Old School Tony Deden

“Never think you are wealthy because the price of your house has gone up.”

"If private equity had to pay top dollar for their capital, they couldn't afford to destroy companies for a living. This would not be a profitable business.”

Here's the latest PPI Index, and my proprietary U.S. Dollar Index:

"Assuming that these figures the government is using are not correct, then we're not talking about economic growth, but actually a contraction in real terms, inflation adjusted."

“The citizens of California have never been safer from wildfire risk”

- Patti Poppe, PG&E CEO, 2024

“Warren Buffett’s warning that wildfires have turned utilities across the western US into risky investments is mistaken — at least in California, according to the head of the state’s largest electricity provider.

“Frankly, I think Buffett got it wrong in California,” said Patti Poppe, chief executive officer of PG&E Corp., during the company’s investor call Thursday. “California has done the hard work to mitigate both physical and financial risk.”

…“The citizens of California have never been safer from wildfire risk, and I think investors will soon come to believe that,” Poppe said.”

June 2024 Santa Cruz County Grand Jury report on rebuilding after the 2020 fire:

“Out of approximately 700 homes destroyed in the 2020 Santa Cruz Mountains Lightning Complex Fire, only 95 have been rebuilt and occupied 4 years later, with only 158 more in construction. Nearly two-thirds are not being rebuilt.”

“Western business people love the suspension of civil rights because they believe it will never negatively affect them personally.”

I have to put this out today, even though CPI is tomorrow (and will be over the Fed’s made-up “2%-target” for the 44th straight month,) because I still have a lot of things to go through, and this post is getting fat (and happy).

Lots of good stuff below (I’m biased.) Look at this like a magazine, not a tweet.

More on the Southern California fires, market valuations, private equity, real estate delinquencies, homelessness, value investing(!), guns etc., plus the main course, an annotated Tony Deden (Chairman of Edelweiss Holdings) interview with friend of the show Tim Price and Paul Rodriguez.

Tony is so old school that if he ever went on CNBC he’d probably completely dumbfound the Fast Money panel, and make Scott Wapner cry (these are good things.)

Big fan of Mr. Deden. Enjoy.

“The issue isn't insurance companies going bankrupt in California since, as you mentioned, there are virtually no homeowners insurance plans with wildfire coverage that are underwritten by anything other than the California FAIR Plan anymore. The California FAIR Plan is both the underwriter for virtually all of California's wildfire insurance as well as the guarantee association that is owned/run by the state.

The issue is that the price controls combined with the state pillaging the FAIR Plan's funds for "other stuff" means that it only has $400 million to cover the losses. This is combined with the fact that California has a potentially >$60 billion budget deficit for 2025 that they don't know how they'll fund (the actual deficit isn't actually known because the state is deliberately excluding certain items from its calculation of it, such as $20 billion that it needs to pay to the Federal Government this year. The deficit is not less than $38 billion with a middle estimate of ~$60 billion. The high estimate is "who knows?").

The California Department of Insurance's official plan on how to now "fund" the FAIR Plan's multibillion dollar exposure is to prevent insurance companies from non-renewing existing plans as of January 9 and to threaten unspecified penalties for insurance companies that don't retroactively renew policies that were non-renewed in the past few months. That wouldn't necessarily do much even if it was able to be implemented, never mind that its unconstitutional and has a 0% chance of going through.

Because there's very few policies written by insurance companies, their exposure is so low that there isn't really a concern about any of them becoming insolvent. The real issue is that the FAIR Plan is very clearly insolvent, there is no viable mechanism to fund it, and the FAIR Plan itself is supposed to be the entity covering claims against insolvent insurers.

This isn't a situation that has ever happened in the modern US and no one knows how it's going to play out.”

Another comment from the NakedCapitalism article:

“I have now had 5 patients and friends as of today with their home in Ca a total loss. These are millions of dollars. 2 are uninsured completely.

My real estate agent patient had some news today. Every single available home in our area was sold this week. She now has over 200 squillionaires fighting over any and every home that is coming up on the market. All refugees from California. They know it will be years if ever that they have a home there again and they went out – to any desirable place in the country. The 18 million dollar high end homes are not involved so far. She told me that twice this week they have bid the home up over a million from asking – sight unseen.”

And this:

“The wealthy Palisades is a family neighborhood. “There’s nothing to go back to: no schools, no grocery stores.” The implication is that families will be strongly inclined to move to functioning communities and may stay there due to not wanting to uproot their kids yet again.

By contrast, in Altadena, which is more middle class, many of the residents are multi-generational. They could not have afforded to buy the homes they lived in and cannot afford to rebuild. Nearly all will be underinsured, particularly in light of the way building costs will be sure to rise as a result of competition for materials and contractors.

Another potential stumbling point is pressure to rezone. For instance, there will be pressure to allow more multi-family housing, the arguments including climate change benefits (lower materials use, cheaper cooling and heating) and arguably faster restoration of housing for if nothing else, the benefit of businesses.”

“The fires also wiped out the homes of Californians in the middle class who bought into affluent neighborhoods decades ago, when the properties were still within reach for teachers, plumbers, and nurses. After years of rising home values, many of them have the bulk of their wealth tied up in homes that are now ash.

“It was our retirement. It was our investment. It was our equity. It was everything,” said John Kastanas, a 63-year old who works in an administrative role at the California Institute of Technology, of his historic home that burned in Altadena.

Now, those middle-class homeowners face a crushing housing crunch. Los Angeles was already experiencing an acute shortage of homes. Its real-estate prices are more than double the national level. In the wake of the fire, thousands of people desperate for temporary housing are flooding a cutthroat rental market, where bidding wars are breaking out for leases. Some are considering leaving for good…

For those who lost their homes, much of the value of their properties is in the land they still own, but rebuilding on it will be a long and expensive process. It’s unclear how many homeowners in these areas lack insurance or are underinsured. A number of leading insurers have stopped selling new home-insurance policies in the state. State Farm said last year it would not renew 69% of its property policies in the Pacific Palisades…

“What scares me is rebuilding my home,” she said. “$800,000 [insurance] is a lot of money if you live in Iowa. But I am going to build my home in the Palisades again. How far is that money going to go?” The typical home value in the Palisades, filled with celebrity residents like Tom Hanks and Ben Affleck, was $3.4 million in November...

Many who lost their homes in the wildfires could end up discovering that their insurance policies won’t cover the full cost of rebuilding. They could pay the difference out of pocket, or they might decide to sell the empty lot, take the insurance payout and find a new home somewhere else.”

These fires will have ramifications we can't even imagine yet, and the really sick thing is that the politicians who basically allowed this to happen will be presiding over Newsom's "California 2.0". It's gonna be ugly.

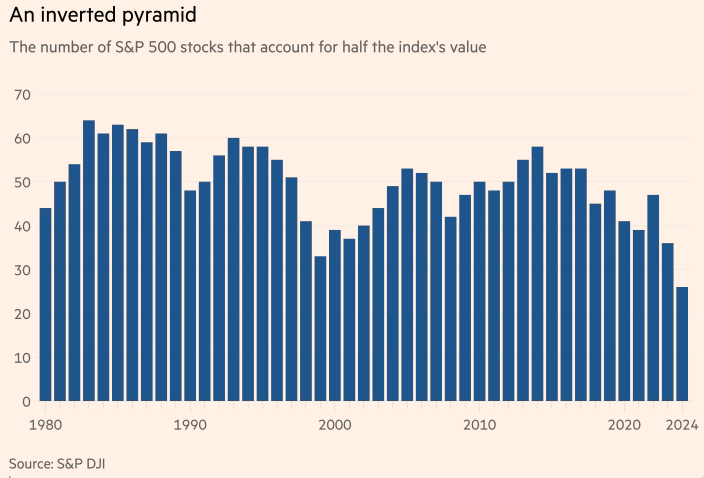

“Of particular note is how S&P 500 valuations are stretched across every conceivable metric.”

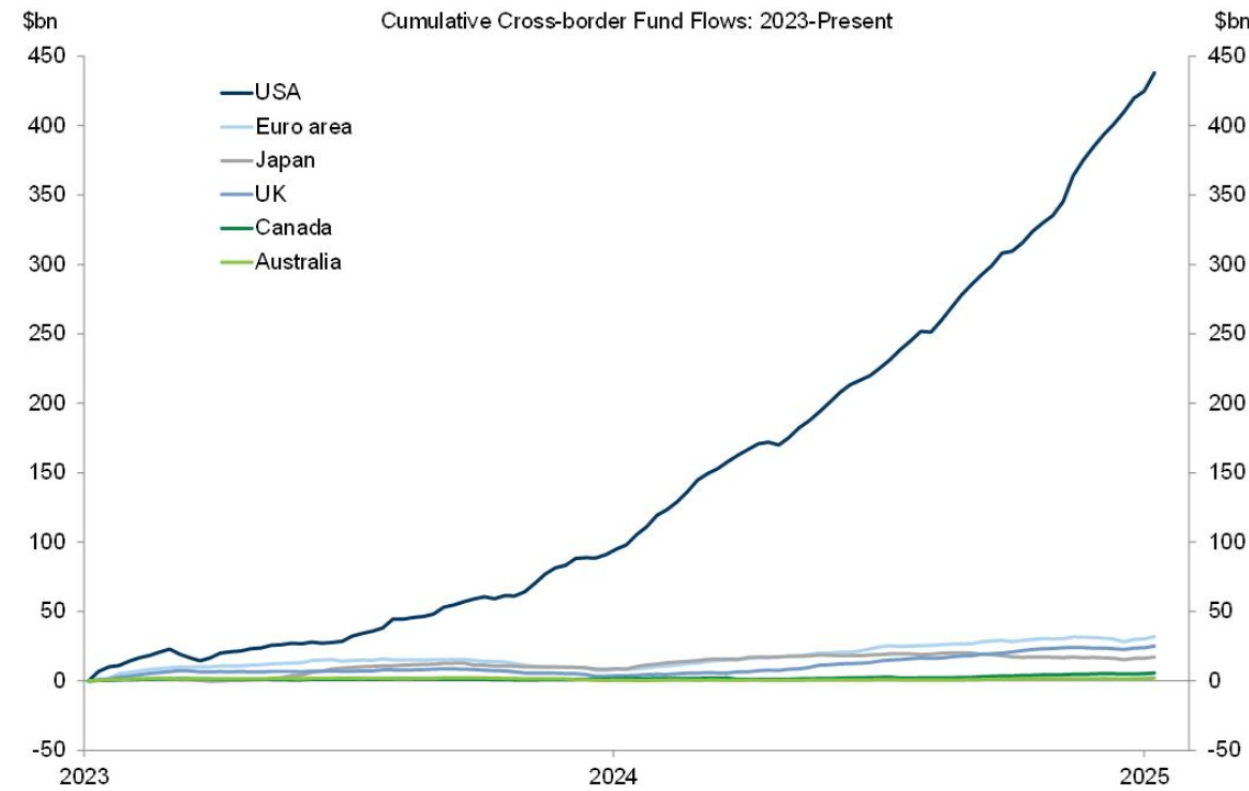

Dan Rasmussen: US tech stock mania is global. Here's a list of most-bought stocks in Japanese NISA portfolios:

“A Nippon individual savings account (NISA) is an account that is meant to help residents in Japan save money with tax-exempt benefits.”

A comment someone sent me made to Bill Fleckenstein:

“I think the ingrained impulse to "Buy The Dip" remains until the first "perceived" support area is broken.

There aren't many players who can grasp the concept of "bear market" so it will take time and several failed rallies to convince a new generation. Meanwhile, the passive bid plus buybacks remain as "props" making an "unwind" a drawn-out process (barring, of course, a sudden, news-generated crash).

Most media coverage of the bond market seems focused on blaming Trump tariff hype. However, the crack in the bond market started well before Trump was elected and was directly related to the Fed screwing around with that last rate cut in September. The extreme momentum behind the bond selloff seems more than a minor reaction to some nebulous tariff hype.

I think the "smart money" is jumping ship BEFORE 2025 when the UST market gets jammed up with auctions for $5-6 trillion to roll over maturing debt plus another couple of trillion in "new" toilet paper (...er, bonds, or IOUs, or whatever you want to call the stuff) to "pay" the interest on existing debt and finance even more of the PONZI game.

When Rick Perry was seeking the Republican nomination for president in 2016, he mentioned that Social Security was a simple PONZI scheme (which it is) and he was immediately blasted from all sides and eliminated from the running. Of course, the entire financialization of the US economy is a giant PONZI scheme, requiring ever higher debt and leverage to keep everything afloat. (But that's just my opinion).

If that kind of thinking goes "main stream", we will see "...Life Imitating art..." where the "Art" is that excellent movie, "Margin Call".”

I remember the 2000-2003 bear market. It was brutal in that it just went on and on, much slower than 2008-2009.

…and from 2001-2003 - 13 Fed rate cuts, the first on January 3, 2001:

This has to be some sort of sign…

“Greenlight Capital’s David Einhorn has long been talking about how markets are “fundamentally broken”, but he reckons things will get much worse before they get better — if they ever do get better.”

”Overvalued can become more overvalued, and undervalued becomes more undervalued, and you’re not having capital efficiency in the way that the markets are designed to create. And this creates what I call a very, very stable disequilibrium . . . And I don’t know if or when this will ever reverse. If it ever does, there’s going to be a ton of carnage that will come from that.”

“I view what’s going on right now as part of market structure being fundamentally broken. It’s passive flows, and other people who are investing money mostly care about price, not value. They don’t have an opinion about value. And so things become untethered from their actual value, and that creates a fundamentally risky situation…Many of these companies are trading for far more than they can conceivably be worth. And it does seem that over some probably long period of time — or maybe much sooner than everybody expects — things eventually tend to revert towards value.”

A market anecdote and chart via Alyosha:

“I am reminded of the tale about a guy who buys every share of stock in a company he likes (in this case, America), driving the price ever higher. Then, at the very top, he tells his broker to sell it. “I want to take a profit and sell,” he says. And the broker says, “Who to?””

BlackRock private equity fund takes more than $600mn hit on investment

“A leading BlackRock private equity fund has lost more than $600mn on an investment in an insurance outsourcing company after the business struggled with its debt load.”

More commentary here.

Chris Wood

“I would say in the last few years private equity has become almost a parody of its former self, and a lot of a lot of companies have been bought. The alternative asset class has grown dramatically, it's completely unregulated, and basically what they're doing is putting debt on the companies they acquire, which can mean it's not much fun working for a company owned by P.E., but the key point is it's all boomed, private equity, because of zero rates. It's all down to Ben Bernanke, and I would say a lot of the political issues today - all the obvious inequalities, the whole Main Street going bust, Wall Street being bailed out in 2008 - all this stuff is the reason why the Donald Trump phenomenon exists…”

“The real stress actually is on the companies acquired by P.E., because they have the debt put on them. They're on floating rate debt, and most times they didn't hedge the interest rate risk. That's where the stressors are, but the stressors are being covered up because there's another asset class that's booming. I think people got a bit nervous allocating more to P.E., but the real booming asset class in the US in the last two or three years has been private credit, and private credit - estimates say it's funding 60% to 70% of P.E., so if there's an area in the US where we're suddenly going to get a problem coming out of left field ,this will be the area.”

CMBS Loan Loss Report: Volume of Loan Losses Increases in December 2024

And yet…

“Tishman Speyer and Henry Crown have raised $2.65 billion in the commercial mortgage-backed securities market for The Spiral office tower in New York, kicking off the single asset, single borrower sector that analysts expect to post a banner year.

The bond priced on Tuesday, with the top tranche paying out a coupon of 5.47%, according to a person with knowledge of the matter, who asked not to be identified discussing private information. An additional $200 million in debt will also be securitized in future deals, the person added, bringing the total amount raised to $2.85 billion.”

A “single asset, single borrower” loan, at about 1.25% over the U.S. 10-year yield. I’d take Dogecoin instead1.

Bank of Hysteria

“Bank of America, which is scheduled to release fourth quarter figures on Thursday morning, could see unrealized losses on its $568 billion held to maturity portfolio (as distinct from held for sale securities which are marked to market, with unrealized losses deducted from reported capital) top $111 billion. That compares to $86 billion three months earlier and compares to the bank’s $200 billion in tangible equity as of Sept. 30.

The Charlotte-based behemoth undertook an ill-timed shopping spree during the zenith of the bygone bull market, building its HTM holdings to $675 billion from $216 billion over the two years through 2021. With those assets yielding a paltry 2% on average and the roll-off from maturing securities registering at a 6% to 7% annual pace in recent quarters, “the low yield on its portfolio could be a drag on its profits for some time,” Bary notes.”

Real Estate

“Unemployment as the stated reason for delinquency is approaching double the pre-covid norms. This stands in contrast to the recent jobs numbers and steady growth in social security directed payroll tax receipts (subject of an upcoming post). An interesting discrepancy.” - John Comiskey

Melody Wright: “Using Black Knight data for Nov, GNMA loans are 22% of the market and are 8.51% delinquent...this excludes the buyouts (link below explaining) Private loans are 3% of the market and are 12.17% delinquent. That's 25% of the market at elevated delinquency levels”

“As a general rule the rent-to-own business model boils down to new and creative ways to screw people.”

“Rent-to-own startup Divvy Homes is being acquired in a fire sale by Charleston, South Carolina-based Maymont Homes, according to multiple people familiar with the matter. Maymont, a division of Brookfield Properties, manages a portfolio of single-family rental homes…

With U.S. housing supply at record lows, Divvy initially gained traction with families that had been priced out of homeownership, promising them a pathway to the American Dream and distancing its brand from the rent-to-own category’s predatory history. Divvy bought a home of the customer’s choosing and then rented it back to them while setting aside a portion of their monthly payments for a future downpayment. Customers had three years to buy the home outright at a predetermined price…

In the four years following its 2017 founding, the San Francisco-based startup raised more than $400 million in venture capital from investors including Andreessen Horowitz and Tiger Global Management, as well as $1 billion in debt. By 2022, Divvy was on track to book more than $100 million in annual revenue…

…as the company expanded to new cities, customer complaints accumulated. In October 2022, Fast Company reported that Divvy was failing to address residents’ requested repairs, charging higher rents than its landlord peers, and evicting renters in greater numbers than before. Even some customers who had successfully bought their homes from Divvy said they were dissatisfied with the process and its costs.

At the same time, the Federal Reserve was raising interest rates, dealing a blow to Divvy’s business model. [CEO] Hefets, at one time, had suggested that Divvy’s model would insulate it from such macroeconomic swings. But by late 2023, Divvy had conducted three rounds of layoffs, putting it in league with other struggling proptech startups.”

Another creature of the ZIRP era.

It seems this is Fairfax County, Virginia, outside our nation’s capitol, where the median household income is about double the national average:

Speaking of abandoned new home sites in Austin (in my prior post,) here’s a video Melody and Travis did back in April 2024.

Tony Deden

“I think it was Richard Ellis who said that the business of deploying your capital is sort of like the game of tennis, which is different than any other game, and that is it's not how many goals you score, it’s how many errors you don't make. It's about not making errors rather than winning goals.”

“[What were the things that contributed to failure?] Well, largely hubris”

“I think the human element, in my view, is the largest factor in corporate failure. And frankly, that human element is one that you will not find in financial accounts, ever.”

“I have met a lot of entrepreneurs in my life, I mean a lot. I have been to more factories than you can care to think about. And none of these people are concerned with financial markets. None.”

“So you ask a question. What worries you the most? An entrepreneur - he will never say it's the Federal Reserve Bank, or the European Central Bank, or is it monetary policy or it's economic fiscal policy. They'll never say that. What concerns them is their people, their economic relevance, their competition, their technical skillset, their ability to survive, the ability to be resilient, the ability to profit and redeploy their capital appropriately. This is what interests them. This is what interests entrepreneurs or business owners. And so it is only in the financial world that we tend to constantly compare ourselves in terms of money, without really focusing on the means or the objectives that we have in pursuing whatever it is that we pursue.”

“My own suspicion is that just about everybody involved in finance has no clue what money even is. [Do you agree with that?] Absolutely. Someone said money's like time - everyone knows what time it is, but ask them what is time? And that's a much more difficult question. No, I mean, this is really true. I mean, we measure something, we build something, and and we're using a tool that itself has no yardstick.”

“There was a lot of work involved in producing the products that we take for granted. So there's a misallocation of capital, because the money going to the stock market does not really produce more things. There's no new food being created, there's no more capacity being created. There's just more money and there's higher asset prices. There's no increase in wealth. There's an increase in money that finds itself in these forms.”

“Look at the rise, not just the rise of equities market - this notion of private equity and all kinds of other things have come as a result of this stakeholder capitalism idea that has destroyed our society and destroyed our money and our savings. Then there are other factors involved when you bring the interest rate down to 0%, and you destroy those who've saved their entire life in order to have something in their retirement. You create a culture of speculation.”

“The stock market is not a very good measure of the health of an economic system at all, particularly nowadays and particularly in the United States.”

“You cannot compare what is happening today with the traditional role of the capital markets that used to be there for capital formation, but today you have no savings. In fact, no one even talks about the word savings anymore. People borrow money, and they call it their capital to employee as they wish. And the only purpose is to make money, and to make money as soon as possible, as fast as possible, damn the consequences.”

“A fellow told me once, he says everybody who comes to our shop to talk to us, analysts and others, they always want to know why is it that we don't leverage our balance sheet to earn more per share, or why can’t we do this or can we do that? And the only issue is how can we do certain things to make the price go up, the price of the shares. Hardly anybody's interested in the real business of business.”

“I think that a lot of people who are involved in even in industry have been deluded over the last so many years by the destruction of money and savings that has taken place”

“We're no longer a culture of production, we're a culture of consumption, and thinking about today, we've eaten the seed for tomorrow completely. But you know, there've been difficult times in the past, many, many, and even worse, but we've never had it this universal, more or less, global. Well, I should exclude parts of Asia, I suppose, and parts of the world, but at least in the Western world we've never had such a disintegration in every respect as we face today. And I'm not sure what impact that has long term on many of the things we take for granted.”

“Would you guys have anticipated what is happening in the UK today, once an extraordinary country, or Germany or France or Canada or name it? None of us would have anticipated that…”

“I think that impoverishment is an ongoing affair. We might be seeing a lot of money and a lot of progress, but realistically, the vast bulk of people are being impoverished today. The middle class has been destroyed in the Western world.”

"It's virtually impossible for people these days to start a family, because they can't afford to do it."

“A lot of this has come as a result of the destruction of society, because of the destruction of money. It's no secret that our parents - with one income in the family - were able to support an entire family. It's not secret at all. In fact, most of them were able to save money. In fact, all of them did, because our parents came out of their their parents. Our parents came. My parents came out of the war. It's no secret that money has been destroyed, and at the same time, as a result of that, we have a heightened time preference. No one is willing to make an investment today that will bear fruit in their children's lifetime. No one cares. At the same time, we own more material things than our parents did.”

“It's only a complete failure of something that is going to bring about a rejuvenation in ideas that matter. So the question is that when there's a fire someplace and everything is destroyed, what is it that remains that has value? And this is really what I'm interested in.”

“I think you need to have a culture, a culture that thinks about tomorrow and the next five, ten, fifteen, twenty years. It is only then that you're able to make the kind of decisions that are wise. If you think about next quarter, and if you think about next year to please your banks, your investment bankers or those who rent your common stock for whatever period it is that they rent it for, you are going to make the kind of errors that will put you out of business sooner, regardless how long you've been in business.”

On Valuation

“Back in 2001, I think, I was in a conference in Brussels, and a guy was sitting next to me at a table, one of these round tables. It was a young analyst from a bank in Brussels. And he says, have you heard of Lotus Bakeries? And I said no. He says the company just listed a few of their shares, raised some money to expand their factory.

So what do they do?

They make cookies.

So I looked it up real fast and I called them up and I said, my name is Tony Deden, and I'm in Brussels. You're not far away. Could I drop by and say hello? And they said welcome. And so I went to see them, and I was fascinated with his business.

They made cookies, but I love their culture. I love their business, I love their product. Everything about them was just extraordinary, except that the shares were selling at 58 times trailing earnings, and 20 times book value, and all those other metrics that you will just squirm if you saw them.

But it was, it was only €30 per share. So I said to myself, I love this business. These people are incredible. I love what they do, but it's too expensive. I'll look at it next year. I'll put it on a little list. And next year it was selling for 80 and it was still very expensive. I waited, and next year it was selling for 150, and for 310 years later. Still very expensive, and at some point it went to 2800 euro per share.

And I looked back and I said what is it that I missed? What did I not see? There must have been some sort of factor that I did not see in here. Why is a company that is, you know, the family owned 90% of the shares or 85%, something like that? I don't know, very little float, but very expensive. And all of a sudden I understood, I understood that invisible bit that it was difficult. It would have been a difficult thing to see. And don't ask me what it is because it would vary from a business to a business.

And then when the company decided that they're going to scrap the dividends so they can raise money to finance their expenses in the United States, and the shares went from $2800 to €2000. Oh, not dollars, euro. And I've made- I bought my first shares in my company at €2000 per share.

Now I could have bought it for 30. Now it's selling today for roughly €11,000 per share, the same company that some 22 years ago was selling for 30. Now, granted, it’s a bit rich to say the least, and I've let some of the shares go, but the point is that you are looking at invisible aspects of what something may be worth that you cannot always put in a nice neat formula.

And where I think I have failed often times, both on the decision to do something or not to do something, is on relying too much on financial metrics. And I think those are very useful, there's no question about it. But they do not lend themselves as much as one would think, to the idea of what something is worth to me. And remember, the idea of financial accounts when it was first accounting was first established, was never meant to be a tool for valuation. It was meant to be a tool for accountability to the owners of companies.”

“I bought my first gold in 2002. And, you know, I've owned a lot of it over the years, but I never saw it as an investment. And I've explained very diligently exactly why it is that we own it, but it ends up having been the very best investment I've ever made over the last 20 years.” [Gold is up about 9x since 2002, vs approx. 8.5 for the S&P 500 total return]

“There's a fellow I've known for years. He's a very responsible fund manager, and I would say 40% of his assets are in medium-term bonds. Now if you tell him that perhaps he may want to rethink this, he's very convinced this is a very good way to preserve his capital. I don't think so.”

"I have no particular dreams as to legacy. I think that if you live your life well and you have the respect of your friends and the love of those around you, and you've done the right thing in the way God gave you the light to see what was right, you've lived a good life."

“It's not that the world back in the 1980s was any better than it is today, but today you don't trust anything. I mean, I don't trust The Wall Street Journal, I don't trust the Financial Times. I don't trust the government statistics. I don't trust anything that comes out of any official. I don't trust most corporations. And so when you have when you have a complete loss of trust - I don't trust audited accounts. Every every fraud out there had an audited account…The thing is, when there's this loss of trust, you're on your own, and you can never have progress in a society without trust. Trust is a glue that holds societies together. And so this is what we have.”

“Price: Do you have your own official inflation figures and things like that?”

“Of course, not a waste of time.”At the end of the interview, Tony Deden recommends The Gulag Archipelago, by Aleksandr Solzhenitsyn.

Tony Deden of Edelweiss Holdings 2018 chat with Grant Williams is probably the best financial philosophy discussion I've heard.

“The world is full of complainers, and the fact is, nothin' comes with a guarantee. Now I don't care if you're the Pope of Rome, President of the United States, or Man of the Year; somethin' can always go wrong. Now go on ahead, complain, tell your problems to your neighbor, ask for help, and watch him fly. Now, in Russia, they got it mapped out so that everyone pulls for everyone else…that's the theory, anyway. But what I know about is Texas, and down here…you're on your own.”

Opening monologue in Blood Simple

“The day after the session with the Stones, Clayton suffered a miscarriage. She attributes it to the strain she put on her body pushing the heavy studio doors and reaching to hit the vocal peaks. “We lost a little girl. It took me years and years and years to get over that. You had all this success with Gimme Shelter and you had the heartbreak with this song.” Although she recorded her own version of the song for her 1970 studio album (itself entitled Gimme Shelter), it took her a long time to listen to the Stones’ song because she so closely associated it with losing her child. “It left a dark taste in my mouth. It was a rough, rough time.”"“

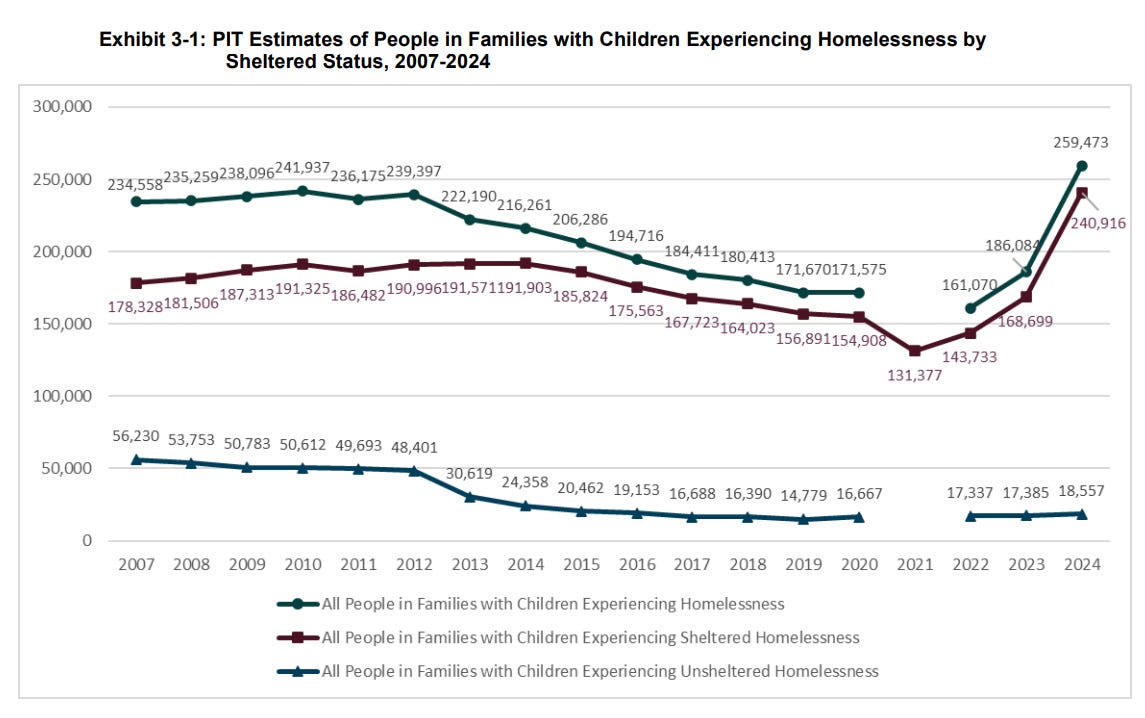

The 2024 Annual Homelessness Assessment Report (AHAR) to Congress

“On a single night in January 2024, 259,473 people in families with children were experiencing homelessness in the United States, the largest number since data collection began. Nine in ten people experiencing homelessness as families were sheltered.”

“The fact that we didn't see a similar spike in 2008 shows you that this crisis is real”

Guns on the Roof

I’m surprised the numbers aren’t higher. I’m sure they are in my neighborhood (and the gun laws here are absurd.)

“The upheavals caused by inflations are so profound that people prefer to hush them up and conceal them.”

Elias Canetti, Crowds and Power

I own zero Dogecoin. Sometimes I wish I didn’t.

Excellent post and thank you. Will be listening to that Grant Williams/Tony podcast today.

I live in a high gun ownership state. In a meeting with partners and staff a few years ago, someone mentioned something about concealed carry, and how many people actually carry. Someone asked me what I thought, and I replied “if you’ve seen me in anything other than my jammies, I’ve had a gun.” Side glances ensued. “You asked.”