Sauve qui peut

A warning, not encouragement.

Welcome to my Substack:

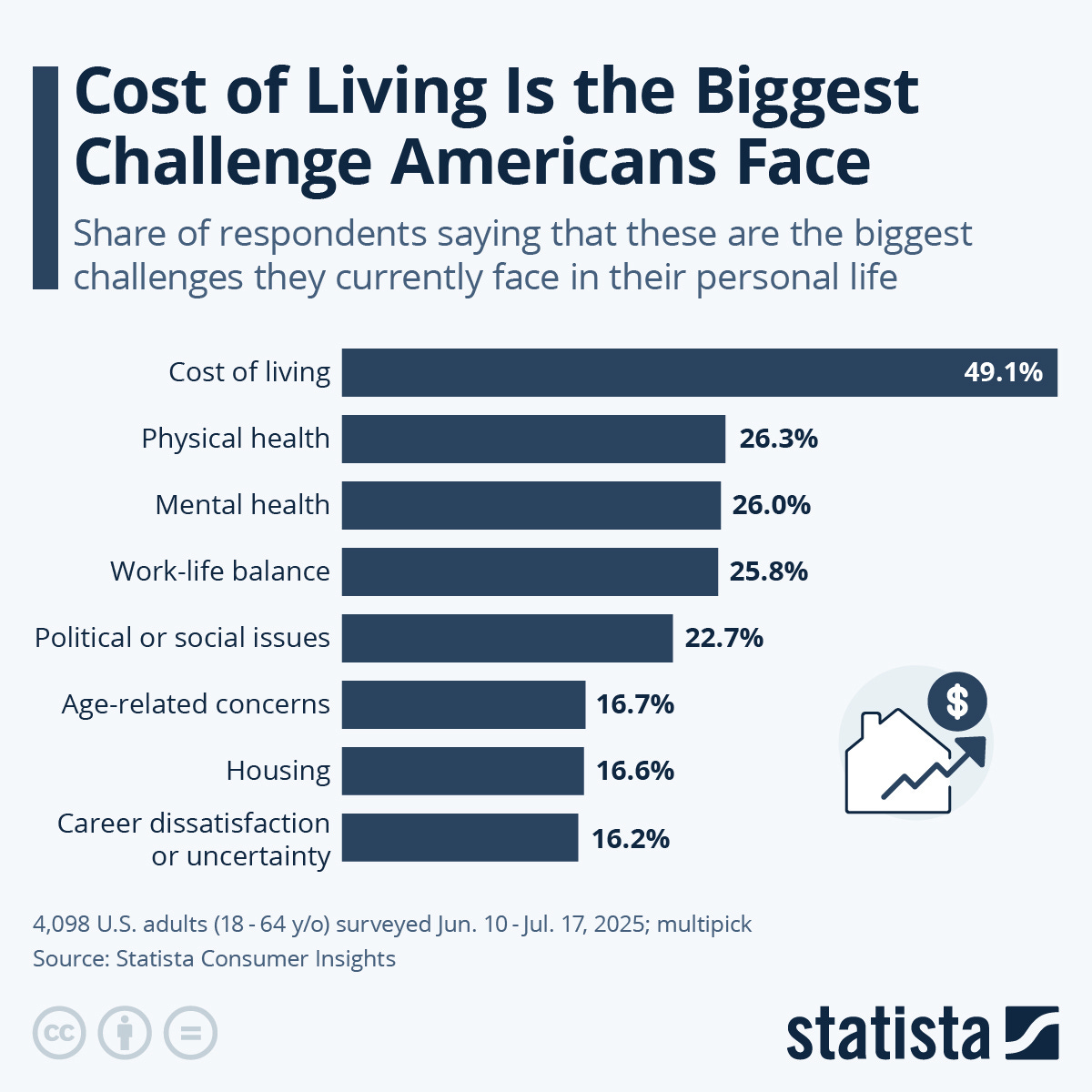

Cost of Living Is the Biggest Challenge Americans Face Note that every other category listed above is also affected by the cost of living, especially housing.

Meanwhile, the Fed actively sought to spike CPI, and now is seemingly satisfied that it has been well above their made-up 2% target for four and a half years.

Core PCE has now been above the Fed’s made-up “2% target” since April 2021, and above their actual mandate of “stable prices” since forever.

As Marc Faber said to Julia La Roche:

“Ordinary people are struggling, but ordinary people are never interviewed on CNBC, or on your program, or on Fox News. They have no voice, so the elite can tell the public, ‘Oh, the economy is doing well.’”

Or, as Louis-Vincent Gave said:

“I grew up in France, so I had a good dose of Marx in my education. The first thing Marx teaches you is that revolutions are typically the result of inflation.”

My nom de guerre was always meant as a warning, not encouragement.

“I’d never trust anyone on the right or the left who is inconsistent on free speech. A person willing to abandon this fundamental American principle for short-term politics—justifying their own hypocrisy by citing the other side’s hypocrisy—can’t be counted on to uphold anything.”

This is nuts:

Train Wreck

Excellent. By Marvin Barth…

“I think some perspective on the Jerome Powell Fed is in order. I have been shocked by the number of people in markets, academia and the press that rate Chairman Powell favorably. That was true even before President Trump made a martyr of him. Yet, Jerome Powell is far more likely to be remembered as one of the worst chairpersons in the Fed’s history.”

Währung

“Other languages have no equivalent for the word ‘Wahrung’. They call it ‘monnaie’ or ‘currency’ and thus ‘coin’ or ‘circulation medium’. The German word expresses most succinctly the real significance of the means of payment: it must ‘last’ (wahren - to last) and it must have stability, i.e., it must maintain its value.”

- Hjalmar Schacht, The Magic of Money

Via Grant’s:

The stock market’s rapid post Liberation Day ascent leaves the S&P 500 priced at more than 40 times its cyclically adjusted price-to-earnings ratio, eclipsing the 38.6 times logged in fall 2021 to mark the richest reading in history after the dot-com bubble, which saw a 44.2 CAPE in fall 1999…

Today’s freewheeling backdrop likewise helps flip the leveraged finance issuance machine into high gear, with the month-to-date supply of new junk bonds topping $35 billion as of this morning by Bloomberg’s count, on pace to log the most active single month since September 2021…

Option-adjusted spreads on the ICE BofA U.S. Corporate Index crouch at just 74 basis points, their lowest since 1998

“Data sifted by Truflation show a 1.98% rise in the price level since April 2 “Liberation Day,” equivalent to a 4.22% annualized rate.”

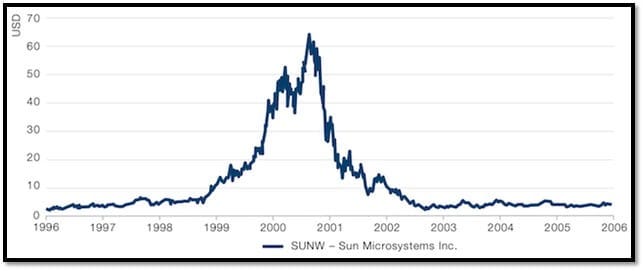

Wow: Price to Sales.

Here’s Sun Microsystems co-founder Scott McNealy in March 2002:

Two years ago we were selling at 10 times revenues when we were at $64. At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don't need any transparency. You don't need any footnotes. What were you thinking?

Dotcom on Steroids

Key Takeaways

Today’s market, particularly in the tech sector, exhibits dotcom-era overvaluation, with lofty multiples, slower earnings growth, and a weaker macroeconomic backdrop, in our view

We believe today’s technology sector no longer represents forward-looking quality due to decelerating revenue growth, collapsing free cash flow, and increasing competition

We see better investment opportunities outside the tech sector, offering similar potential returns at lower risk and aligning with the goals of compounding capital with strategic downside risk management

The Fed is Too Restrictive!

Markets hit record highs as ‘FOMO’ infects investors Lots of comments

The spokesmodels on the infomercial were talking about Greenspan’s famous 1996 “Irrational Exuberance” remark this week, so I sent them this:

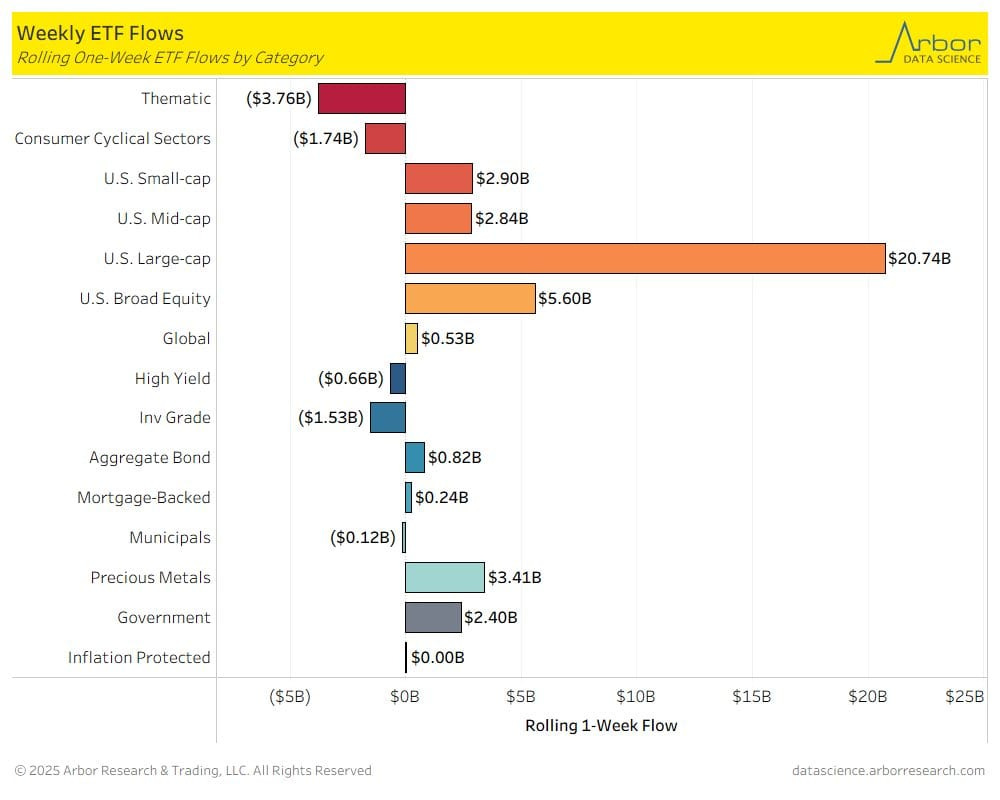

Weekly ETF Fund Flows

‘Pension funds should have 20 per cent of equities invested in UK, says think-tank’

“…an allocation that could drive more than £75bn into British stocks by the end of the decade.”

Another form of price-insensitive investing?

“British pension funds have rapidly moved away from UK equities in recent years, with DC fund allocation to UK stocks falling from more than 40 per cent of total equities in 2013 to 9 per cent by 2023…

Proposed so-called “mandation” of pension funds into UK assets has faced fierce resistance in recent months due to the fiduciary duty of pension funds managers and trustees to invest in the best interest of their members.”

Gustavo Franco

“A former Governor of the Brazilian Central Bank, he is best known for being one of the “fathers” of the Real Plan, the 1994 monetary reform that ended hyperinflation in Brazil.”

Paul Buitink: “Would you say then that the burden of hyperinflation falls primarily on the shoulders of the poor and the vulnerable in society.”

Gustavo Franco: “Absolutely.”

Interesting that, in the end, his solution sounds a lot like “we got lucky.”

“We’ve been adopting his1 definition of hyperinflation, first as an episode that starts when inflation hits 50% per month. It’s a huge number - it should be something over 10,000% per year, 50% per month, okay? But in practice what happens with 10% per month is not that different from what happens with 50%, and that has been noted by a number of other researchers questioning this definition of hyperinflation”

“In Brazil there’s this curious denial about hyperinflation, and I remember politicians telling me do not use that word - you’re going to scare people unnecessarily.”

“You lose faith in currency with 10% per month [inflation], 5% per month, or 50% per month. It’s not clear. Somewhere in that a moment happens2, the moment in which there’s a - I don’t know, a click - something happens, and politicians say that’s too much, society says it’s too much, and then something is done.”

Brazil “was like 15 years with average monthly inflation at something like 15%, 20% per month”

“It’s perhaps one of the definitions and one of the moments in which you know you are under a high inflation is when you don’t look into yearly rates anymore, it’s month by month”

“It’s vicious. The atmosphere gets poisoned. Only living through that could I understand what people told of the memory of Weimar, and how poisoned it had become, and how that could then produce social outcomes” like Hitler.

“Those protected navigate that process with less damage than the unprotected, so society become becomes more unequal, more tense, more politically contentious, uh, poisoned.”

“It’s very divisive and it’s interesting that it’s not so visible in its political implications, so much so that denying the whole thing is so dominant for so many years, at least that was the experience of of my country. It took years for the political establishment to accept that the problem was inflation and inflation wasn’t the solution”

“The first more notable effort to fight inflation deployed basically a price freeze, which is a pretty intuitive way of fighting inflation, at least in the minds of politicians. The simplicity of the concept - you pass legislation saying changing prices is illegal, it’s simple enough, right? So it doesn’t work, but we tried it five times, starting in 1986, the last one was 1991. Five times, only to learn that you can’t end inflation with a price freeze.”

“One feature of our experience was little use of dollars, dollar accounts and gold. Very little, and that is a bit of a contrast with our neighbors in Latin America”

“Winning over hyperinflation in Brazil was a matter of producing a positive fiscal result, properly measured, primary Surplus mostly, number one, and number two to un-capture the central bank to redefine money governance essentially”

“There’s no miracle [ending hyperinflation], but there’s the right timing for this to to be applied, and it was the right time. I think we’re lucky, or destiny was written”

“Brazil produces gold, and there’s a mechanism of acquisition of locally produced gold by the Central Bank still there. To my knowledge, it was never important for us as a reserve asset really…I know nothing about gold”

William White

“It’s going to be like the European crisis, but at the core now, with France being the object of of concern, as opposed to much smaller peripheral countries, which makes it inherently just that much more dangerous”

“Any single pension fund probably should be shorting bonds, and shorting French bonds in particular, but if everybody does it, then you’re actually precipitating the crisis that you’re trying to avoid, and the end result will be much worse than if you didn’t do it in the first place”

“What’s the French phrase, sauve qui peut? You know, if you can save yourself, you should.”

“Every time the answer to the problem is exactly the same, which is print the

money, but in printing the money, all you’re doing basically is encouraging people to take out more debt, which then becomes the the basis for the next crisis.”

“You can do something that’s right for today, but make things far worse tomorrow. Okay, that’s a problem, and that’s what I think the central banks have done.”

“You just have this sense out there that there’s been this big increase in in borrowing, but we don’t really know who’s been doing the lending, and we don’t really know who’s been doing the borrowing, so it’s very hard to get a sense of where the weak spots are and what you might do about it.”

“There are no good alternatives. There are only bad alternatives. The question is, which one is the least bad?”

“I can’t imagine - maybe it’s just a failure of my imagination - a new Bretton Woods, where the Chinese and the Russians and the Americans and the Europeans sitting around the table drumming up a new Breton Woods agreement, not least because - and I have no answer for this - every major country has got a big debt overhang problem, and every major country in that sense wants more inflation, which implies in a certain sense more depreciation. So the cure is all the major currencies should depreciate, and then you sort of say, wait a minute, that’s not possible. So we’re into a funny old world here in terms of what choices people make as they try to deal with this debt problem, and how you decide to sort your currency out is going to be a big factor.”

Meh.

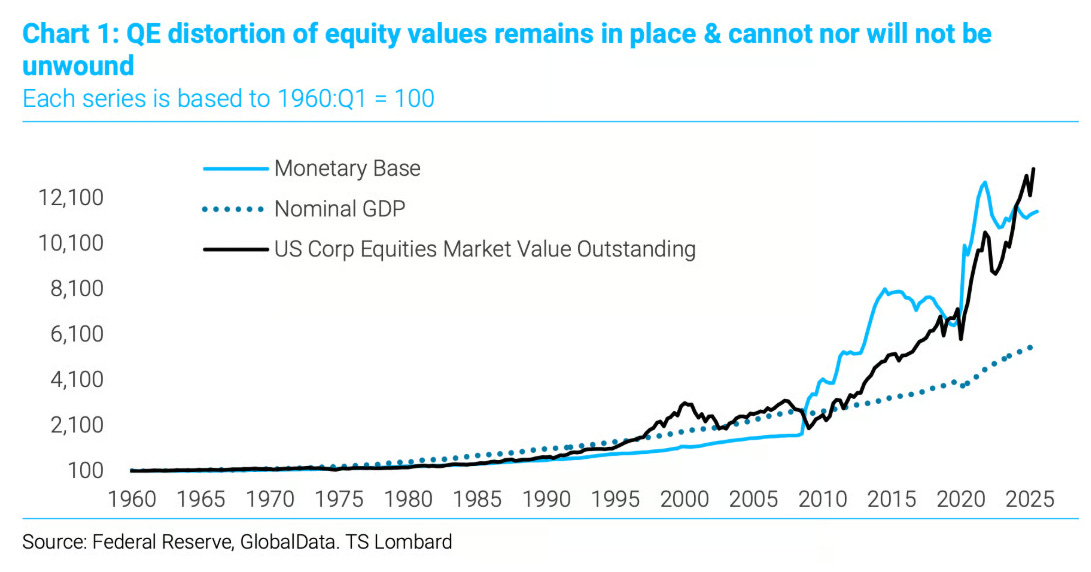

"QE is the Fed directly growing the monetary base, complicit with a rising Federal deficit, and then holding the base (reserves) at the Fed by paying interest. This inflates financial assets but not real growth."

”That sense of froth…”

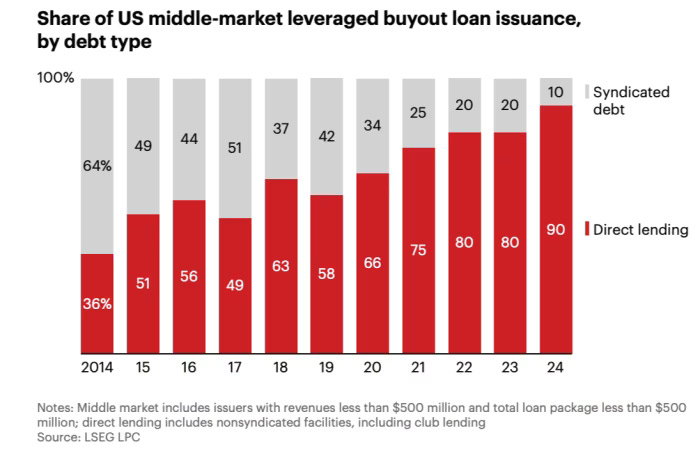

How bad could private credit default rates get?

Alphaville isn’t sure quite what proportion of private credit direct lending ends up financing private equity portfolio companies. So we had a go sampling the Blackstone Private Credit Fund’s massive $71bn portfolio of borrowers, sorting alphabetically the 713 entities to which they lend money and then looking up how they are classified by PitchBook.

After the first 100 we got bored, but noted that 90 per cent of the non-CLO borrowers were classified as “Private Equity-Backed”. So to be clear, we’re not saying that 90 per cent of private debt is definitively financing private equity portfolio companies. But it seems reasonable to think that a decent chunk of it does.

Moreover, as Bain & Company’s annual private equity study shows, even if not all private credit flows into financing middle-market private equity leveraged buyouts, almost all middle-market private equity leveraged buyouts are now financed by private credit:

Adam Street Partners — a private market asset manager with just over $62bn of AuM — has invested its clients in a wide range of other managers’ PE funds for decades. And over these decades it has kept track not only of what happened to overall PE fund returns, but also all the individual portfolio companies that have been bought and sold by these PE funds.

The record they’ve built up is far from a complete picture of the industry. But it does — according to Jeff Diehl, the firm’s managing partner and head of investments — capture the fate of more than 5,784 realised, and a further 4,156 active, individual PE buyout portfolio companies. So, what proportion of these buyout companies bombed?

In the 20 years to 2013, the share of portfolio companies that either went bust or were sold at close to zero was just over 15 per cent…that one in six PE fund buyout companies have turned out to be complete turnips in yesteryear sounds bad if an increasing share of this crop’s debt is in the hands of private credit funds.

But hold on. In the 10 years since then, the doughnut rate has been a lowly 3.5 per cent. Have the increasingly big bucks paid to PE managers maybe led them to step up their game and dodge the dodgiest companies? Have better underwriting standards meant buyout companies are no longer likely to collapse under the weight of debt with which they are saddled?

No, says Diehl. What is really going on in this chart is a lack of PE exits…Diehl expects that between a tenth and a quarter of portfolio companies acquired by PE buyout funds between 2016 and 2022 will ultimately be write-offs.

Top H-1B Users

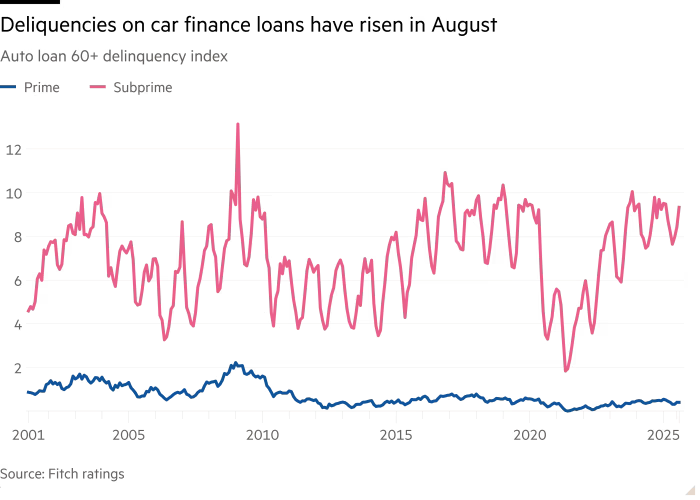

‘Americans Owe a Staggering $1.66 Trillion in Auto Debt, Report Finds’

According to the report, the average car payment in the States is now around $745, with average loan amounts totaling over $41,000; nearly 20 percent of buyers have found themselves with payments of more than $1000 a month. Loan terms are also creeping back to rates similar to those before the Great Recession, with one in five buyers stretched out on a seven-year term. We’ve even seen the return of the eight-year loan, which all but disappeared following the sub-prime lending crisis.

Speaking of the Great Recession, auto buyers are also defaulting in their payments in ways we haven’t seen since 2008. Delinquencies on payments are almost on par with pre-crisis figures, and have dramatically outpaced the rates experienced during COVID. An analysis of the New York Fed’s consumer credit panel found that buyers in 2024 with an above-average credit score (620-679) were twice as likely to fall behind on payments than they were prior to the pandemic. That's particularly true of buyers aged 18-29, who, according to the report, are falling into serious delinquency (90 days late or longer) more than older generations. Repossessions were also up 43 percent from 2022 to 2024, representing the highest rates since 2009.

Things aren’t much better on the used car side of things. Prices were up 6.3 percent year-over-year as of June3, continuing the trend started during the supply constraints of the pandemic. Furthermore, one-in-four trade-in vehicles have negative equity attached, meaning that people are upside down on a large portion of the cars on sale today.

Tricolor: The Gift That Keeps On Giving

Tricolor Interest Payouts Clawed Back From Bondholder Accounts

“Some Tricolor Holdings asset-backed bond holders who received interest payments last week have seen those funds clawed back in recent days…The rare claw back highlights the ongoing confusion and operational challenges weeks after Tricolor’s sudden collapse. Amid allegations of fraud, banks are exploring whether the same collateral was pledged to multiple lenders while Kroll Bond Rating Agency Monday cut the credit grades on Tricolor’s securities as many as 19 levels, to CCC and lower.”

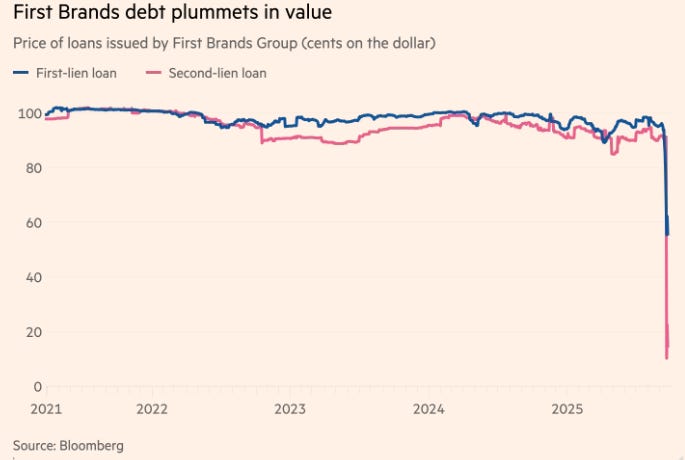

Now “auto parts supplier First Brands Group” has also collapsed.

“The speed with which First Brands’ finances have deteriorated has shocked debt investors, who were already unnerved by the sudden collapse into bankruptcy of US subprime car lender Tricolor Holdings.”

“Entities tied to First Brands Group and its founder Patrick James have filed for bankruptcy protection in the US, compounding issues at the car parts supplier whose troubles have roiled credit markets.

Carnaby Capital Holdings and several entities that raised debt linked to First Brands Group filed for Chapter 11 proceedings on Wednesday, raising the likelihood that the business is itself on the brink of bankruptcy.

First Brands Group is estimated to have raised as much as $10bn in debt and off-balance sheet financing.”

US debt investors raise alarm over lending standards

Concerns come after unravelling of two companies deemed just weeks ago to be in strong health

The failure of subprime auto lender Tricolor Holdings at the start of this month followed by the exploration of bankruptcy proceedings by car parts supplier First Brands Group have wrongfooted investors.

Tricolor had won pristine triple-A ratings as it borrowed in credit markets, while First Brands may have amassed as much as $10bn in debt and off-balance sheet financing and was close to raising even more last month.

Investors were ready to dismiss each as one-off incidents, but taken together, the two offer signs of cracks within credit markets, which have become a critical source of funding for consumers and businesses as traditional banks have retreated since the financial crisis.

“A second investor who has since sold their position in packaged-up Tricolor loans said they had no idea how potential financial irregularities went unnoticed by JPMorgan Chase, one of the banks that underwrote debt offerings.

“That’s the shocking part of it,” the investor said. “JPMorgan is one of the most sophisticated lenders in the entire world. How the hell could they have missed this?”

JPMorgan declined to comment.”

Meanwhile…Auto lender’s bust raises alarms over financial health of US households

Angela Brown and her husband clean air-conditioning systems at hotels across Texas, relying on cars they bought from subprime auto dealer Tricolor to reach jobs at other ends of the state.

But last October, Tricolor repossessed Brown’s Ford Edge sport-utility vehicle, and in July, it took back her husband’s Ford F-150 pick-up truck. “We’re still trying to play catch-up to this day,” said Brown. “I think it’s just a hard time for everybody right now…

Tricolor’s failure was a “potential bellwether for where the economy is going”, said Brett House, an economics professor at Columbia Business School. “Low-income Americans tend to do absolutely everything possible to remain current on auto payments, even when they face substantial financial distress. Having a car is essential to having work in the US.”

…Brown, the Tricolor customer whose two cars were repossessed, said her life began to unravel after she bought the vehicles.

Both cars broke down in rapid succession, she said. They wound up in Tricolor’s repair shop for months on end, hindering her ability to work even as she still had to continue paying the pricey twice-monthly loan instalments.Brown still has one other car purchased from Tricolor, a now-discontinued Ford Taurus from 2015, which she wants to keep making payments on. But she has always paid over the phone. “And now that’s up in the air,” she said. “Every other day I’ve called. And there’s nobody there to answer.””

Carmax, “the biggest seller of used cars, said Thursday that its sales and profit plunged in the latest quarter…“The consumer has been distressed for a little while. I think there’s some angst,” CarMax Chief Executive Bill Nash told analysts on a call Thursday…Profits at the company’s finance arm were also down, as the performance of loans originated in 2022 and 2023 deteriorated and the company increased its provision for losses.”

And lastly:

Ford is racing to sell more F-150 pickups this quarter by offering lower interest rates to buyers with the weakest acceptable credit histories. The deal available until the end of the month will allow consumers with shakier credit profiles to pay the lower interest rate offered to those with stellar credit records.

Stan Druckenmiller, Lost Tree Club, 1-18-15

Well, I made a lot of mistakes, but I made one real doozy. This is kind of a funny story - at least it is 15 years later - because the pain has subsided a little. But in 1999, after Yahoo and America Online had already gone up like tenfold, I got the bright idea at Soros to short internet stocks. And I put $200 million in them in about February and by mid-march, the $200 million short I had lost $600 million on, gotten completely beat up, and was down like 15 percent on the year. And I was very proud of the fact that I never had a down year, and I thought, well, I’m finished.

So, the next thing that happens is - I can't remember whether I went to Silicon Valley or I talked to some 22-year-old with Asperger's - but whoever it was, they convinced me about this new tech boom that was going to take place. So I went and hired a couple of gun slingers, because we only knew about IBM and Hewlett-Packard. I needed Veritas and Verisign. So, we hired this guy, and we end up on the year — we had been down 15% and we ended up like 35 percent on the year. And the Nasdaq's gone up 400 percent. So, I'll never forget it.

January of 2000, I go into Soros's office and I say I'm selling all the tech stocks, selling everything. This is crazy at 104 times earnings. This is nuts. As I explained earlier, we're going to step aside, wait for the next fat pitch. I didn't fire the two gun slingers. They didn't have enough money to really hurt the fund, but they started making 3 percent a day, and I'm out. It is driving me nuts. I mean their little account is like up 50 percent on the year. I think Quantum was up seven. It's just sitting there.

So like around March I could feel it coming. I just- I had to play. I couldn't help myself. And three times during the same week I pick up a - don't do it. Don't do it. Anyway, I pick up the phone finally. I think I missed the top by an hour. I bought $6 billion worth of tech stocks. and in six weeks I had left Soros, and I had lost $3 billion in that one play.

You asked me what I learned. I didn't learn anything. I already knew that I wasn't supposed to do that. I was just an emotional basket case and couldn't help myself. So, maybe I learned not to do it again. but I already knew that.

“The thief or swindler who has gained great wealth by his delinquency has a better chance than the small thief of escaping the rigorous penalty of the law; and some good repute accrues to him from his increased wealth and from his spending the irregularly acquired possessions in a seemly manner.”

Thorstein Veblen

Condo prices in Killeen, TX, a little over an hour north of Austin, have collapsed by 40% since the peak in mid-2022 and have given up the entire 52% spike from mid-2020 to mid-2022, plus some. The spike had been driven by FOMO-madness and the Fed’s Free Money policies. This is one of the fastest-growing cities around; its population has surged by 35% in the past 15 years to 160,000 in 2024.

But Killeen and other cities like this with condo markets in free-fall don’t qualify for our list here because they’re too small.

"Housing is a big deal for the Trump administration. They're getting ready to probably announce a housing emergency in the U.S., because of affordability. This was caused by the Fed. The Fed drove home prices up." - Chris Whalen

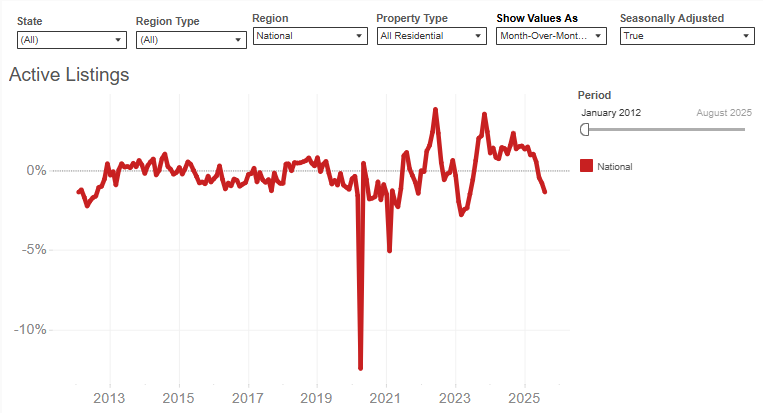

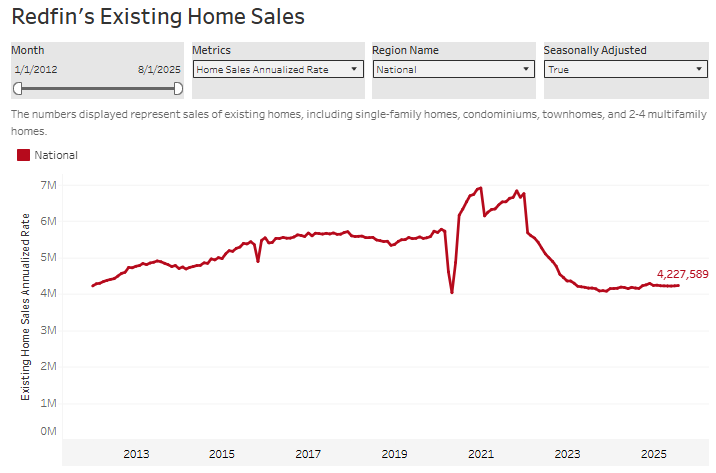

Housing Supply Drops Most in 2 Years as Sluggish Demand Spooks Sellers

Active listings fell 1.4% in August—the biggest decline since 2023—as homebuying anxiety spilled over to sellers.

Mortgage rates dropped to the lowest level in about a year, which has led to an increase in refinancing activity but hasn’t yet translated into a jump in sales.

Redfin expects existing-home sales to end 2025 roughly in line with 2024, which was the slowest year since 1995—but the outlook could improve if rates fall further.

Home prices rose 1.7% year over year in August, the biggest uptick in five months.

Ed Dowd

“Lower home prices are good for the the millennials and the Gen X that are younger. That is not necessarily a bad thing. Obviously I don't want people to lose their jobs, but this financial reset is basically a passing of the baton of generational wealth from boomers back down to the generation below that's actually doing the work. My fear is we get more of the same. If we have a correction, what do we expect? The Fed will do what it does, do unprecedented monetary policy. The Trump administration might do things that harm the younger generation long term by bailing out the boomers again. So, this is a generational kind of battle that's been going on, and the boomers have been bailed out since the great financial crisis.”

“Historically, when we get to these types of dividend yields on the total stock market, the 10-year forward projected returns - which we wrote about in February - are zero. What that means is if you buy in your 401k a basket of the S&P right now, including dividends, 10 years from now, you're projected to get back to even.”

“This is a class issue. That's it. When you think that way, and you say, “What what do I have in common with an oligarch worth a hundred billion dollars?" Absolutely nothing.”

“What happened during Covid with these vaccines is one of the greatest crimes against humanity…It is a mass poison…the implications of a COVID reckoning are so scary, and that's why it's the elephant in the room. They don't like to talk about it because corporate America would be liable. Fortune 500 companies mandated this, so it's not just pharmaceutical industry, it's a lot of people.”

“You have to resist any kind of calls like we saw with Pam Bondi talking about hate speech, which Charlie Kirk said was nonsense. Anything that curtails our speech, no.”

“I'm a freedom-loving individual, and I know what's coming. They're going to try. These people cannot admit that the system - they screwed it up - and in the collapse they're going to blame everybody but themselves, and try to control and take everything.”

Marty: “Ed, Alex Karp stood up in LA last week at the All-In Summit and promised us that Palantir is not surveilling or spying on individual American citizens. It will never do that.”

Ed: “I don't believe that for a second.”

Scott Bessent

From a recent now-deleted podcast…

Scott Bessent hasn’t been allowed to visit China, Beijing or Macau for the last decade due to critical comments made on Australian TV post-Xi’s promotion

He owns a lot of physical gold that he stores in vaults in Texas

He refuses to higher graduates from Harvard after having a failed 0/5 hit rate on prior hires

He was targeting $40-50/barrel for oil to…

Target of 3% GDP growth and flat fiscal budget to grow out of fiscal debt load months before he was officially nominated which was when this interview was conducted

He is incredibly hawkish on China and thinks they haven quietly been at war with us and we just haven’t realized it

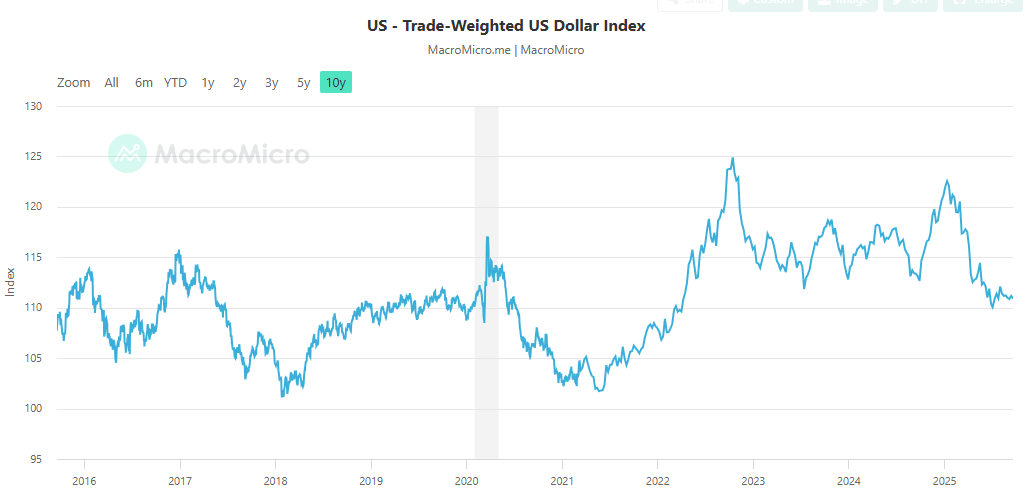

Gold / Oil Ratio

“I think it is unbelievably dangerous for government to put itself in the position of saying we’re going to decide what speech we like and what we don’t, and we’re going to threaten to take you off air if we don’t like what you’re saying."

EYE ON THE MARKET • MICHAEL CEMBALEST

”AI related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November 2022.”

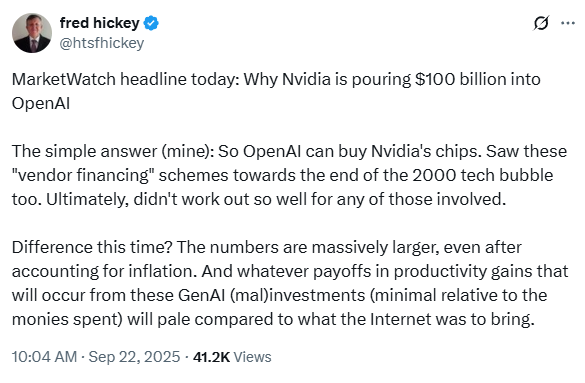

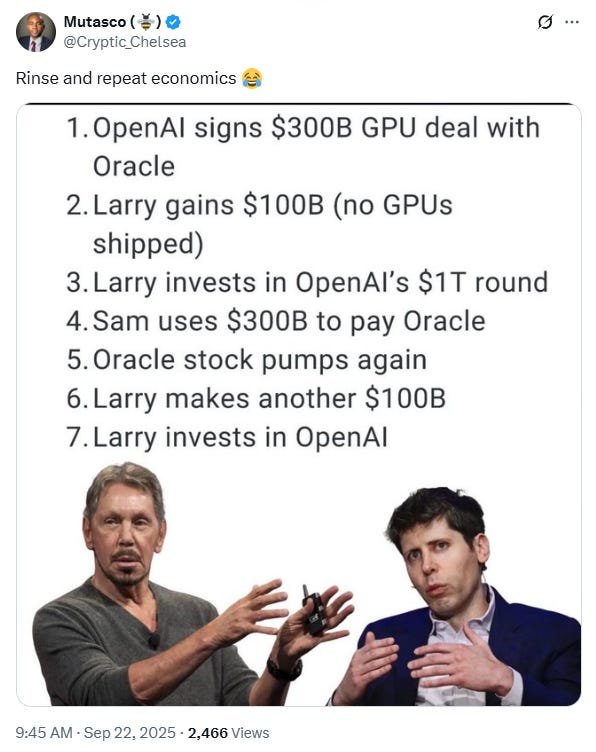

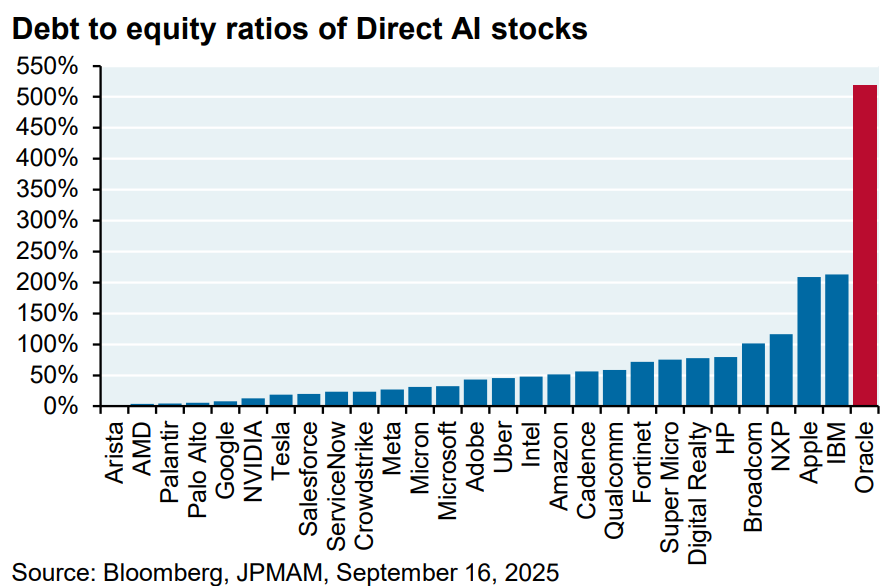

On OpenAI/Oracle and the capital cycle:

“There is no way for Oracle to pay for this with cash flow. They must raise equity or debt to fund their ambitions. Until now, the AI infrastructure boom has been almost entirely self-funded by the cash flows of a select few hyperscalers. Oracle has broken the pattern. It is willing to leverage up to hundreds of billions to seize a share. The stable oligopoly is cracking…The implications are profound. Amazon, Microsoft and Google can no longer treat AI infrastructure as a discretionary investment. They must defend their turf. What had been a disciplined, cashflow-funded race may now turn into a debt-fueled arms race”.

Doug O’Laughlin, Fabricated Knowledge, Sept 2025

A.I.

“The numbers that are being thrown around are so extreme that it’s really, really hard to understand them,” Einhorn said. “I’m sure it’s not zero, but there’s a reasonable chance that a tremendous amount of capital destruction is going to come through this cycle.”

LLM’s are Glorified Autocomplete.

I’ve been lied to several times.

Most bad data “came from Reddit and Quora – which are hardly sources of accurate information. There appear to be no mechanisms to see if the data is correct, they just scrape websites and take it as gospel....a lot of what they present is junk.”

Tavi Costa

“This is a defining question for the US in the years ahead: How long can America afford to sit out the global rush for gold? US gold reserves are now at 90-year lows, while the rest of the world has pushed their holdings to near 50-year highs. At one point, America held over 50% of global gold reserves. Today? Just 20%. My view: It’s only a matter of time before US policymakers are forced to rethink this stance.”

“My problem is when I drink heavily I sometimes do little bits that only I’m aware of.”

Rod Serling on Censorship, 1959

If anyone has too much Bitcoin and would like to send me some, I’m willing to help out: bc1qkvxy0f8tnxnjddwtyg3jshwgck4e9haw8e8kf9

I’m reminded of this passage from Dying of Money:

“The most extraordinary feature of the Reichsmark’s joyride was not any attack against it but quite the opposite, an incredible (”pathological,” it was later called) willingness on the part of investors at home and abroad to take and hold the torrents of marks and give real value for them.

Until 1922 and the very brink of the collapse, Germans and especially foreign investors were absorbing marks in huge quantities. Only the international reputation of the Reichsmark, the faith that an economic giant like Germany could not fail, made this possible. The storage factor caused by the investor’s willingness to save marks kept the marks from being dumped immediately into the markets, and thereby for a long while held prices in check.

The precise moment when the inflation turned upward toward the vertical climb was undoubtedly timed by no event but by the dawning psychological awareness of the German and foreign investor that Germany was not going to back its money. With that, the rush to get out of the mark was on. Like a dam bursting, the seas of marks flooded into the markets and drove prices beyond all bounds. The German government strove mightily to outflood the sea.”

Rudy: Our lack of feedback is inversely proportional to how much we like your post.

Keep them coming.

Besides the sometimes cynical humour I suspect to underly your posts (while enjoying it) I'm most excited about the embedded history lessons.