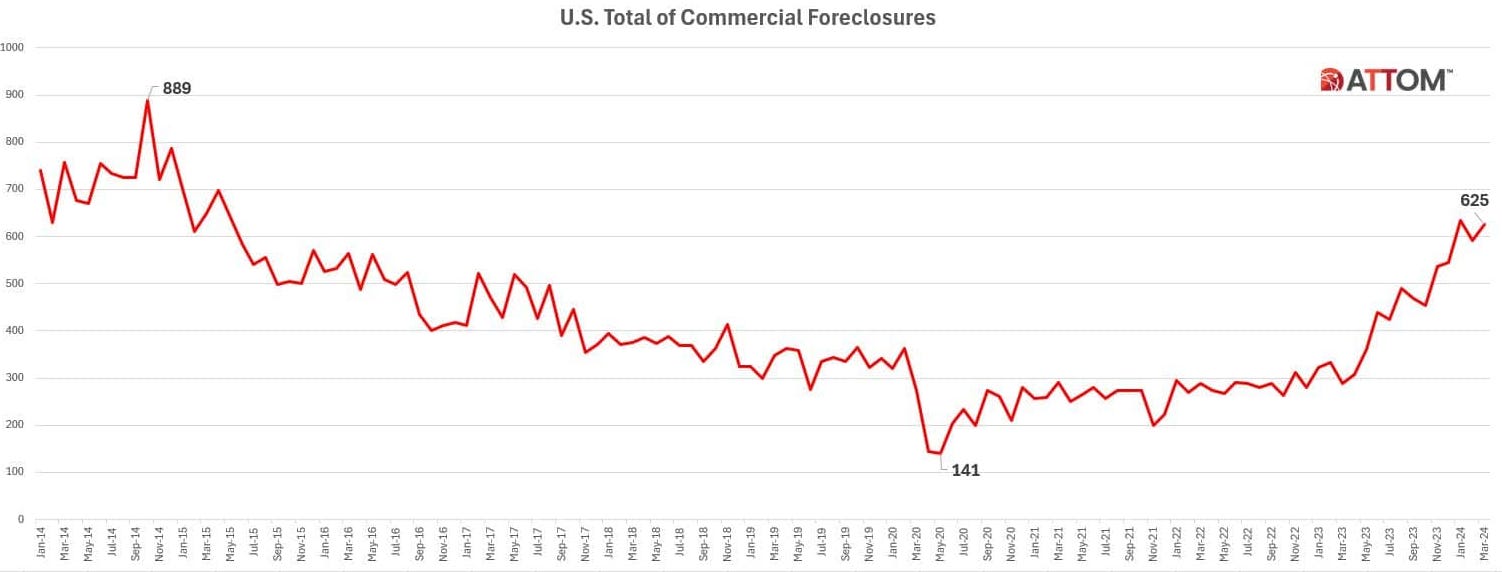

“I can assure you that there is a tsunami of terrible, terrible businesses and assets that need to be rationalized, and the total addressable market - if you think of it this way - is bigger than it's ever been, and growing.”

Fed Decision Tomorrow. No Change(?)

Number go up.

Five years of inflation in Buenos Aires via Chris Arnade

That's about a 96% annual empanada inflation rate.

"So we have the lowest interest rates in four-thousand and twenty years, and the ONLY observation of substantial volumes of negative nominal yields in 4,020 years, and we are maximum bullish on bonds, collectively. Now that, gentlemen, is a paradox."

Jim Grant on the Sherman Show podcast, November 2020

"The iShares 20+ Year Treasury Bond ETF (TLT), which sports a hefty $44 billion in assets under management, has absorbed a 49% downdraft since August 2020, remaining only 6.5% above its post-crisis lows."

- Grant’s

TLT

OK, sports fans. Today we have a number of observations from Jim Grant, plus Milton Berg, Frédéric Bastiat, Lyn Alden, Wilhelm Röpke, Chris Whalen etc. Also, Apple and Microsoft seen safer than Treasuries, hotel trends, the usual CRE, small business pain, short-term rentals, Egypt, Sedona, Florida, Dallas, Otis Redding, black holes, inflation(!), and other stuff.

Plus ça change, plus c'est la même chose

“Citing data from BondCliQ, MarketWatch pointed out yesterday that a pair of bonds issued by Apple and Microsoft maturing early next year have each changed hands at negative spreads versus Treasurys, i.e., investors perceive those securities to be sounder than U.S. government obligations. “That’s possible only because of the demand for credit”

- Grant’s

Milton Berg

“A central bank is not healthy for the strength of the economy. It's certainly not healthy for the typical United States citizen. It's very helpful for the Goldman Sachs Partners who benefit from the inflationary moves of the Fed, but it's not beneficial to a person who wants to save money.”

“Where did the Fed get the idea that a 2% inflation is ideal? It makes absolutely no sense. The ideal is 0% inflation, not 2% inflation. It absolutely makes no sense.”

US Hotels Report First Decline in Revenue per Available Room of the Post-Pandemic Era

“U.S. hotel revenue per available room declined 2.2% in March, marking the first year-over-year RevPAR loss of the post-pandemic era.”

“At the same time, moderate ADR [average daily rate] growth more than offset demand deficits, and the continued ability to drive rates despite economic doomsaying helped bolster industry optimism and RevPAR growth.”

This is how I see it - not just in hotels: fewer customers paying more.

More evidence of the bifurcation between the haves and have nots here?

“With the speed and size of occupancy declines accelerating through the classes, industry normalization no longer fully explains the phenomenon. All classes continue to report year-over-year declines in weekend occupancy through the first quarter, but only luxury through upscale classes have grown weekday occupancy. A general decline in overall leisure travel and increased selectivity in business travel appears likely.”

Self Storage Market Outlook – April 2024

“In March, all the top 31 metro areas had negative street rate growth year-over-year. The decrease in combined same-store rates for non-climate-controlled units and same-store climate-controlled units, ranged between -2.4 percent in Denver and -7.5 percent in Atlanta.”

Small changes so far, but interesting to me in that for the last couple years “Self Storage,” seems to have been universally considered one of the strongest CRE sectors.

Also, “Industrial” in general:

Industrial Owners In Dallas See Huge Value Increases, Warn Of Potential Shockwaves

“Dude, are they living under a rock?” was one of the more G-rated texts local property tax consultant Ryan Chismark received after the Dallas Central Appraisal District released its estimates for industrial values the morning of April 15.

After several years of juggernaut performance, the appraisal district is demanding industrial owners pay the piper. Despite the sector’s success, the timing of the decision has elicited strong reactions among owners struggling to reconcile double-digit increases with the loss of income they have endured over the last 18 months.

With initial value estimates showing increases of between 53% and 70% in just one year, consultants are preparing for a heated protest and litigation season, the outcome of which could put cash-strapped tenants at greater risk of buckling under the pressure.

“We’ve never seen more than 25% increases on initial values,” KE Andrews Director Tony Trahan said. “This is a complete shock to the system for all property owners and tenants — it came out of left field.”

US Small-Business Rent Delinquencies Rise to a Three-Year High

“The Small Business Rent report from Alignable, which provides an online networking platform for owners, found that 43% of small businesses were unable to pay their rent in full due to economic headwinds. That’s the highest rent delinquency rate since March 2021.

Independent restaurants are having the most trouble, with 52% not paying April rent on time. On the other hand, just 20% of small manufacturers are delinquent. More than half of small-business owners say that their rents are higher now than they were six months ago. Of those, 11% are paying at least 20% more than they did last fall…Increasing costs and declining revenues are hitting firms…Some 34% say they only have one month or less cash on hand. The survey of 4,171 small-business owners was conducted during the first three weeks of April.”

Best economy ever.

Retail Distressed Loan Rates (2005–2024)

So this is laggy data from FRED, but interesting…

Median Sales Price of Houses Sold for the United States/Median Household Income in the United States

Houses are too expensive.

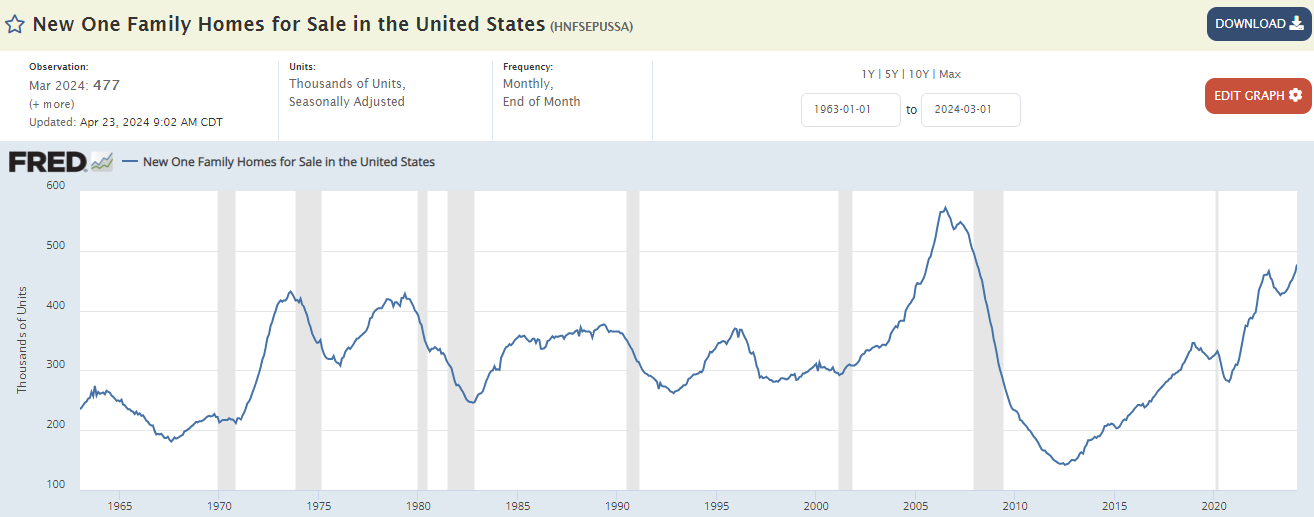

New Home Sales

I saw someone post the below chart of New one-family homes for sale, and someone else mentioned that - adjusted for population - it was not as high as it looked historically, which makes sense.

So I thought - what’s the ratio of new one-family houses sold to new houses for sale? I don’t know what this means for certain, but the sales/listings ratio is historically very low.

In fact, since 1963, every other time this ratio was at this level, we were in, or soon to be in, a recession.

Mortgage Rates

"It was the zero-percent era that made a 5%-plus rate dangerous."

- Jim Grant

“Over the past few years, the same mortgage rate that averaged around 3% to 4% went as low as 2% during the COVID-19 pandemic, when the Federal Reserve cut interest rates. “That’s an unreal market — it’s never happened in the history of our country,” Liniger said. “And so what you have is an entire generation of homebuyers who have gotten used to 2.5% to 5%.””

From 1971 thorough 2008 - according to Freddie Mac - 30-year fixed-rate mortgages averaged 9.11% (the median was 8.57%). Think about that.

Then from 2009 through 2021 - the ZIRP era - rates averaged 4%, and the median was 3.98%.

Also during the period the Fed bought $2.7 TRILLION of MBS.

Now we have over 7% rates, and they STILL own $2.385 TRILLION of MBS.

We’ve almost normalized rates. What hasn’t normalized is house prices (or the Fed’s balance sheet.)

“There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must before seen.

Yet this difference is tremendous; for it almost always happens that when the immediate consequence is favorable, the later consequences are disastrous, and vice versa. Whence it follows that the bad economist pursues a small present good that will be followed by a great evil to come, while the good economist pursues a great good to come, at the risk of a small present evil.”

Sedona

“Babies have been born in tents. There’s a secret food bank that school teachers – and others – visit. Families are sleeping in the woods. The lure of Sedona’s red rocks and crystal shops tends to eclipse an unfortunate truth— a growing number of people who work in Sedona can no longer afford to live here…The average home price in Sedona is $944,879 — nearly double what it was 4 years ago, according to Zillow. But many middle-class workers are not looking for a home to buy, they just want four walls and a roof to rent. Even a one-bedroom apartment can be a lot to wish for these days. “So what people used to pay, $1,200-$1,500 a month in rent are now paying $2,500 to $3,000 a month”…

Short-term rentals…make up almost 17% of Sedona’s housing inventory… ”corporations [are] coming in and buying a group of houses.” Some of those corporations…have made offers $100,000 over asking price.”

Short-Term Rentals

“You would see tourists on the streets in neighborhoods where there weren’t any hotels,” recalls New York-based artist and activist Murray Cox. The sound of rolling suitcases could be heard at all hours. Once tight-knit communities began to feel lifeless. When Cox ran the numbers on his own neighborhood — Bed-Stuy in Brooklyn — he found about 1,000 listings. Cox also heard horror stories from other parts of the city. “People would move into a building and then find that the building was full of tourists day in and day out,” he says. “In some cases, they would be so uncomfortable they’d feel forced to leave…

So, in September of 2023, New York City decided to do something about it. A series of bold requirements capped the total number of short-term rentals (STRs) and limited guests to just two at a time. They required STR operators to be primary homeowners — and to be present in the home while hosting. The city also promised to enforce those requirements, a move that would wipe out nearly 90% of active listings at the time.”

…“It didn’t take very long for people to realize the sharing economy was basically a scam…people weren’t just renting out a sofa or a spare bedroom.” Instead, people saw an economic opportunity they could invest in. And they started buying whole homes to rent out on Airbnb.”

About two-thirds of Airbnb rentals in the U.S. are in a property portfolio, which means the host owns and rents more than one property.

Nearly 23% of Airbnb hosts had two or more entire homes or apartments listed on the site. That made up 607,085 listings—or 63% of entire-home listings.

The top 1% of operators have more than 300,000 Airbnb listings among them—a stat that points to huge conglomerates gobbling up the market.

“In Atlanta, nearly 11% of all rental homes in the five-county area are now owned by three real-estate companies, a recent study by researchers at Georgia State University found. A 2022 analysis by the U.S. Department of Housing and Urban Development said 21% of Atlanta rental homes were owned by some large institution.”

Florida

“The rising cost of home insurance for one Palm Beach County condo is a story that seems to playing out at condos all across Florida. "It's shocking to watch in a few years to go from under $100,000 to pushing a half a million," Christina Auer said. "It's out of line." That fast increase in just a couple of years trickles down to the condo residents, who pay for it in their monthly fees…

Insurance experts tell WPTV that the days of cheaper policies are not coming back…."Everyone is selling," Auer said about her neighbors struggling with the insurance costs. "The cost is so great the condos aren't selling as quick as they were."“

Egyptian Real Estate Update

Fears grow Egypt’s huge new £46bn city could cause major headache 'as it's unaffordable'

“The city, known as the New Administrative Capital, is rising in the middle of the desert some 20 miles east of Cairo….

"It's a city for six million people and I don't think there are six million people that can actually afford this city."

The starting price for an apartment in the New Administrative Capital still under construction, the Journal reported, is at £64,230. In 2020, the average income of a household in an Egyptian urban community was approximately £2,087.”

“Sometimes I think war is God's way of teaching us geography.”

Via Trepp:

“Private equity real estate funds are expected to sell $2.2 trillion of commercial real estate assets worldwide between this year and 2029. That's because, as pointed out by Oxford Economics, a U.K.-based research company, those funds are reaching the end of their lifespan.

For starters, Oxford expects maturing funds to sell some $300 billion of properties this year and $400 billion in 2025. Closed-end private equity real estate funds have amassed quite the war chest over the last decade - about $1.2 trillion of commercial real estate assets under management globally. That's up from $500 billion in 2013…”

Now, if they’d only sell their residential holdings, and not to other private-equity firms…

Speaking of Trepp, here’s their latest podcast, where - for the first time I believe - someone suggests that possibly, maybe, things might end up kind of like 2008 (for CRE at least).

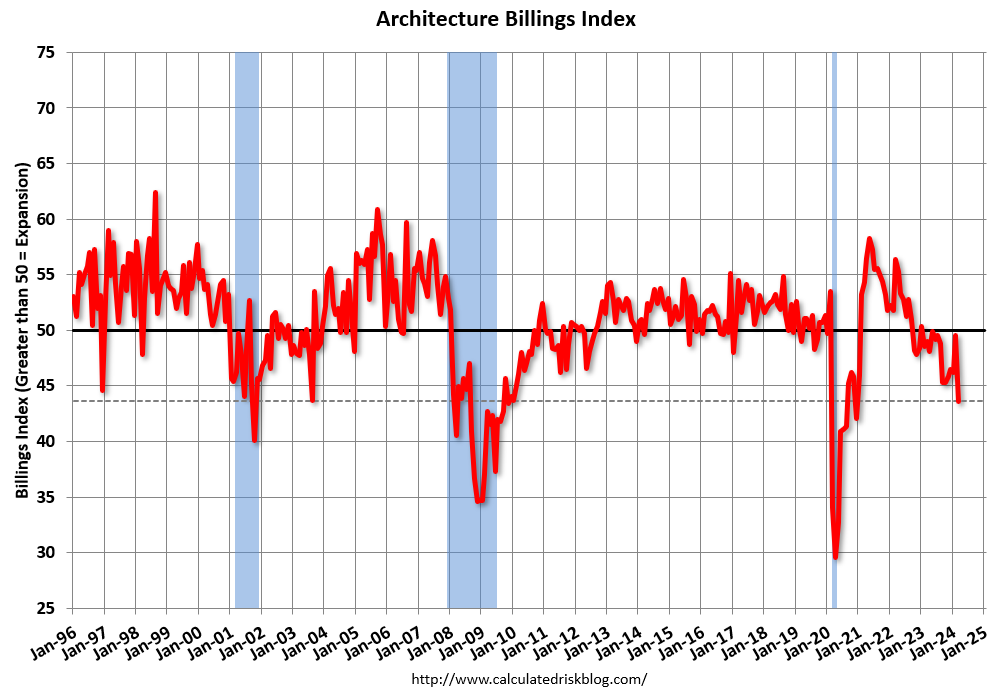

"Architecture firm billings retreat further in March"; Multi-family Billings Decline for 20th Consecutive Month

“The ABI score is a leading economic indicator of construction activity, providing an approximately nine-to-twelve-month glimpse into the future of nonresidential construction spending activity.”

Chris Whalen

“If investors cannot finance aspirational assets at zero carry, what does that say about the assets?”

“A number of players in the world of private equity have turned to leverage to offset the illiquidity of PE holdings, a decidedly bad choice in a rising interest rate market. The assumption, of course, is that the Fed eventually will drop short-term rates…short-term funding is now above the average asset returns of many banks. Funds, dealers and other nonbank players are points underwater on funding vs existing assets. PE assets that were acquired or financed during the 2019-2022 period are likewise upside down in terms of today’s cost of leverage…

The brutal math of cap rates makes you appreciate why the FOMC says that “price stability” = 2%. For the American commercial real estate market to work, it needs at least 2% inflation annually or the whole heavily leveraged pile of bollocks collapses. But the same can be said of leveraged PE investments, especially the aspirational stories that assume an easy exit via IPO…”

“The prospect of heavily leveraged PE [private-equity] portfolio companies eventually defaulting on debt raises fond memories of fraudulent conveyance claims years ago in a certain federal receivership in Houston, TX. The political backlash against PE firms raping private companies and then leaving the creditors for dead in bankruptcy is building. More of such behavior suggests may tip over the proverbial dung wagon in favor of federal legislation to discourage leveraged PE transactions.” - Whalen

“0% inflation feels like deflation for people who have made commitments that depend on gradual currency devaluation.”

Multifamily

Tides Equities faces three foreclosures in Fort Worth

(I’ve mentioned Tides a few times.)

“Three Fort Worth properties owned by the Los Angeles-based firm are scheduled for a May foreclosure auction…Tides, a syndicator that pools money to buy multifamily properties, has been struggling to pay off debt tied to its properties for over a year, after rising interest rates ballooned debt service across its massive multifamily portfolio.”

“We were able to get a loan modification from the lender, but unfortunately it wasn’t enough of a concession to change the math equation to risk new investment dollars into the asset. It is imperative that we never risk good money after bad unless we feel there is a path to recouping not only this new money, but a majority of the original investment as well.”

“Tides is not the only multifamily syndicator that has landed in trouble, after racking up portfolios of value-add apartment complexes while debt was cheap. GVA, another syndicator, is delinquent on more than $600 million in securitized debt and has lost a number of properties in Texas to foreclosure.“

S&P 500 Priced in Oil Since 1983

S&P 500 Priced in Gold since 1980

S&P 500 vs M2

(I know some people don’t like these sorts of charts, and that’s OK.)

Emerging Markets (EEM) Relative to the S&P 500

“Inflation is the way in which a national economy reacts to a continuous overstraining of its capacity”

“We can see the problem in its true perspective when we come to realize that inflation is the way in which a national economy reacts to a continuous overstraining of its capacity, to demands which are extravagant and insistent, to a tendency towards excess in every sphere and all circles, to presumptuous overconfidence in oneself, to a frivolous attempt always to draw bigger cheques on the national economy than it can honour and to a perverse desire to combine what is incompatible.

People want to invest more than savings permit; they demand wages higher than the growth of productivity justifies; they want more imports than exports can earn; and above all, the government, which should know better, raises its claims on this overstretched economy higher and higher. Thus, there is a riot of claims and an insufficiency of goods produced to meet them.

Just as there are organs in the human body, in which, if consistently abused, ailments slowly but surely accumulate, eventually taking their revenge, so the national economy has its own equally sensitive organ. That organ is money. It becomes feeble and ceases to resist, and it is this enfeeblement which we call inflation, a dilation of money so to speak, a managerial disease of the national economy.”

Wilhelm Röpke, 1957

Jim Grant comments:

Röpke “hates inflation, as we all should, whatever our preferred school of economic thought—Austrian, monetarist, Keynesian or other. The integrity of the currency is a moral question, because money is work and work is heartbeat sand heartbeats are finite.

If you accept that proposition, you will have scant patience for the Fed’s self-assigned remit of skimming 2% a year from the purchasing power of the dollar. What is it, really, besides monetary shoplifting, tricked out in the econometricians’ algebra?”

“Net negative savings is no everyday occurrence. Prior to 2023, the U.S. Bureau of economic Analysis identifies only seven prior examples since 1929. rach was a period that most Americans would probably not care to relive: 1931–34 and 2008–10. Last year was the only one of the seven that was not the occasion of, or in close proximity to, a major slump.” - Jim G.

Lacy Hunt discussed this in my recent post, Chancellor and Hunt.

“I would say the combination of very high public debts, substantial ongoing deficits, and then pretty substantial interest payments on those existing debts has kind of put them [the Fed] past the Event Horizon, where that the set of choices they have is now very narrow.”

At this point it seems pretty bleak. Damned if you, damned if you don’t in terms of ways to position oneself for possible futures.

On one hand, being in a net short fiat position (through mortgage, other debt) seems best if the path to Weimar-level hyperinflation is relatively straightforward.

But that same positioning is devastating if we have a few deflationary collapses in between.

Hard to know what we’ll encounter on the road that lies ahead even if we know the destination.

I remember after my first trip in Feb 2023 when I talked about the sheer amount of self storages out there I saw on the road on xTwitter and how it was problematic (always right next door to a new car wash and new-build site) I would get serious hate. Wild. Great post!