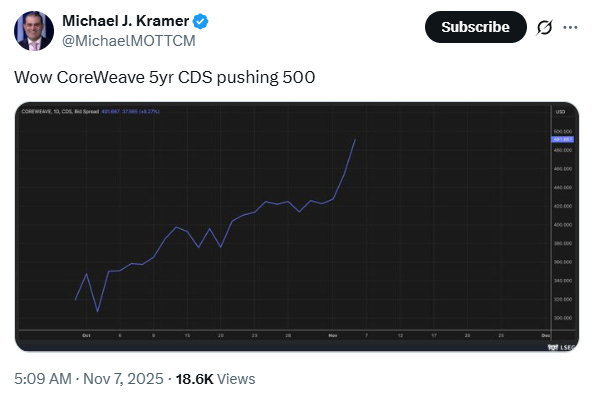

The false security of consensus

Pure contempt.

“Don’t take refuge in the false security of consensus.”

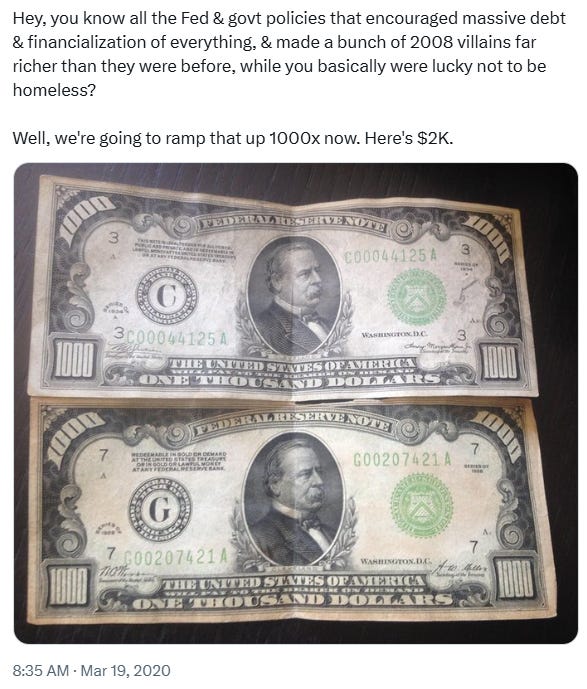

So now we’re going to get checks for $2,000, and we’re going to get 50-year mortgages, and that’ll make housing more affordable!

I’m having flashbacks to March 2020:

And another one that aged well:

I shouldn’t joke, because I know everyone is suffering from extreme fear right now, with the SPX 2.8% below all-time highs…

Some good podcasts below, Mike Burry philosophizes, a great essay, some AI nonsense, sentiment dissonance, our feudal housing system, crypto lending, auto finance, rents, some songs - plus the usual random stuff.

Hey - let’s be careful out there.

Sometimes, we see bubbles.

Sometimes, there is something to do about it.

Sometimes, the only winning move is not to play.

Michael Burry

“Burry’s tweet is pure contempt. The system is rigged. He knows it. The man who shorted the world is staring at a market that refuses to bleed. Liquidity is fake. Repo lines exploding. Twenty billion pulled through the Standing Repo Facility. Highest on record. That means collateral stress. That means the banks are out of ammo. Fed steps in. Pretends it’s normal. Pumps synthetic liquidity into a corpse and calls it stability. That’s what he’s watching. The same guy who made billions shorting real collapse now sees the same signs but can’t touch it. Because every signal that should trigger the crash is sterilized by policy. Repo backstops. Treasury buybacks. QE in drag. There is no market left. Only a simulation of one. He saw 2008 and made billions. Now he sees 2025 and can’t even place the bet. Because the casino rewired the chips. That’s why he said it. Not to warn. He’s tired.”

Burry in 2010: I Saw the Crisis Coming. Why Didn’t the Fed?

“Our leaders in Washington either willfully or ignorantly aided and abetted the bubble. And even when the full extent of the financial crisis became painfully clear early in 2007, the Federal Reserve chairman, the Treasury secretary, the president and senior members of Congress repeatedly underestimated the severity of the problem, ultimately leaving themselves with only one policy tool — the epic and unfair taxpayer-financed bailouts. Now, in exchange for that extra year or two of consumer bliss we all enjoyed, our children and our children’s children will suffer terrible financial consequences.”

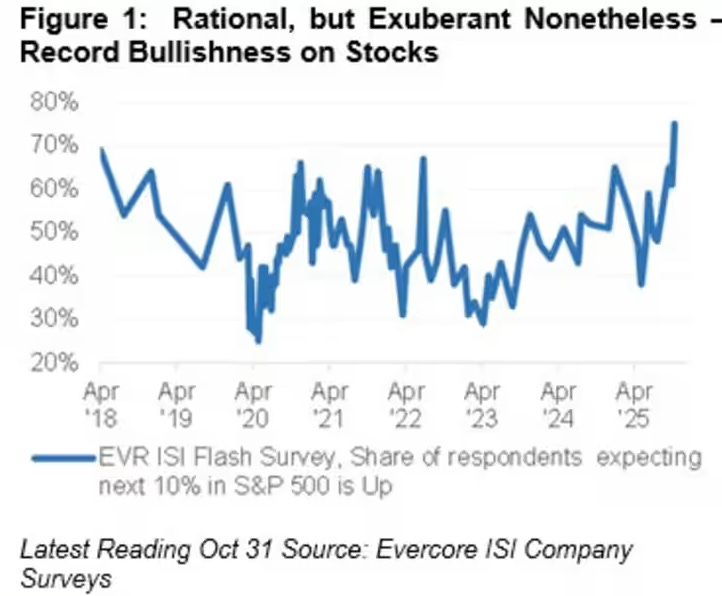

Also: “AAII Asset Allocation to stocks increased last month to the highest since Jul’24 while their cash allocation dropped to the lowest in 4 years.”

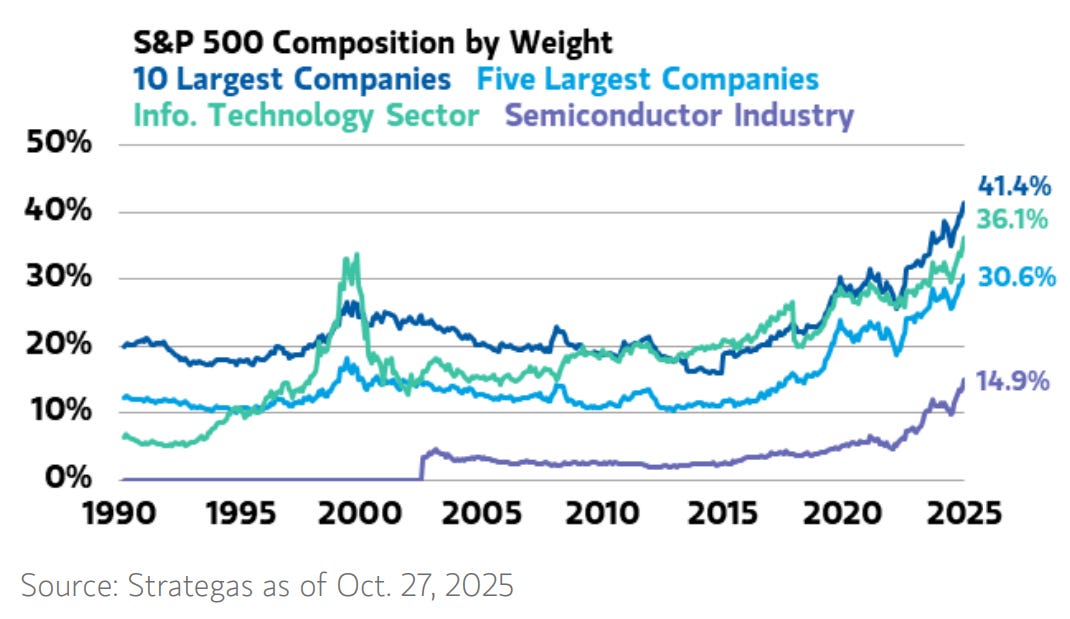

Everyone Owns The Same Stocks

“Volatility can never be destroyed, it can only be transmuted in shape and form. The mainstream view that central banks have somehow suppressed tail risk runs I think quite counter to common sense...they’ve taken tail risk from the present and shifted it to the future.”

“This is the problem with central banks the world over: they are in the business of imposing prosperity through financial means, rather than by treating prosperity as a co-product of actual growth. Their intentions are the best but what they are doing is incalculable harm.”

Jim Grant, 2011

(Source: My notes from a now-deleted Bloomberg interview with Grant and Jim Rickards)

Excellent essay worth reading:

The Theater of Nominal Growth

What does it mean for a system to contract when contraction itself has been made politically unacceptable?

For generations, contraction was something visible and undeniable. It meant markets plunging, banks collapsing, jobs vanishing. The word carried the weight of catastrophe: breadlines in 1929, foreclosures in 2008, the familiar rhythm of boom and bust that capitalism seemed to demand. That rhythm has been disrupted. Debt levels are too high to allow cleansing cycles, and policymakers are too dependent on asset prices to permit their fall. The bust has not been eliminated, only suppressed and reshaped into something less obvious but no less real.

The machinery of the present era pushes us relentlessly in one direction. Banks create credit with keystrokes, index funds direct flows upward regardless of valuation, deficits grow larger with no desire to shrink them, and the dollar’s reserve status sustains it all from abroad. What once acted as a check on excess through rising rates, falling markets, and painful but cleansing contractions has been disarmed. Markets are no longer signals to guide policy. They are instruments of policy itself.

You could see the shift clearly in 2008, when the infamous subprime mortgage crisis did not end with defaults clearing the system but with risk transferred onto the government’s balance sheet. The precedent was set. Every major disruption since has been met the same way. During the pandemic, interest rates were slashed to zero while the Federal Reserve quietly eliminated bank reserve requirements. In 2023, when Silicon Valley Bank collapsed, the response was not to let markets adjust but to conjure up the Bank Term Funding Program, a new facility designed overnight to contain losses. Later that year, Janet Yellen began skewing debt issuance heavily towards bills in order to ease pressure on longer-term rates. Each episode carries a similar rhythm: when trouble emerges, the acronym factory opens for business. Losses are papered over, confidence is restored, and the next act of the play begins. Contraction, in nominal terms, is treated as something to be prevented at any cost.

That shift changes everything. Losses are not permitted to clear, so imbalances pile higher. Debt is not allowed to shrink, so it multiplies. Every downturn is met with fiscal expansion that forces monetary accommodation. The result is a system that must keep moving forward, because to stop even briefly would be to reveal the magnitude of the distortions underneath. Contraction is not gone, it has simply been outlawed in nominal terms.

But absence from the numbers is not absence from life. Shrinkage has migrated into quieter corners. Wages rise, yet never enough to catch the cost of rent, food, or healthcare. Capital is funneled into favored sectors while others wither. Retirement ages drift higher not as a choice but as necessity. Children inherit a world of debt and narrower opportunities. Even when markets soar, the story changes once translated into real terms: a local stock market may triple, but when measured against gold, dollars, or Bitcoin, the line flattens or turns down. Expansion on paper, contraction in reality.

This is not a crisis that arrives with sudden crashes and sirens. It is a crisis that creeps. It erodes freedom without announcing itself, narrowing horizons even as headlines proclaim prosperity. The odds of a classic collapse remain low. Policymakers will do almost anything to prevent outright nominal declines. More likely is the steady erosion we already feel: numbers that climb while lives contract. The only true rupture would come if faith in the currency itself is lost. That remains unlikely in the near term, but history is clear that when such faith breaks, it breaks suddenly.

Every society that tried to abolish contraction eventually discovered it had only shifted form. Rome debased its coins until citizens could no longer afford bread. Argentina watched its stock market soar as households fell into poverty. In every case, the charts told one story while lived experience told another. We are following that script now. Multiples expand while households shrink. Indices climb while opportunity evaporates.

The lesson is not just financial but philosophical. A system cannot suspend gravity forever. It can mask decline, displace it, rename it, but it cannot erase it. Contraction will always find its way, even if it wears a different mask.

This is the new theater. Whether we adapt or resist, the system will force its terms upon us, for better or for worse.

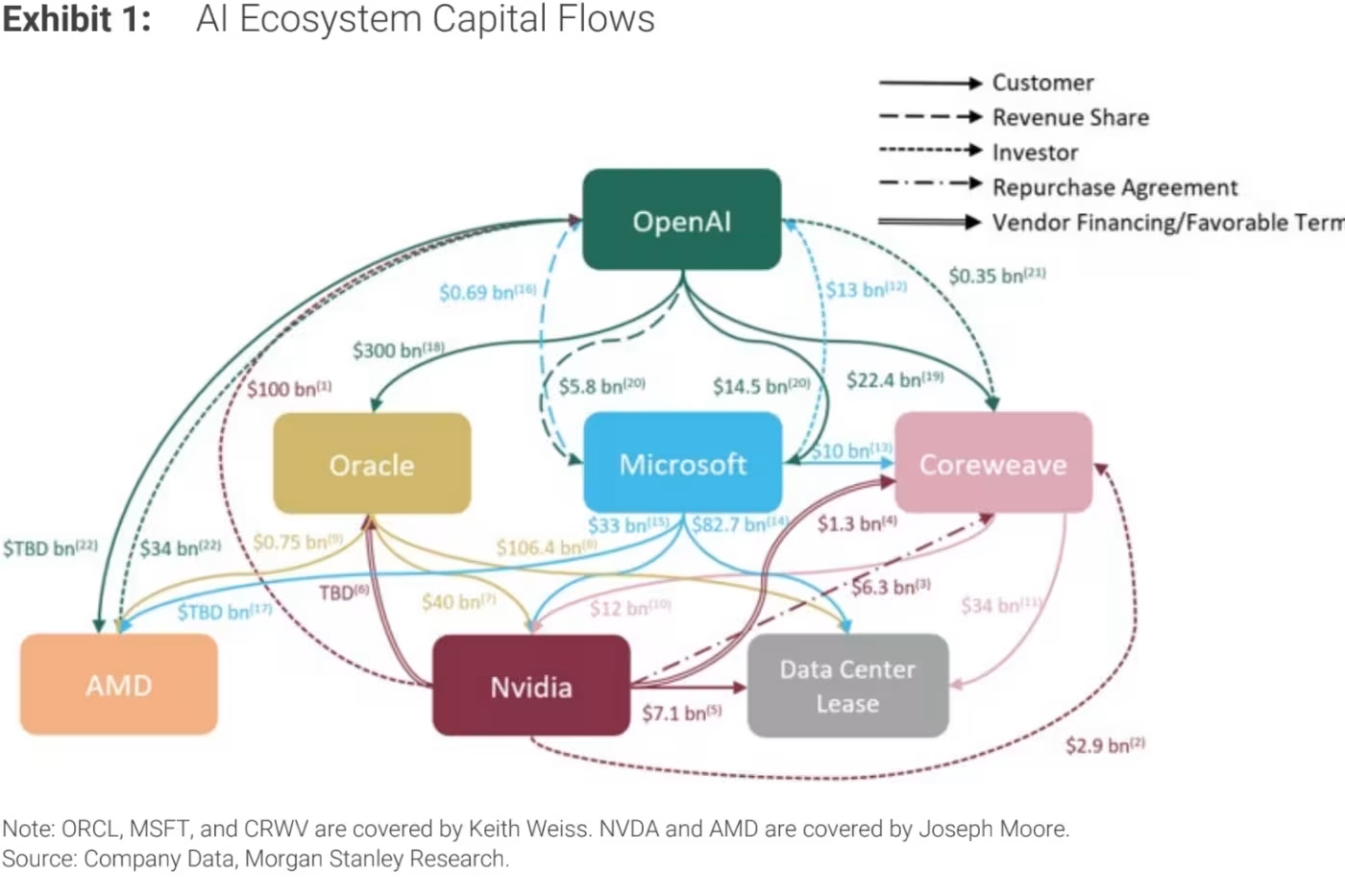

The AI Buildout is So Big Even a Haunted House Owner Wants In

He wants to turn the nearly 130-acre grounds into a world-class data center, the kind of massive server facility that is central to the artificial intelligence boom. Never mind this is his first foray into such an investment, one that would require more cash than any of his past projects. He’s also not fretting about corralling the necessary electricity, which would be enough to power as many as 400,000 homes…

“If you don’t have expertise in developing data centers historically, you don’t know what you don’t know,” said Dan Golding, chief technology officer at data center consultancy ASG…“The upsides of the data center would be there would be no more haunted house”…

I just re-word reality.

As I put it 12 years ago…

“When economic expansion becomes driven solely by debt creation, central bank actions, credit availability & multiple expansion, rather than anything fundamental, you enter this dangerous stage where it becomes a snake devouring its own tail.”

“Probably the thing that people talk about the most - and I say it’s surprising, because I live in Manhattan, I’m relative to the average person doing fine economically, and the people around me are above average income earners - the pervasive conversation is inflation.”

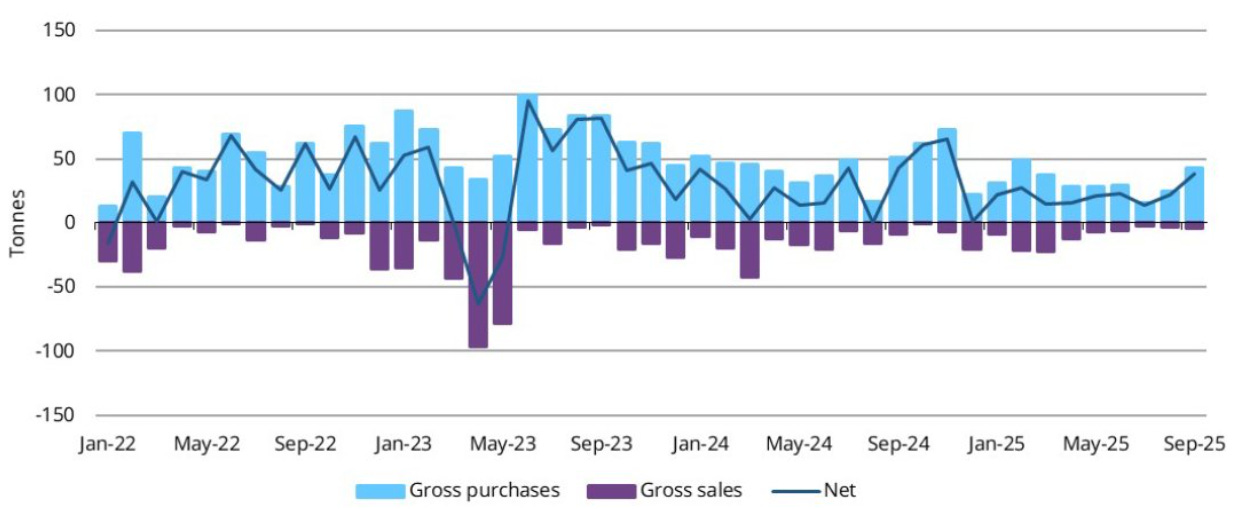

Central Bank Gold Buying

“I sincerely believe, with you, that banking establishments are more dangerous than standing armies ; and that the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”

Thomas Jefferson

Letter to John Taylor, May 28, 1816

Rents

Apartment List: Asking Rent Growth -0.9% Year-over-year

Cotality: Single Family Rents Up 2.3% year-over-year

Zillow: Rents up 1.7% year-over-year

“At manufactured home parks – sometimes called trailer parks or mobile home parks – rents are rapidly rising due to large-scale buyouts by private equity firms…

In 2020 and 2021, institutional investors accounted for 23% of all manufactured home park purchases, up from 13% between 2017-2019. Now, 23 private equity firms own over 1,800 parks in the U.S.”

“The tendency of an inconvertible paper currency was to create fictitious wealth, bubbles which, by their bursting, produced inconvenience. Though we had hitherto escaped this danger, we were never secure against it, and had no solid ground to stand on, till the paper was capable of being changed for money at command.”

Robert Jenkinson, Lord Liverpool, May 26, 1818

US Median First-Time Homebuyer Age Now at Record-High of 40

“The age at which people purchase their first home has climbed rapidly since 2021, when the median was 33, according to a National Association of Realtors survey of transactions from July 2024 through June. In 1981, when the survey was first conducted, the median age was 29 years old.”

“Over the past year, first-time buyers accounted for 21% of the market, the lowest since the NAR began collecting such data in 1981 and about half the pre-2008 norm.”

“An estimated 1.73 million vehicles were repossessed last year, the most since recession-wracked 2009…“It’s like history repeating itself,” said Detroit repossessor George Badeen, president of Allied Finance Adjusters, a trade group…”

Nice subprime auto overview below…

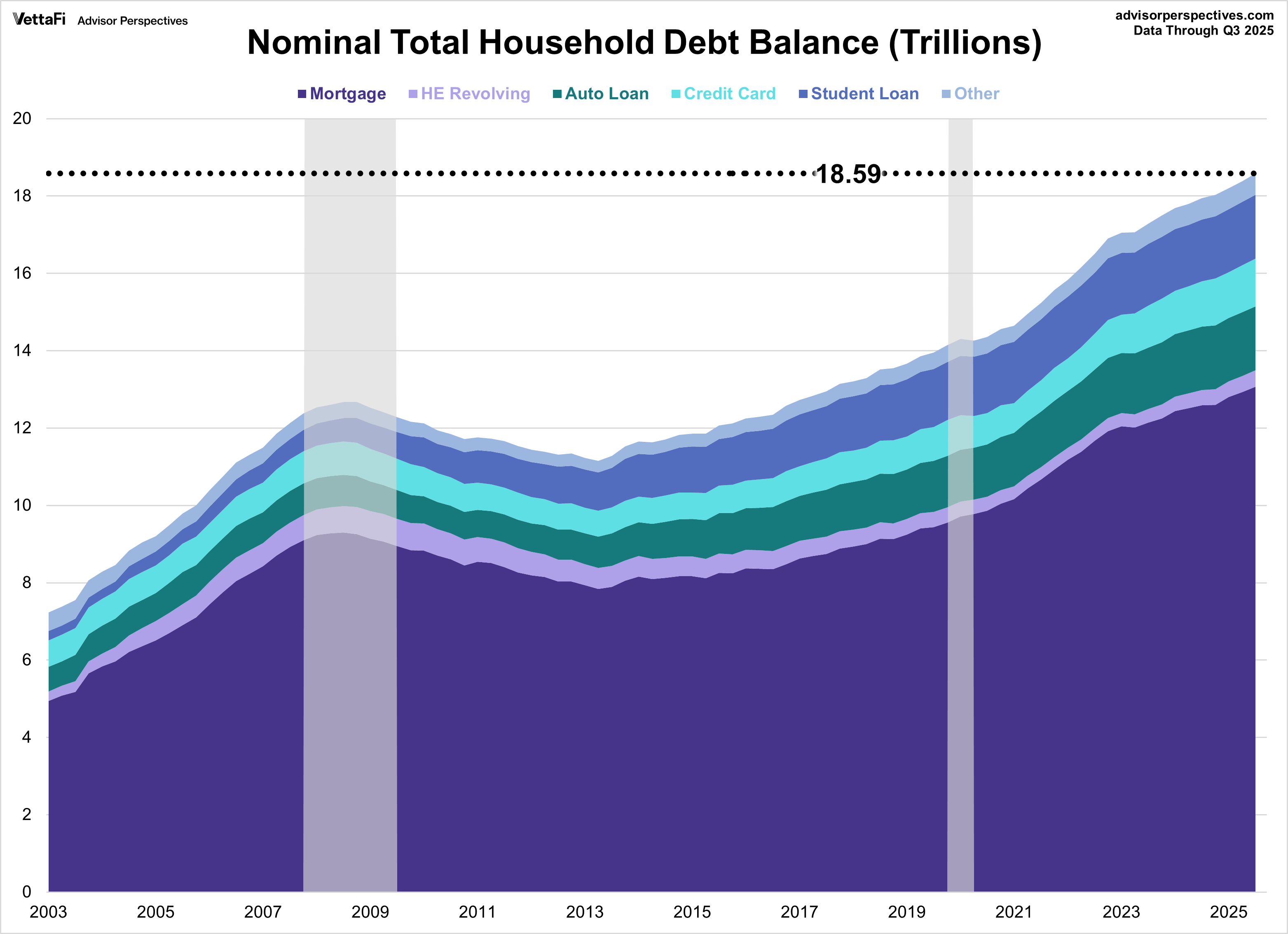

Household Debt Rises to $18.59 Trillion in Q3 2025

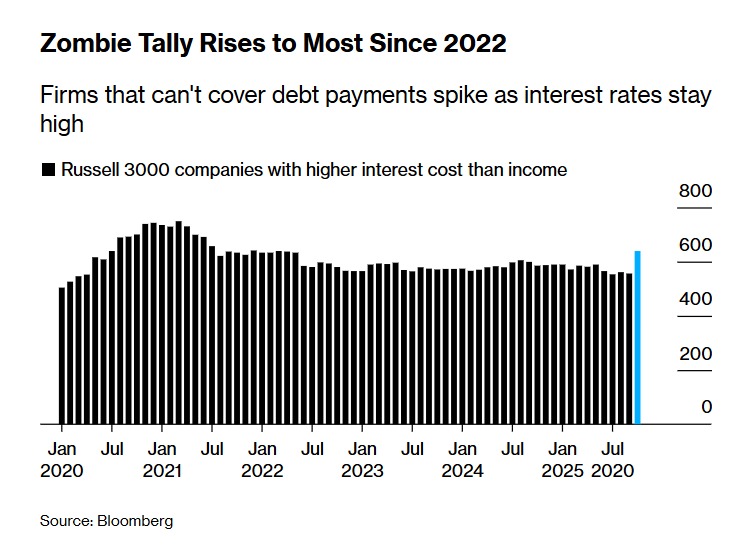

Zombies

“It worries me when I see interest coverage below one”

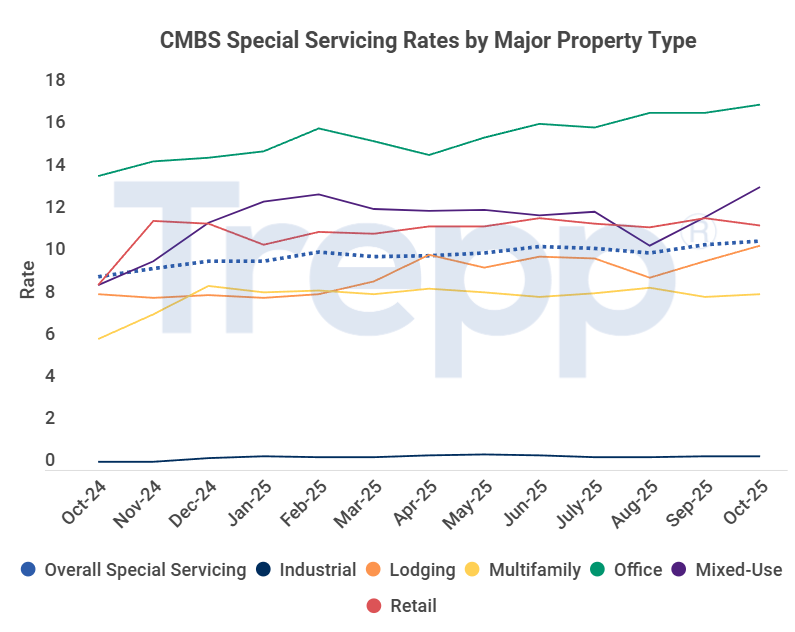

“The Trepp CMBS Special Servicing rate rose to another record in October, climbing 19 basis points to hit 10.84%.”

“In the latter stages of the war all the belligerent governments practised, from necessity or incompetence, what a Bolshevist might have done from design.”

Peter Atwater

“What has been so fascinating to me in this second administration of President Trump is that he campaigned on one theme and yet has behaved in another. His initial themes were all about domestic policy, and yet if you look at where he’s traveled, where his focus is, it’s all been on an international stage. And I can’t think of a place where those at the bottom would least wish him to be. They want him in West Virginia, they want him in Kentucky. And I’m really befuddled, we’re not seeing the rallies. The contrast to me is really striking. And this whole thing with the gilded ballroom, it’s not a political statement. Again, I can’t think of a worse symbol at a time when those at the bottom are struggling.”

Demetri Kofinas

“This administration is in a class of its own in terms of its corruption, in terms of its public-facing, outwardly unapologetic corruption, which is a very different type of corruption from the kind you do in secret, where you can do as much as you can get away with, that people won’t catch you. But what we’re going through is a re-establishment of norms and a public defacing of the values that many people may have skirted, but that we had all agreed were things to aspire to.”

Atwater

“I think it’s emblematic of the invulnerability that those are the top now feel, that in every dimension of their life they are untouchable.”

Grant Williams

“I wonder, going back to FDR, at the time, obviously in the 1930s, politics was not necessarily a means to become wealthy. It was an enterprise you went into when you were already wealthy and you wanted to give something back. And now politics has become a way to get fabulously wealthy because not only are the opportunity’s there, but to your earlier point, the fact that the grift is now out in the open.”

Atwater

“When you’re watching the news and the stories that you’re being bombarded with, appreciate that they are being curated to mirror your mood, and that our news delivery system, our story system today is a series of deliberate echo chambers that are trying to capture you and to keep your mood in a place that often is irritable and objectionable so that that’s what keeps your attention.”

Podcasts

The Quiet Repricing of Reality ft. Adam Rozencwajg “Energy was 3% of the S&P 500 in 1968. In 1982 it was 33%. Which is a mind-blowing statistic. Today it’s two and a half.”

Late Cycle Dynamics With Doug Noland “There’s fragility everywhere, and everything looks fine as long as you continue to have leveraged speculation, you continue to have all this liquidity. It doesn’t work well in reverse. The credit cycle doesn’t work in reverse. The leveraged speculation doesn’t work well in reverse.”

Richard Bernstein on Why Everyone Owns the Same Bubble “People don’t care about valuation…people just don’t care about diversification anymore…what makes me concerned more than anything else would be if the Fed really does continue to cut rates, because I don’t think that’s needed in the economy, and I think that that will just cause more speculation. Now people say, well, what’s bad about that? What’s bad about that is you get the gross misallocation of capital in the economy.”

Brent Johnson on Stablecoins “What percent of the global population outside of the U.S. - if given the chance - would choose to earn and transact in dollars versus anything else? Easily 50% and probably 70%. So essentially that’s the opportunity the U.S. stablecoin unlocks. It’s enormous.”

Jack Gamble: “White collar crime begets blue collar crime. I think as a country we don’t prosecute white collar crime nearly frequently enough, or severely enough when we actually do do it. And I think we need to change that.”

Michael Every: “…Decades in which not just the U.S., but Europe and every major Western economy has done everything it can to get rid of all its productive potential and to shovel it offshore. It was absolutely the norm. That’s how you made your money on Wall Street. That’s how you, you know, got a nice slush fund if you’re a politician, just ensure that you offshored absolutely everything. Sliced up the value chain into a million different pieces, and very, very few of them were still within the U.S., and everyone was happy…people just simply didn’t care because they were getting paid.”

Craig Fuller of FreightWaves: “Pakistan is the epicenter of a lot of this

freight fraud, these Pakistani families that have created a billion dollar cottage industry of basically ripping off American businesses through trucking…freight dropped by as much as a third during the Great Financial Crisis, and that’s what we’re seeing right now…what we call the long haul sector, which is energy, auto, housing, and manufacturing - it’s off 30%. That’s very GFC-style vibes.”

Mike Green: “This tends to be where things go wrong. We build a model of the world, we engage in particular behaviors based on that model, and it turns out the model is wrong”

Chaos: Charles Manson, the CIA, and the Secret History of the Sixties with Tom O’Neill and Nick Bryant “I don’t think they wanted him or his followers to kill an eight and a half month pregnant woman, but I do think that they were pushing him and provoking him and experimenting on him and his group to see what they could do, and there was a history of that in the MKUltra program. The ultimate goal was to create programmed assassins.”

“The key to risk management is accountability, because you can’t model risk. You can’t know. The only thing that will make people behave appropriately is skin in the game.”1

“Ben Bernanke thought it would be a great idea to tell people to take risk. There’s only one problem. Ben Bernanke never took any risk as in investor in his life. He’s a professor. He’s never sat behind a desk and taken risk and lost money, and until you’ve done that, you don’t know what it involves. So the people making policy, they’re all theory, and the problem is that economics doesn’t work in theory, it works in practice.”

Michael Lewitt, 2016 on Realvision

“Based on our technical indicators, the bounce in the dollar could have further to run.” - some guy

“Miracles, it could be said, are not just puzzling for historians but also immensely frustrating. The further one goes back in time, the more difficult it becomes not to bump into them, or into their preternatural demonic counterparts. The testimonies are simply there in the historical record, cluttering it up abundantly, and their existence cannot be denied. But ironically, it is ultimately impossible to prove that what is claimed in these testimonies happened exactly as recorded. Beyond the realm of faith, the evidence can seem insufficient despite its sheer volume. Hence the frustration.”

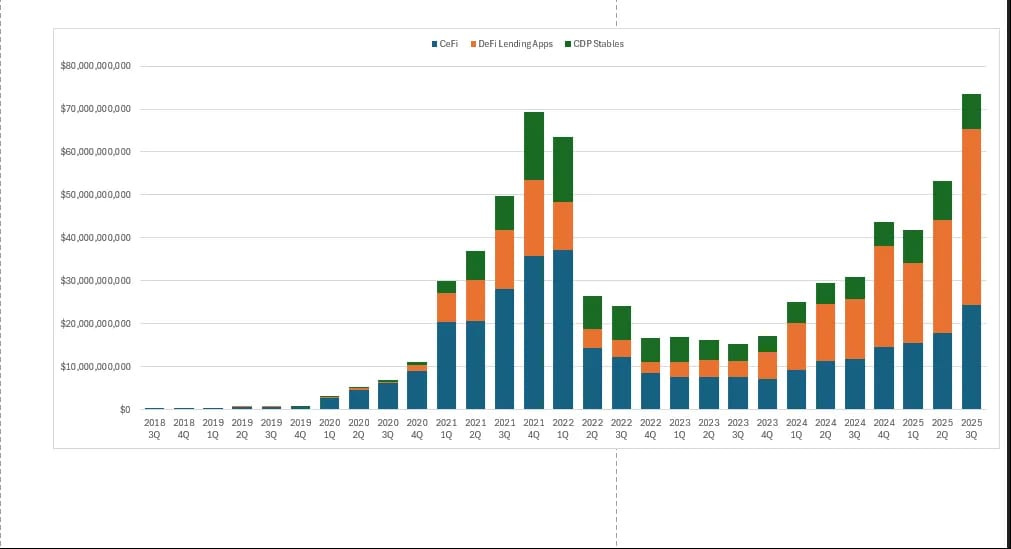

Crypto Lending!

“Crypto lending is one of the key indicators for market sentiment as retail investors use lending to add leverage and enhance returns and traders such as hedge funds tap into lending for short-term liquidity to execute trades. A boom in so-call digital asset treasury companies have led firms to borrow cash against their crypto holdings to generate yields. Now many of those firms have seen the value of their crypto holdings tumble.”

‘He was always broke and trying to borrow money. That was another reason he didn’t like me – I would never lend him a cent. Whenever he was talking about being hard up he often used to say that he thought the easiest way to make money would be to start a religion.’

Nieson Himmel, former roommate of L. Ron Hubbard

“To comprehend is to complicate, to augment in depth. It is to widen on all sides.

It is to vivify.”

“I raised this issue with a very important oil contractor from New Orleans with whom I was hunting in Scotland.

I asked him, ‘Do you know who assassinated Kennedy?’ He answered me without blinking: ‘’Yes.’‘

It was not a crazy, isolated shooter who killed the President”

Giscard d’Estaing, President of France 1974-1981

As Rick Santelli said in 2017, “The only regulation that works is failure.”

This is your best email yet. I thought that after Grant's quote and the AI ecosystem graph, and then the hits just kept coming.

I don’t get the 50 year mortgage.

I mean, if the goal is to make home ownership more ‘affordable’, well for 99% of prospective buyers that means can they cover the monthly nut.

And if the 2nd goal is to help young people buy homes, why stop at 50 years.

It’s a rare buyer who

looks at an amortization table, it’s just about the payment.

So with that in mind, why 50. Let’s just go with a LEM. A life expectancy mortgage.

At whatever age you buy, your mortgage can be as long as your life expectancy. So a 24 year old female buying her first home, her life expectancy is 82 years. So she should be able to get a 58 year note.

My new LEM product fulfills both goal. Lowers monthly payments more than a 50 year mortgage and encourages grade schoolers to buy homes.

I’m seeking financing for a product launch.

Alternatively we could just go right to a hundred years.