The Bezzle

A net increase in psychic wealth.

“As to whether I have been deceived, disillusioned…The answer is yes, I suppose. I had the misfortune to be nourished by the dreams and visions of great Americans—the poets and seers. Some other breed of man has won out.”

Here’s my expert technical analysis of the QQQ’s:

This funny video explaining cryptocurrency - almost 3 years old - went viral again. It’s satire. Most people did not seem to realize that.

Amazon vs Nvidia

The Bezzle

“In many ways the effect of the crash on embezzlement was more significant than on suicide. To the economist embezzlement is the most interesting of crimes. Alone among the various forms of larceny it has a time parameter. Weeks, months, or years may elapse between the commission of the crime and its discovery. (This is a period, incidentally, when the embezzler has his gain and the man who has been embezzled, oddly enough, feels no loss. There is a net increase in psychic wealth.) At any given time there exists an inventory of undiscovered embezzlement in—or more precisely not in—the country's businesses and banks. This inventory—it should perhaps be called the bezzle—amounts at any moment to many millions of dollars. It also varies in size with the business cycle.

In good times people are relaxed, trusting, and money is plentiful. But even though money is plentiful, there are always many people who need more. Under these circumstances the rate of embezzlement grows, the rate of discovery falls off, and the bezzle increases rapidly. In depression all this is reversed. Money is watched with a narrow, suspicious eye. The man who handles it is assumed to be dishonest until he proves himself otherwise. Audits are penetrating and meticulous. Commercial morality is enormously improved. The bezzle shrinks.”

- John Kenneth Galbraith, The Great Crash 1929

An insightful reply to the above:

People think they're going to get paid X, but they're only going the get X/2, either through outright default, or the sneakier default of inflation.

WSJ Fed Publicist Nick Timiraos, September 2020

No one in Congress objected to the Fed’s “new inflation strategy” of seeking above-2% inflation for an extended period of time. This was a financial war crime.

Ben?

So Neel Kashkari replied to Timiraos’ tweet, and I responded to Kashkari.

Almost 4 years later:

“One of the most profound comments that I’ve heard over the past couple of years was with a labor leader who represents low-income service workers…She said to me, inflation is worse than a recession. That is contrary to conventional economic thinking." - Kashkari

Conventional economic thinking is nonsense.

Yet there is never any accountability at the Federal Reserve for their horrific policy errors which permanently harm hundreds of millions of Americans.

fyi Here is the RSS feed for the podcasts I've been on, if you want to import them into a podcast app or something. A while back I went with "All I Wanted Was A Pepsi" as my Substack podcast title, after the Suicidal Tendencies song, “Institutionalized.”

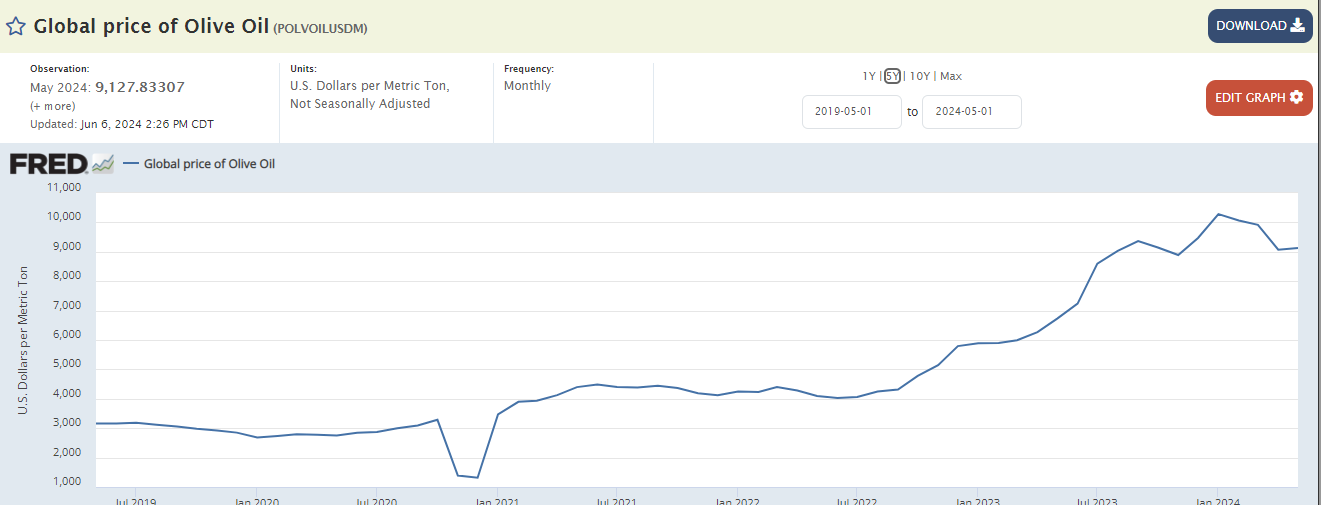

Below the fold we have, among other things, Rob Arnott, a funny takedown of current A.I. hype, some tunes, systemic risks at the banks (and the FDIC), “economic realities”, NYC lofts for $175 a month, permanently high plateaus, assorted real estate madness, Dallas suburbs, reaching for yield, Canadians, hordes, Cem Karsan, low-IQ lenders, private-perfidy I mean equity, a new Japanese word, Utah highway patrol, comets, CLO’s, probability, panic, Yellen-bashing, and olive oil. Hope you see something that interests you.

I’ll try to take tomorrow off from reading, and rest the eleven brain cells left.

Also, I did not watch the “debate,” nor did I discuss it here!

“People talk about monetary policy having long and variable lags. That's another way of saying we have no clue if there's any relationship at all.”

A Gundlach quote from last time I wanted to highlight:

“Year-end 2021, anybody with a brain knew that inflation was not going to be transitory, and it was going to go up well above that 2% number, and bond yields in treasuries were at one-percent or lower. That's a horrible investment. It's not even an investment. It's just a thing that you own because you're too dumb to sell it.”

Here’s Stan Druckenmiller on a related topic back in October 2023:

Bifurcated Economy

Vail Resorts: “Skier visitation from lift ticket guests was down 17% compared with the prior year period, but total net revenue for the company increased 3.6% to nearly $1.3 billion for the three-month period that ended April 30.”

Been noticing this trend for a while. Lower unit sales, higher revenue. If you have to ask how much it is, you can’t afford it.

Let’s Talk About A.I.

I started working as a data scientist in 2019, and by 2021 I had realized that while the field was large, it was also largely fraudulent. Most of the leaders that I was working with clearly had not gotten as far as reading about it for thirty minutes despite insisting that things like, I dunno, the next five years of a ten thousand person non-tech organization should be entirely AI focused. The number of companies launching AI initiatives far outstripped the number of actual use cases. Most of the market was simply grifters and incompetents (sometimes both!) leveraging the hype to inflate their headcount so they could get promoted, or be seen as thought leaders.

The above is the funniest article I’ve read since this review of “Hamilton.” So many great lines. Highly recommended. Bad language.

I wrote in 2015 “I really don't want gold to go to $10k. I'd rather have it be $500 or something and have society actually deal with problems.”

“I don't own gold because I think it might go from $2,375 to $2,538, or some number like that. I own gold because I'm afraid that it's going to $7,000 or $8,000 or $9,000, and the set of circumstances that would cause that price performance would damage other parts of my portfolio and my life.”

“As we say at Grant’s, we’ll know more in ten years.” - JG

Paul Kupiec on the health of and risks to the institution of banking. “When banks fail, the loss rates on their assets are pretty high, 20% or more.”

The FDIC’s Deposit Insurance Fund (DIF) reserve ratio was 1.17 percent on March 31, 2024. That means 1.17 cents for every dollar of deposits (but we have a printing press...)

Kupiec has a new article out, “Commercial Real Estate and Bank Systemic Risk”

Regulatory guidance suggests that bank CRE concentration ratios above 3 may be indicative of excessive CRE loan exposure. (The preferred supervisory CRE concentration ratio is a bank’s total CRE loans divided by the sum of its Tier 1 capital plus ALLL balances.)

At a minimum, regulatory guidance suggests that supervisory CRE concentration ratios greater than 3 warrant additional examiner scrutiny. Using the supervisory CRE loan concentrations measure, there are 1,763 banks with CRE concentration ratios greater than 3, including 274 with concentrations greater than 5 and 77 over 6. Most of these CRE concentrations are at smaller banks, but there are 2 banks with assets between $50 billion and $250 billion with supervisory CRE concentration ratios greater than 5.

First Republic Bank

First Republic had a high concentration of CRE loans and a large unrecognized interest rate driven market-value loss on its assets.

As of December 2023, the most recent regulatory data available, Republic First reported $5.88 billion in assets including $1.6 billion in CRE loans. With $288 million in regulatory capital, Republic First had a Tier 1 leverage ratio of 4.4% and a supervisory CRE Tier 1 + ALLL concentration ratio of 5.19.

According to my calculations, on a mark-to-market basis, Republic First had over $600 million in unrecognized mark-to-market losses, making the real market value of its Tier 1 capital negative $400 million. The FDIC cost of resolving of Republic First largely agrees with this unrecognized-loss estimate considering that the FDIC loss also likely reflects an additional discount for the bank’s CRE loan concentration. The Republic First resolution cost the deposit insurance fund $667 million.

A list of all bank failures can be found here.

Brookfield’s Plan To Transform $10B Mall Portfolio Snagged By Market Realities

“Brookfield Property Partners spent more than $9B in 2018 to become one of the largest mall owners in the U.S. with its acquisition of mall owner General Growth Properties, betting on its ability to transform those assets by adding residences, hotels and offices. Six years later and after committing at least $2.5B to property upgrades, Brookfield’s pledges have gone largely unfulfilled.

Brookfield has completed significant redevelopment at only two properties and has just two others in the immediate pipeline, The Wall Street Journal reports. Brookfield contends it is only now ramping up but acknowledged that economic realities had delayed some of the firm’s vision…

The asset manager said at the time that it would convert most of the company’s 125 malls into mini cities that included residences, offices or hotels to complement the retail offerings. Brookfield has finished significant upgrades in Atlanta and Seattle, and it has redeveloped more than 40 former department stores since the acquisition.”

Two out of 125 ain’t bad, right? Stupid “economic realities.” More on Brookfield can be found here.

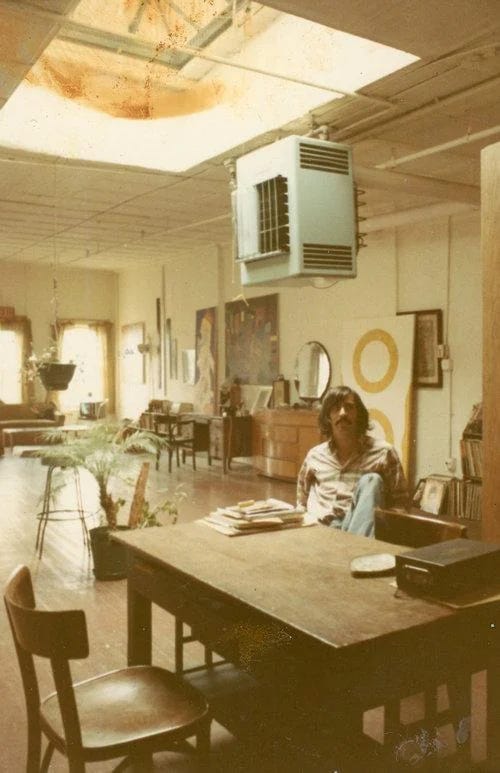

“I used to live in a NYC loft in the 1970s: A 5 flight walk-up, but 2000 sq ft at $175 a month”

“And with a skylight! A SKYLIGHT?!? People would push their own mothers into oncoming traffic for 2,000' with a skylight today.”

I haven’t been to New York since 2019 and have no idea what this would rent for today. How much can one banana cost?

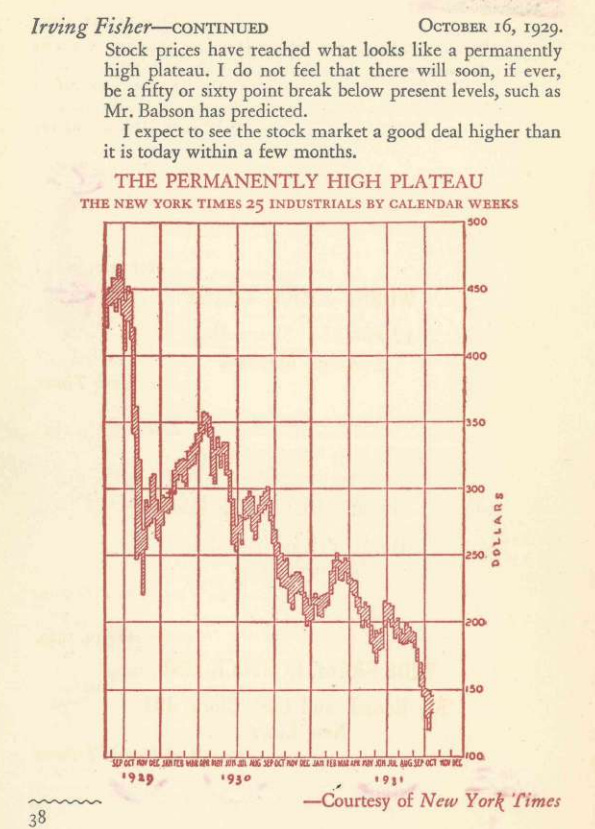

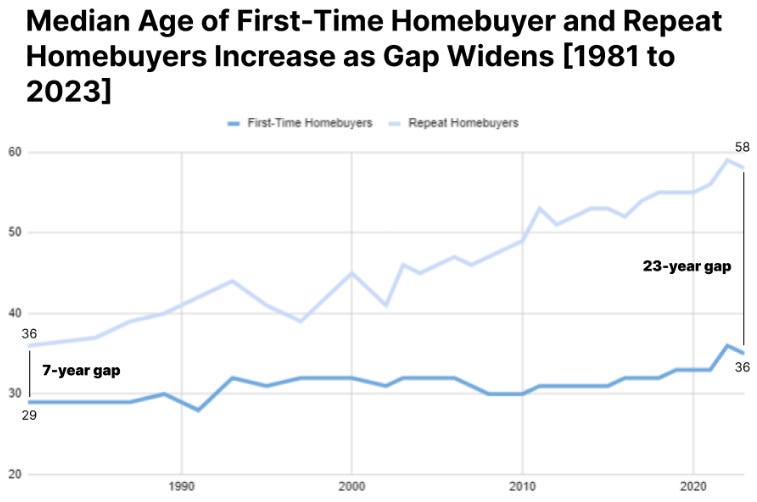

A Permanently High Plateau

“What I'm saying may sound very different from what you hear.” - Melody Wright

That’s why I like her housing analysis so much. Also her comment, “We are just living on narrative right now,” applies to far more than just real estate.

“…according to a LendingTree study, 60% of Americans live paycheck-to-paycheck. Almost 11% of people over 65 live in poverty. Yes, it’s lower than other age groups, but increasing. Whether we like to acknowledge it or not, all Boomers are not rich. In fact, they are the biggest contributor to our increasing homeless population. With the increases in property taxes and insurance this year across the country (not just TX and FL), many Boomers may soon find themselves dangerously close to falling into poverty.”

I hate this

We’ve financialized everything.

So is gas.

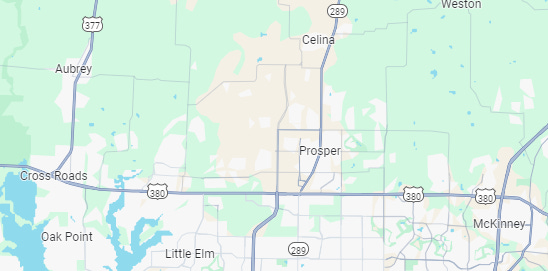

North of Dallas

Aubrey, Prosper, Mckinney, and other residents around 380, why are so many people selling?

“I've been looking into a few neighborhoods throughout Downtown DFW and its suburbs and noticed that a lot of the Northern DDFW new build communities have a LARGE amount of people selling.”

Some of the top comments:

I have no proof, but I think return to office mandates are making people regret moving an hour away from work.

I wonder if it's the astronomical property taxes and insurance, and paychecks not keeping up.

I can attest to this. We decided to buy in Aubrey last year and foolishly thought traffic couldn’t be that bad. I work in Las Colinas and it’s a nightmare everyday. Love our house and the general area but there are many regrets with the time it takes even to go to the grocery store.

The drive. The traffic. 380 is a complete shit show - you can not go grocery shopping 2 miles down the road unless you like being in a car for 20 minutes. The infrastructure is not built for the mass people that have moved there. Everything is a 1 lane road. I don’t believe the roads will be complete until 2029. My commute to work was an hour and 20 each way every single day and I hated it so much, so I had to sell

Isn’t this what they said about Allen, Plano and Frisco ten to twenty years ago?

Have you driven 380. It is a death trap.

Even when the construction of the flyovers between FM 720 and DNT are completed, living north will continue to be hell for years to come. Too many 2 lane roads and 4 way stops. The developers, and the politicians who take their money, are absolutely corrupt. These mega developments should not be allowed without proper road infrastructure.

You’re spot-on; when folks in city planning make those same points, the common response is along the lines of: “We can’t do anything that would make a developer rethink building! We have to build as much housing as we can, or we won’t get enough tax revenue to build out the infrastructure needed for all these people!”

From personal experience, the massive communities that spring up overnight built by national homebuilders have lots of build issues. I have theories on why that is but won't get into it. We had roof and plumbing issues requiring major repairs when the house was less than 3 years old. Multiple neighbors have had similar issues. Friends in Prosper also have similar issues.

Land Surveyor who works in these communities. These places are no longer an hour from Dallas. They are nearly 3 if you live far enough away from 75 or too north of 380. You will pay twice as much a month on tolls as gasoline. The "walkable" layout is not walkable. Like dude the first week you walk around without an umbrella in July you'll list it too. The trees are too young. The shade is decades away from being consistent. The amenities? They actually aren't that complete and you'll be driving into minimum Plano and Frisco all the time if not Dallas as well for real shopping or fun...Also, they aren't well built. The explosion in trades has more illegal 20 year olds slapping together houses than ever before and it shows. The quality of homes from my builders is TERRIBLE. I make sure the shitty house lands in the right spot and try and keep the fence guys straight…Cannot believe someone is paying some of these fucking dumb ass kids to install high end amenities in expensive housing.

[Commenting on the above post re: build quality] I understand everyone being preoccupied with the commute and traffic issues because they are right-now problems that hit you in the head every day. But this is a huge long-term issue that's harder for people to see but equally important.

I bought in Aubrey in 2020 and saw the building and traffic explosion. My commute to work turned into an hour and a half each way. Just going to Walmart to grab something “quickly” in Crossroads was a couple hour adventure with all the roadworks and traffic. I sold and moved to Edmond, Oklahoma this year. Similar house/lifestyle but with only a 12 minute commute to work and none of the astronomical property taxes. I was sad bc at the beginning, loved north Texas. By the end, we were just existing - cost of living increased so much, hated trying to go out to do anything bc just sat on the 380 or Fishtrap Rd, weather extremes and trouble with the grid, increased crime and my kiddo’s elementary school going on lockdown several times. The lack of infrastructure and support services made for a lacking quality of life for sure.

There are lots of homes that are rentals owned by BlackRock and other companies in that area and sometimes they divest.

Our mortgage went from $3600/mo to $4600/mo. We are seriously feeling the stress burning an extra thousand a month in taxes. We'd sell and downsize but we'll be in the same damn boat financially but with a smaller home, so we have to stay put. Purchased in 2015 for $450ish, thankfully with 2.5%, now worth a million. It's stupid. This isn't sustainable for anyone.

After having moved to Chicago from DFW, I’ve found the income tax here in IL, 4.9% basically is a wash with DFW when you consider the property taxes. Dont let people fool you that it’s somehow so cheap and wonderful to live in a place with no state income tax.

REACH FOR YIELD

Real Estate Investors Are Wiped Out In Bets Fueled By Wall Street Loans

Lynn Nathe was growing tired of the meager gains from her family’s retirement account. In late 2021, she invested $200,000 with a company that was making 30% returns by buying the hottest ticket in global real estate: U.S. apartments.

Now, she says, most of that money is gone…

Much of the worry over U.S. commercial property has legitimately centered on the office market, where more than $38 billion in buildings were in distress as of March, compared with about $10 billion for apartments, according to MSCI. But multifamily buildings make up the biggest share of properties with potential distress—exceeding even offices—with more than $56 billion worth of real estate at risk of financial trouble, the firm’s data show. And unlike office buildings, largely backed by major financial institutions, much of the unraveling is centered on personal investors…

“When you’re at a casino, you know what you’re doing is gambling,” said Aleksey Chernobelskiy, whose firm, Centrio Capital Partners, runs a service helping retail investors salvage their investments in multifamily deals. “Here, people were gambling but they didn’t know it.”

This was largely because of insane ZIRP policy:

“Nathe was pulled in as crowd-sourced investments were playing a larger role in the financial landscape. At a time meme-stock buyers were banding together to topple hedge funds and crypto bros were sending Bitcoin to the moon, everyday investors were also targeting real estate, leveraging technology to build empires of Airbnb vacation homes, self-storage facilities and most of all, apartments.

Nathe started following a wealth influencer named Mir Jafer Ali Joffrey, who went by the nickname “Buck.” He had an earlier career as a cosmetic surgeon, with a Chicago-area clinic that offered liposuction and Brazilian butt lifts. After striking wealth with real estate, he turned to full-time investing about a decade ago.

Joffrey hosted a podcast called Wealth Formula dedicated to personal finance and helping people invest their way to an easier life. One guest was LePage, a former project manager for telecom and utility companies who began flipping houses in Phoenix after the financial crisis. She parlayed that into a business and formed Western Wealth Capital with David Steele in 2014. The company turned into a success; LePage, in an email to Bloomberg, said the firm had average annualized returns of more than 30% from 2014 to 2022…

Nathe was sold. She took $50,000 stakes in four Western Wealth deals: one in Arizona and three in Texas, including the Carling…

You can read the rest of Nathe’s tragic saga if you want.

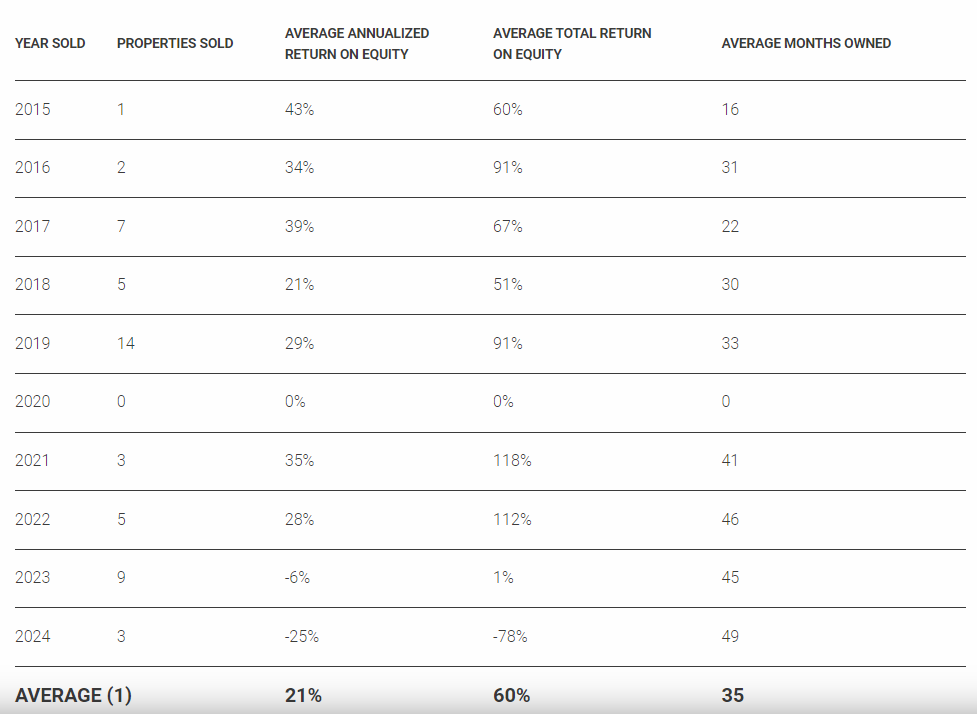

So I went to the Western Wealth Capital website. I’m reminded a bit of Taleb’s Turkey. Not sure if these numbers are audited in any way.

As Gundlach said in my last post, No Fatal Errors!

So “Western Wealth Communities is a people-first property management company, that strives for excellence at every point, and with every person involved,” and is owned by Western Wealth Capital.

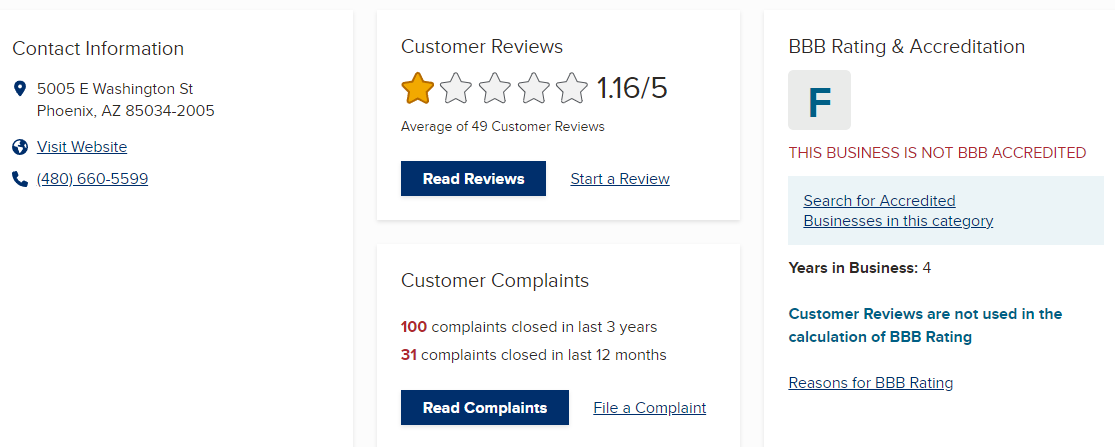

The Better Business Bureau has more color on that part of the operation:

Caveat emptor.

“I think the correct monetary policy is keep it simple. The long end of the curve - managed by the market, by the bid and asks of millions of investors - sets the long-term real cost of capital. Why not just keep the short rate half a percent or a percent below the long rate, and just use that as your guide? The Fed likes to say they're data dependent, but the data they depend on seems to change from one meeting to the next. Seems like they choose whatever data confirms what they want to do anyway.1

Why not use the one data point that is set by the market, long rates, as your most important data point, and say we'll just keep the short rate half a percent or a percent below that? That would suggest a much lower rate than today. Slashing rates today would probably not be a good idea, but moving gently and gradually in that direction is probably harmless. Zero interest rates for a decade plus was incredibly stupid.”

In other words, you could replace the FOMC with an A.I. bot that could figure out every month whether the Fed Funds rates should be 50bps-100bps below the 10-year (which is today at 4.29%.)

‘More money has been lost reaching for yield than at the point of a gun.’

"California’s teacher pension fund experienced a 9% real estate loss in 2023."

Canadian pension funds retool real estate strategies amid market slump

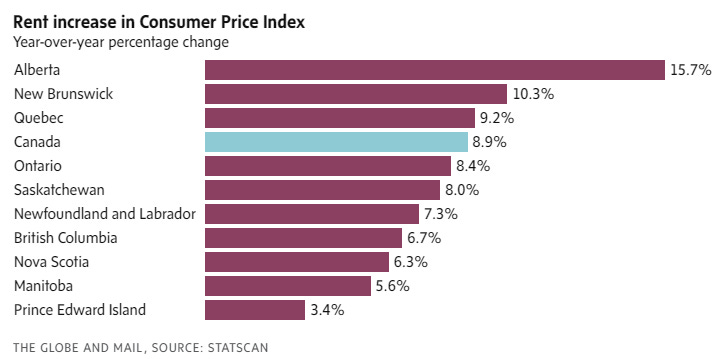

Canadian rents rose 8.9 per cent in May, year-over-year, up from 8.2 per cent in April. This was the largest increase Statscan has observed since changing its rent methodology in 2019.

“Societally it’s a disaster”

“I think this policy of letting in as many people as possible is designed to stimulate the economy, and just give them government goodies, and they'll spend it immediately, and it's increasing the velocity of money, and there's also of course you want to change the the the make-up of the country in terms of voting. I mean the Democrats obviously want more Democratic voters, so they're letting in illegal immigrants, but it also stimulates the economy in the short term, and economically it's a bonus. Societally it's a disaster, because you're letting in people too fast, you're not vetting them, they're not coming in the traditional way, and a lot of these people are unskilled, so societally it's a disaster. Economically it it actually helps.”

Replacement Migration: Is it A Solution to Declining and Ageing Populations? United Nations, March 2000

“The Quant Community has gotten itself besotted with the notion of dive into history, find the relationships that appear in history, concoct a story for why this should work after you've already identified that it worked, and then presume that it'll work in the future. That's not scientific method, and so the Quant Community today I think is not that much closer to scientific method than the old rule of thumb investors of the 40’s and 50’s.”

Vanguard FTSE All-World ex-US ETF (VEU) vs SPY

The idea here was to show the massive U.S. outperformance since 2011, which Arnott mentions.

Cem Karsan: “The cost has been inequality”

With Grant Williams and Bill Fleckenstein

“interest rates are going bottom left, top right.”

“The final moves are everybody is short and they’re right, but they can’t stay anymore and they have to buyback. That’s the impulse that comes at the end. The biggest gains come at the end and it’s very vertical and then almost a V into these big declines.”

“We knew in ‘98 that markets were already getting way too expensive and that there was a tech bubble brewing and things kept going for two years and eventually crashed. We knew, people were talking in ‘05, ‘06 about the housing bill, it just went till ‘08. So it’s coming.”

“I think we’re probably going up quite a bit before we come down. That said it’s coming and the cause of it is very different this time. And that’s important. It’s a very different thing than ‘07, ‘08. It’s a very different thing than ‘99, 2000. How? Because of this inflationary piece. The Fed has been able, for 30, 40 years, to come to the rescue without any hindrance, without any cost really to what they’ve done. The cost has been inequality.”

“…the loss of faith in the Fed’s ability to bail out the markets like they have in the past, will eventually cause a much bigger issue. It’s important, in 1968, the PE multiple of the S&P 500 was around mid-twenties. By 1982 it was four. How do you get to four? Because you get ten-year interest rates at 20%. Why would you buy a risk asset for anything higher than four multiple? So if rates keep going higher, at some point the math just doesn’t work for markets. It’s that simple. And rates will have to go higher if we have a decline because the Fed won’t just be, in my opinion, be able to just do what it’s done every other time. And I think that’s what’s really different this time and that’s what makes us much less likely to be just a V bottom like we saw last time around. This is a decade long phenomenon in my opinion, and this is, in my opinion, a dead decade, in nominal terms and in real terms, a awful market environment for investing in equities.”

“…dispersion in the market, the single names moving away from each other and having all of this volatility underneath the surface, while the index is very placid, is what we’re seeing. And what that tells you is that the underlying forces, and I think of it as the more fundamental volatility circumstances of the market, are actually increasingly, they’re dangerous. There’s issues under the hood, but it’s all being held by this index plug.”

On the Fed monetizing the debt: “The Federal Reserve will buy those holdings is my point. And they’ll internalize the debt and they’ll digest it. They’ll hit a button and then shake hands with the treasury. And it’s nothing different than just printing dollars. It’s the same thing.”

Karsan makes the point that Treasury monetization will not hurt the dollar because the U.S. dollar is underpinned by “power, and power is absolute.” I’m sure you could’ve made that argument about the British pound in times past. It seems to me that there is strong motivation now more than ever for 7 billion or so people to figure out if they want this situation to be permanent. Fleckenstein countered that “maybe against hard assets, the green and paper could decline quite substantially, if we choose that path.

“Lenders have too much money and rather than do the smart thing and save it for a rainy day, they are pouring it into increasingly risky loans with diminishing interest rates, lousy covenants and low liquidity."

- Michael Lewitt

“As reported today in the Financial Times, borrowers in the leveraged bank loan market have repriced about $400 billion of debt at lower rates this year thanks to strong demand from institutional lenders (mostly CLOs). Even without the Fed lowering rates, borrowers have been able to reduce their interest costs by as much as 50 basis points. In January, investors were pricing in six 25 basis-point rate cuts this year; now they will be lucky to see one cut before year end. But lenders have too much money and rather than do the smart thing and save it for a rainy day, they are pouring it into increasingly risky loans with diminishing interest rates, lousy covenants and low liquidity.

This is a byproduct of excessive systemic liquidity resulting from $2 trillion annual fiscal deficits in the United States. Too much money lowers the collective IQ of the market. With increasing signs of economic weakness reflected in lower interest rates, borrowers are acting opportunistically while lenders are acting pro-cyclically (which is another word for foolishly). The leveraged loan market is filled with weak credits with covenants that offer extremely limited lender protections against the increasingly aggressive tactics of borrowers owned by private equity firms. Borrower-on-creditor violence, which normally involves borrowers shifting assets/collateral out of the hands of lenders, is increasingly common when private equity firms see their portfolio companies run into financial trouble.”

Good discussion with Gretchen Morgenson about the dark side of private equity

Tsundoku "means buying books and letting them pile up unread."

"Utah highway patrol officer sits and chats with homeless man and his dog under an overpass...I was so caught off guard by this. I came back around a while later expecting them to be gone, but nope they were still sitting and chatting. Pretty cool."

Of minor interest to me is the Younger Dryas Impact Hypothesis:

Sediment sequences spanning the 12,800-year-old lower Younger Dryas boundary (YDB) were investigated at three widely separated sites in eastern North America (Parsons Island, Maryland, a Newtonville sandpit in southern New Jersey, and Flamingo Bay, South Carolina). All sequences examined exhibit peak abundances in platinum (Pt), microspherules, and meltglass representing the YDB cosmic impact layer resulting from the airbursts/impacts of a fragmented comet ∼12,800 years ago. The evidence is consistent with the Younger Dryas impact hypothesis (YDIH) recorded at ∼50 other sites across North and South America, Europe, Asia, and the Greenland ice sheet. These sequences were also examined for shock-fractured quartz, based on a recent study suggesting that low-shock metamorphism may result from low-altitude bolide airbursts similar to that observed during near-surface atomic detonations. Now, for the first time in a suite of well-separated sites in North America, we report in the YDB the presence of quartz grains exhibiting shock fractures containing amorphous silica. We also find in the YDB high-temperature melted chromferide, zircon, quartz, titanomagnetite, ulvöspinel, magnetite, native iron, and PGEs with equilibrium melting points (∼1,250° to 3,053°C) that rule out anthropogenic origins for YDB microspherules. The collective evidence meets the criteria for classification as an “impact spherule datum.”

If you’d like to take a free online intro to probability course from a Rutgers prof, here you go. There’s a 50-50 chance I will watch it.

I found this to be a good explanation of CLO’s, by Shiloh Bates

Latest Trepp CRE Podcast: “Pressure to Deploy”

This is encouraging:

A post on Reddit with 11,000 upvotes and almost 400 comments, many bashing Janet Yellen.

If you add up Janet Yellen's Citadel b̷r̷i̷b̷e̷s̷ speaking fees in just 2019 and 2020, you get $810k, but a note at the bottom of her financial disclosure report says she got a "refund" for a cancelled event of $50k-$100k. Maybe Zoom wasn't working that day. And have you ever actually listened to her speak? It’s painful.

“I think over the last 30-something years, the Fed has become like the rest of the economic organizations in Washington DC, where they're given an answer and they justify it.” - Alan Boyce, 2016

I love the section about all the AI insanity going on. No one has any idea what it's all about and what changes it would bring. I remember a few years ago I saw something about coal miners leaving the mines and learning to code, with the idea that coal mines have no place in the future and coding will never go away. Fast forward to now, India, China, and even Germany use more coal than ever before and AI is promising to build software without coding. The only person who could see the future was Nostradamus, who did so by staring into his chamber pot for hours on in. No wonder he saw everything going to shit.....

Action-packed edition!

I loved the AI rant. I do not have that guy's level of programming skills, but I was in a PhD program and worked for very well-respected professors in the field (going back to the 70s) and learned a lot of the math that makes these algorithms work. For almost the last decade I have worked as an analytics manager at very large, quite well-known brands. The number of smarmy know-nothings who I've encountered that inexplicably talk down to me in made-up buzzwords really grinds my gears. Most of the company is run on spreadsheets, we have data and report failures every day, I can't even get people to use a simple regression analysis, and somehow and LLM will solve our problems. It's total insanity! Anyway, my team will appreciate this rant (and they work for me so they are used to the language).

The Hamilton piece was also great. The 0.001% American phenomenon really put it in perspective. I remember hearing about it and thought the premise sounded awful. Confirmed.

Tsundoku: Maybe knowing this word exists will help me out. Then again, I expect a physical library of books, records, and movies will turn out to be pretty solid long-term investment regardless of whether I ever read, listen, or watch all of them.