrutinized in court, Whitney Webb reveals how the same powerful players who brought Epstein to prominence were largely responsible for the rise of JPMorgan CEO, Jamie Dimon.

This is an incredibly detailed and important article.

[USVI lawyer Mimi Liu asserts that] “Staley knew, Dimon knew, JPMorgan Chase knew” about Epstein’s criminal activities against minors…

In this article, we will examine how Dimon’s rise to become one of the most powerful men on Wall Street was largely reliant on top executives and directors of Bank One, which boasts incredibly close ties to The Limited’s Leslie Wexner and his right-hand man for many decades, Columbus-area real estate developer John W. Kessler. Kessler and other individuals tied to Wexner were the dominant forces that saw Dimon installed as Bank One’s CEO in 2000. Bank One was acquired by JPMorgan in 2003 and, shortly thereafter, Dimon became CEO of the combined entity. That acquisition, as well as the role of the Crown family in Chicago in Dimon’s selection as Bank One’s CEO, will be discussed in the second part of this series.

Yet, Dimon’s ties to the same networks as Wexner, particularly those characterized by their connections to organized crime and intelligence, preceded his time as Bank One’s CEO by many years. As this article will show, Dimon’s construction of what is now Citigroup, alongside his mentor Sandy Weill, began with their takeover of a company called Commercial Credit Corporation. That company, as well as its parent company, Control Data Corporation, had a troubling history of ties to intelligence networks that were extensively involved in criminal activity – including the so-called “private CIA” formed by CIA veteran Ted Shackley in the 1970s as well as individuals crucial to the Epstein story like Robert Maxwell.

Given these connections, JPMorgan’s claims that Dimon never knew what Jeffrey Epstein was up to during his time with the bank becomes much harder to believe. Furthermore, as future installments of this series will show, the players discussed here – Dimon and Epstein among them – were instrumental in the creation of what would manifest as the 2008 economic crisis. Not unlike some of the events that sparked today’s banking crisis, figures like Jeffrey Epstein, Dimon’s mentor Sandy Weill and the former Treasury Secretaries with close associations with both men, Robert Rubin and Larry Summers, appeared to have engaged in actions that would intentionally provoke the collapse of certain banks to further consolidate the banking sector for their benefit. The goal, both then and now, seems to have been a move towards the logical conclusion of the “too big to fail” banking model — the eventual creation of a centralized cartel of mega-banks that dominate, not only commercial banking, but also central banking.

Also, check out Turn off your tape recorders.

I'm the president of the shadow government

The grand governor of the Federal Reserve

Public enemy of the society

The one you cannot see

The 33 degree

So Alibaba is going to split into six companies you still won’t own?

Just bought some hot shares in Alibaba ? Actually, you didn’t. The entity listed on Nasdaq, with a market capitalization of $443 billion, is a Cayman Islands company with no hard assets or earnings. It is linked to the real Alibaba Group Holding, Jack Ma’s Hangzhou-based e-commerce juggernaut, by a web of contracts that could prove unenforceable in China.

Should people be encouraged to eat the foods decided best for them, such as a plant- or insect-based diet? CBDCs could do the trick. Should people be limited in how much they can spend per week on carbon-intensive purchases? CBDCs could help with that, too.

OneMain is part of Citigroup thanks to a Wall Street dealmaker named Sandy Weill, who realized the stunning possibilities of this kind of business back in 1986. At the time, Weill had recently been eased out from Shearson Lehman/American Express, a financial conglomerate he had helped to build. Eager to get back in the game, he bought a Baltimore firm called Commercial Credit.

In the view of Weill and his protégé, Jamie Dimon, their new acquisition was in the beneficent business of supplying “consumer finance” to “Main Street America.” Their office receptionist, Alison Falls, thought otherwise. Overhearing their conversation at work one day, she called out, “Hey, guys, this is the loan-sharking business. ‘Consumer finance’ is just a nice way to describe it.”

- Andrew Cockburn, Saving the Whale, Again: The catastrophic incompetence of Citigroup

I see stuff like this often over the past year - meh.

Every question I hear is “so what are you buying here?” Retail hasn’t even sold yet. This Conference Board survey thing may be true, but sentiment today is nowhere near as negative as it was during the “Financial Crisis” (i.e, Great Depression II) - certainly not-post Lehman.

This was the bottom: Warren Buffett, March 9, 2009

The unstoppable rise of government rescues The writer is chair of Rockefeller International [Oh boy. Still, not the worst FT op-ed I’ve ever seen.]

The rescues have led to a massive misallocation of capital and a surge in the number of zombie firms, which contribute mightily to weakening business dynamism and productivity. In the US, total factor productivity growth fell to just 0.5 per cent after 2008, down from about 2 per cent between 1870 and the early 1970s.

Instead of re-energising the economy, the maximalist rescue culture is bloating and thereby destabilising the global financial system. As fragility grows, each new rescue hardens the case for the next one.

“Our 21 Lehman systemic risk indicators are pointing at the highest probability of a crash or a sharp drawdown in the next 60 days—the highest probability since COVID,” - Larry McDonald told CNBC Tuesday, March 28.

So sometime around the end of May. Maybe.

Banks are tightening standards for both business and credit card loans.

Junk Debt Spreads Seem Ridiculously Low

Meanwhile…

The Bank of England is pushing pension funds to prepare for a bond market shock more than twice as severe as what they were previously tested against in an effort to avoid a repeat of last year’s gilt market turmoil.

Maybe 0 for 3 is considered good in Cricket but I'm going to have to give the BOE a failing grade here.

Distress in Office Market Spreads to High-End Buildings

Take 777 South Figueroa St. in downtown Los Angeles. Completed in 1991, the 52-story tower features a lobby with 30-foot ceilings and rose-marble-covered walls, a landscaped plaza, valet parking and concierge services. Many of its tenants are financial companies and law firms, according to data from CoStar Group.

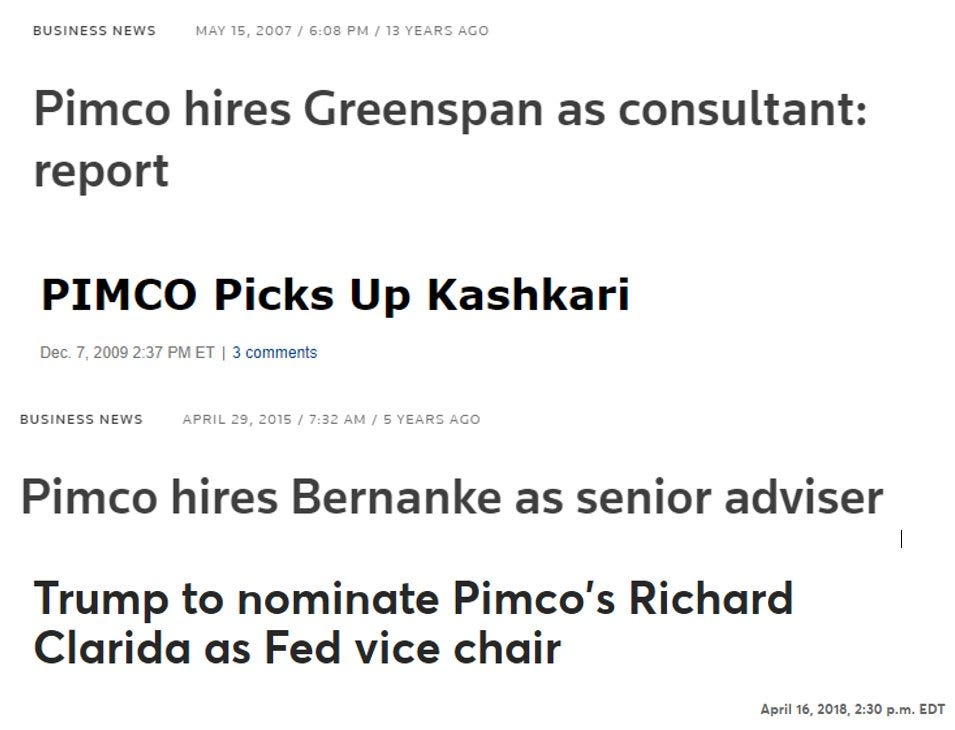

The owner, Brookfield Asset Management, recently defaulted on more than $750 million in debt backing the building and another Los Angeles tower. Meanwhile, asset manager Pimco recently defaulted on a mortgage backed by a portfolio of office buildings including the Twitter headquarters in San Francisco.

Debt on Blackstone buildings 47% more than portfolio’s worth: Moody’s I think they’re referring here specifically to 11 Manhattan multifamily buildings.

“Lowering interest rates are not going to save us. Fifty percent of the offices in America will go into foreclosure this decade. It’s like malls ten years ago. They were in the same place.” - Ben Miller, Fundrise

Phoenix Rising? No, No - This Bird Be Broken

While I was on the road someone asked me why no one was talking about this. My only answer is that you have to see it at scale to be convinced…otherwise you can just attribute it to one neighborhood or an isolated incident. But, you cannot deny it when you drive - avoiding highways - to ensure you see everything. Phoenix, like so many of the other boom towns, has been invaded with locusts in the form of spec homes.

Last Housing Bubble Anecdote: Around 2006 I knew someone who moved to the Inland Empire, CA (it’s an empire!), and went to visit. As I drove there I saw what seemed like miles of brown dirt hills, some with little housing developments on top like mushroom sprouting after a rain. Eventually I saw a scary looking sign twirler at my exit. As I looked for the address, I saw several hand-written signs on lawns - “For Sale -Make Offer”. This was in 2006.

The neighborhood already had clear erosion and drainage issues from a recent downpour too. The house itself, while new, seemed to be of the crappiest construction. I’m no expert, but the windows looked to be made of Styrofoam. They’d paid a pretty penny for it too. Eventually that ended in foreclosure. Anyway, that’s what the post kind of reminded me of.

From 1913 until 2008, the Fed owned precisely zero mortgage-backed securities. While the Fed’s monetary policy decisions still impacted conditions in the housing and mortgage markets, they did so indirectly through the influence the Fed’s purchases and sales of Treasury securities had on market interest rates.

In a radical “temporary” policy response to the 2008 financial crisis, the Fed began intervening directly in the mortgage market. Through a series of MBS purchases, the Fed’s MBS portfolio ballooned from $0 to $1.77 trillion by August 2017. The Fed subsequently altered policy and slowly reduced its MBS holdings. By March 2020, it held about $1.4 trillion in MBS.

When the COVID crisis hit in March 2020, the Fed decided to reinstate its 2008 financial crisis rescue plan. It resumed purchasing MBS as well as Treasury notes and bonds. By the time it stopped its purchases in the spring of 2022, it owned $2.7 trillion in MBS. The Fed had become the largest investor in MBS in the world. By spring 2022, it owned nearly 22 percent of all 1-to-4 family residential mortgages in the U.S.

Sorry crypto people. CNBC is talking about you again.

Miami's brutal crypto comedown The home of the NBA's Miami Heat — which was hastily christened "FTX Arena" after the city signed a $135 million deal with the now collapsed cryptocurrency exchange — has already been renamed the "Miami-Dade Arena."

Here’s a fun anecdote from David Dorr about trying to warn the City of Miami about crypto exchanges "facilitating money laundering and crime."

"They didn’t care."

Send this article to the next journalist who complains of how toxic everything is because they received a mean tweet.

I didn’t think Twitter could get any worse than it was pre-Elon, but I was wrong.

Hey Elon!

Matt Taibbi: People Can Win

the Cybersecurity and Infrastructure Security Agency (CISA), a creepy sub-division of the Department of Homleand Security…quietly eliminated its so-called “MDM” or “Misinformation, Disinformation, and Malinformation” subcommittee…

Just a year ago, the Department of Homeland Security was going all-in on the fight against “MDM.” The notion that America is fatally infected with “Misinformation, Disinformation, and Malinformation” was in fact the animating idea behind the asinine plan the Biden administration announced last April to institute a “Disinformation Governance Board,” which was to be headed by Nina Jankowicz, a self-styled Mary Poppins of digital rectitude:

America took one look at Jankowicz and at most a few fleeting moments considering the “Disinformation Governance Board” plan before concluding, correctly, that it was a beyond-loathsome expression of aristocratic arrogance that needed shutting down before the first Jankowicz presser. Characteristically, the press lied about the public reaction, claiming that the only displeasure was heard from the “GOP.” In fact, all sane people across the spectrum were instantly nauseated, their distress loud enough that the DHS hit “pause” on Jankowicz and the batty MinTruth plan after just three weeks.

The IRS Makes a Strange House Call on Matt Taibbi Probably just a coincidence.

Whenever someone who knows you disappears,

you lose one version of yourself.

Awaken

From your slumber

Terrific evidence-based email on "Misinformation, Disinformation, and Malinformation”.

Looking forward to similar quality emails from Rudy.

I'm getting my money's worth that's for sure! 😅