Need for Speed

Democratizing Gambling

Ring the bells that still can ring

Forget your perfect offering

There is a crack in everything

That’s how the light gets in.

"We shall have world government, whether or not we like it. The question is only whether world government will be achieved by consent or by conquest."

Father of the Federal Reserve Paul Warburg's son, James, in 1950

A very good podcast with Whitney Webb and John Titus

“According to our adjustments, cumulative inflation since 2019 has been understated by nearly half. This has resulted in cumulative growth being overstated by roughly 15%. This is a large amount for just 5 years – for perspective, peak-to-trough drop in real GDP during the 2008 crisis was 4%.

Moreover, these adjustments indicate that the American economy has actually been in recession since 2022.”

“One of my core beliefs is that inflation tends to be a killer of political careers. If the unemployment rates moves from three to five, you got an additional 2% of people that are pissed off at you, but if the inflation rate moves from zero to four - as just occurred in Japan - you've got 100% of people pissed off at you.”

Tom Hoenig on QE

“I think it was just being too focused on a short-run goal rather than looking to the long run”

Paging Bastiat!1

Finance Rate on Consumer Installment Loans at Commercial Banks, New Autos 48 Month Loan

“To be ignorant of what occurred before you were born is to remain always a child."

- Cicero

“Why affordable housing is at risk of disappearing across the US”

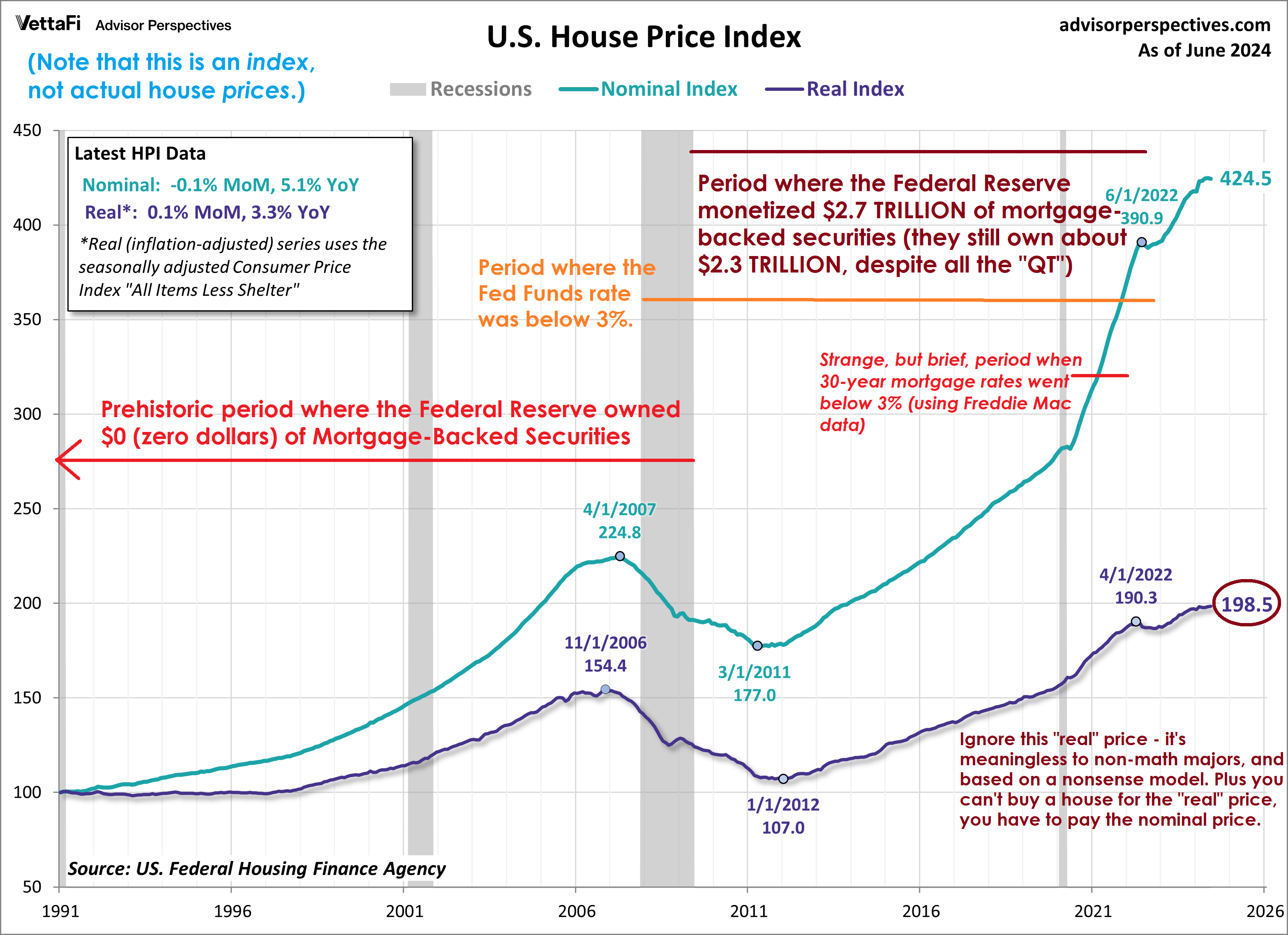

Meanwhile, the Fed owned $0 MBS in 2008:

Melody Wright on California Real Estate

Welcome new paid subscribers. Another eclectic collection of oddities below. Luke Gromen, Chris Whalen, housing, autos, sentiment, David Lynch, The Wire, uncertainty, Hot Chocolate, and more. Godspeed.

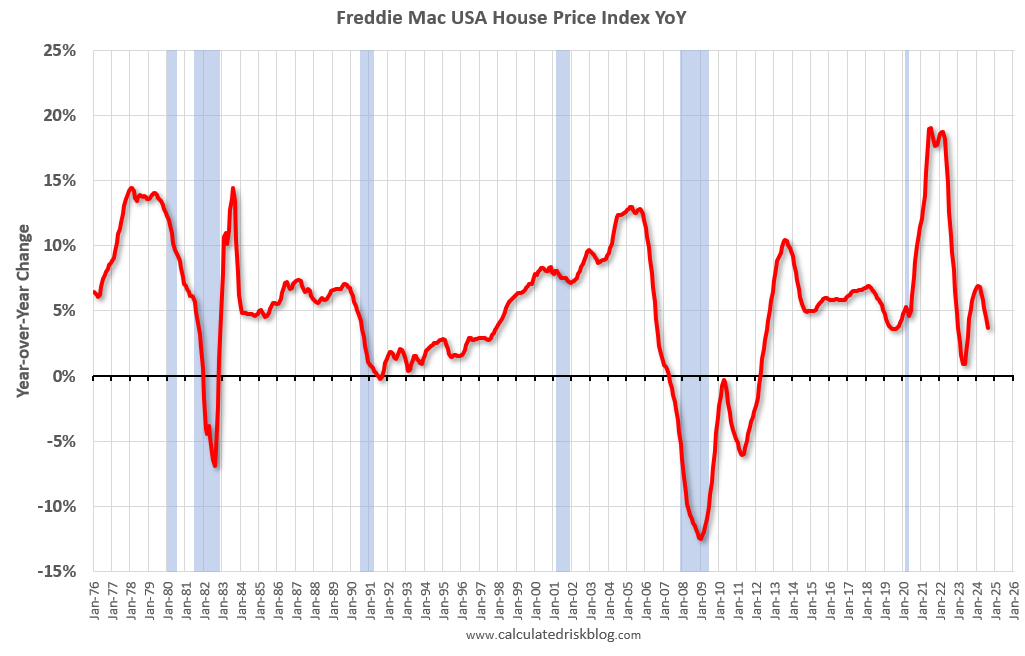

Freddie Mac House Price Index Up 3.7% Year-over-year

My Annotated Guide to the U.S. Housing Market

“The multifamily criticized loans2 rates by MSA are really interesting. The five metros with the highest criticized loan rate for multifamily loans are Atlanta (over 50%), Phoenix (43%), Houston (40%), Dallas (30%), and Washington DC (25%).”

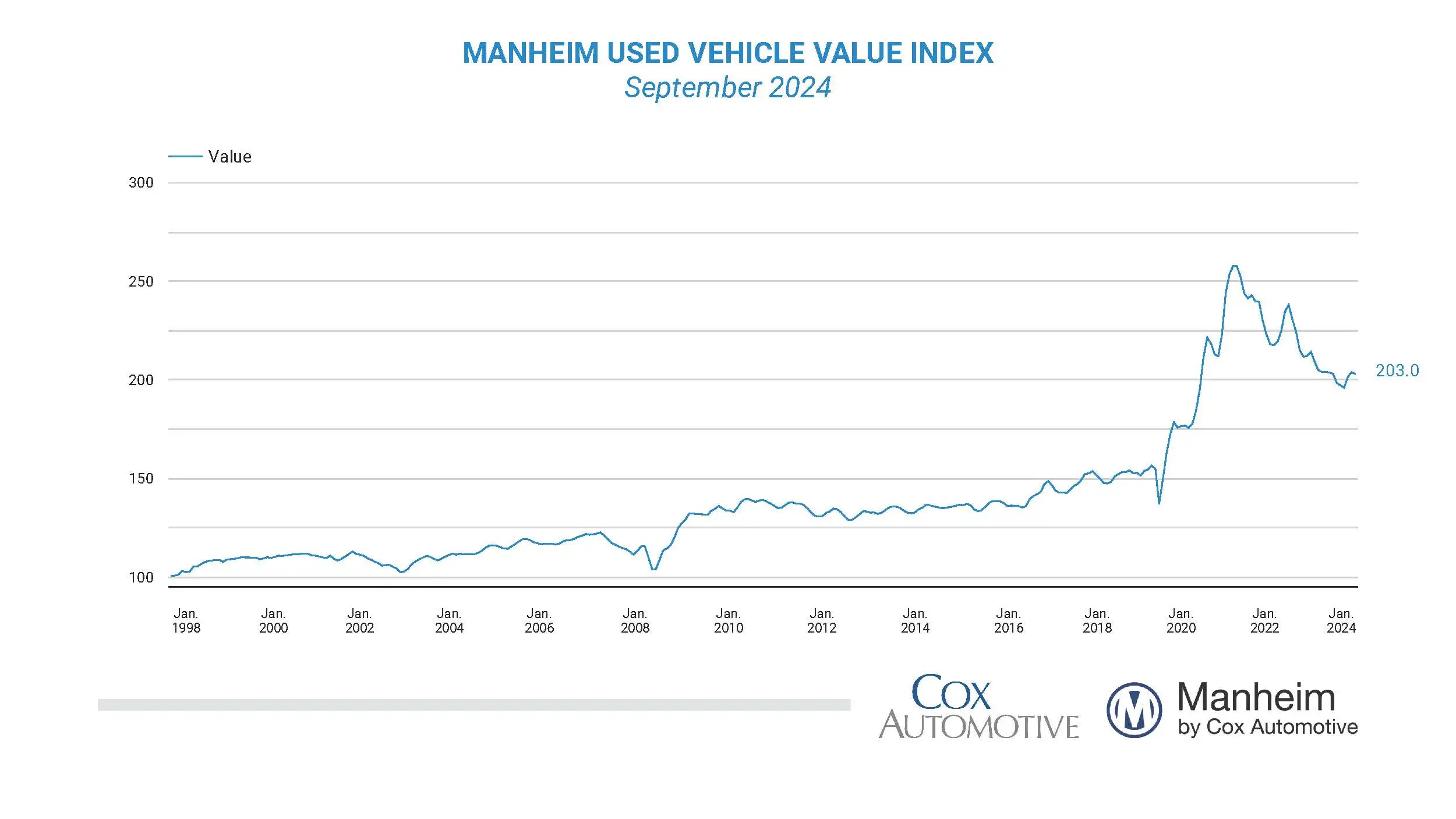

Wholesale Used-Vehicle Prices Declined in September

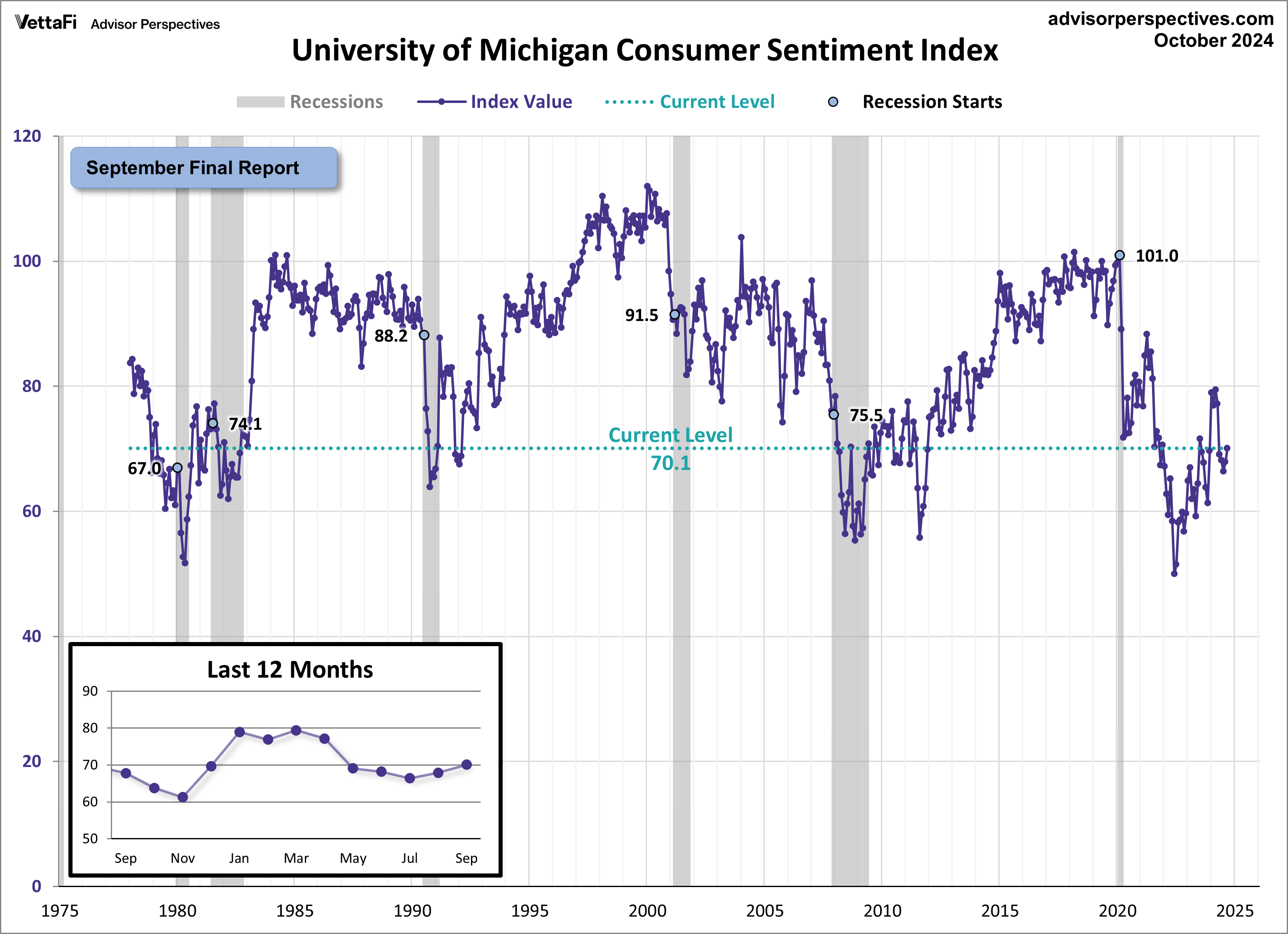

“Michigan Consumer Sentiment Hits Highest Since April 2024”

Green shoots.

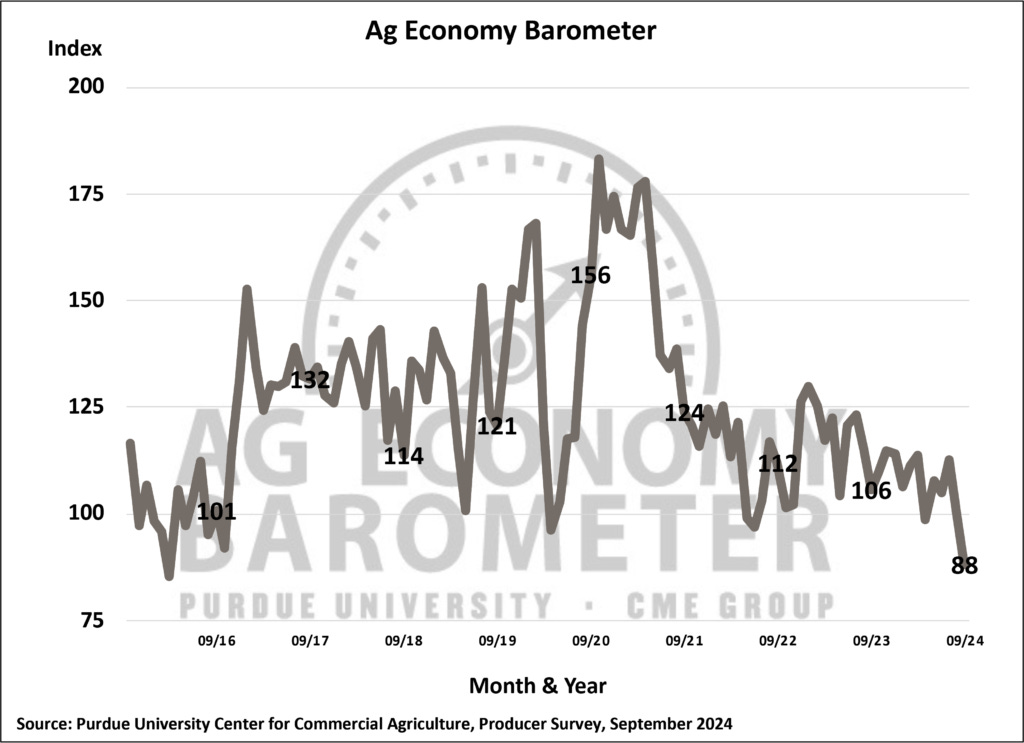

Farmer Sentiment Reaches Lowest Levels Since 2016 as Income Expectations Weaken

NFIB Small Business Uncertainty Index

2000-2009 2009 Monthly 01JAN1970- 40 2010-2019 Copyrighte 2024 Bloomberg Finance L.P. 2020-2029 08:59:4'.")

“Small business owners are feeling more uncertain than ever,” said NFIB Chief Economist Bill Dunkelberg. “Uncertainty makes owners hesitant to invest in capital spending and inventory, especially as inflation and financing costs continue to put pressure on their bottom lines. Although some hope lies ahead in the holiday sales season, many Main Street owners are left questioning whether future business conditions will improve.”

Luke Gromen

MacroVoices #448 Luke Gromen: Why the Gold Recycling Trade is Accelerating

“They have been managing to Treasury volatility. As long as Treasury volatility stays low enough, Treasury markets function, and as Treasury markets function, it's fine, but they have repeatedly injected whatever dollar liquidity is needed to keep Treasury markets functioning. They've been doing it for five years, since the repo rate spike.”

“In June of 2014, when the weighted average maturity, or WAM was 68.4 months, and it was projected to go from 68.4 months in 3Q ‘14 to about 83 months by 2024, where we are today. As John Lennon once said, life was what happens to you while you're busy making other plans. Reality is, that global central banks stopped growing holdings of treasuries the very next quarter after that report came out, and US weighted average maturity has basically never risen from that point. It's basically been flat, with a dip down and a dip back up and come back to this level. So, we're still right around 70 months, when, remember, the plan was in 2024 to be at 83 months. And the question is, what happened? Well, what happened is what we just described, which is when central banks stopped growing their marginal holdings, and then we had to shift to the front end, to where the demand was. And that brings us to the point of this roll dynamic we talked about back in 3Q ‘23, in October of ’23, then Treasury Secretary Jack Lew gave a testimony to Congress around the debt ceiling. He said, “every week we roll over approximately $100 billion in US bills. If US bondholders decided that they wanted to be repaid, rather than continuing to roll over their investments, we could unexpectedly dissipate our entire cash balance.” There is no plan other than raising the debt limit that permits us to meet all of our obligations”

“We were astonished by what we found, which is that the roll that was, the gross issuance that was $100 billion a week in 3Q ‘13, that was $200 billion a week in 3Q ‘18, it's now over $500 billion a week. That's a CAG, or a compound annual growth rate, of over 16% in the past six years. And again, it's the same issue. It's that we are issuing more and more debt, more and more frequently at the front end, because the debt is getting so big, and the sort of big, patient, nonprofit, motivated, creditor central banks haven't bought any US Treasury bonds in 10 years. And so again, this is fine. This doesn't mean, oh, the world's coming to an end, but this is like payday lending kind of stuff, and it has, again, a very specific set of contextual implications, which is issuing more and more bonds at shorter and shorter durations with more and more fickle creditors, in a world where the Fed and Treasury are not allowing Treasury volatility to go above a certain level. The more you issue with the short end with fickle creditors, the more you have to make sure Treasury volatility stays low. And the more you keep Treasury volatility low, the more you got to keep equity vol low, and the more you got to keep equity vol low, the more you're going to see earnings multiples, equity multiples, equity market prices and inflation, and nominal GDP growth had higher sort of ad infinitum, until you drive stocks in the economy high enough that your tax receipts are really reducing your expenditures relative to your receipts.”

Chris Whalen

“We manufacture the appearance of growth”

“This goes back to the writings of Jim Grant and others - we manufacture the appearance of growth through inflation and through monetary policy, but is that incremental additional dollar of GDP growth that the Fed manages to eke out really a dollar in real terms, or is it just nominal? In other words, are we actually growing this economy or is it just fluff, in terms of inflated dollars? I think it's the latter. I think that's the reason that low income families in this country are having such a tough time, because Consumer Price inflation is the big issue this year. That's the only issue that matters, and nobody wants to talk about it.”

Whalen: “What are you doing when you hand millions of families $25,000, and you have them go into a supply-constrained market? Entry-level homes, let's say the bottom quarter, bottom 30% of homes, which are a couple hundred, but there's no supply, so automatically those buyers, those new entrants into the market are going to become the price setters, and prices are going to have to go up….that would be a transfer from people buying those homes to the people selling…we're going to transfer $150 billion to the people who sell their homes.

LaRoche: And those are the asset holders who probably benefited from all of this.

Whalen: Yes.”

“A lot of managers sitting on assets bought at high multiples don’t really want to face reality.”

Easy-peasy credit conditions have allowed p.e. promoters to issue new debt earmarked for their own pockets like never before, as $18.3 billion in domestic leveraged loan supply backing so-called dividend recapitalizations came to market in September according to PitchBook, blowing past the prior single-month peak of $13.4 billion established in July 2021. The year-to-date tally through Monday stands north of $70 billion, nearly matching the record $76 billion logged during full-year, bubbleicious 2021 with one fiscal quarter to spare.

Yet a still-moribund IPO market and muted merger and acquisition activity following the post-pandemic tightening cycle starkly contrast with that ebullience. Private equity exits in the U.S. registered at $141.4 billion over the first six months of 2024 per data from Cambridge Associates, trailing 2023’s near $300 billion full-year pace, which already marked the weakest such output in over a decade.

“There’s been such a lack of M&A activity and leveraged buyout activity that a lot of sponsors are looking at how to return cash to their investors, and if you’re not selling companies, one way to do it is to take dividends,” Lauren Basmadjian, global head of liquid credit at Carlyle Group, told Bloomberg Thursday.

On a global basis, distributions as a share of paid-in capital (DPI) among fund vintages spanning 2007 to 2014 topped 1.0 times (i.e., investors received more cash than their initial outlay) by year seven on average, relays the Financial Times, citing Preqin-compiled data. In contrast, DPI for vintage years 2015 to 2018 stand at less than 0.8 times as of year eight, while distributions for 2019 to 2022 have returned well below 20 cents per paid in dollar on average. Overall, the unrealized industry backlog of unsold portfolio companies stood at a record $3.2 trillion as of Dec. 31 per Bain & Co., double that seen just prior to the pandemic.

“Exits and pressure to return liquidity is sort of the big new topic for the next 12 to 24 months," commented CVC managing partner Giampiero Mazza during a Bloomberg-hosted event in Milan Thursday. “A lot of managers sitting on assets bought at high multiples don’t really want to face reality.”

…“We signed up for a 12-year fund,” Brian Dana, managing principal at Meketa Investment Group, groused to Bloomberg over the summer. “Now they’re asking investors to wait another seven years to get their money back.”

I’m reminded of James Aitken’s August 2024 comment, “The idea that financial conditions, by the way, are actually tight is absolutely laughable...if financial conditions are tight, how come Ares just raised 37 billion in private credit?”

Also via Grant’s:

“U.S. investors funneled a net $282 billion into exchange traded funds over the three months through September per data from Morningstar, pushing year-to-date inflows to $696 billion. That’s on pace to top the $900 billion full-year peak established in 2021 and leave the $1 trillion figure “well within reach,” as the typically bountiful fourth quarter gets underway. Stateside ETF assets reached a tidy $10 trillion, up tenfold since 2010.

ETFs now offer nearly universal access to asset classes and strategies that were once available only to the world’s most sophisticated institutional investors,” Amrita Nandakumar, president of Vident Asset Management, commented on Bloomberg Television, adding that last week’s milestone is a “testament to how much ETFs have democratized investing.”

As an aside…

“We believe we have a responsibility to democratize investing. We’ve done a great job, and the role of ETFs in the world is transforming investing. And we’re only at the beginning of that.” - Larry Fink, July 2023

Back to Grant’s:

“Indeed, Wall Street’s amply demonstrated ability to meet investor demand is once again on display. For instance, 532 such funds now hold a position in AI lynchpin Nvidia according to ETF.com, up from 482 late last year (Grant’s Interest Rate Observer, Dec. 22). This includes funds devoted to tracking only one company, such as the GraniteShares 2x Long NVDA Daily ETF (ticker: NVDL).

…newly minted peer T-REX 2X Long MSTR Daily Target ETF (ticker: MSTU), which ups the ante via 200% daily MicroStrategy exposure, gathered more than $72 million in assets a mere seven trading days after its debut. “Both have robust liquidity,” Balchunas posted on X. “I didn’t think there was room for both. . . it just [shows] how much ‘need for speed’ there is out there.””

‘Private credit’s latest contraption’

The continued financialization of everything.

A few weeks ago, I got a press release from the venerable Carlyle Group announcing the latest cutting-edge contraption in the private credit frenzy. But this particular deal being announced stood out to me. Carlyle said it was partnering with specialised finance upstart Unison, whose founder and chief executive, Sponholtz, is a former Barclays Global Investors executive.

Sponholtz had long believed there was room for innovation in home lending, specifically in how Americans could monetise home equity. Home equity loans, home equity lines of credit and reverse mortgages were all debt products that, one way or another, had to be paid back with interest by homeowners…

Not surprisingly, Unison’s immediate cash does not come cheap. The company will buy as much as a 15 per cent interest in homes, spending between $30,000 and $500,000 per home. The homeowner will pay for an appraisal and Unison will invest at a 5 per cent discount to that appraised value. There is also a 3.9 per cent transaction fee.

And finally at the time of sale, which must happen by year 30, Unison is owed four times the proportion it put in. To put some numbers on it, imagine a deal where the firm buys 10 per cent of a house worth $1mn.

In a decade, let’s say the house is worth $1.5mn. Unison gets its $100,000 back as well as 40 per cent of the gain, or $200,000. The house jumping 50 per cent in value over 10 years reflects an annualised rate of return of 4.1 per cent. Unison’s $100,000 investment turning into $300,000 reflects a return of 11.6 per cent.”

“…Unison wondered if it could merge housing debt and housing equity into a single product. It has, as a result, created the “equity-sharing loan” that resembles a corporate convertible bond with its fixed obligation attached to a call option.

This is how it works: a homeowner takes out a second mortgage in order to get immediate cash — but the interest rate charged on the second mortgage is lower than the market price. In exchange, Unison gets 1.5 times its proportion in the future appreciation of the house (note that this is less than the four times it is owed in the straight equity product described above).

In an example on its website, Unison said it would shave off almost 2 percentage points from a straight loan interest rate (charging 5.2 per cent annually instead of 7 per cent) in the cash “coupon” it is owed. At the end of the 10-year loan, Unison would, however, get its 1.5x appreciation share as well as the capitalised sum total of the 1.8 per cent initial cash interest rate savings (that’s the 7 per cent minus 5.2 per cent).

Carlyle estimates the all-in cost of capital of the equity sharing loan of 10 per cent to 11 per cent: 6 per cent cash interest, 2 per cent of the cash deferred “payment-in-kind” interest and 2 to 3 percentage points of kicker from the equity sharing slice.”

Home equity Unison's CEO Thomas Sponholtz said "We are trying to democratize the rich relative."

“If people in America even understood how the Fed was born, the context of that…banks and individuals - with the will to power that would make Nietzsche blush - became a Constitutionally-allowed fourth branch of government.”

“You know, it does start to feel a little bit like too big to fail, right?

Laura Goodwin, on Boeing

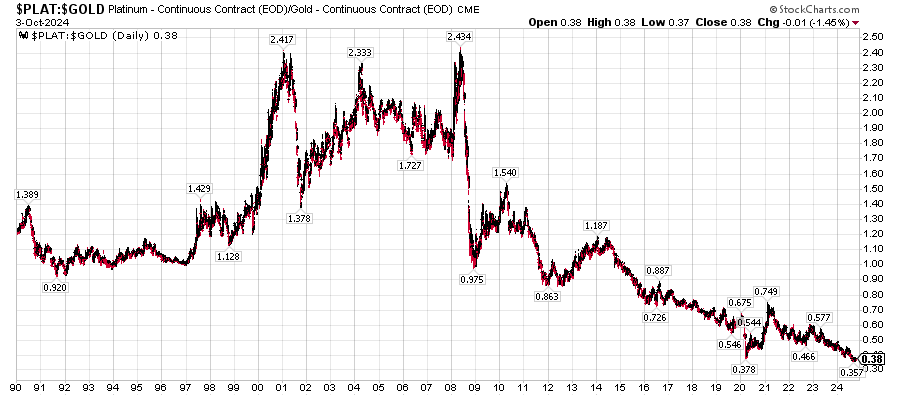

Platinum vs Gold Ratio

Palm Valley Capital Quarterly Letter

This was sent to me by several people. The fund is run by Eric Cinnamond, a very eclectic value investor (I have no money with the fund, but I’ve heard him interviewed before.)

Every day for two years, a steady stream of levered-up multimillionaires has filled CNBC's green room.

"When asset prices are at record highs, what’s more shameful than aristocrats pleading for easy money?"

Eric Cinnamond

Nick Bryant: ‘P. Diddy and US Attorney Damian Williams: Let the Games Begin’

“Andre Damian Williams Jr., U.S. Attorney for the Southern District of New York, once again has the distinction of covering up child sex trafficking. He received that distinction for overseeing a federal grand jury that didn’t indict Sean “Diddy” Combs on a single count of child sex trafficking and/or molestation…

Williams, however, oversaw the Ghislaine Maxwell trial, which was a travesty of justice even before it commenced: Federal prosecutors only indicted Maxwell on one-count of child trafficking, even though her and Epstein had trafficked children for approximately 25 years. Moreover, the federal prosecutors were aware of over 30 child Epstein trafficking victims, but they only called four victims as witnesses, and those victims had been exclusively molested by Epstein and Maxwell. The federal prosecutors were aware of various Epstein procurers (pimps) and numerous perpetrators. But the prosecutors’ flagrant objective was a cover up of the procurers (pimps) and perpetrators in the Epstein network. One-count of child trafficking carries a 15-year to life sentence, and Maxwell was sentenced to 20 years.”

"The American Constitution has been stopping stupid people doing stupid things for a long time. It's a very good constitution."

- Russell Napier

And then we have garbage like this:

“I had the great privilege of meeting John P. St. John, badge No. 1 in LAPD robbery and homicide. He was in charge of the Black Dahlia case. One day John St. John called me and said he’d like to take me to dinner, to show me something. I met with him at Musso & Frank about 8:30 at night, had dinner, and after, he opened his briefcase and took out an 8-by-10 black-and-white, glossy, super beautiful, crisp, clean, focused detail picture of the Black Dahlia laying in the grass. And he said, “David, what do you see?”

I looked at it intensely for like 10 minutes. I finally said, “I don’t see it.” He smiled, put the photo away and never talked about it again. I thought about it day and night; it plagued me. It finally dawned on me much later, that the photos he showed me were taken at night. She wasn’t discovered until the next morning.”

Detective Jimmy McNulty on Presidential Elections

“…These guys - it doesn't matter who you got. None of them has a clue what's really going on. Where I'm working every day, the only way any of them will even find West Baltimore is if, I don't know, Air Force One crash-lands into Monroe Street on its way back to Andrews. It just never connects. Not to what I see, anyway. Hey, that's just me, though.”

A lot of people feel this way nowadays. The two party monopoly’s choice of candidates increasingly seems to be a threat to democracy® too.

Speaking of The Wire, here’s a great commentary on “The Drug War™.”

No, the world doesn't hate America

“That the US is loathed, and as an American you will be bombarded with criticism if you travel abroad, is something you hear a lot from US elites, and while true if your trip is limited to the Sociology department of a foreign university, it’s not the case at all with “normies” in almost every country, who have a great affection for America, or at least the idea of it, because they are not obsessed with current events, and more importantly, are capable of separating politics, and the policies of a political class, from a country’s citizens. If anyone understands you shouldn’t equate a country’s foreign policy with its residents, it is someone who has grown up in a place like Senegal, Bulgaria, or Turkey, with a corrupt and/or autocratic past/present, and a tiny out of touch ruling elite.”

"When I heard Vice President Harris brag about former Vice President Dick Cheney endorsing her candidacy, that put the exclamation point on the fact that the leaders of the Democratic party are for war. I am not."

Dennis Kucinich, former Democratic Congressman

“Ben Lamm, CEO and founder of Colossal Biosciences, now says he's 'positive' the first woolly mammoth calves will be born by late 2028.”

“There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must before seen.Yet this difference is tremendous; for it almost always happens that when the immediate consequence is favorable, the later consequences are disastrous, and vice versa. Whence it follows that the bad economist pursues a small present good that will be followed by a great evil to come, while the good economist pursues a great good to come, at the risk of a small present evil.”

“Criticized loans are those that show preliminary signs of higher risk”

The investment in home equity is absolutely sick. I just watched my wife's grandmother's home sell with most of the equity built up over the years go to medicaid to pay for her care in a nursing home that was run by a private equity outfit. It makes you want to throw up, but food is too expensive to waste. Seems there is a line to pick apart the remains of a lifetime.

That home debt product imo is just another version of those private notes which I think is a much bigger space than people realize. Thank you and great post.