Few seem willing to recognize that the problems our financial system face right now are largely the result of terrible Federal Reserve ZIRP and QE policies, which massively distorted free-market price discovery for much of this century, rather than the return of interest rates to historically normal levels, as leveraged Wall Street asset-gatherers and their scribes suggest.

This video clip with Randy Woodward highlights, among other things, the disastrous consequences of the Federal Reserve - in particular - unnecessarily and massively distorting the mortgage-backed securities (MBS) market in 2020.

Some background:

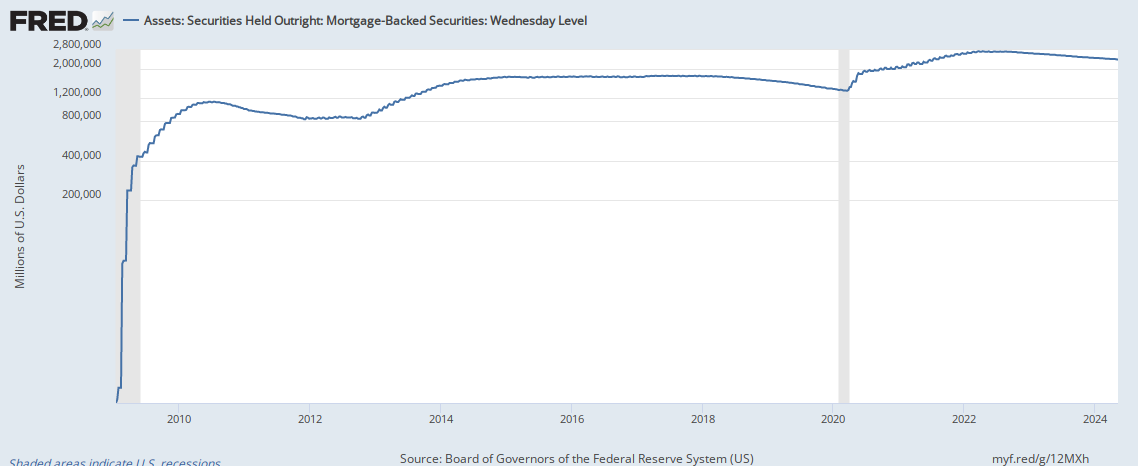

For the first 95 years of the Federal Reserve’s existence, they owned NO mortgage-backed securities.

Then, from January 2009 to June 2010, they purchased1 $1.128 TRILLION, a monstrous amount, ostensibly to save the world, or at least save Wall Street bonuses2.

Despite two very feeble attempts at “QT” in 2011 and 2019, by March 2020, the Federal Reserve had actually increased their MBS holdings to $1.366 trillion.

Then they went insane.

By April 2022, the Federal Reserve had monetized an additional $1.374 TRILLION of MBS, bringing their ownership at the peak to $2.74 trillion. Now, after almost a year of alleged “Quantitative Tightening,” they STILL hold almost $2.6 trillion of MBS, and as bank bond expert Randy Woodward suggests, there was no clear reason for them to buy them at all in 2020.

(A semi-log chart is even funnier)3

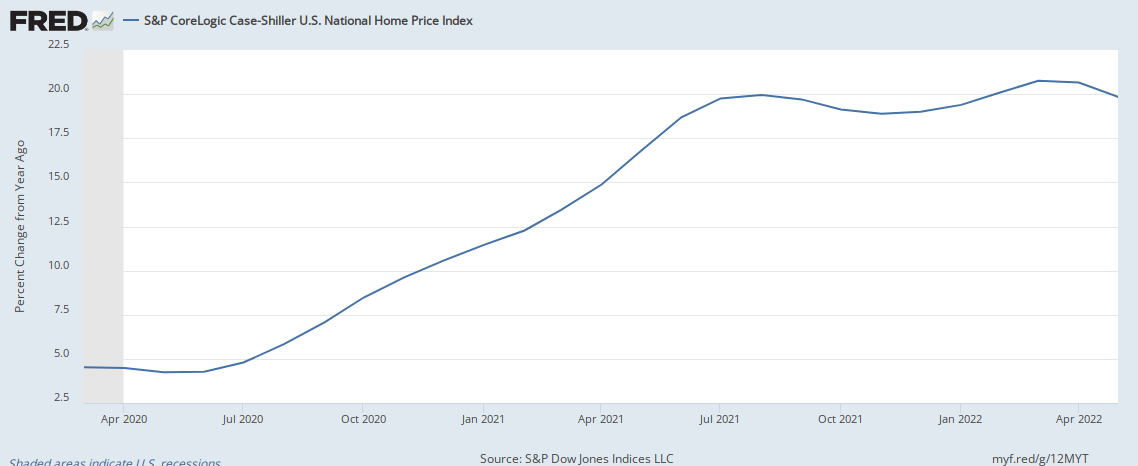

Incredibly, the $1.374 trillion of MBS purchases by the Federal Reserve between March 2020 and April 2022 continued even as the S&P/Case-Shiller U.S. National Home Price Index annual appreciation rate spiked from 4.5% to 20.7%!

They were putting out a fire with gasoline.

Video Clip Transcript

Inside the Financial Storm: Expert Randy Woodward with Michael Gayed

I think the biggest thing is that nobody really understands, or a few people do - and it's okay, because I have a very unique eye line into what's going on. There's not a lot of people that do what I do, that see portfolios, bank portfolios, every single CUSIP they own. This is all I've done my entire career. And I've seen it ebb and flow.

I've seen mistakes made. And my job is to make sure my banks make as few mistakes as possible. But when you got into March 2020, that's really where the massive manipulation started. And it was a double whammy. Because not only did the Fed take rates to zero - and this is the one, the one thing that I'm really curious about, I hope somebody will figure it out someday - is why they were buying mortgages as well.

Because basically what happened is as we went into 2020, we were slowing down in 2019. We're probably likely headed for a recession, which meant my banks had a lot of money to invest, which means all banks probably did too. So they were buying. I'll give you an example, and I use 30 year mortgages as an example. Most banks aren't buying 30 year mortgages. Some did, but most didn't. But it's a good example because I did have some doing that going into late 2019, I'm just going to use a very simple Fannie Mae two and a half percent 30 year mortgage, prices were going up from about September into February 2020. So they were going to about say, 102 - bonds price to par. And you got to pay a premium when rates are lower, and there's more aggressive buying.

Well, something was going on4. Obviously we were getting into COVID. Somebody - I don't know who - all of a sudden had to sell mortgages very badly, and they were flooding the market and prices went down to about par. And I will tell you, my banks were buying hand over fist, as much as they could get, as fast as they could get.

Well, I don't know who that somebody was, but the Fed decided we have to buy those5. We have to save that market. And in one week, they took prices from par 100 cents on the dollar to 105. That is a massive, probably never seen in my career, a move up or down that hard, that fast. So all these banks now are having to deal with these prices, these manipulated prices, by a huge percentage, and on top of it, and that had ramifications - please jump in if I talk too much.

So here you are, Banks have a bunch of money. You just made the main product they want to buy, whether it be agencies and primarily government backed collateral, [higher]. So whether it be just agency debentures or mortgage backed CMO’s, whatever, you just took prices up dramatically, artificially, and forced the bank's hand to have to invest in that world. They can't just sit up on cash.

It doesn't work that way. Then as you go through COVID well, as you go through and they kept rates this way, everything refinances. So all the mortgage bonds that you had all come back to you lightning fast, CPRS, which is a percentage annual rate of prepayment, they come back at 60, 70, 90 CPR, which means basically 80% of all the money you had invested comes back to you, if you have mortgage backed securities. So then it's worse because all the mortgages and all the loans and everything you had that you have on your books, that all has to reprice because of what the Fed is doing.

And then it gets doubly, doubly worse, where now we put out tons of stimulus, a trillion or some in actual money from the government for stimulus, PPE loans, all that jazz. And all that money has to be reinvested at these rates that are the lowest rates in history. And during that entire time, you're literally telling them, hey, rates are going to be low for longer. We're not even thinking about thinking about raising rates. And everybody's like, oh, they were told, they weren't told6. That's ridiculous.

That was about two years of not being told. And all of a sudden inflation goes parabolic and the Fed has to react, for whatever reason, as violently as they did. Here's what you have. Everything that banks own are at a loss. Every bond portfolio in the world is at a loss. And, if you're forced to sell it, like Silicon Valley Bank was forced to sell it, you got a problem. And that's a massive exposure that all banks are sitting on right now.

Clearly the Federal Reserve created a situation back in 2020 which eventually led to the failures of Silicon Valley and Signature banks (I won’t get into the Fed’s long history of abysmal bank regulation in this post.) This is all on them, yet no heads will roll.

In the economy, an act, a habit, an institution, a law, gives birth not only to an effect, but to a series of effects. Of these effects, the first only is immediate; it manifests itself simultaneously with its cause—it is seen. The others unfold in succession—they are not seen: it is well for us if they are foreseen. Between a good and a bad economist this constitutes the whole difference—the one takes account of the visible effect; the other takes account both of the effects which are seen and also of those which it is necessary to foresee. Now this difference is enormous, for it almost always happens that when the immediate consequence is favorable, the ultimate consequences are fatal, and the converse. Hence it follows that the bad economist pursues a small present good, which will be followed by a great evil to come, while the true economist pursues a great good to come, at the risk of a small present evil.

It seems that the Federal Reserve’s irresponsible, short-sighted polices are the real systemic threat.

Check out the entire Youtube interview.

There were two other passages that jumped out at me:

Repocalypse Now

Woodward discusses the transition from LIBOR to SOFR and the September 2019 ‘Repocalypse” here (about 27:52 in):

It’s almost comical because the smartest men7 and women in the world, creating this thing, didn’t see these ramifications coming8…all of a sudden repo blows up, it goes up to 10%, intraday - the fact that that happened, everybody should look at that and say, wow. You guys are supposed to be so smart, geniuses - you did not see that coming. They spent all those years trying to kill LIBOR and sell SOFR, and then SOFR blows up…and that’s where we got the reverse-repo line going, and basically now the Fed took over repo. Literally, that’s how they’re controlling rates.

They control all lending and borrowing rates on the short end for the whole system, and that’s gonna have ramifications, getting rid of a market number like LIBOR, where there’s some credit-stress spread to it, built in - that’s gone - which means new debt based off SOFR is going to be at a much wider spread than in the past, because they have to try to get any possible stress from that loan, from that borrower, they have to price that in at the beginning, because LIBOR won’t do it for them while the loan exists anymore.

“These are extraordinary steps, amazing, historic steps, that they’re having to do. It’s not a good sign.”

What I was amazed about in this process is the reaction to the BTFP program, the bond term funding program the Fed put in place. As far as I know, in the history of humans, that kind of lending has never been done, ever. I will take your collateral that’s worth 80 cents and I will lend you 100 cents. I’ve never heard of that. Also, I will charge you this rate, but if tomorrow the rates lower, I will allow you to change to that lower rate…that’s never been done. It’s an extraordinary facility…now everybody’s like, no big deal. These are extraordinary steps, amazing, historic steps, that they’re having to do. It’s not a good sign…

The Federal Reserve has been rewarded for their repeated incompetence and failure with even more power.

No one in Congress seriously challenges the Federal Reserve. Very few give it a hard time, and then only because they want the infinite Fed fun coupons directed their way.

The Fed enables a profligate (and warmongering) Congress, yet Congress is so corrupt they've completely abdicated everything to the Fed.

“As I peruse the after-market-close postmortem commentary and Twitter feeds from the talking heads every day, I can only emphasize that what's happening to markets today (both debt and equity), no matter what you are being told, even though it's incredibly entertaining, what's happening today has nothing to do with the Trade War, White House Tweets, the Wall, the Shutdown, Democrats, Republicans, Mexicans, Russians or Bob Mueller.....it has everything to do with a decade of horrific, politically motivated, easy way out, global monetary policy. And we are at risk of forfeiting the American Dream because of it.”

“horrific, politically motivated, easy way out, global monetary policy”

Or as I prefer, “monetized.”

To quote Citadel-Intern Ben Bernanke in 2012: “Monetizing the debt means using money creation as a permanent source of financing for government spending."

"The mainstream narrative should therefore be reversed: the stock market did not collapse (in March 2020) because lockdowns had to be imposed; rather, lockdowns had to be imposed because financial markets were collapsing." - Fabio Vighi

Woodward’s comment reminded me immediately of this passage from the excellent Christopher Leonard book, The Lords of Easy Money: How the Federal Reserve Broke the American Economy, detailing a little known $400 billion Federal Reserve hedge-fund bailout in September 2019:

The events of the following Monday showed that the Fed’s New York trading team was essentially flying blind in the age of ZIRP. This meant that the entire leadership team of the Fed, including Jay Powell, was also flying blind. The central bank had transformed the financial landscape by swamping it with money and in doing so had destroyed one monetary regime and replaced it with a new one. But there was no reliable instrument to measure the terrain of the new regime. This fact was made a stark reality on Monday, when the repo market blew up. The resulting market crisis almost became a full-fledged financial crisis, at a moment in history when the markets were supposed to be stable and in good health. The only reason that this didn’t happen was that the Fed stepped in, almost instantaneously, and initiated a $400 billion bailout. This bailout was unprecedented, and it benefitted a small group of hedge funds that had essentially hijacked the repo market and used it as a vehicle to make risky bets. The Fed saved them from the consequences of those bets. But maybe the most remarkable part of the bailout is that the Fed did it without much notice. A $400 billion emergency cash injection was no longer news. The Fed described it as a matter of normal maintenance. But that’s not how it looked from inside the Fed, as the repo market melted down.

“The fed-funds futures market sees U.S. rates effectively stuck at around 0% for the next three years” July 2020

"Arguably, too many of them are obsessed with their models, tweaks, thumb-dials and everything else, most infamously, John Williams, who without any manifest understanding of financial markets, was made President of the New York Fed.” - James Aitken, June 2020

“The Federal Reserve is not a cabal of evil geniuses dedicated to bringing down the global order so as to create a new one with its Wall Street masters in complete control. They are instead a clown-show, a remedial class of halfwits and empty suits opining on topics they would in a just society be banished from entirely.” - Jeff Snider, 2017

{kind=link}

{kind=link}